North America Scientific Instruments Market Size, Share, Growth, Trends, And Forecasts Report, Segmented By End-User, Type And By Country (The United States, Canada, Mexico), Industry Analysis From 2025 to 2033

North America Scientific Instruments Market Size

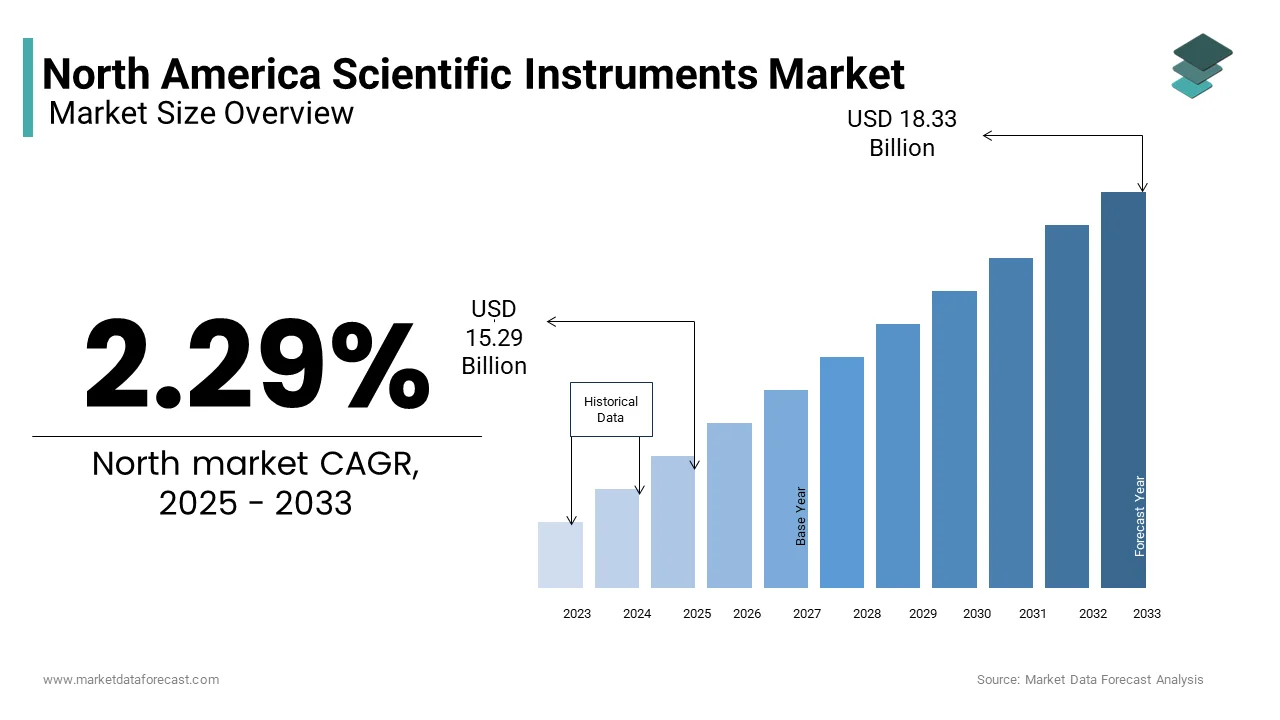

The North American scientific instruments market was valued at USD 14.95 billion in 2024 and is anticipated to reach USD 15.29 billion in 2025 to USD 18.33 billion by 2033, growing at a CAGR of 2.29% during the forecast period from 2025 to 2033.

The scientific instruments include spectrometers, chromatographs, mass spectrometers, electron microscopes, calorimeters, and various laboratory automation systems that support innovation and quality control in diverse applications. As per the National Science Foundation (NSF), the United States alone accounted for over $200 billion in total R&D expenditures in 2023, with life sciences, materials science, and environmental monitoring being key application areas driving demand for advanced instrumentation. The expansion of biopharmaceutical manufacturing, increasing adoption of lab-on-a-chip technologies, and growing need for high-throughput screening in drug discovery are reshaping the landscape.

