Global Nylon Market Size, Share, Trends & Growth Forecast Report – Segmented By Type (Nylon 6, Nylon 6,6), Application, and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) - Industry Analysis From 2025 to 2033

Global Nylon Market Summary

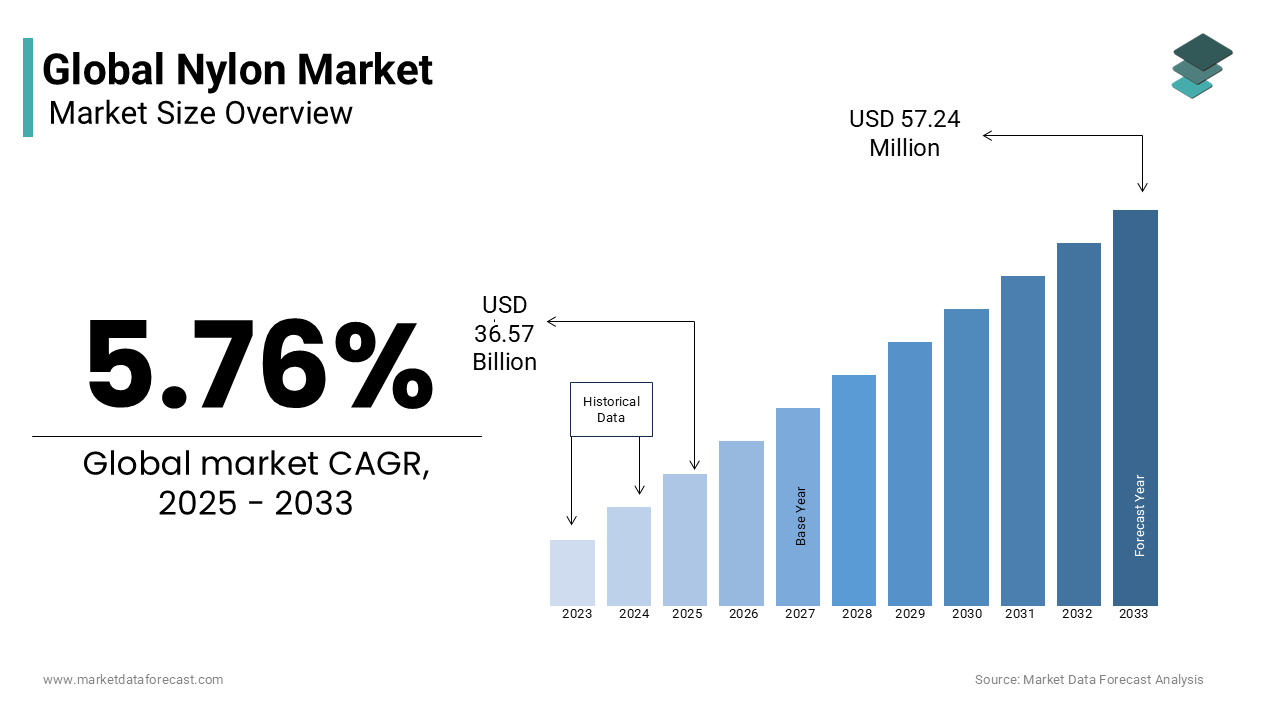

The global nylon market was valued at USD 34.58 billion in 2024, is estimated to reach USD 36.57 billion in 2025, and is projected to expand to USD 57.24 billion by 2033, growing at a CAGR of 5.76% from 2025 to 2033. The growth of the global nylon market is attributed to the increasing demand for lightweight, durable materials in the automotive and electronics industries, rising applications in packaging and textiles, and the expanding use of nylon in industrial machinery and engineering plastics.

Key Market Trends

- Rising adoption of lightweight materials in automotive and aerospace to improve fuel efficiency.

- Increasing use of nylon in electrical and electronics for wiring and insulation applications.

- Expanding applications of nylon films and fibers in packaging, textiles, and consumer goods.

- Growing investments in bio-based and recycled nylon production to meet sustainability goals.

- Continuous innovation in engineering plastics supporting high-performance industrial applications.

Segmental Insights

- Based on type, the Nylon 6 segment dominated the market with 62.7% share in 2024, driven by its affordability, durability, and wide application in textiles, packaging, and automotive components.

- Based on application, the automotive segment led the market with 34.3% share in 2024, fueled by rising demand for lightweight materials to enhance efficiency and reduce emissions.

