- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

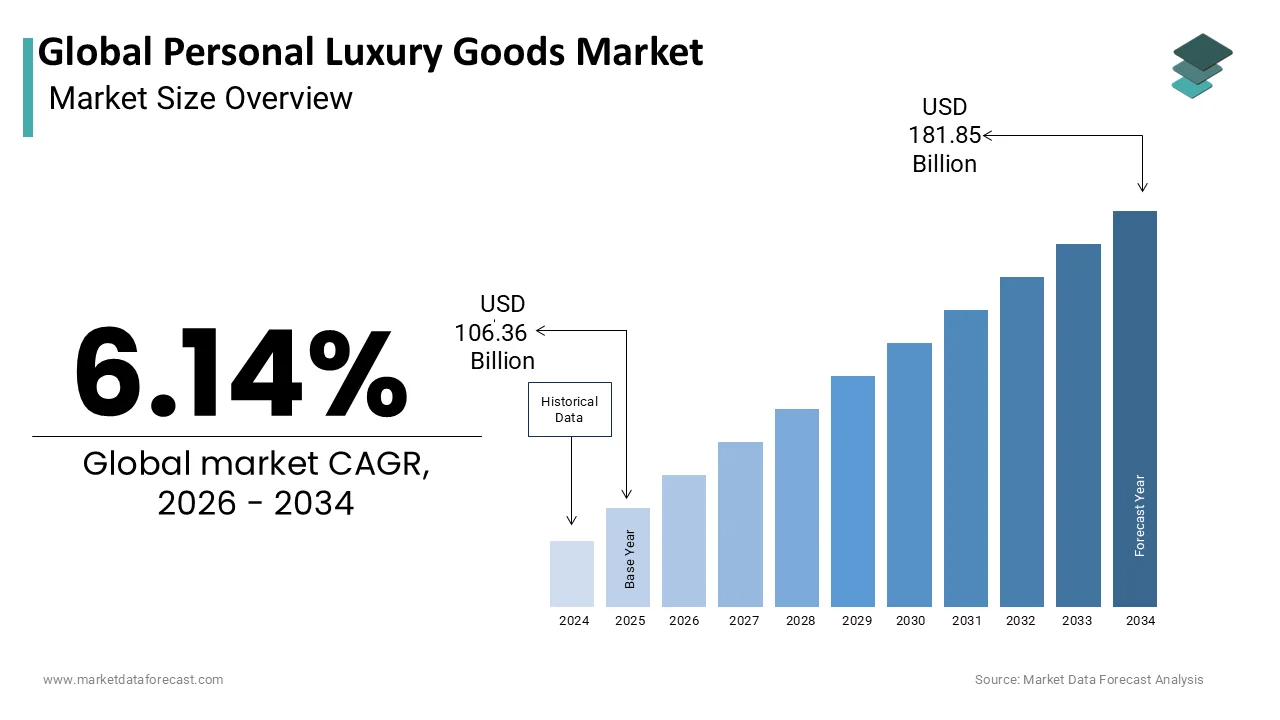

Market Size, 2025

$106.3 BnMarket Estimate, 2026

$112.8 BnMarket Forecast, 2034

$181.8 BnCAGR, 2026–2034

6.14%Executive Summary: Personal Luxury Goods Market

- Market Scope: Comprehensive personal luxury goods industry analysis covering product categories, distribution channels, consumer demographics, regional market shares, digitalization trends, and wealth-generation metrics.

- Market Valuation: Valued at USD 106.36 billion (2025), estimated at USD 112.89 billion (2026), and forecast to attain USD 181.85 billion by 2034, registering a solid CAGR of 6.14% (2026–2034).

- Primary Growth Drivers: Acceleration of digital luxury retail, robust growth among affluent and high-net-worth consumers, and rising online engagement. Key structural and demographic benchmarks include Europe housing over 18 million millionaires (with their population increasing about 5% annually over the past five years), European online fashion and luxury sales growing 15% year-on-year, and 65% of Gen Z consumers utilizing social media to discover new luxury products.

