Global Passenger Car Market Size, Share, Trends & Growth Forecast Report Segmented By Vehicle Type (Hatchbacks, Sedans and SUVs & Crossovers), Propulsion, Vehicle Class, Size, Drivetrain, and Region (North America, Europe, Asia Pacific, Latin America, Middle East, and Africa), Industry Analysis from 2026 to 2034

Global Passenger Car Market Report Summary

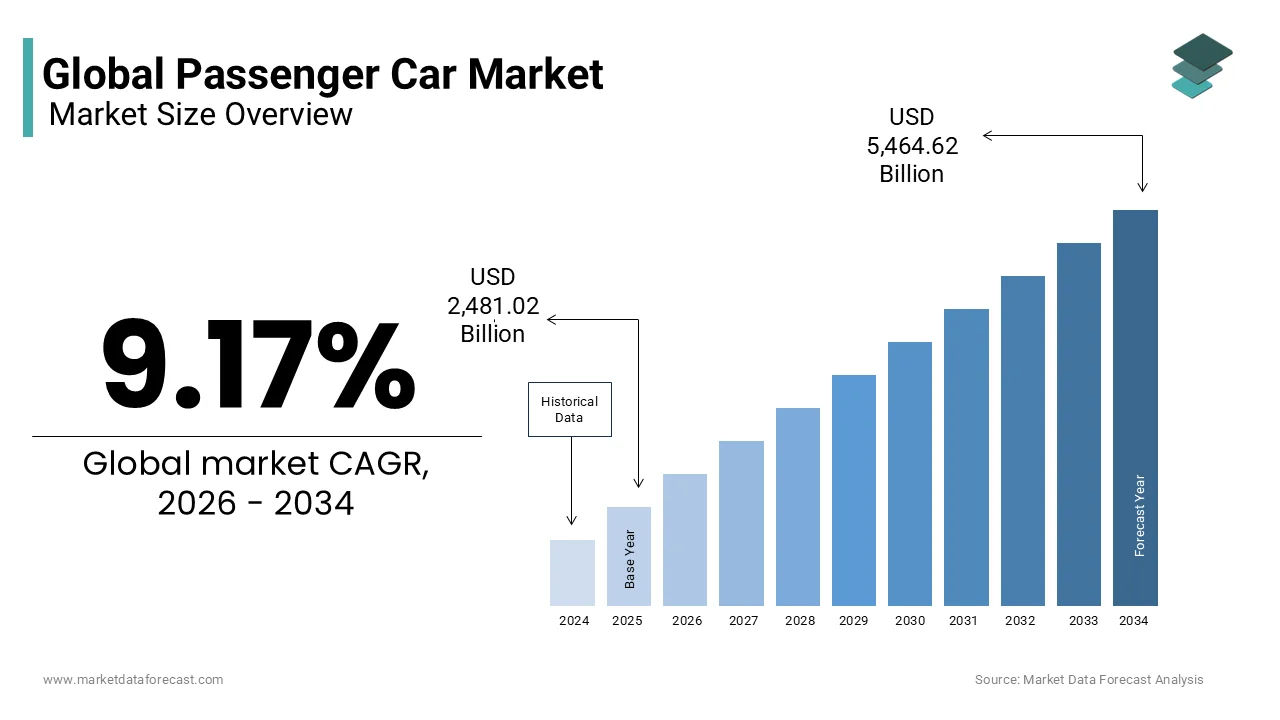

The global passenger car market was valued at USD 2,481.02 billion in 2025, is estimated to reach USD 2,708.53 billion in 2026, and is projected to reach USD 5,464.62 billion by 2034, growing at a CAGR of 9.17% during the forecast period from 2026 to 2034. The growth of the global passenger car market is driven by rising disposable incomes, increasing urbanization, and growing consumer demand for personal mobility. Advancements in automotive technologies, expanding electric and connected vehicle ecosystems, and continuous improvements in safety, comfort, and fuel efficiency are further supporting market growth. Additionally, supportive government policies, increasing vehicle financing options, and rising investments in smart mobility solutions are accelerating the expansion of the passenger car market worldwide.

Key Market Trends

-

Rising demand for SUVs and crossover vehicles is reshaping consumer preferences across global automotive markets.

-

Increasing adoption of connected, autonomous, and advanced driver assistance systems (ADAS) is enhancing vehicle safety and driving experience.

-

Growing investments in electric and hybrid passenger vehicles are supporting the transition toward sustainable mobility.

-

Continuous advancements in infotainment, digital cockpit technologies, and in-car connectivity are improving customer experience.

-

Expanding automotive production capacity and favorable financing options are driving passenger car sales in emerging economies.

Segmental Insights

-

Based on vehicle type, the SUVs and Crossovers segment dominated the global passenger car market in 2025. The segment's leadership is attributed to increasing consumer preference for spacious interiors, enhanced safety features, higher ground clearance, and versatile performance across urban and off-road environments.

