North America Vascular Guidewires Market Size, Share, Trends & Growth Forecast Report By Product (Coronary Guidewires, Peripheral Guidewires), By Coating Type, By End-User, and By Country (United States, Canada & Rest of North America) – Industry Analysis and Forecast, 2026 to 2034

Market Size, 2025

$1,006.60 BnMarket Estimate, 2026

$1,058.03 BnMarket Forecast, 2034

$1,576.35 BnCAGR, 2026–2034

5.11%North America Vascular Guidewires Market Summary

The North America Vascular Guidewires Market size was valued at USD 957.66 billion in 2024 and is anticipated to reach USD 1499.71 billion by 2033, growing at a CAGR of 5.11 % from 2024 to 2033. The market is gaining momentum due to the rising demand for remote cardiac care, the growing burden of cardiovascular diseases, and technological advancements in AI-powered diagnostics and wearable cardiac monitoring devices.

Key Market Trends & Insights

- North America dominated the global market with a largest share in 2024.

- North America is projected to grow at the fastest rate between 2024 and 2033.

- Based on technology, the IT services segment is the fastest-growing with a projected CAGR of 5.11 %.

- AI and wearable tech adoption are key trends driving innovation in the market.

Market Size & Forecast

- 2024 Market Size: USD 957.66 billion

- 2033 Projected Market Size: USD 1499.71 billion

- CAGR (2024–2033): 5.11 %

- North America: Largest market in 2024

- North America: Fastest-growing region

North America Vascular Guidewires Market Size

The North America Vascular Guidewires Market was valued at USD 1,006.60 billion in 2025, is estimated to reach USD 1,058.03 billion in 2026, and is projected to reach USD 1,576.35 billion by 2034, growing at a CAGR of 5.11% from 2026 to 2034.

The North America Vascular Guidewires Market encompasses the production, distribution, and utilization of guidewires—thin, flexible medical devices used to navigate catheters through vascular pathways during interventional procedures such as angioplasty, stenting, and thrombectomy. These devices are critical in guiding therapeutic and diagnostic tools to targeted areas within the cardiovascular system with precision and minimal trauma. The market is primarily driven by technological advancements in minimally invasive procedures and an aging population prone to chronic cardiovascular diseases.

According to the Centers for Disease Control and Prevention (CDC), heart disease remains the leading cause of death in the United States, contributing to approximately 697,000 deaths annually. This growing prevalence of cardiovascular disorders has significantly increased the demand for vascular interventions, thereby driving the need for high-performance vascular guidewires.

Canada also plays a pivotal role, with steadily rising investments in healthcare innovation and medical device manufacturing. Health Canada's regulatory framework ensures the rapid approval of novel guidewire technologies, supporting market growth. As per Statistics Canada, the proportion of the population aged 65 and older reached nearly 19% in 2023, further amplifying the incidence of vascular conditions requiring interventional treatments.

MARKET DRIVERS

Increasing Prevalence of Peripheral Arterial Disease (PAD)

The escalating incidence of peripheral arterial disease (PAD), particularly among aging populations is one of the key drivers fueling the North America Vascular Guidewires Market. PAD affects blood flow to the limbs and often necessitates endovascular interventions where vascular guidewires play a central role in navigating catheters through narrowed or blocked arteries. According to the American Heart Association (AHA), more than 8.5 million people in the United States suffer from PAD, with the condition being most prevalent in individuals over the age of 65.

This growing patient pool directly translates into higher procedural volumes involving vascular guidewires. In 2023, over 1.2 million peripheral vascular interventions were performed across the U.S., many of which required the use of specialized guidewires for successful navigation and treatment delivery. Furthermore, as per the Society of Interventional Radiology, the number of outpatient-based interventional procedures has risen by nearly 12% year-over-year, indicating a strong shift toward less invasive treatments that rely heavily on precision instruments like vascular guidewires. Additionally, awareness campaigns by organizations such as the Vascular Disease Foundation have contributed to early diagnosis and timely intervention, further stimulating market growth.

