North America Polypropylene Copolymer Market Size, Share, Trends & Growth Forecast Report By End-Use (Rigid Packaging, Textiles, Technical Parts, Films, Consumer Products, and Others), and Country (The United States, Canada and Rest of North America), Industry Analysis From 2026 to 2034

Market Size, 2025

$16.76 BnMarket Estimate, 2026

$17.28 BnMarket Forecast, 2034

$22.09 BnCAGR, 2026–2034

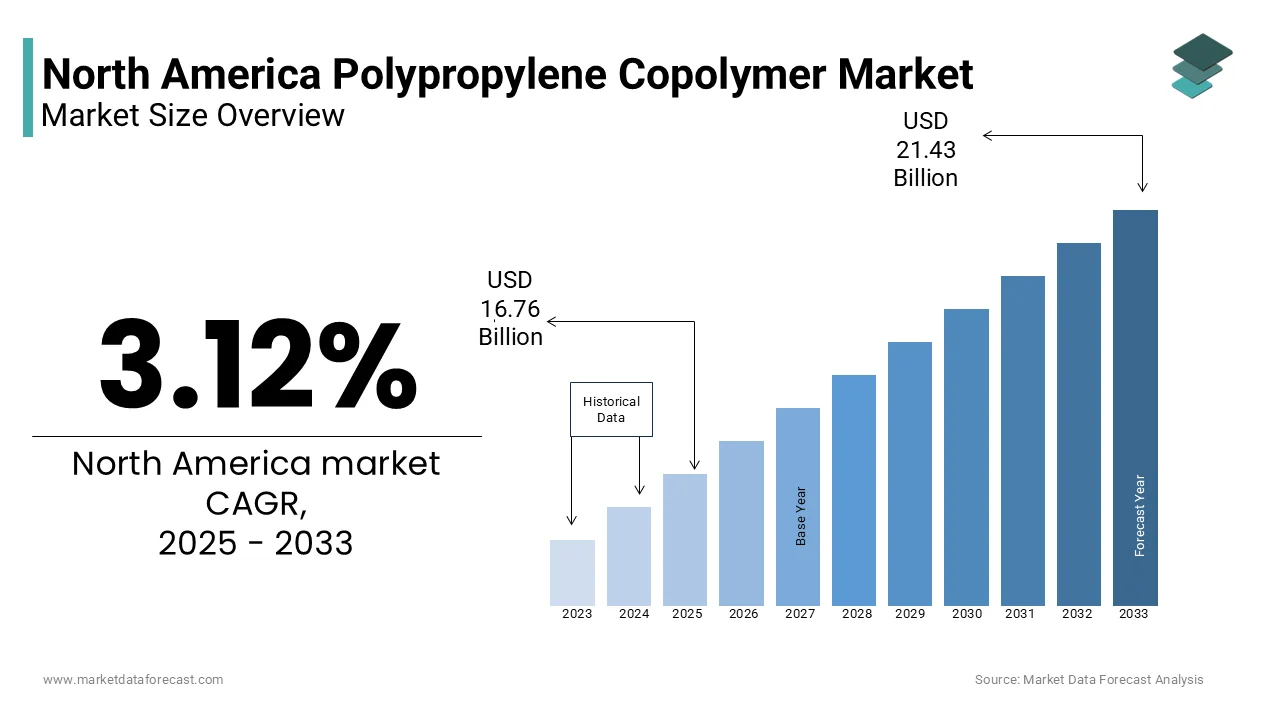

3.12%North America Polypropylene Copolymer (PPC) Market Report Summary

The North America polypropylene copolymer (PPC) market was valued at USD 16.76 billion in 2025, is estimated to reach USD 17.28 billion in 2026, and is projected to reach USD 22.09 billion by 2034, growing at a CAGR of 3.12% during the forecast period from 2026 to 2034. The growth of the North America polypropylene copolymer market is driven by increasing demand for lightweight and durable plastic materials across packaging, automotive, healthcare, and consumer goods industries. The superior impact resistance, flexibility, and chemical stability of polypropylene copolymers make them a preferred material for a wide range of industrial and commercial applications. Additionally, growing investments in sustainable packaging, advancements in polymer processing technologies, and rising demand for recyclable plastics are supporting market expansion across the region.

