North America Speed Sensor Market Size, Share, Trends & Growth Forecast Report By Type (Hall Effect Speed Sensor, Variable Reluctance Speed Sensor, RF [Inductive] Speed Sensor, Magnetoresistive Speed Sensor), Industry Vertical (Automotive, Aerospace & Defense, Consumer Electronics, Medical), and Country (United States, Canada, Mexico, Rest of North America) – Industry Analysis, 2026 to 2034

Market Size, 2025

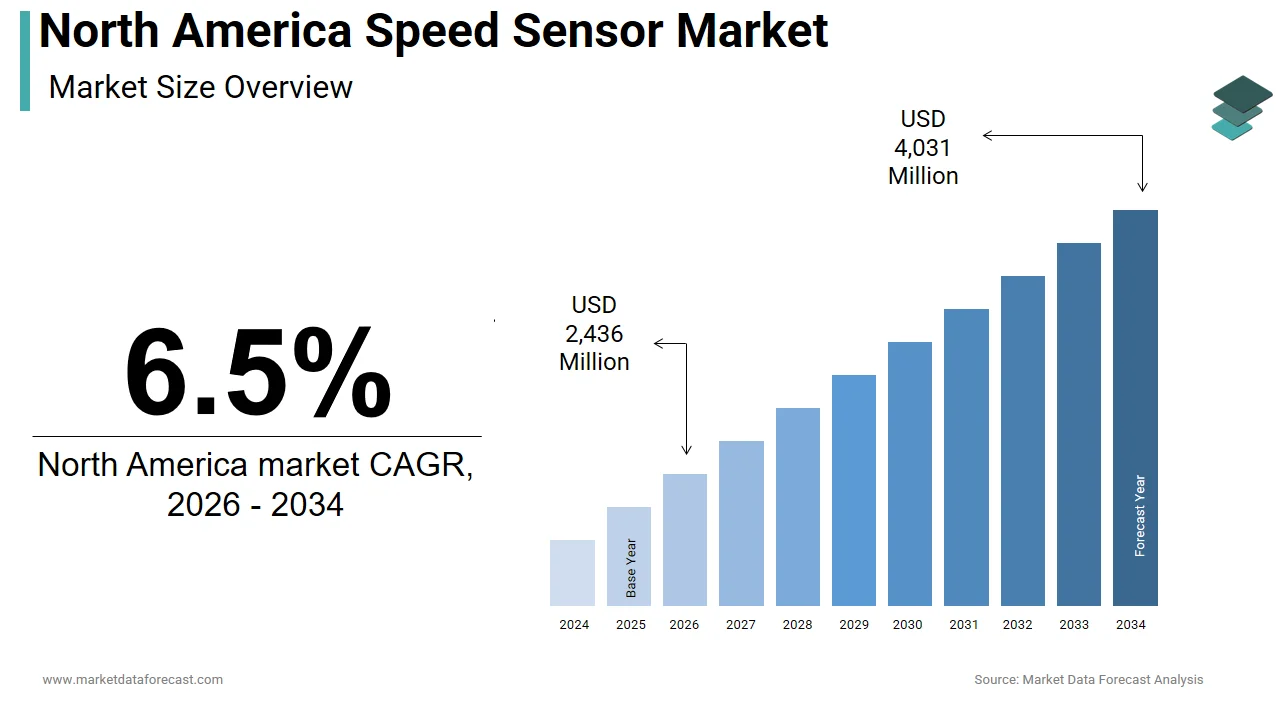

$2,287 MnMarket Estimate, 2026

$2,436 MnMarket Forecast, 2034

$4,031 MnCAGR, 2026–2034

6.5%North America Speed Sensor Market Size

The size of the North America speed sensor market was worth USD 2,287 million in 2025. The regional market is anticipated to grow at a CAGR of 6.5% from 2026 to 2034 and be worth USD 4,031 million by 2034 from USD 2,436 million in 2026.