Technological Advancements in Guidewire Design and Material Innovation

Rapid advancements in guidewire technology have significantly enhanced their performance, durability, and maneuverability, making them indispensable in complex vascular procedures. Manufacturers are increasingly focusing on developing hydrophilic-coated, ultra-low profile, and shapeable-tip guidewires to improve navigational accuracy in tortuous anatomy. For instance, Boston Scientific and Abbott have introduced next-generation guidewires featuring nanotechnology coatings that reduce friction and enhance trackability, directly influencing procedural success rates.

These enhancements allow physicians to perform intricate interventions with greater confidence, especially in small vessel or chronic total occlusion (CTO) cases. Moreover, the integration of smart materials like nitinol—a nickel-titanium alloy known for its superelasticity—has revolutionized guidewire design, enabling better flexibility and resistance to kinking. Such improvements not only enhance clinical outcomes but also reinforce the sustained demand for advanced vascular guidewires in North America.

MARKET RESTRAINTS

High Cost of Advanced Vascular Guidewires and Limited Reimbursement Coverage

Despite the growing demand for vascular guidewires, one of the primary restraints impeding market expansion in North America is the high cost associated with advanced guidewire systems. Premium products incorporating features such as variable stiffness, micro-coatings, and shape memory alloys can cost several hundred dollars per unit.

While private insurance plans in the U.S. typically offer broader coverage, Medicare reimbursement policies often limit full payment for certain high-end guidewire models, creating financial pressure on healthcare providers. This dynamic discourages widespread adoption of cutting-edge guidewire technologies, especially in publicly funded or budget-constrained facilities. In Canada, the situation is somewhat similar. Although public healthcare systems cover most vascular procedures, procurement decisions are often based on cost-efficiency rather than innovation. Consequently, despite the availability of superior guidewire solutions, economic constraints remain a notable barrier to market penetration.

Stringent Regulatory Requirements and Lengthy Approval Processes

The regulatory landscape governing medical devices in North America, particularly in the United States, imposes significant challenges on manufacturers seeking to commercialize new vascular guidewire technologies. The U.S. Food and Drug Administration (FDA) mandates rigorous pre-market evaluations, including extensive clinical trials and quality assurance protocols, before granting clearance or approval.

Such prolonged timelines delay market entry and increase development costs, especially for smaller companies without substantial capital reserves. In Canada, while the regulatory process is slightly less burdensome, Health Canada still requires comprehensive documentation under the Medical Devices Regulations (SOR/98-282). As per a 2022 review by the Therapeutic Products Directorate, Class III device submissions, which include certain types of vascular guidewires, take up to 18 months for final approval. These delays hinder the speed at which innovative guidewire solutions reach clinicians and patients, ultimately slowing market growth in the region.

MARKET OPPORTUNITIES

Expansion of Outpatient Catheterization Labs and Ambulatory Surgical Centers (ASCs)

The proliferation of outpatient catheterization labs and ambulatory surgical centers (ASCs) across North America presents a significant growth opportunity for the vascular guidewires market. These facilities provide cost-effective, minimally invasive interventional services, reducing hospital admission durations and lowering overall healthcare expenditures. According to the Ambulatory Surgery Center Association (ASCA), more than 6,300 ASCs were operational in the U.S. in 2023, collectively performing over 24 million procedures annually.

With increasing preference for same-day interventions, the demand for vascular guidewires tailored for outpatient use is surging. Many ASCs prioritize efficiency and rapid recovery, favoring guidewires that offer ease of use, reduced procedural times, and compatibility with a broad range of catheter systems. Moreover, regulatory support and favorable reimbursement policies have accelerated the transition of vascular interventions from traditional hospitals to ASCs. This evolving care delivery model is expected to boost the consumption of vascular guidewires outside hospital environments, offering manufacturers a lucrative and expanding market segment.

Rising Adoption of Robotic-Assisted Vascular Interventions

The integration of robotics into vascular interventional procedures is emerging as a transformative trend in cardiology and vascular surgery, opening new avenues for vascular guidewire manufacturers. Robotic-assisted platforms, such as those developed by Corindus Vascular Robotics (a Siemens Healthineers company), enable precise control over guidewire manipulation and catheter navigation, enhancing procedural safety and reproducibility.