Regional Insights

- Asia-Pacific was the top-performing region in the global nylon market, accounting for 58.4% share in 2024, supported by robust growth in automotive, electronics, and textile manufacturing industries.

- North America showed steady growth due to advanced engineering applications and strong automotive production.

- Europe maintained a significant position, driven by sustainability regulations and industrial demand.

- Latin America is expanding gradually with increasing adoption of nylon in packaging and consumer products.

- Middle East & Africa are emerging markets, supported by growing demand in construction and industrial sectors.

Competitive Landscape

Key players in the global nylon market include BASF SE, DuPont de Nemours, Inc., Invista (Koch Industries, Inc.), Ascend Performance Materials LLC, Lanxess AG, Solvay S.A., Toray Industries, Inc., UBE Industries Ltd., Radici Group, Domo Chemicals, Formosa Plastics Corporation, Hyosung Chemical, Nilit Ltd., and Shenma Industrial Co., Ltd. These companies are focusing on expanding production capacity, innovating bio-based nylon solutions, and strengthening supply chains to maintain competitiveness.

Global Nylon Market Size

The Nylon Market was valued at USD 34.58 billion in 2024, is estimated to reach USD 36.57 billion in 2025, and is projected to reach USD 57.24 billion by 2033, growing at a CAGR of 5.76% from 2025 to 2033.

Nylon is a synthetic polyamide polymer. It is distinguished by its high tensile strength, abrasion resistance, thermal stability, and versatility in both fiber and engineering resin forms. First developed by DuPont in the 1930s, nylon has evolved into a foundational material across industries ranging from automotive and electronics to textiles and consumer goods. Its molecular structure enables exceptional durability under mechanical stress, making it ideal for applications such as gears, bearings, tire cords, and sportswear. According to the study, notable metric tons of nylon were produced globally, with a significant portion integrated into long-life industrial components rather than disposable items. As per the American Chemistry Council, nylon 6 and nylon 6,6 account for more than 85% of total production, derived from monomers like caprolactam and hexamethylenediamine. As per the research, nylon-based composites are replacing metals in lightweight automotive systems, reducing vehicle mass in specific components, thereby enhancing fuel efficiency and lowering emissions.

MARKET DRIVERS

Expansion of Lightweight Materials in Automotive Engineering

The automotive industry’s relentless pursuit of fuel efficiency and emissions reduction accelerates the growth of the nylon market. Engineering-grade nylons, particularly nylon 6,6 and glass-enhanced variants, are being increasingly adopted in under-the-hood components such as radiator end tanks, air intake manifolds, and sensor housings due to their ability to withstand high temperatures and corrosive fluids. According to the study, every reduction in vehicle weight improves fuel economy, prompting automakers to replace metal parts with high-performance polymers. As per the research, nylon usage in passenger vehicles has increased over the past decade, with a car containing kgs of nylon-based components. In electric vehicles, nylon is used in battery enclosures and charging connectors for its electrical insulation and flame-retardant properties.

Rising Demand for High-Performance Textiles in Technical Apparel

The global surge in demand for functional and performance-driven textiles, particularly in sportswear, outdoor gear, and protective clothing, propels the growth of nylon market. Nylon’s superior elasticity, moisture wicking, and resistance to UV degradation make it ideal for activewear and military uniforms. According to the study, sales of performance apparel in North America exceeded in notable billion in 2023. The U.S. Army’s adoption of nylon-blend combat uniforms, which offer enhanced durability and ballistic protection, reflects its strategic importance in defense applications. Apart from these, the rise of athleisure has blurred the line between sport and casual wear by increasing consumer preference for stretchable and wrinkle-resistant materials. Therefore, nylon remains indispensable in the evolution of modern technical textiles because brands are prioritizing long-lasting and high-function fabrics.

MARKET RESTRAINTS

Dependence on Petrochemical Feedstocks and Price Volatility

Heavy reliance on fossil fuel-derived intermediates such as benzene, butadiene, and adipic acid restricts the growth of nylon market. This dependency exposes the market to fluctuations in crude oil prices and geopolitical supply disruptions. According to the International Energy Agency, crude oil prices decreased between 2022 and 2023, directly impacting the cost of caprolactam and hexamethylenediamine—key precursors for nylon 6 and nylon 6,6. As per the research, an increase in crude prices can raise nylon manufacturing costs, squeezing profit margins for producers and discouraging long-term contracts. Apart from these, adipic acid production generates nitrous oxide (N₂O), a potent greenhouse gas with 265 times the global warming potential of CO₂. These environmental and economic vulnerabilities are prompting regulatory scrutiny and pushing companies to seek alternative and sustainable feedstocks.