-

Based on propulsion, the Internal Combustion Engine (ICE) segment held the largest share of the global passenger car market in 2025. The segment's dominance is driven by its extensive fueling infrastructure, widespread availability, established manufacturing ecosystem, and affordability across various vehicle categories.

-

Based on vehicle class, the mid-range segment accounted for the largest share of the global passenger car market in 2025. The segment's growth is supported by its balance of affordability, advanced features, fuel efficiency, and reliability, making it the preferred choice among a broad consumer base.

-

Based on drivetrain, the Front Wheel Drive (FWD) segment dominated the global passenger car market in 2025. The segment's leadership is attributed to its cost-effectiveness, improved fuel efficiency, compact design, and widespread adoption across hatchbacks, sedans, and crossover vehicles.

Regional Insights

-

The global passenger car market is witnessing strong growth due to rising vehicle ownership, technological innovation, and increasing consumer demand for safe, efficient, and connected mobility solutions.

-

Asia-Pacific dominated the global passenger car market by accounting for 45.6% of the market share in 2025. The region's leadership is driven by rapid urbanization, rising disposable incomes, expanding automotive manufacturing capacity, and strong demand for passenger vehicles in major economies such as China, India, Japan, and South Korea.

-

Europe remains a significant market due to its strong automotive manufacturing base, increasing adoption of electric vehicles, and stringent vehicle safety and emission regulations.

Competitive Landscape

The global passenger car market is highly competitive, with leading automakers focusing on vehicle electrification, connected mobility, autonomous driving technologies, and product innovation to strengthen their market positions. Companies are investing in research and development, strategic collaborations, digital manufacturing, and sustainable mobility solutions to meet evolving consumer preferences and regulatory requirements. Key players operating in the global passenger car market include Bayerische Motoren Werke AG, Daimler AG (Mercedes-Benz AG), Ford Motor Company, General Motors Company, Honda Motor Co. Ltd., Hyundai Motor Company, Kia Corporation, Nissan Motor Co. Ltd., Toyota Motor Corporation, and Volkswagen AG.

Global Passenger Car Market Size

The global passenger car market size was valued at USD 2,481.02 billion in 2025, and is expected to be worth USD 5,464.62 billion by 2034 from USD 2,708.53 billion by 2026. The market is growing at a CAGR of 9.17% during the forecast period.

A passenger car is any motor vehicle designed and constructed primarily for the transportation of people rather than goods or cargo. This includes a diverse range of vehicle types such as sedans hatchbacks sport utility vehicles and coupes that cater to individual consumer needs rather than commercial freight or mass transit. The market serves as a critical pillar of the global economy influencing employment rates technological innovation and infrastructure development. According to the International Organization of Motor Vehicle Manufacturers global production of passenger cars exceeded 60 million units in recent years reflecting sustained demand despite economic fluctuations. The transition towards electrification and digital connectivity has fundamentally altered the competitive landscape prompting traditional manufacturers to rethink their product strategies. Also, the World Health Organization (WHO) reports that road traffic injuries result in 1.19 million annual deaths and stand as the leading cause of mortality globally for children and young adults aged 5 to 29 years. Consumer preferences are shifting towards vehicles that offer enhanced comfort connectivity and environmental sustainability. The integration of artificial intelligence and autonomous driving features is transforming the passenger car from a mere mode of transport into a mobile living space. Urbanization trends and changing mobility patterns further influence market dynamics as consumers seek flexible ownership models. This evolving ecosystem requires manufacturers to balance heritage engineering with cutting edge software capabilities to meet the expectations of modern drivers who prioritize experience efficiency and safety in their daily commutes.

MARKET DRIVERS

Rising Disposable Income and Urbanization Driving Personal Mobility Demand

The steady increase in global disposable income coupled with rapid urbanization boosts the expansion of the passenger car market. As economies develop particularly in emerging markets individuals gain greater financial freedom to invest in personal transportation which offers convenience and status. The World Bank indicates that while overall global growth remains slow, emerging economies in Asia, led by rapid middle-class expansion in India and China, continue to drive strong localized demand for personal mobility. Urban sprawl often outpaces the development of efficient public transportation systems creating a necessity for personal cars to bridge the gap between residential areas and employment centers. In many developing nations owning a car is viewed as a significant milestone of social advancement and economic stability. The flexibility provided by personal vehicles allows families to manage complex schedules involving work education and leisure activities more effectively than fixed route public transit. Additionally the rise of dual income households increases the need for multiple vehicles per family to accommodate separate commuting requirements. Government initiatives to improve road infrastructure in rural and semi urban areas further facilitate car ownership by enhancing accessibility. The psychological appeal of privacy and comfort within a personal vehicle also drives demand among consumers who value control over their travel environment. This combination of economic capability and lifestyle necessity ensures robust demand for passenger cars across diverse geographic regions.

