North America Wooden Furniture Market Size, Share, Trends & Growth Forecast Report, Segmented By Type, Material, End-user, Distribution Channel, And By Country (USA, Canada, Mexico), Industry Analysis From 2026 to 2034

Market Size, 2025

$188.37 BnMarket Estimate, 2026

$190.47 BnMarket Forecast, 2034

$210.38 BnCAGR, 2026–2034

1.11%North America Wooden Furniture Market Report Summary

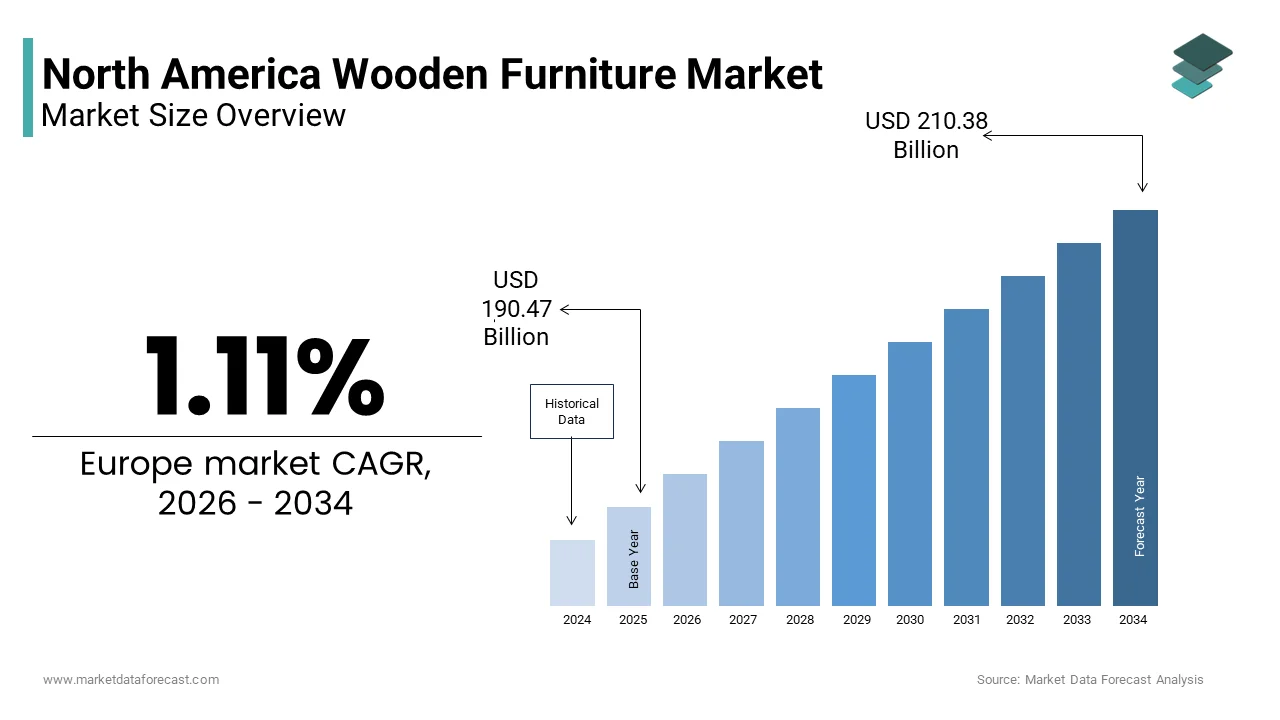

The North American wooden furniture market was valued at USD 188.37 billion in 2025, is estimated to reach USD 190.47 billion in 2026, and is projected to grow to USD 210.38 billion by 2034, expanding at a CAGR of 1.11% during the forecast period from 2026 to 2034. Market growth is primarily driven by steady residential construction, home renovation activity, long replacement cycles for furniture, and sustained consumer preference for durable and natural materials. The market benefits from the resilience of residential demand, increasing interest in solid wood craftsmanship, and gradual recovery in discretionary consumer spending. Additionally, the integration of sustainable sourcing practices and omnichannel retail strategies is supporting long-term market stability.

Key Market Trends

- Continued consumer preference for solid wood furniture due to its durability, longevity, and premium aesthetic appeal.

- Rising demand for functional wooden furniture such as dining tables, work-from-home desks, and multipurpose tablesis driven by hybrid work lifestyles.

