North America Paper Machine Oil Market Size, Share, Trends & Growth Forecast Report, Segmented By Product, Machine, End-User, And By Country (USA, Canada, Mexico), Industry Analysis From 2026 to 2034

North America Paper Machine Oil Market Report Summary

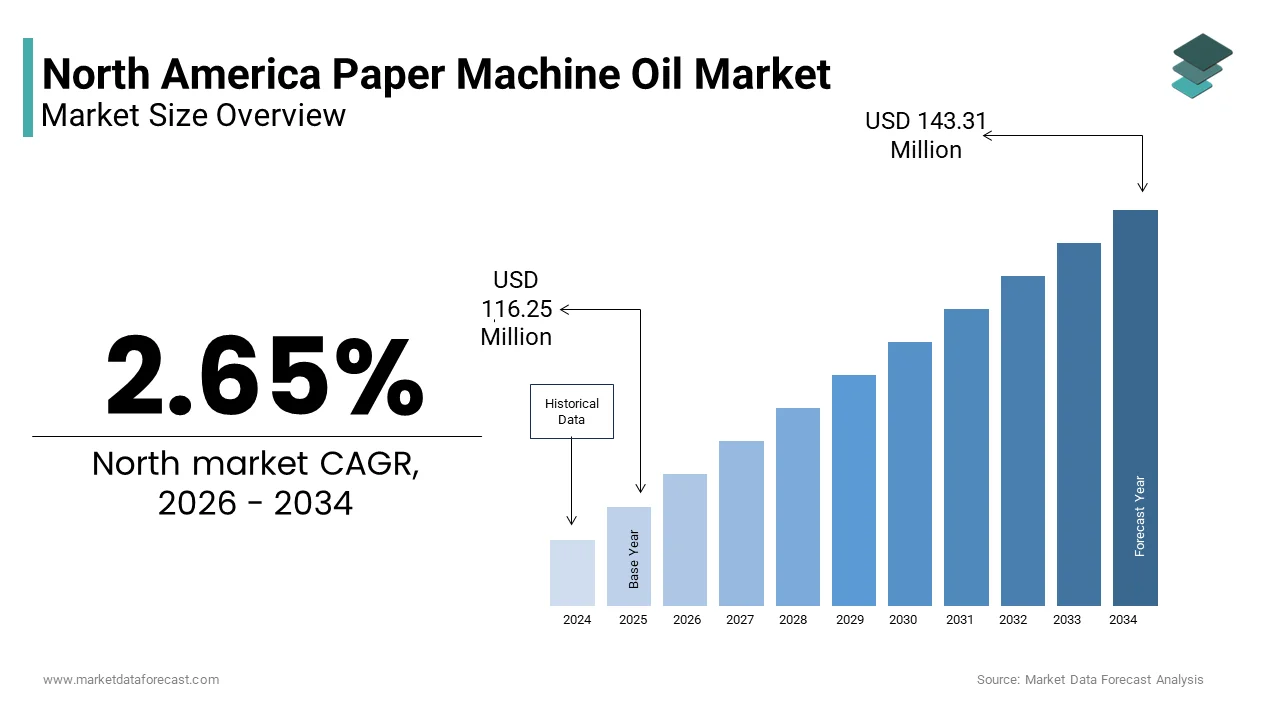

The North America paper machine oil market was valued at USD 113.25 million in 2025, is estimated to reach USD 116.25 million in 2026, and is projected to grow to USD 143.31 million by 2034, registering a CAGR of 2.65% during the forecast period from 2026 to 2034. Market growth is driven by steady paper and packaging production, increasing focus on equipment reliability, rising automation in paper mills, and demand for high-performance industrial lubricants. The continued need to reduce downtime, extend machine life, and improve operational efficiency in paper manufacturing facilities is supporting consistent demand for specialized paper machine oils across North America.

Key Market Trends

- Sustained demand for mineral oil-based paper machine oils due to their cost-effectiveness, proven performance, and wide compatibility with existing paper manufacturing equipment.

- Growing emphasis on lubricant performance optimization, including wear protection, oxidation resistance, and extended oil drain intervals.

- Increasing adoption of predictive maintenance and condition monitoring in paper mills, improving lubricant usage efficiency.

- Rising focus on sustainable and energy-efficient paper production, encouraging the use of advanced lubricant formulations that reduce friction and energy loss.

Segmental Insights

- Based on product type, the mineral oil-based products segment held a dominant share of the North America paper machine oil market in 2024, supported by widespread use in traditional paper manufacturing operations.

- By machine type, the cylinder machines segment accounted for the largest market share in 2024, driven by their continued deployment in paper and board production facilities.

- Based on end use, the original equipment manufacturer (OEM) segment led the market with a 58.2% share in 2024, reflecting strong lubricant demand during machine installation, commissioning, and warranty periods.

Regional Insights

- The United States was the largest contributor to the North American paper machine oil market, accounting for 87.3% of the regional share in 2024, supported by a large installed base of paper mills, high production capacity, and ongoing modernization of manufacturing facilities.

- Canada held 13.3% of the market share in 2024, benefiting from extensive forest resources, a well-established paper manufacturing infrastructure, and a strong emphasis on sustainable industrial practices that favor the adoption of specialized lubricants.

Competitive Landscape

The North American paper machine oil market is characterized by the presence of global lubricant manufacturers and specialized industrial oil suppliers competing on formulation quality, performance reliability, and technical service support. Leading companies focus on product innovation, OEM partnerships, sustainability-oriented formulations, and customized lubrication solutions for paper mills. Prominent players operating in the market include Bechem GmbH, Phillips 66 Company, Exxon Mobil Corporation, Chevron Inc., Petro-Canada Lubricants, TotalEnergies, Castrol Limited, and ALCO LLC.