A speed sensor is an electronic device used to measure rotational or linear velocity in various mechanical systems. These sensors are extensively deployed across automotive, industrial automation, aerospace, rail transport, and energy generation sectors to ensure precision, safety, and efficiency. The U.S. remains the largest contributor to this regional market due to its robust automotive industry and widespread adoption of smart manufacturing practices. Speed sensors play a crucial role in enhancing vehicle performance and ensuring compliance with emissions standards. As per Environment and Climate Change Canada, over 80% of new vehicles registered in 2023 featured advanced driver-assistance systems (ADAS), many of which rely on speed sensors for functions such as anti-lock braking, cruise control, and traction management. Additionally, industrial applications including robotics and turbine monitoring further expand the scope of speed sensor usage.

MARKET DRIVERS

Growth in Automotive Electrification and Advanced Driver-Assistance Systems (ADAS)

The rapid growth of electric vehicles (EVs) and the increasing integration of advanced driver-assistance systems (ADAS) are propelling the growth of the North America speed sensor market. Speed sensors are essential components in EV drivetrains, where they monitor rotor speeds to optimize energy efficiency and battery management. According to the U.S. Department of Energy, EV sales in the United States increased by 50% in 2023 compared to the previous year, signaling a major shift in automotive technology that directly benefits the speed sensor industry. Moreover, ADAS technologies such as adaptive cruise control, lane-keeping assist, and automatic emergency braking depend heavily on accurate speed data from multiple sensors throughout the vehicle. The National Highway Traffic Safety Administration (NHTSA) reported that over 90% of new passenger vehicles sold in 2023 included at least one form of ADAS feature, up from 70% in 2021.

Expansion of Industrial Automation and Smart Manufacturing

Industrial automation and the proliferation of smart manufacturing processes are also expected to drive the growth of the North America speed sensor market. Speed sensors are integral to the operation of automated production lines, conveyor belts, robotic arms, and CNC machines, where precise motion control enhances productivity and reduces mechanical wear. According to the Association for Advancing Automation, investments in factory automation equipment in North America rose by 11% in 2023, which reflects a strong commitment to digital transformation across the manufacturing sector. In addition to traditional manufacturing, industries such as pharmaceuticals, food processing, and logistics have increasingly adopted automated solutions requiring real-time speed monitoring. Furthermore, government initiatives supporting reshoring and domestic manufacturing resilience have encouraged companies to upgrade their facilities with intelligent machinery. The Canadian Manufacturers & Exporters association noted that Canadian firms invested nearly $12 billion in automation upgrades in 2023 alone.

MARKET RESTRAINTS

High Cost of Advanced Speed Sensing Technologies

The high cost associated with advanced sensing technologies is limiting the growth of the North America speed sensor market. High-performance speed sensors, particularly those used in aerospace, defense, and precision manufacturing, incorporate complex materials, embedded microprocessors, and specialized calibration processes, all of which contribute to elevated price points. This financial barrier is particularly pronounced for small and medium-sized enterprises (SMEs) that may lack the capital required for large-scale sensor deployment. A survey by the National Association of Manufacturers found that nearly 55% of SMEs cited equipment costs as a limiting factor when upgrading to automated systems. While long-term operational savings and improved efficiency justify these investments, the initial outlay discourages rapid adoption among budget-conscious operators.

Complexity in Integration with Legacy Systems

The difficulty associated with integrating modern speed sensing technologies into legacy industrial and transportation systems also hinders the growth of the North America speed sensor market. Many manufacturing plants, rail networks, and older vehicle fleets still operate on outdated control architectures that were not designed to accommodate digital sensor inputs or real-time data analytics. According to a white paper published by the Industrial Internet Consortium, approximately 60% of industrial equipment installed before 2015 lacks compatibility with current IoT-enabled sensor systems. The U.S. Department of Transportation reported that several railway operators faced delays in implementing positive train control (PTC) systems due to challenges in integrating modern speed and location sensors with older locomotive designs. Additionally, the need for skilled technicians to manage integration and calibration adds another layer of complexity. A study by the Manufacturing Institute revealed that workforce shortages in automation and electronics hindered the adoption of sensor-based technologies in over 40% of surveyed manufacturing firms.