Key Market Trends

-

Rising demand for lightweight and recyclable plastic materials is driving the adoption of polypropylene copolymers across multiple industries.

-

Increasing use of polypropylene copolymers in rigid packaging applications is supporting market growth due to their durability and cost-effectiveness.

-

Growing automotive production is boosting demand for lightweight polymer components that improve fuel efficiency and vehicle performance.

-

Advancements in polymer processing technologies are enhancing product quality, impact resistance, and application versatility.

-

Increasing focus on sustainable packaging solutions and circular economy initiatives is encouraging the use of recyclable polypropylene materials.

Segmental Insights

-

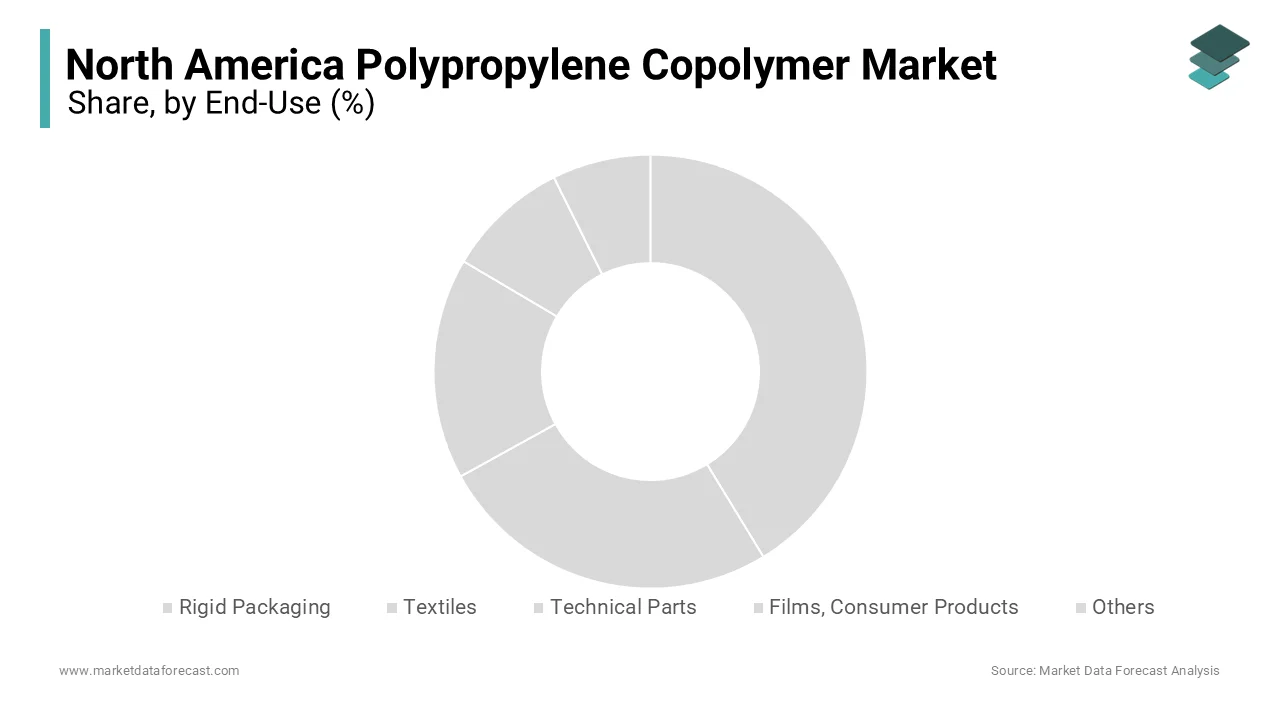

Based on end use, the rigid packaging segment dominated the North America polypropylene copolymer market by accounting for 40.3% of the market share in 2025. The segment's leadership is attributed to the increasing demand for durable, lightweight, and recyclable packaging solutions across the food and beverage, healthcare, and consumer goods industries.

Regional Insights

-

The North America polypropylene copolymer market is witnessing steady growth due to expanding packaging applications, increasing industrial manufacturing, and growing demand for high-performance polymer materials.