North America Paper Machine Oil Market Size

The North America paper machine oil market size was valued at USD 113.25 million in 2025 and is anticipated to reach USD 116.25 million in 2026 and USD 143.31 million by 2034, growing at a CAGR of 2.65% during the forecast period from 2026 to 2034.

Introduction to the NorthAmericana Paper Machine Oil Market

The paper machine oil is an important operational need of paper and pulp manufacturing facilities across the United States and Canada. These specialized lubricants are engineered to withstand the unique operating conditions encountered in paper production environments, including high temperatures, moisture exposure, and continuous operation under significant mechanical stress. Paper machine oils must provide exceptional oxidation resistance, water separation capabilities, and anti-wear protection to ensure optimal performance of complex machinery, including Fourdrinier wires, press rolls, and dryer sections. According to the American Forest & Paper Association, the paper and pulp industry in North America operates approximately 280 major facilities, each requiring extensive lubrication systems to maintain production efficiency and equipment longevity. The chemical composition of these lubricants typically includes advanced additive packages that enhance thermal stability and prevent deposit formation, which is given that paper machines often operate continuously for weeks without shutdown.

MARKET DRIVERS

Increasing Paper Production Capacity and Mill Modernization

The expansion of paper production capacity and ongoing mill modernization initiatives aremajor fafactorsropelling the growth of the North America paper machine oil market. As paper manufacturers invest in advanced machinery and upgrade existing equipment to improve efficiency and product quality, the demand for specialized lubricants increases proportionally. Modern paper machines operate at higher speeds and temperatures, which create more demanding conditions that require premium lubricants with enhanced performance characteristics. The average paper machine now operates at speeds exceeding 1,500 meters per minute, compared to 800 meters per minute two decades ago, significantly increasing mechanical stress on bearings, gears, and other components. This technological advancement necessitates the use of high-performance synthetic oils and advanced mineral oils that can withstand extreme operating conditions while maintaining optimal lubrication properties. Additionally, the shift toward lightweight paper grades and specialty papers requires more precise machine control and consistent operating parameters, further driving demand for specialized lubricants that ensure equipment reliability and consistent product quality. Mill operators recognize that proper lubrication directly impacts production uptime, with well-maintained lubrication systems reducing unplanned downtime by up to 35% according to industry maintenance studies. The continuous operation requirements of modern paper machines, often running 24/7 with minimal shutdown periods, create sustained demand for high-quality lubricants that can maintain performance over extended drain intervals while protecting expensive machinery investments.

Stringent Equipment Maintenance Requirements and Reliability Standards

The implementation of rigorous equipment maintenance protocols and reliability-centered maintenance practices in paper mills is significantly prompting the growth of the North American paper machine oil market. Modern maintenance strategies emphasize predictive and preventive approaches that rely heavily on high-quality lubricants to extend equipment life and minimize failure risks. The International Society of Automation reports that effective lubrication programs can reduce overall maintenance costs by 20-30% while extending equipment life by 40-50%, making premium lubricants a cost-effective investment for mill operators. Paper machine operators increasingly adopt condition-based monitoring technologies that track oil performance parameters such as viscosity, oxidation levels, and contamination indicators, creating demand for oils with consistent quality and predictable performance characteristics. The complexity of modern paper machines, with some installations containing over 500 lubrication points, requires specialized oils that can meet diverse operational requirements across different machine sections while maintaining compatibility with monitoring systems. Maintenance departments now specify lubricants based on detailed technical requirements, including thermal stability, hydrolytic stability, and compatibility with seals and materials used in modern paper machine construction. This heightened focus on maintenance excellence drives demand for premium paper machine oils that offer extended service life, consistent performance, and compatibility with advanced monitoring technologies, supporting the overall reliability objectives of paper manufacturing operations.

MARKET RESTRAINTS

Environmental Regulations and Sustainability Pressures

Environmental regulations and sustainability initiatives by creating pressure for manufacturers to develop more environmentally acceptable lubricants, while maintaining performance standards is strictly hampering the growth of the North American paper machine oil market. The Environmental Protection Agency's Toxic Substances Control Act and various state-level environmental regulations increasingly restrict the use of certain chemical additives and base stocks traditionally used in industrial lubricants. Paper mills operating near water bodies face particularly stringent discharge limitations that affect lubricant selection and disposal practices. According to the Environmental Defense Fund, over 60% of North American paper mills are located within 50 miles of protected waterways, subjecting them to enhanced environmental compliance requirements that impact lubricant choices. The push toward biodegradable and environmentally acceptable lubricants often results in higher product costs and potential performance compromises, as bio-based alternatives may not provide the same level of protection under extreme operating conditions encountered in paper machines. Additionally, the complexity of paper machine oil formulations makes it challenging to achieve complete biodegradability while maintaining essential performance characteristics such as thermal stability and oxidation resistance. Waste oil disposal regulations have become increasingly restrictive, with many states implementing extended producer responsibility programs that require lubricant suppliers to manage end-of-life disposal, adding costs and logistical complexities to the supply chain. The European Union's REACH regulations, while not directly applicable to North America, influence global lubricant formulations and create additional compliance burdens for multinational suppliers serving both markets. Paper mill operators must balance environmental compliance requirements with operational performance needs, often resulting in complex lubricant selection processes that can slow adoption of new products and create uncertainty for lubricant suppliers seeking to develop sustainable alternatives.

