North America Semiconductor Materials Market Size, Share, Trends & Growth Forecast Report, Segmented By Type, End-User, And Country (US, Canada, Mexico, and Brazil), Industry Analysis From 2025 to 2033

North America Semiconductor Materials Market Size

The North America semiconductor materials market was valued at USD 23.73 billion in 2024 and is anticipated to reach USD 21.73 billion in 2025 from USD 33.87 billion by 2033, growing at a CAGR of 4.03% during the forecast period from 2025 to 2033.

The North American semiconductor materials market is a cornerstone of global electronics manufacturing, underpinned by robust demand from industries such as consumer electronics, automotive, and telecommunications. Despite challenges such as fluctuating raw material prices and supply chain disruptions, the market remains resilient.

MARKET DRIVERS

Rising Demand for Advanced Electronics

The exponential growth of advanced electronics is a primary driver propelling the semiconductor materials market forward. Consumer electronics, including smartphones, laptops, and smart home devices, dominate semiconductor applications. For example, Apple’s iPhone series alone consumes over 5 billion worth of semiconductors annually, creating significant demand for high−purity silicon wafers and photomasks. Additionally, the proliferation of 5G technology has spurred demand for gallium arsenide and indium phosphide, essential for high−frequency communication chips. Verizon’s 5G expansion plans rely heavily on these materials. Furthermore, gaming consoles like Sony’s PlayStation 5 require cutting-edge semiconductors, driving demand for specialty gases used in etching processes. These trends collectively showcase how the relentless pace of technological advancement fuels sustained growth in the semiconductor materials market.

Automotive Industry Electrification

The electrification of the automotive industry represents another major driver for semiconductor materials. Electric vehicle (EV) sales in North America are projected to grow by 25% annually through 2027. This surge necessitates advanced semiconductor components, particularly power semiconductors made from silicon carbide (SiC) and gallium nitride (GaN). Similarly, Ford’s commitment to producing 2 million EVs annually by 2026 amplifies demand for related materials. Autonomous driving systems further compound this trend, with sensors and AI processors relying on sophisticated semiconductor architectures. Deloitte estimates that semiconductor content per vehicle will increase by 30% over the next five years, directly benefiting suppliers of wafer fab materials. These developments position the automotive sector as a pivotal force shaping the trajectory of the semiconductor materials market.

MARKET RESTRAINTS

Restraint Supply Chain Vulnerabilities

Supply chain vulnerabilities pose a significant restraint on the semiconductor materials market. Geopolitical tensions and trade restrictions have disrupted the flow of critical raw materials, such as rare earth elements and silicon. China’s dominance in rare earth metal production, controlling a significant portion of global supply, exacerbates risks for North American manufacturers. For instance, export bans during the U.S.-China trade war led to shortages of neodymium, vital for permanent magnets used in semiconductors. Additionally, logistical bottlenecks caused by the pandemic delayed shipments of specialty gases and photoresists, increasing lead times. These disruptions hinder timely project completions, particularly for large-scale fabs. While initiatives like the Critical Minerals Mapping Initiative aim to mitigate dependencies, localized sourcing often entails higher costs, limiting affordability for smaller enterprises.

High Production Costs

High production costs are another critical challenge impacting the industry. Manufacturing semiconductor-grade materials requires stringent purity standards and energy-intensive processes, elevating operational expenses. Additionally, labor shortages in skilled technical roles delay ramp-ups of new facilities. These financial pressures weigh heavily on smaller players, unable to absorb additional expenses. While economies of scale offer some relief, they often come at the expense of reduced flexibility, creating a delicate balance between cost management and innovation.

MARKET OPPORTUNITIES

Expansion of IoT and Edge Computing

The rapid expansion of the Internet of Things (IoT) and edge computing presents a transformative opportunity within the semiconductor materials market. Sensors, microcontrollers, and memory chips form the backbone of IoT devices, driving demand for materials like silicon-on-insulator (SOI) wafers and copper interconnects. Edge computing further amplifies this trend, with hyperscale data centers investing heavily in advanced semiconductors. These innovations ensure a steady pipeline of projects, positioning semiconductor materials manufacturers at the forefront of digital transformation while fostering innovation tailored to emerging demands.

