North America Respiratory Trainer Market Size, Share, Trends & Growth Forecast Report - Segmented By Type (Resistance Training Devices, Endurance Devices), Application and Country (The United States, Canada and Rest of North America), Industry Analysis From 2026 to 2034

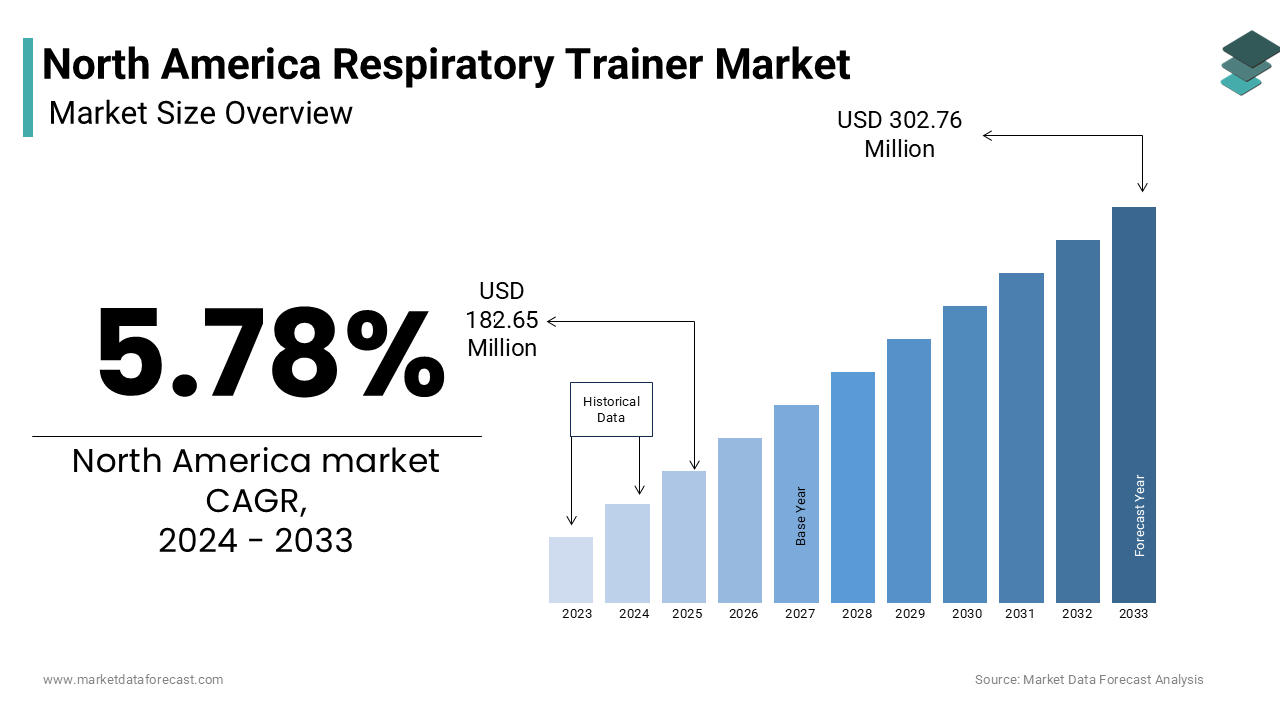

Market Size, 2025

$193.21 MnMarket Estimate, 2026

$204.38 MnMarket Forecast, 2034

$320.38 MnCAGR, 2026–2034

5.78%North America Respiratory Trainer Market Size

The North America respiratory trainer market size was valued at USD 193.21 million in 2025 and is anticipated to reach USD 204.38 million in 2026 from USD 320.38 million by 2034, growing at a CAGR of 5.78% during the forecast period from 2026 to 2034.

The respiratory trainer enhances pulmonary muscle strength, improves breathing efficiency, and supports respiratory rehabilitation. Their application spans patients recovering from respiratory illnesses such as chronic obstructive pulmonary disease (COPD), post-COVID-19 pulmonary complications, and neuromuscular disorders, as well as healthy individuals seeking performance optimization. As per the Centers for Disease Control and Prevention, approximately 16 million Americans have been diagnosed with COPD, a condition that directly impairs respiratory muscle function and necessitates targeted breathing interventions.

MARKET DRIVERS

Rising Prevalence of Chronic Respiratory Diseases and Associated Pulmonary Muscle Dysfunction

The escalating burden of chronic respiratory conditions is driving the growth of the North America respiratory trainer market. Chronic obstructive pulmonary disease (COPD), asthma, and interstitial lung diseases significantly compromise diaphragmatic strength and ventilatory efficiency, necessitating targeted respiratory muscle training as part of standard care. According to the American Lung Association, one in five adults over the age of 65 in the United States has been diagnosed with COPD, a condition intrinsically linked to inspiratory muscle fatigue and reduced exercise tolerance. Respiratory trainers mitigate these effects by progressively strengthening the diaphragm and intercostal muscles, thereby improving lung capacity and reducing dyspnea.

