North America Peptide Therapeutics Market Research Report By Type, Application, Type of Manufacturers, Route of Administration, Synthesis Technology & Country (The United States, Canada and Rest of North America) – Industry Analysis( 2026 to 2034)

North America Peptide Therapeutics Market Size

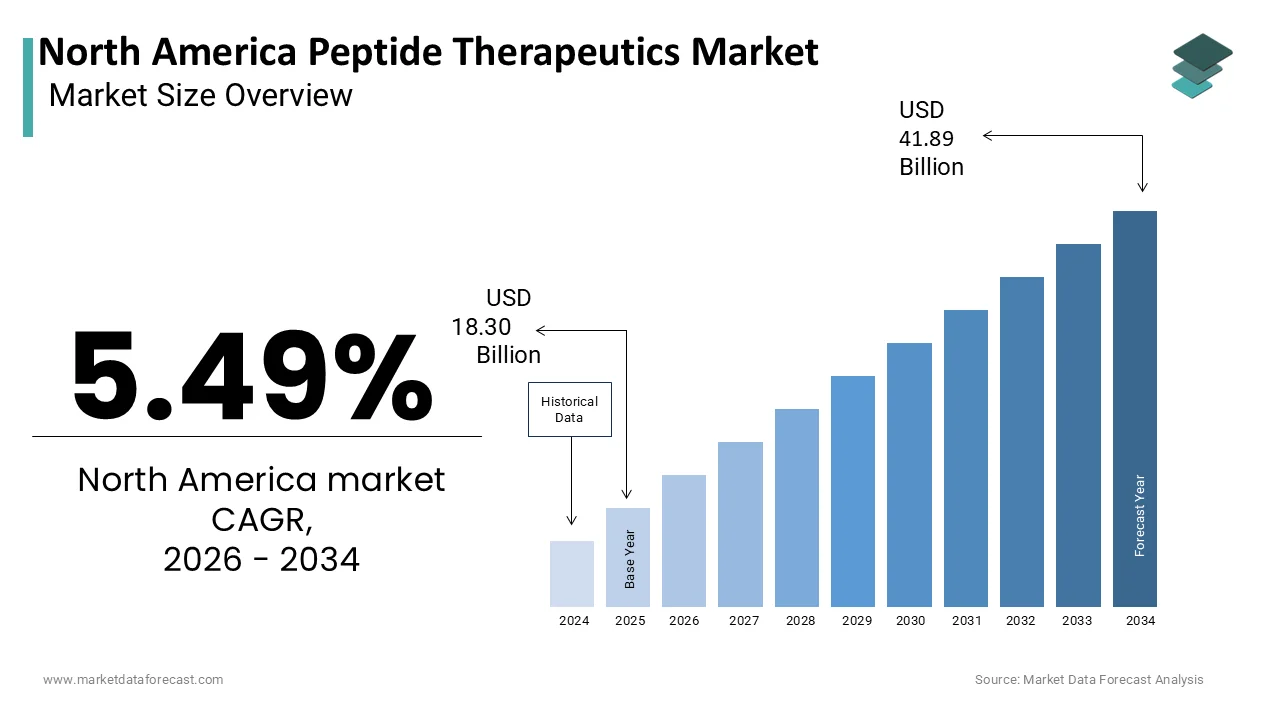

The North America Peptide Therapeutics Market Size was valued at USD 18.30 billion in 2025, is expected to have 9.64% CAGR from 2026 to 2034, and be worth USD 41.89 billion by 2034 from USD 20.06 billion in 2026.

Peptide therapeutics are short chains of amino acids designed to mimic natural peptides in the body, offering highly specific and targeted treatment for a range of diseases, including cancer, diabetes, cardiovascular disorders, and autoimmune conditions. In North America, the market for peptide-based therapies is experiencing robust growth due tothe rising prevalence of chronic diseases, rapid advancements in biopharmaceutical research, and increasing investments by pharmaceutical companies in novel drug development.

The United States and Canada are at the forefront of this expansion, driven by strong R&D infrastructure, favorable regulatory frameworks, and a high level of healthcare expenditure. According to the Centers for Disease Control and Prevention (CDC), more than 60% of adults in the U.S. suffer from at least one chronic disease, making targeted therapies such as peptides increasingly important in clinical practice. Additionally, the National Institutes of Health (NIH) has significantly increased funding for biotechnology and pharmaceutical innovation, supporting the discovery and commercialization of next-generation peptide drugs. North America also benefits from a well-established ecosystem of academic institutions, contract research organizations, and biotech startups actively engaged in developing novel peptide formulations.

