Global Precision Farming Market Size, Share, Trends, and Growth Forecast Report, Segmented By Offering ( Hardware, Automation, Control), Software (Web-based, Cloud-based Software, and Services), Technology (Guidance System, Variable –rate Technology), Application and Region (North America, Europe, Asia Pacific, Latin America, and Middle East - Africa), Industry Analysis From (2025 to 2033)

Global Precision Farming Market Size

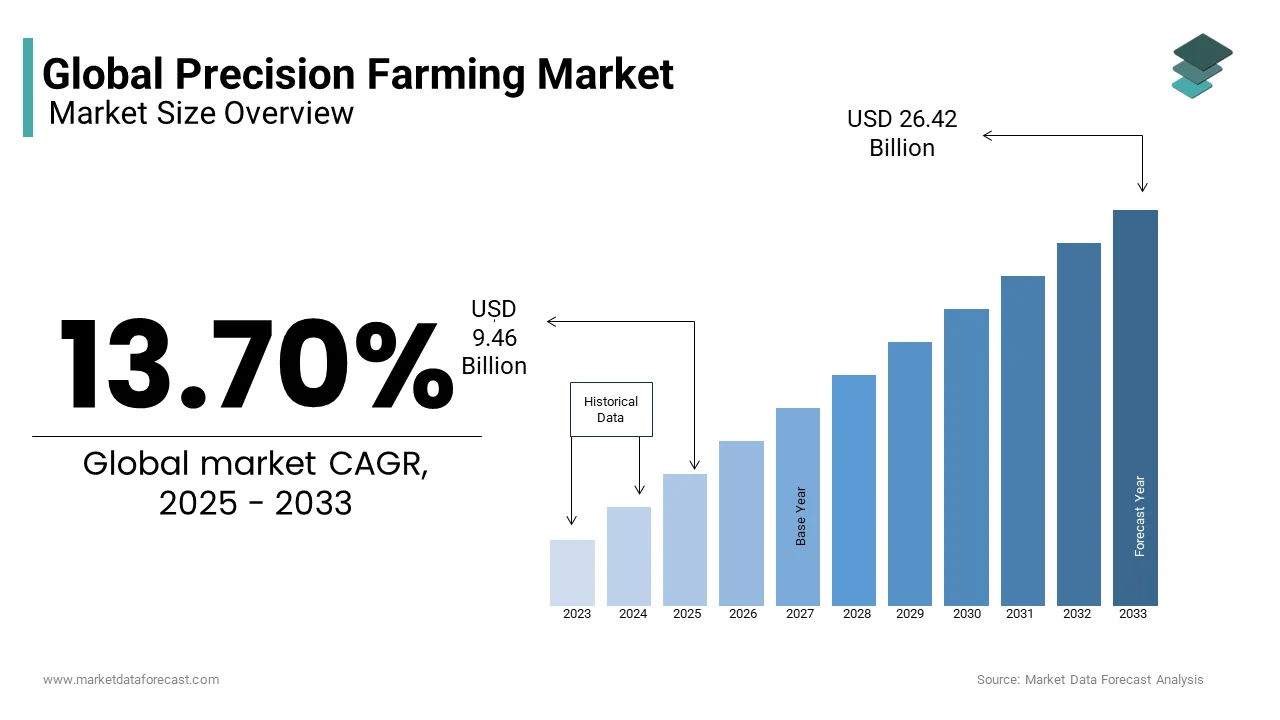

The global precision farming market was valued at USD 8.32 billion in 2024 and is anticipated to reach USD 9.46 billion in 2024 from USD 26.42 billion by 2033, growing at a CAGR of 13.7% during the forecast period from 2025 to 2033.