-

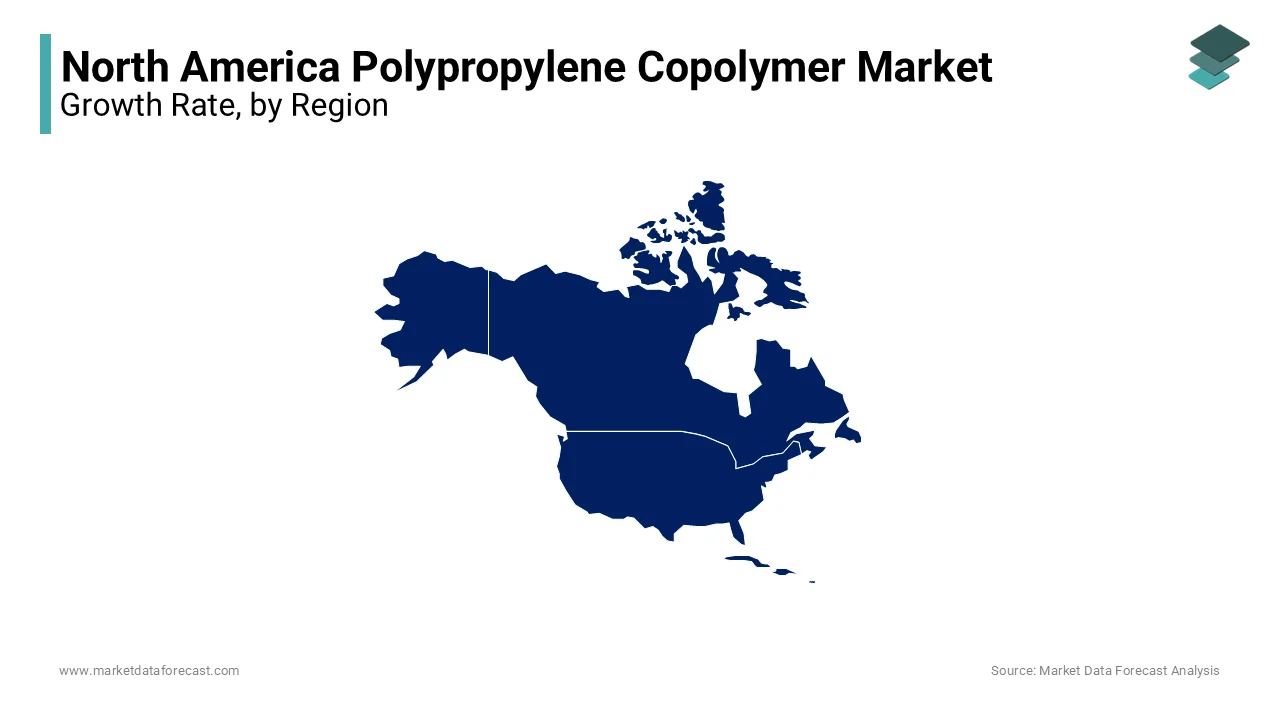

The United States dominated the North America polypropylene copolymer market by accounting for 70.4% of the regional market share in 2025. The country's leadership is supported by its well-established petrochemical industry, strong packaging and automotive sectors, advanced manufacturing capabilities, and increasing investments in sustainable polymer production.

Competitive Landscape

The North America polypropylene copolymer market is moderately competitive, with manufacturers focusing on product innovation, sustainable polymer solutions, and production capacity expansion to strengthen their market positions. Companies are investing in advanced polymer technologies, strategic collaborations, and recyclable material development to meet the growing demand from packaging, automotive, healthcare, and industrial applications. Key players operating in the North America polypropylene copolymer market include LyondellBasell Industries N.V., ExxonMobil Chemical, Braskem S.A., and Total Petrochemicals & Refining USA, Inc.

North America Polypropylene Copolymer Market Size

The North America polypropylene copolymer (PPC) market size was valued at USD 16.76 billion in 2025 and is predicted to be worth USD 22.09 billion by 2034 from USD 17.28 billion in 2026, growing at a CAGR of 3.12% from 2026 to 2034.