Stringent Government Regulations Promoting Safety and Efficiency Standards

Strict government regulations regarding vehicle safety emissions and fuel efficiency significantly drive innovation and replacement cycles in the passenger car market. Regulatory bodies worldwide mandate the inclusion of advanced safety features such as automatic emergency braking lane keeping assist and blind spot monitoring to reduce accident rates. According to the National Highway Traffic Safety Administration vehicles equipped with these advanced driver assistance systems have demonstrated a substantial reduction in rear end collisions and lane departure incidents. These mandates compel manufacturers to integrate sophisticated software and sensor technologies into even entry level models thereby increasing the overall value and appeal of new vehicles. Stringent regulatory frameworks, such as the upcoming Euro 7 standards in Europe and the finalized Tier 4 criteria pollutant rules by the U.S. Environmental Protection Agency (EPA), mandate that global automakers dramatically curb vehicle emissions to avoid compliance penalties. Fuel economy regulations encourage the adoption of lightweight materials and aerodynamic designs which improve performance and reduce operating costs for consumers. Tax incentives and subsidies for low emission vehicles further stimulate demand for hybrid and electric passenger cars. The periodic tightening of these regulations creates a continuous cycle of technological upgrades ensuring that older vehicles become obsolete faster. Consumers are motivated to upgrade to newer models that comply with the latest standards and offer better resale value. This regulatory pressure acts as a powerful engine for market growth by driving both voluntary and mandatory vehicle replacements.

MARKET RESTRAINTS

High Initial Purchase Costs and Financing Constraints Restricting Affordability

The substantial initial purchase cost of these cars, combined with rising interest rates, restricts the growth of the passenger car market. This trend is particularly true for first-time buyers. The average transaction price for new vehicles has increased dramatically due to the integration of expensive technologies such as large touchscreens advanced sensors and complex powertrains. According to Kelley Blue Book the average price of a new car in the United States exceeded 48000 dollars in recent years placing it out of reach for many budget conscious consumers. High inflation rates have eroded purchasing power making it difficult for households to justify large discretionary expenditures on automobiles. Financing constraints further exacerbate this issue as central banks raise interest rates to combat inflation leading to higher monthly loan payments. Many potential buyers face rejection for auto loans or are offered unfavorable terms due to tighter lending standards imposed by financial institutions. The total cost of ownership including insurance maintenance and fuel adds to the financial burden discouraging some consumers from entering the market. In emerging economies currency depreciation against the dollar increases the cost of imported vehicles and components further limiting affordability. Younger demographics increasingly prefer alternative mobility solutions such as ride hailing and car sharing to avoid the long term financial commitment of ownership. These economic barriers suppress demand and slow down the replacement cycle for existing vehicle owners.

Supply Chain Disruptions and Semiconductor Shortages Impacting Production

Persistent supply chain disruptions and shortages of critical components such as semiconductors severely constrain the production capacity of manufacturers within the passenger car market. The automotive industry relies on a complex global network of suppliers for thousands of parts and any bottleneck can halt assembly lines. According to AutoForecast Solutions the global automotive industry lost millions of vehicle productions in recent years due to chip shortages affecting everything from infotainment systems to engine control units. Geopolitical tensions trade wars and natural disasters further exacerbate these vulnerabilities by disrupting the flow of raw materials and finished components. The just in time manufacturing model adopted by most automakers leaves little room for inventory buffers making them highly susceptible to sudden supply shocks. Logistics challenges including port congestion and shipping container shortages increase lead times and transportation costs. The scarcity of rare earth metals needed for electric vehicle batteries and motors also poses a long term risk to production scalability. Manufacturers struggle to predict delivery timelines leading to customer dissatisfaction and order cancellations. The inability to meet demand results in lost revenue and market share for brands that cannot deliver vehicles promptly. While efforts are being made to diversify supply chains and localize production, these structural issues remain a persistent drag on market growth. Consequently, market stability continues to be negatively impacted.

MARKET OPPORTUNITIES

Expansion of Electric Vehicle Infrastructure Creating New Adoption Pathways

The rapid expansion of charging infrastructure is a key growth area for the passenger car market. This development alleviates range anxiety and accelerates the adoption of electric vehicles. Governments and private companies are investing billions in building fast charging networks along highways and in urban centers to support the growing fleet of electric cars. The International Energy Agency (IEA) shows that the global network of public electric vehicle charging infrastructure has cleared several million operational points, widening adoption channels for global consumers. This improved accessibility makes electric passenger cars a viable option for long distance travel and daily commuting without the fear of running out of power. Home charging solutions are also becoming more affordable and easier to install further enhancing convenience for owners. The development of ultra fast charging technologies reduces charging times to minutes rather than hours making the refueling experience comparable to conventional gasoline stations. Utility companies are introducing smart charging programs that allow users to charge during off peak hours at lower rates reducing operational costs. The integration of renewable energy sources with charging stations enhances the environmental appeal of electric vehicles. As infrastructure becomes more ubiquitous consumer confidence in electric technology grows driving demand for new models. This supportive ecosystem enables automakers to phase out internal combustion engines more aggressively and capture a larger share of the sustainable mobility market.

