Global Refrigerants Market Size, Share, Trends & Growth Forecast Report By Type (CFCs, HCFCs, HFCs, Inorganic Refrigerants), Application, and Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Industry Analysis From 2025 to 2033

Global Refrigerants Market Size

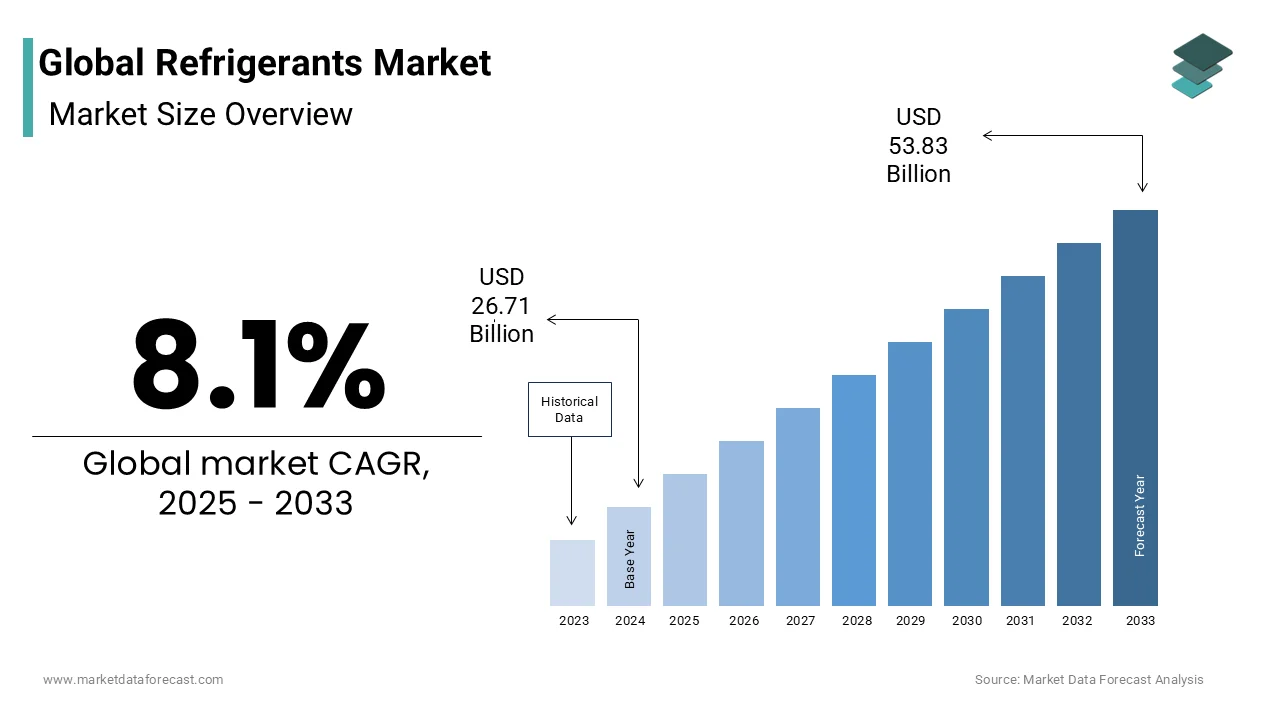

The global refrigerants market size was valued at USD 26.71 billion in 2024. The global market is estimated to be growing at a CAGR of 8.1% from 2025 to 2033 and worth USD 53.83 billion by 2033, from USD 28.87 billion in 2025.

Refrigerants are thermodynamic working fluids engineered to absorb and reject heat through phase transitions within vapor-compression or absorption cycles, enabling precise environmental control in cooling, freezing, and climate systems. Their molecular architecture, spanning chlorofluorocarbons, hydrofluorocarbons, hydrofluoroolefins, and natural substances like ammonia or CO₂, dictates efficiency, safety, and environmental impact. The global stationary air conditioning and commercial refrigeration units rely on synthetic refrigerants, with HFCs alone servicing large number of cooling devices worldwide.