MARKET DRIVERS

Rising Demand for Rigid Packaging Solutions

The growing demand for rigid packaging solutions is a pivotal driver of the North American polypropylene copolymer (PPC) market. Industries such as food and beverage, pharmaceuticals, and household goods rely heavily on PPC-based containers and caps to ensure product safety and shelf life. For instance, Nestlé announced in 2023 that it aims to transition 100% of its packaging to recyclable or reusable materials by 2026 by creating significant opportunities for PPC manufacturers. Furthermore, the rise of e-commerce has amplified demand for durable yet lightweight packaging solutions.

Increasing Adoption in Automotive Applications

The increasing adoption of polypropylene copolymers in automotive applications is another major driver of the North American market. According to the Center for Automotive Research, reducing vehicle weight by 10% can improve fuel efficiency by up to 6-8% by making PPC an indispensable material for modern vehicle designs. In 2022, the U.S. automotive sector consumed over 4 million metric tons of PPC, as reported by the American Chemistry Council. This surge is attributed to the integration of PPC in components such as bumpers, dashboards, and interior trims, which offer superior strength-to-weight ratios compared to traditional materials. The rise of electric vehicles (EVs) has further accelerated this trend, with EV manufacturers prioritizing lightweight components to extend battery range.

MARKET RESTRAINTS

Volatility in Crude Oil Prices

Fluctuations in crude oil prices pose a significant challenge to the North American polypropylene copolymer (PPC) market, as PPC production is heavily reliant on petrochemical feedstocks. Since PPC is derived from propylene, a byproduct of crude oil refining, these price swings directly impact production costs and profit margins. Such volatility forces companies to pass on additional costs to end-users that is ascribed to hinder the growth of the market. Smaller players often struggle to absorb these price shocks. The unpredictability of raw material costs remains a persistent barrier to consistent growth in the PPC market.

Stringent Environmental Regulations

Stringent environmental regulations targeting plastic waste and emissions are increasingly constraining the North American PPC market. According to the National Oceanic and Atmospheric Administration, plastic waste accounts for over 80% of marine debris in North America by prompting governments to implement stricter policies. Canada’s Single-Use Plastics Prohibition Regulations, effective from December 2022, ban the manufacture and import of certain plastic products, which is impacting demand for traditional PPC-based materials. Similarly, California’s extended producer responsibility laws require manufacturers to manage the lifecycle of plastic products, adding compliance costs. A study by Deloitte estimates that regulatory compliance expenses for the plastics industry could rise by 15% annually over the next decade. They impose operational challenges and necessitate significant investments in R&D for alternative materials while these measures aim to promote sustainability.

MARKET OPPORTUNITIES

Expansion of Recycled PPC Applications

The growing emphasis on circular economy principles presents a lucrative opportunity for the North American PPC market. Innovations in mechanical and chemical recycling technologies are enabling the production of high-quality compounds suitable for diverse industries. For instance, Adidas announced in 2023 that it aims to use 100% recycled polyester in its products by 2026, which is creating a ripple effect across the supply chain. Furthermore, the Recycling Partnership estimates that investing in recycling infrastructure could quadruple the current recycling rate by 2030.

Growth in Technical Parts and Components

The advent of advanced technical parts and components represents another promising avenue for the PPC market. North America leads this trend, with industries such as aerospace, defense, and electronics adopting PPC-based components for their thermal stability and chemical resistance. For example, Boeing partnered with Solvay in 2023 to integrate PPC-based composites into aircraft interiors, which is enhancing durability and performance. Additionally, the rise of smart devices has spurred demand for high-performance PPC materials, benefiting the compounding industry.

MARKET CHALLENGES

Supply Chain Disruptions

Supply chain disruptions remain a critical challenge for the North American PPC market. The reliance on imported raw materials, such as propylene and additives, exposes the industry to geopolitical risks and transportation constraints. For instance, port congestion at major hubs like Los Angeles and Long Beach delayed shipments by an average of 10 days during peak periods, as noted by the Journal of Commerce. These disruptions not only inflate costs but also hinder timely product delivery, eroding customer trust. Smaller players are lacking the resources to diversify suppliers or invest in logistics optimization, which face disproportionate impacts. Addressing these vulnerabilities requires strategic investments in local sourcing and digital supply chain solutions.

