North America Secondary Wood Products Market Size, Share, Trends & Growth Forecast Report - Segmented By Type (Engineered Wood, Wood Furniture), Application and Country (The United States, Canada and Rest of North America), Industry Analysis From 2024 to 2033

North America Secondary Wood Products Market Size

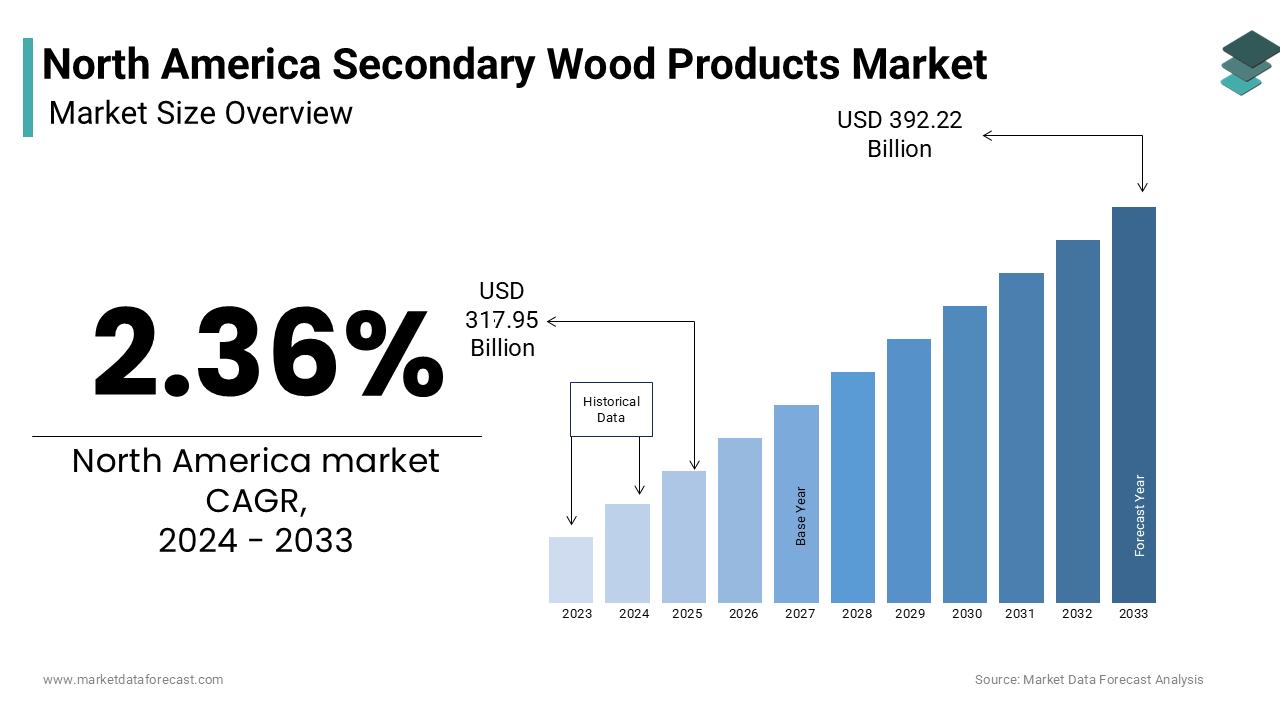

The North America Secondary Wood Products Market is estimated to grow from USD 317.95 billion in 2024 to USD 392.22 billion in 2033, representing a CAGR of 2.36%.

The secondary wood products are processed timber materials derived from primary wood manufacturing, including mouldings, millwork, engineered wood components, and fabricated assemblies used in residential and commercial construction, furniture, and interior design. These products are distinct from raw lumber, as they undergo further value-added treatments such as cutting, shaping, laminating, or coating to meet specific dimensional, structural, or aesthetic requirements. As per the U.S. Forest Service, the United States harvested approximately 14.2 billion board feet of softwood timber in 2022, a significant portion of which feeds into secondary processing facilities across the continent. The integration of digital templating and CNC machining technologies has elevated precision in product output by enabling customization at scale. Moreover, increasing emphasis on sustainable building practices has led to greater demand for secondary wood items certified under standards such as FSC or SCS.