MARKET DRIVERS

Expansion of Biopharmaceutical R&D and Drug Discovery Activities

The rapid expansion of biopharmaceutical research and development (R&D) activities is expected to boost the growth of the North American scientific instruments market. According to the Pharmaceutical Research and Manufacturers of America (PhRMA), over 900 biopharmaceuticals were in active clinical development in the U.S. in 2023, many requiring sophisticated analytical instruments for preclinical testing and formulation analysis. In addition, the rise of personalized medicine and targeted therapies has amplified the demand for high-resolution instruments such as next-generation sequencers, flow cytometers, and liquid chromatography-mass spectrometry (LC-MS) systems. These tools enable precise biomarker identification and pharmacokinetic profiling, which are important for drug approval and commercialization. Furthermore, contract research organizations (CROs) supporting drug discovery have expanded their analytical capabilities, directly contributing to increased procurement of scientific instruments.

Increased Federal and Institutional Funding for Academic and Industrial Research

The robust financial support provided by federal agencies and private institutions for academic and industrial research is driving the growth of the North American scientific instruments market. This influx of capital has led to heightened demand for state-of-the-art laboratory equipment, including high-throughput screening platforms, confocal microscopes, and automated sample preparation systems. Moreover, leading universities such as MIT, Stanford, and the University of Toronto have launched major capital campaigns aimed at upgrading their laboratories, thereby stimulating demand for next-generation scientific instruments. The synergy between government funding, academic innovation, and industry collaboration continues to serve as a powerful catalyst for market expansion across North America.

MARKET RESTRAINTS

High Cost of Advanced Scientific Instruments and Maintenance Requirements

The high acquisition cost and ongoing maintenance requirements associated with advanced analytical equipment are restraining the growth of the North America scientific instruments market. Cutting-edge instruments such as cryo-electron microscopes, nuclear magnetic resonance (NMR) spectrometers, and ultra-high-performance liquid chromatography (UHPLC) systems often carry price tags exceeding several million dollars. These instruments require specialized technical personnel for operation and regular calibration service, adding to long-term operational expenses. A 2023 report by the Association of Biomolecular Resource Facilities (ABRF) indicated that annual service contracts for high-end analytical instruments typically range between 10% and 15% of the purchase price, which poses a financial burden for smaller institutions and startups.

Additionally, fluctuations in currency exchange rates and supply chain disruption, particularly for imported components, can further inflate costs. Many academic and non-profit research labs face budget constraints that limit their ability to upgrade or replace aging equipment.

Regulatory Compliance and Stringent Quality Control Standards

The complexity of regulatory compliance and stringent quality assurance protocols required for instrument validation and usage are hindering the growth of the North American scientific instruments market. Scientific instruments employed in pharmaceutical, clinical diagnostics, and environmental testing must adhere to rigorous standards set by agencies such as the U.S. Food and Drug Administration (FDA), Environmental Protection Agency (EPA), and Health Canada. These regulations mandate comprehensive documentation, traceable calibration, and periodic audits to ensure data integrity and reproducibility. For instance, laboratories operating under Good Laboratory Practice (GLP) and Good Manufacturing Practice (GMP) frameworks must undergo frequent inspections to maintain certification. According to the American Society for Quality (ASQ), compliance-related overhead can increase operational costs by up to 20%, discouraging some smaller firms from investing in high-end instrumentation. Moreover, evolving digital compliance requirements, such as 21 CFR Part 11 for electronic records and signatures, necessitate additional software integration and cybersecurity measures.

MARKET OPPORTUNITIES

Growth in Precision Medicine and Personalized Healthcare Applications

The expanding field of precision medicine and personalized healthcare is driving the growth of the North American scientific instruments market. Advances in genomics, proteomics, and metabolomics have created a growing demand for highly sensitive and accurate analytical tools capable of detecting minute molecular variations in patient samples. According to the National Institutes of Health (NIH), the All of Us Research Program had enrolled over one million participants by early 2024 by accelerating the shift toward individualized treatment strategies that rely on detailed biomarker profiling. Scientific instruments such as next-generation sequencers, digital PCR systems, and high-resolution mass spectrometers are playing a pivotal role in enabling this transformation. Companies like Thermo Fisher Scientific and Agilent Technologies have introduced benchtop sequencing platforms tailored for hospital and clinical research settings, making genomic analysis more accessible.

