North America Vanilla and Vanillin Market Size, Share, Trends & Growth Forecast Report By Bean Color (Red Color, Black Color), Type, Application, and Country (The United States, Canada and Rest of North America), Industry Analysis From 2026 to 2034

North America Vanilla and Vanillin Market Size

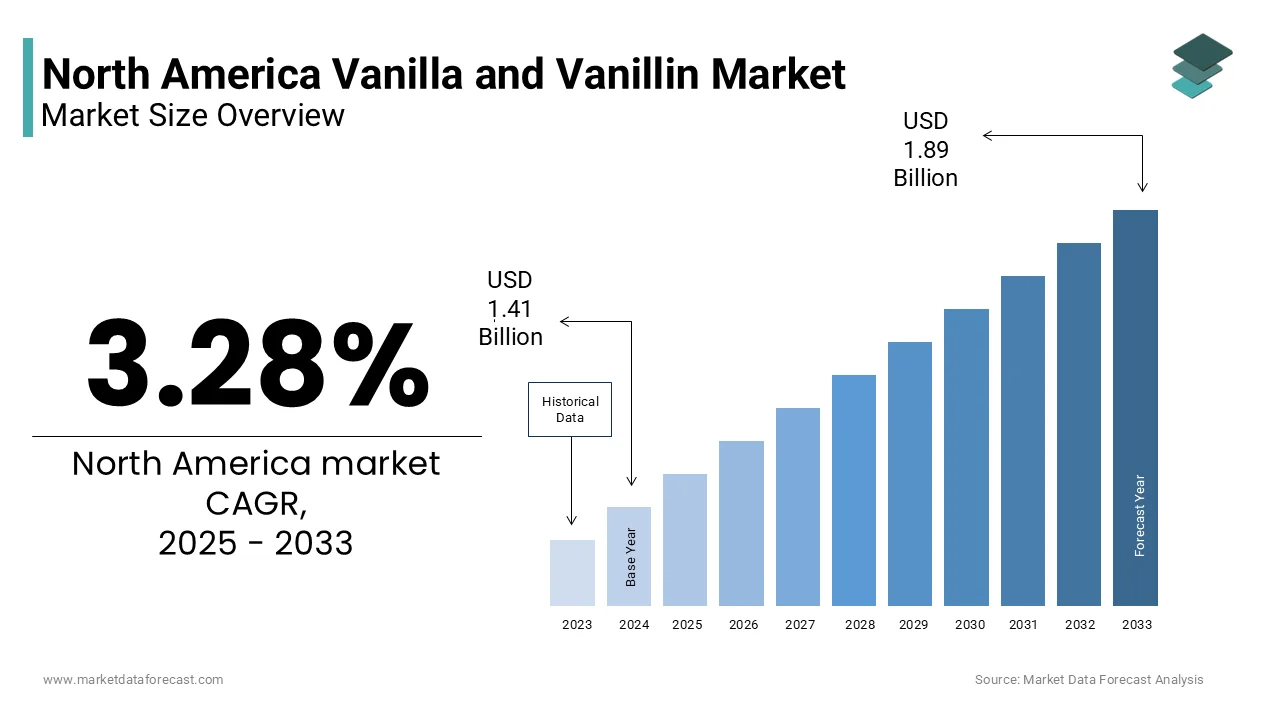

The vanilla and vanillin market size in North America was valued at USD 1.46 billion in 2025 and is predicted to be worth USD 1.95 billion by 2034 from USD 1.51 billion in 2026 and grow at a CAGR of 3.28% from 2026 to 2034.

The vanilla and vanillin are the extracts derived from Vanilla planifolia beans, alongside synthetic vanillin produced through chemical or bio-based processes. Predominantly used in food and beverage, pharmaceutical, and personal care applications, vanilla remains the second-most extensively used flavoring agent globally after salt. As per the International Trade Administration, the United States imported approximately 2,100 metric tons of vanilla beans and extracts in 2022, with Madagascar accounting for nearly 70% of total bean imports. Additionally, the rise of biotechnology-driven vanillin production, such as that developed by Evolva through yeast fermentation, reflects a growing shift toward sustainable and traceable alternatives.