- Growing emphasis on sustainably sourced wood and eco-certified materials, particularly in residential furniture segments.

- Gradual expansion of online and direct-to-consumer furniture sales, complemented by physical showrooms for high-value purchases.

- Increased adoption of timeless and minimalist furniture designs, favoring long-term usability over fast furniture trends.

Segmental Insights

- Based on product type, the tables segment held the largest share of the North American wooden furniture market in 2024, accounting for 28.3%, supported by strong demand across dining, office, and living room applications.

- By material, the solid wood segment dominated the market with a 42.3% share in 2024, reflecting consumer trust in durability, repairability, and premium craftsmanship.

- By end use and distribution channel, the residential segment remained dominant in 2024, driven by home renovation, replacement demand, and personalized interior design preferences.

Regional Insights

- The United States was the dominant contributor to the North American wooden furniture market, accounting for 89.3% of the regional share in 2024, supported by a large housing base, high renovation spending, and strong demand for premium and customized furniture.

- Canada represented the second-largest market, driven by sustainable housing trends, urban household growth, and a preference for eco-friendly wooden furnishings.

Competitive Landscape

The North American wooden furniture market is characterized by the presence of established global brands and strong domestic manufacturers competing on design, brand trust, sustainability, and omnichannel reach. Leading players focus on product innovation, solid wood offerings, customization, and digital retail expansion to strengthen market positioning. Prominent companies operating in the market include IKEA, Ashley Furniture Industries, Steelcase, Herman Miller, La-Z-Boy, Haverty Furniture Companies, Natuzzi, Duresta Upholstery, and Kuka Home.

North America Wooden Furniture Market Size

The North American wooden furniture market was valued at USD 188.37 billion in 2025 and is anticipated to reach USD 190.47 billion in 2026 from USD 210.38 billion by 2034, growing at a CAGR of 1.11% during the forecast period from 2026 to 2034.

Introduction to the NorthAmericana Wooden Furniture Market

The wood remains one of the dominant materials in residential and non-residential construction, with over 80% of newly built homes in 2023 incorporating solid wood or engineered wood products for interior applications. The prevalence of wood in home furnishings is further supported by the Environmental Protection Agency's data, which indicates that nearly 60% of American households prefer natural materials like wood for aesthetic and environmental reasons. Meanwhile, the National Association of Home Builders states that 72% of new single-family homes constructed in the U.S. during 2023 included hardwood flooring in at least one room.

MARKET DRIVERS

Rising Demand for Sustainable and Eco-Friendly Home Furnishings

Sustainability has become a purchase criterion are made from responsibly sourced materials, which is escalating the growth of the North American wooden furniture market. The rising demand for sustainable and eco-friendly home furnishings is significantly boosting the growth ofthe North American wooden furniture market. According to a 2023 Nielsen report, 66% of global consumers are willing to pay more for sustainable goods, with North America leading this trend. This shift is particularly pronounced in the furniture industry, where consumers increasingly seek transparency regarding sourcing practices and environmental impact. Millennials and Gen Z consumers, who represent few of homebuyers, prioritize green living, further amplifying the preference for sustainably produced wooden furniture.

Growth in Homeownership and Residential Construction Activity

The resurgence in homeownership and residential construction is additionally enhancing the growth of the North American wooden furniture market. The U.S. Department of Housing and Urban Development revealed that new home construction permits rose by 9.2% in 2023 compared to the previous year, signaling renewed confidence in the housing market. Similarly, Statistics Canada reported a 7.6% increase in residential building permits in the third quarter of 2023, primarily driven by urban infill projects and suburban expansion. Homeowners investing in property improvements often allocate substantial budgets toward interior furnishings, particularly custom wooden pieces such as dining tables, wardrobes, and shelving units. This sustained investment in home aesthetics and functionality creates a robust pipeline of demand for high-quality wooden furniture, especially among middle- and upper-income demographics seeking durability and timeless design.

MARKET RESTRAINTS

Volatility in Raw Material Prices and Lumber Costs

Fluctuations in lumber pricesares majorly degrading the growth of the North American wooden furniture market. This erratic pricing directly impacts production costs, forcing manufacturers to adjust pricing strategies and margins. The Canadian Federation of Independent Business reported that 37% of small furniture manufacturers in Canada cited raw material cost inflation as a top operational concern in 2023. In the U.S., the Producer Price Index (PPI) for wood products showed a 22% year-over-year increase in early 2022, straining profit margins for mid-sized furniture producers reliant on domestic timber supplies. Additionally, supply chain disruptions stemming from trade disputes, such as the ongoing U.S., Canada softwood lumber tariffs,s have exacerbated sourcing challenges. These persistent cost pressures limit manufacturers' ability to offer competitive pricing while maintaining quality, ultimately constraining market growth.