Integration of Advanced Connectivity and Software Defined Features

The integration of advanced connectivity and software defined features offers a significant opportunity for automakers to differentiate their products and create new revenue streams, which is anticipated to accelerate the expansion of the passenger car market. Modern passenger cars are increasingly becoming software defined vehicles where value is derived from digital services rather than just mechanical hardware. According to McKinsey and Company software and electronics will account for up to 50 percent of a car total value by 2030 highlighting the shift in consumer priorities. Features such as over the air updates allow manufacturers to improve vehicle performance add new functionalities and fix bugs remotely extending the lifecycle of the car. Subscription based services for navigation entertainment and autonomous driving capabilities provide recurring revenue opportunities beyond the initial sale. Connectivity enables seamless integration with smart home devices and personal smartphones creating a cohesive digital ecosystem for users. Data collected from connected vehicles can be used to offer personalized insurance rates predictive maintenance alerts and targeted marketing. The ability to customize the user interface and driving experience through software appeals to tech savvy consumers who expect their cars to evolve over time. Partnerships with technology firms enable automakers to leverage expertise in cloud computing and artificial intelligence. This digital transformation opens new avenues for innovation and customer engagement positioning passenger cars as intelligent mobile platforms.

MARKET CHALLENGES

Volatility in Raw Material Prices Affecting Manufacturing Margins

The volatility in prices of critical raw materials such as steel aluminum lithium and copper remains a serious hurdle for the profitability and pricing stability of the passenger car market. These materials are essential for vehicle construction and battery production and their costs are subject to global market fluctuations. According to the World Bank commodity prices for metals experienced sharp increases in recent years due to supply constraints and heightened demand from the energy transition. Rising input costs force manufacturers to either absorb the losses reducing their profit margins or pass the costs onto consumers risking reduced demand. The transition to electric vehicles intensifies this challenge as batteries require significant amounts of lithium cobalt and nickel which are sourced from geopolitically sensitive regions. Trade policies and export restrictions on these materials can further disrupt supply and inflate prices. Manufacturers struggle to hedge against these fluctuations effectively due to the long lead times involved in vehicle production. Price instability makes it difficult to plan long term budgets and set competitive retail prices. Smaller automakers with less bargaining power are particularly vulnerable to these cost pressures. The industry faces the dual challenge of securing sustainable supplies while managing cost efficiency. This uncertainty complicates strategic planning and investment decisions in new technologies and production facilities.

Cybersecurity Threats and Data Privacy Concerns in Connected Vehicles

The increasing connectivity of these cars introduces severe cybersecurity threats and data privacy concerns that challenge consumer trust, regulatory compliance, and the expansion of the passenger car market. Modern vehicles are essentially computers on wheels with numerous entry points for potential cyberattacks including Bluetooth Wi Fi and cellular connections. According to Upstream Security cyberattacks on the automotive sector have increased significantly in recent years targeting vehicle control systems and personal data. A successful breach could allow hackers to take control of critical functions such as steering braking or acceleration posing serious safety risks. The collection of vast amounts of user data including location history driving habits and personal information raises privacy issues under regulations like the General Data Protection Regulation. Automakers must invest heavily in robust encryption firewalls and intrusion detection systems to protect against these threats. However keeping pace with evolving cyber tactics requires continuous updates and vigilance which adds to operational complexity. Consumer awareness of these risks is growing leading to hesitation in adopting fully connected features. Liability issues in the event of a cyber incident remain legally ambiguous creating uncertainty for manufacturers. Ensuring end to end security across the entire vehicle lifecycle is a daunting task that requires collaboration with specialized security firms. Failure to address these challenges can result in reputational damage legal penalties and loss of market share.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 9.17% |

| Segments Covered | By Vehicle Type, Propulsion, Vehicle Class, Size, Drivetrain, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Bayerische Motoren Werke AG, Daimler AG (Mercedes-Benz AG), Ford Motor Company, General Motors Company, Honda Motor Co. Ltd., Hyundai Motor Company, Kia Corporation, Nissan Motor Co. Ltd., Toyota Motor Corporation, and Volkswagen AG |

SEGMENTAL ANALYSIS

By Vehicle Type Insights

The SUVs and Crossovers segment dominated the global passenger car market and held a substantial share in 2025. This dominance of the segment was driven by consumer preference for vehicles that offer higher seating positions, better visibility, and the ability to handle diverse road conditions, including light off-roading. Consumers increasingly favored these vehicles for their versatility, spaciousness, and perceived safety. Families prioritize the increased cargo capacity and flexible seating arrangements which accommodate children sports equipment and grocery shopping with ease. Automakers have responded by expanding their SUV portfolios across all price points from compact crossovers to full size luxury models ensuring broad market penetration. The marketing of SUVs as lifestyle vehicles that support outdoor activities and urban commuting resonates strongly with modern consumers. Additionally the robust design of SUVs appeals to buyers concerned about safety in collisions with smaller vehicles. The availability of all wheel drive options in many SUV models further enhances their appeal in regions with harsh weather conditions. Manufacturers leverage platform sharing strategies to produce SUVs efficiently reducing costs while maintaining high profit margins. This segment benefits from continuous innovation in features such as panoramic sunroofs advanced towing capabilities and rugged styling cues that differentiate them from traditional sedans.