Integration of AI and Machine Learning in Instrumentation for Enhanced Data Analysis

The integration of artificial intelligence (AI) and machine learning (ML) into scientific instrumentation represents a transformative opportunity for the North American market. These technologies are increasingly being embedded into analytical platforms to automate data interpretation, improve predictive accuracy, and reduce manual intervention in experimental workflows. Major instrument manufacturers are incorporating AI-driven analytics into mass spectrometry, spectroscopy, and flow cytometry systems to enhance pattern recognition and accelerate discovery cycles. For example, Leica Microsystems and Zeiss have introduced AI-powered digital pathology scanners that streamline tissue analysis and flag anomalies with greater consistency than traditional methods.

MARKET CHALLENGES

Supply Chain Disruptions and Component Shortages Impacting Instrument Availability

The ongoing volatility in global supply chains, which is regarding semiconductor components, precision sensors, and optical elements, is impeding the growth of the North American scientific instruments market. The pandemic-induced disruptions of recent years have been followed by geopolitical tensions, export restrictions, and logistical bottlenecks that continue to affect lead times and instrument availability. Manufacturers such as PerkinElmer and Bruker have reported extended delivery windows for certain products due to delays in sourcing high-precision lenses, detectors, and cooling modules. Additionally, inflationary pressures and rising freight costs have contributed to higher instrument prices, placing further strain on institutional budgets. These supply-side constraints pose a serious challenge to market growth for academic and clinical users who depend on the n timely procurement of equipment for research continuity and patient diagnostics.

Talent Shortage and Training Gaps in Specialized Instrument Operation

The shortage of skilled professionals trained to operate and maintain advanced analytical equipment is additionally to act as a barrier to the growth of the North American scientific instruments market. Moreover, the lack of standardized training programs for next-generation instrumentation limits the effective utilization of high-end tools. A 2023 study published in Analytical Chemistry found that nearly one-third of newly acquired instruments in academic settings were underutilized due to insufficient operator knowledge.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 1.73% |

| Segments Covered | By End-user, Type, and Country |

| Various Analyses Covered | Global, Regional, and country-level analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country's Covered | The United States, Canada, and the Rest of North America |

| Market Leaders Profiled | Thermo Fisher Scientific Inc., Agilent Technologies Inc., Danaher Corporation, PerkinElmer Inc., Bruker Corporation, Shimadzu Corporation, Waters Corporation. |

SEGMENTAL ANALYSIS

By End-Use Insights

The industrial segment dominated the North America scientific instruments market by accounting for 58.3% of the share in 202,4, with the rapid expansion of the biopharmaceutical sector, particularly in the U.S., where over 900 drug candidates were in active development in 2023, as reported by PhRMA. These developments necessitate high-throughput screening platforms, chromatography systems, and mass spectrometers for drug discovery and quality assurance. Additionally, the growing adoption of process analytical technology (PAT) frameworks in manufacturing has increased demand for real-time monitoring instruments. Another major factor contributing to this dominance is the rise in contract manufacturing and research organizations (CMOs and CROs). According to Deloitte, the number of outsourced R&D contracts in life sciences grew by nearly 14% in 2023.

The academic segment is projected to grow with a CAGR of 7.6% from 2025 to 20,33 with the surge in grants awarded by agencies such as the National Institutes of Health (NIH), which allocated over $47 billion in fiscal year 2023 for biomedical research across academic institutions, as per NIH’s official budget report. Universities are leveraging these funds to upgrade their laboratories with advanced tools like cryo-electron microscopes, confocal imaging systems, and automated sequencing platforms. Additionally, there has been a growing emphasis on interdisciplinary research and innovation hubs. For instance, MIT launched its nanofabrication facility in 2023, investing over $70 million in cutting-edge instrumentation.

By Type Insights

The scientific analytical instruments segment held the dominant share of the North America scientific instruments market in 2024 due to the escalating demand for high-resolution instruments such as gas chromatographs, mass spectrometers, and nuclear magnetic resonance (NMR) spectrometers in drug development and quality control processes. Another factor boosting the growth of the segment is the expansion of industrial R&D initiatives, especially in the chemicals and petrochemicals industries.