Investments in Quantum Computing

Quantum computing represents another promising avenue for growth in the semiconductor materials market. Governments and private entities are channeling billions into research and development, aiming to harness quantum mechanics for computational breakthroughs. The U.S. Department of Energy allocated 1.2 billion to quantum initiatives in 2022, focusing on superconducting qubits and photonic circuits. These applications require exotic materials like niobium titanium nitride (NbTiN) and sapphire substrates, creating lucrative niches for suppliers. Moreover, quantum computing could generate 850 billion in economic value by 2040, signifying immense potential for semiconductor materials aligned with these cutting-edge technologies.

MARKET CHALLENGES

Intense Competition Among Suppliers

Intense competition among suppliers poses a formidable challenge for participants in the semiconductor materials market. Consolidation among distributors and OEMs has led to downward pressure on pricing, eroding profitability. Smaller firms struggle to compete against larger players, leveraging economies of scale to offer discounted rates. Additionally, counterfeit products flooding the market exacerbate the issue, undermining trust and reducing willingness to pay premium prices for quality goods. This cutthroat environment stifles investment in R&D, hindering innovation and differentiation, ultimately threatening long-term sustainability for mid-tier enterprises.

Regulatory Compliance and Environmental Concerns

Regulatory compliance and environmental concerns present another significant challenge for the industry. Policies mandating reduced carbon emissions and sustainable practices add layers of complexity to manufacturing processes. For instance, California’s Proposition 65 restricts hazardous substances in products, compelling companies to adopt eco-friendly materials. However, transitioning to greener alternatives can elevate operational costs. Additionally, compliance audits and certifications prolong product approval timelines, delaying market entry. These regulatory pressures weigh heavily on smaller players, unable to absorb additional expenses. While beneficial for environmental sustainability, stringent norms inadvertently impede rapid market penetration, creating a delicate balance between innovation and cost management.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 4.03% |

| Segments Covered | By Type, End-Use,e r and Country |

| Various Analyses Covered | Global, Regional, Country-Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | USA, Canada, Mexico, Rest of North America |

| Market Leaders Profiled | Shin-Etsu Chemical Co., Ltd. (Japan), Sumco Corporation (Japan), Samsung Electronics (South Korea), Applied Materials, Inc. (U.S.), Amkor Technology, Inc. (U.S.), JCET Group (China), Dow Inc. (U.S.), Kyocera Corporation (Japan), Tokyo Electron Limited (Japan), Rogers Corporation (U.S.), BASF SE (Germany). are the market players that are dominating the North America semiconductor materials market. |