MARKET DRIVERS

Increasing Prevalence of Chronic Diseases Driving Demand for Targeted Therapies

The rising burden of chronic diseases such as diabetes, cancer, and cardiovascular disorders is a key driver fueling the demand for peptide therapeutics in North America. According to the Centers for Disease Control and Prevention (CDC), approximately 37 million Americans suffer from diabetes, with type 2 diabetes accounting for nearly 90–95% of cases. The high specificity and efficacy of peptides in modulating biological pathways make them ideal candidates for managing these conditions. Moreover, the aging population across North America further amplifies the demand for chronic disease management solutions. As per the U.S. Census Bureau, the proportion of individuals aged 65 and above is projected to reach nearly 25% of the total population by 2060. This demographic shift is expected to sustain the demand for innovative peptide therapeutics in the coming decades.

Expansion of Biopharma Innovation Hubs and Increased R&D Investments

The rapid expansion of biopharmaceutical innovation hubs across North America has significantly accelerated the development and commercialization of peptide therapeutics. The United States and Canada are leading this transformation by offering robust regulatory frameworks, state-of-the-art laboratory infrastructure, and favorable funding policies. Major pharmaceutical players such as Amgen, Eli Lilly, and Novo Nordisk have established dedicated R&D centers focused on peptide engineering and targeted delivery systems. Academic institutions like Harvard Medical School, Stanford University, and the University of Toronto are also conducting groundbreaking research in peptide vaccine development and immune modulation. Government-led initiatives, including the U.S. Biomedical Advanced Research and Development Authority (BARDA), support public-private partnerships aimed at accelerating the translation of scientific discoveries into clinical applications. These advancements collectively contribute to a thriving ecosystem for peptide therapeutics, which is positioning North America as a global leader in the field.

MARKET RESTRAINTS

High Manufacturing Costs and Complex Production Requirements

One of the most significant barriers to the widespread adoption of peptide therapeutics in North America is the high cost associated with synthesis and large-scale manufacturing. Peptides are typically produced through solid-phase peptide synthesis (SPPS) or recombinant DNA technology both of which require specialized equipment, highly skilled personnel, and stringent quality control measures. Moreover, scaling up peptide production while maintaining consistency and purity remains a technical challenge, especially for longer-chain peptides. For instance, the synthesis of a 40-amino-acid-long peptide can take several weeks and yield only a fraction of the desired product after purification.

Regulatory Complexity and Stringent Approval Processes Across the Region

The regulatory landscape for peptide therapeutics in North America is highly rigorous, posing a major challenge for market participants. In the United States, the Food and Drug Administration (FDA) requires extensive preclinical and clinical data before approving new peptide drugs, often extending the approval timeline beyond two years. As per a Deloitte report, nearly 40% of pharmaceutical firms operating in North America cite regulatory hurdles as a major obstacle to timely product launches. These bureaucratic inefficiencies hinder innovation diffusion and delay patient access to life-saving peptide therapie, in niche therapeutic areas where clinical validation is complex. Additionally, post-marketing surveillance requirements imposed by both agencies add another layer of scrutiny.

MARKET OPPORTUNITIES

Integration of AI and Machine Learning in Peptide Discovery and Drug Design

The integration of artificial intelligence (AI) and machine learning (ML) into peptide discovery is revolutionizing the way new therapeutics are designed and optimized. Traditional methods of peptide drug development are time-consuming and resource-intensive, but AI-driven platforms enable faster identification of lead candidates with enhanced stability, potency, and reduced side effects. According to Accenture, AI applications in drug discovery could save the pharmaceutical industry up to USD 100 billion annually by 2030, with peptides being a major beneficiary of this transformation.

In the U.S., companies like Insilico Intelligence and Recursion Pharmaceuticals are leveraging deep learning models to accelerate peptide-based drug development. For example, Insilico developed an AI platform capable of generating novel peptide sequences tailored for specific disease targets, reducing early-stage discovery timelines by 60%. Additionally, collaborations between academic institutions and tech firms are gaining traction; the Massachusetts Institute of Technology (MIT) partnered with Alphabet’s DeepMind to develop ML models for predicting peptide-drug interactions, improving success rates in preclinical trials. As governments and private investors continue to fund digital health innovation, AI-enabled peptide research is poised for exponential growth.

