North America Silk Market Research Report Based on Type (Mulberry silk, Tussar silk, Eri silk), Application (Textile, Cosmetics, Medical), and Country (The U.S., Canada and Rest of North America) – Analysis on Size, Share, Trends, & Growth Forecast (2026 to 2034)

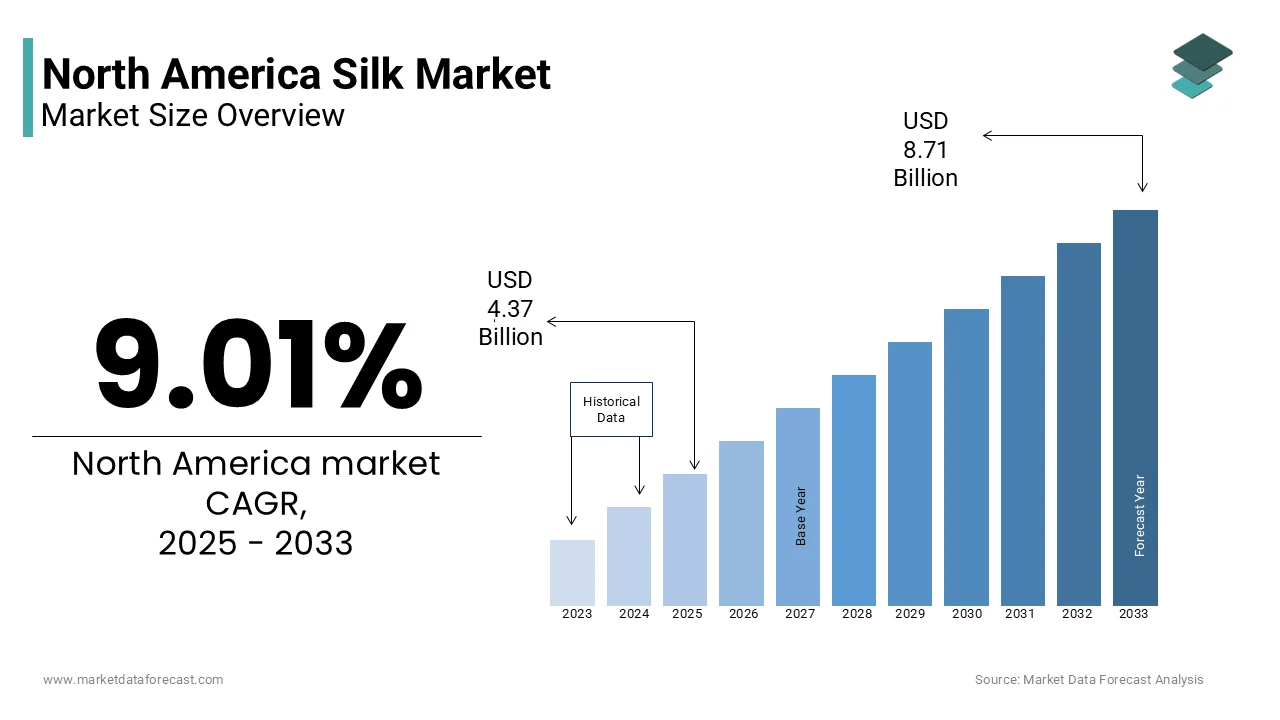

Market Size, 2025

$4.36 BnMarket Estimate, 2026

$4.75 BnMarket Forecast, 2034

$9.47 BnCAGR, 2026–2034

9.01%North America Silk Market Size

The North American silk market size was worth USD 4.36 billion in 2025 and is anticipated to reach a valuation of USD 9.47 billion by 2034 from USD 4.75 billion in 2026, growing at a CAGR of 9.01% during the forecast period.

