Global Paper Bags Market Size, Share, Trends and Growth Forecasts Report, Segmented By Product, Price Point, End-User, Distribution Channel, And Region (North America, Europe, Asia-Pacific, Latin America, Middle East And Africa), Industry Analysis (2026 to 2034)

Global Paper Bags Market Summary

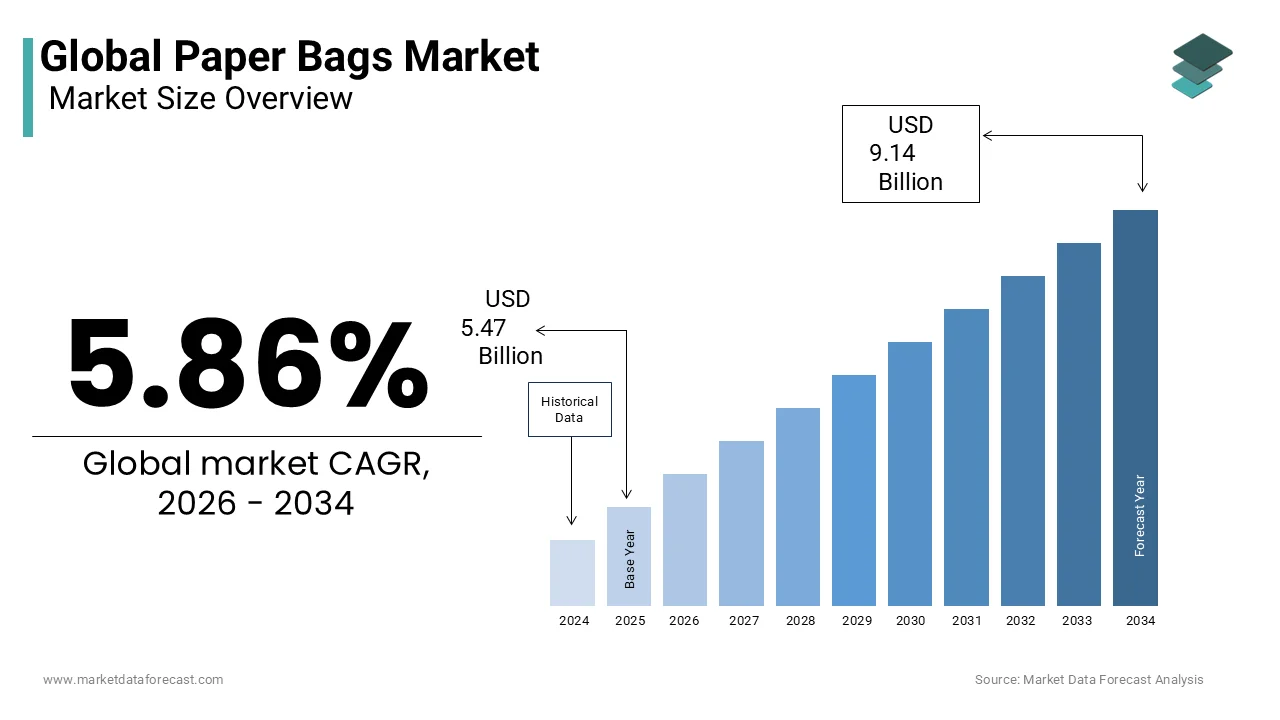

The global paper bags market, valued at USD 5.47 billion in 2025, is projected to reach USD 9.14 billion by 2034, expanding at a CAGR of 5.86% driven by plastic bans, sustainable retail packaging, and e-commerce growth.

Market Snapshot

- 2025 Market Size: USD 5.47 billion

- 2026 Estimate: USD 5.79 billion

- 2034 Forecast: USD 9.14 billion

- CAGR (2026–2034): 5.86%

- Base Year: 2025

- Forecast Period: 2026–2034

Quick Growth Drivers

- Global regulatory bans on single-use plastics

- Rising consumer preference for eco-friendly packaging

- E-commerce expansion and paper-based delivery solutions

- Retail branding through sustainable packaging

- Growth in recycled and alternative fiber technologies

Principal Restraints

- Higher production cost versus plastic bags

- Energy- and water-intensive kraft paper manufacturing

- Limited durability in wet or heavy-load conditions

- Carbon footprint concerns in lifecycle assessments

High-Value Opportunities

- E-commerce paper mailers and reinforced delivery bags

- Water-resistant plant-based coatings

- Bamboo, hemp, and agro-residue fiber integration

- Premium branded packaging for luxury retail

- Closed-loop recycled paper bag production systems

Key Market Challenges

- Volatility in pulp and kraft linerboard pricing

- Competition from reusable cotton totes and bioplastics

- Supply chain disruptions in wood pulp

- Margin pressure in price-sensitive markets

Leading Players

Some of the companies that are playing a dominating role in the global paper bags market include:

- International Paper

- Smurfit Kappa Group

- Mondi plc

- Nippon Paper Industries Co., Ltd.