Increasing Competition from Alternative Materials and Imported Furniture

The alternative materials, such as metal, plastic, and composite wood substitutes, alongside a surge in low-cost imported furniture is additionally limiting the growth of the North American wooden furniture market. These products often undercut domestic wooden furniture prices due to lower labor and manufacturing costs abroad. Furthermore, innovations in engineered materials have led to enhanced performance and aesthetics, attracting price-sensitive consumers. A 2023 survey by the American Home Furnishings Alliance revealed that 31% of respondents indicated a willingness to consider non-wood alternatives for long-term durability and maintenance ease. In Canada, the Conference Board of Canada reported that 40% of furniture retailers observed declining sales of traditional solid wood items in favor of hybrid or synthetic options. This shift is particularly evident in younger demographics, where 52% of Gen Z consumers expressed openness to mixed-material designs as per a Statista consumer behavior study. The traditional wooden furniture makers must innovate or reposition their offerings to maintain market share against both international competitors and emerging material technologies.

MARKET OPPORTUNITIES

Customization and Personalization Trends Among Affluent Consumers

The increasing appetite for personalized and artisanal furniture manufacturers is creating new opportunities for the growth ofthe North American wooden furniture market. As per a 2023 McKinsey & Company consumer insights report, 58% of affluent North American households are willing to invest in bespoke furnishings to reflect individual style and craftsmanship. Custom wooden furniture allows for tailored dimensions, finishes, and functionalities by aligning with the growing emphasis on interior design personalization. Etsy’s 2023 marketplace analysis revealed that custom wooden furniture listings increased by 26% year-over-year, indicating a broader shift toward artisanal and made-to-order goods. Additionally, the rise of digital configurators and virtual showrooms enables manufacturers to offer interactive customization experiences by enhancing customer engagement and conversion rates. The Small Business Administration notes that small-scale furniture artisans employing fewer than 20 people account for 28% of all woodworking businesses in the U.S., highlighting the market’s potential for niche, high-value offerings. Manufacturers who integrate advanced design software with traditional woodworking techniques can tap into this expanding segment while commanding premium pricing.

Expansion of E-Commerce Platforms and Direct-to-Consumer Sales

The rapid digitization of retail channels through e-commerce and direct-to-consumer (DTC) models is also expected to enhance the growth of the North American wooden furniture market. Notably, wooden furniture categories such as dining sets, bedroom collections, and office desks witnessed above-average growth, driven by improved logistics and visual merchandising capabilities. Shopify’s 2023 merchant survey indicated that 39% of furniture sellers on its platform experienced over 20% revenue growth, with wooden furniture brands outperforming others due to their perceived value and aesthetic appeal. Amazon’s “Handmade” and “Local” initiativesalso provide platforms for small wooden furniture artisans to access broader markets without significant upfront investment. Additionally, the rise of augmented reality (AR) tools allows customers to visualize wooden furniture in their spaces, reducing return rates and boosting consumer confidence. Brands leveraging omnichannel strategies combining online presence with localized showrooms or pop-ups are better positioned to capture evolving consumer expectations for convenience and tactile experience.

MARKET CHALLENGES

Skilled Labor Shortage in Woodworking and Manufacturing

The shortage of skilled craftsmen and technicians capable of executing precision woodworking tasks is one of the challenges for the growth of the North American wooden furniture market. This shortage is compounded by an aging workforce, with the Bureau of Labor Statistics indicating that 22% of current furniture manufacturing workers are over the age of 55 and nearing retirement. In Canada, the Canadian Manufacturers & Exporters association noted that 43% of wood product firms struggle to fill skilled positions, particularly in CNC machining, joinery, and finishing. The lack of trained personnel not only delays production timelines but also affects product quality and innovation capacity. Educational institutions and vocational schools are attempting to bridge this gap through partnerships with industry leaders, yet the mismatch between training output and labor demand remains a persistent issue.

