North America Personal Emergency Response Systems (PERS) Market Size, Share, Trends & Growth Forecast Report By Type (Mobile Based, Landline Based, Standalone), End User & Country (The United States, Canada & Rest of North America), Industry Analysis From 2025 to 2033

North America Personal Emergency Response Systems (PERS) Market Size

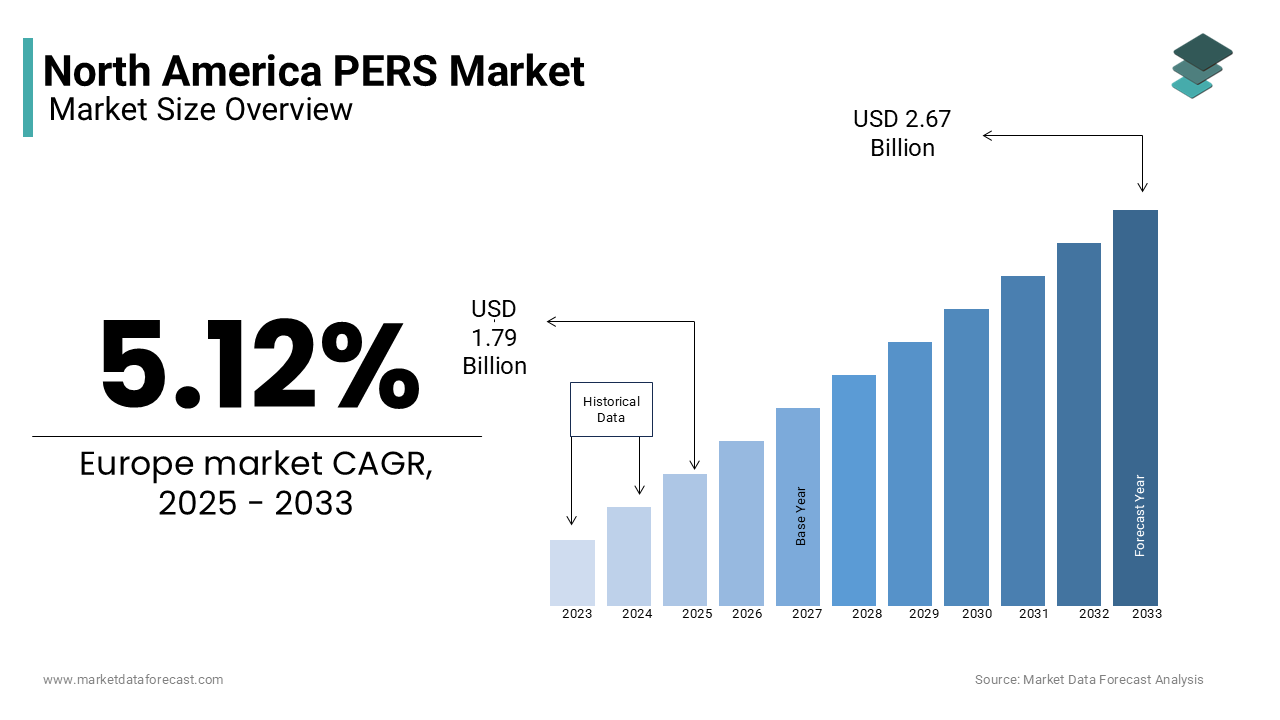

The personal emergency response systems (PERS) market in North America is anticipated to rise from USD 1.70 billion in 2024 to USD 2.67 billion in 2033, growing at a CAGR of 5.12%.

Personal Emergency Response Systems (PERS) refer to the network of wearable and in-home technologies designed to enable individuals, primarily seniors and those with chronic conditions, to summon immediate assistance during medical or safety emergencies. These systems typically consist of a base unit connected to a monitoring center and a portable help button, with modern iterations incorporating fall detection, GPS tracking, and two-way voice communication. According to the U.S. Census Bureau, over 57 million Americans were aged 65 and older in 2023, a figure projected to reach 80 million by 2040. The Centers for Disease Control and Prevention reports that one in four Americans aged 65+ experiences a fall annually, with falls being the leading cause of injury-related death in this demographic. These demographic and safety realities have elevated PERS from a niche service to a critical component of aging-in-place infrastructure.

MARKET DRIVERS

The rapidly aging population and the strong cultural preference for independent living among older adults are the primary drivers of the North American PERS Market. According to the U.S. Census Bureau, the 65+ age cohort grew by 38% between 2010 and 2023, with nearly 90% of seniors expressing a desire to remain in their homes as they age, as confirmed by the National Council on Aging. This "aging in place" trend intensifies demand for safety technologies that mitigate risks without necessitating institutional care. In 2023, the AARP Public Policy Institute found that over 14 million households with seniors had adopted some form of home-based emergency response system, often subsidized through Medicare Advantage plans. Similarly, in Canada, the proportion of citizens over 65 is expected to reach 25% of the population by 2035, according to Statistics Canada, driving provincial health authorities to integrate PERS into home care programs.