- Novolex

- Billerud

Global Paper Bags Market Size

The global paper bags market size was valued at USD 5.47 billion in 2025 and is anticipated to reach USD 5.79 billion in 2026 and USD 9.14 billion by 2034, growing at a CAGR of 5.86% during the forecast period from 2026 to 2034.

The paper bags are serving as an alternative to single-use plastic. These bags are increasingly adopted across retail, food service, and e-commerce sectors due to their biodegradability and alignment with sustainability mandates. As per the United Nations Environment Programme, over 130 countries have implemented regulatory measures restricting non-biodegradable plastic bags, accelerating the shift toward paper-based alternatives.

MARKET DRIVERS

Global Regulatory Crackdown on Single-Use Plastics

The stringent government policies targeting single-use plastic are a major factor propelling the growth of the paper bags market. According to the United Nations Conference on Trade and Development, as of 2023, 156 countries have adopted some form of plastic regulation, including full bans, taxes, or phase-out timelines. Canada classified single-use plastic bags as toxic substances under the Canadian Environmental Protection Act in 2022, mandating a complete phase-out by the end of 2023. As per the European Environment Agency, EU-wide restrictions have reduced plastic bag consumption by 60% since 2010, with paper bags filling a significant portion of the void.

Rising Consumer Demand for Sustainable Packaging

Environmental awareness among consumers is expected to fuel the growth of the paper bags market. Consumers consider sustainability an important factor when choosing products, with 62% willing to pay a premium for eco-friendly packaging across the world. In the U.S., the Sustainable Packaging Coalition found that 65% of shoppers are more likely to patronize retailers that use recyclable or compostable bags. E-commerce platforms such as Amazon and Flipkart have also transitioned to paper-based packaging for deliveries in response to consumer pressure. The preference for paper bags is evolving from a compliance-driven necessity to a strategic branding and customer retention tool.

MARKET RESTRAINTS

Higher Production Cost Compared to Plastic Alternatives

The elevated cost of production relative to plastic counterparts is restraining the growth of the paper bags market. This cost differential stems from raw material sourcing, energy-intensive pulping processes, and transportation.Weighty paper bags are heavier, increasing logistics expenses. According to the Food and Agriculture Organization, Kraft paper production consumes approximately 4,000 liters of water and 2,500 kWh of energy per metric ton, making it resource-intensive. As per a 2022 study by the Swedish Environmental Research Institute, the carbon footprint of a paper bag can be up to three times higher than that of a conventional plastic bag when factoring in production and transport.

Limited Durability and Functional Performance

Paper bags exhibit inferior performance under moisture, weight, and repeated use conditions, which restricts their applicability in certain retail and industrial environments. According to the Technical Association of the Pulp and Paper Industry, standard paper bags lose up to 60% of their tensile strength when exposed to humidity or light rain, making them unsuitable for wet climates or outdoor use. A 2023 test conducted by the UK’s Waste and Resources Action Programme (WRAP) found that paper bags typically withstand only 2–3 reuse cycles before structural failure, compared to 7–10 for reusable polypropylene or cotton bags. These limitations increase the need for double-bagging or supplementary packaging, undermining waste reduction goals.

MARKET OPPORTUNITIES

Expansion of E-Commerce and Sustainable Delivery Packaging

The exponential growth of online shopping is creating a fertile ground for innovation in paper-based packaging solutions. According to the U.S. Census Bureau, e-commerce sales in the United States reached $1.03 trillion in 2023, accounting for 15.6% of total retail sales, up from 11.8% in 2019. This surge has amplified demand for durable, recyclable, and brand-enhancing packaging. Companies like Amazon, Alibaba, and Zalando are increasingly replacing plastic mailers with paper-based padded envelopes and box fillers. As per the International Post Corporation, 68% of global postal operators reported a shift toward paper-based shipping materials in 2023 to meet sustainability targets. Innovations such as water-resistant coatings derived from plant-based waxes and reinforced paper handles are enhancing functionality.