SEGMENTAL ANALYSIS

By Type Insights

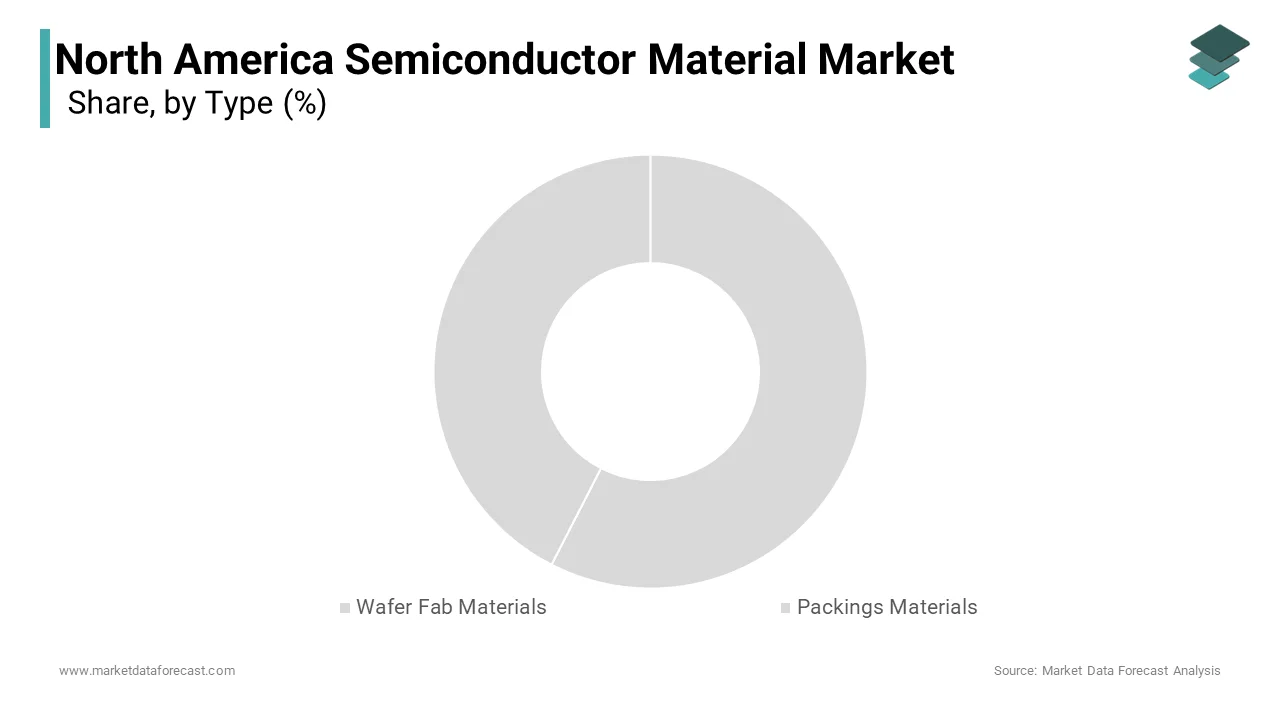

The Wafer fab materials segment dominated the North America semiconductor materials market by capturing 65.8% of total revenue in 2024. This is due to their indispensability in semiconductor fabrication, where purity and precision are paramount. According to SEMI, silicon wafers account for a significant portion of wafer fab material consumption, driven by the proliferation of advanced nodes below 7nm. Intel’s fabs in Arizona and Oregon, for instance, utilize millions of silicon wafers annually to produce cutting-edge CPUs. Specialty gases like nitrogen trifluoride (NF3) and silane are equally critical, with Air Products reporting a significant increase in demand for these materials in 2022.

Packaging materials are experiencing the highest growth rate, with a projected CAGR of 7.8% through 2033. This acceleration is fueled by advancements in chip packaging technologies, such as fan-out wafer-level packaging (FOWLP) and 3D integration. Copper pillars and redistribution layers (RDLs) exemplify this trend; TSMC’s InFO technology, utilized in Apple’s A-series chips, requires extensive quantities of electroplated copper. Similarly, automotive applications adhere to stringent thermal management requirements, necessitating reliable packaging materials like epoxy molding compounds. Canada’s biotech sector relies heavily on automated systems, further boosting demand. Another contributing factor is the rise of heterogeneous integration, where interconnected dies demand flexible, low-latency materials.

By End-User Insights

The consumer electronics segment constituted the largest end-user segment by commanding 40.5% of the North America semiconductor materials market in 2024. This dominance arises from the critical role semiconductors play in enabling functionality across smartphones, tablets, and wearables. For instance, Apple’s M1 chips incorporate over 16 billion transistors, driving demand for silicon wafers and photoresists. Gaming consoles like Sony’s PlayStation 5 further amplify demand, with AMD’s RDNA 2 architecture relying on advanced lithography techniques.

Automotive applications are witnessing the swiftest growth, with a CAGR of 9.2% anticipated through 2033. This trajectory aligns with the burgeoning emphasis on vehicle electrification and autonomous systems. Power semiconductors made from silicon carbide (SiC) and gallium nitride (GaN) are particularly crucial, with Tesla’s Model 3 incorporating SiC-based inverters. Autonomous driving systems further compound this trend, with LiDAR sensors and AI processors relying on sophisticated semiconductor architectures. Technological advancements enabling higher efficiency and lower maintenance costs further accelerate uptake.

COUNTRY ANALYSIS

United States Semiconductor Materials Market Analysis

The United States dominated the North American semiconductor materials market by holding a staggering 80.2% share in 2024. Its dominance stems from unparalleled innovation hubs and progressive policies. Intel's fabs in Arizona and Oregon, along with other facilities, consume a significant amount of materials annually, with the investment costs and material consumption for new fabs in Arizona reaching billions of dollars. Federal funding initiatives, such as the National Science Foundation’s $10 billion allocation for semiconductor R&D, further bolster demand. Regional disparities also influence growth patterns; Texas, home to Samsung’s Austin facility, drives high-purity silicon consumption, while California’s Silicon Valley fosters innovation in advanced packaging. These factors collectively fortify the U.S.’s pole position, reinforcing its role as the epicenter of innovation and consumption within the regional market.