MARKET DRIVERS

Escalating Demand for Natural Flavoring Agents in Premium Food Products

The surging consumer demand for natural, minimally processed ingredients particularly in premium food segments such as artisanal ice creams, organic baked goods, and plant-based dairy alternatives, which is significantly fuelling the growth of the North America vanilla and vanillin market. As per the Organic Trade Association, sales of organic food products in the United States reached $68.5 billion in 2023, reflecting a compound annual growth rate of 6.2% over the previous five years. Vanilla, being the most widely preferred natural flavor, plays a pivotal role in this expansion. This shift is particularly evident in the dairy-alternative sector, where almond, oat, and coconut milk products frequently use natural vanilla to enhance palatability. According to the Plant Based Foods Association, retail sales of plant-based foods surpassed $8 billion in 2023, with flavored varieties accounting for over 55% of volume. The reliance on natural vanilla in these products stems from its clean-label appeal and consumer perception of authenticity.

Growth of the Craft Confectionery and Artisanal Beverage Sector

The proliferation of small-batch confectioners, craft chocolatiers, and specialty beverage producers are prompting the growth of the North America vanilla and vanillin market. Independent producers in this segment prioritize flavor complexity and ingredient provenance, favoring natural vanilla over synthetic alternatives. As per the National Confectioners Association, craft chocolate sales in the U.S. grew by 12.4% in 2023, reaching $2.1 billion in retail value, with vanilla-infused products representing nearly 30% of new product launches. These artisans often source single-origin vanilla beans from Madagascar or Papua New Guinea to ensure distinctive flavor profiles, contributing to a niche yet influential segment of the market. Similarly, the specialty coffee industry, which the National Coffee Association reports now accounts for over 40% of total U.S. coffee consumption, has seen a rise in vanilla-flavored cold brews and latte syrups made with real vanilla extract. Small distilleries and craft soda makers also incorporate natural vanilla into spirits and carbonated beverages by aligning with consumer desires for premiumization.

MARKET RESTRAINTS

Volatility in Natural Vanilla Bean Supply Due to Climatic and Geopolitical Factors

The supply chain disruptions and fluctuations of the raw materials is restricting the growth of the North America vanilla and vanillin market. Cyclones, prolonged droughts, and erratic rainfall patterns have repeatedly disrupted harvests; for instance, Cyclone Ava in 2018 and Cyclone Diane in 2019 collectively reduced Madagascar’s vanilla yield by an estimated 30%, as documented by the United Nations Food and Agriculture Organization. These climatic shocks trigger speculative trading and price volatility vanilla bean prices surged to over $600 per kilogram in 2018, compared to a historical average of $40, according to the International Nut and Dried Fruit Council. Additionally, political instability and weak governance in key producing regions exacerbate risks.

High Production Costs and Regulatory Hurdles for Natural Vanilla

The economic and regulatory burden associated with cultivating and certifying natural vanilla presents a significant restraint on its availability and affordability in North America. Vanilla is one of the most labor-intensive agricultural commodities, requiring hand-pollination, a nine-month curing process, and skilled post-harvest handling. According to the International Labour Organization, it takes approximately 600 hours of labor to produce one kilogram of cured vanilla beans, which is making it vastly more expensive than synthetic alternatives. This labor intensity translates into high retail costs—pure vanilla extract averages $15 to $30 per ounce in the U.S., as per the U.S. Bureau of Labor Statistics’ Consumer Price Index data from 2023. Moreover, compliance with organic, fair trade, and non-GMO certifications are increasingly demanded by North American consumers that adds further financial strain on producers.

MARKET OPPORTUNITIES

Advancement in Fermentation-Derived Vanillin Production

The emergence of bio-based vanillin produced through microbial fermentation presents a transformative opportunity for the North American market, offering a sustainable and scalable alternative to both synthetic and natural vanilla. Companies such as Solvay and Evolva have pioneered fermentation technologies using renewable feedstocks like ferulic acid from rice bran or lignin from wood pulp. As per the U.S. Department of Energy’s Bioenergy Technologies Office, bio-vanillin production can reduce greenhouse gas emissions by up to 60% compared to petrochemical-derived vanillin. Additionally, bio-vanillin offers greater supply chain resilience, as it is not dependent on tropical agriculture. The U.S. Environmental Protection Agency notes that domestic fermentation facilities could reduce reliance on imported vanilla by up to 25% by 2030 if scaled appropriately. Furthermore, partnerships between biotech firms and food manufacturers, such as the collaboration between Givaudan and Solvay, are accelerating commercial adoption.