MARKET DRIVERS

Surge in Global Food Demand

One of the primary drivers of the potash fertilizers market is the escalating global demand for food, fueled by population growth and shifting dietary preferences. By 2050, the world population is projected to surpass 9.7 billion, according to the United Nations, necessitating a 60–70% increase in food production. Potash plays a crucial role in enhancing crop yield and quality, especially for potassium-responsive crops such as fruits, vegetables, sugar beets, and cereals. In 2023, global cereal production rose to 3.01 billion metric tons, as reported by the Food and Agriculture Organization (FAO), directly increasing the need for potassium-based fertilizers. Countries like India and China are major consumers, with India importing over 5 million metric tons of muriate of potash (MOP) annually to support domestic agricultural productivity.

Expansion of Precision Farming Practices

Precision farming techniques are rapidly gaining traction worldwide, significantly boosting the demand for potash fertilizers. These technologies enable farmers to apply fertilizers more efficiently based on soil composition and crop requirements, minimizing waste and maximizing yield. This shift supports targeted use of potash in developed regions like North America and Western Europe, where adoption rates are highest. In the U.S., over 40% of farms now utilize GPS-guided systems for fertilizer application, as stated by the USDA in 2024. Similarly, in Germany, the Federal Ministry of Food and Agriculture reported that precision nutrient management boosted potash efficiency by up to 20% in 2023 by reducing environmental impact while improving productivity.

MARKET RESTRAINTS

Volatility in Raw Material Prices

A significant restraint impacting the potash fertilizers market is the volatility in raw material prices, which affects both production costs and end-user affordability. Potash extraction involves substantial energy inputs, making it sensitive to fluctuations in natural gas and electricity prices. This increase raised operational expenses for potash producers, many of whom rely on energy-intensive mining processes. Additionally, geopolitical disruptions in Eastern Europe have led to inconsistent supply flows of key inputs. For instance, sanctions imposed on Russian and Belarusian potash exports in early 2023 caused short-term supply shocks and price spikes exceeding 15% in some Asian markets, according to ICIS. These price instabilities strain farmers’ budgets, especially in emerging economies where fertilizer subsidies are limited. As a result, inconsistent pricing undermines long-term investment in potash infrastructure and hampers market expansion despite strong underlying demand fundamentals.

Environmental Regulations and Sustainability Concerns

Environmental concerns surrounding potash mining and usage are increasingly shaping regulatory frameworks, which are posing a challenge to market growth. While potash itself is not inherently harmful, the mining process can lead to land degradation, water contamination, and high carbon emissions. Similarly, in Canada, the Saskatchewan government introduced new emission reduction targets requiring potash producers to cut greenhouse gas emissions by 30% by 2030, as outlined in the provincial Climate Strategy. These regulations drive up compliance costs for manufacturers, slowing down project approvals and expansions. Moreover, consumer awareness about sustainable agriculture is growing, leading to a shift toward organic and alternative nutrient sources. These environmental pressures are compelling industry players to invest in greener extraction methods and circular economy models, though such transitions often require time and capital.

MARKET OPPORTUNITIES

Rise in Specialty Potash Products

A promising opportunity within the potash fertilizers market lies in the growing demand for specialty potash products tailored for high-value crops and precision agriculture applications. Unlike conventional muriate of potash (MOP), specialty forms such as sulfate of potash (SOP) and potassium nitrate offer enhanced compatibility with chloride-sensitive crops like fruits, vegetables, and nuts. In 2023, SOP accounted for nearly 15% of total potash consumption, which is primarily driven by horticultural sectors in the U.S., Australia, and Latin America. For example, California’s almond growers applied SOP on over 80% of orchards, citing improved yield and resistance to disease, as reported by the Almond Board of California. Additionally, companies like K+S Potash Canada and Compass Minerals are expanding SOP production capacity to meet this niche demand. With rising investments in controlled-release fertilizers and hydroponic farming, the market for specialized potash variants is poised for sustained growth, offering a strategic avenue for differentiation among producers.