Environmental Impact of Microfiber Shedding and Non-Biodegradability

Nylon’s environmental footprint is increasingly scrutinized due to its persistence in ecosystems and contribution to microplastic pollution, which impedes the growth of the nylon market. When nylon textiles are washed, they release microfibers that infiltrate waterways and marine environments. According to the research, synthetic fibers account for a portion of primary microplastics in oceans, with nylon being one of the most persistent due to its resistance to biodegradation. As per a study by the University of Plymouth, washing synthetic clothes releases hundreds of thousands of microfibers into wastewater. The European Chemicals Agency has classified certain synthetic fibers as Substances of Very High Concern (SVHC) under REACH, potentially leading to future restrictions. Furthermore, nylon does not decompose naturally. It can persist in landfills for a long period of time. These ecological concerns are driving consumer backlash and regulatory burden, which compels brands to explore biodegradable alternatives or closed-loop recycling systems.

MARKET OPPORTUNITIES

Development of Bio-Based and Recycled Nylon

The emergence of bio-based and mechanically/chemically recycled nylon is setting up new opportunities for the growth of nylon market. Companies are developing nylon from renewable feedstocks such as castor oil, corn, and lignin, reducing reliance on fossil fuels. Arkema's Rilsan PA11, derived from castor beans, has been shown to emit approximately 70% less carbon dioxide than conventional nylon 6. Similarly, Aquafil’s ECONYL regenerated nylon, produced from fishing nets, fabric scraps, and industrial waste, has diverted metric tons of waste from landfills and oceans since 2011, according to the company’s sustainability report. The Cradle to Cradle Products Innovation Institute certifies several recycled nylon products for material health and recyclability. Thus, demand for circular nylon solutions is accelerating as the EU Strategy for Plastics mandating that all plastic packaging be reusable or recyclable by 2030. Fashion brands have committed to recycled or bio-based nylon in their collections, which signals a structural shift in material sourcing.

Integration into Additive Manufacturing and 3D Printing

Emergence as a preferred material in industrial additive manufacturing (AM), particularly in selective laser sintering (SLS) and fused filament fabrication (FFF) processes, provides new opportunities for the nylon market. This emergence is due to its excellent mechanical properties and design flexibility. According to the research, a portion of functional 3D-printed parts in aerospace, automotive, and medical devices use nylon-based powders. These materials enable rapid prototyping, complex geometries, and lightweight end-use components without tooling costs. As per the study, GE Aviation has 3D-printed nylon fuel nozzles for LEAP engines, reducing part count and weight. In healthcare, customized nylon prosthetics and surgical guides are improving patient outcomes. The U.S. Food and Drug Administration has cleared multiple nylon-based 3D-printed medical devices, strengthening regulatory acceptance. Hence, nylon’s role in digital manufacturing is poised for exponential growth.

MARKET CHALLENGES

Technical Limitations in High-Humidity and Hydrolytic Environments

Nylon exhibits significant hygroscopicity by absorbing moisture from the environment, which compromises its mechanical performance in high-humidity or aqueous conditions, challenges the growth of the nylon market. According to the American Society for Testing and Materials, nylon 6 can absorb up to 2.5% of its weight in water at 50% relative humidity, leading to dimensional instability and reduced tensile strength. In automotive applications, this can result in warping of intake manifolds or sensor housings. The European Polymer Journal emphasizes that prolonged exposure to hot water or steam can cause hydrolysis, particularly in nylon 6,6, degrading polymer chains and shortening component lifespan. This limitation necessitates protective coatings or copolymer modifications, increasing production complexity and cost. In marine and outdoor applications, hydrolytic degradation reduces durability by requiring alternative materials or hybrid designs. Overcoming this inherent vulnerability remains an important technical hurdle for broader adoption in demanding environments.

