Global Organic Electronics Market Size, Share, Trends & Growth Forecast Report By Material, By Application, and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa) – Industry Analysis and Forecast, 2026 to 2034

Global Organic Electronics Market Size

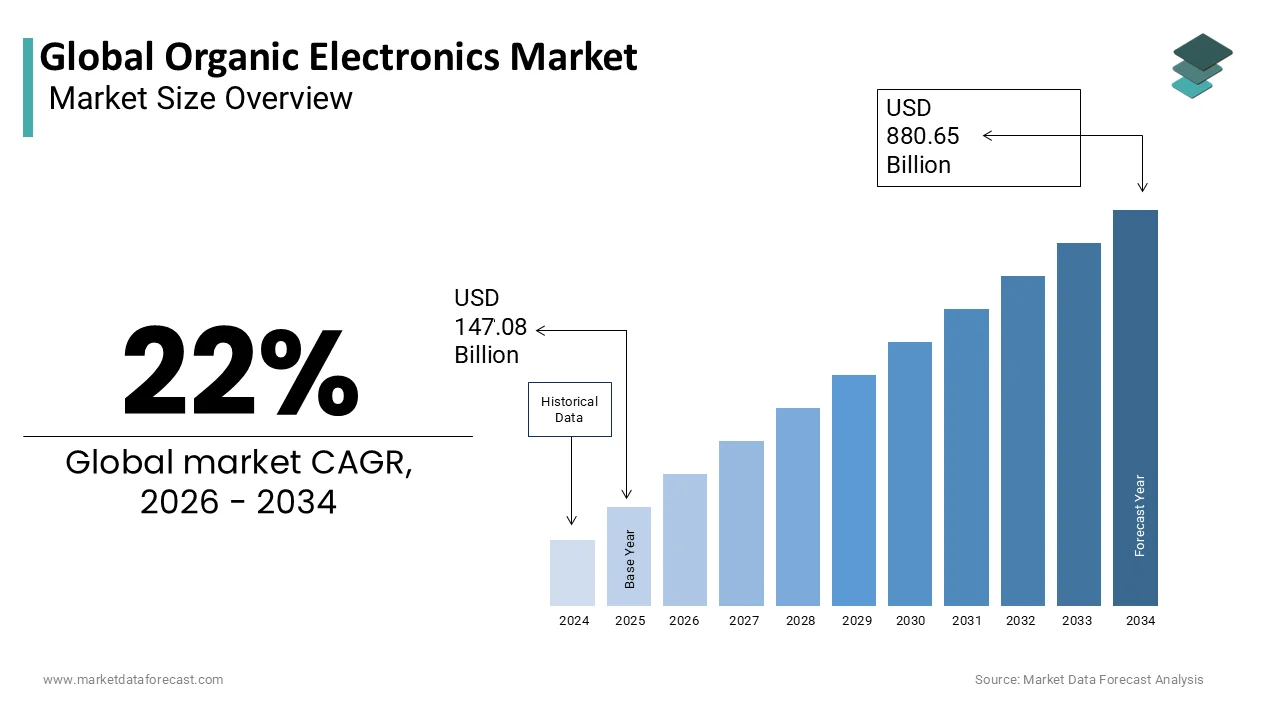

The Global Organic Electronics Market was worth USD 147.08 billion in 2025 and is anticipated to reach a valuation of USD 880.65 billion by 2034 from USD 179.44 billion in 2026. It is predicted to register a CAGR of 22% 2025 to 2033.

Organic electronics refers to the field of science and engineering that utilizes organic molecules and polymers—typically carbon-based compounds—as active components, replacing traditional inorganic semiconductors such as silicon. These materials exhibit unique electrical and optical properties, enabling flexible, lightweight, and cost-effective alternatives across various applications including organic light-emitting diodes (OLEDs), organic photovoltaics (OPVs), organic field-effect transistors (OFETs), and sensors. The technology is increasingly being integrated into consumer electronics, healthcare monitoring systems, smart packaging, and wearable devices due to its compatibility with large-area and low-temperature fabrication processes.

MARKET DRIVERS

Rising Demand for Flexible and Foldable Consumer Electronics

Among the most significant drivers of the organic electronics market is the growing consumer preference for flexible and foldable electronics. With advancements in display technologies, major tech companies are launching smartphones, tablets, and wearables featuring bendable screens made using organic materials. For instance, Samsung and LG have pioneered the commercialization of foldable OLED devices, which rely on organic semiconductors for their flexibility and durability.

