North America Rare Sugar Market Size, Share, Trends & Growth Forecast Report By Product (D-Mannose, Allulose, Tagatose, D-Xylose, L-Arabinose, L-Fucose), By Application, and Country (The United States, Canada and Rest of North America), Industry Analysis From 2025 to 2033

North America Rare Sugars Market Size

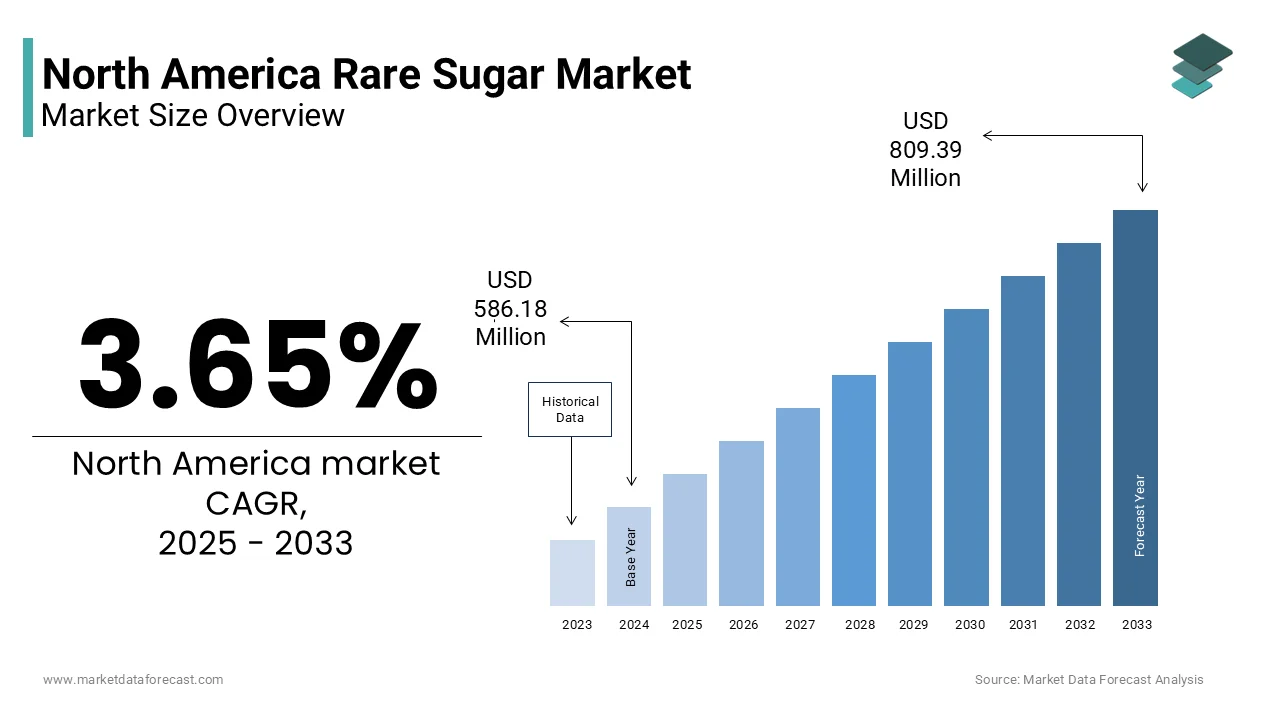

The Rare sugars market size in North America was valued at USD 586.18 million in 2024 and is predicted to be worth USD 809.39 million by 2033 from USD 607.58 million in 2025 and grow at a CAGR of 3.65% from 2025 to 2033.

The rare sugars offer reduced caloric content while maintaining similar taste profiles, which is making them increasingly attractive for use in food, beverages, dietary supplements, and pharmaceuticals. In recent years, growing consumer awareness around health and wellness has driven interest in alternative sweeteners that do not compromise on taste or texture. Moreover, scientific research institutions like the U.S. Department of Agriculture (USDA) have been exploring the metabolic benefits of certain rare sugars, particularly allulose, which has shown potential in regulating blood glucose levels and reducing fat accumulation. Additionally, rising investments by ingredient manufacturers in scalable enzymatic conversion technologies are enhancing the feasibility of large-scale rare sugar production.

