Global Pet Food Processing Market Size, Share, Trends, COVID-19 Impact & Growth Forecast Report, Segmented By Type (Forming Equipment, Baking & Drying Equipment, Cooling Equipment, Mixing & Blending Equipment and Coating Equipment), Form (Wet and Dry), Pet Type (Cats, Dogs and Fish), By Sales Channel (Specialized Pet Shops, Online Stores, Hypermarkets/Supermarkets, and Grocery Stores), And Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa), Industry Analysis from 2025 to 2033

Global Pet Food Processing Market Size

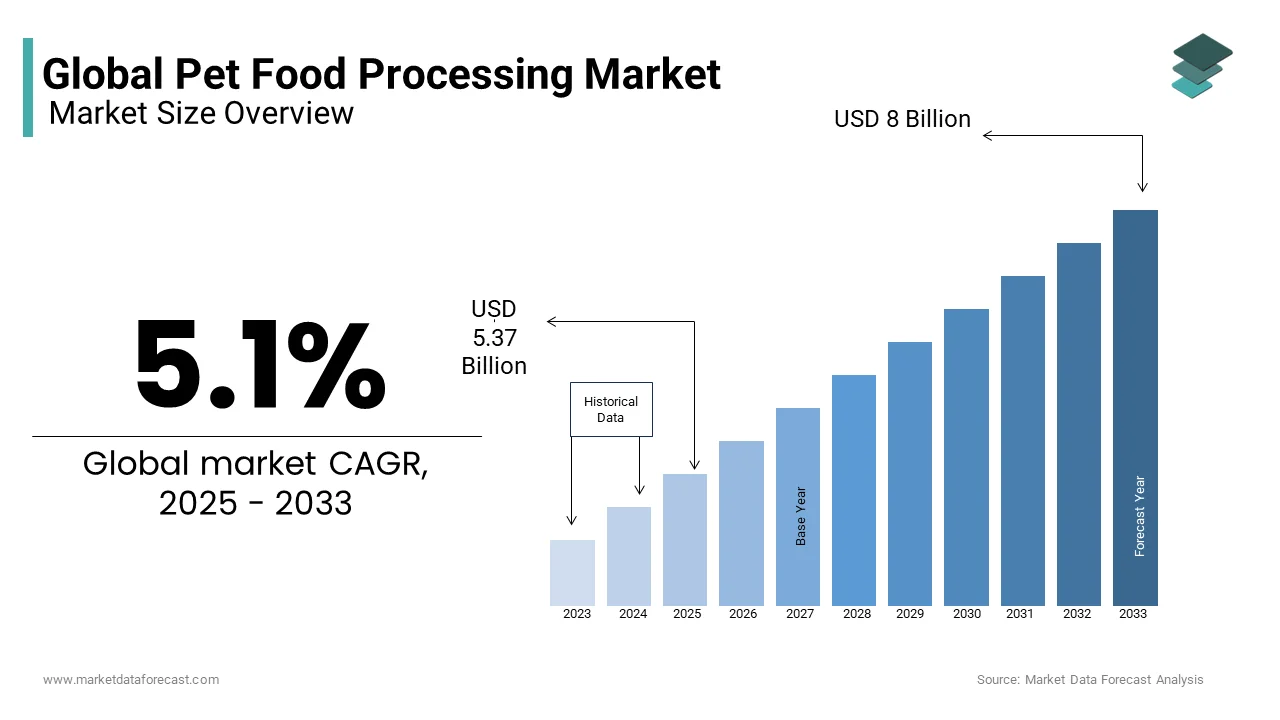

The global pet food processing market was valued at USD 5.11 billion in 2024 and is anticipated to reach USD 5.37 billion in 2025 from USD 8 billion by 2033, growing at a CAGR of 5.1% during the forecast period from 2025 to 2033.

MARKET OVERVIEW

Pet food is a high-grade animal food for consumption between pets, and its quality is suitable for human consumption and traditional food. Pet food processing takes place in all the stages where various machinery and labor are involved in the production of the last product, which is used for the consumption of food.

The rising preference for leading makers to develop innovative products and augment pet adoption trends globally are also anticipated to fuel the demand in this business going forward.

MARKET GROWTH

Consumer trends related to pet food products are increasing, such as the growing preference for high-quality commercial products for pet food, which are promoting the call for pet food processing around the world.

MARKET DRIVERS

With increasing consumer awareness of organic and natural pet food products, manufacturers had to shift their focus from synthetic products to natural products, one of the main factors affecting the global market. As a family partner, the tendency to adopt dogs is expected to increase, driving demand for the products. In particular, pets like dogs are seeing an upward trend in the concept of pet humanization. This has increased the number of people who own dogs and feed premium food. There are factors that are expected to offset the growth of the market during the forecast schedule as interest in product premiumization increases among pet food manufacturers and the population of pets grows in various regions. These aspects are further predicted to accelerate the growth of the global pet food processing market. Unlike most existing pet foods, organic and natural pet foods are used on a large scale. Increased demand for dog food coupled with high traction in the premium pet food sector is expected to lead the pet food market during the forecast period. Dry food is in high demand compared to other products, and it is convenient to keep. This is having a positive impact on urban consumers who are increasingly choosing dry pet food. This type of product is low in protein, fat and carbohydrates, making canned foods more delicious for cats and dogs. Wet/canned pet food is easy to digest, minimizing backyard cleaning activities. The high digestibility provided by wet food is desirable for cats and dogs suffering from the disease and demanding eaters.