Silk, a protein-based natural fibre produced mainly by the Bombyx mori silkworm, remains a premium material due to its tensile strength, biocompatibility, and lustrous finish. Despite limited domestic sericulture, the region maintains a robust demand driven by fashion industries and advanced material research. Silk is known as the "Queen of Textiles," and is prized for its shimmering lustre, soft feel, and elegant drape. It is also one of the strongest natural fibres and possesses excellent properties, including breathability and thermal regulation, which help keep the wearer cool in warm weather and warm in cool weather. As per the Textile Exchange, silk accounts for less than 0.2% of global fibre production, yet commands a disproportionately high value in speciality segments, particularly in medical sutures and cosmetic formulations, where its biodegradability and hypoallergenic properties are increasingly leveraged.

MARKET DRIVERS

Sustainable Textiles Driving North America Silk Demand

The escalating demand for sustainable and biodegradable textiles in the luxury fashion sector is driving the North American silk Market growth. Consumers are increasingly favouring eco-conscious materials, with silk emerging as a preferred alternative to synthetic fibres due to its renewable origin and low environmental footprint during decomposition. According to the Sustainable Apparel Coalition, more than half of high-income consumers in the U.S. and Canada consider environmental impact when purchasing luxury garments. As per the American Association of Textile Chemists and Colourists, Silk, unlike polyester, which persists in landfills for centuries, degrades within 1–3 years under composting conditions. Furthermore, luxury brands such as Stella McCartney and Ralph Lauren have integrated certified silk into their collections is citing traceability and sustainability.

Biomedical Uses Accelerating Silk Market Expansion

Another significant driver is the expanding application of silk fibroin in biomedical and biotechnological fields. Silk’s unique protein structure offers exceptional mechanical strength, biocompatibility, and controlled biodegradability, making it ideal for advanced medical devices. According to the National Institutes of Health, silk-based scaffolds are being used in over 45 clinical trials globally for tissue engineering, including nerve regeneration and cartilage repair. In the U.S., the Food and Drug Administration has cleared more than 12 silk-based medical products since 2015, including sutures, wound dressings, and drug delivery matrices. Researchers at Tufts University have demonstrated that silk fibroin can stabilise vaccines without refrigeration, a breakthrough with implications for thermostable pharmaceuticals. As per the Biomedical Engineering Society, the global market for silk-derived biomaterials is expanding at a compound annual growth rate of 9.3%, with North America accounting for nearly 40% of R&D investment. This scientific validation is catalysing institutional adoption and venture funding, further entrenching silk’s role beyond textiles.

MARKET RESTRAINTS

Ethical Concerns Over Conventional Sericulture Practices

The ethical and animal welfare concerns associated with conventional sericulture are significantly restraining the North American Silk Market. Traditional silk harvesting involves boiling silkworm pupae alive to extract continuous fibres, which is a process criticised by animal rights organisations. According to a 2023 survey conducted by the Humane Society of the United States, half of the American consumers expressed discomfort with this practice, which is prompting a shift toward alternatives like peace silk (Ahimsa silk) or synthetic substitutes. However, Ahimsa silk, which allows moths to emerge before fibre collection, yields shorter, less uniform fibres is reducing its commercial viability. As per the Global Fashion Agenda, only 5% of silk-labelled products in North America are verified as ethically sourced. The certification bodies like PETA have listed conventional silk as non-vegan is influencing major retailers such as Nordstrom and Macy’s to restrict or label silk products more transparently. This growing scrutiny limits market expansion, particularly among a younger, ethically driven population.

Climate Risks and Supply Chain Instability Limit Growth

The vulnerability of silk supply chains to climate variability and agricultural instability is another factor hindering the North American Silk Market's growth. Silk production is highly dependent on mulberry cultivation and silkworm rearing, both sensitive to temperature, humidity, and pest outbreaks is limiting the market growth. According to the Food and Agriculture Organisation, a 1.5°C rise in average temperature can reduce cocoon yield by up to 20%, as observed in Karnataka, India, the world’s largest silk-producing region during the 2022 heatwave. Droughts and erratic monsoon patterns have led to a decline in raw silk output in India between 2021 and 2023, directly affecting export availability to North America. The U.S. International Trade Commission confirms that import lead times for raw silk have increased by an average of 18 days due to production delays. Moreover, the absence of scalable domestic sericulture in North America exacerbates dependency on volatile international sources.