Expansion into Emerging Agricultural Markets

Emerging agricultural economies present a substantial growth opportunity for the potash fertilizers market, particularly in Sub-Saharan Africa and Southeast Asia. These regions currently exhibit low potash application rates but are experiencing rapid agricultural intensification due to population growth and food security concerns. In Indonesia, the Ministry of Agriculture reported a 22% increase in potash imports in 2023, which is driven by rising palm oil and rice production. These developments signal a growing awareness of soil nutrient management and government-backed initiatives aimed at boosting fertilizer accessibility. Companies such as OCP Group and Uralkali are actively engaging in partnerships and distribution agreements across these regions to capitalize on the evolving demand landscape, positioning emerging markets as a key frontier for future market expansion.

MARKET CHALLENGES

Geopolitical Instability in Key Supply Regions

Geopolitical instability in major potash-producing countries presents a persistent challenge to the stability and predictability of the global potash fertilizers market. According to the International Fertilizer Association, these sanctions disrupted global potash supply chains, causing short-term price increases of up to 20% in parts of Asia and Latin America during mid-2023. Although alternative suppliers such as Canada and Brazil ramped up production, they could not fully offset the disruption, leading to supply shortages in several developing nations reliant on affordable imports. Furthermore, ongoing tensions in Eastern Europe continue to create uncertainty around export policies and logistics.

Declining Farmer Profit Margins in Developing Economies

Declining profit margins among farmers in developing economies pose a significant challenge to the consistent uptake of potash fertilizers. In countries like India, Nigeria, and Bangladesh, where smallholder farming dominates, fluctuating crop prices and rising input costs are squeezing farm incomes. According to the Food and Agriculture Organization (FAO), real farm income in India declined by nearly 8% in 2023, despite bumper harvests in certain regions, due to falling prices for staples such as wheat and rice. This financial pressure leads many farmers to reduce or delay fertilizer purchases for higher-cost nutrients like potash. Data from the Indian Ministry of Agriculture shows that potash consumption dropped by 6% in FY 2023 compared to FY 2022, despite government subsidy programs. Similar trends were observed in West Africa, where erratic rainfall and inflationary pressures reduced disposable income for agricultural inputs. The International Fund for Agricultural Development (IFAD) noted that over 60% of smallholder farmers in Sub-Saharan Africa lacked access to credit in 2023, which is limiting their ability to invest in soil-enhancing nutrients.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 13.7% |

| Segments Covered | By Offering, Software, Technology, Applications, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Raven Industries, Deere & Company, AGCO Corporation, Trimble Navigation Ltd, Monsanto Company, DuPont, Agjunction, Inc, Precision Planting, Inc, SST Development Group, Dickey-John Corporation, and Others. |

SEGMENTAL ANALYSIS

By Offering Insights

The Hardware segment dominated the global precision farming market by accounting for 42.3% of the market share in 2024. According to the U.S. Department of Agriculture (USDA), over 65% of large-scale U.S. farms now use GPS-based auto-steer tractor systems, which are reducing overlap during planting and spraying by up to 10%, thereby enhancing efficiency and lowering input costs. In Europe, Germany's Federal Ministry of Food and Agriculture noted that drone usage for crop monitoring increased by 25% in 2023, with over 10,000 hectares surveyed weekly using multispectral imaging. Meanwhile, in the Asia-Pacific region, China’s Ministry of Agriculture invested USD 2 billion in drone-assisted pesticide application programs by aiming to reduce chemical runoff and improve application accuracy.

The Control segment is swiftly emerging with a CAGR of 15.8% from 2025 to 2033, owing to the driven by the increasing integration of automated control systems into farm machinery, irrigation setups, and climate management tools by enabling real-time adjustments based on sensor inputs and environmental conditions.

One key factor fueling this expansion is the adoption of smart irrigation controllers, which optimize water usage based on soil moisture levels and weather forecasts. According to the International Water Management Institute (IWMI), smart irrigation adoption in India increased by 18% in 2024, with farmers reporting up to 30% reductions in water consumption without yield loss.