MARKET DRIVERS

Urbanization and Heat Waves Drive Refrigerant Demand

The accelerating global urbanization and rising thermal stress, which intensifies demand for space cooling and cold-chain infrastructure that drives the growth of the refrigerants market. According to the study, 2023 was the hottest year on record, with many days exceeding 1.5°C above pre-industrial levels, triggering unprecedented air conditioner adoption. As per research, rapid growth in air conditioning demand across India, China, and Southeast Asia is driving a shift toward refrigerants that balance efficiency with environmental responsibility. Rising urban temperatures in these regions are increasing the need for cooling solutions that perform under extreme heat while meeting stricter climate regulations.

Global Climate Policies Promote Low-GWP Refrigerants

International climate agreements are increasingly shaping the direction of industrial chemical usage, and is propelling the expansion of the refrigerants market. Many countries are now working to phase down substances with high global warming potential in line with global environmental commitments. According to study findings, this coordinated effort encourages the adoption of more sustainable alternatives and supports long-term transitions toward cleaner technologies across both developed and developing economies. As per research, regulatory measures in the European Union are strongly influencing the direction of refrigerant innovation worldwide. Stricter phase‑outs of high‑GWP substances are encouraging manufacturers, particularly in the U.S., to expand production of advanced HFO blends that meet new environmental standards.

MARKET RESTRAINTS

Legacy Systems Hinder Adoption of Next-Gen Refrigerants

The persistent technological and infrastructural incompatibility of next-generation refrigerants with legacy HVAC&R systems, which is creating costly retrofitting barriers, restricts the growth of the refrigerants market. Heating, and Refrigeration Institute, a portion of existing commercial refrigeration units in North America still operate on R-404A or R-22, neither compatible with lower-pressure HFOs or flammable A2L refrigerants without compressor and lubricant overhaul. According to research, the transition to newer refrigerants presents significant economic and technical challenges for many market participants. In the U.S., smaller operators face high costs when upgrading existing systems to meet environmental standards, creating barriers to rapid compliance. As per study, developing economies encounter additional hurdles due to limited technical expertise in handling advanced refrigerant classes.

Raw Material Supply Fragility Restricts Market Growth

The supply chain fragility of important raw materials required to synthesize low-GWP refrigerants, particularly fluorochemical feedstocks, which hampers the expansion of the refrigerants market. As per the study, China controls a portion of global fluorspar production, the primary source of hydrofluoric acid essential for HFO manufacturing, and imposed export restrictions on high-purity grades in 2023, triggering a price surge. As per research, supply chain limitations and trade policies are influencing the availability and pricing of next‑generation refrigerants across major markets. European producers continue to face material barriers that hinder consistent production, even as demand accelerates. According to study, U.S. trade measures have further complicated the landscape by driving price fluctuations for certain refrigerant types.

MARKET OPPORTUNITIES

Ultra-Low-GWP Blends Offer Minimal Retrofitting Solutions

The rapid commercialization of ultra-low-GWP hydrofluoroolefins and blends, engineered for direct replacement in existing systems with minimal retrofitting, offers new opportunities for the expansion of the refrigerants market. According to research, the global refrigerant landscape is rapidly evolving toward formulations that combine climate responsibility with energy efficiency. The U.S. and other major economies are approving new low‑GWP blends that deliver comparable performance to traditional options while aligning with environmental targets.

Natural Refrigerants Gain Traction in Industrial Use

The resurgence of natural refrigerants, such as ammonia, CO₂, and hydrocarbons, in industrial and commercial applications, driven by zero-GWP mandates and efficiency breakthroughs, gives further opportunities for the growth of the refrigerants market. As per research, natural refrigerants are steadily transitioning from niche applications to mainstream climate solutions across multiple regions. Europe is advancing the use of CO₂ systems in commercial refrigeration, while India continues to expand uptake of hydrocarbon‑based air conditioning aligned with national safety standards. According to study, industrial facilities are also adopting ammonia systems for their superior energy performance and environmental benefits.