Key Market Segment Metrics (2026–2034)

| Category | Leading Segment (2025 Position) | Fastest-Growing Segment |

|---|---|---|

| By Product Type | Luxury fashion and apparel (dominated with a 40.4% global market share in 2025) | Fine jewelry and luxury watches (projected to grow at an 8.5% CAGR) |

| By Distribution Channel | Exclusive brand boutiques and flagship retail stores (held the major share in 2025) | Online retail platforms and digital commerce (forecast to expand at a 10.4% CAGR) |

| By Consumer Demographics | High-net-worth individuals / HNWIs (held the largest overall market share) | Young affluent and Gen Z consumers (projected to grow fastest at a 9.1% CAGR) |

| By Region | Europe (held the leading global share in 2025, with the EU accounting for ~30% of global personal luxury consumption) | Emerging luxury markets expanding across Asia-Pacific and high-net-worth corridors |

Major Market Players & Market Structure

Market Structure: Highly competitive and prestigious global luxury goods marketplace featuring historic European heritage conglomerates and independent design houses competing intensely on vertical integration, digital transformation, omnichannel retail, sustainable raw material sourcing, circular-economy resale models, strategic acquisitions, personalization, and emerging-market expansion (such as Lacoste's strategic expansion targeting an increase in U.S. sales from USD 400 million to USD 800 million).

Key Companies: LVMH, Kering, Compagnie Financière Richemont, Prada, Chanel, Hermès, Burberry, Rolex, Tiffany & Co., and Valentino.

Global Personal Luxury Goods Market Size

The global personal luxury goods market size was valued at USD 106.36 billion in 2025 and is projected to grow from USD 112.89 billion in 2026 to USD 181.85 billion by 2034, the market is expected to grow at a CAGR of 6.14% from 2026 to 2034.

Personal luxury goods include high-value items such as leather goods, footwear, ready-to-wear apparel, jewelry, watches, and cosmetics that serve as symbols of status, craftsmanship, and individual expression. These products are characterized by premium pricing, exclusive distribution channels, and strong brand heritage that transcends mere functional utility. In Europe, this sector is deeply intertwined with cultural identity and artistic tradition, particularly in nations like France and Italy, where artisanal skills have been preserved for centuries. The consumption patterns reflect broader socioeconomic trends, including wealth distribution and consumer confidence levels. According to Eurostat, the household final consumption expenditure on clothing and footwear in the European Union reached approximately 200 billion euros in recent years, indicating a robust baseline for luxury spending within these categories. Furthermore, data from the United Nations World Tourism Organization reveals that international tourist arrivals in Europe exceeded 700 million in 2023, with a significant portion of travel budgets allocated to shopping for luxury items. This influx of global visitors sustains demand in key retail hubs such as Paris, Milan, and London. The market operates within a complex ecosystem of supply chain intricacies, intellectual property protection, and evolving consumer ethics. As digital transformation reshapes retail interactions, the definition of luxury expands to include experiential elements and personalized services, reinforcing the emotional connection between brands and affluent consumers across the continent.

MARKET DRIVERS

Resurgence of High Net Worth Individual Population Driving Exclusive Demand

The expanding population of high-net-worth individuals is fuelling the expansion of the personal luxury goods market, which is creating a stable base of consumers with significant disposable income. Wealth accumulation in Europe has been steady, driven by asset appreciation in real estate and equity markets. According to the Credit Suisse Global Wealth Report, the number of millionaires in Europe increased by 5% annually over the past five years and is reaching over 18 million individuals. This demographic prioritizes quality, exclusivity, and brand heritage, often viewing luxury purchases as investments or stores of value rather than mere consumables. The concentration of wealth in urban centers such as Zurich, Geneva, and Monaco creates localized hubs of intense luxury consumption. These consumers are less sensitive to economic fluctuations compared to mass market buyers, ensuring consistent demand even during periods of broader economic uncertainty. Additionally, the intergenerational transfer of wealth is accelerating, with younger heirs entering the market with distinct preferences for sustainability and digital engagement. Brands that cater to this segment through private client services, bespoke offerings, and invitation-only events foster deep loyalty. The desire for social distinction and membership in exclusive circles motivates repeated purchases of high-ticket items such as haute couture and fine jewelry. This psychological need for status reinforcement among the affluent class sustains the premium pricing power of luxury brands and drives continuous innovation in product design and customer experience.