However, the SUV segment continues to grow at a CAGR of 6.1% due to the introduction of electric and hybrid variants that combine efficiency with utility. According to Cox Automotive the average transaction price for SUVs remains higher than sedans encouraging manufacturers to prioritize their production. The development of compact electric SUVs has opened new demographics including young urban professionals who previously preferred hatchbacks. These vehicles offer the tech forward image of electric mobility with the practicality of an SUV body style. Government incentives for electric vehicles often apply to SUVs making them financially attractive despite their larger size. The perception of SUVs as safer and more prestigious drives demand in emerging markets where car ownership is a status symbol. Automakers are discontinuing sedan models in favor of crossover SUVs to streamline production and meet consumer demand. This strategic shift ensures that SUVs capture the majority of future growth in the passenger car sector.

By Propulsion Insights

The Internal Combustion Engine (ICE) segment led the passenger car market and accounted for the majority share in 2025. This leading position was attributed to the extensive network of fueling stations worldwide, which provides convenience and reliability for long-distance travel. Established infrastructure and lower upfront costs gave this segment its majority share. According to the International Energy Agency ICE vehicles still represented over 80 percent of global car sales in 2023 despite the rapid rise of electrification. Consumers in many regions remain hesitant to adopt electric vehicles due to concerns about charging availability and range anxiety particularly in rural areas. The lower purchase price of ICE vehicles makes them accessible to budget conscious buyers in developing economies where electricity grids may be unstable. Established manufacturing processes and supply chains for engines and transmissions allow automakers to produce ICE vehicles efficiently and profitably. The familiarity of driving and maintaining ICE vehicles reduces the learning curve for owners. Additionally the resale value of ICE vehicles remains relatively stable in many markets due to consistent demand. Technological improvements in engine efficiency and emissions control have extended the viability of ICE technology in the face of stricter regulations. Hybrid vehicles which combine ICE with electric motors also contribute to this segment's longevity by offering a transitional solution for consumers not ready for full electrification.

The Electric propulsion segment is predicted to witness the highest CAGR of 20.6% between 2026 and 2034 owing to stringent government mandates to reduce carbon emissions and substantial investments in charging infrastructure. Governments in Europe China and North America offer tax credits rebates and non monetary incentives such as access to bus lanes to encourage adoption. Automakers are launching a wide variety of electric models across all segments making them competitive with ICE counterparts in terms of performance and features. Advances in battery technology have significantly improved driving ranges reducing range anxiety and making electric cars suitable for daily use. The lower operating and maintenance costs of electric vehicles appeal to consumers seeking long term savings. Corporate fleets are transitioning to electric vehicles to meet sustainability goals driving bulk purchases. Consumer awareness of environmental issues and the desire for quiet smooth driving experiences further boost demand. The expansion of fast charging networks along highways facilitates long distance travel enhancing the practicality of electric vehicles. These factors collectively accelerate the transition from fossil fuels to electric mobility.

By Vehicle Class Insights

In 2025, the Mid-Range segment held the largest share of the passenger car market because of its balance of affordability features and reliability. This class appeals to the broadest demographic including families young professionals and small business owners who seek value without compromising on quality. Automakers invest heavily in this segment offering well equipped models with advanced safety features connectivity and comfortable interiors at competitive prices. The availability of financing options and leasing programs makes mid range cars accessible to middle income households. Brands in this segment benefit from strong reputation for durability and low maintenance costs which are key decision factors for buyers. The variety of body styles available including sedans hatchbacks and compact SUVs ensures that consumers can find a vehicle that suits their lifestyle. Mid range cars often serve as the entry point for brand loyalty with customers upgrading within the same marque over time. Manufacturers achieve economies of scale in this segment allowing them to offer competitive pricing while maintaining healthy margins. The segment benefits from continuous updates in technology and design keeping it relevant and attractive to modern consumers.

The Premium segment is estimated to register the fastest CAGR of 8.2% over the forecast period. This quick surge of the segment is propelled by rising disposable incomes and the desire for luxury and status. Affluent consumers in emerging markets such as China and India are increasingly purchasing premium vehicles as symbols of success and social standing. Premium brands offer superior craftsmanship advanced technology and exclusive services that appeal to discerning buyers. The integration of cutting edge features such as autonomous driving aids premium audio systems and bespoke customization options differentiates these vehicles from mass market alternatives. High net worth individuals view premium cars as investment pieces and lifestyle accessories rather than mere transportation. The growth of electric luxury vehicles has attracted tech savvy buyers who appreciate the combination of performance and sustainability. Limited edition models and personalized buying experiences enhance the exclusivity and appeal of premium brands. Corporate executives and celebrities influence trends by adopting premium vehicles generating media attention and aspirational demand. The segment benefits from stronger residual values and dedicated customer service networks. As wealth distribution shifts globally the premium segment continues to outpace other classes in growth potential.