The adoption of organic electronics in flexible displays is not limited to smartphones. Applications such as rollable televisions, e-paper, and curved monitors are gaining traction, further boosting market expansion.

Organic materials offer distinct advantages in these applications, including mechanical flexibility, low power consumption, and compatibility with plastic substrates. These characteristics make them ideal for next-generation electronics that prioritize portability and user experience.

Moreover, innovations in printed electronics, enabled by organic semiconductors, are reducing manufacturing costs and facilitating mass production. Companies such as FlexEnable and Plastic Logic are actively developing organic thin-film transistor (OTFT)-based backplanes for flexible displays, contributing to wider industry adoption. This growing momentum underscores the pivotal role of flexible electronics in shaping the future of consumer technology.

Expansion of Internet of Things (IoT) and Smart Wearables

Another critical driver of the organic electronics market is the rapid proliferation of Internet of Things (IoT) devices and smart wearables. These technologies require compact, energy-efficient, and flexible components to function effectively in diverse environments—from healthcare monitoring to industrial automation. Organic electronics, particularly organic photovoltaics (OPVs) and organic sensors, are well-suited for powering and integrating into IoT ecosystems due to their lightweight nature and adaptability to unconventional surfaces.

The IoT saw exponential growth which necessitates scalable and cost-effective electronic solutions, where organic materials offer a compelling alternative to conventional silicon-based electronics. For example, Enfucell, a Finnish company specializing in organic printed batteries, has developed ultra-thin, flexible batteries compatible with RFID tags and smart labels used in logistics and retail IoT applications.

Additionally, the healthcare sector is increasingly adopting organic electronics for wearable sensors that monitor vital signs such as heart rate, blood oxygen levels, and glucose concentration. These sensors are often embedded in skin patches or textiles, leveraging the biocompatibility and conformability of organic materials. Organic electronics play a pivotal role in enabling disposable, stretchable, and non-invasive diagnostic tools, aligning with the broader digital transformation in healthcare.

MARKET RESTRAINTS

High Manufacturing and Material Costs

Despite the promising potential of organic electronics, one of the primary restraints impeding widespread adoption is the relatively high manufacturing and material costs associated with these technologies. Unlike traditional silicon-based electronics, which benefit from decades of mature manufacturing infrastructure and economies of scale, organic electronic components are still produced using complex and expensive fabrication techniques. For instance, vacuum deposition methods used in OLED manufacturing require high-purity organic materials and costly equipment, significantly increasing capital expenditures. This cost differential is primarily attributed to the specialized coating and encapsulation processes required to protect organic layers from environmental degradation.

Moreover, the synthesis of high-performance organic semiconductors—such as conjugated polymers and small molecules—remains a technically challenging and resource-intensive endeavor.

In addition to raw material expenses, the lack of standardized manufacturing protocols across different applications further escalates production costs. While industries such as display manufacturing have established some level of standardization, other segments like organic photovoltaics and printed sensors remain fragmented, hindering cost reductions through volume scaling.

Limited Longevity and Environmental Sensitivity

A major technical limitation affecting the organic electronics market is the relatively short operational lifespan and susceptibility of organic materials to environmental factors such as moisture, oxygen, and ultraviolet radiation. Organic semiconductors, especially those used in OLEDs and OPVs, degrade over time when exposed to ambient conditions, leading to performance deterioration and reduced device reliability. This poses a significant challenge for applications requiring long-term stability, such as outdoor signage, automotive displays, and building-integrated solar panels.

According to a 2025 white paper published by Fraunhofer Institute for Organic Electronics, Electron Beam and Plasma Technology (FEP), the typical operational lifetime of an OLED under continuous usage ranges between 20,000 to 50,000 hours, which is considerably lower than that of LED or LCD counterparts. Similarly, organic photovoltaic cells suffer from efficiency losses over time; as per a study published in Advanced Energy Materials, the efficiency of OPV modules can decline by up to 20% within five years if not adequately protected against environmental exposure.

To mitigate these issues, manufacturers must invest heavily in advanced encapsulation techniques and barrier films, which add to both the cost and complexity of production. Despite improvements in multilayer barrier coatings and getter materials, achieving the same durability as inorganic electronics remains elusive.