Stringent Environmental Regulations and Compliance Costs

The stringent environmental regulations governing emissions, waste disposal, and chemical usage in furniture manufacturingares also likely to inhibit the growth of North American wooden furniture producers. The U.S. Environmental Protection Agency enforces strict guidelines under the Clean Air Act and Toxic Substances Control Act, requiring manufacturers to adopt cleaner production technologies and reduce volatile organic compound (VOC) emissions. Compliance with these standards often necessitates capital-intensive upgrades to finishing equipment and ventilation systems. In Canada, Environment and Climate Change Canada has introduced stricter limits on formaldehyde emissions from composite wood products, whicareis affecting imported components used in domestic assembly. The California Air Resources Board reported that over 30% of furniture manufacturers faced penalties or audits in 2023 due to non-compliance with VOC standards. Additionally, certification processes for sustainable sourcing and carbon footprint tracking add administrative burdens. Companies must balance adherence to evolving regulations with maintaining profitability, especially when competing against less-regulated foreign manufacturers.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 1.11% |

| Segments Covered | By Type, Material, End-user, Distribution Channel, And By Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | United States, Canada, Mexico, etc. |

| Market Leaders Profiled | IKEA (SE), Ashley Furniture Industries (US), Steelcase (US), Herman Miller (US), La-Z-Boy (US), Haverty Furniture Companies (US), Natuzzi (IT), Duresta Upholstery (GB), Kuka Home (CN) |

SEGMENT ANALYSIS

By Product Insights

The tables segment was the largest by holding 28.3% of the North American wooden furniture market share in 2024, with the fundamental role tables play in both residential and commercial settings, serving as essential functional and aesthetic elements in dining rooms, living spaces, and work environments. The versatility of wooden tables across various interior design styles, from traditional to contemporary, ensures consistent demand regardless of shifting fashion trends. Each of these units typically incorporates 2-3 wooden tables on average, including dining tables, coffee tables, and occasional tables. The National Association of Home Builders indicates that 78% of new single-family homes include hardwood dining tables as standard furnishings, while 65% feature additional wooden accent tables. This construction-driven demand is further amplified by the preference for durable, long-lasting materials in new developments, with wooden tables offering both aesthetic appeal and functional longevity. The commercial segment has emerged as a significant growth driver for wooden table demand, particularly following the post-pandemic shift toward hybrid work environments that emphasize collaborative spaces. The trend toward biophilic design principles, which incorporate natural materials to enhance workplace wellness, has specifically favored wooden tables over alternative materials. This commercial demand is projected to grow as companies continue investing in employee-centric workspace designs that utilize natural materials to create welcoming environments.

The beds segment is lucratively growing with an anticipated CAGR of 6.8% from 2025 to 2033, owing to the changing consumer preferences toward premium bedroom furnishings and the increasing recognition of bedroom environment, as personal sanctuaries requiring investment in quality sleep solutions. The escalation in luxury home renovation projects has significantly boosted demand for high-end wooden beds and bedroom collections. Luxury furniture retailers have responded by expanding their wooden bedroom collections, with Ethan Allen reporting a 22% increase in wooden bed sales in 2023 compared to 2022. The integration of augmented reality features allows consumers to virtually place wooden beds in their bedrooms before purchase by reducing return rates by 28%, as reported by Shopify's merchant analytics. Custom wooden bed manufacturers have particularly benefited from direct-to-consumer online models, with small artisans experiencing 45% average revenue growth through digital sales channels.

By Material Insights

The solid wood segment was the largest by holding 42.3% of the North American wooden furniture market share in 2024, with the consumer perceptions of authenticity, durability, and timeless aesthetic appeal that solid wood products inherently possess. The material's natural grain patterns, ability to be refinished multiple times, and resistance to wear ensure long-term value retention that appeals to both residential and commercial buyers. Solid wood furniture commands significant pricing premiums in the North American market, with consumers demonstrating consistent willingness to pay 40-60% more for solid wood pieces compared to engineered alternatives. Wealth-X's 2023 affluent consumer report indicates that households earning over $250,000 annually allocate 12% more of their discretionary income toward solid wood furniture compared to previous years. The Smithsonian Institution's Furniture Conservation Program notes that properly maintained solid wood pieces can retain structural integrity for over 100 years.