MARKET CHALLENGES

Shortage of Certified Technicians Limits Refrigerant Use

The global shortage of certified technicians trained to handle flammable A2L and high-pressure CO₂ refrigerants is limiting the growth of the refrigerants market. As per the U.S. Bureau of Labor Statistics, only 14% of HVAC technicians in 2023 held certification for handling mildly flammable refrigerants, despite their mandated adoption in new equipment. In Southeast Asia, the ASEAN Centre for Energy confirmed that less than 5% of service personnel are trained in CO₂ system maintenance, risking improper charging and efficiency loss. Hence, regulatory deadlines will collide with operational reality because of the lack of synchronized workforce development, which triggers compliance failures and safety incidents.

Fragmented Safety Standards Slow Global Market Rollout

The absence of globally harmonized safety standards for next-generation refrigerants A2L-class mildly flammable fluids is creating fragmentation and design paralysis, which also slows down the rise of the refrigerants market. According to research, varying regulatory standards for refrigerant charge sizes are influencing product design and market rollout across different regions. Manufacturers are often required to develop localized models to meet country‑specific safety and performance requirements, which adds complexity to global deployment strategies.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 8.1% |

| Segments Covered | By Type, Application and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | Honeywell International Inc., Gujarat Fluorochemicals Limited, SRF Limited, Daikin Industries, Ltd., Asahi Glass Corporation, The Chemours Company, Sinochem Group, Airgas Refrigerants Inc., Linde Group and Mexichem |

SEGMENT ANALYSIS

By Type Insights

The hydrofluorocarbons (HFCs) segment dominated the refrigerants market by accounting for 63.1% of share in 2024 with the transitional necessity, as HCFCs like R-22 are phased out under the Montreal Protocol, HFCs such as R-134a, R-410A, and R-404A became the default replacement due to non-ozone-depleting properties and compatibility with existing compressor oils and system architectures. As per research, traditional refrigerants like R‑134a and R‑404A have long dominated automotive and commercial cooling applications due to their reliability and established service networks. Also, the U.S. and Latin American markets, in particular, continue to depend on these formulations because of their proven performance across diverse conditions.

The inorganic refrigerants segment is expected to grow with a CAGR of 12.4% from 2025 to 2033. The rapid expansion of the inorganic refrigerants segment is propelled by regulatory mandates and thermodynamic breakthroughs. According to research, regulatory frameworks in Europe are accelerating the adoption of low‑GWP refrigerants, positioning natural options such as CO₂ and propane as the preferred choices for new equipment. The shift reflects both policy pressure and growing recognition of their long‑term environmental and performance benefits.

By Application Insights

The air conditioners segment was the largest segment and held 49% share in 2024. The dominance of the air conditioning segment is driven by both climatic shifts and demographic trends, making its growth trajectory largely inevitable. Prolonged periods of high temperatures in densely populated regions are fueling widespread adoption of cooling systems as a necessity rather than a luxury. According to study, markets such as India and China remain heavily reliant on established refrigerant technologies, while rising urban heat intensifies demand across Southeast Asia.

The chillers segment is expected to exhibit a noteworthy CAGR of 9.8% during the forecast period. The growth of the chillers segment is fueled by data center and industrial process cooling demand, global data center energy consumption, which relies heavily on precision chillers, grew in 2023, as per study. According to research, temperature control has become a core requirement in pharmaceutical and biotech manufacturing, emphasizing the need for highly reliable chiller systems. Also, in the U.S., strict regulatory standards ensure that biologics and other sensitive products are maintained under precisely managed thermal conditions. As per study, Europe is also advancing the transition toward low‑GWP refrigerants in industrial chillers to align with evolving environmental policies.