MARKET DRIVERS

Rising Demand for Low-Calorie Natural Sweeteners

The increasing consumer preference for natural, low-calorie sweeteners as an alternative to artificial options and high-calorie carbohydrates is fuelling the growth of the North America rare sugar market. According to the National Institutes of Health (NIH), obesity rates in the U.S. have continued to rise, with over 40% of adults classified as obese in 2023. This has prompted a shift toward healthier dietary choices in beverages, snacks, and processed foods. Rare sugars such as allulose and tagatose offer sweetness levels comparable to sucrose but with significantly fewer calories and minimal impact on blood glucose. Food and beverage companies have responded swiftly to this demand. Major players like PepsiCo, Nestlé, and The Coca-Cola Company have introduced product lines featuring rare sugars in their formulations, capitalizing on the growing clean-label movement.

Advancements in Production Technologies and Enzymatic Conversion Methods

The rapid advancement in biotechnological methods that enable cost-effective and scalable production of rare sugars is escalating the growth of the North America rare sugar market. Traditional extraction methods were inefficient due to the scarcity of these sugars in nature. However, breakthroughs in enzymatic isomerization and microbial fermentation have transformed production capabilities. According to the U.S. Department of Agriculture (USDA), research conducted at its Agricultural Research Service (ARS) has led to the development of efficient enzyme-based conversion techniques that convert abundant sugars like fructose into rare variants such as allulose with high yields. Companies such as Tate & Lyle and Matsutani Chemical Industry Co., Ltd. have leveraged these advancements to scale up industrial production, reducing costs and improving supply chain reliability. Furthermore, academic institutions like the University of California, Davis, and industry consortia are investing in fermentation-based processes to produce rare sugars using renewable feedstocks. These developments are not only enhancing economic viability but also aligning with sustainability goals, which is further supporting market expansion across North America.

MARKET RESTRAINTS

High Production Costs and Limited Economies of Scale

The relatively high production cost associated with their synthesis is limiting the growth of the North America rare sugar market. Unlike conventional sweeteners derived from corn or sugarcane, rare sugars require complex enzymatic or microbial conversion processes that are still in early stages of industrial optimization. According to the Biotechnology Innovation Organization (BIO), current manufacturing techniques for rare sugars such as allulose and tagatose involve multi-step biochemical transformations that increase energy consumption and processing time. This results in higher per-unit production expenses compared to widely available alternatives like stevia or erythritol. Additionally, limited economies of scale hinder widespread adoption. While ongoing R&D efforts aim to improve yield rates and streamline production workflows, the current financial burden on manufacturers limits the affordability of rare sugar-based products for mass-market consumers.

Regulatory Uncertainty and Labeling Ambiguities

The regulatory ambiguity surrounding the classification and labeling of rare sugars is another factor to hinder the growth of the North America rare sugar market. Although the FDA granted favorable treatment to allulose by excluding it from total and added sugars on nutrition facts panels, other rare sugars remain subject to inconsistent guidelines. As per the Center for Science in the Public Interest (CSPI), there is an ongoing debate regarding how rare sugars should be categorized in terms of digestibility, caloric value, and metabolic impact. Moreover, some consumer advocacy groups argue that the current labeling exemptions may mislead buyers about the overall nutritional content of products containing rare sugars.

MARKET OPPORTUNITIES

Expansion in Functional Foods and Dietary Supplements

The expanding functional foods and dietary supplements sector is creating new opportunities in the next coming years. Consumers are increasingly seeking products that deliver health benefits beyond basic nutrition, including improved digestion, weight management, and enhanced immunity. According to the Council for Responsible Nutrition (CRN), over 75% of U.S. adults take dietary supplements regularly, with demand growing for formulations that incorporate natural, low-calorie ingredients. Pharmaceutical and nutraceutical companies are leveraging these attributes to develop innovative products ranging from prebiotic blends to sports nutrition bars and protein shakes. Startups and established brands alike are exploring rare sugar applications in probiotic beverages and functional confectionery items designed for diabetic and fitness-focused consumers. Additionally, clinical studies published by institutions like the Harvard T.H. Chan School of Public Health have linked certain rare sugars to anti-inflammatory and antioxidant effects, which is further validating their role in preventive healthcare.