Expansion of Vanilla Use in Functional and Medicinal Applications

Vanilla and its primary compound vanillin are gaining traction in pharmaceutical and nutraceutical formulations due to their antioxidant, anti-inflammatory, and neuroprotective properties. Vanillin has demonstrated potential in inhibiting oxidative stress and modulating cellular pathways linked to chronic diseases. As per the National Institutes of Health, vanillin exhibits an ORAC (Oxygen Radical Absorbance Capacity) value of 950 µmol TE/g, placing it among the more potent natural antioxidants. Research published by the Journal of Agricultural and Food Chemistry indicates that vanillin can reduce neuroinflammation markers by up to 40% in preclinical models, suggesting utility in cognitive health supplements. Vanillin is being explored as a stabilizing agent in protein supplements and as a palatability enhancer in pediatric and geriatric medications. The U.S. Pharmacopeial Convention reports that over 150 FDA-approved drugs contain vanillin or its derivatives as excipients. Moreover, the rise of personalized medicine and plant-based therapeutics is driving interest in naturally derived active ingredients.

MARKET CHALLENGES

Adulteration and Lack of Standardization in Vanilla Products

The widespread adulteration of natural vanilla extract and mislabeling of vanillin sources are also to degrade the growth of the North American vanilla and vanillin market. The high price of pure vanilla creates strong incentives for economic fraud, including the dilution of extracts with synthetic vanillin, coumarin, or tonka bean derivatives. According to the U.S. Food and Drug Administration’s 2022 Import Alert, over 18% of imported vanilla products were detained at U.S. ports due to undeclared synthetic additives or misrepresentation of origin. The American Oil Chemists’ Society found in a 2023 study that 30% of commercially available “pure vanilla extract” in major U.S. retailers contained detectable levels of ethyl vanillin, a synthetic compound not permitted in FDA-compliant pure extracts. This undermines consumer trust and complicates compliance for ethical manufacturers. Furthermore, the absence of universal traceability standards makes it difficult to verify bean provenance.

Environmental Degradation from Vanilla Farming in Source Regions

The environmental toll of vanilla cultivation in primary exporting countries indirectly affects the sustainability and long-term viability of the North American supply chain. In Madagascar, where most vanilla is grown, the expansion of vanilla farms has led to deforestation and biodiversity loss in tropical rainforest zones. As per Conservation International, over 10,000 hectares of primary forest were cleared for vanilla cultivation between 2017 and 2022, primarily in the Sava region. This deforestation contributes to soil erosion, reduced water retention, and habitat destruction for endemic species such as the black-and-white ruffed lemur. The United Nations Development Programme notes that unsustainable farming practices, including slash-and-burn techniques and excessive use of agrochemicals, have degraded nearly 40% of cultivated vanilla land in Madagascar. These ecological impacts threaten the longevity of vanilla production, increasing vulnerability to climate change and pest infestations such as the vanilla beetle. For North American importers committed to ESG (Environmental, Social, and Governance) principles, these environmental externalities pose reputational risks and compliance challenges under emerging due diligence regulations like the EU Deforestation Regulation, which may influence U.S. corporate policies.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.28% |

| Segments Covered | By Bean Color, Type, Application, and Region |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | The United States, Canada, Mexico, and Rest of North America |

| Market Leaders Profiled | Givaudan SA, Symrise AG, Firmenich SA, Archer Daniels Midland Company, Solvay SA, Sensient Technologies Corporation, Borregaard ASA, Evolva Holdings SA, Lesaffre et Compagnie, and International Flavors & Fragrances Inc. (IFF), and others |

SEGMENTAL ANALYSIS

By Bean Color Insights

The black beans segment held a dominant share of the North American vanilla market in 2025 with their extended post-harvest processing, which imparts a deep, rich aroma and higher vanillin concentration. According to the United States Department of Agriculture, black beans undergo a curing process lasting 4 to 6 months, during which enzymatic browning and oxidation significantly increase vanillin levels to an average of 2.5% by dry weight nearly 40% more than red beans. This biochemical enhancement makes them ideal for high-end flavor formulations in premium ice creams, chocolates, and spirits.