Increasing Adoption of Respiratory Training in Sports Performance and High-Altitude Conditioning

The integration of respiratory trainers into athletic performance regimens is additionally fuelling the growth of the North America respiratory trainer market. Elite athletes, military personnel, and fitness enthusiasts are increasingly utilizing inspiratory muscle training (IMT) devices to enhance oxygen uptake, delay ventilatory fatigue, and improve endurance. As per the National Collegiate Athletic Association, over 480,000 student-athletes participate in organized college sports across the United States, many of whom are now incorporating respiratory conditioning into their training protocols.

MARKET RESTRAINTS

Limited Reimbursement Coverage for Respiratory Training Devices in Outpatient and Home Settings

The absence of comprehensive insurance reimbursement policies is restraining the growth of the North America respiratory trainer market. According to the Centers for Medicare & Medicaid Services, only pulmonary rehabilitation programs conducted in certified outpatient clinics are eligible for reimbursement under Medicare Part B, with no provision for take-home training devices. This policy gap forces patients to bear the full cost of devices, which typically range from $75 to $300 by creating a financial barrier for low- and middle-income individuals. Furthermore, a 2022 survey by the Respiratory Health Association found that 68% of pulmonologists refrain from prescribing respiratory trainers due to patient affordability concerns.

Lack of Standardization and Regulatory Ambiguity in Device Classification

The substantial regulatory fragmentation is impeding consistent product evaluation and clinical integration, which is degrading the growth of the North American respiratory trainer market. As per FDA guidelines, devices intended solely for "improving athletic performance" or "general breathing fitness" fall outside the scope of medical device regulation, enabling non-clinical products to enter the market without rigorous validation. Moreover, the absence of standardized performance metrics complicates comparative assessments.

MARKET OPPORTUNITIES

Integration of Digital Health Platforms and Smart Respiratory Trainers

The adoption of respiratory training with digital health technologies is lucratively to promote the growth of the North American respiratory trainer market. Smart respiratory trainers equipped with Bluetooth connectivity, real-time biofeedback, and mobile app integration are gaining traction among both clinicians and consumers. These devices enable remote monitoring of breathing metrics such as inspiratory force, training adherence, and muscle endurance, facilitating personalized rehabilitation programs. According to the Office of the National Coordinator for Health Information Technology, over 90% of U.S. hospitals now use certified electronic health record systems, which is creating infrastructure for integrating patient-generated respiratory data into clinical workflows. Companies like PHASYS and Breather2GO have launched FDA-cleared devices that sync with telehealth platforms by allowing pulmonologists to adjust training regimens based on real-world performance data. Furthermore, the Federal Communications Commission reports that 97% of Americans have access to broadband internet, enabling seamless data transmission from home-based devices.

Expansion of Pulmonary Rehabilitation Access Through Home-Based Care Models

The shift toward decentralized healthcare delivery in home-based pulmonary rehabilitation is another attribute boosting the growth of the North American respiratory trainer market. Traditional pulmonary rehab programs require patients to attend supervised sessions at medical facilities, a model that excludes many due to geographic, mobility, or time constraints. The Veterans Health Administration reported a 55% increase in remote pulmonary rehab enrollment between 2021 and 2023, with respiratory trainers distributed as core components of home kits. The program demonstrated a 34% reduction in hospital readmissions for COPD patients within six months of completion.

MARKET CHALLENGES

Low Clinical Awareness and Underutilization by Healthcare Providers

The limited awareness and integration into standard clinical protocols are challenging the growth of the North American respiratory trainer market. A 2023 survey conducted by the American College of Chest Physicians revealed that only 38% of pulmonologists routinely recommend inspiratory muscle training to their patients, even in cases of documented respiratory muscle weakness. This gap persists despite guidelines from the American Association for Respiratory Care endorsing respiratory muscle training as a beneficial adjunct in COPD and neuromuscular disease management. Furthermore, time constraints in primary care settings discourage in-depth discussions about non-pharmacological interventions.

Consumer Misconceptions and Market Saturation with Non-Clinical Devices

The increasingly fragmented by consumer confusion stemming from the proliferation of non-clinical, performance-oriented breathing devices is hampering the growth of the North American respiratory trainer market. Products marketed under terms like “breathing optimizers,” “lung strengtheners,” or “altitude simulators” often lack clinical validation yet dominate online retail platforms, which is creating misperceptions about efficacy and safety. According to the Better Business Bureau, consumer complaints related to misleading claims about respiratory devices increased by 62% between 2020 and 2023, with many users reporting no measurable improvement in breathing capacity. Additionally, the conflation of respiratory training with practices like “holotropic breathing” or “Wim Hof method” accessories further blurs the distinction between therapeutic tools and wellness trends.