Another pivotal factor is the integration of PERS into value-based care models and government-backed health initiatives. The Centers for Medicare & Medicaid Services (CMS) pointed out in 2023 that over 70% of Medicare Advantage plans now cover PERS as a supplemental benefit, recognizing its role in reducing hospital admissions and emergency response costs. PERS users had a lower rate of fall-related hospitalizations compared to non-users, translating to significant cost savings for payers. These systemic validations position PERS as both a clinical and economic imperative in elder care.

The advancement of mobile and AI-enhanced PERS technologies, which expand usability beyond fixed home systems, is another major driver. According to the Federal Communications Commission, over 73% of 65+ Americans now own a smartphone, enabling the adoption of mobile PERS with GPS and automatic fall detection. Philips’ Lifeline with AutoAlert system, for instance, detects falls with 95% accuracy, as validated by clinical trials cited in the Journal of the American Geriatrics Society. In 2023, as per the GreatCall (a Lively company), 40% of its subscribers activated emergency response while outside the home, underscoring the demand for mobility-based protection. The integration of artificial intelligence, such as predictive analytics that identify movement anomalies, further enhances proactive intervention.

Additionally, partnerships between PERS providers and telehealth platforms are increasing service utility. The National Institute on Aging showcases that AI-driven behavioral monitoring can detect early signs of cognitive decline through changes in daily activity patterns captured by PERS-linked sensors. These technological evolutions transform PERS from reactive tools into proactive health management systems, broadening their appeal beyond emergency response to holistic senior wellness.

MARKET RESTRAINTS

The persistent affordability and insurance coverage gap, particularly for low-income and rural populations, is one major restraint in the North American PERS Market. As per the U.S. Department of Health and Human Services, over 15 million older adults live below or near the poverty line, limiting their ability to adopt even subsidized systems. In rural areas, where emergency response times average 25 minutes compared to 8 minutes in urban centers, as per the National Rural Health Association, access to PERS is paradoxically lowest despite higher need.

A further contributing factor is the lack of universal reimbursement policies across state and federal programs. While Medicare Part B does not cover PERS, reliance on Medicare Advantage plans creates disparities in access based on geographic location and plan selection. A 2023 Government Accountability Office review found that PERS coverage varied in 34 states, with some Medicaid waivers offering limited support. In Canada, only four provinces provide partial funding for PERS, according to the Canadian Institute for Health Information. These inconsistencies fragment the market and discourage widespread adoption, particularly among vulnerable populations who stand to benefit most from immediate emergency connectivity.

User resistance due to stigma, usability challenges, and distrust in technology among older adults is another significant restraint. According to the Pew Research Center, only 53% of Americans aged 65+ feel confident using digital health tools, and many perceive PERS devices as symbols of frailty or loss of independence. As per the National Council on Aging, cognitive decline affects 11% of adults over 65, impairing their ability to activate help buttons during emergencies.

Additionally, design limitations in early-generation devices, such as bulky wearables, short battery life, and poor water resistance, have contributed to low adherence. In assisted living facilities, staff turnover and inadequate training further reduce system reliability. Without intuitive interfaces, continuous support, and destigmatized branding, even the most advanced PERS solutions face an uphill battle in achieving consistent, long-term user engagement.

MARKET OPPORTUNITIES

The integration of PERS with broader smart home and remote patient monitoring (RPM) ecosystems, enabling holistic health management, is a transformative opportunity. According to the Office of the National Coordinator for Health Information Technology, over 60% of RPM programs now include PERS data as part of care coordination for patients with chronic conditions. Companies like Amazon Halo and Google Nest are embedding emergency response features into voice-activated home hubs, allowing seniors to summon help via voice command.

A different key enabler is the expansion of PERS into non-elderly populations, including individuals with disabilities, mental health conditions, and post-surgical patients. The CDC estimates that 61 million U.S. adults live with a disability, many of whom face elevated risks of falls or medical emergencies at home. Startups like Bay Alarm Medical have launched specialized systems for epilepsy and cardiac patients with seizure detection and ECG integration. These expansions redefine PERS as a universal safety platform, unlocking new market segments and justifying broader insurance inclusion.

The advancement of AI-driven predictive analytics and machine learning to transition PERS from reactive to preventive care tools is another significant opportunity. According to the MIT AgeLab, behavioral sensors linked to PERS can detect subtle changes in gait, sleep patterns, and daily routines up to 14 days before a fall or health crisis. The National Institute of Biomedical Imaging and Bioengineering confirms that machine learning models can predict fall risk with over 80% accuracy by analyzing historical activity data.