By Software Insights

The Cloud-Based Software segment was the largest in the precision farming software market by capturing 38.3% ofthe market share in 2024 due to the scalability, accessibility, and real-time data processing capabilities offered by cloud platforms, which are increasingly being adopted by both large agribusinesses and smallholder farmers. According to the U.S. Department of Agriculture (USDA), over 50% of American farms with more than 500 acres now use cloud-connected farm management platforms, such as those provided by John Deere and Climate FieldView, to track field operations, manage inputs, and analyze yield trends. In India, the Ministry of Electronics and Information Technology reported that cloud-based advisory services reached over 8 million farmers in FY 2024 by leveraging satellite imagery and AI models to provide localized crop recommendations.

The services segment is expected to register a CAGR of 17.2% during 2025 – 2033. The rapid growth of the segment is fueled by the rising demand for agricultural consulting, data interpretation, training, and managed service offerings among small and medium-sized farms that lack in-house technical expertise. The expansion of agronomic advisory services powered by AI and remote sensing technologies is also driving the growth of the segment. In India, the National Bank for Agriculture and Rural Development (NABARD) reported that agritech startups offering precision farming-as-a-service reached over 5 million farmers in FY 2024, which is delivering tailored recommendations via mobile apps and SMS alerts. Similarly, in Sub-Saharan Africa, Hello Tractor, a Nigerian agtech firm, launched a subscription-based farm planning service by integrating GPS tracking and yield prediction models to support tractor-sharing cooperatives.

By Technology Insights

The Guidance System segment led the precision farming technology market by holding 35.4% of the total share in 2024 with the widespread adoption of GPS-based steering systems in tractors, planters, and harvesters, which significantly enhance field efficiency, reduce overlaps, and minimize input wastage.

According to the U.S. Department of Agriculture (USDA), over 70% of U.S. corn and soybean farms utilized GPS auto-steer systems in 2024, which is leading to a 10–15% reduction in fuel and chemical usage. These developments illustrate how guidance systems have become foundational to modern mechanized farming, driving both economic and environmental efficiencies across global croplands.

The Remote Sensing segment is likely to register a CAGR of 16.5% from 2025 to 2033. This surge is driven by the increasing deployment of satellite imaging, drone-based multispectral sensors, and ground-based monitoring devices, which enable real-time crop health assessments and resource optimization. One of the primary factors behind this growth is the integration of remote sensing with AI-driven analytics, allowing farmers to detect stress indicators, predict yields, and adjust inputs accordingly. According to the European Space Agency (ESA), Copernicus Sentinel satellite data was accessed by over 2 million farmers across the EU in 2024 by supporting precision irrigation and nitrogen management decisions. In India, the Indian Space Research Organisation (ISRO) launched a mobile app called "CropAssure", which uses satellite NDVI maps to assess crop performance, reaching over 3 million farmers by mid-2024.

By Application Insights

The Yield Monitoring segment accounted in holding 28.7% of the precision farming market share in 2024, with the increasing need for accurate yield data to inform input optimization, financial forecasting, and long-term land management strategies.

According to the U.S. Department of Agriculture (USDA), over 80% of large-scale corn and wheat farms in the U.S. now utilize combine-mounted yield monitors, generating detailed field maps that help identify underperforming zones. Meanwhile, in Brazil, Embrapa launched an AI-enhanced yield prediction model for soybeans by integrating real-time satellite data and historical performance metrics to assist growers in risk assessment and contract pricing.

The Weather Tracking & Forecasting segment is anticipated to register a CAGR of 18.1% during the forecast period. This rapid expansion is driven by the rising unpredictability of climatic conditions and the urgent need for adaptive farm management strategies. According to the World Meteorological Organization (WMO), global extreme weather events increased by 35% in 2023 compared to the previous decade, which is prompting farmers to seek real-time weather insights to protect crops from heatwaves, droughts, and unseasonal rainfall.