Digital Transformation and E-Commerce Integration Expanding Consumer Reach

The rapid adoption of digital technologies and e-commerce platforms has revolutionized access to personal luxury goods, which is removing geographical barriers, engaging younger demographics, and contributing to the personal luxury goods market expansion. Luxury brands have shifted from resisting online sales to embracing omnichannel strategies that blend physical exclusivity with digital convenience. As per the European E-Commerce Association, online sales of fashion and luxury goods in Europe grew by 15% year on year, outpacing overall retail growth. Social media platforms such as Instagram and TikTok have become critical discovery channels, where visual storytelling influences purchasing decisions among millennials and Generation Z consumers. These digital natives expect seamless transactions, augmented reality try-on features, and personalized recommendations powered by artificial intelligence. Brands invest heavily in sophisticated websites and mobile applications that replicate the ambiance of flagship stores through high-resolution imagery and virtual consultations. The integration of live streaming events and digital fashion shows allows brands to reach global audiences instantly, creating buzz and immediate demand. Furthermore, data analytics enable companies to understand consumer behavior precisely, tailoring marketing messages and inventory allocation to specific regions and preferences. This digital shift also facilitates direct-to-consumer relationships, reducing reliance on third-party wholesalers and increasing profit margins. The ability to engage customers 24 hours a day across multiple touchpoints ensures that luxury remains relevant and accessible in an increasingly connected world.

MARKET RESTRAINTS

Economic Volatility and Inflationary Pressures Restraining Discretionary Spending

Economic instability and rising inflation rates are significant restraints on the personal luxury goods market by eroding consumer purchasing power and confidence. High inflation affects the cost of living, forcing households to prioritize essential expenses over discretionary luxury purchases. According to Eurostat, the annual inflation rate in the Euro area peaked at 10.6% in late 2022, remaining elevated in subsequent periods, which significantly impacted household budgets. Consumers become more cautious with spending, delaying, or canceling purchases of non-essential high-value items. The uncertainty surrounding interest rates and potential recessions leads to a savings-oriented mindset, reducing the liquidity available for luxury consumption. Middle-income aspirational buyers, who form a substantial part of the luxury customer base, are particularly vulnerable to these economic shocks. They may trade down to affordable luxury segments or seek discounts, putting pressure on brand pricing strategies. Additionally, currency fluctuations affect the profitability of international luxury groups and the affordability of imported goods for local consumers. A strong euro can make European luxury goods more expensive for tourists from other regions, potentially dampening duty-free sales. Retailers face higher operational costs due to energy price hikes and wage increases, squeezing margins if they cannot pass these costs onto price-sensitive customers. This economic environment necessitates careful inventory management and strategic pricing adjustments to maintain sales volumes without diluting brand equity.

Stringent Sustainability Regulations and Ethical Sourcing Requirements Increasing Compliance Costs

The implementation of strict sustainability regulations and ethical sourcing requirements imposes substantial operational burdens and costs on luxury goods manufacturers, which further impedes the expansion of the global market. European Union policies such as the Corporate Sustainability Reporting Directive mandate detailed disclosures on environmental and social impacts, requiring extensive data collection and verification processes. As per the European Commission, companies must comply with new eco-design standards that dictate material durability, recyclability, and carbon footprint limits. Luxury brands, which often rely on rare materials such as exotic leathers and precious metals, face heightened scrutiny regarding their supply chains. Ensuring traceability from raw material extraction to final product assembly requires significant investment in technology and supplier audits. Failure to comply can result in hefty fines and reputational damage, as consumers increasingly penalize brands associated with environmental harm or labor violations. The transition to sustainable practices involves redesigning products, sourcing alternative materials, and modifying manufacturing processes, all of which entail high upfront costs. Small artisanal suppliers may struggle to meet these regulatory demands, threatening the availability of traditional craftsmanship inputs. Moreover, greenwashing accusations pose a risk if marketing claims do not align with actual practices, leading to consumer distrust. Navigating this complex regulatory landscape diverts resources from creative innovation and marketing, challenging brands to balance compliance with profitability while maintaining their image of exclusivity and desirability.

MARKET OPPORTUNITIES

Expansion into Emerging Markets and Digital Native Consumer Segments

Targeting emerging markets and engaging digital native consumer segments offer substantial opportunities for the personal luxury goods market. Countries in Eastern Europe and Asia exhibit rising middle classes with an increasing appetite for Western luxury brands. As per the World Bank, GDP per capita in several emerging European economies has grown by over 4% annually, enhancing purchasing power. Brands can leverage digital platforms to enter these markets with lower initial investment compared to establishing physical stores. Collaborating with local influencers and adapting marketing narratives to cultural nuances helps build brand affinity among new consumers. Additionally, the rise of the metaverse and non-fungible tokens offers novel avenues for brand expression and revenue generation. Luxury houses are experimenting with virtual garments and digital collectibles that appeal to tech-savvy younger audiences. These digital assets allow consumers to express status in online environments, creating a new category of luxury consumption. Partnerships with gaming platforms and virtual worlds enable brands to reach millions of users globally. Furthermore, offering personalized customization services through digital interfaces enhances customer engagement and loyalty. By embracing these technological frontiers, luxury brands can diversify their revenue streams and remain relevant to future generations of consumers who value digital ownership and interactive experiences as much as physical possessions.