The reclaimed wood segment is projected to grow at the fastest CAGR of 9.3% from 2025 to 2033, which is evolving consumer preferences toward sustainable living practices and unique aesthetic experiences that mass-produced furniture cannot provide. The environmental benefits of reclaimed wood furniture have become primary purchase drivers for North American consumers, increasingly concerned about sustainable living practices. The reuse of reclaimed wood prevents approximately 2.3 million tons of wood waste from entering landfills annually, according to Environmental Protection Agency waste diversion statistics. The distinctive visual characteristics of reclaimed wood, including weathering marks, nail holes, and color variations, provide aesthetic uniqueness that cannot be replicated through conventional manufacturing processes. Interior design professionals report that 62% of high-end residential projects in 2023 incorporated reclaimed wood elements to create signature design statements,s according to the American Society of Interior Designers' annual survey. Custom furniture makers specializing in reclaimed wood report average project values 85% higher than conventional wood projects, reflecting consumer willingness to pay premiums for unique aesthetic experiences. This visual appeal extends to commercial applications, where hospitality and restaurant sectors utilize reclaimed wood furniture to create distinctive brand identities that differentiate them from competitors.

By End Use and Distribution Channel Insights

The residential segment held a dominant share of the North American wooden furniture market in 2,024 owing to the fundamental role that wooden furniture plays in creating comfortable, aesthetically pleasing home environments. Residential consumers consistently prioritize durability, aesthetic appeal, and long-term value when making furniture purchases, characteristics that wooden furniture inherently provides. Steady household formation rates and sustained homeownership levels continue to drive robust demand for residential wooden furniture across North America. These new homeowners demonstra ate higher propensity for wooden furniture investments, with 74% indicating preferences for natural materials over synthetic alternatives in initial furnishing decisions. Regional variations show particularly strong demand in suburban markets, where newly constructed homes feature extensive wooden furniture packages including dining sets, bedroom suites, and living room collections.

The online retail segment is expected to grow at the fastest CAGR of 12.4% from 2025 to 2033, with the growth trajectoryreflectings fundamental shifts in consumer shopping behaviors, technological advancements in e-commerce platforms, and improved logistics capabilities that have made purchasing large furniture items online increasingly convenient and reliable. Advanced technological features integrated into online furniture retail platforms have revolutionized consumer confidence and purchasing behavior for wooden furniture. Significant investments in logistics infrastructure and delivery capabilities have addressed traditional barriers to online furniture purchasing, particularly concerns about damage during shipping and complex assembly requirements.

COUNTRY ANALYSIS

United States Wooden Furniture Market Analysis

The United States was the top performer of the North American wooden furniture market by holding 89.3% of the share in 2024, with the country's vast consumer base, diverse demographic preferences, and robust manufacturing infrastructure that supports both domestic production and import activities. The U.S. Census Bureau reported that 1.5 million new housing units received building permits in 2023, representing the highest level since 2007 and indicating strong underlying demand for residential furnishings. Apartment developers increasingly specify wooden furniture for lobby areas, community rooms, and rental units to create premium living experiences that justify higher rents. The trend toward urban infill projects in major metropolitan areas such as New York, Los Angeles, and Chicago has created concentrated demand zones that support specialized wooden furniture suppliers and custom manufacturers. Regional variations in wood species preferences reflect local architectural traditions and climate considerations, with oak dominant in the Midwest, maple popular in New England, and cherry favored in the Mid-Atlantic states,s according to the Hardwood Manufacturers Association regional preference survey.

Canada Wooden Furniture Market Analysis

Canada wooden furniture market was next in accounting for a significant share in 2024. Canada has a strong forestry heritage, a well-established manufacturing base, and consumer preferences that align closely with premium wooden furniture offerings. Canada's position as a global forestry leader directly influences its wooden furniture market dynamics, with the country ranking fifth worldwide in forest area coverage and maintaining sustainable harvesting practices that support long-term material availability. This localization trend is particularly pronounced in provinces with established furniture manufacturing traditions, such as Ontario and British Columbia, where regional brands command significant market share despite higher price points. The Canadian government's emphasis on sustainable development has created favorable conditions for wooden furniture manufacturers, with federal procurement policies favoring domestically produced sustainable furniture for public sector projects.