The red beans segment is projected to grow with a CAGR of 9.4% from 2026 to 2034 owing to a rising demand for minimally processed, terroir-expressive vanilla in craft culinary applications. Red beans, also known as "red-cured" or "semi-cured," undergo a shorter, controlled drying process of 6 to 8 weeks, preserving floral and fruity top notes that are often lost in full curing. Additionally, their vibrant appearance and moisture retention make them particularly suitable for direct culinary use in syrups, infusions, and cocktail garnishes. The Plant Based Foods Association reports that red beans are increasingly used in non-dairy yogurts and fermented beverages, where their lighter profile avoids overpowering delicate bases.

By Type Insights

The madagascar bourbon segment was the largest and held a prominent share of the North American vanilla market in 2-24. The beans, which is derived from Vanilla planifolia grown in Madagascar’s Sava region, contain vanillin concentrations averaging 2.2% to 2.8%, among the highest of all vanilla types, according to the Journal of Essential Oil Research. This potency allows for efficient extraction and consistent performance in industrial-scale applications such as baked goods, dairy products, and ready-to-drink beverages. Additionally, established trade relationships and certification programs enhance supply stability. As per the Fair Trade America 2023 report, nearly 40% of Madagascar vanilla entering the U.S. carries Fair Trade or Rainforest Alliance certification, appealing to ethically conscious brands.

The tahitian vanilla segment is likely to grow at a CAGR of 5.4% during the forecast period with the growing prominence for the clean-label trends in premium spirits. Craft distillers in California and Oregon are increasingly infusing vodkas and gins with Tahitian beans. The Alcohol and Tobacco Tax and Trade Bureau recorded a 27% rise in spirit labels declaring Tahitian vanilla between 2022 and 2023.

By Application Insights

The food and beverages segment held a dominant share of the North American vanilla and vanillin market in 2025 with the vanilla’s role as the most widely used natural flavor in edible products, spanning dairy, confectionery, and beverage categories. The rise of plant-based alternatives has further amplified demand; the Plant Based Foods Association notes that 65% of oat and almond milk products use vanilla to mask beany aftertastes, with sales of flavored plant milks reaching $2.8 billion in 2023. Additionally, ready-to-drink coffee beverages, which the National Coffee Association says grew by 14% in 2023, rely heavily on vanilla for sweetness and complexity without added sugar. Moreover, the FDA’s recognition of vanilla extract as a safe and natural ingredient supports its unrestricted use in organic and non-GMO products, reinforcing its centrality in the evolving food landscape.

The pharmaceutical segment is expected to grow with a CAGR of 10.8% from 2026 to 2034 owing to the vanillin’s dual functionality as a flavor-masking agent and bioactive compound in medicinal formulations. Pediatric and geriatric medications often incorporate vanillin to improve palatability, particularly in liquid suspensions and chewable tablets. The American Academy of Pediatrics reports that 78% of children’s liquid antibiotics and vitamins contain vanillin or ethyl vanillin to enhance compliance. Research published by the National Institutes of Health demonstrates that vanillin reduces oxidative stress markers by up to 35% in preclinical models, supporting its inclusion in nutraceuticals and cognitive health supplements. Additionally, vanillin is used as a stabilizing excipient in protein-based drugs due to its ability to inhibit aggregation.