Public Perception of Plastics

Public perception of plastics as environmentally harmful continues to challenge the PPC market. A survey conducted by Pew Research Center revealed that 72% of Americans view plastic pollution as a major environmental issue, influencing purchasing decisions and policy advocacy. This sentiment fuels corporate commitments to reduce plastic usage, such as Coca-Cola’s pledge to collect and recycle the equivalent of every bottle it sells by 2030. However, such initiatives inadvertently suppress demand for PPC, forcing manufacturers to innovate rapidly. Additionally, misinformation about the recyclability of certain plastics complicates efforts to promote sustainable alternatives. For example, Greenpeace’s 2023 report criticized the efficacy of chemical recycling by casting doubt on its viability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.82% |

| Segments Covered | By End-Use, and Region |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | The United States, Canada, Mexico, and Rest of North America |

| Market Leaders Profiled | LyondellBasell Industries N.V., ExxonMobil Chemical, BASF SE, Braskem S.A., SABIC, and Total Petrochemicals & Refining USA, Inc. |

SEGMENTAL ANALYSIS

By End-Use Insights

The Rigid packaging segment dominated the North American PPC market with 40.3% of share in 2025. The growth of the segment is attributed due to its widespread use in industries such as food and beverage, pharmaceuticals, and household goods, where durability and cost-effectiveness are paramount. PPC-based containers and caps are favored for their excellent chemical resistance and lightweight properties, making them ideal for mass production. The U.S., being a major hub for consumer goods manufacturing, benefits from abundant raw material availability by reducing production costs. Furthermore, advancements in polymer science have enhanced the performance characteristics of PPC by enabling its application in high-performance sectors like healthcare.

Technical parts segment is likely to experience a CAGR of 6.2% from 2026 to 2034. This growth is fueled by increasing demand for durable and lightweight materials in industries such as aerospace, defense, and electronics. Additionally, the rise of smart devices has spurred demand for high-performance PPC materials by benefiting the compounding industry.

REGIONAL ANALYSIS

The United States polypropylene copolymer (PPC) market was the largest by capturing 70.4% of the share in 2025 with a robust industrial ecosystem, technological leadership, and favorable regulatory frameworks that support manufacturing activities. This abundant supply of raw materials ensures cost competitiveness and scalability for PPC manufacturers. The automotive sector, concentrated in states like Michigan, Ohio, and Indiana, drives significant demand for PPC-based lightweight components, which are critical for improving fuel efficiency and meeting stringent emissions standards. Additionally, the rise of e-commerce has amplified demand for rigid packaging solutions, with PPC being a preferred material due to its durability and cost-effectiveness. Investments in recycling infrastructure, such as Loop Industries’ partnership with Suez, further bolster the market by aligning with sustainability goals. Government incentives for sustainable practices, such as tax credits for bio-based products, encourage innovation and adoption of eco-friendly PPC formulations.

Canada was accounted in holding 16.1% of the North American PPC market share in 2025. According to Environment and Climate Change Canada, the country has set ambitious targets to achieve zero plastic waste by 2030 by fostering demand for recycled and bio-based PPC materials. Ontario and Quebec serve as key manufacturing hubs by hosting facilities operated by multinational companies like Nova Chemicals and Dow Chemical. These regions benefit from proximity to major automotive OEMs, including Toyota and Honda, which utilize PPC-based components for lightweighting and durability. Canada’s commitment to renewable energy further supports the development of bio-based PPC, as evidenced by BioAmber’s expansion of succinic acid production facilities, which provide feedstock for bioplastics. The Canadian government’s National Research Council funds R&D initiatives aimed at advancing sustainable PPC technologies by enabling local players to compete globally.

COMPETITIVE LANDSCAPE

The North American PPC market is characterized by intense competition, driven by the presence of global giants, regional players, and niche innovators vying for market share. Companies like LyondellBasell, BASF, and SABIC dominate the landscape, leveraging their technological expertise, extensive distribution networks, and economies of scale to maintain leadership positions. These firms invest heavily in R&D to develop advanced materials that cater to evolving industry needs, such as lightweighting, electrification, and sustainability.