The Scientific Clinical Analyzers segment is anticipated to grow with a CAGR of 8.2% during the forecast period. The growing prevalence of chronic diseases such as cancer, diabetes, and cardiovascular disorders, which require continuous patient monitoring through biochemical analyzers, immunoassay systems, and hematology analyzers, is likely to promote the growth of the segment. Additionally, advancements in point-of-care testing (POCT) and molecular diagnostics have expanded the utility of clinical analyzers beyond traditional labs. Companies like Roche Diagnostics and Abbott Laboratories introduced portable molecular testing devices in 2023 that enable faster results without centralized lab support.

COUNTRY-LEVEL ANALYSIS

United States Scientific Instruments Market Analysis

The United States was the top performer in the North American scientific instruments market by holding 86.3% of the share in 2024, with the strong government funding, particularly through agencies such as the National Institutes of Health (NIH) and the National Science Foundation (NSF), which together allocated over $55 billion in 2023 for research and infrastructure development. In addition, the presence of leading scientific instrument manufacturers and service providers, including Thermo Fisher Scientific, Agilent Technologies, and Waters Corporation, supports domestic innovation and global export capabilities.

Canada Scientific Instruments Market Analysis

Canada was ranked second by occupying 12.3% of the North American scientific instruments market share in 2024 due to the increase in federal and provincial funding for post-secondary research. Innovation, Science and Economic Development Canada reported that in 2023, over $2.3 billion was invested in research infrastructure through programs like the Canada Foundation for Innovation (CFI). Additionally, the Canadian healthcare system's emphasis on precision diagnostics and public health surveillance has boosted demand for clinical analyzers and genomic sequencing platforms. The Public Health Agency of Canada (PHAC) expanded its national pathogen sequencing initiative in 2023, integrating next-generation sequencers into routine disease tracking.

COMPETITIVE LANDSCAPE

The competition in the North American scientific instruments market is highly dynamic, shaped by a mix of established multinational corporations, regional players, and emerging innovators. Market participants are continuously adapting to rapid technological advancements, shifting regulatory landscapes, and increasing demand for high-precision, automated, and AI-integrated solutions. The presence of leading pharmaceutical, biotechnology, and academic institutions in the region fuels intense rivalry, as vendors strive to offer differentiated products and value-added services.

Key players focus on strengthening their foothold through innovation, strategic mergers and acquisitions, and expanding their service ecosystems beyond hardware to include software and analytics platforms. Customer relationships are increasingly built around end-to-end solutions, including technical support, training, and cloud-based data management. At the same time, smaller niche firms are gaining traction by introducing disruptive technologies in specialized domains such as portable diagnostics, microfluidics, and real-time monitoring systems.

The market is also witnessing growing collaboration between instrument manufacturers and healthcare providers to develop tailored solutions for precision medicine and point-of-care diagnostics.

KEY MARKET PLAYERS

These are the market players that are dominating the North American scientific instruments market.

- Thermo Fisher Scientific Inc

- Agilent Technologies Inc.

- Danaher Corporation

- PerkinElmer Inc.

- Bruker Corporation

- Shimadzu Corporation

- Waters Corporation

Top Players In The Market

- Thermo Fisher Scientific is a global leader in scientific instruments, offering a comprehensive portfolio that spans analytical equipment, laboratory consumables, and diagnostic tools. The company plays a pivotal role in advancing research, clinical diagnostics, and industrial applications across North America. Its strong presence in both academic and commercial sectors has made it a go-to provider for high-performance instrumentation.

- Agilent Technologies is renowned for its expertise in life sciences, diagnostics, and applied chemical markets. The company provides cutting-edge chromatography, spectroscopy, and mass spectrometry solutions that support innovation in drug discovery, environmental testing, and food safety. Agilent's customer-centric approach and continuous R&D investments have promoted its position in the North American market.

- PerkinElmer specializes in advanced imaging, informatics, and detection technologies that cater to pharmaceutical, biotech, and academic institutions. Known for its integrated workflows and automation capabilities, PerkinElmer enhances laboratory efficiency and accelerates discovery processes. Its strategic focus on sustainability and digital transformation further strengthens its footprint in the North American scientific instruments landscape.