Economic Pressures and Cost Optimization Initiatives

Economic pressures and cost optimization initiatives within the paper industry create significant restraints for manufacturers seeking to reduce operational expenses, while maintaining production efficiency, which is expected to eelevates growth of the North America paper machine oil market. The paper industry has experienced margin compression due to increased raw material costs, energy price volatility, and competitive pressures from digital media substitution, forcing mill operators to scrutinize all operational expenditures, including lubricant purchases. According to the Institute of Paper Science and Technology, North American paper mills have reduced maintenance budgets by an average of 15% over the past three years, directly impacting lubricant purchasing decisions and favoring lower-cost alternatives over premium products. The commoditization of certain paper grades has intensified price competition, pushing manufacturers to minimize all non-essential expenses,s including specialized lubricants that may offer superior performance but at higher costs. Many mills have implemented centralized procurement strategies that prioritize volume discounts and standardization over product specialization, potentially compromising equipment protection and long-term reliability. The economic uncertainty created by global trade tensions and supply chain disruptions has further pressured mill operators to reduce inventory levels and consolidate supplier relationships, limiting opportunities for specialized lubricant suppliers to demonstrate value propositions. Additionally, the cyclical nature of paper demand creates fluctuating operational requirements that make long-term lubricant planning challenging, often resulting in suboptimal product selection during periods of cost pressure. These economic constraints force lubricant suppliers to compete primarily on price rather than performance, potentially undermining the market's ability to support technological advancement and premium product development that could benefit long-term equipment reliability and operational efficiency.

MARKET OPPORTUNITIES

Development of Advanced Synthetic and Bio-Based Lubricant Technologies

The advancement of synthetic and bio-based lubricant technologies, as manufacturers seek solutions that combine environmental sustainability with enhanced performance characteristics, cs certainnly to create new opportunities for the growth of the North American paper machine oil market. Next-generation synthetic base stocks offer improved thermal stability, extended service life, and superior oxidation resistance compared to conventional mineral oils, addressing the demanding operating conditions of modern paper machines. According to the National Institute of Food and Agriculture, bio-based lubricants can achieve performance levels comparable to petroleum-based alternatives while offering enhanced biodegradability and reduced environmental impact, making them attractive for environmentally conscious mill operators. The development of ester-based synthetic oils specifically formulated for paper machine applications has shown promise in extending drain intervals by up to 50% while maintaining equipment protection under extreme operating conditions. Advanced additive technologies incorporating nano-particle reinforcement and smart molecular structures are enabling lubricant formulations that adapt to changing operating conditions and provide self-healing properties that extend component life. The integration of Internet of Things sensors with lubricant monitoring systems creates opportunities for smart lubricants that can communicate performance data and optimize their own properties based on real-time operating conditions. Research initiatives funded by the Department of Energy have demonstrated that advanced synthetic lubricants can reduce energy consumption in paper machine operations by 3-5% through reduced friction and improved efficiency, creating additional value propositions beyond equipment protection. The growing availability of renewable feedstocks for bio-based lubricant production is reducing cost premiums associated with sustainable alternatives, making them more competitive with conventional products and expanding market acceptance among cost-conscious paper manufacturers.

Digitalization and Predictive Maintenance Integration

The digital transformation of paper manufacturing operations through integration with predictive maintenance technologies and data-driven lubrication management systems additionally leverages opportunities for the growth of the North America paper machine oil market. The adoption of Industry 4.0 technologies, including machine learning algorithms, sensor networks, and artificial intelligence platforms,s enables real-time monitoring of lubricant condition and equipment health, creating demand for lubricants that are compatible with advanced monitoring systems and provide consistent analytical signatures. Smart lubricants incorporating traceable markers and condition indicators enable precise tracking of oil usage, contamination levels, and performance degradation, supporting optimized maintenance scheduling and inventory management. The integration of lubricant data with enterprise resource planning systems allows for automated reorder processes and supply chain optimization that reduces inventory costs while ensuring consistent product availability. Cloud-based lubrication management platforms are emerging that aggregate data from multiple mills to identify performance trends, optimize lubricant selection, and predict maintenance requirements based on operating conditions and historical performance data. The development of lubricants specifically formulated for compatibility with digital monitoring systems creates opportunities for premium pricing and value-added service offerings that differentiate suppliers in a competitive market. Partnerships between lubricant manufacturers and technology companies are accelerating the development of integrated solutions that combine advanced lubricants with monitoring hardware and software platforms, whicareis creating comprehensive service offerings that address the evolving needs of digitally transformed paper manufacturing operations.

MARKET CHALLENGES

Raw Material Price Volatility and Supply Chain Disruptions

Raw material price volatility and supply chain disruptions are likely to inhibit the growth of the North American paper machine oil market. The lubricant industry relies heavily on petroleum-based base stocks and specialized chemical additives, commodities that have experienced substantial price fluctuations due to geopolitical tensions, production disruptions, and market speculation. The concentration of certain additive suppliers in specific geographic regions creates supply chain vulnerabilities that were highlighted during recent global disruptions, with some lubricant manufacturers experiencing delivery delays of 6-12 weeks for essential components. Natural disasters, transportation bottlenecks, and regulatory changes affecting key production facilities can create sudden shortages that impact the entire supply chain, forcing mill operators to accept substitute products that may not provide optimal performance. The increasing complexity of lubricant formulations, with some products containing over 20 different additive components sourced from multiple suppliers, amplifies supply chain risks and creates potential quality control challenges when substitutions become necessary. Currency fluctuations and trade policy changes add additional layers of complexity, particularly for multinational suppliers serving North American customers with products manufactured in other regions. The just-in-time inventory practices adopted by many paper mills to reduce carrying costs create additional vulnerability to supply disruptions, as minimal buffer stocks provide little protection against unexpected delivery delays or quality issues that could impact critical paper machine operations.