Smaller players, on the other hand, focus on specialized segments, such as bio-based and recycled PPC, to carve out a competitive edge. Their agility and ability to respond quickly to market trends allow them to capture niche opportunities that larger companies may overlook. For instance, startups like BioAmber and NatureWorks are pioneering the development of bioplastics derived from renewable resources by gaining traction among environmentally conscious consumers.

The market is witnessing increased consolidation, with mergers and acquisitions driving economies of scale and expanding product portfolios. Regulatory pressures and consumer demand for sustainable solutions are reshaping competitive dynamics, compelling companies to adopt circular economy principles and invest in recycling technologies. Innovation remains a key differentiator, with companies striving to develop cutting-edge materials that meet stringent performance and environmental standards.

Additionally, collaborations and partnerships are becoming more prevalent, enabling companies to pool resources and expertise to address complex challenges. For example, LyondellBasell’s partnership with Karo Recycling and BASF’s collaboration with Quantafuel highlight the growing importance of joint ventures in driving innovation and achieving sustainability goals. These trends underscore the dynamic nature of the North American PPC market, where competition is fierce but opportunities abound for those who can adapt and innovate.

KEY MARKET PLAYERS

Some of the key players in the North America polypropylene copolymer (PPC) market are

-

LyondellBasell Industries N.V.

-

ExxonMobil Chemical

-

BASF SE

-

Braskem S.A.

-

SABIC

-

Total Petrochemicals & Refining USA, Inc.

TOP PLAYERS IN THE MARKET

- LyondellBasell is a global powerhouse in the polypropylene copolymer (PPC) market, contributing significantly to North America’s industrial landscape. The company specializes in producing high-performance polyolefins and engineered plastics, serving industries such as automotive, packaging, and consumer goods. Its proprietary Catalloy process enables the production of advanced PPC compounds with superior impact resistance and flexibility by making them ideal for demanding applications. LyondellBasell is also a pioneer in sustainability by launching initiatives to produce 2 million metric tons of recycled and renewable-based polymers annually by 2030.

- BASF SE is another key player in the North American PPC market that renowned for its innovative product portfolio and commitment to sustainability. These high-performance thermoplastics are widely used in automotive and electronics applications due to their excellent mechanical properties and thermal stability. BASF is investing heavily in circular economy initiatives by collaborating with partners like Quantafuel to advance chemical recycling technologies.

- SABIC is a prominent player in the North American PPC market by offering a diverse range of high-performance materials tailored to meet industry needs. SABIC’s expertise in engineering thermoplastics positions it as a preferred supplier for aerospace, defense, and automotive applications. The company is also advancing its sustainability agenda by targeting a 25% reduction in carbon emissions by 2030. SABIC’s TRUCIRCLE initiative promotes the use of certified circular polymers, reinforcing its commitment to environmental stewardship. In addition, SABIC’s recent expansion of its compounding plant in Ohio underscores its focus on enhancing production capacity and meeting growing demand for advanced materials.

TOP STRATEGIES USED BY KEY PLAYERS

Key players in the North American PPC market employ a variety of strategies to maintain their competitive edge and capitalize on emerging opportunities. Mergers and acquisitions are a common tactic, allowing companies to expand their product portfolios and geographic reach. For instance, LyondellBasell’s acquisition of A.

Investments in research and development (R&D) are another critical strategy, with companies focusing on innovation to address evolving market demands. BASF’s ChemCycling project exemplifies this approach, as it seeks to convert plastic waste into valuable feedstock for new compounds. SABIC’s TRUCIRCLE initiative by promoting the use of certified circular polymers to meet sustainability goals.

Collaborations and partnerships are also prevalent, enabling companies to leverage complementary strengths and accelerate growth. For example, LyondellBasell partnered with Karo Recycling in 2023 to establish a mechanical recycling facility in Texas, enhancing its recycled polymer offerings. BASF collaborated with Quantafuel to advance chemical recycling technologies, while SABIC worked closely with OEMs to develop customized solutions for specific applications.