Canada Semiconductor Materials Market Analysis

Canada is contributing notably to overall revenues. The prominence is derived from abundant natural resources and proactive sustainability measures. Quebec's mining sector contributes significantly to North America's silicon feedstock supply, showcasing the importance of robust material infrastructure. Urban centers like Toronto prioritize green building codes, mandating energy-efficient wiring systems.

The Rest of North America is a smaller player in the market. Despite its smaller footprint, this region exhibits remarkable dynamism, buoyed by rapid industrialization and trade agreements. Mexico’s proximity to the U.S. fosters cross-border collaborations. The USMCA agreement facilitates seamless supply chains, enhancing accessibility for manufacturers. Moreover, Mexico’s automotive sector, producing significant amounts of vehicles annually, relies on advanced power and control cables for assembly lines. Renewable energy projects, such as Iberdrola’s Puebla wind farms, further stimulate demand.

COMPETITIVE LANDSCAPE

The North American semiconductor materials market is characterized by intense competition, driven by the presence of established multinational corporations alongside emerging regional players. The competitive landscape is shaped by factors such as technological innovation, pricing pressures, regulatory compliance, and customer preferences. Leading firms like Shin-Etsu Chemical, Sumitomo Chemical, and Air Products dominate the market, collectively accounting for a significant portion of total revenue. However, smaller companies are gaining traction by targeting niche segments and offering cost-effective solutions.

A key aspect of the competition revolves around product differentiation. Established players focus on developing proprietary technologies, such as Shin-Etsu’s high-purity silicon wafers and Sumitomo’s gallium arsenide substrates. These innovations enable them to command premium pricing and secure lucrative contracts. Meanwhile, price wars remain prevalent, especially among mid-tier competitors vying for market share.

Another dimension of competition lies in sustainability. As environmental regulations tighten, companies that fail to adopt eco-friendly practices risk losing market share. Furthermore, digital transformation plays a crucial role, with firms integrating IoT-enabled sensors into production lines for real-time monitoring and predictive maintenance. This trend is particularly evident in advanced packaging and lithography applications, where reliability and performance are paramount.

Despite these challenges, the market remains resilient, supported by robust demand from industries such as consumer electronics, automotive, and telecommunications. Companies that can balance innovation, cost management, and sustainability are likely to emerge as leaders in this dynamic landscape.

KEY MARKET PLAYERS

These are the market players that are dominating the North American semiconductor materials market, including.g

- Shin-Etsu Chemical Co., Ltd. (Japan)

- Sumco Corporation (Japan)

- Samsung Electronics (South Korea)

- Applied Materials, Inc. (U.S.)

- Amkor Technology, Inc. (U.S.)

- JCET Group (China)

- Dow Inc. (U.S.)

- Kyocera Corporation (Japan)

- Tokyo Electron Limited (Japan)

- Rogers Corporation (U.S.)

- BASF SE (Germany).

Top Players In The Market

The North American semiconductor materials market features prominent players like Shin-Etsu Chemical, Sumitomo Chemical, and Air Products. Shin-Etsu is a key player in innovative solutions, including high-purity silicon wafers and photoresists. Sumitomo excels in advanced materials like gallium arsenide and indium phosphide. Air Products leverages its extensive distribution network, serving diverse sectors. Together, these leaders drive technological advancements, setting benchmarks for quality and reliability worldwide.

Top Strategies Used By Key Market Participants

The North American semiconductor materials market is highly competitive, with leading players employing a mix of innovative and strategic approaches to maintain their dominance. These strategies are designed to address challenges such as supply chain disruptions, high production costs, and intense competition while capitalizing on emerging opportunities like IoT, quantum computing, and automotive electrification. Below is an in-depth analysis of the top strategies adopted by key companies operating in this space.

Vertical Integration and Strategic Partnerships

Vertical integration has become a cornerstone for many semiconductor material suppliers, enabling them to control the entire value chain from raw material extraction to finished product delivery. For instance, Shin-Etsu Chemical, one of the largest players in the market, owns mining operations in Japan and North America that supply high-purity quartz and silicon feedstock. This vertical integration allows Shin-Etsu to reduce dependency on third-party suppliers and ensure consistent quality. Additionally, strategic partnerships have gained prominence, particularly with semiconductor manufacturers. Such collaborations not only secure long-term contracts but also enable joint R&D efforts, accelerating innovation. Similarly, Air Products formed a strategic alliance with TSMC to supply specialty gases for its advanced nodes, enhancing customer loyalty and market share.