COMPETITIVE LANDSCAPE

The North American wooden furniture market exhibits intense competitive dynamics characterized by the coexistence of large-scale manufacturers, regional specialists, and emerging boutique brands vying for market share across diverse consumer segments. The competitive landscape is shaped by factors including brand reputation, product quality, pricing strategies, distribution capabilities, and innovation in design and manufacturing technologies. Established players leverage their extensive resources and market presence to maintain leadership positions through economies of scale, comprehensive product portfolios, and robust distribution networks. However, smaller manufacturers and artisanal brands compete effectively by emphasizing unique design aesthetics, superior craftsmanship, and personalized customer service that larger competitors may struggle to replicate. The market's fragmentation creates opportunities for niche players to capture specialized segments while established companies pursue market consolidation through strategic acquisitions and partnerships. Competition intensity varies across product categories, with mass-market segments experiencing price-based competition while premium segments focus on differentiation through quality, design innovation, and brand positioning. The increasing importance of sustainability and environmental responsibility has created new competitive dimensions where companies must balance traditional competitive factors with emerging consumer priorities related to ethical manufacturing and environmental impact.

KEY MARKET PLAYERS

A Few of the dominant players in the North American wooden furniture market are

- IKEA (SE)

- Ashley Furniture Industries (US)

- Ethan Allen Inc.

- Bassett Furniture Industries Inc.

- Steelcase (US)

- Herman Miller (US)

- La-Z-Boy (US)

- Haverty Furniture Companies (US)

- Natuzzi (IT)

- Duresta Upholstery (GB)

- Kuka Home (CN)

Top Players In The Market

- Ashley Furniture Industries stands as the dominant force in the North American wooden furniture market, operating as both a manufacturer and retailer with extensive vertical integration capabilities. The company's comprehensive approach spans from raw material sourcing to final product delivery, enabling cost efficiencies and quality control throughout the production process. Ashley's extensive distribution network encompasses company-owned retail stores, independent dealers, and online platforms, providing ubiquitous market coverage across diverse consumer segments. Their product portfolio ranges from affordable mass-market wooden furniture to premium collections, catering to varying income demographics and design preferences. The company's investment in automated manufacturing technologies has enhanced production capabilities while maintaining competitive pricing structures. Ashley's commitment to sustainable practices includes sourcing certified wood materials and implementing environmentally responsible manufacturing processes.

- Ethan Allen represents the pinnacle of luxury wooden furniture manufacturing in North America, distinguished by its focus on high-end custom and semi-custom furniture solutions. The company's vertically integrated business model encompasses design services, manufacturing facilities, and exclusive retail showrooms, creating a seamless customer experience from initial consultation to final installation. Ethan Allen's reputation for exceptional craftsmanship and timeless design aesthetics has cultivated a loyal customer base among affluent consumers seeking premium wooden furniture investments. Their team of interior designers provides personalized consultation services, ensuring that each furniture piece aligns with individual client preferences and spatial requirements. The company's commitment to traditional woodworking techniques, combined with modern manufacturing efficiencies, produces furniture that balances artisanal quality with contemporary functionality. Ethan Allen's emphasis on sustainable practices includes partnerships with certified forestry operations andthe implementation of eco-friendly finishing processes. Their extensive training programs for design consultants and craftsmen ensure consistent quality standards while maintaining the company's heritage of excellence in wooden furniture creation.

- Bassett Furniture Industries maintains a prominent position in the North American wooden furniture market through its specialized focus on bedroom and dining room furniture collections. The company's heritage, dating back to 191,9 has established strong brand recognition for quality craftsmanship and traditional American furniture design. Bassett's manufacturing facilities utilize both domestic and imported wood species to create diverse product lines that appeal to various consumer preferences and budget considerations. Their retail strategy emphasizes partnership with independent furniture dealers, creating an extensive network of showrooms that showcase their wooden furniture collections while maintaining local market presence. The company's investment in computer-aided design and manufacturing technologies has enhanced product development capabilities while preserving traditional woodworking techniques. Bassett's commitment to customer satisfaction includes comprehensive warranty programs and responsive customer service that supports long-term product performance. Their adaptive business model has successfully navigated industry challenges while maintaining profitability and market relevance through strategic focus on core competencies in bedroom and dining furniture manufacturing.

Top Strategies Used By Key Market Participants

Vertical Integration and Supply Chain Control

Leading North American wooden furniture manufacturers have increasingly adopted vertical integration strategies to gain greater control over their supply chains and production processes. This approach involves acquiring or developing capabilities across multiple stages of the furniture manufacturing value chain, from raw material sourcing and processing to final product assembly and distribution. By controlling upstream activities such as lumber procurement, wood processing, and component manufacturing, companies can ensure consistent quality standards while reducing dependency on external suppliers. This strategy also enables better cost management by eliminating intermediary markups and providing greater visibility into material costs and availability. Additionally, vertical integration allows manufacturers to respond more quickly to market demands and design changes, as they maintain direct control over production timelines and customization capabilities. The approach has proven particularly valuable in managing supply chain disruptions and material shortages that have characterized recent market conditions.