MARKET OPPORTUNITIES

Biotechnology Advancements Creating New Silk Materials

The development of recombinant silk proteins through biotechnology is creating opportunities for the growth of the North American silk Market. Companies such as Bolt Threads and Spiber Inc. are engineering microbial fermentation processes to produce synthetic spider silk, bypassing the need for silkworms. For instance, Evolved by Nature, which produces fermentation-derived "Activated Silk” and is based in North America, announced in 2022 that it was working toward a production capacity of 900 metric tons per year. These bioengineered silks offer superior tensile strength up to five times that of natural silk and can be customised for specific applications. In 2022, Adidas and The North Face launched limited-edition apparel using Microsilk, a yeast-fermented silk analogue is signalling commercial viability. This innovation reduces ethical concerns,s and supply chain risks is positioning North America as a leader in next-generation silk materials.

Growing Demand for Silk in Wearables and Smart Textiles

The integration of silk in wearable health technology and smart textiles provides emerging opportunities for the growth of the North American Silk Market. Silk’s dielectric properties, flexibility, and ability to support embedded electronics make it ideal for biocompatible sensors. Researchers at the University of Illinois have developed silk-based epidermal electronics that monitor vital signs with clinical accuracy. According to the IEEE Transactions on Biomedical Engineering, silk substrates enable transient electronics that dissolve harmlessly after use, reducing medical waste. As per the National Science Foundation report, funding for silk-integrated wearable projects has increased by 33% since 2020. Silk’s role as a foundational material in this sector offers substantial growth potential for North American innovators and manufacturers.

MARKET CHALLENGES

Lack of Traceability Undermines Trust in Silk Sourcing

The lack of standardised traceability and transparency in silk sourcing is posing significant challenges in the growth of the North American silk Market. Unlike organic cotton or wool, silk lacks a unified certification framework in the region is leading to widespread mislabeling and greenwashing is enhancing the market growth. The absence of blockchain-enabled tracking or DNA-based authentication complicates verification. As per the Textile Fibre Products Identification Act, it does not mandate origin disclosure for imported silk, which is creating loopholes. As per the International Sericulture Commission, only a few per cent of silk entering the U.S. is accompanied by verifiable production data. This opacity undermines consumer trust and hinders premium pricing, especially as demand for ethical luxury intensifies. Without regulatory harmonisation and investment in digital traceability, the market risks reputational erosion and stagnation.

High Production Costs Restrict Silk’s Market Expansion

The high cost of production and processing, which limits silk’s accessibility beyond niche markets, is another major challenge limiting the North American Silk Market. Natural silk requires labour-intensive rearing, harvesting, and degumming processes, contributing to elevated prices. As per the American Chemical Society, the energy-intensive degumming phase, which removes sericin using boiling alkali solutions, accounts for nearly 30% of total processing costs. The skilled labour for hand-weaving and finishing is scarce in North America, leading to an increasing reliance on offshore manufacturing. According to the National Council of Textile Organisations, domestic silk garment production requires 4.7 times more labour hours than synthetic alternatives. These economic barriers restrict scalability and discourage mass-market adoption is confining silk to high-margin, low-volume segments despite its functional advantages.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 9.01% |

| Segments Covered | By Type, Application, Region. |

| Various Analyses Covered | Global, Regional andCountry-Levell Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | United States, Canada, Mexico |

| Market Leaders Profiled | Silk Road Collection, Mulberry Park Silks, Dharma Trading Co., Silk Baron, Harts Fabric, Thai Silks, Fine Silks, Valley Forge Fabrics, Thai Silk Magic, Mood Fabrics, and Others. |