SEGMENTAL ANALYSIS

By Type Insights

The resistance training devices segment was accounted in holding a significant share of the North America respiratory trainer market in 2024 with the threshold and flow-dependent inspiratory muscle trainers that apply calibrated resistance to strengthen the diaphragm and intercostal muscles. As per the American Thoracic Society, MIP values below 70 cm H₂O are associated with higher risks of hospitalization and ventilatory failure, which makes resistance training an intervention. Furthermore, the widespread adoption of devices like the POWERbreathe K-Series and Threshold IMT in Veterans Health Administration facilities has institutionalized their use. The U.S. Department of Veterans Affairs reports that over 42,000 veterans with chronic respiratory conditions received resistance training devices through home care programs in 2023.

The endurance segment is anticipated to grow with a CAGR of 11.8% from 2026 to 2034 with devices focusing on sustained breathing exercises that improve ventilatory stamina rather than maximal muscle force, aligning with emerging applications in athletic performance and post-acute recovery. A pivotal driver is their adoption in high-intensity interval training (HIIT) and endurance sports, where delayed respiratory fatigue enhances aerobic capacity. The National Collegiate Athletic Association notes that over 70 NCAA Division I programs now incorporate endurance-focused respiratory training into off-season conditioning. As per the Centers for Disease Control and Prevention, more than 6 million Americans report persistent fatigue and dyspnea months after SARS-CoV-2 infection.

By Application Insights

The adult segment held a prominent share of the North America respiratory trainer market in 2025 with the high prevalence of chronic respiratory diseases among the adult population, particularly those aged 45 and above. A study published in The New England Journal of Medicine found that adults with COPD who engaged in supervised inspiratory training reduced their risk of respiratory-related hospitalization by 37% over 12 months.

The pediatric application segment is emerging with an expected CAGR of 10.3% from 2026 to 2034 with the rising clinical recognition of respiratory muscle dysfunction in children with neuromuscular and congenital disorders. As per guidelines from the American Academy of Pediatrics, early initiation of inspiratory muscle training can delay the onset of hypoventilation by up to two years in DMD patients. While traditionally managed pharmacologically, emerging protocols now include respiratory conditioning to reduce bronchial hyperresponsiveness.

REGIONAL ANALYSIS

United States Respiratory Trainer Market Insights

The United States was the top performer in the North America respiratory trainer market by capturing 76.3% of share in 2025 with its advanced healthcare infrastructure, high prevalence of chronic respiratory diseases, and robust reimbursement frameworks for pulmonary rehabilitation. According to the American Lung Association, 35 million Americans suffer from chronic lung conditions, which creates a vast patient pool requiring respiratory support. Furthermore, the U.S. leads in clinical innovation over 120 FDA-cleared respiratory training devices are currently marketed, including smart models with telehealth integration. The country’s strong research ecosystem also drives adoption; institutions like the Mayo Clinic and National Institutes of Health continue to publish pivotal studies validating respiratory training efficacy.

Canada Respiratory Trainer Market Insights

Canadian respiratory trainer market was positioned second with 14.3% of share in 2025 with a publicly funded healthcare system that emphasizes preventive and rehabilitative care, fostering gradual but steady adoption of respiratory conditioning tools. A 2023 evaluation by the McGill University Health Centre found that patients using resistance trainers in home-based rehab reduced emergency department visits by 29% over six months. However, access disparities persist—rural and remote populations, particularly in northern territories, face limited availability of specialized respiratory care. To address this, Indigenous Services Canada has launched pilot tele-rehabilitation projects incorporating portable respiratory trainers for First Nations communities.

KEY MARKET PLAYERS

- Teleflex Incorporated

- Koninklijke Philips N.V.

- Smiths Medical, Inc.

- Vyaire Medical, Inc.

- IngMar Medical

- POWERbreathe International Limited

- PN Medical

- Aleas Europe LLC

- Aspire Products, LLC

- Airofit

COMPETITIVE LANDSCAPE

The competitive landscape of the North America respiratory trainer market is marked by a blend of medical technology leaders and specialized niche innovators, each striving to establish clinical relevance and user trust. Established players leverage their reputation in respiratory care to extend into muscle training, emphasizing scientific validation and integration with existing healthcare ecosystems. Differentiation is achieved through technological sophistication, such as real-time biofeedback, app connectivity, and ergonomic design, rather than price competition. Companies are increasingly focused on building ecosystems where devices interact with broader health monitoring platforms, enhancing utility and adherence. Strategic positioning involves aligning with clinical guidelines, securing endorsements from professional societies, and embedding products into rehabilitation protocols. Brand credibility, regulatory compliance, and partnerships with healthcare providers serve as key differentiators.