MARKET OPPORTUNITIES

Growth in Sustainable and Biodegradable Electronic Devices

One of the emerging opportunities for the organic electronics market lies in the development of sustainable and biodegradable electronic devices. As global awareness of environmental issues intensifies, there is increasing pressure on the electronics industry to reduce electronic waste and adopt eco-friendly materials. Organic electronics, particularly those based on biodegradable polymers and natural derivatives, present a viable solution to this challenge. These materials can be designed to decompose naturally after use, minimizing environmental impact while maintaining functional electronic properties.

According to the United Nations University’s Global E-waste Monitor 2023, global electronic waste generation reached 62 million metric tons in 2022, with only 22% being formally recycled. This growing concern has spurred regulatory initiatives and corporate sustainability goals aimed at promoting greener electronics. In response, academic and industrial research efforts are focusing on creating organic semiconductors derived from cellulose, lignin, and other plant-based materials. For instance, researchers at Stanford University have successfully demonstrated fully biodegradable transistors using natural rubber and organic conductive polymers, opening new pathways for disposable electronics in healthcare, packaging, and agriculture.

Moreover, companies such as Novalia and Armorphous Technologies are developing printable organic circuits on compostable substrates, targeting applications in smart packaging and single-use sensors. Governments in Europe and North America are also incentivizing green electronics through policies such as the European Green Deal and EPA sustainability guidelines, further accelerating the adoption of environmentally friendly electronic components. This shift toward sustainability presents a significant growth avenue for the organic electronics industry.

Integration into Smart Textiles and E-Skin Applications

Another transformative opportunity for the organic electronics market is its integration into smart textiles and electronic skin (e-skin) applications. These technologies involve embedding flexible, lightweight electronic components into fabrics and synthetic skins to enable real-time sensing, communication, and energy harvesting capabilities. Organic electronics, with their inherent flexibility, transparency, and compatibility with soft substrates, are ideally suited for these applications, offering advantages over rigid silicon-based alternatives.

Much of this growth is driven by demand from healthcare, defense, and fitness sectors, where wearable biosensors and adaptive clothing are becoming essential. Organic semiconductors enable the creation of stretchable and conformable sensor arrays that can monitor physiological parameters such as body temperature, muscle activity, and hydration levels.

E-skin, another cutting-edge application, is being developed for robotics, prosthetics, and medical diagnostics. Researchers at the University of Tokyo and Tsinghua University have demonstrated e-skin prototypes using organic field-effect transistors (OFETs) that mimic human touch sensitivity. As the demand for human-centric interfaces and responsive wearable systems grows, organic electronics are poised to play a pivotal role in advancing this frontier.

MARKET CHALLENGES

Technical Limitations in Charge Carrier Mobility and Efficiency

One of the foremost technical challenges facing the organic electronics market is the relatively low charge carrier mobility and efficiency compared to inorganic semiconductors. Charge carrier mobility refers to the ease with which electrons or holes move through a material under an applied electric field. In organic semiconductors, this mobility is typically several orders of magnitude lower than that of silicon or gallium arsenide, limiting the speed and performance of organic-based devices such as transistors and photovoltaics.

According to a 2025 review published in Advanced Electronic Materials , the average charge carrier mobility in state-of-the-art organic semiconductors ranges between 0.1 cm²/V·s and 10 cm²/V·s, whereas crystalline silicon exhibits mobilities exceeding 1,000 cm²/V·s. This disparity restricts the operational frequency of organic field-effect transistors (OFETs) to below 100 MHz, making them unsuitable for high-speed computing or telecommunications applications. Besides, organic photovoltaic (OPV) cells suffer from lower power conversion efficiencies.

Efforts to enhance mobility and efficiency through molecular engineering and nanostructuring have shown promise, but scalability remains a concern. For instance, conjugated polymers such as poly(3-hexylthiophene) (P3HT) and small-molecule semiconductors like pentacene have been extensively studied, yet achieving consistent performance across large-area devices remains challenging.

Lack of Standardization and Industry Collaboration

A significant structural challenge hindering the organic electronics market is the lack of standardization and cohesive industry collaboration across the value chain. Unlike the well-established standards governing silicon-based electronics, the organic electronics sector lacks universally accepted design rules, testing protocols, and manufacturing benchmarks. This fragmentation complicates product development, hampers interoperability, and discourages large-scale investment from system integrators and end-users.