SEGMENTAL ANALYSIS

By Type Insights

Mulberry silk dominated the North American Silk Market with a significant share in 2025. The presence of superior quality, consistent texture, and widespread acceptance in luxury textile manufacturing is majorly boosting the segment growth. The primary driver of segment growth is consumer preference for high-lustre, smooth fabrics in premium apparel and home textiles. As per the National Retail Federation, more than half of luxury sleepwear and women’s blouses sold in high-end U.S. department stores are made from 100% Mulberry silk, which is fueling its entrenched position in fashion. According to as noted by the American Association of Textile Chemists and Colourists, fibre’s compatibility with digital printing and dyeing processes enhances its appeal among designers, which confirms its colour-fastness rating exceeds that of wild silks by up to 30%.

The Eri silk segment is estimated to register at a CAGR of 9.8% between 2026 to 2034 in the North America Silk Market. This acceleration is primarily fueled by its ethical production method, which allows the silkworm to complete its life cycle before fibre extraction is aligning with rising vegan and cruelty-free consumer values. According to a 2023 Humane Society of the United States report, more than half of millennial and Gen Z consumers in North America actively avoid products involving animal harm is making Eri silk a compelling alternative. As per the Fibre Industry Association of North America, Eri silk usage in sustainable fashion brands increased around 65% between 2021 and 2023, with labels like Pact and Tentree incorporating it into seasonal collections. Furthermore, its thermal-regulating properties retain warmth in winter and remain breathable in summer is making it ideal for activewear and infant clothing. It is found that Eri fabric maintains 18% better moisture wicking than Mulberry silk under controlled conditions.

By Application Insights

The textile application segment led the North America Silk Market with a significant share in 2025. The enduring demand for silk in high-end fashion, lingerie, and bedding, where tactile luxury and brand prestige are paramount, is driving the segment growth. The growing consumer inclination toward premium sleep wellness products fuels the segment expansion. As per the Consumer Technology Association, sales of silk pillowcases and sleep masks surged annually between 2020 and 2023, driven by dermatological claims of reduced facial friction and hair breakage. As per the American Academy of Dermatology, clinical studies showing that silk reduces transepidermal water loss by 40% compared to cotton are reinforcing its appeal in beauty-adjacent textiles. The luxury fashion houses such as Tom Ford and Burberry continue to prioritise silk in their seasonal lines, with wear collections incorporating silk.

The medical application segment is emerging as the fastest-growing by registering a CAGR of 11.3% from 2026 to 2034 in the North America Silk Market. The rapid expansion is propelled by silk fibroin’s increasing use in regenerative medicine and implantable devices, leading to segment growth. One prominent driver is its FDA-approved status for surgical sutures, with over 8 million silk-based sutures used annually in the U.S. Beyond sutures, silk is being engineered into scaffolds for tissue regeneration. Researchers at the Cleveland Clinic have developed silk-based meniscus implants currently in Phase III trials, demonstrating 90% biocompatibility and structural integration in human subjects. Moreover, silk’s ability to stabilise labile drugs and vaccines is enabling room-temperature storage, which has attracted pharmaceutical partnerships, including one with Merck & Co., by accelerating commercialisation in drug delivery systems.

REGIONAL ANALYSIS

United States Market Analysis

The United States was the top performer in the North American Silk Market with a significant share in 2025. The nation’s dominance is due to its vast luxury retail infrastructure, advanced biomedical research ecosystem, and high per capita spending on premium textiles. Hundreds of speciality silk retailers operating nationwide, including e-commerce platforms like Slip and Cuyana, in the U.S. have cultivated a sophisticated consumer base willing to pay a premium price for a silk pillowcase set. The country also leads in medical silk innovation, housing most of North America’s silk-based biotech firms, including FibroBiologics and Evolved by Nature. According to the National Science Foundation, U.S. institutions filed patents related to silk biomaterials in 2022 alone is reinforcing their technological edge. The convergence of fashion demand and scientific advancement solidifies the U.S. as the central hub for silk consumption and innovation.