Development of Circular Economy Models and Resale Platforms

The development of circular economy models and participation in the resale market offer significant opportunities for luxury brands to enhance sustainability and capture additional value, which is another prominent opportunity for the global market. The second-hand luxury market is expanding rapidly, driven by consumer interest in vintage items and sustainable consumption. According to ThredUp’s Resale Report, the global second-hand market is projected to grow twice as fast as the primary apparel market. Luxury brands can launch their own certified pre-owned programs to control the quality and authenticity of resold items. This strategy allows them to retain customer relationships throughout the product lifecycle and attract price-sensitive buyers who aspire to own luxury goods. Implementing take-back schemes and repair services extends product longevity and reinforces brand commitment to durability. These initiatives align with growing consumer demand for ethical practices and reduce environmental impact. Collaborating with established resale platforms provides access to existing customer bases and logistical infrastructure. Brands can use data from resale transactions to understand product durability and consumer preferences, informing future design decisions. Moreover, circular models create new revenue streams through service fees and refurbished sales. By leading the transition toward a circular economy, luxury houses can differentiate themselves from fast fashion competitors and strengthen their brand narrative around timeless value and responsibility.

MARKET CHALLENGES

Counterfeit Products Undermining Brand Integrity and Revenue

The proliferation of counterfeit products is a severe challenge to the personal luxury goods market by undermining brand integrity and diverting revenue. Advanced manufacturing techniques have enabled the production of high-quality fakes that are difficult to distinguish from authentic items. As per the Organisation for Economic Cooperation and Development, trade in counterfeit and pirated goods amounts to hundreds of billions of dollars globally, with luxury items being the primary targets. Counterfeits dilute brand exclusivity and damage reputation when consumers associate poor-quality fake products with the original brand. Legal enforcement against counterfeiters is complex and costly, involving cross-border coordination and intellectual property litigation. Online marketplaces facilitate the sale of fake goods, making it difficult for brands to monitor and remove listings effectively. Consumers who unknowingly purchase counterfeits may become dissatisfied and lose trust in the brand. Additionally, the existence of cheap alternatives reduces the perceived value of authentic luxury items, pressuring brands to justify their premium pricing. Protecting intellectual property requires continuous investment in anti-counterfeit technologies such as blockchain tracking and holographic labels. However, these measures add to production costs and may not fully deter determined counterfeiters. The constant battle against fakes distracts management's focus and resources from core business activities, hindering innovation and growth potential in the legitimate market.

Supply Chain Disruptions and Raw Material Scarcity Affecting Production

Supply chain disruptions and scarcity of raw materials are further impeding the personal luxury goods market expansion worldwide. Luxury items often depend on specialized materials such as high-grade leather, silk, and precious stones, which are subject to volatile availability and pricing. According to the European Central Bank, supply bottlenecks have led to significant delays and cost increases in various manufacturing sectors. Climate change impacts agricultural outputs, affecting the quality and quantity of natural fibers and leathers. Geopolitical tensions and trade restrictions further complicate the sourcing of materials from key regions. Labor shortages in skilled artisanal roles, such as leather crafting and watchmaking, exacerbate production constraints. Training new artisans takes years, limiting the ability to scale up production quickly in response to demand spikes. Logistics challenges, including port congestion and transportation delays, affect the timely distribution of finished goods to retail outlets. These disruptions force brands to hold higher inventory levels, tying up capital and increasing storage costs. Inability to meet customer demand due to stockouts can lead to lost sales and diminished brand loyalty. Companies must diversify their supplier base and invest in supply chain resilience, but these strategies require substantial time and financial commitment. Balancing the need for exclusivity with the imperative of reliable availability remains a delicate operational challenge for luxury manufacturers.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Distribution Channel, Demographic, and Region |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | LVMH (Moet Hennessy Louis Vuitton, Kering, Richemont, Prada, Chanel, Hermes, Burberry, Rolex, Tiffany & Co., Valentino, and others. |