The inconsistency makes it difficult for original equipment manufacturers (OEMs) to assess the suitability of organic components for integration into commercial products. Furthermore, the absence of standardized metrics for lifetime testing, efficiency measurement, and environmental resilience exacerbates market uncertainty.

Collaboration among academia, research institutions, and industry players remains limited, despite the inherently interdisciplinary nature of organic electronics. For example, while universities and public research labs generate novel materials and device architectures, the transition to industrial-scale production is often hindered by proprietary barriers and insufficient knowledge transfer.

Initiatives such as the EU-funded ORGALIME project and Japan’s NEDO programs aim to bridge these gaps by fostering partnerships and establishing pilot production lines. However, until comprehensive standards and collaborative frameworks are widely adopted, the organic electronics industry will continue to face hurdles in achieving mainstream commercial viability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Material, Application, and Region. |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | AGC (Japan), Sumimoto (Japan), BASF (Germany), Bayer Material Science (Germany), Heliatek |

SEGMENTAL ANALYSIS

By Material Insights

The semiconductor materials had the largest share. In 2025, semiconductor-based organic materials accounted for over 38% of the global market. This dominance is primarily driven by their critical role in enabling core functionalities across various applications such as OLED displays, organic photovoltaics (OPVs), and sensors.

The demand for high-performance organic semiconductors is being fueled by advancements in display technology, particularly in flexible and foldable OLEDs. Companies like Samsung Display and LG Display are heavily investing in R&D to enhance the efficiency and stability of organic semiconductor layers, which directly impacts device performance and longevity.

In addition, the rise in demand for energy-efficient lighting solutions is further boosting this segment. These materials offer advantages such as tunable emission wavelengths and compatibility with low-cost printing processes, making them indispensable in next-generation optoelectronics.

Conductive ink is currently the fastest-growing material segment within the organic electronics market, projected to expand at a CAGR of 12.6%. This rapid growth is largely attributed to the increasing adoption of printed electronics across industries such as consumer goods, healthcare, and automotive. Conductive inks, typically composed of silver nanoparticles, carbon nanotubes, or graphene, enable cost-effective and scalable fabrication of flexible circuits, RFID tags, and touch sensors.

Another key driver is the expansion of smart packaging and wearable electronics. Companies such as Henkel AG & Co. KGaA and DuPont de Nemours, Inc. are actively developing novel formulations to improve conductivity and printability, further accelerating industry adoption. The convergence of IoT and additive manufacturing is also enhancing the scalability of conductive ink-based systems, reinforcing its position as the fastest-growing segment in the organic electronics landscape.

By Application Insights

Display remained the dominant application segment in the organic electronics market, accounting for a 42.5% of the total market share in 2025. This overwhelming dominance stems from the widespread use of organic light-emitting diodes (OLEDs) in smartphones, televisions, tablets, and wearable devices.

The surge in demand for high-resolution, energy-efficient, and flexible displays has been the primary growth catalyst. Notably, OLEDs now represent a significant share of smartphone display shipments worldwide, replacing traditional LCDs due to their superior contrast ratios and thinner form factors.

Moreover, the introduction of foldable and rollable display technologies has further propelled the segment. Besides, automotive OEMs are increasingly adopting OLED instrument clusters and infotainment screens, with BMW, Mercedes-Benz, and Tesla incorporating these displays into new vehicle models.

Organic photovoltaics (OPV) is emerging as the fastest-growing application segment in the organic electronics market, exhibiting a CAGR of 14.2%, driven by its lightweight, flexibility, and compatibility with transparent substrates.

One of the key drivers behind this rapid growth is the increasing deployment of OPV in portable and off-grid power generation systems. Unlike conventional silicon solar cells, organic photovoltaics can be printed on flexible plastic films, making them suitable for integration into backpacks, tents, and even clothing. Heliatek, a German OPV manufacturer, has developed ultra-thin solar foils with efficiencies, which are being used in architectural applications such as window tinting and façade integration.

Besides, the rise of sustainable building initiatives and green energy policies is fueling interest in OPV. Governments in Japan and the European Union have introduced subsidies for organic solar installations in urban infrastructure projects. Moreover, research institutions like Fraunhofer ISE continue to push the boundaries of OPV efficiency, with laboratory prototypes achieving notable level. As efficiency improves and costs decline, OPV is poised to become a mainstream solution in niche but rapidly expanding energy markets.

