- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

Market Size, 2025

$1.49 BnMarket Estimate, 2026

$1.5 BnMarket Forecast, 2034

$2.63 BnCAGR, 2026–2034

6.51%North America Micronutrient Fertilizer Market Report Summary

The North America micronutrient fertilizer market was valued at USD 1.49 billion in 2025, is estimated to reach USD 1.59 billion in 2026, and is projected to reach USD 2.63 billion by 2034, growing at a CAGR of 6.51% during the forecast period from 2026 to 2034. The growth of the North America micronutrient fertilizer market is driven by increasing demand for high-yield crop production, growing awareness of soil nutrient deficiencies, and the adoption of precision agriculture practices. Farmers are increasingly utilizing micronutrient fertilizers to improve crop quality, enhance nutrient uptake, and maximize agricultural productivity. Additionally, rising investments in sustainable farming, advanced fertilizer formulations, and modern agricultural technologies are supporting market expansion across the region.

Key Market Trends

-

Rising adoption of precision agriculture is increasing the demand for micronutrient fertilizers to improve crop productivity and nutrient efficiency.

-

Growing awareness of soil micronutrient deficiencies is encouraging farmers to use balanced fertilization practices.

-

Increasing demand for high-quality agricultural produce is driving the application of zinc and other micronutrient fertilizers.

-

Advancements in chelated and specialty fertilizer formulations are improving nutrient availability and crop performance.

-

Government initiatives promoting sustainable farming and efficient nutrient management are supporting long-term market growth.

Segmental Insights

-

Based on product, the zinc segment dominated the North America micronutrient fertilizer market by accounting for 35.9% of the market share in 2025. The segment's leadership is attributed to the widespread prevalence of zinc-deficient soils and the essential role of zinc in improving crop growth, yield, and resistance to environmental stress.