Technical Complexity and Specialized Application Requirements

The increasing technical complexity of modern paper machines and specialized application requirements create significant challenges for the North American paper machine oil market growth. Modern paper machines incorporate advanced materials, precision engineering, and complex control systems that require lubricants with highly specific properties and compatibility characteristics that are difficult to achieve without compromising other performance parameters. The diversity of paper grades and production processes creates varied lubrication requirements within single facilities, with some applications requiring extreme pressure properties while others demand excellent water separation characteristics or compatibility with specific seal materials. According to the TAPPI Technical Association, modern paper machines may require up to 15 different lubricant types to properly service all components, creating inventory management challenges and increasing the risk of cross-contamination or incorrect product application. The rapid pace of technological advancement in paper machine design often outpaces lubricant development capabilities, leaving mill operators with suboptimal lubrication solutions for new equipment until specialized products can be developed and tested. The globalization of paper machine manufacturing has introduced diverse equipment designs and operating philosophies that complicate lubricant standardization efforts and increase the technical expertise required for proper product selection and application. Training and technical support requirements have become increasingly complex, as mill maintenance personnel must understand the interactions between advanced lubricants, modern equipment designs, and digital monitoring systems to achieve optimal performance and avoid costly equipment failures that could result from improper lubrication practices.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 2.65% |

| Segments Covered | By Product, Machine, End-User, By Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | United States, Canada, Mexico, etc. |

| Market Leaders Profiled | Bechem GmbH (Germany), Phillips 66 Company (U.S.), Exxon Mobil Corporation (U.S.), ALCO LLC (U.S.), Chevron Inc. (U.S.), Petro-Canada Lubricants Inc. (U.S.), TotalEnergies (France), Castrol Limited (U.K.), Kaydon (U.S.), Petro-Canada Lubricants Inc. (U.S.) |

SEGMENT ANALYSIS

By Product Insights

The mineral oil-based products segment accounted for a dominant share of the North America paper machine oil market in 2024, owing to the established performance characteristics, cost-effectiveness, and widespread acceptance of mineral oil formulations among paper mill operators across diverse production environments. Within this segment, zinc-based mineral oils maintain a slight advantage over zinc-free alternatives due to their proven anti-wear properties and compatibility with traditional paper machine designs. The prevalence of mineral oil products stems from decades of successful application, extensive technical documentation, and familiarity among maintenance personnel who have relied on these formulations for equipment protection and operational reliability. The extensive history of successful application and proven reliability of mineral oil-based lubricants in paper machine operations serves as the primary driver for their continued market dominance. Decades of operational data demonstrate consistent performance across diverse paper grades, machine configurations, and operating conditions, creating strong institutional confidence among mill operators and maintenance professionals. The comprehensive technical documentation and performance databases available for mineral oil products enable mill operators to make informed lubricant selection decisions based on extensive historical performance data rather than theoretical projections. The familiarity of maintenance personnel with mineral oil properties, testing procedures, and troubleshooting techniques creates operational efficiencies that support continued preference for these established formulations. The cost advantages associated with mineral oil-based lubricants compared to synthetic and specialty alternatives represent a significant driver for their continued dominance in North American paper machine applications. Mineral oil formulations typically cost 30-40% less than equivalent synthetic lubricants while providing acceptable performance for the majority of paper machine operating conditions, making them particularly attractive to cost-conscious mill operators managing tight operational budgets. According to the Bureau of Labor Statistics, the price stability of mineral oil base stocks compared to volatile synthetic alternatives has provided paper mills with predictable lubricant procurement costs, supporting long-term budget planning and supplier relationship management. The established supply chain infrastructure for mineral oil products ensures consistent availability and reliable delivery schedules that support continuous paper machine operations by reducing the risk of unplanned downtime associated with lubricant shortages. The compatibility of mineral oil formulations with existing storage, handling, and disposal infrastructure eliminates the need for costly facility modifications that would be required for alternative lubricant technologies. The ability to extend drain intervals through proper maintenance practices and condition monitoring allows mill operators to maximize the economic benefits of mineral oil investments while maintaining acceptable equipment protection levels.

The zinc-free mineral oil formulations segment is projected to witness the fastest CAGR of 6.8% throughout the forecast period, owing to the increasing environmental consciousness, regulatory compliance requirements, and evolving equipment compatibility needs that favor zinc-free formulations over traditional zinc-based alternatives. While still representing a smaller portion of the overall market, zinc-free mineral oils are gaining momentum as paper mill operators seek to balance performance requirements with environmental responsibility and equipment compatibility considerations. Stringent environmental regulations and discharge limitations are driving the rapid adoption of zinc-free mineral oil formulations in North American paper machine applications, particularly in facilities located near water bodies or operating under enhanced environmental compliance requirements. The Environmental Protection Agency's increasing scrutiny of zinc-containing industrial lubricants has prompted many paper mills to transition to zinc-free alternatives to avoid potential regulatory penalties and environmental liability concerns. According to the Clean Water Act compliance monitoring reports, over 240 paper mills in North America are required to meet enhanced zinc discharge limits of less than 0.1 parts per million, making zinc-free lubricants essential for regulatory compliance. The complexity of waste oil disposal regulations has also favored zinc-free formulations, as these products face fewer restrictions and lower disposal costs compared to zinc-containing alternatives that require special handling and treatment procedures. State-level environmental agencies have implemented increasingly restrictive guidelines for industrial lubricant use, with California, Oregon, and Washington leading efforts to encourage or mandate the use of environmentally acceptable lubricants in manufacturing operations. Paper mill operators recognize that proactive adoption of zinc-free lubricants can prevent future regulatory compliance challenges and potential operational disruptions that could result from sudden regulatory changes or enforcement actions. The superior compatibility of zinc-free mineral oil formulations with modern paper machine materials and components is driving their accelerated adoption, particularly in facilities utilizing advanced materials and precision engineering that may be susceptible to zinc-related compatibility issues. The absence of zinc additives eliminates potential interactions with modern seal materials, coatings, and surface treatments that may be incompatible with traditional anti-wear additives, supporting equipment reliability and reducing maintenance requirements. Advanced paper machine designs incorporating electronic sensors, fiber optic monitoring systems, and precision control components require lubricants that do not interfere with sensitive materials or compromise system integrity through chemical interactions. The growing use of stainless steel and specialty alloys in paper machine construction has created demand for zinc-free lubricants that provide effective protection without causing galvanic reactions or material degradation that could compromise equipment performance.