Top Strategies Used By Key Market Participants

- One major strategy employed by key players in the North American scientific instruments market is product innovation through continuous R&D investment. Companies are developing next-generation instruments with enhanced sensitivity, automation, and integration capabilities to meet evolving industry demands. These innovations help firms differentiate their offerings and maintain dominance in competitive segments such as genomics and proteomics.

- The strategic acquisitions and partnerships are another key approach followed by the market key players. Companies can expand their product portfolios, enter new therapeutic areas, and strengthen their distribution networks by acquiring niche technology providers or forming alliances with research institutions and healthcare organizations. These collaborations also enable access to specialized expertise and accelerate time-to-market for new solutions.

- The digital transformation and AI integration have become central to competitive differentiation. Leading firms are embedding artificial intelligence and machine learning into instrument software to enhance data analysis, improve workflow efficiency, and support predictive diagnostics. This shift is not only improving user experience but also aligning scientific instruments with broader trends in smart laboratories and precision medicine adoption.

RECENT MARKET NEWS

- In February 2024, Thermo Fisher Scientific introduced a new line of benchtop mass spectrometers designed specifically for academic and clinical research labs. This launch aimed to provide researchers with greater accessibility to high-resolution analytical tools without compromising performance, thereby expanding the company’s reach in the mid-tier instrumentation segment.

- In May 2024, Agilent Technologies formed a strategic alliance with a leading U.S.-based university to co-develop next-generation metabolomics platforms. The partnership focused on integrating novel separation techniques with AI-driven data interpretation to enhance biomarker discovery and disease profiling capabilities.

- In August 2024, PerkinElmer announced the expansion of its digital lab ecosystem by launching an integrated cloud-based platform that enables remote instrument control, data sharing, and collaborative research workflows. This move was intended to support the growing trend of decentralized and hybrid research environments.

- In October 2024, Danaher Corporation acquired a startup specializing in microfluidic chip technology for point-of-care diagnostics. This acquisition was aimed at enhancing Danaher’s portfolio in miniaturized, portable analytical devices suitable for field and clinical use.

- In December 2024, Bruker launched a new cryo-electron microscopy solution tailored for structural biology applications in academic and government research centers. The initiative was designed to make high-end imaging more accessible to non-commercial research institutions while reinforcing Bruker’s dominance in advanced microscopy.

MARKET SEGMENTATION

This research report on the North America Scientific instruments market is segmented and sub-segmented into the following categories.

By End-Use

- Industrial

- Government Institutes

- Academics

By Type

- Scientific Clinical Analyzers

- Scientific Analytical Instruments

By Country

- The United States

- Canada

- Mexico

Frequently Asked Questions

What are scientific instruments?

Scientific instruments are specialized devices used in research, measurement, and analysis to advance knowledge across science, industry, and medicine.

Why is the North American market for scientific instruments important?

This region drives global scientific innovation with its investment in research, advanced healthcare, and thriving technology sectors.

Who uses scientific instruments in North America?

They are essential for academic researchers, healthcare professionals, industrial labs, and quality-control teams across various industries.

What trends are shaping the market currently?

Increasing automation, miniaturization, and integration with digital technologies are making scientific instruments more efficient and versatile.

What challenges do market players face?

Managing rapid technological change and meeting strict regulatory standards while ensuring cost-effectiveness are ongoing challenges.

Are sustainability concerns relevant in this sector?

Yes, manufacturers and users focus on energy efficiency, safe material use, and responsible disposal to reduce the environmental footprint.

How is digital technology impacting scientific instruments?

Digital integration is enabling better data accuracy, real-time analytics, and remote monitoring for more dynamic research.

What industries are fueling new demand?

Biotechnology, pharmaceuticals, environmental testing, and advanced materials industries are driving strong demand for next-gen instruments.

What is the outlook for new entrants in the market?

Competition is tough, but innovation in niche applications or cost-effective manufacturing can open doors for startups.

How is collaboration influencing the industry?

Partnerships between academia, tech companies, and manufacturers are accelerating product development and adoption of advanced solutions.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com