-

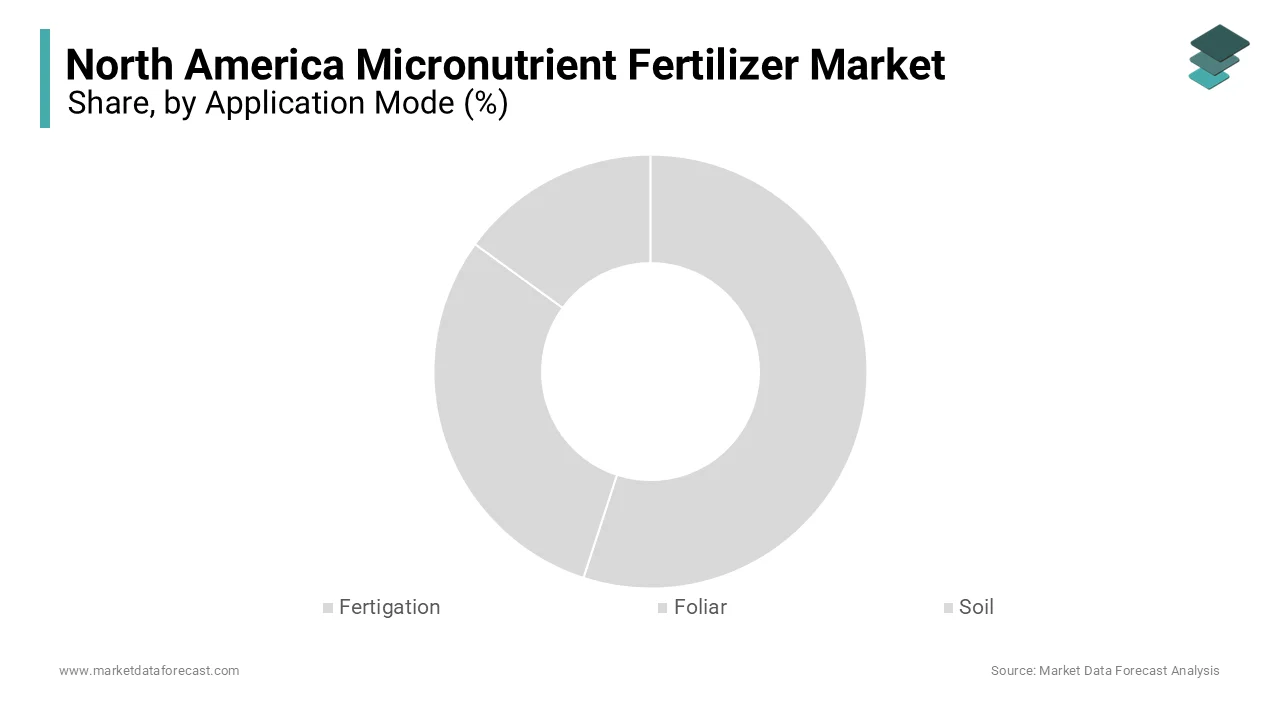

Based on application mode, the soil application segment held the largest share of 60.7% of the North America micronutrient fertilizer market in 2025. The segment's dominance is driven by its cost-effectiveness, ease of application, and ability to provide sustained nutrient availability for a wide range of crops.

Regional Insights

-

The North America micronutrient fertilizer market is witnessing steady growth due to increasing adoption of modern farming practices, rising demand for sustainable agriculture, and growing emphasis on improving soil health.

-

The United States dominated the North America micronutrient fertilizer market by accounting for 75.7% of the regional market share in 2025. The country's leadership is supported by its large agricultural sector, widespread adoption of precision farming technologies, increasing focus on soil fertility management, and strong investments in agricultural innovation.

Competitive Landscape

The North America micronutrient fertilizer market is moderately competitive, with companies focusing on innovative fertilizer formulations, sustainable nutrient management solutions, and strategic collaborations to strengthen their market positions. Manufacturers are investing in research and development, specialty fertilizer technologies, and precision agriculture solutions to improve crop productivity and support sustainable farming practices. Key players operating in the North America micronutrient fertilizer market include BASF Cognis, Evonik Industries, Ecover, Lion Corporation, Croda International PLC, Biotensidon GmbH, AkzoNobel N.V., Saraya Co., Ltd., Jeneil Biotech, Inc., and Givaudan SA (Soliance).

North America Micronutrient Fertilizer Market Size

The North America micronutrient fertilizer market size was valued at USD 1.49 billion in 2025 and is predicted to reach USD 2.63 billion by 2034 from USD 1.59 billion in 2026, growing at a CAGR of 6.51% from 2026 to 2034.

MARKET DRIVERS

Rising Awareness of Soil Nutrient Deficiencies

The increasing awareness of soil nutrient deficiencies is a key driver of the North American micronutrient fertilizer market. Farmers are increasingly recognizing the importance of micronutrients like zinc, boron, and manganese for optimal crop growth. According to the International Plant Nutrition Institute (IPNI), over 60% of North American farmland suffers from micronutrient imbalances, creating steady demand for targeted solutions. Additionally, government initiatives have promoted soil testing programs, with a notable increase in soil analysis requests in recent years. These programs have highlighted the need for micronutrient fertilizers, particularly in regions with intensive monoculture practices. Also, micronutrient applications improved crop yields considerably in deficient soils, showcasing their critical role in modern agriculture.

Adoption of Precision Agriculture Technologies

The adoption of precision agriculture technologies significantly contributes to the growth of the micronutrient fertilizer market. Precision farming leverages GPS, sensors, and data analytics to identify specific nutrient deficiencies in soils, enabling targeted fertilizer applications. Similar, precision agriculture systems reduced fertilizer wastage in in the last few years, enhancing cost efficiency for farmers. Additionally, the integration of micronutrient fertilizers into precision farming practices has improved their adoption rates.

MARKET RESTRAINTS

High Costs of Micronutrient Fertilizers

High costs associated with micronutrient fertilizers pose a significant restraint to the North American market. Producing micronutrient fertilizers involves complex processes, including chelation and encapsulation, which require substantial investment. Like, the average cost of micronutrient fertilizers is considerably higher than that of macronutrient fertilizers, making them less accessible to small-scale farmers. Additionally, the lack of economies of scale further exacerbates the issue, as smaller manufacturers struggle to compete with established fertilizer producers. In addition, only a small portion of small farms in North America can afford micronutrient fertilizers, limiting their widespread adoption. These financial barriers hinder market growth and restrict accessibility.