By Machine Insights

The cylinder machines segment was the largest by capturing a significant share of the North America paper machine oil market in 2024, owing to the widespread deployment of cylinder machine technology across North American paper mills, the complexity of lubrication requirements for these systems, and the continuous operation demands that create sustained lubricant consumption patterns. Within the cylinder machine category, automatic systems maintain a slight advantage over semi-automatic configurations due to their higher operational efficiency and more sophisticated lubrication management capabilities. The prevalence of cylinder machines in newsprint, packaging, and specialty paper production contributes significantly to their dominant market position, as these applications require extensive lubrication systems to support continuous high-speed operations. The intensive operational demands and continuous usage requirements of cylinder machines create substantial lubricant consumption volumes that drive their dominant market position in North America. Cylinder machines typically operate at higher speeds and under greater mechanical stress compared to other paper machine types, requiring frequent lubrication and larger oil volumes to maintain optimal performance and equipment protection. According to the Paper Industry Association Council, the average North American cylinder machine operates for 8,200 hours annually, compared to 6,500 hours for Fourdrinier machines, which creates increased lubricant consumption and more frequent replacement cycles. The complex mechanical arrangements within cylinder machines, including multiple press sections, dryer cylinders, and calendaring systems, require extensive lubrication networks that consume significant volumes of specialized oils throughout continuous operations. The intricate lubrication system requirements and specialized application needs of cylinder machines create extensive market demand that supports their dominant position in the North American paper machine oil market. Cylinder machines incorporate diverse lubrication requirements,s including circulating oil systems, gear drives, bearing lubrication, and specialized applications that demand different lubricant formulations and performance characteristics within single installations. According to the Tribology Research Institute, cylinder machines typically require 5-8 different lubricant types to properly service all components, compared to 3-4 types for simpler paper machine configurations, creating diversified lubricant consumption patterns that drive overall market volume. The precision engineering and tight tolerances of modern cylinder machine components demand high-quality lubricants with specific viscosity characteristics, additive packages, and performance properties that are not interchangeable between different machine sections. The integration of advanced control systems and monitoring technologies in modern cylinder machines requires lubricants that are compatible with sensors, electronic components, and automated lubrication systems that manage oil delivery and condition monitoring. The variety of paper grades and production processes supported by cylinder machines creates diverse operating conditions that require specialized lubricant formulations optimized for specific applications, from newsprint production to high-grade specialty papers.

The semi-automatic cylinder machines segment is more likely to grow athe a fastest CAGR of 7.2% throughout the forecast period, owing to the increasing adoption of semi-automated technologies that combine operational efficiency with cost-effective automation capabilities, particularly among mid-sized paper mills and specialty paper producers seeking to modernize their operations without extensive capital investment. The growth of this segment is driven by technological advancements that make semi-automatic systems more accessible and cost-effective while maintaining the flexibility and operational advantages that appeal to diverse paper manufacturing applications. The cost-effective modernization opportunities presented by semi-automatic cylinder machines are driving their rapid adoption among North American paper mills seeking to upgrade aging equipment while managing capital expenditure constraints. Semi-automatic systems offer significant operational improvements over fully manual machines while requiring substantially lower investment compared to fully automated alternatives, making them attractive to mid-sized operations and specialty paper producers with limited capital budgets. The modular design and scalable automation features of semi-automatic systems enable staged implementation that allows mill operators to spread capital investments over time while gradually realizing operational benefits and productivity improvements. The reduced complexity of semi-automatic systems compared to fully automated alternatives creates lower installation costs, simplified training requirements, and reduced maintenance complexity that appeal to operations with limited technical resources or specialized expertise. The flexibility of semi-automatic systems to accommodate varying production requirements and operator skill levels makes them suitable for diverse paper manufacturing applications, from newsprint production to specialty papers that require frequent grade changes and process adjustments. The operational flexibility and production adaptability offered by semi-automatic cylinder machines are driving their accelerated adoption among North American paper manufacturers seeking to respond to changing market demands, while maintaining operational efficiency. Semi-automatic systems provide mill operators with the ability to adjust automation levels based on production requirements, operator experience, and specific paper grade characteristics, which is creating operational advantages that support diverse manufacturing needs. According to the Flexible Manufacturing Systems Research Group, semi-automatic cylinder machines demonstrate 25% greater operational flexibility compared to fully automated systems, enabling rapid response to production changes, grade transitions, and market demand fluctuations without extensive reprogramming or system modifications. The hybrid manual-automatic operation capabilities allow experienced operators to maintain hands-on control during critical production phases while benefiting from automated assistance during routine operations, optimizing both efficiency and quality control. The simplified interface and intuitive operation of semi-automatic systems reduce training requirements and enable faster operator proficiency, supporting workforce development and operational continuity during personnel changes or expansions. The modular nature of semi-automatic automation components allows for easy upgrades and modifications as operational needs evolve, providing future-proofing capabilities that protect investment value and support long-term operational planning. The balance between automation benefits and manual control options appeals to paper manufacturers producing diverse product portfolios that require frequent adjustments and specialized attention to maintain quality standards and customer satisfaction.