MARKET OPPORTUNITIES

Rising Demand for Predictive Maintenance in Industrial Applications

The growing adoption of predictive maintenance strategies across industrial operations. Traditional reactive and preventive maintenance approaches are being replaced by condition-based monitoring systems that utilize real-time data from speed sensors to anticipate equipment failures before they occur. Industries such as oil and gas, power generation, and heavy machinery are investing in vibration and speed monitoring solutions to enhance asset reliability. As per the Electric Power Research Institute (EPRI), over 65% of utility companies in the U.S. had implemented or planned to implement predictive maintenance tools by the end of 2023. Moreover, the convergence of speed sensing with artificial intelligence and cloud computing is enabling smarter diagnostics and remote monitoring capabilities. Companies like Siemens, Honeywell, and Rockwell Automation are actively developing integrated solutions that combine speed data with machine learning algorithms to generate actionable insights.

Expansion of Renewable Energy Infrastructure

The accelerating development of renewable energy infrastructure is a substantial growth opportunity for the North America speed sensor market. Wind and hydroelectric power generation systems require highly accurate speed sensors to regulate turbine rotation and optimize energy output. According to the U.S. Department of Energy, wind energy accounted for nearly 12% of total electricity generation in the U.S. in 2023, with over 15 gigawatts of new capacity added during the year. Wind turbines rely on speed sensors to maintain optimal blade rotation speeds under varying wind conditions. Hydroelectric plants also benefit from speed monitoring technologies, particularly in variable-speed pumped storage systems that adjust turbine speeds based on grid demand.

MARKET CHALLENGES

Rapid Technological Obsolescence and Short Product Lifecycles

The rapid pace of technological obsolescence, which results in shorter product lifecycles and increased pressure on manufacturers to continuously innovate, is limiting the growth of the North America speed sensor market. Sensor technologies must keep up with advancements in connectivity, miniaturization, and data processing capabilities. This accelerated innovation cycle poses challenges for both manufacturers and end-users. Equipment suppliers must invest heavily in research and development to stay ahead of emerging trends, while customers face the dilemma of purchasing products that may become obsolete within a few years. Additionally, the transition from analog to digital sensor interfaces has created compatibility issues with legacy systems, which require additional engineering efforts for seamless integration.

Regulatory Compliance and Standardization Gaps Across Industries

The regulatory compliance and the lack of universal standards for speed sensor specifications present a growing challenge for market participants in North America. According to the International Organization for Standardization (ISO), over 20 different national and international standards apply to speed sensor applications, complicating product development and market entry. For example, the automotive sector adheres to ISO 2631 for vibration measurement, while the aerospace industry follows RTCA DO-160 for avionics certification. These variations force manufacturers to produce customized sensor variants for different applications, increasing costs and development timelines. Additionally, the absence of harmonized calibration protocols creates inconsistencies in accuracy and reliability assessments.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Industry Vertical, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | United States, Canada, Mexico, Rest of North America |

| Market Leaders Profiled | Rockwell Automation, Inc., ABB, NXP Semiconductors, STMicroelectronics, Infineon Technologies AG, Schneider Electric, Smith Systems, Inc., HYDAC Technology Corporation, Micro-Epsilon, Texas Instruments Incorporated, Continental AG, Bosch Engineering, Motion Sensors, Inc., Rechner Sensors, and Honeywell International Inc. |

SEGMENTAL ANALYSIS

By Type Insights

The hall Effect speed sensors segment was the largest and held 39.6% of the North America speed sensor market share in 2024, with their ability to provide accurate digital output signals without mechanical wear. The growing integration of electronic control systems in modern vehicles. As per data from the U.S. Department of Transportation, over 90% of new passenger vehicles sold in 2023 included advanced driver-assistance systems (ADAS), many of which rely on Hall Effect sensors for real-time rotational speed monitoring. Additionally, these sensors are preferred for their immunity to dust and vibration, making them ideal for use in harsh environments such as off-road equipment and manufacturing automation.