Growth of Personalized Medicine and Precision Therapeutics in Oncology and Autoimmune Disorders

The rise of personalized medicine is creating a strong foundation for the expansion of peptide therapeutics, particularly in oncology and autoimmune disease treatment. Unlike traditional therapies that follow a one-size-fits-all approach, personalized medicine leverages genetic profiling and biomarker analysis to tailor treatments for individual patients. According to the American Society of Clinical Oncology (ASCO), the use of targeted therapies in cancer treatment has increased by over 40% in the past five years, with peptides playing a pivotal role in developing tumor-specific agents.

In the U.S., the National Cancer Institute (NCI) has launched several initiatives to integrate genomic data into clinical decision-making, supporting the development of peptide vaccines targeting specific neoantigens in cancer patients.

MARKET CHALLENGES

Shortage of Skilled Workforce in Peptide Chemistry and Biopharmaceutical Development

Despite the growing demand for peptide-based therapies, North America faces a critical shortage of professionals trained in peptide chemistry, formulation science, and biopharmaceutical development. Developing high-quality peptide drugs requires expertise in areas such as solid-phase synthesis, cyclization, and bioconjugatio,n specialized skills that are not widely available across all universities and training programs. According to the American Chemical Society, less than 10% of pharmaceutical graduates in the U.S. receive formal training in peptide synthesis techniques. While top-tier institutions like MIT, Stanford, and the University of California, San Diego offer advanced courses, there is a notable gap in workforce readiness at the industrial level. This scarcity of skilled labor affects both academia and industry, slowing down the pace of drug discovery and development. Moreover, competition for experienced peptide scientists is intensifying, with multinational corporations offering premium salaries, making it difficult for smaller biotech firms to retain top talent.

Limited Oral Bioavailability and Stability Issues in Peptide-Based Drugs

A persistent scientific challenge in the field of peptide therapeutics is their poor oral bioavailability and susceptibility to enzymatic degradation. Most peptides are administered via injection because they are rapidly broken down in the gastrointestinal tract when taken orally. In response, researchers across North America are exploring strategies such as chemical modifications, encapsulation in nanoparticles, and prodrug approaches to enhance peptide stability. However, these innovations come with added complexity and cost. For instance, the development of oral insulin formulationsis ae long-standing goal in peptide therapeutics has faced repeated setbacks due to insufficient absorption and inconsistent efficacy.

REPORT COVERAGE

| METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Application, Type of Manufacturers, Route of Administration, Synthesis Technology and Country. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | The U.S., Canada and Rest of North America |

| Market Leader Profiled | Pfizer, Inc., Bristol-Myers Squibb Company, Ever Neuro Pharma GmbH, Takeda Pharmaceutical Company Limited, AstraZeneca PLC, GlaxoSmithKline plc |

SEGMENTAL ANALYSIS

By Type Insights

The generic peptide therapeutics segment was the largest and held 55.3% of the North America peptide therapeutics market share in 2025. In the United States, the expiration of patents on several blockbuster peptides has led to a surge in biosimilar development. According to the U.S. Food and Drug Administration (FDA), over 12 new generic peptide drugs were approved between 2021 and 2023, significantly expanding treatment accessibility. Moreover, regulatory agencies such as Health Canada have introduced expedited approval pathways for biosimilar peptides, encouraging domestic manufacturers to scale up production. As per the Canadian Generic Pharmaceutical Association, generic peptides now represent nearly half of all prescribed diabetes medications in Canada.

The innovative peptide therapeutics segment is projected to grow with a CAGR of 14.7% in the next coming years. Additionally, advancements in AI-driven drug design and synthetic biology have accelerated the development of long-acting, high-stability peptides tailored for chronic disease management. Companies like Amgen, Novo Nordisk, and Eli Lilly are leading the charge in bringing these innovations to market. The innovative peptide segment is set to experience rapid expansion across North America as patient demand for precision medicine rises and regulatory agencies prioritize fast-track approvals.

By Application Insights

The metabolic disorders segment was accounted in holding 38.1% of the North American peptide therapeutics market share in 2025. According to the Centers for Disease Control and Prevention (CDC), over 37 million Americans suffer from diabetes, with type 2 diabetes affecting nearly 95% of diagnosed cases. The widespread adoption of GLP-1 receptor agonists peptide-based drugs such as semaglutide and liraglutide has surged in recent years due to their efficacy in glycemic control and weight management.