Integration into Plant-Based and Alternative Protein Products

The integration of advanced system into plant-based and alternative protein products is solely to propel the growth of the North America rare sugar market. According to the Good Food Institute (GFI), the plant-based food market in the U.S. reached $8.3 billion in retail sales in 2024, with alternative proteins accounting for a significant share. However, many of these products struggle with off-flavors, excessive browning during cooking, or undesirable textures, prompting manufacturers to explore novel ingredient solutions. Rare sugars such as erythritose and ribose have demonstrated unique Maillard reaction properties that help mimic the flavor development of traditional animal-based proteins. Moreover, their moisture-retention capabilities aid in improving the juiciness and tenderness of plant-based meats. Companies like Beyond Meat and Impossible Foods are actively researching ways to incorporate rare sugars into their formulations to optimize sensory attributes. Meanwhile, startups specializing in fermentation-derived ingredients are developing customized rare sugar blends tailored for clean-label, high-protein diets.

MARKET CHALLENGES

Limited Consumer Awareness and Understanding

The limited awareness and understanding among consumers regarding the benefits and functionalities of rare sugars is restricting the growth of the North America rare sugar market. While terms like “allulose” and “tagatose” are becoming more common in ingredient lists, many consumers remain unfamiliar with what these substances are and how they differ from traditional sweeteners or artificial alternatives. According to a survey conducted by the International Food Information Council (IFIC), less than 30% of respondents could correctly identify allulose as a naturally occurring sugar substitute with minimal caloric impact. Manufacturers and trade associations are working to address this issue through educational campaigns and clearer labeling practices. However, misinformation spread via social media and influencer-driven content sometimes exacerbates confusion rather than clarifying it.

Supply Chain Constraints and Feedstock Availability

The dependency on stable supply chains and availability of raw materials used in their production is also hampering the growth of the North America rare sugar market. While enzymatic conversion and microbial fermentation have enabled scalable synthesis, these processes rely heavily on consistent supplies of base sugars such as fructose and lactose, which are sourced from agricultural commodities. According to the U.S. Department of Agriculture (USDA), fluctuations in crop yields due to climate variability, geopolitical tensions, and trade policies can disrupt the availability and pricing of feedstocks essential for rare sugar manufacturing. Moreover, the reliance on specialized enzymes and fermentation strains adds another layer of complexity to production logistics. Companies must navigate sourcing constraints related to patented biocatalysts and maintain strict quality control protocols to ensure consistency in output.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 3.65% |

| Segments Covered | By Product, Application, and Region |

|

Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | The United States, Canada, Mexico, and Rest of North America |

| Market Leaders Profiled | Douglas Laboratories, Tate & Lyle, The Sanwa Starch Co., Ltd., DuPont de Nemours, Inc., Nutraceuticals Group USA, Samyang Corporation, Matsutani Chemical Industry Co., Ltd., Bonumose, Ingredion Incorporated, and Sweet Cures, and others |

SEGMENTAL ANALYSIS

By Product Insights

The allulose segment held 38.2% of the North America rare sugar market share in 2024 with its widespread adoption across food and beverage applications due to its near-identical taste and texture to sucrose while offering negligible caloric impact. Additionally, clinical studies supported by the USDA have demonstrated that allulose may help regulate postprandial blood glucose levels and support weight management, further enhancing its appeal in dietary supplements and functional foods. Major food companies such as Tate & Lyle, Cargill, and Ingredion have scaled up production capabilities, reducing costs and improving supply chain efficiency.

The tagatose segment is expected to grow with a CAGR of 14.7% in the next coming years with the increasing scientific recognition of its prebiotic properties and glycemic control benefits. According to research published by the Journal of Nutrition and Metabolism, tagatose has demonstrated potential in promoting gut microbiota balance and enhancing insulin sensitivity, making it a promising ingredient for metabolic health products. Moreover, tagatose’s ability to function as both a sweetener and a texturizing agent makes it ideal for use in low-sugar dairy alternatives, baked goods, and confections. Companies like Beneo and Matsutani Chemical have expanded their commercial offerings to include tagatose-based formulations tailored for clean-label and keto-friendly markets.