Advancements in Recycled and Alternative Fiber Sourcing

Technological progress in fiber sourcing and recycling is unlocking new opportunities for sustainable paper bag production. According to the American Forest & Paper Association, 68% of paper consumed in the U.S. was recovered for recycling in 2023, the highest rate among all packaging materials. This robust recycling infrastructure supports the production of high-quality recycled paper bags without compromising strength. Furthermore, companies are exploring non-wood fibers such as bamboo, hemp, and agricultural residues byproducts of rice and wheat farming to reduce reliance on virgin wood pulp.

MARKET CHALLENGES

Supply Chain Vulnerability to Raw Material Fluctuations

Highly susceptible to volatility in pulp and paper supply, which is driven by geopolitical, climatic, and logistical disruptions, is hindering the growth of the aper bags market. According to the Food and Agriculture Organization’s Global Forest Resources Assessment 2025, global wood pulp production declined by 4.2% in 2022 due to reduced output in major producing regions such as Finland, Canada, and Brazil. In 2023, benchmark Kraft linerboard prices surged by 22% year-on-year, as reported by RISI, a leading pulp and paper market intelligence firm, due to constrained supply and high energy costs. These fluctuations directly impact manufacturing margins and retail pricing, discouraging long-term contracts.

Competition from Reusable and Alternative Biodegradable Materials

The intensifying competition from reusable textiles and emerging bioplastics, which offer superior durability and lower environmental impact over multiple uses, is also hampering the growth of the aper bags market. According to a lifecycle assessment by the Danish Environmental Protection Agency, a cotton tote must be reused at least 7,000 times to match the environmental footprint of a single-use plastic bag when considering water, energy, and emissions. According to the European Bioplastics Association, global production capacity for biodegradable plastics is expected to grow by 40% by 2027, with materials like polylactic acid (PLA) and PHA gaining traction in flexible packaging.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Price, End-User, Distribution Channel, and Region |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Ronpak, Inc., International Paper Company, Smurfit Kappa Group, Global-Pak, Inc., Novolex, Welton Bibby And Baron Limited, United Bag, Inc., Mondi Plc., York Paper Company Ltd., Paperbags Ltd |

SEGMENTAL ANALYSIS

By Product Insights

pasted-open-mouth paper bag segment dominated the global paper bags market by capturing 38.2% of the market share in 2025, with its widespread use in the food and retail sectors. These bags are typically made from multi-ply kraft paper with adhesive-sealed bottoms, offering superior moisture resistance when lined with polyethylene or biodegradable coatings. As per the U.S. Department of Agriculture, 72% of commercial bakeries and milling operations in North America rely on this format for bulk packaging, citing consistent load-bearing capacity and printability for branding.

The flat-bottom paper bag segment is projected to grow at a CAGR of 14.3% during the forecast period, with the rising demand in e-commerce, luxury retail, and sustainable branding, where aesthetic appeal and structural integrity are paramount. According to McKinsey & Company, 62% of premium fashion and lifestyle brands have transitioned tto oflat-bottomm paper bags for in-store and delivery packaging to enhance unboxing experiences. These bags are often customized with embossing, foil stamping, and eco-friendly inks, aligning with brand sustainability narratives. Additionally, the growth of direct-to-consumer (DTC) models has amplified demand for durable, shippable paper bags. Innovations such as water-resistant coatings derived from cornstarch and reinforced laminates have extended the functional lifespan of these bags, enabling reuse.

By Price Point Insights

The economy segment accounted in holding 52.3% of the paper bags market share in 2025, with its adoption across price-sensitive industries and developing economies where cost efficiency is a primary purchasing criterion. Economy paper bags are typically uncoated, use lower grammage paper, and lack elaborate printing or reinforced handles, making them ideal for bulk industrial packaging and basic retail use. In urban retail markets, supermarkets and wet markets in countries like Indonesia, Nigeria, and Bangladesh continue to distribute economy paper bags as a low-cost alternative to plastic. Additionally, municipal waste management programs in cities such as Manila and Lagos have subsidized the distribution of economy paper bags to support plastic phase-out initiatives.

The premium price segment is projected to register a CAGR of 13.8% throughout the forecast period with the integration of brand differentiation, sustainability storytelling, and experiential retail. Premium paper bags are characterized by high grammage paper, custom designs, reinforced handles, and eco-certifications such as FSC or PEFC, catering to luxury fashion, cosmetics, and high-end grocery retailers. According to a 2023 report by Bain & Company, 74% of luxury consumers consider packaging an integral part of brand identity, with 58% more likely to repurchase from brands that use sustainable, aesthetically refined packaging. Companies like Gucci, Sephora, and Whole Foods have adopted premium paper bags featuring embossed logos, matte finishes, and plant-based inks to reinforce brand prestige. Moreover, social media influence has amplified the role of packaging in consumer engagement.