Focus on Sustainability and Eco-Friendly Solutions

Sustainability has emerged as a key differentiator in the semiconductor materials market, driven by stricter environmental regulations and growing consumer awareness. Leading players are investing heavily in developing eco-friendly alternatives to traditional materials. This initiative aligns with global sustainability goals and appeals to environmentally conscious clients like Apple and Samsung. Similarly, Entegris introduced GreenG, a range of sustainable specialty gases compliant with NFPA standards, catering to the rising demand for green manufacturing processes. These innovations not only enhance brand reputation but also position companies as leaders in sustainable practices, giving them a competitive edge in the market.

Expansion of Manufacturing Facilities and Regional Localization

To meet surging demand and mitigate supply chain vulnerabilities, major players are expanding their manufacturing capacities through greenfield investments or upgrades to existing plants. By integrating Praxair’s operations, Linde achieved cost efficiencies and improved its ability to serve key clients. Regional localization not only reduces lead times and transportation costs but also ensures compliance with procurement mandates, thereby strengthening the competitive edge of these companies.

RECENT MARKET NEWS

- In April 2023, Shin-Etsu Chemical launched EcoSilicon, a revolutionary line of recyclable silicon wafer-reducing material waste by 25%. This initiative strengthened its reputation as an innovator and positioned it as a preferred supplier for eco-conscious clients.

- In June 2023, Sumitomo Chemical partnered with Intel to co-develop advanced gallium arsenide substrates for 5G applications. This collaboration enabled both companies to secure multi-billion-dollar contracts, addressing the growing demand for high-frequency semiconductors.

- In August 2023, Air Products unveiled GreenGas, a line of sustainable specialty gases compliant with NFPA standards. These gases cater to the rising demand for environmentally friendly manufacturing processes, appealing to tech giants like Apple and Samsung.

- In October 2023, Linde acquired Praxair’s U.S. assets for $7 billion, expanding its footprint in the North American market. This acquisition streamlined operations and enhanced access to key clients in the semiconductor industry.

- In December 2023, Entegris invested $1 billion in a new facility in Texas, focusing on advanced filtration systems for semiconductor fabs. This expansion underscored Entegris’ commitment to meeting regional demand effectively.

MARKET SEGMENTATION

This research report on the North American semiconductor materials market is segmented and sub-segmented into the following categories.

By Type

- Wafer Fab Materials

- Silicon

- Photoresist

- Photomasks

- Chemicals

- CMP

- Gases

- Silicon-On-Insulator (SOI)

- Targets

- Packaging Materials

- Lead frames

- Substrates

- Bonding Wire

- Die Attach

- Mold Compounds

- Encapsulants

- Ceramic Packages

- Other Packaging Materials

By End-user

- Consumer Electronics

- Automotive

- Telecommunications

- Industrial

- Healthcare

- Aerospace and Defense

- Others (Energy and Utilities)

By Country

- The USA

- Canada

- Mexico

Frequently Asked Questions

What is the North America semiconductor materials market?

The North America semiconductor materials market covers materials used to make chips, including wafers, chemicals, gases, and packaging materials.

What drives growth in the North America semiconductor materials market?

Growth is fueled by rising chip demand in electronics, EVs, AI systems, and advanced manufacturing.

Why is the North America semiconductor materials market important?

It supports domestic chip production, strengthens supply chains, and boosts technological competitiveness.

Which materials dominate the North America semiconductor materials market?

Silicon wafers, photoresists, specialty chemicals, and CMP slurries are the most widely used.

Which industries use the North America semiconductor materials market the most?

Consumer electronics, automotive, telecom, and data centers heavily depend on semiconductor materials.

What challenges affect the North America semiconductor materials market?

High production costs, supply chain constraints, and dependence on imported raw materials.

How is government support shaping the North America semiconductor materials market?

Programs like the CHIPS Act encourage local manufacturing and reduce reliance on overseas suppliers.

Which countries dominate the North America semiconductor materials market?

The U.S. leads strongly, followed by Canada and Mexico with growing electronics manufacturing activity.

How do electric vehicles impact the North America semiconductor materials market?

EVs require advanced chips, boosting demand for high-performance semiconductor materials.

What technological trends shape the North America semiconductor materials market?

AI chips, smaller nodes, EUV lithography, and advanced packaging are driving material innovation.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com