By Drivetrain Insights

The Front Wheel Drive segment was the largest in the passenger car market and occupied a commanding share in 2025. Several key factors fueled this growth, including production cost-efficiency, optimized cabin space, and practical daily performance. This drivetrain configuration allows for more interior cabin space as there is no need for a driveshaft tunnel to the rear wheels. According to sources, front wheel drive vehicles account for over 60 percent of global passenger car production reflecting their dominance in the economy and mid range segments. The simpler mechanical layout reduces manufacturing costs and weight improving fuel efficiency which is a key selling point for budget conscious consumers. Front wheel drive provides adequate traction for most urban and suburban driving scenarios making it the preferred choice for compact cars and family sedans. The predictable handling characteristics of front wheel drive vehicles are easier for average drivers to manage enhancing safety and confidence. Automakers leverage platform sharing to produce front wheel drive models efficiently across multiple brands. The widespread availability of replacement parts and service expertise further supports the popularity of this drivetrain. While not ideal for high performance or off road use front wheel drive meets the needs of the majority of drivers who prioritize practicality and economy. Its dominance is reinforced by the prevalence of small and medium sized vehicles which form the bulk of global sales.

The All Wheel Drive segment is anticipated to witness the fastest CAGR of 7.3% from 2026 and 2034. This rapid expansion of the segment is fuelled by the popularity of SUVs and crossovers. Consumers increasingly prefer all wheel drive for its enhanced traction and stability in adverse weather conditions such as rain snow and ice. According to Edmunds all wheel drive is becoming a standard feature in many mid size and luxury SUVs reflecting changing consumer preferences. The rise of electric vehicles has facilitated the adoption of all wheel drive as electric motors can be easily placed on both axles without complex mechanical linkages. This configuration offers superior acceleration and handling performance appealing to enthusiasts and safety conscious buyers. Marketing campaigns emphasize the safety benefits of all wheel drive encouraging adoption in regions with variable climates. The premiumization of the market means more buyers are willing to pay extra for the added security and performance of all wheel drive. Automakers are introducing intelligent all wheel drive systems that automatically distribute power to wheels with the most grip enhancing efficiency and control. The expansion of the SUV segment which predominantly features all wheel drive options directly contributes to this growth. Consumers seek versatile vehicles capable of handling diverse driving conditions. As a result, all-wheel drive becomes an increasingly attractive proposition.

REGIONAL ANALYSIS

Asia Pacific Passenger Car Market Analysis

Asia Pacific outperformed other regions in the global passenger car market and accounted for a 45.6% share in 2025. This supremacy of the APAC market was driven by massive populations and rapid economic development. China serves as the primary engine of growth with the world largest automotive market supported by strong government policies promoting electric vehicle adoption. According to the China Association of Automobile Manufacturers passenger car sales in China exceeded 20 million units in 2023 reflecting robust domestic demand. India and Southeast Asian countries like Thailand and Indonesia are also experiencing significant growth as rising middle classes aspire to car ownership. Local manufacturing hubs in the region enable cost effective production for both domestic consumption and export. Governments in Asia Pacific are investing heavily in infrastructure including roads and charging networks to support vehicle usage. The preference for compact and fuel efficient vehicles aligns with urban density and traffic conditions in major cities. Joint ventures between international and local automakers facilitate technology transfer and market access. The region leads in electric vehicle adoption due to aggressive subsidies and regulatory mandates. Consumer preferences are shifting towards SUVs and connected vehicles mirroring global trends. The dynamic nature of the Asia Pacific market offers immense opportunities for innovation and expansion.

Asia Pacific Passenger Car Market Analysis

North America followed closely behind in the global passenger car market because of high vehicle ownership rates and a preference for larger vehicles. The United States accounts for the majority of regional sales driven by consumer demand for SUVs trucks and crossovers. According to the U.S. Bureau of Economic Analysis (BEA), domestic light vehicle sales in the United States demonstrated resilience in 2023 by rising to approximately 15.5 million units despite high interest rates and economic headwinds. Canada and Mexico contribute to regional growth through integrated supply chains under trade agreements. Consumers in North America prioritize performance comfort and technology leading to higher average transaction prices. The widespread availability of credit and leasing options facilitates vehicle purchases. Government incentives for electric vehicles are accelerating the transition to cleaner mobility particularly in states like California. The region hosts major automakers who are investing billions in electric and autonomous vehicle technologies. High mileage driving habits increase the demand for durable and reliable vehicles. Aftermarket services and customization are popular among consumers enhancing the ownership experience. North America remains a key testing ground for new automotive technologies and business models.

Europe Passenger Car Market Analysis

Europe holds a significant share of the global passenger car market due to strict environmental regulations and a high adoption of diesel and electric vehicles. The European Union aims to ban the sale of new internal combustion engine cars by 2035 prompting automakers to accelerate electrification plans. Also, the European Automobile Manufacturers Association (ACEA) show that new passenger car registrations in the EU expanded by 13.9% over the course of 2023 to reach 10.5 million units. Countries like Germany France and the United Kingdom lead in automotive innovation and luxury vehicle production. Consumers in Europe prioritize fuel efficiency safety and environmental sustainability influencing vehicle design and features. Dense urban environments favor compact cars and hatchbacks although SUVs are gaining popularity. Government subsidies and tax benefits for electric vehicles drive adoption rates. The region has a well developed charging infrastructure supporting electric mobility. Strong labor unions and manufacturing traditions ensure high quality production standards. Cross border trade within the EU facilitates efficient distribution of vehicles. Europe continues to lead in setting global standards for emissions and safety.