The magnetoresistive speed sensors segment is projected to grow with an expected CAGR of 11.6% in the next coming years. The rising demand for autonomous and semi-autonomous vehicles, which require highly precise speed measurement for navigation, obstacle detection, and adaptive control systems is ascribed to bolster the growth of the segment. The National Highway Traffic Safety Administration noted that nearly all Level 3 and above autonomous prototypes tested in North America in 2023 utilized magnetoresistive technology for wheel and shaft speed monitoring. Additionally, industrial sectors such as aerospace, robotics, and renewable energy are adopting magnetoresistive sensors for turbine monitoring and precision motion control.

By Industry Vertical Insights

The automotive industry dominated the North America speed sensor market with a 46.3% share in 2024. Speed sensors play a crucial role in modern vehicles, supporting functions such as transmission control, ABS, traction control, cruise control, and engine management. The widespread adoption of advanced driver-assistance systems (ADAS) is also expected to fuel the growth of the segment. The National Highway Traffic Safety Administration reported that over 90% of new vehicles registered in 2023 featured some form of ADAS functionality, many of which depend on speed sensors for real-time data input. Furthermore, government regulations mandating enhanced vehicle safety features have accelerated the integration of multi-sensor systems in both conventional and electric vehicles. Additionally, the rise of electric mobility has significantly increased sensor requirements per vehicle. The U.S. Department of Energy indicated that each electric vehicle incorporates an average of 8–12 speed sensors to monitor motor rotation, battery efficiency, and regenerative braking performance.

The industrial segment is anticipated to grow with a CAGR of 10.9% in the coming years, with the increasing adoption of automation, smart manufacturing, and condition-based maintenance strategies across production facilities. The implementation of Industry 4.0 technologies, including IoT-enabled sensors, real-time analytics, and machine learning-based diagnostics, is levelling up the growth of the segment. Furthermore, industries like oil and gas, power generation, and logistics are investing heavily in asset health monitoring to reduce unplanned downtime and improve operational efficiency. The Electric Power Research Institute (EPRI) reported that more than 60% of utility companies in the U.S. had integrated real-time speed monitoring into their turbine maintenance protocols by the end of 2023.

COUNTRY-LEVEL ANALYSIS

United States Speed Sensor Market Insights

The United States was accounted in holding 82.1% of the North America speed sensor market share in 2024, with the country’s robust automotive industry, extensive industrial automation infrastructure, and growing emphasis on electric mobility. According to the U.S. Department of Commerce, the transportation equipment manufacturing sector recorded a 6.4% increase in capital investment in 2023, reinforcing demand for precision sensing technologies. The industrial sector is also expanding its reliance on speed sensors for predictive maintenance and process optimization.

Canada Speed Sensor Market Insights

Canada was positioned second in the North America speed sensor market by accounting for 14.3% of the share in 2024. The country’s market expansion is primarily fueled by investments in aerospace engineering, railway modernization, and industrial automation initiatives. The aerospace industry in Quebec and Ontario, where several aircraft component manufacturers operate. The Canadian Space Agency and Bombardier Aerospace have been integrating advanced speed monitoring systems in avionics and propulsion units, aligning with global trends in flight safety and efficiency. Additionally, Transport Canada’s push for positive train control (PTC) systems has led to increased adoption of speed sensors in locomotives and rail signaling networks. Industrial automation is another significant growth area. The Canadian Manufacturers & Exporters association reported that over $12 billion was invested in automation upgrades in 2023 alone.

COMPETITIVE LANDSCAPE

The competition in the North America speed sensor market is characterized by a mix of established global players and emerging regional specialists, all striving to capture a larger share of an increasingly technology-driven industry. Major corporations like Honeywell, TE Connectivity, and Infineon dominate due to their deep technical expertise, broad product portfolios, and strong distribution networks. However, growing demand from automotive electrification, industrial automation, and aerospace modernization is attracting new entrants and niche sensor developers, intensifying market rivalry.