Intensifying Regulatory and Consumer Demand for Circularity

The increasing push from regulators and consumers to transition toward circular models, yet recycling infrastructure remains underdeveloped and economically constrained, degrading the growth of the nylon market. Mechanical recycling of nylon is limited by degradation in polymer chain length after repeated processing, reducing performance. According to the study, only a portion of global plastic waste is recycled, with engineering plastics like nylon facing even lower recovery rates due to sorting challenges. Chemical recycling, which breaks nylon down to monomers for repolymerization, is promising but costly. As per the study, depolymerization technologies require more energy than virgin production. The EU’s Ecodesign for Sustainable Products Regulation (ESPR) mandates digital product passports and recycled content thresholds, compelling manufacturers to redesign supply chains. However, the lack of standardized collection systems for post-industrial and post-consumer nylon waste hampers scalability. Bridging this gap demands coordinated investment in sorting, logistics, and policy alignment to make circular nylon commercially viable.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Type, Application and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East, and Africa |

| Key Market Players | BASF SE, DuPont de Nemours, Inc., Invista (Koch Industries, Inc.), Ascend Performance Materials LLC, Lanxess AG, Solvay S.A., Toray Industries, Inc., UBE Industries Ltd., Radici Group, Domo Chemicals, Formosa Plastics Corporation, Hyosung Chemical, Nilit Ltd., and Shenma Industrial Co., Ltd. |

SEGMENTAL ANALYSIS

By Type Insights

The Nylon 6 segment was the prominent type in the nylon market by capturing a 62.7% of the global market share in 2024. The growth of the Nylon 6 segment is driven by its versatility, cost efficiency, and well-established supply chain, particularly in fiber and engineering resin applications. The widespread availability of caprolactam, its primary feedstock, which is produced at scale in China and Europe, also propels the growth of this segment. According to the study, notable metric tons of caprolactam were produced globally, with China accounting for a portion of the output. This regional concentration enables lower production costs and faster integration into downstream industries. Nylon 6 fiber is extensively used in textiles, including apparel, carpets, and tire cords, due to its excellent dyeability and abrasion resistance. Its compatibility with recycling streams, both mechanical and chemical, further enhances its industrial appeal.

The Nylon 6,6 segment is anticipated to witness the fastest CAGR of 6.8% from 2025 to 2033. Factors such as its superior thermal stability, chemical resistance, and mechanical performance in high-stress engineering applications are boosting the expansion of nylon6,6 segment in the global market. Unlike nylon 6, nylon 6,6 requires both adipic acid and hexamethylenediamine (HMD), giving it a more uniform molecular structure and higher melting point (265°C vs. 220°C), making it ideal for under-the-hood automotive components and electrical insulation. According to the research, a portion of air intake manifolds in modern internal combustion and hybrid vehicles use nylon 6,6 due to its ability to withstand prolonged exposure to heat and engine fluids. Apart from these, rising demand for high-performance connectors and battery housings in electric vehicles is accelerating adoption. Hence, its performance advantages make it indispensable in next-generation mobility and industrial systems.

By Application Insights

The automotive segment led nylon market by capturing 34.3% of the global market share in 2024. The growth of the automotive segment is driven by the material’s important role in lightweighting, fuel efficiency, and durability across vehicle systems. Nylon 6 and nylon 6,6 are used in over 100 components per vehicle, including radiator end tanks, fuel lines, sensor housings, and engine covers. According to the study, polymer-based materials constitute a portion of average vehicle weight, with engineering nylons being the most prevalent high-performance option. In electric vehicles, nylon is essential for battery cooling plates, charging inlets, and high-voltage cable insulation due to its flame-retardant and dielectric properties. Therefore, demand for high-temperature-resistant nylon continues to rise across both combustion and electric platforms.

The Electrical & Electronics (E&E) segment is on the rise and is expected to be the fastest growing segment in the global market by witnessing a CAGR of 7.2% during the forecast period. The proliferation of compact and high-performance electronic devices requiring materials with excellent insulation, dimensional stability, and flame resistance is accelerating the expansion of Electrical & Electronics (E&E) segment in the global market. Nylon 6,6 and glass-reinforced grades are widely used in connectors, switches, circuit breakers, and semiconductor packaging due to their ability to withstand soldering temperatures and resist tracking under electrical stress. According to the study, a portion of consumer electronics connectors contain nylon-based components. The rise of 5G infrastructure, IoT devices, and power electronics in renewable energy systems has further amplified demand. Apart from these, the shift toward miniaturization requires polymers that maintain integrity at microscopic scales, which is a niche where nylon excels, ensuring sustained growth in this high-tech domain.