REGIONAL ANALYSIS

United States Vanilla and Vanillin Market

The United States vanilla and vanillin market held 89.2% of the share in 2025. The country imported 2,150 metric tons of vanilla beans and extracts in 2023, with Madagascar supplying 68% of total bean volume, according to the Foreign Agricultural Service. The presence of major flavor houses such as International Flavors & Fragrances (IFF) and Givaudan, alongside a robust network of artisanal producers, sustains high demand for premium vanilla. The rise of clean-label trends has intensified scrutiny on ingredient sourcing, with the Organic Trade Association reporting that 62% of U.S. consumers check for “natural vanilla” on product labels. Regulatory clarity from the FDA further shapes market dynamics, particularly in defining “pure vanilla extract.” Additionally, the U.S. leads in bio-vanillin adoption, with companies like Solvay scaling fermentation-derived production in Pennsylvania.

Canada Vanilla and Vanillin Market

Canada vanilla and vanillin market was next by accounting for 11.2% of the share in 2025 with a strong preference for ethically sourced and organic vanilla, influenced by stringent labeling regulations and high consumer awareness. The Canadian Food Inspection Agency reports that imports of certified organic vanilla extract rose by 18% in 2023, outpacing overall vanilla import growth. Quebec and British Columbia have emerged as centers for craft chocolate and specialty baking, where single-origin vanilla is increasingly used. The Canadian Confectionery Association notes that artisanal chocolate sales grew by 13% in 2023, with vanilla-infused products accounting for nearly 40% of new launches. Additionally, Health Canada’s recent alignment with U.S. FDA standards on natural flavors has facilitated cross-border product development.

COMPETITIVE LANDSCAPE

The competitive landscape of the North America vanilla and vanillin market is characterized by a dynamic interplay between global flavor giants, niche natural suppliers, and emerging biotech innovators. Established players dominate through extensive R&D capabilities, global supply chains, and deep integration with major food and personal care brands. Their strength lies not only in ingredient supply but in their ability to provide end-to-end formulation support, sensory analysis, and regulatory guidance. At the same time, smaller specialty suppliers and ethical sourcing collectives are gaining traction by catering to the premium and artisanal sectors, where origin transparency and bean provenance are paramount. The rise of bio-based vanillin has intensified competition, with several companies racing to commercialize fermentation-derived alternatives that meet natural labeling standards. This technological shift is reshaping traditional supplier relationships and creating new alliances between biotech firms and consumer goods manufacturers. Additionally, sustainability commitments are becoming a key differentiator, with brands increasingly evaluated on their environmental and social impact in vanilla-producing regions.

KEY MARKET PLAYERS

Some of the key players in the North America vanilla and vanillin market are

- Givaudan SA

- Symrise AG

- Firmenich SA

- Archer Daniels Midland Company

- Solvay SA

- Sensient Technologies Corporation

- Borregaard ASA

- Evolva Holdings SA

- Lesaffre et Compagnie

- International Flavors & Fragrances Inc. (IFF)

TOP PLAYERS IN THE MARKET

- Symrise AG operates as a global leader in flavor and fragrance innovation, with a significant footprint in the North American vanilla and vanillin sector. The company leverages its expertise in both natural extraction and synthetic biosynthesis to deliver consistent, high-quality vanillin solutions to food, beverage, and personal care manufacturers. Symrise has developed proprietary fermentation technologies that enable sustainable production of vanillin from renewable raw materials, positioning it at the forefront of clean-label ingredient development. Its North American operations are deeply integrated with major consumer goods companies, where it functions not only as a supplier but also as a formulation partner. By investing in sensory science and application technology, Symrise ensures its vanilla offerings meet evolving consumer demands for authenticity and traceability.

- Firmenich International SA, now part of dsm-firmenich following a strategic merger, has long been a dominant force in the global flavor landscape, with a strong presence in North America’s vanilla and vanillin market. The company excels in natural vanilla sourcing, maintaining direct relationships with smallholder farmers in Madagascar and Indonesia to ensure quality and sustainability. Firmenich’s approach combines traditional botanical knowledge with advanced analytical techniques to preserve the complexity of natural vanilla profiles. It has pioneered biotechnological alternatives to synthetic vanillin, including yeast-fermented vanillin that meets natural labeling standards in the U.S. and Canada. Its innovation pipeline focuses on enhancing flavor performance while reducing environmental impact, aligning with the values of premium food and fragrance brands.