Digital Transformation and E-commerce Expansion

Market leaders have aggressively pursued digital transformation initiatives to enhance their online presence and capitalize on the growing preference for digital shopping experiences. This strategy encompasses comprehensive website development, implementation of advanced e-commerce platforms, and integration of digital marketing technologies to reach broader consumer audiences. Companies are investing heavily in virtual reality and augmented reality technologies that allow customers to visualize furniture pieces within their own spaces before making purchase decisions. Social media engagement and influencer partnerships have become integral components of digital marketing strategies, enabling brands to showcase their wooden furniture collections to targeted demographics. Additionally, manufacturers are implementing sophisticated customer relationship management systems to personalize shopping experiences and improve customer retention. The digital transformation extends to internal operations through enterprise resource planning systems and automated inventory management, enhancing operational efficiency while supporting omnichannel retail strategies.

Sustainable Manufacturing and Eco-Friendly Product Development

Environmental consciousness has emerged as a critical strategic focus for North American wooden furniture manufacturers seeking to align with evolving consumer preferences and regulatory requirements. Leading companies are implementing comprehensive sustainability initiatives that encompasthe s responsible sourcing of wood materials, the adoption of eco-friendly manufacturing processes, and the development of environmentally conscious product lines. This strategy involves obtaining certifications from recognized environmental organizations and implementing circular economy principles that minimize waste generation and promote material recycling. Manufacturers are increasingly utilizing reclaimed wood and rapidly renewable materials in their product offerings to appeal to environmentally conscious consumers. Energy efficiency improvements in manufacturing facilities, water conservation measures, and the reduction of harmful chemical usage in finishing processes represent additional components of sustainable manufacturing strategies. Companies are also developing take-back programs and furniture recycling initiatives to extend product lifecycle management and demonstrate corporate environmental responsibility.

MARKET SEGMENTATION

This is the research report on the North American wooden furniture market, which is segmented and sub-segmented into the following categories.

By Type

- Sofas

- Chairs

- Tables

- Beds

- Cabinets

By End-user

- Residential

- Commercial

- Institutional

By Material

- Solid Wood

- Engineered Wood

- Reclaimed Wood

- Composite Wood

By Distribution Channel

- Online Retail

- Offline Retail

- Direct Sales

By Country

- United States

- Canada

- Mexico

Frequently Asked Questions

What is the North America wooden furniture market?

The North America wooden furniture market includes the production, distribution, and sale of interior and exterior furniture primarily made of wood for residential, office, hospitality, and outdoor use.

Why is wooden furniture popular in North America?

Wooden furniture is valued for its durability, natural aesthetics, sustainability potential, and long lifespan, making it a preferred choice for homes and businesses.

What drives growth in the North America wooden furniture market?

Growth is driven by housing market expansion, rising disposable incomes, consumer preference for natural materials, eco-friendly trends, and increasing renovation and hospitality investments.

What types of wooden furniture are included in this market?

Key categories include living room, bedroom, dining, office, outdoor, and accent furniture, across various wood types and finishes.

How does sustainability impact the market?

Consumers increasingly demand sustainably sourced wood, FSC certification, low-VOC finishes, recycled wood blends, and eco-friendly manufacturing processes.

Which wood types are most commonly used?

Common wood types include oak, maple, walnut, cherry, pine, teak, and engineered woods like plywood and MDF.

Who are the main buyers of wooden furniture?

Major buyers include homeowners, renters, interior designers, commercial businesses, hospitality operators, and institutional purchasers.

How does online retail affect the wooden furniture market?

Online sales growth provides broader consumer reach, virtual customization tools, convenient delivery, and access to niche and direct-to-consumer wooden furniture brands.

What challenges does the market face?

Challenges include volatile raw material costs, supply chain disruptions, import/export fluctuations, labor shortages, and environmental regulations.

How do trends like customization affect demand?

Customization fuels demand as consumers seek bespoke design, unique finishes, modular systems, and furniture tailored for small or multifunctional spaces.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com