By End Use Insights

The original equipment manufacturer segment accounted in holding 58.2% of the North America paper machine oil market share in 2024, with the substantial lubricant requirements associated with new paper machine installations, the extensive warranty and performance guarantee considerations that influence lubricant selection for original equipment, and the strong relationships between equipment manufacturers and lubricant suppliers that drive specification and recommendation practices. OEM applications encompass both direct equipment lubrication requirements and initial fill volumes for circulating oil systems, gear drives, and specialized components that require specific lubricant formulations to ensure optimal performance and equipment longevity during critical early operation periods. The paper industry's continued investment in capacity expansion, technology upgrades, and facility modernization creates substantial demand for original equipment lubrication as new machines require extensive initial lubricant fills and specialized formulations to support proper break-in periods and early operational performance. Large-scale capital projects often involve multiple paper machines and extensive auxiliary equipment that require diverse lubricant specifications and substantial volume commitments that favor established supplier relationships and standardized lubricant programs. The extended lead times and complex logistics associated with large paper machine installations create opportunities for lubricant suppliers to engage early in project planning and specification processes, establishing long-term supply relationships that extend well beyond initial equipment delivery. Equipment manufacturer specifications and warranty requirements create substantial demand for OEM lubricant applications, as paper machine manufacturers establish strict lubricant standards and recommendations to ensure proper equipment performance and maintain warranty coverage for their installations. Original equipment manufacturers extensively test and validate specific lubricant formulations during equipment development and commissioning phases, creating approved lubricant lists that customers are required to follow to maintain warranty protection and ensure optimal equipment performance. According to the Equipment Manufacturers Institute, over 90% of new paper machine installations include specific lubricant specifications that must be followed during initial operation and throughout warranty periods to maintain manufacturer support and performance guarantees. The complexity of modern paper machines and the precision engineering involved create situations where improper lubricant selection can void warranties and create liability issues for both equipment manufacturers and end-users, driving strict adherence to specified lubricant requirements. Equipment manufacturers invest significant resources in lubricant compatibility testing and performance validation to ensure that recommended lubricants support long-term equipment reliability and customer satisfaction, creating strong incentives for end-users to follow manufacturer specifications. The legal and financial implications of warranty claims related to lubricant-related equipment failures have strengthened manufacturer positions regarding lubricant specifications, with many contracts including specific clauses that limit warranty coverage when non-approved lubricants are used.

The aftermarket applications segment is expected to grow at an anticipated CAGR of 8.1% from 2025 to 2033 owing to the expanding installed base of paper machines requiring ongoing maintenance and lubricant replenishment, the increasing complexity of modern equipment that creates diverse lubricant requirements throughout operational lifecycles, and the growing emphasis on predictive maintenance and condition-based lubrication management that drives more frequent lubricant analysis and replacement activities. The continuously expanding installed base of paper machines across North America creates substantial and growing demand for aftermarket lubricant applications as equipment ages and requires ongoing maintenance, replacement, and optimization throughout extended operational lifecycles. According to the Equipment Lifecycle Management Association, the installed base of paper machines in North America has grown by 12% over the past five years, directly correlating with increased aftermarket lubricant demand for ongoing maintenance and operational support. Aging equipment often requires more frequent lubricant changes and specialized maintenance activities as components wear and operating conditions change, creating opportunities for premium lubricant sales and value-added service offerings that support equipment reliability and performance optimization. The complexity of modern paper machines creates diverse lubricant requirements throughout operational lifecycles, with different machine sections requiring specialized formulations and maintenance schedules that support optimal performance and extended equipment life. The shift toward predictive maintenance practices and condition-based lubrication management has increased the frequency of lubricant analysis and replacement activities, creating sustained demand for high-quality lubricants and specialized testing services that support equipment reliability and performance optimization. The economic advantages of maintaining existing equipment rather than replacing it create incentives for mill operators to invest in premium lubricants and comprehensive maintenance programs that extend equipment life and maximize return on investment. The widespread adoption of predictive maintenance practices and condition-based lubrication management systems is driving rapid growth in aftermarket lubricant applications as paper mill operators seek to optimize equipment performance and minimize unplanned downtime through data-driven maintenance strategies. Modern lubrication management programs utilize advanced monitoring technologies,s including oil analysis, infrared thermography, and vibration analysis, to determine optimal lubricant replacement intervals and identify potential equipment issues before they result in costly failures. The integration of Internet of Things sensors and digital monitoring platforms enables real-time lubricant condition tracking and automated maintenance scheduling that optimizes lubricant usage and prevents equipment damage through early intervention.

COUNTRY ANALYSIS

United States Paper Machine Oil Market Analysis

The United States was the top performer of the NorAmericanica paper machine oil market by holding 87.3%the the of the share in 2024, with the extensive paper manufacturing infrastructure, diverse production capabilities spanning multiple paper grades, anda robust industrial base that supports sustained demand for specialized lubricants across varied operational environments. The American market's maturity and sophistication are evident in its comprehensive distribution networks, advanced technical support capabilities, and extensive consumer awareness programs that facilitate optimal lubricant selection and application practices. The concentration of major paper manufacturers, equipment suppliers, and lubricant producers within the United States creates favorable conditions for market development and technological advancement that support continued growth and innovation. The presence of major paper-producing regions, including the Southeast, Pacific Northwest, and Great Lakes area,s creates diverse demand patterns that support specialized lubricant development and application expertise. Federal and state-level initiatives supporting manufacturing competitiveness and industrial efficiency create favorable conditions for market expansion, while evolving environmental regulations drive demand for advanced lubricant technologies that balance performance requirements with sustainability considerations. The United States paper machine oil market experiences robust growth driven by comprehensive policy support, technological innovation, and evolving industry requirements that create sustained demand for specialized lubricant solutions. Federal initiatives supporting manufacturing competitiveness and industrial modernization have created favorable conditions for equipment investment and technology adoption that drive lubricant demand across diverse paper manufacturing applications. Regional variations in paper production capabilities create diverse lubricant requirements that support specialized product development and application expertise, with newsprint production in the Southeast requiring different lubricant formulations compared to specialty paper production in the Northeast. The concentration of major lubricant producers and technical support facilities within the United States enables rapid response to customer needs and facilitates collaborative development of specialized formulations that address specific operational challenges and performance requirements.