These systems require compatible guidewires engineered for seamless interaction with robotic arms, prompting manufacturers to develop specialized product lines optimized for automated use. Furthermore, physician training programs and hospital investments in hybrid operating rooms equipped with robotic capabilities are accelerating adoption. These developments signal a paradigm shift in vascular intervention techniques, where high-precision guidewires will become integral components of next-generation interventional suites, offering substantial growth potential for the market.

MARKET CHALLENGES

Shortage of Skilled Interventional Specialists and Training Gaps

The shortage of trained interventional cardiologists, vascular surgeons, and radiologists capable of handling advanced guidewire technologies, is a major challenge confronting the North America Vascular Guidewires Market. Complex vascular procedures demand high levels of expertise, particularly when using next-generation guidewires designed for chronic total occlusions (CTOs) or navigating tortuous anatomy.

According to the Association of American Medical Colleges (AAMC), the U.S. faces a projected shortfall of up to 124,000 physicians by 2034, including specialists in interventional cardiology. In 2023, only about 1,200 interventional cardiology fellows completed training nationwide, falling short of the annual requirement estimated at 1,500 by the American College of Cardiology (ACC). This gap limits the number of professionals proficient in advanced guidewire techniques, thereby constraining the uptake of sophisticated products. Moreover, training disparities exist between academic medical centers and community hospitals, where access to hands-on simulation labs and continuing medical education (CME) programs is limited. These workforce and educational challenges hinder the uniform adoption of advanced vascular guidewires across the healthcare spectrum, posing a structural impediment to market growth despite the availability of innovative products.

Supply Chain Disruptions and Raw Material Constraints

The vascular guidewires industry in North America is increasingly vulnerable to supply chain disruptions and raw material shortages, which pose significant operational risks. Guidewires are composed of specialty materials such as nitinol, platinum, and stainless steel, all of which are subject to fluctuating global markets and geopolitical tensions. For instance, the global nitinol supply chain, crucial for producing superelastic guidewires, experienced bottlenecks in 2023 due to export restrictions from Japan and China. According to the Specialty Steel Industry of the Americas (SSIA), lead times for nitinol wire stock increased by 40% during this period, affecting production schedules for major guidewire manufacturers.

Similarly, platinum, a key component in guidewire distal tips for radiopacity, is sourced predominantly from Russia and South Africa. Geopolitical instability in these regions has led to price volatility. These cost pressures are passed on to healthcare providers, limiting procurement budgets and delaying equipment upgrades. Furthermore, the U.S.-China trade tensions have impacted logistics networks, causing extended delivery times for imported components. These persistent supply-side challenges threaten to disrupt production cycles and inflate product costs, ultimately affecting market dynamics in the North American vascular guidewires sector.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Coating Type, End-User and Country. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | The U.S., Canada and Rest of North America |

| Market Leader Profiled | Abbott Laboratories, Terumo Corporation, B. Braun Melsungen AG |