The oncology applications segment is likely to grow with a CAGR of 16.3% during the forecast period. As reported by the American Cancer Society, over 1.9 million new cancer cases were diagnosed in the U.S. in 2023 alone. In response, pharmaceutical companies and research institutions are investing heavily in peptide vaccines, radiolabeled peptides, and peptide-drug conjugates (PDCs) for precision oncology. In Canada, the Terry Fox Research Institute estimates that breast, prostate, and colorectal cancers account for more than 40% of all diagnoses in the country. Peptide-based immunotherapies are gaining traction in personalized cancer treatment strategies, with clinical trials demonstrating improved tumor targeting and immune activation. Regulatory agencies such as the FDA have also expedited approvals for innovative oncology drugs.

By Type of Manufacturers Insights

The In-house manufacturing segment held dominant share of the North American peptide therapeutics market in 2025. In the United States, major players like Amgen, Eli Lilly, and Novo Nordisk operate advanced manufacturing facilities that comply with stringent international standards set by the FDA and EMA. These companies benefit from proximity to research centers and favorable regulatory conditions that facilitate rapid product development. Similarly, in Canada, Apotex and Bausch Health have invested heavily in vertical integration, building dedicated peptide synthesis units capable of producing both APIs and finished dosage forms. As per the Canadian Intellectual Property Office, over 70% of domestically produced peptides are manufactured in-house by top-tier companies.

The outsourced segment is swiftly emerging with a CAGR of 18.1% during the forecast period. The U.S. has become a global hub for contract manufacturing organizations (CMOs) specializing in peptides. According to the Biotechnology Innovation Organization (BIO), outsourcing activity in the peptide space grew by 35% in 2023, with companies like Bachem, Lonza, and Polypeptide Group offering end-to-end services for API synthesis and formulation development.

By Route of Administration Insights

The parenteral route segment dominated the North American peptide therapeutics market with significant share in 2025. In the United States, the majority of approved peptide drugs are administered via injection, with the FDA approving only one oral peptide formulation in the last decade. Canada follows a similar trend, with most hospitals and clinics relying on injectable peptide therapies for conditions such as diabetes, cancer, and hormone deficiencies. As per the University of Toronto’s Leslie Dan Faculty of Pharmacy, intravenous and subcutaneous routes remain the gold standard for delivering peptides due to their predictable pharmacokinetics and rapid onset of action.

The oral route of administration segment is likely to grow with a CAGR of 19.5% over the forecast period. This growth is primarily driven by advancements in formulation technologies aimed at overcoming the traditional barriers associated with oral peptide delivery. In the U.S., companies like Encelle and Oramed Pharmaceuticals are pioneering oral insulin formulations designed to enhance peptide absorption without compromising stability. Collaborative efforts between academia and industry are further accelerating progress. In California, Stanford University partnered with a Silicon Valley biotech firm to develop enteric-coated microcapsules that protect peptides from gastric degradation.

By Synthesis Technology Insights

The solid Phase Peptide Synthesis (SPPS) segment was accounted in holding a dominant share of the North American peptide therapeutics market in 2025. In the U.S., SPPS is extensively used by leading pharmaceutical companies such as Amgen, Merck, and Bristol Myers Squibb for the development of complex cyclic peptides. According to the Journal of Peptide Science, over 90% of commercially synthesized peptides in the U.S. utilize SPPS due to its superior purification efficiency and reproducibility.

The hybrid synthesis technology segment is likely to grow with a CAGR of 20.4% in the next coming years. In the U.S., companies like Genscript and Pepscan have pioneered hybrid approaches to synthesize difficult sequences such as disulfide-rich peptides and post-translationally modified proteins. According to the Biotechnology Innovation Organization, hybrid methods have enabled a 60% reduction in synthesis time for peptides above 40 amino acids. Academic institutions are also advancing this field. MIT’s Koch Institute for Integrative Cancer Research is leveraging hybrid technology to produce therapeutic peptides with enhanced stability and bioactivity.

COUNTRY LEVEL ANALYSIS

The United States was the largest contributor with 82.1% of the North America peptide therapeutics market share in 2025. According to the National Institutes of Health (NIH), over USD 45 billion was allocated toward biomedical research in 2023, with a significant portion directed toward peptide and protein-based drug discovery. The U.S. Food and Drug Administration (FDA) has implemented expedited approval pathways for innovative therapies, particularly in oncology and metabolic disorders. Major pharmaceutical players such as Eli Lilly, Amgen, and Novo Nordisk are expanding their peptide portfolios, while startups like PepGen and Aegle Therapeutics are driving innovation in neuromuscular and dermatological applications.