Additionally, interoperability with electronic health records (EHRs) is enabling real-time clinical interventions. With CMS incentivizing preventive care under value-based models, AI-enhanced PERS systems are gaining traction as cost-effective tools for early intervention. These innovations position PERS not merely as emergency buttons, but as intelligent health surveillance platforms central to the future of decentralized care

SEGMENTAL ANALYSIS

By Type Insights

The Mobile-Based PERS segment dominated the market by capturing 47.4% of total PERS units deployed in 2024. This dominance is driven by the increasing mobility needs of aging populations and the limitations of fixed-location systems. According to the Centers for Disease Control and Prevention, a significant share of fall-related injuries among seniors occur outside the home, including in driveways, garages, and gardens, where landline-based systems offer no protection. As per the Federal Communications Commission, 74% of Americans aged 65+ now own smartphones, enabling seamless integration of GPS-enabled wearable devices with emergency monitoring services. A further key driver is the expansion of cellular network coverage and the adoption of LTE-M and 5G IoT connectivity, which support reliable real-time tracking. AT&T’s 2023 connectivity report confirms that its nationwide LTE-M network now covers 98% of the U.S. population, allowing mobile PERS devices to function across urban and rural areas. With Medicare Advantage plans increasingly covering mobile PERS, and seniors demanding freedom without compromising safety, this segment has become the standard for modern emergency response.

The Standalone PERS segment is emerging as the fastest-growing type and is projected to expand at a CAGR of 11.2% from 2025 to 2033. Unlike landline or mobile systems dependent on external infrastructure, standalone devices operate via private wireless networks or satellite connectivity, making them ideal for rural and off-grid locations. According to the National Rural Health Association, over 12 million seniors reside in rural areas where broadband penetration is below 60%, limiting the effectiveness of internet- or phone-dependent systems. Standalone units, such as those using LoRaWAN or mesh network technology, can transmit alerts directly to monitoring centers without reliance on home phone lines or cellular signals. A different critical factor is their resilience during natural disasters and power outages. These systems often include solar charging and multi-day battery backup, ensuring continuous operation. As climate-related disruptions increase, standalone PERS is gaining recognition as a critical component of disaster-resilient elder care.

By End-User Insights

The Home-Based Users segment commanded the PERS market by accounting for 64.2% of total system installations in 2024. This lead position is due to the overwhelming preference for aging in place, with nearly 89% of adults aged 65+ expressing a desire to remain in their own homes, according to the U.S. Census Bureau’s American Housing Survey. An additional major driver is the cost-effectiveness of home-based PERS compared to institutional care. Additionally, integration with smart home assistants, such as Amazon Alexa’s emergency calling feature, has enhanced usability. With family caregivers increasingly relying on remote monitoring tools, home-based PERS has become a cornerstone of independent living strategies across North America.

The Assisted Living Facilities segment is the fastest-growing end-user category, projected to grow at a CAGR of 9.8% from 2023 to 2030, according to the National Center for Assisted Living. This growth is driven by regulatory mandates and rising liability concerns in residential care settings. As per the U.S. Department of Health and Human Services, over 800,000 residents live in assisted living facilities, where fall rates are 50% higher than in private homes, as per the CDC’s National Center for Injury Prevention and Control. A further key factor is the integration of PERS into electronic health records and facility-wide monitoring systems. With increasing scrutiny on care quality and staffing ratios, operators are investing in scalable, centralized PERS platforms to enhance safety and operational compliance. As the assisted living population grows, projected to reach 1.2 million by 2030, this segment is becoming a high-priority deployment zone for advanced emergency response technologies..

REGIONAL ANALYSIS

The United States held the dominant position in the North American PERS Market by commanding a substantial share of regional revenue in 2024, as reported by the U.S. Department of Health and Human Services. The country’s position is underpinned by its large aging population, advanced healthcare infrastructure, and favorable reimbursement policies through Medicare Advantage plans. With 57 million Americans aged 65 and older, and one in four experiencing a fall annually, according to the Centers for Disease Control and Prevention, demand for emergency response systems is both urgent and sustained. The Centers for Medicare & Medicaid Services confirms that over 70% of Medicare Advantage plans now include PERS as a supplemental benefit, covering millions of beneficiaries. The Federal Communications Commission’s support for LTE-M networks has also enabled nationwide deployment of mobile PERS, ensuring coverage even in remote regions.

Canada is functioning as a progressive but smaller-scale adopter of PERS technologies. The country’s universal healthcare system does not directly fund PERS, but provincial home care programs and private insurers are increasingly integrating these systems. Statistics Canada reports that the senior population will reach 10.4 million by 2035, driving demand for aging-in-place solutions. The Canadian Institute for Health Information notes that falls are the leading cause of hospitalization among seniors, with over 80,000 admissions annually. Though adoption lags behind the U.S., Canada’s focus on integrated home care and digital health innovation positions it for accelerated growth in the coming decade.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Some of the prominent companies dominating the North American personal emergency response systems (PERS) market profiled in the report include ADT Corporation, Life Guardian Technologies LLC, Koninklijke Philips N.V., Tunstall Healthcare Group Ltd, Bay Alarm Medical Company, Philips Electronics V, Alert One Services LLC and Medical Guardian LLC.