REGIONAL ANALYSIS

South Korea had a commanding position in the Asia-Pacific organic electronics market, contributing 18.5% of the regional market share in 2025. As a technological powerhouse, the country is home to major players such as Samsung Display and LG Display, which dominate global OLED production.

Government support has played a crucial role in fostering innovation and investment. The Ministry of Trade, Industry and Energy (MOTIE) has allocated over KRW 1 trillion ($750 million) since 2020 toward next-generation display and sensor technologies. Additionally, South Korea leads in foldable display adoption, with domestic brands launching multiple flagship devices annually.

The nation is also advancing organic photovoltaics (OPV) for smart city and mobility applications. Institutions like the Korea Institute of Science and Technology (KIST) are collaborating with startups to develop transparent OPV modules for windows and electric vehicles.

China ranks second in the Asia-Pacific organic electronics market, capturing around 22% of the regional market share in 2025. The country’s dominance is underpinned by its extensive manufacturing capabilities and government-led initiatives to boost domestic semiconductor and display industries.

Beijing’s "Made in China 2025" strategy has prioritized advanced electronics, including organic semiconductors, as a strategic sector. The Chinese government also offers tax incentives and land subsidies to attract foreign and domestic firms, reinforcing its position as a global production hub.

Beyond displays, China is expanding into organic sensors and printed electronics. For example, Tsinghua University and the Suzhou Industrial Park have established dedicated research centers focused on organic field-effect transistors (OFETs) for biomedical applications.

Japan is maintaining a strong foothold through decades of expertise in material science and precision engineering. Japanese firms such as Sumitomo Chemical, Canon Tokki, and Mitsubishi Chemical play pivotal roles in supplying high-purity organic semiconductors and deposition equipment essential for OLED manufacturing.

The country has also been at the forefront of organic photovoltaics (OPV) research. Companies like Ricoh and Panasonic have commercialized semi-transparent OPV modules for integration into office buildings and transportation hubs.

Additionally, Japan is pioneering organic electronics in robotics and e-skin applications. Researchers at the University of Tokyo have demonstrated flexible tactile sensors using organic transistors capable of detecting pressure changes as low as 1 kPa.

The United States is maintaining a leadership position through innovation-driven R&D and strong venture capital backing. Silicon Valley and Boston remain epicenters for startups and academic research in organic semiconductors, flexible sensors, and printed electronics.

Major tech firms such as Apple, Google, and Meta are investing in next-generation displays for AR/VR headsets, smartwatches, and foldable phones, driving demand for organic materials. Furthermore, the Department of Energy has funded several OPV projects aimed at lightweight solar solutions for military and aerospace applications.

In addition, U.S. universities like Stanford and MIT are leading breakthroughs in biodegradable and stretchable electronics. Startups such as Glowee and Armorphous Technologies are commercializing organic-based smart labels and biosensors for retail and health monitoring.

Germany is leveraging its strong industrial base and commitment to sustainability. As a leader in mechanical engineering and chemical manufacturing, the country hosts key players such as BASF, Merck KGaA, and Siemens, which are actively involved in developing organic semiconductors, encapsulation materials, and smart sensors.

The German government supports the sector through programs like the “High-Tech Strategy” and the Fraunhofer Society, which conducts applied research in organic electronics.

Germany is also a pioneer in organic photovoltaics for architectural integration. Companies like Heliatek and NextGen Nano are deploying OPV modules in façades and windows to generate clean electricity while maintaining aesthetic appeal. Besides, the automotive sector, led by BMW and Volkswagen, is exploring organic electronics for interior lighting and dashboard displays. As the EU enforces stricter emissions regulations, Germany’s role in shaping the future of sustainable electronics will continue to grow.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Some of the notable companies leading the global organic electronics market profiled in the report are AGC (Japan),Sumimoto (Japan),BASF (Germany),Bayer Material Science (Germany),Heliatek (Germany),Covestro (Germany),DuPont (US),LG Display (South Korea),Samsung (South Korea),Philips (Netherlands)

The organic electronics market is characterized by intense competition driven by rapid technological advancements and the presence of both established corporations and emerging startups. Major players leverage deep R&D capabilities and extensive supply chain networks to maintain dominance, particularly in core segments like OLED displays and organic semiconductors. However, increasing interest from startups specializing in printed electronics, flexible sensors, and sustainable materials is reshaping the competitive landscape. These newer entrants often bring disruptive innovations that challenge traditional manufacturing paradigms. Additionally, regional disparities in regulatory frameworks, raw material availability, and government funding further influence market dynamics. As demand grows across diverse applications—from smart textiles to building-integrated photovoltaics—companies are under pressure to differentiate through proprietary technologies, strategic alliances, and vertical integration. This evolving environment fosters continuous innovation but also intensifies the race for market share, compelling firms to refine their offerings and expand into untapped application areas.