COUNTRY ANALYSIS

Top Leading Countries In The Market

North America Precision Farming Market Analysis

North America outperformed other regions in the global precision farming market with 34.4% of share in 2024,w ith the widespread adoption of advanced agricultural technologies in the U.S. and Canada. The region is characterized by a high degree of mechanization, strong agri-tech investment, and early integration of AI, IoT, and satellite-based farm management tools. According to the U.S. Department of Agriculture (USDA), over 75% of large-scale U.S. farms now use GPS auto-steer systems to improve planting efficiency and reduce input waste.

Europe Precision Farming Market Analysis

Europe was positioned second by holding 26.4% of the global precision farming market in 2024, with Germany, France, and the Netherlands leading adoption due to strong policy backing and emphasis on sustainable agriculture. The European Union’s Common Agricultural Policy (CAP) mandates data-driven farm management practices, encouraging widespread deployment of precision tools.

According to the German Federal Ministry of Food and Agriculture, over 40% of arable land in Germany uses variable rate technology (VRT), optimizing fertilizer and pesticide application based on soil-specific needs. In France, INRAE (French National Research Institute for Agriculture, Food and Environment) found that drone-based crop monitoring increased by 22% in 2024, particularly among vineyards and cereal producers.

Asia Pacific Precision Farming Market Analysis

Asia-Pacific is the fastest-growing region in the precision farming market, with rapid expansion driven by India, China, and Japan, where government-backed digital agriculture programs are accelerating technology uptake. The region is witnessing a shift toward data-driven farm management due to increasing labor shortages, rising input costs, and the need for resource conservation.

According to the Indian Ministry of Electronics and Information Technology, the "Digital Agriculture Mission" achieved coverage of over 10 million farmers by FY 2024 by delivering mobile-based advisory services powered by AI and remote sensing. In China, the Ministry of Agriculture and Rural Affairs reported that over 120,000 agricultural drones were deployed nationwide,y covering more than 1 billion mu (66.7 million hectares) of farmland for precision spraying and monitoring.

Latin America Precision Farming Market Analysis

Latin America is expected to have steady growth opportunities in the coming years. The region is increasingly adopting GPS-guided tractors, drone-based scouting, and cloud-connected farm management software to optimize yields and reduce environmental impact. According to Embrapa, Brazil’s national agricultural research agency, over 4 million hectares of soybean fields used variable rate application (VRA) technology in 2024 by improving nutrient efficiency and lowering input costs. Chile’s fruit export sector is also embracing precision irrigation controllers, with AgroSuper reporting a 25% reduction in water usage across avocado orchards using smart drip systems. Meanwhile, in Mexico, the National Institute for Forestry, Agricultural and Livestock Research (INIFAP) expanded drone-assisted pest detection programs in corn-growing regions by enhancing early warning capabilities.

Middle East And Africa Precision Farming Market Analysis

The Middle East and Africa precision farming market growth is driven by Egypt, South Africa, Kenya, and Israel, where water scarcity, food security concerns, and urban agriculture initiatives are prompting investment in digital solutions. According to Egypt’s Ministry of Agriculture, smart irrigation systems were adopted on over 500,000 feddans (approximately 530,000 acres) in 2024, supported by government subsidies aimed at reducing freshwater consumption.

COMPETITIVE LANDSCAPE

- The global precision farming market is highly dynamic and increasingly competitive, characterized by rapid technological advancements, strong participation from multinational agribusinesses, and rising influence from agritech startups. Established players like John Deere, Trimble, Ag Leader Technology, CNH Industrial, and BASF Digital Farming dominate due to their extensive R&D investments, integrated hardware-software ecosystems, and robust distribution networks. However, they face growing competition from AI-focused startups, drone manufacturers, and cloud-based agronomy service providers in emerging markets where affordability and localization play crucial roles in adoption.

- One of the defining aspects of this competition is the race to offer end-to-end digital farming solutions that seamlessly integrate field data, machine automation, predictive analytics, and supply chain insights. While large corporations focus on building comprehensive platforms through acquisitions and partnerships, smaller firms are disrupting traditional models with low-cost, modular, and open-access applications tailored for smallholder farmers. Additionally, government-backed digital agriculture initiatives in countries like India, China, and Kenya are reshaping demand patterns, creating new entry points for both domestic and international players.