Expanding production capacity is another key strategy, with companies investing in new facilities to meet rising demand. SABIC’s recent expansion of its Ohio compounding plant highlights this trend, as does Dow Chemical’s introduction of a circular polymer platform aimed at recycling 1 million metric tons of plastic waste annually by 2030. These strategies collectively enable companies to differentiate themselves, drive innovation, and strengthen their market positions.

RECENT HAPPENINGS IN THE MARKET

- In April 2023, LyondellBasell partnered with Karo Recycling to establish a state-of-the-art mechanical recycling facility in Texas. This initiative aims to enhance the company’s recycled polymer offerings by aligning with its goal to produce 2 million metric tons of recycled and renewable-based polymers annually by 2030.

- In June 2023, BASF launched a new line of bio-based polyamides designed specifically for the automotive and electronics sectors. These materials are derived from renewable feedstocks and offer superior mechanical properties by addressing growing demand for sustainable alternatives.

- In August 2023, SABIC opened a new compounding plant in Ohio, expanding its production capacity for high-performance thermoplastics. This facility will cater to the aerospace, defense, and automotive industries by reinforcing SABIC’s position as a leader in advanced materials.

- In October 2023, Covestro acquired ResinTec , a leading provider of recycled plastic compounds. This acquisition strengthens Covestro’s portfolio of sustainable materials and enhances its ability to meet customer demand for eco-friendly solutions.

- In December 2023, Dow Chemical introduced a circular polymer platform aimed at recycling 1 million metric tons of plastic waste annually by 2030. This initiative underscores Dow’s commitment to sustainability and positions it as a frontrunner in the transition to a circular economy.

MARKET SEGMENTATION

This research report on the North America polypropylene copolymer market has been segmented and sub-segmented based on the following categories.

By End-Use

- Rigid Packaging

- Textiles

- Technical Parts

- Films, Consumer Products

- Others

By Country

- The United States

- Canada

- Rest of North America

Frequently Asked Questions

1. What is driving the North America Polypropylene Copolymer Market growth?

The market is driven by rising demand from the packaging, automotive, healthcare, and consumer goods industries, along with increasing demand for lightweight, durable, and recyclable polymer materials.

2. What is the forecast for the North America Polypropylene Copolymer Market?

The market is expected to grow steadily during the forecast period, supported by expanding industrial applications, technological advancements, and increasing investments in sustainable polymer production.

3. What are the key trends in the North America Polypropylene Copolymer Market?

Major trends include the development of recyclable polypropylene grades, bio-based polymers, lightweight automotive components, advanced polymer processing, and sustainable packaging solutions.

4. What opportunities exist in the North America Polypropylene Copolymer Market?

Opportunities are emerging from the growing adoption of electric vehicles, increasing demand for eco-friendly packaging, expansion of healthcare applications, and investments in circular economy initiatives.

5. What challenges affect the North America Polypropylene Copolymer Market?

The market faces challenges such as fluctuating raw material prices, environmental concerns over plastic waste, stringent regulations, and competition from alternative materials.

6. Which country leads the North America Polypropylene Copolymer Market?

The United States leads the market due to its strong petrochemical industry, large manufacturing base, high polymer production capacity, and robust demand from key end-use sectors.

7. Which industry drives demand for polypropylene copolymers in North America?

The packaging industry is the largest consumer of polypropylene copolymers, followed by the automotive, healthcare, consumer goods, and construction industries.

8. How is the packaging industry boosting the polypropylene copolymer market?

The packaging industry increases demand by using polypropylene copolymers in food containers, flexible packaging, rigid packaging, and other lightweight, durable, and recyclable packaging products.

9. What factors are restraining the North America Polypropylene Copolymer Market?

Growth is restrained by volatile feedstock prices, stricter environmental regulations, recycling challenges, and increasing adoption of biodegradable alternatives.

10. Who are the major players in the North America Polypropylene Copolymer Market?

Leading companies focus on expanding production capacity, developing high-performance polypropylene copolymers, investing in sustainable materials, and strengthening their regional market presence.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com