REGIONAL ANALYSIS

Asia Pacific Market Analysis

Asia Pacific outperformed other regions in the global refrigerants market and accounted for 38.1% of share in 2024. The domination of the Asia Pacific in the global market is propelled by thermal stress and manufacturing scale. China alone produced millions of room air conditioners in 2023, according to the study, with a portion transitioning to R-32 under national efficiency standards. India is advancing the use of hydrocarbon‑based systems to promote zero‑GWP solutions in residential applications, while Japan continues to expand adoption of next‑generation refrigerants aligned with international climate goals. According to study, Southeast Asia’s rapidly growing cooling demand underscores the need for scalable and low‑impact solutions that balance affordability and efficiency. The region’s collective progress reflects a coordinated movement shaped by regulation, manufacturing, and climatic reality.

Europe Market Analysis

Europe refrigerants market held 27.9% of the share in 2024. The growth of the Europe is propelled by the legislative aggression and circular economy integration. The European Union’s F-Gas Regulation banned R-404A in new equipment from January 2024 and mandates a HFC consumption cut by 2030. Germany and France are advancing large‑scale adoption of natural and CO₂‑based technologies, reinforcing the region’s commitment to sustainable cooling practices. As per research, the European Union’s integrated monitoring platforms are transforming how environmental performance is tracked across the entire refrigerant lifecycle.

North America Market Analysis

North America refrigerants market growth is likely to grow with the U.S. Environmental Protection Agency’s SNAP Program, which approved next-generation refrigerant substitutes, more than any other jurisdiction. The U.S. and Canada are advancing policies that limit the use of high‑GWP substances, encouraging faster adoption of sustainable alternatives like R‑454B, R‑32, and CO₂ systems. According to study, modernization of cooling infrastructure across commercial and industrial facilities remains central to achieving these goals.

Latin America Market Analysis

Latin America is refrigerants market growth is likely to grow with the regulatory delay but accelerating thermal urgency. Brazil accounts for a portion of regional demand, as per research, with R-410A still dominating a share of new AC installations. However, change is accelerating. Chile has strengthened its environmental framework to support low‑GWP equipment imports, while Mexico is witnessing strong private‑sector adoption of CO₂‑based systems. As per study, rising urban temperatures across the region are expanding residential cooling demand, even in areas without formal phase‑down mandates.

Middle East and Africa Market Analysis

The Middle East and Africa region is predicted to expand in the global refrigerants market over the forecast period due to the extreme climates and infrastructural disparity. Saudi Arabia’s Vision 2030 allocated funds to modernize district cooling infrastructure, as per the study, mandating low-GWP fluids in all new chiller plants. South Africa leads in natural refrigerant adoption, a portion of new industrial refrigeration systems installed in 2023 used ammonia, according to the study. Nigeria’s cold chain continues to rely on older refrigerants due to cost constraints and limited technical expertise, while the UAE is advancing cutting‑edge tracking technologies to improve refrigerant management.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

Some of the key players dominating the global refrigerants market are

- Honeywell International Inc.

- Gujarat Fluorochemicals Limited

- SRF Limited

- Daikin Industries, Ltd.

- Asahi Glass Corporation

- The Chemours Company

- Sinochem Group

- Airgas Refrigerants Inc.

- Linde Group

- Mexichem

TOP STRATEGIES USED BY KEY MARKET PLAYERS

Leading players prioritize molecular innovation to develop low-GWP, non-flammable, drop-in refrigerants compatible with legacy infrastructure. They vertically integrate production to secure fluorochemical feedstock amid geopolitical volatility. Strategic partnerships with OEMs embed refrigerant selection early in equipment design cycles. Global technician training programs accelerate safe adoption of mildly flammable A2L fluids. Digital platforms track refrigerant lifecycle emissions and reclamation rates to meet ESG mandates. Patent licensing and regulatory lobbying shape global standards. Geographic expansion targets emerging markets with rising cooling demand but lagging phase-down enforcement. Circular economy models, reclaim, repurpose, recycle, transform refrigerants from consumables to managed assets under extended producer responsibility frameworks.