MARKET DRIVERS

Rising Residential Construction and Remodeling Activity

The surge in residential construction and renovation projects is propelling the growth of the North America secondary wood products market. As urban populations expand and housing inventories remain tight, developers and homeowners increasingly invest in customized millwork, cabinetry, flooring, and trim solutions core components of the secondary wood segment. According to the U.S. Census Bureau, approximately 1.44 million housing units were authorized in the United States in 2023, reflecting a 3.2% year-on-year increase despite elevated interest rates. Secondary wood manufacturers benefit from this sustained demand, particularly as modular and prefabricated home construction gains traction, requiring precision-cut components produced off-site.

Growing Emphasis on Sustainable and Certified Wood Sourcing

The environmental consciousness and regulatory pressure have significantly influenced procurement practices within the construction and design industries is enhancing the growth of the North America secondary wood products market. Architects, developers, and institutional buyers are increasingly prioritizing materials with verifiable environmental credentials, particularly those certified by the Forest Stewardship Council (FSC) or the Sustainable Forestry Initiative (SFI). As per the American Wood Council, over 40% of all wood products sold in the U.S. in 2023 originated from forests managed under third-party certification programs, a figure that has steadily risen over the past decade. This shift is reinforced by green building standards such as LEED (Leadership in Energy and Environmental Design), which award points for using certified wood, thereby incentivizing developers to specify compliant secondary wood components. Moreover, consumer surveys conducted by FPInnovations in 2023 revealed that 68% of Canadian homeowners prefer building materials with recognized sustainability labels.

MARKET RESTRAINTS

Volatility in Softwood Lumber Supply and Trade Disputes

The vulnerability to fluctuations in softwood lumber availability and pricing, largely due to protracted trade is hampering the growth of the North America secondary wood products market. Canada supplies approximately 30% of the softwood lumber consumed in the U.S., according to the U.S. International Trade Commission, making the downstream secondary sector highly dependent on cross-border supply chains. However, recurring disputes over alleged subsidies have led to the imposition of countervailing and anti-dumping duties, with U.S. Customs and Border Protection collecting over $5.6 billion in duties on Canadian lumber imports between 2017 and 2023, as confirmed by Global Affairs Canada. These tariffs contribute to input cost instability, forcing secondary manufacturers to absorb higher raw material expenses or pass them on to customers, potentially dampening demand. Furthermore, regional harvest restrictions in British Columbia due to beetle infestations and wildfire-related logging curtailments have reduced fiber availability.

Labor Shortages and Skilled Workforce Deficit

The shortage of skilled labor poses a significant operational challenge in precision craftsmanship and advanced manufacturing roles is limiting the growth of the North America secondary wood products market. The sector requires workers proficient in CNC operation, woodworking machinery maintenance, and quality control skills that are increasingly scarce amid an aging workforce and declining vocational training enrollment. As per the Bureau of Labor Statistics, the median age of woodworkers in the United States was 45.3 years in 2023, with nearly 30% of incumbent workers aged 55 or older, indicating an impending wave of retirements. Compounding the issue, the National Wood Flooring Association in 2023 reported that only 12% of community colleges in the U.S. offer dedicated woodworking or millwork programs, down from 21% in 2015, limiting the pipeline of qualified entrants. This deficit impedes production scalability and increases reliance on automation, which itself requires specialized technicians. Moreover, wage competition with adjacent industries such as construction and metal fabrication has driven up labor costs; the average hourly wage for wood product manufacturing workers rose to $24.80 in 2023, a 15% increase since 2020, according to Statistics Canada.