Limited Awareness Among Farmers

Limited awareness among farmers about the benefits and application of micronutrient fertilizers presents another major restraint for the market. Many farmers, particularly in rural areas, remain unfamiliar with the advantages of micronutrients over traditional fertilizers. Like, a significant of farmers in the Midwest reported insufficient knowledge about micronutrient usage in 2023. This lack of awareness is compounded by inadequate outreach programs and marketing efforts by manufacturers. Also, limited number of agricultural extension services provide training on micronutrient fertilizers. These gaps in education and communication impede the adoption of micronutrient fertilizers, slowing market expansion and innovation.

MARKET OPPORTUNITIES

Expansion in Organic Farming Initiatives

The growing popularity of organic farming initiatives offers significant opportunities for the micronutrient fertilizer market. Organic farming relies heavily on natural inputs to maintain soil health, creating steady demand for bio-based micronutrient fertilizers. Additionally, certification programs like USDA Organic mandate the use of non-synthetic inputs, further propelling demand. Also, a substantial portion of organic farmers in North America utilize micronutrient fertilizers to enhance soil fertility and crop yield.

Integration with Smart Farming Solutions

The integration of micronutrient fertilizers with smart farming solutions presents a transformative opportunity for the market. Smart farming technologies, such as IoT-enabled sensors and drones, enable real-time monitoring of soil health and nutrient levels, ensuring precise fertilizer application. Similarly, smart farming systems improved fertilizer efficiency in recent years, reducing waste and environmental impact. Additionally, government incentives for sustainable agriculture have accelerated the adoption of these technologies. These advancements position micronutrient fertilizers as a key component of sustainable and data-driven farming practices.

MARKET CHALLENGES

Regulatory Hurdles for Product Approvals

Regulatory hurdles for product approvals present a critical challenge for the micronutrient fertilizer market. While governments promote sustainable agriculture, the process of obtaining certifications for new formulations remains lengthy and complex. Also, the average time required for micronutrient fertilizer approval longer, compared to earlier one for macronutrient fertilizers. This delay stifles innovation and limits the introduction of advanced products into the market. Besides, inconsistent regulatory frameworks across states create confusion among manufacturers. In addition, a notable share of micronutrient fertilizer companies face regulatory bottlenecks, hindering their ability to scale operations.

Short Shelf Life and Storage Constraints

One of the primary challenges impacting the North American micronutrient fertilizer market is the short shelf life and storage constraints of certain formulations. Micronutrient fertilizers, particularly liquid variants, are highly sensitive to temperature and humidity variations, requiring specialized storage facilities. Similarly, improper storage can reduce the efficacy of micronutrient fertilizers within a short span to time. This issue is exacerbated in regions with extreme weather conditions, such as the southern United States. Apart from these, the lack of standardized storage facilities among distributors creates logistical challenges. Further, a large number of micronutrient fertilizers lose potency during transportation, deterring farmers from adopting them.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.51% |

| Segments Covered | By Product, Application Mode, Crop Type, and Region |

|

Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | The United States, Canada, Mexico, and Rest of North America |

| Market Leaders Profiled | BASF Cognis, Evonik Industries, Ecover, Lion Corporation, Croda International PLC, Biotensidon GmbH, AkzoNobel N.V., Saraya Co., Ltd., Jeneil Biotech, Inc., Givaudan SA (Soliance)., and others |

SEGMENTAL ANALYSIS

By Product Insights

The segment of Zinc dominated the North American micronutrient fertilizer market by holding a 35.9% of the total share in 2025. This dominance is driven by its critical role in enhancing crop immunity and enzyme activity, particularly in field crops like corn and wheat. One key factor is the widespread prevalence of zinc deficiency in soils across North America. Like, a substantial share of farmland in the Midwest exhibits zinc deficiencies, creating steady demand for zinc-based fertilizers. Also, government initiatives promoting soil health have bolstered its adoption. These elements collectively reinforce the leadership position of zinc in the market.