By End User Insights

The food and beverage sector segment accounted in holding 35.4% of the global paper bags market share in 2025. According to the U.S. Food and Drug Administration, over 80% of commercial bakeries use paper bags for packaging bread, muffins, and pastries due to their breathability, grease resistance (when coated), and compostability. Additionally, regulatory mandates are accelerating adoption. In India, the Food Safety and Standards Authority mandates that unpackaged snacks and street food be served in biodegradable containers, including paper bags. Innovations such as water-based barrier coatings and antimicrobial treatments are enhancing shelf life and safety, which is making paper viable for moist or oily foods.

The retail sector segment is expected to grow with a CAGR of 13.1% during the forecast period, with the transformation of paper bags from utilitarian carriers to strategic branding tools in apparel, electronics, and lifestyle retail. The shift is particularly pronounced in omnichannel retail, where in-store purchases and e-commerce deliveries converge. Moreover, plastic restrictions in retail environments are tightening globally. The rise of pop-up stores, seasonal boutiques, and luxury gift packaging is further increasing demand for customizable, high-quality paper bags.

REGIONAL ANALYSIS

Europe Paper Bags Market Analysis

Europe was the top performer of the paper bags market by accounting for 36.3% of the market share in 2025. The European Union has been at the forefront of plastic reduction policies, with the European Environment Agency reporting that 27 member states have implemented full or partial bans on single-use plastic bags since 2015. Countries like France and Italy have gone further by mandating that all non-reusable bags be compostable or recyclable, favoring paper-based solutions. The presence of major paper producers such as Billerud (Sweden) and Mondi (Austria) ensures a stable supply of sustainable materials.

North America Paper Bags Market Analysis

North America's paper bags market growth is likely to witness a prominent CAGR in the coming years. As per the United States Environmental Protection Agency, over 120 billion plastic bags are used annually in the U.S., prompting cities like New York, San Francisco, and Seattle to enforce strict bans or fees. In response, retailers including Target, Walmart, and Kroger have transitioned to paper bags as a primary alternative.

Asia Pacific Paper Bags Market Analysis

Asia Pacific paper bags market is growing due to rapid urbanization and policy-driven plastic phase-outs. Japan’s Packaging Recycling Law mandates that retailers reduce plastic use, encouraging paper alternatives. However, affordability remains a challenge while urban centers adopt premium paper bags, rural areas rely on lower-cost options.

Latin America Paper Bags Market Analysis

Latin America paper bags market growth is likely to grow, with Brazil and Mexico emerging as key adopters due to rising environmental awareness and regulatory developments. However, limited domestic paper production and reliance on imported kraft pulp constrain scalability. The Middle East & Africa paper bags market is anticipated to grow in the coming years. As per the Dubai Municipality, paper bag usage in retail outlets increased by 55% in 2023. Saudi Arabia’s Vision 2030 includes waste reduction targets, which are driving public and private sector adoption of eco-friendly packaging.

COMPETITIVE LANDSCAPE

The paper bags market is characterized by intensifying competition as environmental regulations and consumer preferences reshape packaging ecosystems. Global manufacturers compete with regional converters on innovation, cost, and sustainability credentials. While large players leverage scale and R&D to offer advanced, certified paper solutions, local firms respond with lower-cost, customized options tailored to domestic regulations. The shift from plastic has attracted new entrants, including biotech startups developing plant-based coatings and digital packaging designers. Consolidation is emerging, with larger firms acquiring niche converters to expand service offerings.

KEY MARKET PLAYERS

A few of the market players in the global paper bags market include

- Ronpak, Inc.

- Nippon Paper Industries Co., Ltd.

- International Paper Company

- Smurfit Kappa Group

- Global-Pak, Inc

- Novolex

- BillerudKorsnäs (now part of Holmen AB)

- Welton Bibby

- Baron Limited

- United Bag, Inc.

- Mondi Plc.

- York Paper Company Ltd

- Paperbags Ltd.

Top Players in the Market

- Mondi, a global leader in sustainable packaging, plays a pivotal role in the Asia Pacific paper bags market through its integrated production facilities and customer-centric innovation. The company operates key manufacturing plants in China, India, and Vietnam, enabling the localized supply of kraft paper and fabricated bags for industrial and retail clients. Mondi has strengthened its regional presence by launching EcoSolutions, a consultative service that helps brands transition from plastic to recyclable paper-based packaging. In 2023, it introduced a water-resistant, fully recyclable paper bag for the foodservice sector in collaboration with major quick-service restaurant chains in Singapore and Australia. The company also achieved FSC and ISO 14001 certifications across its Asia operations, reinforcing environmental compliance.