MARKET OPPORTUNITIES

Expansion of Mass Timber and Prefabricated Construction

The accelerating adoption of mass timber and off-site construction methodologies is creating new opportunities in the next coming years. Engineered wood systems such as cross-laminated timber (CLT), nail-laminated timber (NLT), and dowel-laminated timber (DLT) rely heavily on precision-fabricated components mouldings, connectors, and panelized units that fall within the secondary processing domain. According to the U.S. Department of Energy, over 1,200 mass timber projects were completed or underway across the United States by the end of 2023, a fivefold increase since 2018. Canada is equally active, with British Columbia’s Ministry of Forests reporting 520 approved mass timber constructions between 2015 and 2023, including the 18-story Brock Commons Tallwood House in Vancouver. These projects demand extensive secondary wood components for interior finishes, stairwells, and cladding, creating new revenue streams for manufacturers. Additionally, modular housing initiatives are gaining momentum; the Manufactured Housing Institute noted that factory-built homes accounted for 11% of all new single-family homes in the U.S. in 2023, up from 8% in 2020. These units incorporate pre-finished wood trims, cabinets, and flooring by enabling secondary producers to integrate into high-efficiency supply chains.

Digitalization and Adoption of Advanced Manufacturing Technologies

The integration of digital manufacturing technologies is greatly influencing the growth of North America’s secondary wood products market by enabling greater customization, efficiency, and scalability. Computer-aided design (CAD), computer numerical control (CNC) machining, and industrial Internet of Things (IIoT) platforms are allowing manufacturers to produce complex, made-to-order components with minimal waste and reduced lead times. According to a 2023 survey by the Association of Woodworking & Furnishings Suppliers, 68% of mid-to-large-sized secondary wood firms in the U.S. have adopted CNC systems, while 41% utilize real-time production monitoring tools. These technologies facilitate just-in-time manufacturing, aligning with lean construction practices and reducing inventory costs. Furthermore, Building Information Modeling (BIM) is increasingly used in architectural workflows, allowing seamless data transfer from design to fabrication. Autodesk reported that over 70% of architecture firms in North America employed BIM for residential and commercial projects in 2023, enhancing compatibility with digital wood manufacturing systems. Additionally, additive manufacturing techniques, such as 3D-printed wood composites, are being piloted for custom mouldings and decorative elements, offering new design possibilities. The National Institute of Standards and Technology emphasized in 2023 that digital twin implementations in wood fabrication could reduce production errors by up to 28%, improving yield rates.

MARKET CHALLENGES

Supply Chain Fragmentation and Logistical Inefficiencies

A fragmented and often inefficient supply chain is likely to degrade the growth of the North American secondary wood products market. Unlike integrated primary producers, many secondary manufacturers operate as small or regional entities with limited control over upstream sourcing and downstream distribution. This fragmentation leads to inconsistent raw material quality, delayed deliveries, and higher transaction costs. According to the North American Industry Classification System, over 60% of secondary wood product establishments in the U.S. employ fewer than 20 workers, as reported by the U.S. Census Bureau in 2023, limiting their bargaining power with suppliers and carriers. Additionally, regional disparities in raw material availability create imbalances; for instance, the southeastern U.S. produces abundant southern yellow pine, but lacks sufficient secondary processing capacity, while the Pacific Northwest faces diminishing log supply despite having established millwork clusters. This misalignment forces manufacturers to source materials over longer distances by increasing carbon footprints and costs.

Regulatory and Code Compliance Complexity

Navigating the complex web of building codes, environmental regulations, and safety standards is likely to additionally to hinder the growth of the North America secondary wood products market. Each jurisdiction maintains distinct requirements for fire resistance, emissions, structural performance, and labeling, necessitating product re-engineering or re-certification for different markets. In the United States, compliance with ASTM standards, ICC-700 National Green Building Standard, and California’s stringent CARB Phase 2 regulations for formaldehyde emissions demands rigorous testing and documentation. As per the Architectural Woodwork Institute, over 40% of custom millwork projects in 2023 required region-specific modifications to meet local code mandates, increasing design and production timelines. Moreover, evolving fire safety codes for tall wood buildings require secondary components to undergo extensive flame spread and smoke development testing, as outlined by the National Research Council of Canada. The cost of compliance is substantial; FPInnovations estimated in 2023 that certification and testing expenses accounted for 8–12% of total production costs for medium-sized wood fabricators. Smaller firms, lacking in-house regulatory expertise, often rely on third-party consultants, further increasing overhead.