Top Players in the North America Respiratory Trainer Market

Philips Respironics

Philips Respironics has established itself as a pivotal innovator in the respiratory care domain, extending its expertise beyond traditional ventilation into the specialized realm of respiratory muscle training. The company integrates user-centric design with clinical rigor, offering devices that align with pulmonary rehabilitation protocols used in major healthcare institutions. Its focus on seamless integration with digital health platforms enables clinicians to monitor patient progress remotely, enhancing adherence and outcomes. The company’s commitment to advancing respiratory health through technology-driven therapy positions it as a key influencer in shaping modern breathing rehabilitation standards globally.

Hamilton Medical

Hamilton Medical is renowned for its engineering excellence and deep clinical engagement in respiratory care support. While primarily recognized for its intensive care ventilators, the company has expanded its influence into respiratory conditioning by contributing to the development of protocols that incorporate muscle training in weaning processes and post-ICU recovery. Its devices are frequently used in academic medical centers where evidence-based practices are refined, allowing Hamilton Medical to indirectly shape the application of respiratory trainers in complex patient management. The company emphasizes precision, reliability, and physiological alignment in its technologies, which is fostering trust among clinicians managing patients with severe respiratory compromise.

GE Healthcare

GE Healthcare contributes to the respiratory trainer ecosystem through its comprehensive monitoring and diagnostic platforms that support the assessment of respiratory muscle function. While not a direct manufacturer of standalone training devices, the company enables the clinical validation and deployment of respiratory training by providing tools that measure inspiratory pressure, lung volumes, and ventilatory efficiency. These capabilities are integral to identifying patients who would benefit from targeted muscle conditioning and for tracking therapeutic progress. Integrated within hospital pulmonary labs and sleep clinics, GE Healthcare’s systems support decision-making that precedes and follows respiratory training interventions. The company’s global footprint and integration with electronic medical records allow for scalable implementation of respiratory health programs.

Top Strategies Used by Key Market Participants

One of the primary strategies employed by leading companies is the integration of digital health technologies into respiratory training devices. This digital transformation supports telehealth adoption and aligns with the shift toward decentralized care models.

Another key approach is strategic collaboration with healthcare institutions and research organizations. Companies partner with academic medical centers, veterans’ health networks, and pulmonary associations to validate device efficacy through clinical studies and incorporate feedback into product development. These alliances not only strengthen scientific credibility but also facilitate faster adoption within clinical workflows.

RECENT MARKET DEVELOPMENTS

- In March 2024, Philips Respironics launched a new digital respiratory training platform integrated with its existing sleep and respiratory care ecosystem by enabling remote monitoring and personalized training plans for patients undergoing pulmonary rehabilitation.

- In June 2023, Hamilton Medical collaborated with the University of Pittsburgh Medical Center to develop clinical protocols incorporating respiratory muscle training in post-ICU recovery programs by enhancing the scientific foundation for its use in care weaning.

- In January 2024, GE Healthcare introduced an advanced pulmonary function module within its patient monitoring systems by allowing clinicians to assess inspiratory muscle strength and identify candidates for respiratory training within hospital settings.

- In September 2023, a leading respiratory device startup partnered with the U.S. Olympic Training Center to deploy smart respiratory trainers for endurance athletes, which is marking a strategic expansion into high-performance sports conditioning.

- In May 2024, a major home healthcare provider integrated FDA-cleared respiratory trainers into its national tele-rehabilitation program for chronic lung disease patients, which is significantly expanding access to home-based breathing therapy.

MARKET SEGMENTATION

This research report on the North America Feeding Tubes Market is segmented and sub-segmented based on categories.

By Type

- Resistance Training Devices

- Endurance Devices

By Application

- Adults

- Pediatrics

By Country

- U.S.

- Canada

- Rest of North America

Frequently Asked Questions

What is the North America Respiratory Trainer Market?

It is the market for medical devices designed to strengthen respiratory muscles, improve lung function, and support rehabilitation in patients with chronic respiratory diseases, post-viral conditions, and athletes seeking enhanced performance.

What factors are driving market growth?

Rising prevalence of chronic respiratory diseases, increasing post-COVID complications, growing adoption in sports training, and emphasis on non-pharmacological therapies are key growth drivers.

What is the future outlook of this market?

The market is expected to grow steadily with rising healthcare awareness, expansion of home healthcare programs, and adoption of respiratory training in both clinical and fitness settings.

What are the major challenges faced by this market?

Limited patient awareness, high device costs for advanced models, and adherence issues in long-term home-based respiratory training are key challenges.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com