Differentiation strategies primarily revolve around technological innovation, product miniaturization, and enhanced sensor accuracy tailored for high-performance applications. Companies are also focusing on system integration capabilities, ensuring compatibility with evolving electronic control modules in vehicles and industrial equipment. Additionally, the push toward sustainability and energy-efficient operations is influencing sensor design and material selection, prompting manufacturers to align with environmental compliance standards.

Customer relationships and after-sales support play a crucial role in maintaining brand loyalty, especially in sectors requiring long-term calibration and service agreements. ;The competition extends beyond hardware to include embedded software features and data analytics capabilities as industries continue to adopt digital transformation. This evolving landscape necessitates constant adaptation, which is pushing vendors to invest in R&D, form strategic alliances, and expand into high-growth application areas to sustain their market positions.

KEY MARKET PLAYERS

Noteworthy Companies dominating the North America speed sensor market profiled in the report are

- Rockwell Automation, Inc.

- ABB

- NXP Semiconductors

- STMicroelectronics

- Infineon Technologies AG

- Schneider Electric

- Smith Systems, Inc.

- HYDAC Technology Corporation

- Micro-Epsilon

- Texas Instruments Incorporated

- Continental AG

- Bosch Engineering

- Motion Sensors, Inc.

- Rechner Sensors

- Honeywell International Inc.

TOP LEADING PLAYERS IN THE MARKET

- Honeywell is a global leader in sensing technologies and plays a pivotal role in the North America speed sensor market. The company offers a broad portfolio of high-precision speed sensors tailored for automotive, aerospace, industrial automation, and transportation applications. Honeywell’s expertise lies in developing sensors that deliver superior accuracy, durability, and performance under extreme conditions. Its innovation in MEMS-based and magnetic sensing solutions has positioned it as a trusted partner for OEMs across multiple sectors, which is contributing significantly to its strong presence in the regional market.

- TE Connectivity is a key player known for its robust engineering capabilities and extensive range of speed sensing solutions designed for both commercial and industrial applications. The company focuses on delivering customized sensor technologies that meet evolving industry standards, particularly in automotive and rail transport systems. TE Connectivity emphasizes reliability and integration, enabling seamless compatibility with modern electronic control units. Its strategic partnerships and continuous R&D investments have reinforced its competitive edge in the North American speed sensor landscape.

- Infineon has emerged as a major contributor to the North America speed sensor market through its semiconductor-driven sensing solutions. The company specializes in Hall Effect and magnetoresistive speed sensors used extensively in electric vehicles, ADAS, and industrial motor control systems. Infineon's commitment to advancing mobility and automation has made its sensor technologies integral to next-generation vehicle platforms and smart manufacturing ecosystems.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Product Innovation and Technology Differentiation Leading players prioritize continuous innovation to develop advanced speed sensor technologies that offer higher accuracy, durability, and integration capabilities. The companies aim to introduce next-generation sensors that cater to emerging applications such as autonomous driving, predictive maintenance, and Industry 4.0 systems.

Strategic Collaborations and Partnerships To enhance market reach and accelerate technology deployment, firms engage in strategic alliances with automotive manufacturers, industrial automation providers, and government agencies. These collaborations facilitate co-development of specialized sensor solutions, ensuring alignment with evolving industry requirements and regulatory standards.

Expansion into High-Growth Application Segments Market participants are actively expanding their presence in fast-growing verticals such as electric vehicles, aerospace navigation, and renewable energy monitoring. The companies strengthen their foothold and diversify revenue streams in the North America speed sensor market.

RECENT MARKET DEVELOPMENTS

- In February 2024, Honeywell launched a new line of high-resolution magnetoresistive speed sensors designed specifically for next-generation autonomous vehicle platforms by aiming to enhance precision in wheel and shaft speed detection while improving system reliability.