SEGMENTAL ANALYSIS

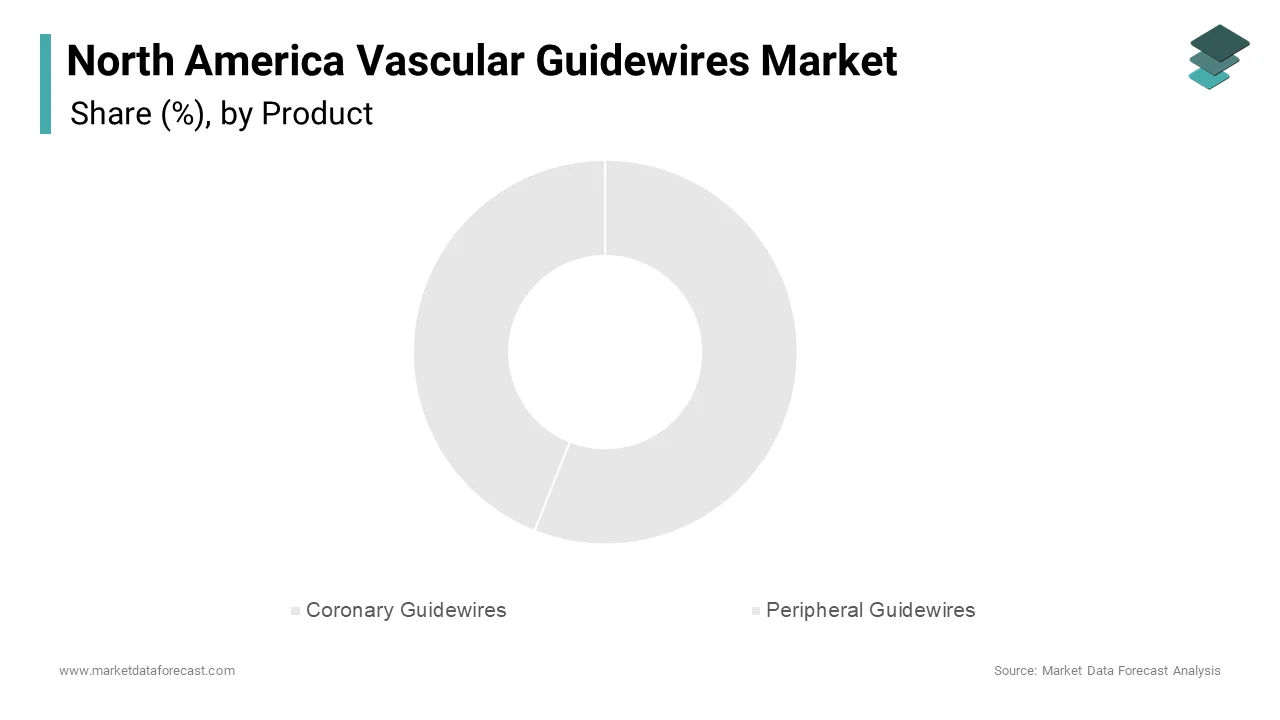

By Product Insights

The coronary guidewires segment accounted for a 56.4% of the North America Vascular Guidewires Market and is maintaining their position as the dominant product category. This dominance is primarily attributed to the High prevalence of coronary artery disease (CAD) and the widespread adoption of percutaneous coronary interventions (PCIs) across hospitals in the U.S. and Canada is largely attributed to the growth of this segment. According to the American Heart Association (AHA), over 18.2 million adults in the United States suffer from CAD, with more than 600,000 PCIs performed annually. Each PCI procedure typically involves the use of at least one coronary guidewire, often multiple depending on complexity. Additionally, the aging population in North America has significantly contributed to the rise in cardiovascular diseases.

Technological advancements have also played a critical role in sustaining this segment's leadership. Innovations such as hydrophilic-coated and shapeable-tip guidewires are predominantly used in coronary interventions due to their precision and ease of navigation through complex anatomy. The U.S. Food and Drug Administration (FDA) approved over 15 new coronary guidewire models between 2021 and 2023, reinforcing continuous product development efforts by key players like Abbott and Boston Scientific. The growing integration of robotics in coronary procedures has further increased reliance on specialized coronary guidewires capable of interfacing with automated systems.

The peripheral guidewires are projected to grow at the fastest CAGR of 9.3% during the forecast period. Surging demand driven by rising incidence of peripheral arterial disease (PAD) and increasing utilization of endovascular techniques for limb salvage and stroke prevention is expanding this segment. Data from the Centers for Disease Control and Prevention (CDC) indicates that more than 8.5 million Americans suffer from PAD, with over 1.2 million peripheral vascular interventions conducted annually. This surge in peripheral interventions has directly boosted the demand for specialized guidewires designed to navigate tortuous vessels in the lower extremities and carotid arteries.