Top Players in the market

One of the leading players in the organic electronics market is Samsung SDI , a South Korean conglomerate that plays a pivotal role in OLED panel manufacturing. The company has been instrumental in advancing flexible and foldable display technologies, supplying high-quality organic electronic components to flagship smartphones and wearable devices. Samsung SDI’s continuous investment in R&D and large-scale production facilities has enabled it to maintain a strong foothold in the global market while setting benchmarks for performance and innovation.

Another key player is LG Display , a subsidiary of LG Corporation, known for its leadership in OLED television panels and transparent organic display solutions. The company has pioneered applications beyond consumer electronics, including automotive displays and signage. LG Display's commitment to developing energy-efficient and lightweight organic electronics has contributed significantly to expanding the technology’s adoption across multiple industries.

Universal Display Corporation (UDC) is a major innovator in phosphorescent OLED materials and technologies. Unlike traditional manufacturers, UDC focuses on material development and licensing, supplying essential intellectual property and high-performance organic compounds to leading display makers worldwide. Its proprietary technologies have enhanced device efficiency and lifespan, making it a foundational contributor to the growth of the organic electronics ecosystem.

Top strategies used by the key market participants

A primary strategy adopted by leading companies in the organic electronics market is intensive investment in research and development . Firms are continuously exploring new materials, fabrication techniques, and device architectures to enhance performance, durability, and cost-efficiency. This focus on innovation allows them to stay ahead in a rapidly evolving technological landscape.

Another crucial approach is strategic partnerships and collaborations with academic institutions, startups, and industry peers. These alliances help accelerate the commercialization of advanced organic electronic solutions and foster cross-sector integration across healthcare, automotive, and smart infrastructure domains.

Lastly, many key players emphasize expansion into emerging applications and verticals such as wearable electronics, IoT-enabled sensors, and biodegradable devices. By diversifying their product portfolios and targeting niche markets, companies can unlock new revenue streams and drive broader adoption of organic electronics.

RECENT HAPPENINGS IN THE MARKET

In February 2025, Samsung Display announced a collaboration with a leading Japanese chemical manufacturer to develop next-generation encapsulation materials for OLED panels. This partnership aims to improve the longevity and environmental resistance of organic electronic components, enhancing overall device reliability.

In June 2025, Universal Display Corporation (UDC) expanded its global footprint by opening a new materials research and development center in Germany. The facility is focused on accelerating the discovery of novel phosphorescent and thermally activated delayed fluorescence (TADF) materials to support high-efficiency OLEDs.

In September 2025, LG Display unveiled plans to integrate organic electronics into vehicle cockpits by partnering with a European automotive OEM. This initiative is intended to advance the use of transparent and curved OLED displays in next-generation electric vehicles.

In November 2025, BASF entered into a joint development agreement with a South Korean startup specializing in organic photovoltaics. The collaboration seeks to create scalable, high-performance OPV modules tailored for indoor energy harvesting and portable power generation.

In March 2025, Sumitomo Chemical launched a dedicated division for organic semiconductor materials, focusing on customized formulations for flexible electronics and sensor applications. This strategic move strengthens its position as a critical supplier in the organic electronics value chain.

MARKET SEGMENTATION

This research report on the global organic electronics market has been segmented and sub-segmented based on the diagnostic type, surgery type, and region.

By Material

- Semiconductor Materials

- Conductive Ink Materials

By Application

- Display Applications

- Organic Photovoltaics (OPV)

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

What are the key applications of organic electronics?

Major applications include OLED displays and lighting, organic solar cells (OPVs), organic field-effect transistors (OFETs), and sensors.

What are the advantages of organic electronics over traditional electronics?

They offer benefits such as flexibility, lightweight, low manufacturing costs, mechanical robustness, and potential for large-area fabrication.

What materials are commonly used in organic electronics?

Materials include conductive polymers like PEDOT:PSS, small molecules such as pentacene, and carbon-based semiconductors.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com