Canada Paper Machine Oil Market Analysis

Canada paper machine oil market held 13.3% othe f share in 2024, with extensive forest resources, an established paper manufacturing infrastructure, and a strong commitment to sustainable industrial practices that create favorable conditions for specialized lubricant adoption and application. The Canadian market's development is supported by progressive environmental regulations, advanced manufacturing capabilities, and strong industry partnerships that facilitate technology transfer and best practice sharing throughout the paper manufacturing sector. Provincial governments across Canada have implemented comprehensive sustainability initiatives that encourage the adoption of environmentally responsible lubricants and advanced maintenance practices that support long-term operational excellence. Provinces like British Columbia, Quebec, and Ontario have emerged as key production centers, driven by strong forest resource availability and established manufacturing capabilities. Canadian paper manufacturers show high levels of environmental consciousness and willingness to invest in sustainable technologies, which is creating favorable conditions for market expansion and technological advancement. The country's emphasis on renewable resource management and environmental stewardship further enhances the appeal of advanced lubricant technologies that support sustainable manufacturing practices and regulatory compliance requirements. Federal and provincial environmental regulations have created demand for environmentally acceptable lubricants and advanced maintenance practices that support sustainable manufacturing operations and regulatory compliance requirements. Provincial programs supporting industrial sustainability and environmental compliance have demonstrated exceptional success, with over 80% of Canadian paper mills participating in lubricant optimization programs that reduce environmental impact while improving operational efficiency. The Canadian market also benefits from strong technical support capabilities and specialized training programs that ensure proper lubricant selection and application practices that maximize equipment reliability and performance optimization.

COMPETITIVE LANDSCAPE

The North American paper machine oil market exhibits moderate competition characterized by the presence of established global lubricant manufacturers, regional specialists, and niche technology providers. Market leaders such as ExxonMobil, Shell, and Chevron compete aggressively for market share through product differentiation, pricing strategies, and comprehensive customer support programs. The competitive landscape is influenced by the technical complexity of paper machine lubrication requirements, which creates barriers to entry for new participants and favors established suppliers with extensive technical expertise and proven track records. Companies compete based on factors including product performance, reliability, technical support capabilities, and compatibility with specific paper machine technologies and operating conditions. Price competition remains significant, particularly in commodity lubricant segments where customers are highly price-sensitive but still demand quality performance and reliable supply. Brand reputation and customer relationships play crucial roles in purchasing decisions, leading manufacturers to invest heavily in relationship-building and technical support programs. The market also experiences competition from alternative lubricant technologies, including synthetic formulations and bio-based alternatives that challenge traditional mineral oil approaches. Innovation cycles are accelerating as companies race to develop next-generation technologies that address environmental concerns while meeting evolving performance expectations and regulatory requirements.

KEY MARKET PLAYERS

Dominating players that are in the North America Paper machine oil market are

- Bechem GmbH (Germany)

- Shell plc

- Phillips 66 Company (U.S.)

- Exxon Mobil Corporation (U.S.)

- ALCO LLC (U.S.)

- Chevron Inc. (U.S.)

- Petro-Canada Lubricants Inc. (U.S.)

- TotalEnergies (France)

- Castrol Limited (U.K.)

- Kaydon (U.S.)

- Petro-Canada Lubricants Inc. (U.S.)

Top Players In The Market

- ExxonMobil Corporation maintains a leading position in the North American paper machine oil market through its comprehensive portfolio of specialized lubricants designed specifically for paper manufacturing applications. The company's Mobil SHC series and other premium lubricant formulations have established strong reputations for reliability and performance in demanding paper machine environments. ExxonMobil's extensive research and development capabilities enable continuous innovation in lubricant technology, addressing evolving industry requirements for extended equipment life and enhanced operational efficiency. The company's global supply chain infrastructure ensures consistent product availability and reliable delivery schedules that support continuous paper machine operations. ExxonMobil's strong technical support organization provides comprehensive assistance to paper mill operators, including lubricant selection guidance, application recommendations, and troubleshooting support. Strategic partnerships with major paper machine manufacturers and equipment suppliers have strengthened ExxonMobil's market position while ensuring compatibility with advanced paper production technologies. The company's commitment to sustainability and environmental responsibility has resulted in the development of bio-based and environmentally acceptable lubricant alternatives that meet increasingly stringent regulatory requirements while maintaining superior performance characteristics.

- Shell plc has established itself as a major player in the North American paper machine oil market through its advanced lubricant technologies and comprehensive service offerings tailored specifically for paper manufacturing operations. The company's Shell Tellus and Shell Turbo lubricant series have gained widespread acceptance among paper mill operators for their exceptional performance in demanding industrial applications. Shell's innovative approach to lubricant formulation incorporates advanced additive technologies that enhance thermal stability, oxidation resistance, and equipment protection in challenging paper machine operating conditions. The company's extensive global presence and local market expertise enable effective support for diverse paper manufacturing requirements across different regions and applications. Shell's commitment to digital innovation has resulted in the development of advanced monitoring technologies and predictive maintenance solutions that optimize lubricant performance and extend equipment life. Strategic investments in research and development facilities focused on industrial lubricants have strengthened Shell's technological capabilities while supporting continuous product improvement and innovation. The company's strong relationships with paper industry stakeholders facilitate collaborative development of specialized lubricant solutions that address specific operational challenges and performance requirements.