COMPETITION OVERVIEW

Competition in refrigerants is a high-stakes molecular race, but of compliance, compatibility, and climate impact. Players battle to engineer fluids that satisfy conflicting imperatives: zero ozone depletion, ultra-low GWP, non-flammability, energy efficiency, and drop-in retrofit capability. Regulatory timelines, particularly Kigali and F-Gas, dictate market access, turning policy into product roadmaps. Incumbents face disruption from natural refrigerant adopters and chemical startups with novel synthesis pathways. Differentiation pivots on certification velocity, global service networks, and compressor OEM alliances.

TOP PLAYERS IN THE MARKET

- Honeywell is recognized as a major contributor to the development of environmentally responsible refrigerant technologies. The company’s innovations focus on low‑GWP formulations that offer energy efficiency while meeting evolving climate regulations. The partnerships with equipment manufacturers and global training initiatives are helping accelerate the transition toward safer, next‑generation cooling systems. Through sustained research and policy engagement, the company continues to play an influential role in shaping the future of the refrigerant industry worldwide.

- Chemours Company dominates through its Opteon portfolio of HFO-based refrigerants engineered for performance parity with legacy HFCs. Collaborative efforts with government and industry partners are helping to validate performance improvements while maintaining compatibility with existing systems. According to study findings, the company’s approach integrates environmental responsibility into every stage of product development, combining digital tracking tools and advanced chemistry to support transparent and low‑impact cooling solutions during the ongoing refrigerant transition.

- Daikin Industries, Ltd. operates as both refrigerant producer and end-system manufacturer, uniquely integrating fluid chemistry with compressor and heat exchanger design. The company’s strategy emphasizes developing low‑GWP alternatives that maintain system performance while reducing environmental impact. According to study findings, initiatives such as refrigerant recovery and reuse programs highlight a closed‑loop model that supports both regulatory compliance and long‑term sustainability. This integrated approach positions Daikin as a leader in balancing advanced technology with environmental responsibility across the cooling industry.

MARKET SEGMENTATION

This research report on the global refrigerants market is segmented and sub-segmented into the following categories.

By Type

- CFCs

- HCFCs

- HFCs

- Hydrocarbons

- Inorganic Refrigerants

- Mixtures

By Application

- Air Conditioners

- Refrigerators

- Chillers

- Heat Pumps

- Electronics Devices

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What are refrigerants?

Refrigerants are chemical substances used in cooling, air conditioning, and refrigeration systems to absorb and release heat efficiently.

2. What are the main types of refrigerants?

Key types include hydrofluorocarbons (HFCs), hydrofluoroolefins (HFOs), natural refrigerants like ammonia, CO₂, and hydrocarbons, and blended formulations.

3. What factors are driving the growth of the refrigerants market?

Growth is fueled by urbanization, rising global temperatures, demand for air conditioning and cold-chain infrastructure, and stricter environmental regulations.

4. What challenges restrict the refrigerants market?

Challenges include incompatibility with legacy HVAC&R systems, high retrofitting costs, raw material supply fragility, and regulatory compliance complexity.

5. What role do natural refrigerants play in the market?

Natural refrigerants such as CO₂, ammonia, and hydrocarbons are gaining adoption due to zero-GWP mandates, energy efficiency, and environmental benefits.

6. How does regulatory fragmentation affect the refrigerants market?

Varying regional safety standards and charge size requirements force manufacturers to develop localized solutions, slowing global deployment.

7. Which regions are leading the global refrigerants market?

Asia-Pacific, North America, and Europe are major markets due to growing HVAC demand, industrial refrigeration, and adoption of low-GWP alternatives.

8. What is the future outlook for the global refrigerants market?

The market is expected to grow steadily with increasing adoption of low-GWP and natural refrigerants, technological innovations, and alignment with global environmental standards.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com