REGIONAL ANALYSIS

Asia Pacific Nylon Market Insights

Asia-Pacific outperformed other regions in the nylon market in 2024 by accounting for 58.4% of the global market share. The dominant position of Asia Pacific in the global market can be attributed to China, which functions as the world’s largest producer and consumer of both nylon 6 and caprolactam. According to the China Petroleum and Chemical Industry Federation, China produced large metric tons of caprolactam, supporting a vast downstream textile and automotive manufacturing base. India and Southeast Asian nations are rapidly expanding their use of engineering plastics in automotive components and consumer electronics. As per the research, regional electronics exports exceeded a substantial amount in 2023, driving demand for high-performance insulating materials. Japan remains a leader in high-grade nylon resins for precision machinery and robotics. Also, government initiatives like Make in India and China’s Dual Circulation strategy are promoting domestic manufacturing. Asia-Pacific continues to serve as the primary engine of global nylon demand and integrating production from raw materials to finished goods.

North America Nylon Market Insights

North America is the next prominent region in the nylon market with 16.5% share of the global market in 2024. Factors such as the advanced automotive manufacturing, aerospace engineering, and high-end electronics are majorly driving the North America in this market. The United States serves as the primary consumer and innovation hub. The U.S. auto industry consumes significant metric tons of engineering thermoplastics annually, with nylon being a key material for under-the-hood applications, as per the study. Companies like DuPont and Invista maintain R&D centers focused on high-temperature, flame-retardant, and recycled nylon formulations. The Department of Energy supports initiatives to increase polymer recycling, including nylon, under the Plastics Innovation Challenge. Apart from these, the aerospace sector uses nylon in wire harnesses and interior components due to its low smoke and toxicity emissions. Hence, demand for performance-grade nylon is expected to rise, which strengthens North America’s role as a high-value and technology-driven market.

Europe Nylon Market Insights

Europe is moving ahead steadfastly in the nylon market, with Germany, Italy, and France leading in automotive, industrial machinery, and textile applications. The region emphasizes sustainability and regulatory compliance, positioning it as a leader in circular economy practices for polymers. According to the study, a portion of nylon used in the EU is recycled or bio-based, supported by schemes. Germany’s automotive industry, the largest in Europe, relies heavily on nylon 6,6 for fuel-efficient and electric vehicle components. As per research, a portion of fluid-handling systems in industrial machinery use nylon tubing due to its chemical resistance. Apart from these, the EU’s Green Deal and Ecodesign Directive are accelerating the shift toward durable, repairable, and recyclable materials by favoring high-performance polymers like nylon. Europe remains an important market for advanced, sustainable nylon solutions due to strict emissions targets and a strong industrial base.

Latin America Nylon Market Insights

Latin America grew gradually in the nylon market, with Brazil and Mexico serving as the primary industrial centers. Brazil is the largest consumer, driven by its automotive, textile, and appliance sectors. According to the study, a portion of new passenger vehicles produced in the country incorporates nylon-based components for lightweighting and corrosion resistance. The automotive industry in Mexico, integrated into North American supply chains, uses nylon in wiring harnesses, connectors, and interior trims for export-oriented production. As per the research, nylon fiber demand in sportswear and hosiery has grown, supported by rising middle-class consumption. However, local resin production remains limited, with most nylon grades imported from the U.S. and Europe. Despite infrastructure challenges, growing industrialization and regional trade agreements are expected to gradually expand the market’s footprint in the coming decade.

Middle East and Africa Nylon Market Insights

The Middle East and Africa are expected to grow in the nylon market during the forecast period, with South Africa, Saudi Arabia, and the UAE as the main demand centers. South Africa hosts the region’s most developed plastics processing industry, using nylon in automotive parts, electrical components, and industrial machinery. In the Gulf, rapid urbanization and infrastructure development are increasing demand for durable materials in HVAC systems, wiring, and construction films. The Saudi Vision 2030 program includes the expansion of domestic manufacturing, including polymers and composites. As per the study, Saudi Arabia is investing in integrated chemical parks to produce downstream derivatives, potentially including nylon intermediates. Current consumption is low. But, long-term industrial diversification plans suggest gradual growth in high-value polymer applications.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

- BASF SE

- DuPont de Nemours, Inc.

- Invista (Koch Industries, Inc.)

- Ascend Performance Materials LLC

- Lanxess AG

- Solvay S.A.

- Toray Industries, Inc.

- UBE Industries Ltd.

- Radici Group

- Domo Chemicals

- Formosa Plastics Corporation

- Hyosung Chemical

- Nilit Ltd.

- Shenma Industrial Co., Ltd.