Canada Market Analysis

Canada held a prominent share by accounting for 9.5% in the North American silkarket between 2026 and 2034. The country’s market status is characterised by steady demand in sustainable luxury fashion and a growing interest in ethical textiles. Canadian consumers exhibit a strong preference for traceable, eco-friendly materials, with more than half willing to pay a premium for certified sustainable apparel. This has led to increased adoption of Eri and peace silk by domestic brands such as Encircled and Tentree. Moreover, Canada’s publicly funded healthcare system is exploring silk-based wound care solutions to reduce long-term treatment costs. The Canadian Institutes of Health Research funded a 2022 trial at the University of British Columbia demonstrating that silk-chitosan dressings accelerated diabetic ulcer healing by 35% compared to conventional gauze is signalling potential for broader medical integration.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

A few of the notable players in the North American silk market include

- Silk Road Collection

- Mulberry Park Silks

- Dharma Trading Co.

- Silk Baron

- Harts Fabric

- Thai Silks

- Fine Silks

- Valley Forge Fabrics

- Thai Silk Magic

- Mood Fabrics

- Others

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

Key players in the North American silk market are deploying innovation-driven strategies to consolidate their positions. Leading companies are investing heavily in biotechnology to develop recombinant silk proteins, reducing dependency on traditional sericulture. Strategic partnerships with academic institutions and healthcare organisations are accelerating clinical validation of silk-based medical devices. Firms are also expanding vertically by integrating R&D, manufacturing, and commercialisation under one ecosystem to enhance control over quality and scalability. Another prevalent strategy is securing government grants and private funding to support sustainable production methods. The brands are emphasising traceability and eco-certifications to appeal to ethically conscious consumers. Mergers with biotech startups and entry into hybrid applications such as smart textiles and wearable health sensors are further strengthening competitive advantage across both luxury and scientific domains.

COMPETITION OVERVIEW

The competition in the North American silk Market is intensifying as traditional textile suppliers face disruption from biotech innovators and sustainable fashion brands. Unlike conventional markets dominated by importers and fabric distributors, North America’s landscape is increasingly shaped by science-led enterprises developing high-performance silk alternatives. Companies are competing not on volume but on technological differentiation, regulatory approvals, and sustainability credentials. The absence of large-scale domestic sericulture has created an opening for bioengineered silk producers to capture premium segments. Smaller niche players focus on ethical sourcing and artisanal branding, while larger firms leverage institutional partnerships and federal funding. Intellectual property, particularly in protein engineering and medical applications, has become prominent. As consumer and regulatory demands evolve, competitive advantage is shifting toward innovation, traceability, and cross-sector adaptability.

TOP PLAYERS IN THE MARKET

- Evolved by Nature, headquartered in Massachusetts, is a pioneering biomaterials company transforming the North American silk market through its proprietary Activated Silk™ platform. The company leverages recombinant silk protein technology to produce sustainable, biocompatible materials for luxury textiles and medical applications. In recent years, it has deepened its collaboration with major fashion brands such as Stella McCartney and Capri Holdings to integrate silk-infused fabrics into high-performance apparel. In 2023, Evolved by Nature launched a scalable production facility in Albany, New York, by enabling commercial-grade output of liquid silk for cosmetics and wound care. Its partnership with the U.S. Department of Energy’s BioDesign Institute has accelerated R&D in carbon-negative textile processing is positioning the company at the forefront of clean bio-manufacturing in the North American silk landscape.