The expansion of disposable income has led to an increase in pet adoption trends and increased pet acceptance in the world, which is the most important aspect that is supposed to drive market development. In addition, the introduction of new technologies in the field of pet food also offers development prospects. As interest in nutritious pet food expands, manufacturers focus on putting resources into new ingredients. This is expected to further expand the demand for specific hardware, which will promote the development of the global pet food processing market. The market has increased the demand for pet food supplies, a larger pet population, and increased awareness of pet health and humanized pets. Developing countries like Brazil, Argentina, China, and India have high growth potential in the pet food processing equipment market, offering new development opportunities to market participants.

MARKET RESTRAINTS

Increasing issues related to pet obesity and food recalls by several companies are hampering business growth in the worldwide market. The depreciation of processing equipment for the production of pet food is a key factor that is expected to slow the growth of the market.

Impact of COVID-19 on the Pet Food Processing Market

The limitation in manufacturing activities due to the COVID-19 pandemic is hampering pet food processing production. The current situation is unfavorable in the demand for pet food processing market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2023 |

| Forecast Period | 2025 to 2033 |

| CAGR | 5.1% |

| Segments Covered | By Type, Form, Pet Type, Sales Channel, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Mars Petcare US Inc, TiernahrungDeuerer GmbH, Procter & Gamble Company, Heristo Aktiengesellschaft, Big Heart Pet Brands, Blue Buffalo Co., Ltd, Diamond Pet Foods, WellPet LLC, Nestle Purina PetCare, Hill's Pet Nutrition and Others. |

SEGMENTAL ANALYSIS

By Pet Type Insights

it is estimated that the dog sector will dominate the value-based pet food processing market. Dog food appears to be in increasing demand as the number of dog populations increases throughout the region. As the trend towards the humanization of pets increased, dog owners were encouraged to accept dogs as companions due to their friendliness.

By Type Insights

The forming equipment sector dominated the global pet food processing market in 2019. Pet food processors are shifting their focus towards extrusion-based manufacturing. The introduction of the new extrusion technology and its use in the pet food sector are factors that are expected to drive the market demand for training equipment. The mixing and blending equipment segment is expected to grow at an average annual rate of 4% during the forecast period. This is due to the automation of the processing equipment. The segment growth is also expected to be driven by the introduction of effective integrated and multi-functional processing systems. As concern for pet health increases, the demand for quality products increases, resulting in the demand for special pet food processing machines.

By Form Insights

The production of dry pet food is on the rise, and sales are expected to continue to rise in developing countries like China, Russia, and Poland. The demand for dry pet food products is increasing due to the profitability of dry form, ease of handling, and ease of bulk purchase. Also, as the use of extrusion technology increases, the production of dry pet food remains large. Wet pet food is expected to have the highest annual growth rate of 5.0% between 2020 and 2025. Various types of wet pet food include semi-wet, canned, and sauce treatments. The high water content of this product helps keep pets hydrated and helps improve pet urinary tract function.

By Sales Channel Insights

the global pet food processing market is divided into specialized pet shops, online stores, hypermarkets/supermarkets, and grocery stores. The specialized pet stores accounted for a prominent portion of the worldwide market in the review period, which, however, is predicted to be dominated by online stores in the coming years. This is credited to the increasing digitization across the globe.

REGIONAL ANALYSIS

Regional segmentation consists of past, present, and projected demand for pet food processing in the Middle East and Africa, North America, Asia Pacific, Latin America, and Europe. These regions are further segmented as Canada, Mexico, the United States, France, the United Kingdom, China, Germany, India, Japan, Brazil, Korea, and Argentina.

The North American market is estimated to occupy the majority during the forecast period. The dominance of the region is primarily due to the increasing trend in the humanization of pets, which has greatly increased the pet population, increasing the demand for pet food products worldwide. Additionally, the growing awareness of pet owners has increased the need for manufacturers to meet the highest standards of food safety, driving growth in the North American pet food processing market. The Asia Pacific area is one of the most important and potential markets in this industry. The Asia Pacific region has mature markets like Australia and Japan, and emerging markets like China, India, and Thailand. In addition, Japan is one of the top pet food markets in the Asia Pacific and is expected to dominate during the outlook period, and the pet food market share is expected to reach approximately 46.6% by late 2022. Apartment culture, the trend of nuclear families, and the pet food market dominated Japan. The growing pet ownership in Australia has complemented the growth of the pet food market, making it the second most prominent market in the region. Demand for newer and newer equipment is expected to increase in the future, so it is expected to have a major impact on the equipment industry. Europe is considered the leading market for quality pet food.

KEY MARKET PLAYERS

Mars Petcare US Inc, TiernahrungDeuerer GmbH, Procter & Gamble Company, HeristoAktiengesellschaft, Big Heart Pet Brands, Blue Buffalo Co., Ltd, Diamond Pet Foods, WellPet LLC, Nestle Purina Pet Care, Hill's Pet Nutrition. Some of the market players that are dominate the global pet food processing market.

MARKET SEGMENTATION

This research report on the global pet food processing market is segmented and sub-segmented into the following categories.

By Type

- Forming Equipment

- Baking and drying equipment

- Coating equipment

By Form

- Wet

- Dry

By Pet Type

- Cats

- Dogs

- Fish

By Sales Channel

- Specialized pet shops

- Online stores

- Hypermarkets/Supermarkets

- Grocery Stores

By Region

- North America

- Europe

- Asia-Pacific

- South America

- Middle East & Africa

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com