The competitive landscape of the North America Personal Emergency Response Systems (PERS) Market is characterized by a mix of established medical device companies, security service providers, and agile health tech innovators vying for dominance in a rapidly evolving sector. Incumbents like Philips and ADT leverage brand trust, nationwide monitoring infrastructure, and payer partnerships to maintain leadership. Meanwhile, digital-first companies such as Bay Alarm Medical and MobileHelp differentiate through flexible pricing, advanced mobile connectivity, and AI-enhanced features. Competition is intensifying around product intelligence, ease of use, and integration with broader care ecosystems. Regulatory support, reimbursement expansion, and rising demand for aging-in-place solutions are driving innovation. However, fragmentation in coverage, technological disparities, and user adoption barriers create both challenges and opportunities. The market is shifting from basic emergency calling to proactive health monitoring, redefining PERS as a core component of decentralized, preventive care.

Top Players in the Market

Philips plays a pivotal role in the North America Personal Emergency Response Systems (PERS) Market through its Lifeline portfolio, which integrates advanced medical alert technologies with nationwide monitoring services. The company has strengthened its position by introducing AI-powered fall detection algorithms and GPS-enabled mobile devices that function seamlessly across urban and rural environments. It also launched voice-activated emergency calling through integration with Amazon Alexa, enhancing usability for users with limited mobility. Philips continues to invest in predictive analytics, leveraging real-world data to anticipate health events before they occur. While active in the Asia Pacific region through telehealth collaborations in Australia and Singapore, its core innovation and deployment remain centered on North American aging-in-place ecosystems.

ADT LLC has emerged as a dominant force in the PERS market by leveraging its national security infrastructure and brand recognition in home safety. The company offers a comprehensive PERS solution under its ADT Medical Alert brand, combining 24/7 professional monitoring with cellular and GPS technology for both in-home and mobile use. The company has also partnered with health systems like Banner Health to deploy PERS for high-risk patients transitioning from hospital to home. In the Asia Pacific region, ADT’s presence is limited to security services, with no significant PERS expansion; however, its North American model is being studied by smart city initiatives in Japan and South Korea for elderly safety applications.

Bay Alarm Medical is a key innovator in the PERS space, known for its flexible, no-contract subscription model and early adoption of LTE-based connectivity. The company offers a full suite of devices, including waterproof wearables, fall detection pendants, and smartphone-integrated apps, catering to tech-savvy seniors and caregivers. It also expanded its integration with electronic health records through partnerships with remote patient monitoring platforms. While primarily focused on the U.S. market, Bay Alarm has received interest from healthcare providers in Australia and New Zealand seeking scalable home-based emergency solutions. However, it has not yet established formal operations in the Asia Pacific region, maintaining a concentrated presence in North America.

Top Strategies Used by the Key Market Participants

Key players in the North America Personal Emergency Response Systems (PERS) Market are implementing strategies centered on technological integration, expansion of insurance and healthcare partnerships, enhancement of AI-driven predictive capabilities, deployment of mobile-first solutions, and seamless interoperability with telehealth and electronic health record systems. Companies are prioritizing user-centric design to improve adoption among seniors, incorporating voice activation, longer battery life, and automatic fall detection. Strategic alliances with Medicare Advantage plans and home health agencies are broadening access and reimbursement pathways. Investment in LTE-M and 5G IoT networks ensures reliable connectivity across diverse geographies. Additionally, firms are focusing on data security, HIPAA compliance, and caregiver engagement features to strengthen trust and retention in a highly sensitive health technology domain.

RECENT MARKET DEVELOPMENTS

- In March 2023, Philips launched its Voice-Activated PERS with Amazon Alexa integration, enabling seniors to summon emergency help using voice commands, a feature now deployed in over 200,000 U.S. households and improving accessibility for users with mobility or visual impairments.

-

In June 2023, ADT expanded its partnership with UnitedHealthcare to include ADT Medical Alert as a covered benefit in select Medicare Advantage plans, providing subsidized devices to over 150,000 beneficiaries across 12 states.

MARKET SEGMENTATION

This research report on the North American personal emergency response systems (PERS) market is segmented and sub-segmented into the following categories.

By Type

- Mobile Based

- Landline Based

- Standalone

By End-User

- Home-Based Users

- Senior Living Facilities

- Assisted Living Facilities

- Others.

By Country

- United States

- Canada

- Rest of North America

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com