Moreover, the expansion of ambulatory surgical centers (ASCs) offering outpatient peripheral interventions has fueled market growth. According to the Ambulatory Surgery Center Association (ASCA), peripheral vascular procedures in ASCs grew by 18% year-over-year in 2023, favoring cost-effective and minimally invasive treatments that rely extensively on peripheral guidewires. Additionally, manufacturers have intensified R&D investments into developing ultra-low profile and steerable peripheral guidewires tailored for chronic total occlusions (CTOs).

By Coating Type Insights

The Coated guidewires segment led the North America vascular guidewires market in 2024 by capturing a 64.3% of total revenue. The dominance of this segment is primarily driven by the superior performance characteristics offered by coated guidewires, including enhanced lubricity, reduced friction, and improved trackability through complex vascular anatomy. Hydrophilic and hydrophobic coatings are increasingly preferred in both coronary and peripheral interventions due to their ability to minimize vessel trauma and enhance procedural efficiency. According to a clinical review published in Cardiovascular Engineering and Technology , coated guidewires demonstrated a 20% improvement in lesion crossing success rates compared to non-coated alternatives, particularly in chronic total occlusion (CTO) cases. Additionally, the widespread adoption of coated guidewires in robotic-assisted procedures has further reinforced their market leadership. Manufacturers have also prioritized innovation in coating technologies to meet evolving clinical demands. Furthermore, physician training programs emphasize the benefits of coated guidewires, contributing to higher preference levels among interventional cardiologists.

The Non-coated guidewires segment is expected to register the highest CAGR of 8.1% during the forecast period which is driven by their increasing use in short-duration diagnostic procedures and budget-conscious healthcare settings where cost-efficiency takes precedence over advanced features. Unlike coated guidewires, which are often reserved for complex interventions requiring prolonged navigation, non-coated variants offer sufficient performance for routine angiograms and simple stenting procedures. Public healthcare institutions, particularly in Canadian provinces such as Ontario and Alberta, have been increasingly adopting non-coated guidewires to align with cost-containment strategies. Data from the Canadian Institute for Health Information (CIHI) revealed that procurement budgets for vascular consumables were reduced by 12% in 2023, prompting hospitals to opt for more economical guidewire options. Moreover, non-coated guidewires are witnessing renewed interest in hybrid operating rooms where they serve as initial access tools before transitioning to coated wires for therapeutic phases. Finally, regulatory agencies such as the FDA have streamlined approval processes for basic guidewire models, enabling faster market entry for cost-effective non-coated variants.

By End-User Insights

The hospitals segment remained the largest end-user in the North America vascular guidewires market by accounting for substantial share of total consumption in 2024. This dominance is because of the high volume of inpatient vascular interventions performed in hospital-based catheterization labs and cardiac surgery units, which require a steady supply of guidewires for both emergency and scheduled procedures. These facilities continue to be the primary setting for complex vascular cases, especially those involving chronic total occlusions (CTOs) and multi-vessel disease, where advanced guidewire technology is indispensable. In addition, hospital procurement departments benefit from bulk purchasing agreements with major manufacturers, ensuring consistent supply and cost optimization. Moreover, academic medical centers and teaching hospitals drive innovation adoption, serving as early adopters of next-generation guidewires. Lastly, the availability of comprehensive reimbursement coverage under Medicare Part B for hospital-based procedures ensures financial viability, encouraging continued reliance on hospital settings for high-risk vascular interventions.

The Ambulatory Surgical Centers (ASCs) segment is anticipated to grow at the fastest CAGR of 10.2% from 2025 to 2033 due to the increasing shift of vascular interventions toward outpatient settings driven by cost savings, convenience, and favorable reimbursement policies. According to the Ambulatory Surgery Center Association (ASCA), over 24 million procedures were performed in U.S.-based ASCs in 2023, with vascular interventions representing a growing portion of the case mix. Specifically, peripheral vascular interventions in ASCs saw an increase in volume compared to the previous year, as reported by Definitive Healthcare. Regulatory support has played a pivotal role in this transition. In 2022, the Centers for Medicare & Medicaid Services (CMS) expanded the list of covered interventional cardiology procedures in outpatient settings, including femoral artery angioplasty and carotid stenting, thereby incentivizing providers to move these services outside of hospitals. Cost efficiency remains a compelling driver, as ASCs typically charge less than hospital outpatient departments for similar procedures. This economic advantage appeals to both payers and patients, accelerating the migration of vascular interventions to ASCs. Furthermore, ASCs are increasingly investing in hybrid imaging suites equipped with robotic assistance, enabling them to perform more complex vascular procedures previously confined to hospitals.