SEGMENTAL ANALYSIS

By Type Insights

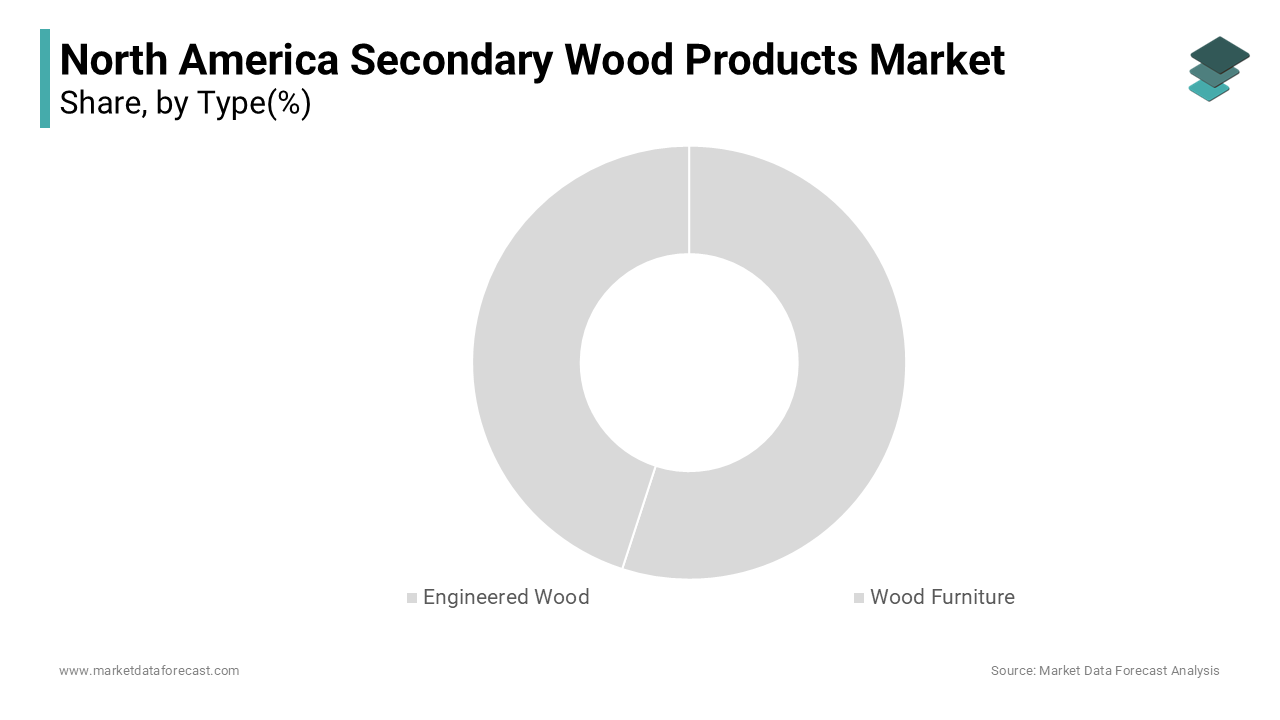

The engineered segment was the largest by capturing 43.2% of the North America secondary wood products market share in 2024 with the integration into structural and semi-structural applications across residential, commercial, and institutional construction. The widespread adoption of engineered wood in residential framing and structural components is fuelling the growth of the North America secondary wood products market. According to the American Wood Council, over 78% of single-family homes constructed in the United States in 2023 incorporated engineered wood in floor systems, roof trusses, or wall assemblies. This preference is reinforced by its performance advantages: a 2022 study by FPInnovations found that I-joists exhibit up to 30% greater span efficiency than comparable dimensional lumber, allowing for open floor plans without intermediate supports. Additionally, engineered wood optimizes fiber utilization; the Forest Products Laboratory estimates that OSB production converts 95% of roundwood into usable panel products, compared to 65–70% for solid sawn lumber. This efficiency reduces waste and supports cost-effective scalability, particularly amid volatile softwood prices.