SEGMENTAL ANALYSIS

By Product Insights

The luxury fashion segment dominated the market by commanding the highest share of the global market in 2025 due to its deep-rooted cultural significance and the powerful narrative of brand heritage that resonates with consumers globally. European houses such as Chanel, Dior, and Gucci have cultivated centuries-old reputations for craftsmanship and artistic innovation, making their ready-to-wear collections highly desirable status symbols. According to Bain and Company, luxury fashion accounts for approximately 35% of the total personal luxury goods market value, reflecting its central role in consumer spending. The visibility of fashion items in social settings and media platforms amplifies their aspirational value, driving consistent demand across diverse demographic groups. Consumers view high-end apparel and accessories as tangible expressions of identity and success, justifying premium pricing. The seasonal nature of fashion collections creates a recurring purchase cycle, encouraging repeat visits to boutiques and online stores. Furthermore, the integration of celebrity endorsements and influencer marketing enhances the desirability of specific lines, creating viral trends that boost sales volumes. The emotional connection fostered through storytelling and exclusive runway events strengthens brand loyalty, ensuring that customers remain committed to specific houses despite economic fluctuations. This enduring appeal of fashion as a medium for self-expression sustains its dominance in the luxury landscape.

On the other hand, the jewelry and watches segment is anticipated to register a CAGR of 8.5% during the forecast period, due to their perception as reliable stores of value and investment assets. Unlike fashion items, ms which may depreciate quickly, high-quality timepieces and fine jewelry often retain or appreciate over time. According to Deloitte, the secondary market for luxury watches has grown significantly, indicating strong investor interest and liquidity. Consumers increasingly view purchases of iconic models from brands like Rolex and Patek Philippe as financial decisions rather than mere consumption. The scarcity of certain models and the complexity of mechanical movements contribute to their long-term value retention. Economic uncertainty prompts wealthy individuals to diversify their portfolios with tangible assets that are portable and universally recognized. Auction houses report record-breaking sales for vintage pieces, reinforcing the investment narrative. Additionally, the transparency provided by blockchain technology for provenance tracking enhances buyer confidence in authenticity and value. This dual function of adornment and asset accumulation makes jewelry and watches particularly attractive to prudent luxury shoppers. The growing awareness of these financial benefits among younger demographics further accelerates market expansion in this category.

By Distribution Channel Insights

The exclusive brand boutiques segment occupied the major share of the personal luxury goods market in 2025 because they offer an immersive brand experience and personalized service that cannot be replicated in other retail environments. These flagship stores are designed as temples of luxury, featuring architectural masterpieces and curated interiors that reflect the brand’s heritage and values. According to McKinsey and Company, over 60% of high-net-worth individuals prefer purchasing luxury goods in boutique settings due to the elevated level of customer care and exclusivity. Staff in these boutiques undergo rigorous training to provide bespoke consultations, styling advice, and after-sales support, fostering deep relationships with clients. The availability of limited edition items and made-to-order services exclusively in boutiques drives foot traffic and enhances brand allure. Private viewing rooms and invitation-only events create a sense of privilege and community among loyal customers. The control over visual merchandising and atmosphere allows brands to communicate their narrative effectively, reinforcing brand equity. This direct interaction enables companies to gather valuable feedback and tailor offerings to local preferences. The tactile experience of touching fabrics and trying on items remains crucial for high-value purchases, ensuring that boutiques remain the preferred channel for discerning shoppers seeking authenticity and prestige.

However, the online retail segment is the fastest-growing distribution channel and is estimated to register a CAGR of 10.4% during the forecast period, owing to the growing preferences of digital native consumers and the convenience of home shopping. Millennials and Generation Z shoppers are comfortable making high-value purchases online, expecting seamless user interfaces and secure payment options. According to Eurostat, e-commerce sales in the European Union increased by 14% year on year, with luxury goods being a significant contributor to this growth. The ability to browse extensive catalogs, compare prices, and read reviews empowers consumers to make informed decisions without visiting physical stores. Mobile optimization allows for shopping on the go, fitting into busy lifestyles. Enhanced logistics services, including same-day delivery and easy returns, mitigate the risks associated with online buying. Virtual try-on technologies and augmented reality features help bridge the gap between physical and digital experiences, allowing customers to visualize products accurately. The availability of exclusive online launches and digital-only collections creates urgency and drives traffic to brand websites. Social commerce integration enables direct purchasing from social media platforms, shortening the customer journey. These conveniences align with modern consumer expectations, accelerating the shift toward online channels for luxury acquisitions.