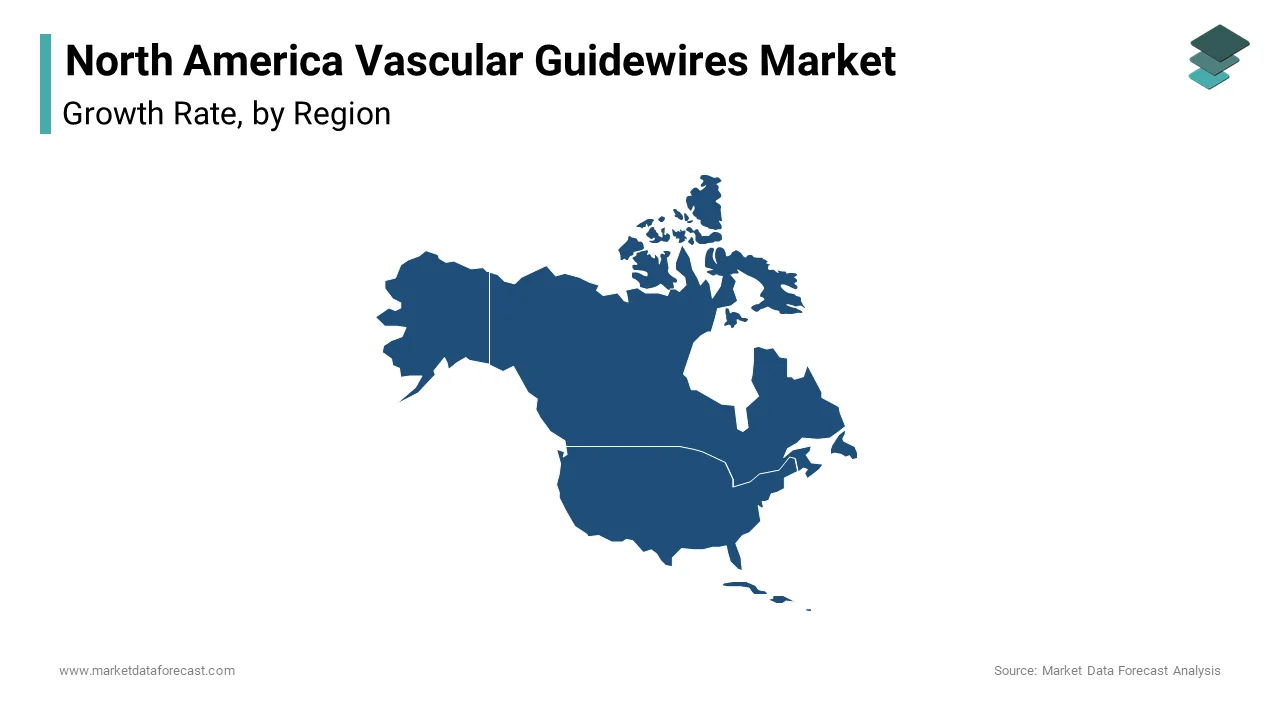

COUNTRY LEVEL ANALYSIS

The United States held the dominant position in the North America vascular guidewires market by accounting for a 76.3% of the regional share in 2024. This lead position is underpinned by a combination of high prevalence of cardiovascular diseases, well-established healthcare infrastructure, and rapid adoption of technologically advanced medical devices. According to the Centers for Disease Control and Prevention (CDC), heart disease remains the leading cause of death in the U.S., responsible for roughly 697,000 deaths annually. Coupled with an aging population the demand for vascular interventions continues to rise. In 2023 alone, over 1.5 million interventional cardiology procedures were performed nationwide, each requiring at least one vascular guidewire. The U.S. also leads in innovation, with major players such as Abbott, Boston Scientific, and Medtronic headquartered in the country and actively launching next-generation guidewire technologies. Reimbursement mechanisms, particularly under Medicare Part B, ensure broad access to vascular interventions, further supporting market expansion. As per the Centers for Medicare & Medicaid Services (CMS), vascular procedure reimbursements grew by 6.5% in 2023, reinforcing financial sustainability for providers and manufacturers alike.