- BillerudKorsnäs, now integrated into Holmen’s packaging division, has expanded its influence in the Asia Pacific region by focusing on high-performance paper solutions for demanding applications. While historically rooted in Europe, the company has intensified its engagement in Asia through strategic partnerships and technical collaborations with converters in Japan, South Korea, and Thailand.

- Nippon Paper Industries is a dominant force in the Asia Pacific paper bags market, leveraging its deep regional footprint and vertical integration from pulp to finished products. Headquartered in Japan, the company supplies a wide range of paper bags to retail, foodservice, and industrial sectors across Japan, China, and Southeast Asia. It has developed specialized grease-resistant and moisture-barrier papers for takeaway packaging, widely adopted by convenience store chains like 7-Eleven and FamilyMart. In 2023, Nippon Paper launched a fully compostable paper bag line using bamboo fiber at its facility in Malaysia, reducing reliance on virgin wood pulp. The company also invested in a new recycling plant in Yokohama to close the loop on post-consumer paper waste.

Top Strategies Used By The Key Market Participants

Key players in the paper bags market are deploying integrated strategies to capture growth amid rising sustainability demands. Companies are investing in R&D to develop high-performance, recyclable, and biodegradable paper grades with enhanced durability and moisture resistance. Firms are expanding manufacturing capacities in Asia and Eastern Europe to serve emerging markets and reduce logistics emissions. Strategic collaborations with retailers and e-commerce platforms help co-design branded, functional packaging. Digital printing adoption allows for customization and small-batch orders.

MARKET SEGMENTATION

This research report on the global paper bags market is segmented and sub-segmented into the following categories.

By Product Type

- Sewn Open Mouth

- Pinched Bottom Open Mouth

- Pasted Valve

- Pasted Open Mouth

- Flat Bottom

By Price Point

- Economy

- Premium

- Medium

By End-User

- Agriculture and Allied Industries

- Building and Cons

- Food and Beverage

- Retail

- Chemicals

- Pharmaceutical

- Merchandise

- Others

By Distribution Channel

- B2B

- B2C

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle-East & Africa

Frequently Asked Questions

What’s driving the growth of the global paper bags market?

Surging bans on single-use plastics and rising consumer preference for eco-friendly packaging—especially in retail, grocery, and foodservice—are accelerating demand. Businesses are adopting paper bags to align with sustainability mandates and enhance brand image.

Which regions lead in paper bag consumption and production?

Europe dominates due to strict environmental regulations and high recycling rates, while Asia-Pacific is the fastest-growing market, fueled by urbanization, e-commerce expansion, and government initiatives against plastic waste.

How are innovations shaping paper bag design and functionality?

Manufacturers are enhancing strength with biodegradable coatings, introducing water-resistant finishes, and integrating smart features like QR codes—balancing sustainability with practicality for modern retail needs.

What are the major challenges in the paper bags industry?

Higher production costs compared to plastic, moisture sensitivity, and supply chain volatility in pulp prices remain key hurdles—though economies of scale and recycling infrastructure are gradually easing these constraints.

Who are the top players in the global paper bags market?

Leading companies include Smurfit Kappa, DS Smith, Mondi, WestRock, and BillerudKorsnäs—renowned for their integrated fiber sourcing, R&D in sustainable packaging, and global supply capabilities serving major retailers and brands.

How do government regulations impact the paper bags market?

Plastic bag bans and extended producer responsibility (EPR) laws in over 100 countries are directly boosting paper bag adoption. Regulatory support for recyclable and compostable packaging creates a favorable policy environment for industry growth.

Are paper bags truly more sustainable than plastic alternatives?

While paper bags have a higher initial carbon and water footprint, they are fully biodegradable, widely recyclable, and made from renewable resources—making them more sustainable over their full lifecycle when sourced responsibly.

What role does e-commerce play in paper bag demand?

E-commerce drives demand for branded, durable, and eco-conscious shipping and delivery bags, especially in the fashion and grocery sectors. Retailers use custom paper bags to enhance unboxing experiences while meeting green logistics goals.

How is the cost of raw materials affecting the market?

Fluctuations in wood pulp and recycled fiber prices—driven by supply constraints and energy costs—impact production expenses. However, long-term contracts and vertical integration by major players help stabilize pricing for end users.

What emerging trends should stakeholders watch?

Trends include the rise of reusable paper-composite bags, digital printing for hyper-personalization, and certifications like FSC or PEFC gaining weight in B2B procurement—reflecting deeper integration of circular economy principles across the value chain.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com