- International Flavors & Fragrances Inc. (IFF) is a key architect of flavor innovation in North America, with a substantial influence on the vanilla and vanillin supply chain. The company integrates natural vanilla sourcing with cutting-edge biotechnology to offer a diversified portfolio that meets the needs of mass-market and specialty producers alike. IFF places strong emphasis on sustainability, investing in regenerative agriculture initiatives and traceability systems that ensure ethical procurement of vanilla beans. Its research capabilities enable the development of vanillin variants with enhanced stability and flavor release, particularly for use in plant-based and functional foods.

TOP STRATEGIES USED BY KEY MARKET PLAYERS

One major strategy employed by leading players is vertical integration into sustainable vanilla sourcing, where companies establish direct partnerships with farming cooperatives in Madagascar, Indonesia, and Papua New Guinea. This approach ensures supply chain transparency, improves bean quality, and supports long-term farmer livelihoods, enhancing both brand credibility and ingredient security.

Another strategy is investment in biotechnology and fermentation-derived vanillin production. Companies are advancing microbial fermentation processes using renewable feedstocks to create natural-identical vanillin that meets clean-label demands. This shift reduces reliance on agricultural volatility and synthetic petrochemical routes, aligning with consumer preferences for sustainable and traceable ingredients. These bio-based innovations also allow for consistent supply and regulatory compliance in organic and non-GMO product lines.

RECENT HAPPENINGS IN THE MARKET

- In March 2023, Symrise AG launched a sustainable vanilla sourcing initiative in partnership with smallholder farmers in Madagascar by aiming to enhance crop yields and post-harvest processing standards through agronomic training and infrastructure support.

- In June 2023, dsm-firmenich announced the commercial-scale production of fermentation-derived vanillin at its facility in North Carolina, which is marking a significant step toward sustainable, non-agricultural vanilla flavor production in North America.

- In September 2023, International Flavors & Fragrances Inc. (IFF) introduced a new line of clean-label vanilla flavor systems specifically designed for plant-based dairy and low-sugar applications by expanding its portfolio for health-focused food manufacturers.

- In January 2025, Givaudan strengthened its natural vanilla supply chain by establishing a direct trade collaboration with a certified organic vanilla cooperative in Papua New Guinea, ensuring traceability and quality for premium clients.

- In May 2025, Kerry Group unveiled a sensory-optimized vanilla blend for frozen desserts, developed using proprietary flavor modulation technology to enhance creaminess and sweetness perception without added sugar.

MARKET SEGMENTATION

This research report on the North America vanilla and vanillin market has been segmented and sub-segmented based on the following categories.

By Bean Color

- Red Beans

- Black Beans

By Type

- Madagascar Bourbon

- Mexican Vanilla

- Indonesian Vanilla

- Tahitian Vanilla

By Application Insights

- Food and Beverages

- Cosmetics

- Pharmaceutical

- Others

By Country

- The United States

- Canada

- Rest of North America

Frequently Asked Questions

1. What is the North America Vanilla and Vanillin Market?

The North America Vanilla and Vanillin Market focuses on natural vanilla beans and synthetic vanillin used as flavoring agents in food, and personal care products.

2. What is driving the growth of this market?

Key drivers include rising demand for natural flavors, growth in bakery and confectionery products, and increasing use of vanillin in pharmaceuticals and cosmetics.

3. Which countries dominate the North America Vanilla and Vanillin Market?

The United States is the largest market, followed by Canada and Mexico due to strong food and beverage industries.

4. What are the main applications of vanilla and vanillin?

Applications include food and beverages, bakery products, confectionery, dairy, pharmaceuticals, and fragrances.

5. What is the difference between vanilla and vanillin?

Vanilla is a natural extract from vanilla beans, while vanillin can be naturally derived or synthetically produced to replicate vanilla flavor.

6. Which segment is growing the fastest in this market?

The natural vanilla segment is growing rapidly due to consumer preference for clean-label and organic ingredients.

7. What challenges does the market face?

Challenges include high costs of natural vanilla, supply shortages, and price fluctuations of vanilla beans.

8. What is the growth outlook for this market?

The market is expected to grow steadily, driven by demand for natural flavors and the expansion of processed food and beverage industries in North America.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com