Canada is positioning it as another major market in the region. The country's strong public healthcare system, increasing geriatric population, and growing emphasis on domestic manufacturing support this significant presence. According to Statistics Canada, the proportion of the population aged 65 and older reached 19% in 2023, driving up the incidence of cardiovascular diseases. As per the Public Health Agency of Canada, circulatory system diseases accounted for 31% of all deaths in 2022, necessitating a rise in vascular interventions. Health Canada’s progressive regulatory framework has enabled expedited approvals for novel guidewire technologies. Additionally, Canada has seen increased investment in medical device manufacturing, with companies like Merit Medical expanding local production facilities. Despite challenges related to reimbursement constraints and centralized procurement, the Canadian vascular guidewires market remains resilient, supported by a robust pipeline of clinical trials and growing adoption of outpatient vascular interventions.

Mexico is emerging as a modest but growing contributor due to improving healthcare infrastructure and rising foreign direct investment in medical device manufacturing. The Mexican Ministry of Health also recorded a 14% rise in interventional cardiology procedures between 2021 and 2023, boosting demand for vascular guidewires. Foreign manufacturers, including Terumo Corporation and Cardinal Health, have established regional distribution hubs in Mexico to serve both domestic and Latin American markets. The Secretariat of Economy noted that medical device exports from Mexico grew by 10% in 2023, highlighting the country's strategic importance in regional trade. However, challenges such as limited insurance coverage and disparities in rural-urban healthcare access constrain market expansion. Nonetheless, ongoing reforms under the IMSS-Bienestar program aim to bridge these gaps, offering long-term growth potential for vascular guidewire suppliers seeking footholds in North America beyond the U.S. and Canada.

The Rest of North America, comprising select Caribbean nations and parts of Central America, collectively represents small share of the regional vascular guidewires market . While relatively small in size, this sub-region presents niche opportunities driven by increasing foreign aid for cardiovascular health programs and gradual improvements in private healthcare infrastructure. In countries like Jamaica and the Dominican Republic, cardiovascular disease mortality rates remain high. However, limited access to advanced vascular interventions constrains widespread adoption of premium guidewires. Nonetheless, international partnerships are fostering progress. These initiatives indirectly stimulate demand for basic vascular guidewires in partner hospitals. Private healthcare clinics in urban centers such as Nassau and San Juan are gradually introducing interventional cardiology services, supported by cross-border procurement from U.S.-based distributors.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Notable manufacturers operating in the North America vascular guidewires market are Abbott Laboratories, Terumo Corporation, B. Braun Melsungen AG, Medtronic plc, Biotronik SE & Co. KG, Cook Medical, Inc., Boston Scientific Corporation, Cardinal Health, Inc., C. R. Bard, Inc., and The Spectranetics Corporation.

The competition in the North America vascular guidewires market is intense and marked by the presence of well-established global players striving to maintain or expand their market dominance. Several manufacturers are engaged in a race to innovate, continuously introducing new products that offer superior performance in navigating complex vascular anatomy. The market is characterized by a high degree of product differentiation, with companies focusing on unique material compositions, coating technologies, and tip designs to gain an edge over rivals. Additionally, brand reputation and physician preference play a critical role in shaping market dynamics. Firms are leveraging strong distribution networks, robust clinical evidence, and targeted marketing to strengthen their positions. Strategic acquisitions, collaborative ventures, and participation in clinical trials further intensify the competitive environment, ensuring that only the most adaptable and innovative companies thrive in this space.