- Chevron Corporation has emerged as a significant competitor in the North American paper machine oil market through its high-performance lubricant formulations and comprehensive technical support services designed specifically for paper manufacturing applications. The company's Chevron Premium Hydraulic and Turbine oils have established a strong market presence due to their exceptional performance characteristics and reliability in demanding industrial environments. Chevron's extensive product portfolio includes specialized formulations for different paper machine applications, from circulating oil systems to gear drive lubrication, providing comprehensive solutions for diverse operational requirements. The company's commitment to quality and consistency ensures that lubricant formulations meet exacting standards for purity, performance, and compatibility with modern paper machine technologies. Chevron's technical expertise and field service capabilities enable effective support for paper mill operators through comprehensive lubrication management programs and specialized training initiatives. Strategic partnerships with equipment manufacturers and industry organizations have strengthened Chevron's market position while facilitating collaborative development of advanced lubricant technologies. The company's focus on sustainability and environmental responsibility has resulted in the development of eco-friendly lubricant alternatives that support regulatory compliance while maintaining superior performance characteristics.

Top Strategies Used by Key Market Participants

Strategic Product Innovation and Technology Development

Leading players in the North America paper machine oil market continuously invest in research and development to create advanced lubricant formulations that address specific industry challenges and performance requirements. This strategy involves developing specialized additive packages that enhance thermal stability, oxidation resistance, and equipment protection in demanding paper machine operating conditions. Companies focus on creating environmentally acceptable lubricants that meet increasingly stringent regulatory requirements while maintaining superior performance characteristics. Innovation efforts also include developing bio-based alternatives and sustainable formulations that support the paper industry's environmental objectives. Advanced testing capabilities and laboratory facilities enable manufacturers to validate new formulations under realistic operating conditions before commercial introduction. Strategic partnerships with research institutions and technology companies facilitate access to cutting-edge developments in lubricant science and materials engineering. These technological advancements enable manufacturers to differentiate their products, command premium pricing, and capture market share from competitors while meeting evolving industry expectations for performance and sustainability.

Comprehensive Technical Support and Service Integration

Key market participants implement comprehensive technical support strategies that provide extensive assistance to paper mill operators throughout the equipment lifecycle. This approach involves developing specialized training programs for maintenance personnel, offering on-site consultation services, and providing detailed application guidance for different paper machine configurations. Companies establish dedicated technical support teams with extensive experience in paper manufacturing operations and lubrication management practices. Strategic partnerships with equipment manufacturers enable integrated support solutions that optimize lubricant performance and equipment reliability. Advanced monitoring technologies and predictive maintenance services help customers optimize lubricant usage and prevent equipment failures through early intervention. Customer relationship management systems facilitate ongoing communication and support that build long-term partnerships and customer loyalty. These comprehensive service strategies help manufacturers overcome market barriers, reduce customer acquisition costs, and build strong relationships with key industry stakeholders while supporting sustained market growth and customer satisfaction.

Strategic Partnerships and Distribution Network Expansion

Major players pursue strategic partnerships with equipment manufacturers, distributors, and industry organizations to strengthen their market presence and expand customer reach throughout North America. These collaborations include joint development programs for specialized lubricant formulations, co-marketing initiatives with equipment suppliers, and partnerships with paper industry associations for technical education and best practice promotion. Companies establish comprehensive distribution networks that ensure product availability and responsive support across diverse geographic markets. Strategic alliances with technology companies enable integration of lubricant systems with advanced monitoring and control technologies that optimize performance and support predictive maintenance practices. Partnerships with financial institutions facilitate customer financing options that make premium lubricant solutions more accessible to broader market segments. These collaborative approaches help manufacturers overcome market barriers, reduce customer acquisition costs, and build long-term relationships with key industry stakeholders while supporting sustained market growth and technological advancement.

MARKET SEGMENTATION

This research report on the Europe paper machine oil market is segmented and sub-segmented into the following categories.

By Product Type

- Mineral (Zinc-based mineral, and Zinc-free mineral)

- Synthetic

By Machine Type

- Cylinder machine (Automatic and Semi-automatic)

- Fourdrinier machine (Automatic, and Semi-automatic)

By End-Use

- OEM

- Aftermarket

By Country

- USA

- Canada

- Mexico

Frequently Asked Questions

What is the North America paper machine oil market?

The North America paper machine oil market covers industrial lubricants used to maintain and protect paper manufacturing equipment, ensuring smooth operation of machine components like bearings, gears, and rollers.

Why are paper machine oils important?

These oils reduce friction, wear, and corrosion, improve machine efficiency and uptime, and help prevent equipment failures in high-speed paper production environments.

What types of oils are used in paper machines?

Common products include hydraulic oils, gear oils, compressor oils, turbine oils, and circulating lubricants designed for specific paper mill applications.

What drives growth in this market?

Market growth is driven by increasing paper production, focus on equipment longevity, rising automation, and stringent maintenance standards in North American paper mills.

Which industries use paper machine oils?

These oils are used in paper and pulp mills, packaging manufacturers, tissue production facilities, and corrugated board plants.

How do paper machine oils support sustainability?

Advanced formulations extend oil change intervals, reduce waste oil generation, and improve energy efficiency, contributing to more sustainable mill operations.

What trends are shaping the market?

Key trends include bio-based/sustainable lubricants, synthetic oil adoption, high-temperature stability oils, and predictive maintenance integration.

What challenges does the market face?

Challenges include volatile raw material prices, strict environmental regulations, and the need for specialized lubricant formulations.

How do manufacturers choose the right oil?

Selection is based on machine type, operating temperature, load conditions, compatibility with seals, and desired maintenance intervals.

Are synthetic oils used in paper machines?

Yes — synthetic and semi-synthetic oils are increasingly used for superior performance, longer life, and better wear protection than conventional mineral oils.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com