The nylon market features a competitive landscape defined by technological differentiation, regional supply chain dynamics, and evolving sustainability standards. Competition is intensifying in high-value applications such as electric mobility, 3D printing, and performance textiles, where material performance and environmental credentials determine market access. The absence of a dominant substitute for nylon in important engineering roles gives established players an advantage, but the rising burden to decarbonize and circularize is reshaping competitive priorities. Companies are increasingly evaluated on their ability to offer traceable, low-impact materials rather than just price and volume. In Asia-Pacific, the convergence of industrial growth, regulatory ambition, and consumer awareness is accelerating innovation, which makes the region the epicenter of strategic rivalry in next-generation nylon development.

Top Players in the Nylon Market

Ube Industries, Ltd.

Ube Industries, a Japanese multinational, is a leading producer of nylon 6 resin and caprolactam, with a strong and expanding presence across the Asia-Pacific region. The company operates integrated production facilities in Japan and has established strategic partnerships with automotive and electronics manufacturers in South Korea, Thailand, and India. It also enhanced its technical service team to support customers in product development and material selection. Ube has invested in sustainable production methods, including energy-efficient polymerization processes, to align with regional environmental regulations. Ube has positioned itself as a trusted innovation partner in Asia-Pacific’s advanced manufacturing ecosystem.

Invista S.à r.l.

Invista, a global leader in polymer and fiber technologies, maintains a significant footprint in the Asia-Pacific nylon market through its flagship brand STAINMASTER for carpets and COOLMAX for performance textiles. The company supplies nylon 6,6 resin and fiber to major apparel, automotive, and industrial customers across China, India, and Vietnam. It also upgraded its regional distribution network in Southeast Asia to improve delivery times for industrial customers. Also, the initiatives strengthen Invista’s reputation as a technology-driven and customer-centric supplier in one of the world’s most dynamic markets.

BASF SE

BASF, headquartered in Germany, plays a pivotal role in the Asia-Pacific nylon market through its high-performance engineering plastics and chemical intermediates. The company supplies nylon 6 and nylon 6,6 resins to automotive, electrical, and industrial clients in China, South Korea, and India, with production and compounding facilities in Nanjing and Mumbai. The company has strengthened its application development centers in Shanghai and Seoul to provide localized engineering support. BASF has strengthened its position as a key enabler of advanced manufacturing across the region.

Top Strategies Used by the Key Market Participants

Key players in the nylon market are deploying integrated strategies to maintain prominence amid rising competition and sustainability demands. Major approaches include vertical integration into feedstock production to secure supply and reduce cost volatility, particularly for caprolactam and adipic acid. Companies are investing in R&D to develop high-performance, flame-retardant, and lightweight grades tailored for electric vehicles and electronics. Sustainability is a central focus, with firms expanding production of bio-based and chemically recycled nylon to meet regulatory and consumer expectations. Strategic partnerships with automakers, textile brands, and electronics manufacturers enable co-development of application-specific materials. Geographic expansion in high-growth regions like India and Southeast Asia is being pursued through local compounding centers and technical service hubs. Digital tools such as material simulation software and lifecycle assessments are also being leveraged to enhance customer engagement and demonstrate environmental compliance.

MARKET SEGMENTATION

The research report on the Nylon Market has been segmented and sub-segmented based on categories.

By Type

- Nylon 6

- Resin

- Fiber

- Nylon 6,6

- Resin

- Fiber

By Application

- Automotive

- Electrical & Electronics

- Appliances

- Film & Coating

- Wire & Cable

- Consumer

- Industrial & Machinery

- Others

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

Which industries use nylon the most?

Major industries include textiles and apparel, automotive and transportation, packaging, electrical and electronics, industrial machinery, and consumer goods.

What factors are driving the growth of the nylon market?

Growth is driven by rising demand for lightweight and durable materials in automotive, increasing textile production, expansion of the electronics industry, and growing applications in packaging and consumer goods.

What are the challenges faced by the nylon market?

Key challenges include fluctuating raw material prices (especially crude oil derivatives), environmental concerns related to plastic waste, and competition from alternative polymers and bioplastics.

Which region dominates the global nylon market?

Asia-Pacific dominates the nylon market due to strong manufacturing bases in China, India, and Japan, along with high demand from textiles, automotive, and electronics sectors.

What is the future outlook for the nylon market?

The nylon market is expected to grow steadily, supported by innovations in high-performance grades, rising demand in EVs and electronics, and a push towards sustainable materials.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com