- FibroBiologics, based in Texaspecialiseszes in medical-grade silk biomaterials for regenerative therapies and implantable devices. The company has advanced silk fibroin into clinical-stage applications, which include orthopaedic scaffolds and neural repair matrices. In 2022, FibroBiologics initiated a Phase II trial for a silk-based meniscus regeneration implant is supported by a grant from the National Institutes of Health. It has also established a strategic alliance with Mayo Clinic to explore silk’s role in reducing post-surgical inflammation. By focusing on FDA-regulated medical innovations, FibroBiologics has differentiated itself from traditional silk suppliers. In early 2025, the company expanded its GMP-compliant manufacturing unit in Dallas is aiming to meet rising demand from biotech partners. Its science-driven approach reinforces North America’s shift toward high-value, non-textile silk applications.

- Bolt Threads, a California-based biotechnology firm, has redefined silk innovation through its Microsilk product, which is a lab-engineered protein mimicking spider silk. Utilising yeast fermentation, the company produces sustainable, animal-free silk without relying on silkworms, addressing ethical and supply chain concerns. In 2021, Bolt Threads partnered with Adidas and The North Face to release performance apparel made from Microsilk is demonstrating commercial feasibility. Although it paused large-scale textile production in 2023 to refocus on high-margin biomedical and cosmetic applications, the company secured millions of investments from the U.S. in June 2025 for silk-based drug delivery systems. This initiative enhances its strategic emphasis on advanced material science and regulatory-grade outputs by reinforcing its growth in next-generation silk solutions.

North America Silk Market News

- In 2022, Evolved by Nature, a biotechnology company known for its Activated Silk™ platform, expanded its commercial footprint and partnerships. Evolved by Nature has formed partnerships with various companies to integrate its sustainable silk technology into new product lines, including in personal care and textiles.

- In August 2025, Bolt Threads completed a business combination with a special purpose acquisition company (SPAC), Golden Arrow Merger Corp, and became a publicly traded company on Nasdaq.

- In April 2025, Evolved by Nature showcased two new ingredients, Activated Silk™ 33B and Activated Silk™ 27P, at a trade show in New York City, which may be the source of the user's confusion about a New York-based event.

MARKET SEGMENTATION

This research report on the North American silk market has been segmented and sub-segmented into the following categories.

By Type

- Mulberry silk

- Tussar silk

- Eri silk

By Application

- Textile

- Cosmetics

- Medical

By Country

- United States

- Canada

- Mexico

- Others

Frequently Asked Questions

1. What is driving the growth of the North America silk market?

Key drivers include rising demand for sustainable luxury textiles, increasing use of silk in biomedical applications, and growth in eco-conscious fashion purchasing.

2. Which countries dominate the North America silk market?

The United States leads the market, followed by Canada, due to strong luxury apparel sectors and active R&D in silk-based biomaterials.

3. What industries primarily use silk in North America?

Silk is widely used in luxury apparel, home furnishings, cosmetics, biomaterials, medical devices, and smart textiles.

4. Why is silk considered a sustainable textile?

Silk is biodegradable, renewable, and has a lower environmental footprint compared to synthetic fibers, making it appealing to eco-conscious consumers.

5. What are the major restraints in the North America silk market?

Ethical concerns about sericulture, limited ethical certifications, and high production costs are major challenges.

6. What opportunities exist for silk in North America?

Biotechnology-driven recombinant silk, silk-based biomaterials, and smart wearables offer strong future growth opportunities.

7. Is silk used in medical and biomedical applications?

Yes. Silk fibroin is increasingly used in tissue engineering, wound dressings, sutures, drug delivery systems, and regenerative medicine.

8. What is the consumer trend toward ethical silk products?

Demand for Ahimsa silk (peace silk) and certified sustainable silk is rising due to growing animal welfare awareness.

9. How is climate variability affecting the North America silk supply?

Dependence on international suppliers—especially China and India—exposes North America to climate-driven production disruptions.

10. What role does recombinant or lab-grown silk play in the market?

Lab-grown spider silk and bioengineered silk fibers are emerging as scalable alternatives with superior performance properties.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com