The wood furniture segment is projected to expand at a CAGR of 6.8% during the forecast period with the rising consumer demand for custom, artisanal, and eco-labeled wood furniture. As per the 2023 Consumer Home Trends Report by the National Association of Home Builders, 64% of new homeowners prioritized furniture with natural materials, with solid wood cited as the most preferred finish. The Sustainable Furnishings Council noted that sales of FSC-certified wood furniture in the U.S. rose by 22% between 2021 and 2023, reflecting stronger eco-conscious purchasing behavior. This revival is supported by nearshoring incentives and rising import logistics costs, with the average container freight rate from Asia to the U.S. West Coast remaining 40% above pre-pandemic levels in 2023, as reported by Drewry Maritime Research.

REGIONAL ANALYSIS

United States was the top performer in the North American secondary wood products market with 68.3% of the share in 2024 with a mature, diversified manufacturing base, extensive construction activity, and deep integration of wood into residential and commercial infrastructure. The country’s leadership is further reinforced by a robust regulatory framework supporting sustainable forestry and green building standards. The U.S. Forest Service reports that over 89 million acres of commercial forestland are actively managed under third-party certification programs such as SFI and FSC, ensuring a steady supply of compliant raw materials for secondary processing. The U.S. Department of Energy notes that over 1,200 mass timber buildings were underway or completed by 2023, creating new pathways for secondary wood integration.

Canada held second position with 24.3% of the North American secondary wood products market share in 2024 with its vast forest resources, advanced processing infrastructure, and strategic export orientation, particularly toward the U.S. market. Quebec, British Columbia, and Ontario serve as primary hubs for secondary wood manufacturing, specializing in high-value millwork, mouldings, and specialty panels. Canada’s forest sector is among the most sustainably managed globally; Natural Resources Canada confirms that 94% of the country’s 347 million hectares of commercial forestland are under certified sustainable management by providing a reliable feedstock for secondary producers. Additionally, Canada is a pioneer in mass timber innovation; the Canadian Wood Council documented 520 approved tall wood buildings between 2015 and 2023, many incorporating domestically fabricated components. However, the sector faces constraints from labor shortages and transportation bottlenecks in British Columbia, where harvest reductions due to mountain pine beetle infestations have limited raw material availability.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

The leading companies in the North America Secondary Wood Products Market are Ashley Furniture Industries, Steelcase, HNI Corporation, Herman Miller, Weyerhaeuser Company, Universal Forest Products (UFP Industries), Arauco, Georgia-Pacific, Kronospan, Louisiana-Pacific, Roseburg Forest Products, Timber Products Company, Tolko Industries, Columbia Forest Products, Norbord Inc., West Fraser Timber Co., and Resolute Forest Products.

The competitive landscape of the North America secondary wood products market is characterized by a blend of large, vertically integrated forest product companies and agile regional manufacturers, each vying for dominance through differentiation in quality, innovation, and sustainability. Incumbent leaders leverage scale, brand recognition, and extensive distribution networks to maintain strong market positions, particularly in engineered wood and structural components. At the same time, niche players are gaining traction by specializing in custom millwork, artisanal furniture, and prefabricated wood systems tailored to green building standards. The rise of mass timber construction and modular housing has intensified rivalry, prompting companies to invest in research, automation, and design collaboration tools to align with modern architectural demands. Geographic proximity and supply chain reliability are becoming decisive factors, especially as reshoring and nearshoring trends accelerate. Competition is further shaped by the growing influence of environmental regulations and certification requirements, which compel manufacturers to demonstrate responsible sourcing and low-carbon production. While price remains a consideration, performance, durability, and compliance are increasingly central to customer decision-making.

Top Players in the North America Secondary Wood Products Market

Louisiana-Pacific Corporation (LP)

Louisiana-Pacific is a leading innovator in engineered wood solutions, which is renowned for its pioneering role in developing oriented strand board (OSB) and advanced structural panels. The company has established a strong footprint in the North American secondary wood market by consistently delivering high-performance building products that meet evolving construction standards. LP emphasizes sustainable manufacturing and has integrated environmental stewardship into its core operations, enabling it to serve both residential and commercial sectors with reliable, code-compliant materials. Its product portfolio extends to siding, trim, and specialty panels, positioning it as a versatile supplier across multiple applications.