By Demographic Insights

The high net worth individuals segment had the largest share of the global personal luxury goods market in 2025 due to their substantial disposable income and capacity for high-value purchases. This group possesses significant financial resources that allow them to buy expensive items such as haute couture, fine jewelry, and luxury vehicles without budget constraints. According to Credit Suisse, the top 1% of wealth holders in Europe own more than 25% of total household wealth, concentrating purchasing power in a small but influential segment. These consumers prioritize quality, exclusivity, and craftsmanship, often viewing luxury goods as essential components of their lifestyle. They are less affected by economic downturns, providing stability to the luxury market during volatile periods. Their spending habits drive demand for limited edition and bespoke items that cater to their desire for uniqueness. High net worth individuals also engage in concierge services and private shopping experiences, contributing significantly to brand revenues. Their influence extends beyond personal consumption, as they often set trends that trickle down to aspirational buyers. Brands focus intensely on cultivating relationships with this segment through exclusive events and personalized communication. The consistent spending power of high-net-worth individuals ensures a stable foundation for the luxury goods industry.

However, the young affluent consumers segment is the fastest-growing demographic and is predicted to grow at a CAGR of 9.1% during the forecast period, owing to the profound influence of social media and digital culture on their buying behavior. This group, comprising millennials and Generation Z, discovers and evaluates luxury brands primarily through digital platforms such as Instagram, TikTok, and YouTube. According to GWI, 65% of Gen Z consumers use social media to discover new luxury products, making digital presence critical for brand relevance. Influencers and celebrities play a pivotal role in shaping perceptions and driving desire for specific items. Young consumers value authenticity and transparency, preferring brands that align with their personal values and social causes. They are more likely to engage with brands that offer interactive digital experiences and gamified content. The fear of missing out on trending items creates urgency and impulse buying behavior. Peer validation through likes and comments reinforces purchasing decisions. Brands that successfully navigate the digital landscape and engage with youth culture see rapid growth in this segment. The ability to virally market products through social channels allows for quick scaling of demand. This digital fluency distinguishes young affluent consumers as a dynamic and rapidly expanding force in the luxury market.

COUNTRY LEVEL ANALYSIS

Europe Personal Luxury Goods Market Analysis

Europe captured the leading share of the global personal luxury goods market in 2025 and is expected to maintain its commanding baseline and central position in the personal luxury goods landscape over the next few years due to its deeply rooted heritage of craftsmanship and a continuous influx of tourism. The region is home to the majority of the world’s leading luxury conglomerates, which benefit from established supply chains and skilled artisanal workforces. According to Eurostat, the European Union accounts for approximately 30% of global personal luxury goods consumption, driven by both domestic demand and international tourism. Countries like France and Italy serve as global hubs for fashion and leather goods production, attracting visitors who seek authentic luxury experiences. The strong cultural emphasis on style and quality sustains high per capita spending on luxury items. Government support for creative industries and protection of geographical indications helps preserve brand integrity. The region’s mature retail infrastructure, including prestigious shopping streets and department stores, facilitates high-volume sales. However, economic volatility and regulatory pressures regarding sustainability pose challenges. Despite these factors, Europe remains a benchmark for luxury standards and innovation. The integration of digital technologies in traditional retail models enhances customer engagement. The region’s ability to blend tradition with modernity ensures its continued leadership in the global luxury landscape.

North America Luxury Goods Market Analysis

North America is projected to witness steady development and remain a vital powerhouse for premium retail over the next few years as its vast network of affluent demographics continues to exercise significant purchasing power. The United States is the largest single-country market for luxury goods, driven by a large population of high-net-worth individuals and a robust middle class with aspirational tendencies. As per the US Bureau of Economic Analysis, personal consumption expenditures on recreational goods and vehicles, which include luxury items, have shown steady growth. The region benefits from advanced retail infrastructure and early adoption of e-commerce trends. Major cities like New York and Los Angeles serve as key fashion capitals, hosting influential events and flagship stores. The diversity of the population creates demand for a wide range of luxury categories, from fashion to cosmetics. Marketing strategies often focus on celebrity endorsements and lifestyle branding to appeal to American consumers. The strong dollar attracts international shoppers, boosting duty-free sales. However, competition from domestic premium brands and changing consumer preferences toward experiences challenge traditional luxury players. The region’s focus on innovation and digital integration keeps it at the forefront of market evolution.