- Regulatory developments, data privacy concerns, and interoperability standards are also shaping the competitive landscape, compelling firms to align with evolving policy frameworks. As the market matures, success will depend on innovation speed, adaptability to regional needs, and the ability to deliver measurable ROI to farmers across different scales of operation.

KEY MARKET PLAYERS

Some of the major players in the Precision Farming market are

- Raven Industries

- John Deere

- Ag Leader Technology

- Deere & Company

- AGCO Corporation

- Trimble Navigation Ltd

- Monsanto Company

- Dupont

- Agjunction, Inc

- Precision Planting, Inc

- SST Development Group

- Dickey-John Corporation.

Top Leading Countries In The Market

- John Deere, a U.S.-based agricultural machinery giant, is a leading force in the precision farming market, offering an integrated suite of GPS-guided tractors, autonomous equipment, and digital farm management platforms. The company’s Operations Center, powered by AI and satellite data, enables farmers to monitor field performance, optimize input usage, and streamline planting decisions. John Deere has also invested heavily in autonomous tractor technology, launching its first fully self-driving model in 2023.

- Trimble Inc. plays a pivotal role in advancing precision farming through its cutting-edge positioning technologies, software solutions, and hardware integrations tailored for modern agricultural operations. The company specializes in GNSS-guided steering systems, yield monitoring tools, and irrigation control devices, which are widely adopted across North and South America, Europe, and Athe sia-Pacific. Trimble’s Connected Farm platform allows real-time data synchronization between farm equipment and management dashboards, improving operational efficiency and decision-making accuracy. In 2024, Trimble expanded its partnership network with agritech startups to enhance AI-driven crop analysis and drone integration.

- Ag Leader Technology, a subsidiary of CNH Industrial, is a major contributor to the global precision farming ecosystem, particularly in mid-sized and family-owned farms across the U.S., Canada, and emerging markets. Known for its affordable yet high-performance guidance systems, soil mapping tools, and variable rate application (VRA) controllers, Ag Leader provides accessible digital farming solutions that bridge the gap between conventional and advanced agri-tech practices. The company's SMS Advanced software suite enables growers to manage field data, prescriptions, and yield analysis from a single interface. In 2024, Ag Leader launched new edge-computing modules for real-time in-field data processing by enhancing responsiveness without relying on constant internet connectivity.

Top Strategies Used by Key Market Participants in the Market

Strategic Acquisitions and Partnerships to Expand Technological Capabilities

Key players are leveraging strategic acquisitions and partnerships to enhance their precision farming portfolios and accelerate innovation. For instance, John Deere acquired Blue River Technology in 2022, strengthening its AI-based crop scouting capabilities. Similarly, Trimble partnered with drone analytics firm Sentera in early 2024, integrating aerial imaging into its farm management platform. These moves allow companies to consolidate expertise, expand product offerings, and improve interoperability across agricultural ecosystems.

Investment in Research and Development for Next-Generation Solutions

Major market participants are prioritizing R&D to develop advanced tools such as autonomous equipment, AI-driven analytics, and IoT-enabled sensors. In 2024, Ag Leader Technology launched edge-computing modules that enable real-time data processing directly on-farm, reducing dependency on internet connectivity. Meanwhile, Deere expanded its autonomous tractor testing programs across U.S. grain farms, aiming to commercialize scalable self-driving solutions.

Expansion into Emerging Markets Through Localized Digital Platforms

To capture growth opportunities in developing regions, key players are launching tailored digital platforms that cater to smallholder farmers and regional agronomic conditions. In mid-2024, Trimble introduced an affordable mobile-based guidance app in India and Brazil, targeting cost-sensitive growers. Similarly, John Deere collaborated with Indian agritech startups to integrate local language interfaces and SMS-based advisory services into its Operations Center by improving accessibility. These localized strategies help global firms penetrate new markets while fostering trust and adoption among diverse farming communities.