Canada was positioned second with a 14.3% of the North America peptide therapeutics market share in 2025. Toronto and Montreal have emerged as key hubs for peptide research, with institutions like the University of Toronto and McGill University conducting groundbreaking work in peptide vaccine development and targeted drug delivery. Canadian firms such as Polypeptide Group Canada and Cyclopharm are scaling up production of both generic and innovative peptides, which is supplying both domestic and international markets. Health Canada has also streamlined approval processes for biosimilar peptides, encouraging local manufacturing and import substitution.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Eli Lilly and Company, Amgen, Inc., Pfizer, Inc., Bristol-Myers Squibb Company, Ever Neuro Pharma GmbH, Takeda Pharmaceutical Company Limited, AstraZeneca PLC, GlaxoSmithKline plc, Novo Nordisk A/S., Novartis AG, Zealand Pharma AG, AmbioPharm Inc., Bachem Holding AG, PolyPeptide Group, Sanofi SA, Amylin Pharmaceuticals, CirclePharma, Inc., PeptiDream Inc., Apitope Technology, Arch NioPartners, and Galena Biopharmaceuticals are some of the major players in the North American peptide therapeutics market.

The competition in the North America peptide therapeutics market is highly dynamic, characterized by the presence of established pharmaceutical giants, fast-growing biotech firms, and specialized contract development organizations. The market is witnessing intense rivalry as companies strive to differentiate themselves through innovation, proprietary technologies, and strategic collaborations. Major players are leveraging their deep financial resources and well-established R&D infrastructure to bring novel peptide-based treatments to market faster than ever before.

At the same time, emerging biotech firms are playing a disruptive role by introducing cutting-edge peptide engineering techniques, AI-assisted drug design, and novel delivery systems. These smaller players often attract venture capital funding and form strategic partnerships with larger pharmaceutical companies to scale up their innovations.

Regulatory support from agencies like the U.S. Food and Drug Administration (FDA) and Health Canada is also influencing competitive dynamics by expediting approvals for breakthrough therapies. This environment fosters rapid product development and commercialization, encouraging new entrants and intensifying market competition.

RECENT HAPPENINGS IN THE MARKET

In February 2025, Eli Lilly announced a strategic collaboration with a Boston-based biotech startup to co-develop next-generation GLP-1 analogs with extended duration and enhanced metabolic effects, aimed at strengthening its dominance in diabetes and obesity treatment markets.

In May 2025, Amgen expanded its peptide R&D division in California by acquiring a boutique peptide engineering firm, reinforcing its capabilities in oncology-focused peptide-drug conjugates and accelerating clinical trial timelines.

In August 2025, Bachem North America launched a state-of-the-art peptide synthesis facility in Pennsylvania, designed to increase production capacity and ensure compliance with FDA's current Good Manufacturing Practice (cGMP) standards for global clients.

In October 2025, Novo Nordisk entered into a licensing agreement with a Canadian biotech firm to gain access to a novel oral peptide delivery platform, marking a significant step toward overcoming traditional barriers in peptide administration.

In December 2025, PepGen, a Massachusetts-based biotech company, initiated a phase II clinical trial in partnership with the NIH to evaluate its proprietary peptide-based therapy for rare neuromuscular diseases, which is signaling growing interest in expanding peptide applications beyond traditional therapeutic areas.

MARKET SEGMENTATION

This research report on the north america peptide therapeutics market has been segmented and sub-segmented into the following categories

By Type

- Generic

- Innovative

By Application

- Metabolic

- oncology applications

By Type of Manufacturers

- In-house

- Outsourced

By Route of Administration

- Parenteral Route

- Oral Route

By Synthesis Technology

- Solid Phase Peptide Synthesis (SPPS)

- Hybrid Technology

By Country

- The United States

- Canada

- Rest of North America

Frequently Asked Questions

What is the North America peptide therapeutics market size?

The North American peptide therapeutics market size is expected to be worth USD 16.69 bn in 2024.

What factors are driving the growth of the peptide therapeutics market in North America?

The growth of the peptide therapeutics market in North America is driven by factors such as the increasing adoption of advanced therapies by healthcare sectors, rising healthcare expenditure, the presence of manufacturing facilities, conducting awareness programs by organizations, and advancements in research and development.

What is the market share of the United States in the North America peptide therapeutics market?

The United States holds a significant market share in the North America peptide therapeutics market due to its strong pharmaceutical industry, extensive manufacturing facilities, and a large number of approved peptide drugs. It is the key driver of market growth in the region.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com