By Application Insights

The food & beverages segment was accounted in holding 45.3% of the North America rare sugar market share in 2024 with the rising demand for low-calorie sweeteners in packaged foods, beverages, and bakery items. Consumers are increasingly seeking healthier alternatives without compromising on taste or texture by making rare sugars like allulose and tagatose ideal replacements for traditional sweeteners.

According to the International Food Information Council (IFIC), over 60% of U.S. consumers actively seek out products labeled as “no added sugar” or “low calorie,” directly influencing formulation strategies among major food and beverage manufacturers. Companies such as PepsiCo, Nestlé, and Furthermore, regulatory support from the FDA, which allows allulose to be excluded from total and added sugar labeling, has encouraged broader industry adoption.

The pharmaceuticals is projected to grow with a CAGR of 13.2% from 2025 to 2033. According to the National Institutes of Health (NIH), several rare sugars including D-mannose, tagatose, and L-fucose are showing promise in modulating immune responses, regulating glucose metabolism, and supporting mucosal health. Clinical trials conducted by academic institutions and biotech firms have demonstrated positive outcomes in metabolic syndrome and inflammatory bowel disease treatment protocols using rare sugar derivatives. In response, pharmaceutical companies are exploring their integration into drug delivery systems, excipients, and active pharmaceutical ingredients (APIs). Startups specializing in biopharmaceutical ingredients, such as Carbosynth and Elicityl, are partnering with contract development and manufacturing organizations (CDMOs) to scale up production for medicinal applications. Moreover, regulatory agencies such as the U.S. Pharmacopeia (USP) are updating monographs to include standardized specifications for rare sugars used in pharmaceutical formulations, facilitating wider acceptance in the sector.

REGIONAL ANALYSIS

United States

The United States was the top performer in the North America rare sugar market with 82.3% of share in 2024 with the strong demand from the food and beverage sector, robust R&D initiatives, and a well-established regulatory framework that supports the commercialization of novel sweeteners. According to the U.S. Department of Agriculture (USDA), the country leads globally in the development and industrial-scale production of rare sugars, particularly allulose and tagatose, through advanced enzymatic conversion techniques. Major ingredient suppliers such as Tate & Lyle, Cargill, and Ingredion have significantly expanded their production capacities to meet growing demand from food manufacturers aiming to reduce sugar content in packaged goods. Moreover, the FDA's decision to exclude allulose from total and added sugar counts on nutrition labels has spurred its adoption in a wide range of products, including soft drinks, snack bars, and sports nutrition beverages.

Canada

Canada was positioned second by holding 13.2% of the North America rare sugar market share in 2024. As per Statistics Canada, the country’s food and beverage industry has been actively adopting low-calorie sweeteners in response to shifting consumer preferences toward reduced-sugar options. The Canadian Sugar Institute reports that in 2024, more than 40% of new product launches in the functional food category included rare sugars as key ingredients. Health Canada has taken steps to reassess nutritional guidelines and update labeling regulations by encouraging manufacturers to explore alternative sweeteners that align with public health goals. Additionally, academic institutions such as the University of Toronto and McGill University are conducting research on the metabolic effects of rare sugars, contributing to growing scientific validation.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Douglas Laboratories, Tate & Lyle, The Sanwa Starch Co., Ltd., DuPont de Nemours, Inc., Nutraceuticals Group USA, Samyang Corporation, Matsutani Chemical Industry Co., Ltd., Bonumose, Ingredion Incorporated, and Sweet Cures are the key players in the North America rare sugar market.

The competition in the North America rare sugar market is characterized by rapid technological advancements, growing consumer awareness, and increasing demand from the food, pharmaceutical, and dietary supplement sectors. Established ingredient suppliers, emerging biotech firms, and research-driven startups are actively vying for market share, each bringing unique capabilities in production, formulation, and regulatory expertise.

Brand positioning is becoming increasingly important as companies seek to differentiate themselves based on purity, functionality, and sustainability credentials. While large-scale manufacturers leverage economies of scale and extensive distribution networks, niche players focus on specialized applications such as medical nutrition and precision fermentation-derived ingredients.

Regulatory developments and labeling policies continue to shape competitive dynamics, influencing how products are marketed and accepted by consumers. Additionally, supply chain reliability and feedstock availability play a role in determining which companies can consistently deliver high-quality rare sugars at competitive prices.