- In May 2024, TE Connectivity announced a partnership with a leading North American electric vehicle manufacturer to integrate its custom-developed speed sensing modules into battery management and regenerative braking systems, which is reinforcing its presence in the automotive sector.

- In July 2024, Infineon introduced an upgraded version of its Hall Effect sensor family, featuring improved signal conditioning and lower power consumption by targeting industrial motor control and aerospace applications across North America.

- In September 2024, Allegro MicroSystems expanded its North American sales and technical support network by opening a new regional headquarters in Michigan, which is positioning itself closer to major automotive clients and accelerating customer response times.

- In November 2024, Bosch Sensortec unveiled a compact multi-axis speed and motion sensing solution aimed at advanced driver-assistance systems by emphasizing integration with AI-based vehicle control architectures to support future mobility trends.

MARKET SEGMENTATION

This North America speed sensor market research report is segmented and sub-segmented into the following categories.

By Type

-

Hall Effect Speed Sensor

-

Amplified

-

Explosion Proof

-

Intrinsically Safe

-

-

Variable Reluctance Speed Sensor

-

Amplified

-

Explosion Proof

-

Intrinsically Safe

-

-

RF (Inductive) Speed Sensor

-

Amplified

-

Explosion Proof

-

Intrinsically Safe

-

-

Magnetoresistive Speed Sensor

-

Amplified

-

Explosion Proof

-

Intrinsically Safe

-

By Industry Vertical

-

Automotive

-

Wheel

-

Powertrain

-

Transmission

-

-

Aerospace & Defense

-

Commercial Aircraft

-

Defense Aircraft

-

-

Consumer Electronics

-

Industrial

-

Food & Beverage

-

Oil & Gas

-

Chemical

-

Power & Utilities

-

Water & Waste Water

-

Metal & Mining

-

Manufacturing

-

-

Medical

By Country

- United States

- Canada

- Mexico

- Rest of North America

Frequently Asked Questions

1. What sectors drive demand for speed sensors in North America?

Key sectors include automotive (especially EVs, ADAS, and autonomous vehicles), industrial automation, aerospace, defense, and consumer electronics

2. Why are speed sensors important for the automotive industry?

Speed sensors are vital for vehicle safety systems (ABS, ESP), engine/transmission controls, fuel efficiency optimization, ADAS, and autonomous driving features

How does industrial automation benefit from speed sensors?

Speed sensors enable precise control, optimization, and monitoring in manufacturing, smart factories, robotics, and process industries, improving efficiency and safety

4. Which types of speed sensors are most commonly used in North America?

Popular types include Hall effect sensors, magneto-resistive sensors, variable reluctance sensors, wheel speed sensors, tachometers, and Doppler radar sensors

5. Who are the leading companies in the North America Speed Sensor Market?

Major players include Honeywell International Inc., Robert Bosch GmbH, STMicroelectronics, Sensata Technologies, DENSO Corporation, Continental AG, and Infineon Technologies AG

6. How is the rise of electric and autonomous vehicles influencing the market?

The growing adoption of EVs and autonomous vehicles amplifies demand for precision speed sensors, essential for safe navigation, powertrain control, and smart vehicle features

7. What impact does IoT and smart city development have on the speed sensor market?

IoT integration and smart city initiatives increase deployment of speed sensors in connected vehicles, industrial machinery, and infrastructure, supporting data-driven optimization

8. What are the main technological trends in the North America Speed Sensor Market?

Trends include wireless and high-resolution sensors, edge computing, AI-enabled data analytics, vibration-based sensing, and integration into ADAS and safety systems

9. What are the biggest challenges facing the speed sensor market?

Key challenges include data overload, integration complexity in industrial automation, supply chain uncertainties, and the need to comply with rigorous standards and compatibility requirements

10. How are speed sensors used in aerospace and defense?

They provide accurate speed and movement data for navigation, flight control, propulsion, and monitoring systems in both commercial and military aircraft

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com