The boron segment is projected to grow at the highest CAGR of 8.5% from 2026 to 2034. This rapid growth is fueled by its increasing use in horticultural crops such as fruits and vegetables, which require boron for cell wall formation and pollination. One significant driver is the rising demand for organic produce. Similarly, organic fruit and vegetable sales grew notably in recent times, creating steady demand for boron-based fertilizers. Another factor is the growing awareness of soil testing among farmers. Furthermore, boron applications improved yields in deficient soils significantly, aligning with sustainability goals.

By Application Mode Insights

The soil application segment dominated the North American micronutrient fertilizer market by capturing 60.7% of the total share in 2025. This dominance is driven by its compatibility with traditional farming practices and ease of integration into existing systems. One key factor is the widespread adoption of soil-applied micronutrients in field crops like corn and soybeans. Like, a considerable share of large-scale farms in North America utilize soil application methods due to their cost-effectiveness and efficiency. Apart from these, the growing trend of precision agriculture has enhanced the accuracy of soil-applied fertilizers, reducing waste and environmental impact. Besides, soil applications accounted for major share of micronutrient fertilizer usage in the past few years, emphasizing their critical role in agriculture.

The fertigation segment is projected to grow at the highest CAGR of 9.2%. This rapid rise is influenced by its ability to deliver nutrients directly to plant roots through irrigation systems, ensuring optimal absorption. One significant propellents is the increasing adoption of drip irrigation technologies. Like, fertigation systems improved nutrient efficiency considerable in 2025, making them a preferred choice for high-value crops like fruits and vegetables. Another factor is the growing emphasis on water conservation.

By Crop Type Insights

The field crops segment commanded the North American micronutrient fertilizer market, with a 55.3% of the total revenue, in 2025. This is credited to the extensive cultivation of crops like corn, wheat, and soybeans, which rely heavily on micronutrient fertilizers for optimal growth. One key factor is the rising global demand for cereals. Similarly, cereal production must increase by substantially by 2050 to meet population needs, necessitating innovative solutions like micronutrient fertilizers. Apart from these, government incentives for sustainable farming practices have bolstered their adoption.

The horticultural crops segment is poised to be the fastest-growing, with a calculated CAGR of 8.8% in the coming years. This way forward is backed by the increasing consumer preference for organic fruits and vegetables, which require micronutrient fertilizers for nutrient enrichment. One significant factor is the expansion of urban farming initiatives. Also, a large number of rooftop farms and vertical gardens were established in in the past few years, creating steady demand for micronutrient fertilizers tailored for fruits and vegetables. Another driver is the growing emphasis on food security.

REGIONAL ANALYSIS

The United States commanded the biggest share of the North American micronutrient fertilizer market by contributing 75.7 % of the region’s total revenue in 2025. The country’s dominance is credited to its robust agricultural base and strong regulatory support for sustainable farming. One key factor is the rising demand for high-yield crops. Like, a significant portion of U.S. farmland utilizes micronutrient fertilizers to address nutrient deficiencies, driving steady demand. Another driver is federal funding for green initiatives. Additionally, advancements in precision agriculture have positioned U.S.-based companies as global leaders.

Canada is seeing a notable expansion in this market. The country’s market growth is driven by its focus on environmental conservation and sustainable agriculture. One significant factor is the use of micronutrient fertilizers in cold-climate farming. Also, a big share of farmers in British Columbia utilizes micronutrient fertilizers to combat soil acidity, ensuring efficient operations. Another driver is the government’s commitment to reducing carbon emissions. Also, micronutrient fertilizers reduced greenhouse gas emissions notably. These initiatives position Canada as a key contributor to the market.

The Rest of North America is contributing considerably to the regional market, as stated by the Inter-American Development Bank. The segment’s growth is fueled by the increasing adoption of micronutrient fertilizers in small-scale farming and urban agriculture. One key factor is Mexico’s investment in rural farming projects, where micronutrient fertilizers are used to improve soil fertility. Another driver is the region’s vulnerability to climate change, prompting the use of micronutrient fertilizers for drought-resistant crops.