TOP PLAYERS IN THE MARKET

Tate & Lyle PLC

One of the leading players in the North America rare sugar market is Tate & Lyle PLC, a global supplier of specialty food ingredients. The company has been instrumental in scaling up allulose production using advanced enzymatic conversion technologies, which is making it more accessible to food and beverage manufacturers seeking reduced-sugar alternatives without compromising taste or texture.

Cargill Incorporated

Another key player is Cargill Incorporated is a major agribusiness and food ingredient provider with a strong presence in the alternative sweetener space. Cargill has invested heavily in fermentation-based rare sugar development, focusing on scalable solutions that support clean-label product formulations across various consumer segments.

Ingredion Incorporated

Ingredion Incorporated also plays a pivotal role in shaping the rare sugar landscape. Known for its portfolio of functional sweeteners and starches, Ingredion has expanded into rare sugars through strategic partnerships and internal R&D initiatives aimed at offering natural, low-calorie options tailored for dietary supplements, pharmaceuticals, and metabolic health products.

TOP STRATEGIES USED BY KEY PLAYERS

A primary strategy employed by key players in the North America rare sugar market is intensive investment in biotechnological innovation to improve production efficiency and yield. Companies are leveraging enzyme engineering and microbial fermentation to enhance scalability and reduce manufacturing costs, enabling broader commercial viability.

Another strategy is expanding partnerships with downstream industries by including food and beverage giants, pharmaceutical firms, and dietary supplement brands. These collaborations help integrate rare sugars into mainstream product lines while aligning formulation strategies with evolving consumer health trends

RECENT HAPPENINGS IN THE MARKET

- In February 2024, Tate & Lyle announced a strategic partnership with a U.S.-based biotechnology firm to develop next-generation enzymatic processes for rare sugar synthesis, which is aiming to enhance production efficiency and reduce environmental impact.

- In May 2024, Cargill launched an expanded line of rare sugar-based sweetener blends tailored for use in low-sugar beverages and dairy alternatives by targeting health-conscious consumers and expanding its presence in the functional food sector.

- In August 2024, Ingredion introduced a new branded platform dedicated to rare sugars, which is designed to support food manufacturers in reformulating products with minimal caloric impact while maintaining sensory appeal and nutritional integrity.

- In October 2024, Beneo GmbH opened a North American innovation center focused on rare sugar applications in sports nutrition, infant formula, and gut health products by strengthening its regional footprint and technical support services.

- In December 2024, Matsutani Chemical Industry Co., Ltd. entered into a joint venture with a U.S. contract manufacturer to locally produce and distribute tagatose-based ingredients, which is improving supply chain responsiveness and supporting growing demand across the continent.

MARKET SEGMENTATION

This research report on the North America rare sugar market has been segmented and sub-segmented based on the following categories.

By Product

- D-Mannose

- Allulose

- Tagatose

- D-Xylose

- L-Arabinose

- L-Fucose

By Application

- Dietary supplements

- Cosmetics & Personal care

- Pharmaceuticals

- Food & Beverages

- Others

By Country

- The United States

- Canada

- Rest of North America

Frequently Asked Questions

1. What are rare sugars?

Rare sugars are naturally occurring sugars found in small amounts, like allulose and tagatose, offering sweetness with fewer calories in the North America Rare Sugar Market.

2. What is the North America rare sugar market size?

The North America rare sugar market is expected to grow steadily due to rising demand for low-calorie sweeteners.

3. Which rare sugar is most popular in North America?

Allulose is the most widely used rare sugar in North America due to its low-calorie profile and sugar-like taste.

4. What is driving growth in the North America rare sugar market?

Health awareness, clean-label demand, and obesity concerns are key drivers for rare sugar market growth.

5. Which industries use rare sugars in North America?

Food & beverage, pharmaceuticals, and nutraceuticals industries are the primary consumers of rare sugars.

6. Which companies are key players in the North America rare sugar market?

Key players include Matsutani, Bonumose, Tate & Lyle, and CJ CheilJedang.

7. Which countries in North America lead rare sugar consumption?

The United States dominates rare sugar consumption in North America.

8. What is the growth forecast for the rare sugar market in North America?

The market is projected to grow at a strong CAGR due to expanding food innovation and sugar reduction trends.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com