Georgia-Pacific Wood Products

Georgia-Pacific operates as a dominant force in the secondary wood landscape through its extensive range of plywood, laminated veneer lumber, and industrial wood components. As a subsidiary of Koch Industries, the company leverages vast forest resources and vertically integrated operations to maintain consistency in quality and supply. It serves a broad spectrum of industries, from home improvement retailers to large-scale construction firms, offering engineered solutions that balance strength, sustainability, and ease of installation. Georgia-Pacific has been instrumental in advancing adhesive technologies that reduce emissions and improve product longevity.

West Fraser Timber Co. Ltd.

West Fraser stands as a major integrated forest products company with a significant presence in both primary and secondary wood manufacturing across North America. The company produces a wide array of value-added wood products, including mouldings, millwork, and engineered components, primarily sourced from its own sawmill operations. Known for operational efficiency and environmental responsibility, West Fraser supplies high-quality secondary wood materials to builders, distributors, and retail partners throughout the U.S. and Canada. Its strategic investments in modernization and cross-laminated timber production have positioned it at the forefront of sustainable construction trends.

Top Strategies Used by Key Market Participants

One of the principal strategies employed by leading companies is vertical integration, enabling greater control over raw material sourcing, production efficiency, and quality assurance. By owning or managing upstream operations such as sawmills and forestlands, firms ensure a steady supply of feedstock while minimizing exposure to market volatility. This integration also supports sustainability claims, as companies can trace wood fiber from forest to finished product, meeting stringent green building requirements.

Another approach is investment in advanced manufacturing technologies, including automation, CNC machining, and digital templating systems. These innovations enhance precision, reduce waste, and allow for scalable customization particularly important in millwork and specialty furniture. Companies are increasingly adopting Industry 4.0 principles to streamline production, improve lead times, and respond dynamically to customer specifications.

A third strategic focus is sustainability-driven branding and certification alignment. Leading players actively pursue FSC, SFI, and PEFC accreditations, positioning their products as environmentally responsible choices. This not only satisfies regulatory and architectural specifications but also strengthens relationships with eco-conscious developers and retailers, differentiating their offerings in a competitive marketplace.

RECENT MARKET DEVELOPMENTS

- In January 2023, West Fraser Timber expanded its engineered wood facility in Alberta, Canada, enhancing its production capacity for laminated veneer lumber and cross-laminated timber. This expansion supports the company’s commitment to sustainable construction and strengthens its role in the growing mass timber sector.

- In June 2022, Louisiana-Pacific launched a new line of low-emission composite siding products designed for high moisture resistance and long-term durability. This innovation reinforces LP’s focus on performance-driven, environmentally responsible building solutions.

- In March 2024, Georgia-Pacific partnered with a digital design platform to integrate its wood panel specifications into Building Information Modeling (BIM) libraries by enabling architects and contractors to seamlessly incorporate its products into construction workflows.

- In September 2023, Canfor Corporation invested in automation upgrades across its secondary wood processing plants in British Columbia, which improved precision and efficiency in moulding and trim manufacturing.

- In February 2022, Roseburg Forest Products introduced a formaldehyde-free adhesive technology in its plywood and panel production by aligning with health and sustainability standards for indoor environments.

MARKET SEGMENTATION

This research report on the North America secondary wood products market is segmented and sub-segmented based on categories.

By Type

- Engineered Wood

- Wood Furniture

By Country

- U.S.

- Canada

- Rest of North America

Frequently Asked Questions

What factors are driving demand for wood furniture in the North America Secondary Wood Products Market?

Rising consumer preference for custom, artisanal, and eco-labeled furniture, along with increasing sales of FSC-certified products, are driving demand.

What is the North America Secondary Wood Products Market?

It refers to the industry that manufactures processed wood-based products such as engineered wood, wood furniture, cabinetry, flooring, and other value-added wood products.

What are the challenges facing the North America Secondary Wood Products Market?

Volatile raw material prices, supply chain disruptions, and competition from imports remain key challenges.

What factors make North America a strong market for secondary wood products?

High construction activity, consumer sustainability awareness, and advanced manufacturing capabilities.

What is the future outlook for the North America Secondary Wood Products Market?

The market is expected to grow steadily with strong demand for engineered wood in construction and rising consumer interest in sustainable wood furniture.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com