COMPETITIVE LANDSCAPE

The North American micronutrient fertilizer market is highly competitive, driven by innovation, regulatory compliance, and diverse applications across crop types and farming practices. Leading players like Mosaic, Nutrien, and Yara dominate the landscape, each targeting specific niches such as zinc fertilizers, precision agriculture integration, and organic farming inputs. The competitive environment is further intensified by the entry of new startups and the adoption of disruptive technologies like IoT-enabled soil sensors. Regulatory frameworks also play a pivotal role, with companies striving to comply with environmental standards while innovating within constraints. Collaborations with research institutions and government bodies provide a competitive edge, fostering innovation. Additionally, price differentiation and feature customization are common tactics to capture market share.

KEY MARKET PLAYERS

Some of the key players in the North American micronutrient fertilizer market are

-

BASF Cognis

-

Evonik Industries

-

Ecover

-

Lion Corporation

-

Croda International PLC

-

Biotensidon GmbH

-

AkzoNobel N.V.

-

Saraya Co., Ltd.

-

Jeneil Biotech, Inc.

-

Givaudan SA (Soliance)

TOP PLAYERS IN THE MARKET

- The Mosaic Company is a leading innovator in the North American micronutrient fertilizer market, renowned for its advanced formulations tailored for field and horticultural crops. The company focuses on developing zinc- and boron-based fertilizers to address widespread soil deficiencies. Additionally, the company partnered with agricultural cooperatives to promote soil health programs, enhancing its regional presence.

- Nutrien Ltd. specializes in producing high-quality micronutrient fertilizers, offering solutions like chelated iron and manganese products for precision agriculture. Known for its commitment to sustainability, Nutrien has introduced eco-friendly formulations that reduce environmental impact. The company also invested in digital platforms to provide farmers with data-driven insights on micronutrient application. These efforts have solidified Nutrien’s reputation as a reliable provider in the micronutrient fertilizer industry.

- Yara International is a key player in the micronutrient fertilizer market, focusing on innovative products for foliar and fertigation applications. Its micronutrient solutions are widely used in high-value crops such as fruits and vegetables. The company also launched educational campaigns to raise awareness about soil nutrient management, targeting small-scale farmers.

TOP STRATEGIES USED BY KEY PLAYERS

Key players in the North American micronutrient fertilizer market employ strategies such as innovation, partnerships, and education to strengthen their positions. Companies like Mosaic and Nutrien focus on developing advanced formulations to address specific soil deficiencies, aligning with sustainability goals. Strategic alliances with agricultural cooperatives and government bodies help expand their reach across diverse farming communities. Yara emphasizes affordability, targeting small-scale farmers through cost-effective solutions. Another common strategy is investing in awareness campaigns to educate farmers about the benefits of micronutrient fertilizers.

RECENT HAPPENINGS IN THE MARKET

- In April 2023, The Mosaic Company launched a line of biofortified micronutrient fertilizers, improving crop immunity and yield, and expanding its product portfolio.

- In June 2023, Nutrien Ltd. expanded its production facilities in Saskatchewan to meet rising demand from organic farmers, reinforcing its supply chain capabilities.

- In August 2023, Yara International conducted field trials in collaboration with U.S. universities to validate the efficacy of its micronutrient fertilizers, ensuring product reliability.

- In October 2023, The Mosaic Company partnered with agricultural cooperatives to promote soil health programs, enhancing its regional presence and brand visibility.

- In December 2023, Nutrien introduced a digital platform providing farmers with data-driven insights on micronutrient application, improving user experience and adoption rates.

MARKET SEGMENTATION

This research report on the North America micronutrient fertilizer market has been segmented and sub-segmented based on the following categories.

By Product

- Boron

- Copper

- Iron

- Manganese

- Molybdenum

- Zinc

- Others

By Application Mode

- Fertigation

- Foliar

- Soil

By Crop Type

- Field Crops

- Horticultural Crops

- Turf & Ornamental

By Country

- The United States

- Canada

- Rest of North America