Top Players in the Market

Boston Scientific Corporation

Boston Scientific is a leading global player in the vascular guidewires market, known for its extensive portfolio of interventional cardiology and peripheral vascular products. The company has consistently focused on innovation, offering advanced guidewire technologies that enhance procedural efficiency and patient outcomes. Its commitment to R&D has resulted in the development of high-performance guidewires with enhanced trackability and durability. Boston Scientific’s strong distribution network and strategic collaborations with healthcare providers have solidified its position as a dominant force in the North American market.

Abbott Laboratories

Abbott plays a pivotal role in shaping the vascular guidewires landscape through its emphasis on cutting-edge medical device solutions. The company's vascular business includes a diverse range of guidewires tailored for both coronary and peripheral interventions. Abbott's continuous investment in product innovation and clinical research has enabled it to maintain a competitive edge. With a focus on integrating smart technologies and improving material design, Abbott has successfully addressed evolving clinical needs, making it a preferred choice among physicians across North America.

Terumo Corporation

Terumo is a globally recognized leader in cardiovascular medical devices and holds a significant presence in the North America vascular guidewires market. Known for its precision-engineered guidewires, Terumo emphasizes quality, reliability, and performance. The company’s product lineup includes a wide array of coronary and peripheral guidewires designed to meet varying procedural complexities. Terumo’s long-standing reputation for excellence, combined with its proactive approach to regulatory compliance and customer engagement, has helped it secure a strong foothold in the region.

Top Strategies Used by Key Players

One of the primary strategies employed by key players is continuous product innovation and technological advancement . Companies are investing heavily in R&D to develop next-generation guidewires with enhanced maneuverability, radiopacity, and biocompatibility. These innovations cater to increasingly complex vascular interventions and support better clinical outcomes.

Another crucial strategy is strategic partnerships and collaborations with academic institutions, hospitals, and technology firms. These alliances help manufacturers gain real-world insights into clinical demands, accelerate product development cycles, and improve adoption rates among physicians.

Lastly, companies are focusing on expanding their geographic footprint and strengthening distribution networks . By enhancing supply chain efficiencies and forming direct sales teams, firms ensure timely product availability and superior customer service, reinforcing their market leadership in North America.

RECENT HAPPENINGS IN THE MARKET

In February 2025, Boston Scientific launched a new line of ultra-low profile guidewires specifically designed for chronic total occlusion (CTO) interventions. This launch aimed to enhance procedural success rates and reinforce Boston Scientific’s leadership in complex vascular cases.

In June 2025, Abbott expanded its vascular device portfolio by entering a strategic collaboration with a European-based medical technology firm to co-develop novel guidewire coatings that improve lubricity and reduce vessel trauma during navigation.

In October 2025, Terumo initiated a direct sales force restructuring across major U.S. markets to improve market penetration and provide more personalized support to interventional cardiologists and vascular surgeons.

In March 2025, Medtronic announced the opening of a dedicated vascular innovation center in California, focusing on accelerating the development of next-generation guidewires integrated with robotic-assisted platforms.

In November 2025, BD (Becton, Dickinson and Company) acquired a small but innovative guidewire startup specializing in AI-enabled vascular navigation systems, aiming to integrate digital guidance tools into traditional guidewire applications.

MARKET SEGMENTATION

This research report on the North American vascular guidewires market has been segmented and sub-segmented into the following categories.

By Product

-

Coronary Guidewires

-

Peripheral Guidewires

By Coating Type

-

Coated

-

Non-Coated

By End-User

-

Hospitals

-

Ambulatory Surgical Centers

By Country

-

The United States

-

Canada

-

Rest of North America

Frequently Asked Questions

Which countries dominate the North American market?

The United States holds the largest market share due to advanced healthcare infrastructure, higher healthcare spending, and a large patient population. Canada follows with increasing adoption of minimally invasive procedures.

Who are the major players in the North America vascular guidewires market?

Boston Scientific Corporation Medtronic plc Terumo Corporation Abbott Laboratories Cardinal Health B. Braun Melsungen AG

What are the major challenges facing the market?

High cost of advanced guidewires Risk of complications during procedures Regulatory barriers and approval processes Product recalls due to safety concerns

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com