RECENT MARKET NEWS

- In February 2024, John Deere announced the launch of its next-generation autonomous tractor equipped with AI-based obstacle detection and adaptive path planning, following successful field trials across U.S. corn and soybean farms.

- In April 2024, Trimble entered into a strategic partnership with Sentera, a leading provider of drone-based agricultural analytics, integrating high-resolution aerial imagery into its Connected Farm platform. This collaboration enabled farmers to access real-time crop health assessments and variable rate application recommendations, significantly improving decision-making accuracy and expanding Trimble’s reach in the remote sensing segment.

- In June 2024, Ag Leader Technology released a new line of edge-computing modules designed to process field data locally without requiring constant cloud connectivity, catering specifically to rural farms with limited internet access. This innovation improved operational efficiency and responsiveness, making precision farming more accessible to small and mid-sized growers across North and South America.

- In August 2024, BASF Digital Farming expanded its Xarvio Scouting app to over 200,000 users globally, introducing enhanced weed and disease identification features powered by deep learning algorithms. The company also launched a subscription-based yield prediction module, further fuelling its presence in AI-driven agronomy services and boosting user engagement in Europe and Asia-Pacific.

- In October 2024, CNH Industrial, parent company of Case IH and New Holland Agriculture, unveiled a new generation of ISOBUS-compatible precision planting systems, compatible with third-party controllers and enabling seamless integration across brands. This move strengthened CNH’s position in the interoperability-driven precision farming market by appealing to farmers seeking flexible and cross-platform digital solutions.

MARKET SEGMENTATION

This research report on the global precision farming market is segmented and sub-segmented into the following categories.

By Offering

- Hardware

- Automation

- Control

By Software

- Web-Based

- Cloud-based software

- Services

By Technology

- Guidance system

- Variable-rate technology

- Remote Sensing

By Application

- Yield Monitoring

- Field Mapping

- Crop Scouting,

- Weather Tracking & Forecasting

- Irrigation Management

- Inventory Management

- Farm Labor Management

- Financial Management

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is the precision farming market?

The precision farming market includes technologies and solutions—such as GPS guidance, IoT sensors, drones, robotics, and data analytics—that help farmers optimize field-level inputs, improve crop yields, and reduce waste through targeted management.

Why is precision farming important in agriculture?

Precision farming enables data-driven decisions, resource-efficient input use (water, fertilizer, pesticides), reduced operational costs, improved yields, and environmental sustainability by matching inputs to field variability.

What technologies are used in precision farming?

Key technologies include GPS/RTK guidance systems, soil and crop sensors, satellite and drone imaging, farm management software, autonomous tractors, IoT platforms, and AI/ML analytics.

What drives growth in the precision farming market?

Growth is driven by rising food demand, labor shortages, environmental concerns, government support for smart agriculture, falling sensor costs, and adoption of digital farming technologies.

Which farming operations benefit most from precision farming?

Precision farming helps with variable rate fertilization, automated irrigation, planting and seeding optimization, pest and disease detection, yield mapping, and field monitoring.

How do drones influence precision agriculture?

Drones provide high-resolution aerial imaging, crop health assessment, real-time field data, and pest/stress detection, enabling quicker and more precise interventions.

How do soil sensors support precision farming?

Soil sensors monitor moisture, temperature, pH, and nutrient levels in real time, allowing site-specific soil management and optimized irrigation/nutrient strategies.

What role does data analytics play in precision farming?

Data analytics processes large datasets to forecast crop performance, optimize inputs, track patterns over time, and support predictive decision-making for improved farm outcomes.

What are the benefits of precision irrigation?

Precision irrigation reduces water use, prevents over-watering, improves crop health, lowers energy costs, and enhances water-use efficiency while maintaining yield quality.

What challenges does the precision farming market face?

Challenges include high technology costs, data integration complexity, lack of technical skills among farmers, connectivity gaps in rural areas, and concerns about data privacy/security.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com