Asia Pacific Luxury Goods Market Analysis

The Asia Pacific region is anticipated to expand at a rapid pace and solidify its role as the primary growth engine for global high-end markets over the next few years. China alone accounts for a substantial portion of global luxury consumption, with consumers increasingly purchasing domestically due to improved retail offerings and government policies. According to the National Bureau of Statistics of China, retail sales of consumer goods have rebounded strongly, with luxury categories outperforming broader trends. Japanese consumers remain sophisticated buyers with a preference for high quality and detailed craftsmanship. South Korea drives trends in beauty and fashion, influencing regional preferences through its cultural exports. The region’s young demographic is highly digitally savvy, adopting online luxury shopping rapidly. Tourism recovery post-pandemic has revitalized duty-free sectors in key hubs like Singapore and Hong Kong. Local brands are gaining traction by blending traditional aesthetics with modern designs. Government initiatives to boost domestic consumption support market growth. The sheer scale of the population and increasing urbanization provide a vast addressable market. This region’s rapid evolution and growing influence reshape global luxury strategies.

Latin America Luxury Goods Market Analysis

Latin America is likely to experience gradual growth and strengthen its position as a highly resilient niche market over the next few years. The market is influenced by economic fluctuations and currency volatility, which affect purchasing power and import costs. As per the Economic Commission for Latin America and the Caribbean, economic recovery efforts are gradually improving consumer confidence. Wealthy elites in major cities drive demand for international luxury brands, often purchasing during travel abroad due to limited local availability and high taxes. However, the expansion of local retail networks and e-commerce platforms is making luxury goods more accessible. Brazilian consumers show strong interest in fashion and jewelry, while Mexican buyers prefer accessories and cosmetics. Cultural festivals and social events stimulate seasonal spending. Counterfeit goods remain a challenge, impacting brand integrity. International brands are entering the market through partnerships with local distributors to navigate regulatory complexities. The growing middle class in urban areas offers potential for future expansion. Despite challenges, the region’s passion for style and social presentation sustains a steady demand for luxury items. Strategic pricing and localized marketing are key to success in this diverse market.

Middle East and Africa Luxury Goods Market Analysis

The Middle East and Africa region is poised to unlock substantial potential and capture a more prominent share of the luxury retail space over the coming years. Saudi Arabia and the United Arab Emirates are key markets, with consumers displaying a high propensity for luxury spending on fashion, jewelry, and watches. As per the World Bank, GDP growth in the GCC supports robust consumer expenditure. The culture of gifting and social display drives demand for high-visibility luxury items. Dubai serves as a regional hub for luxury retail, attracting tourists and residents alike. Africa’s market is nascent but growing, with South Africa and Nigeria leading in luxury consumption among affluent populations. Limited local production means reliance on imports, making exchange rates a critical factor. International brands are expanding their presence through flagship stores in major malls. The young population in Africa presents long-term opportunities as incomes rise. Political stability and infrastructure development are crucial for sustained growth. The region’s appreciation for brand prestige and quality ensures continued interest in global luxury houses. Tailored offerings and respectful engagement with local customs are essential for market penetration.

COMPETITIVE LANDSCAPE

The competition in the personal luxury goods market is characterized by intense rivalry among established conglomerates and independent heritage brands vying for consumer attention and loyalty. Major players leverage their scale and resources to dominate distribution channels and secure prime retail locations globally. Innovation in design and marketing serves as a key differentiator, with brands constantly seeking to refresh their image while preserving core identity. Price competition is minimal due to the emphasis on exclusivity and brand value rather than cost leadership. Instead,d companies compete on customer experience,ce offering personalized services and immersive digital interactions. The threat of new entrants is low due to high barriers related to brand building and capital requirements. Substitute products pose limited threats as luxury goods fulfill emotional and status needs beyond functional utility. Supplier power is moder, ate with specialized artisans holding some leverage. Buyer preferences vary, with high-net-worth individuals demanding exceptional service, while aspirational buyers are more price sensitive. This dynamic environment drives continuous adaptation and strategic maneuvering among market participants.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Global Personal Luxury Goods Market include

- LVMH (Moët Hennessy Louis Vuitton)

- Kering SA

- Compagnie Financière Richemont SA

- Prada S.p.A.