Latin America Passenger Car Market Analysis

Latin America is a growing segment of the passenger car market owing to economic recovery and increasing urbanization. Brazil and Mexico are the primary markets with established automotive industries and growing consumer demand. Economic volatility and currency fluctuations impact affordability but long term trends favor increased motorization. Governments are implementing policies to promote local manufacturing and reduce import tariffs. The preference for flexible fuel vehicles in Brazil supports the use of ethanol blends. Rising middle class populations in urban centers drive demand for entry level and mid range cars. Infrastructure improvements are enhancing road connectivity and vehicle usage. International automakers are expanding production capacities to meet regional demand. Financing options are becoming more accessible supporting vehicle purchases. The region offers potential for growth as economic stability improves.

Middle East and Africa Passenger Car Market Analysis

Middle East and Africa region is likely to expand notably in the global passenger car market during the forecast period. It presents unique dynamics with slow initial adoption but growing interest in passenger cars. Gulf countries like the United Arab Emirates and Saudi Arabia are home to luxury vehicle markets driven by high disposable incomes. The United Nations Economic and Social Commission for Western Asia (ESCWA) details that the adoption of electric vehicles is expanding across Arab transport networks as governments implement national diversification plans to lower hydrocarbon reliance. South Africa leads adoption in sub Saharan Africa driven by urbanization and economic activity. High temperatures and harsh conditions require vehicles with robust cooling and durability. Governments are investing in infrastructure to support mobility. The lack of local manufacturing means reliance on imports affecting pricing. Consumer preference for SUVs and large sedans reflects lifestyle and road conditions. Financial institutions are developing loan products to support car ownership. The region faces challenges related to fuel subsidies and infrastructure but shows potential for growth. Strategic location facilitates trade and logistics operations.

COMPETITIVE LANDSCAPE

The competition in the passenger car market is characterized by intense rivalry among established global manufacturers and emerging electric vehicle specialists who strive to dominate the rapidly evolving mobility landscape. Traditional automakers leverage their extensive manufacturing expertise brand heritage and dealer networks to maintain customer loyalty while transitioning to electric platforms. New entrants disrupt the market with innovative software defined vehicles and direct sales models that challenge conventional business practices. Competitors differentiate themselves through unique design languages advanced driver assistance systems and superior connectivity features. Price competition remains fierce particularly in the economy and mid range segments where consumers are highly sensitive to cost. The shift towards electrification has lowered barriers to entry for technology companies leading to increased collaboration and consolidation. Strategic alliances are crucial for sharing the high costs of research and development in batteries and autonomous technologies. Regulatory pressures regarding emissions and safety standards further intensify competition as manufacturers race to comply while maintaining profitability. The ability to innovate rapidly and deliver sustainable value determines long term success in this dynamic industry.

KEY MARKET PLAYERS

Some of the key players dominating the global passenger car market are

- Bayerische Motoren Werke AG

- Daimler AG (Mercedes-Benz AG)

- Ford Motor Company

- General Motors Company

- Honda Motor Co. Ltd.

- Hyundai Motor Company

- Kia Corporation

- Nissan Motor Co. Ltd.

- Toyota Motor Corporation

- Volkswagen AG

Top Players in the Market

- Toyota Motor Corporation maintains its global leadership through a robust production system and diverse portfolio ranging from compact cars to luxury SUVs. The company has aggressively expanded its hybrid vehicle offerings while investing heavily in battery electric vehicles and hydrogen fuel cell technology. Recent initiatives include strategic partnerships with semiconductor manufacturers to secure supply chains and the launch of new dedicated electric platforms. Toyota focuses on multi pathway strategies to meet varying regional regulations and consumer preferences ensuring broad market appeal. Its commitment to quality reliability and continuous improvement reinforces brand loyalty worldwide. By leveraging its extensive global manufacturing footprint Toyota ensures efficient delivery and localized production capabilities. These efforts strengthen its position as a dominant force capable of adapting to rapid industry changes while maintaining operational excellence and financial stability in the competitive automotive landscape.

- Volkswagen Group plays a pivotal role by driving the industry transition towards electrification with its ambitious ID series and premium electric models. The German conglomerate invests billions in developing proprietary software and battery technologies to enhance vehicle performance and user experience. Recent actions include establishing joint ventures for battery cell production in Europe and North America to reduce dependency on external suppliers. Volkswagen is also restructuring its brands to focus on distinct market segments from mass market to ultra luxury. The company prioritizes sustainable manufacturing processes and circular economy principles to align with strict environmental regulations. By integrating advanced digital services and over the air update capabilities Volkswagen aims to create a seamless connected ecosystem. These strategic moves solidify its reputation as an innovator committed to shaping the future of sustainable mobility and maintaining competitive advantage in key global markets.

- Hyundai Motor Group contributes significantly by offering high value vehicles with advanced technology and distinctive design language. The South Korean manufacturer has gained global recognition for its Ioniq electric vehicle lineup and Genesis luxury brand expansion. Recent strategies involve substantial investments in autonomous driving technology and robotaxi services through partnerships with tech firms. Hyundai is also expanding its production facilities in emerging markets to capture growing demand and mitigate trade barriers. The company emphasizes customer centric innovation by integrating smart connectivity features and personalized user interfaces. Its focus on hydrogen mobility complements its electric vehicle strategy providing comprehensive zero emission solutions. By delivering reliable and stylish vehicles at competitive prices Hyundai attracts a diverse global customer base. These initiatives enhance its brand equity and market presence positioning it as a formidable challenger to established automotive giants in the evolving passenger car sector.

Top Strategies Used by Key Market Participants

Key players in the passenger car market primarily employ platform sharing and modular architecture strategies to reduce development costs and accelerate time to market for new models. Companies invest heavily in electrification and autonomous driving technologies to comply with stringent environmental regulations and meet evolving consumer expectations. Strategic partnerships with technology firms and battery manufacturers are common to secure critical components and enhance software capabilities. Manufacturers also focus on direct to consumer sales models and digital retail experiences to improve customer engagement and transparency. Expansion into emerging markets through local production facilities helps mitigate tariff risks and cater to regional preferences. Sustainability initiatives including carbon neutral manufacturing and circular economy practices are increasingly central to corporate strategies. These approaches enable automakers to maintain profitability while navigating the complex transition towards software defined and electric vehicles in a highly competitive global environment.

Global Passenger Car Market News

- In October 2023, Toyota Motor Corporation partnered with Idemitsu Kosan to jointly develop and mass-produce all-solid-state battery technology, aiming for commercialization by 2027–2028 to significantly enhance future electric vehicle range.

- In October 2024, Hyundai Motor Company entered into a multi-year strategic partnership with Alphabet's Waymo to integrate fully autonomous driving technology into its all-electric IONIQ 5 fleet.

MARKET SEGMENTATION

This research report on the global passenger car market is segmented and sub-segmented into the following categories.

By Vehicle Type

- Hatchbacks

- Sedans

- SUVs & Crossovers

By Propulsion

- ICE

- Electric

By Vehicle Class

- Economy

- Mid-Range

- Premium

By Size

- Small

- Mid-Size

- Large

By Drivetrain

- Rear-Wheel Drive

- Front-Wheel Drive

- All-Wheel Drive

- Four-Wheel Drive

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

1. What is the Passenger Car Market?

The Passenger Car Market encompasses the global production, sale, and distribution of vehicles designed primarily for transporting passengers, including hatchbacks, sedans, SUVs, and crossovers.

2. What factors are driving the growth of the Passenger Car Market?

The market is driven by rising disposable incomes, increasing urbanization, expanding middle-class populations, growing demand for personal mobility, and rapid advancements in automotive technologies.

3. What are the major vehicle types in the Passenger Car Market?

The major vehicle types include hatchbacks, sedans, and SUVs & crossovers, with SUVs experiencing particularly strong demand worldwide.

4. How is vehicle electrification impacting the Passenger Car Market?

The growing adoption of electric passenger cars, supported by government incentives, stricter emission regulations, and advancements in battery technology, is accelerating market growth.

5. Which propulsion types are available in the Passenger Car Market?

Passenger cars are primarily available with internal combustion engine (ICE) and electric propulsion systems, with hybrid models also gaining popularity in many regions.

6. Which region dominates the Passenger Car Market?

Asia-Pacific dominates the Passenger Car Market due to high vehicle production, increasing consumer demand, and the strong presence of leading automotive manufacturers in countries such as China, Japan, and India.

7. Which region is expected to witness the fastest market growth?

The Asia-Pacific region is expected to record the fastest growth owing to rising vehicle ownership, expanding electric vehicle adoption, and supportive government policies.

8. What challenges does the Passenger Car Market face?

Major challenges include fluctuating raw material prices, semiconductor supply constraints, stringent emission regulations, rising manufacturing costs, and economic uncertainties affecting consumer spending.

9. What role do advanced technologies play in the Passenger Car Market?

Advanced technologies such as advanced driver-assistance systems (ADAS), connected vehicle solutions, artificial intelligence, autonomous driving features, and over-the-air software updates are transforming passenger vehicles.

10. Who are the leading companies in the Passenger Car Market?

Leading companies include Toyota Motor Corporation, Volkswagen AG, Hyundai Motor Company, Kia Corporation, Honda Motor Co. Ltd., Nissan Motor Co. Ltd., Ford Motor Company, General Motors Company, Bayerische Motoren Werke AG (BMW), and Mercedes-Benz AG.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com