- Chanel Limited

- Hermès International S.A.

- Burberry Group plc

- Rolex SA

- Tiffany & Co.

- Valentino S.p.A.

TOP LEADING PLAYERS IN THE MARKET

- LVMH Moët Hennessy Louis Vuitton SE stands as a preeminent conglomerate in the global luxury sector, managing a diverse portfolio of prestigious fashion and leather goods brands. The company leverages its extensive network of artisanal workshops to maintain exceptional quality and exclusivity across its product lines. Recent strategic initiatives include significant investments in sustainable sourcing practices and the expansion of digital retail capabilities to engage younger consumers. LVMH actively acquires niche heritage brands to diversify its offerings and capture emerging market trends. The group emphasizes vertical integration to control supply chains and ensure ethical production standards. By fostering innovation in materials and design, LVMH continues to set industry benchmarks for craftsmanship and brand desirability. Their commitment to cultural patronage and environmental responsibility strengthens brand equity and consumer loyalty worldwide.

- Kering SA operates as a leading global luxury group with a strong focus on sustainable development and creative excellence in fashion and leather goods. The company manages iconic houses such as Gucci and Saint Laurent, driving growth through bold artistic directions and digital transformation. Kering has recently intensified its efforts in circular economy initiatives, launching programs for product repair and resale to appeal to environmentally conscious shoppers. The group invests heavily in technology to enhance customer personalization and omnichannel experiences. Strategic partnerships with innovative startups allow Kering to integrate cutting-edge solutions into its operations. By prioritizing transparency and social impact, Kering reinforces its reputation as a responsible leader in the luxury industry. These actions ensure long-term resilience and relevance in a rapidly evolving market landscape.

- Compagnie Financière Richemont SA specializes in hard luxury goods, including jewelry, watches, es anwriting instrumentsts with a portfolio of esteemed maisons. The company focuses on preserving traditional craftsmanship while embracing digital innovation to reach global audiences. Richemont has recently expanded its online distribution networks and enhanced direct-to-consumer capabilities through strategic acquisitions of e-commerce platforms. The group emphasizes sustainability by implementing rigorous standards for the responsible sourcing of precious metals and gemstones. Investments in manufacturing facilities ensure high production capacity and quality control. Richemont also strengthens its position through collaborations with artists and designers to create limited edition collections that drive exclusivity. These efforts maintain the prestige of its brands and attract discerning customers who value heritage and integrity in luxury purchases.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the personal luxury goods market primarily focus on vertical integration to control supply chains and ensure product authenticity. Companies invest heavily in digital transformation to enhance omnichannel experiences and engage younger demographics through social media platforms. Strategic acquisitions of niche brands allow conglomerates to diversify portfolios and capture emerging consumer trends. Sustainability initiatives are central to corporate strategies, with brands adopting circular economy models and ethical sourcing practices. Exclusive partnerships with artists and influencers help maintain brand relevance and create buzz around new collections. Expansion into emerging markets through flagship stores and localized marketing campaigns drives global growth. Personalization services and bespoke offerings strengthen customer loyalty by providing unique and tailored experiences. These strategies collectively enable market leaders to maintain competitive advantage and sustain long-term profitability in the luxury sector.

RECENT HAPPENINGS IN THE MARKET

- In April 2025, Lacoste launched an aggressive push into the lucrative U.S. sportswear market, aiming to double its U.S. sales from $400 million to $800 million. The strategy involved opening new stores, including a flagship on New York's Fifth Avenue, and emphasizing trends in tennis and golf to attract American consumers.

- In February 2025, LVMH, the world's largest luxury conglomerate, invested heavily in sports, securing substantial deals in Formula One, the Paris Olympics and Paralympics, and soccer. This strategy aims to shift the company's focus from products to emotional and experiential services, aligning with the growing consumer interest in luxury experiences.

MARKET SEGMENTATION

This research report on the global personal luxury goods market has been segmented and sub-segmented based on material, product, distribution channel, demographic, and region.

By Product

- Luxury Fashion

- Jewelry & Watches

- Leather Goods

- Fragrances & Cosmetics

- Other Luxury Goods

By Distribution Channel

- Online Retail

- Exclusive Brand Boutiques

- Department Stores

- Luxury Outlet Stores

By Demographic

- Young Affluent Consumers

- High-Net-Worth Individuals (HNWIs)

- Middle-Class Luxury Shoppers

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa