Global Release Liners Market Size, Share, Trends & Growth Forecast Report - Segmented By Substrate Type (Glassine/Calendered Kraft Paper, Polyolefin Coated Paper, Clay Coated Paper and Others), Application, and Region (North America, Europe, Asia Pacific, Latin America, Middle east and Africa) – Industry Analysis (2026 to 2034)

Market Size, 2025

$118.7 BnMarket Estimate, 2026

$128.78 BnMarket Forecast, 2034

$246.79 BnCAGR, 2026–2034

8.4%Global Release Liners Market Report Summary

The global release liners market was valued at USD 118.72 billion in 2025, is estimated to reach USD 128.78 billion in 2026, and is projected to reach USD 246.79 billion by 2034, growing at a CAGR of 8.47% during the forecast period. Market growth is driven by increasing demand for pressure sensitive labels, rising applications in packaging and logistics, and expanding use in hygiene and industrial products. Release liners play a critical role in protecting adhesive surfaces and enabling efficient application across multiple industries. The growth of e commerce, retail packaging, and labeling requirements is further supporting strong global market expansion.

Key Market Trends

- Rising demand for pressure sensitive labels is driving market growth.

- Increasing applications in packaging and logistics sectors are boosting demand.

- Growing use in hygiene products and industrial applications is supporting market expansion.

- Expansion of e commerce and retail industries is enhancing demand for labeling solutions.

- Technological advancements in liner materials and coatings are improving performance and sustainability.

Segmental Insights

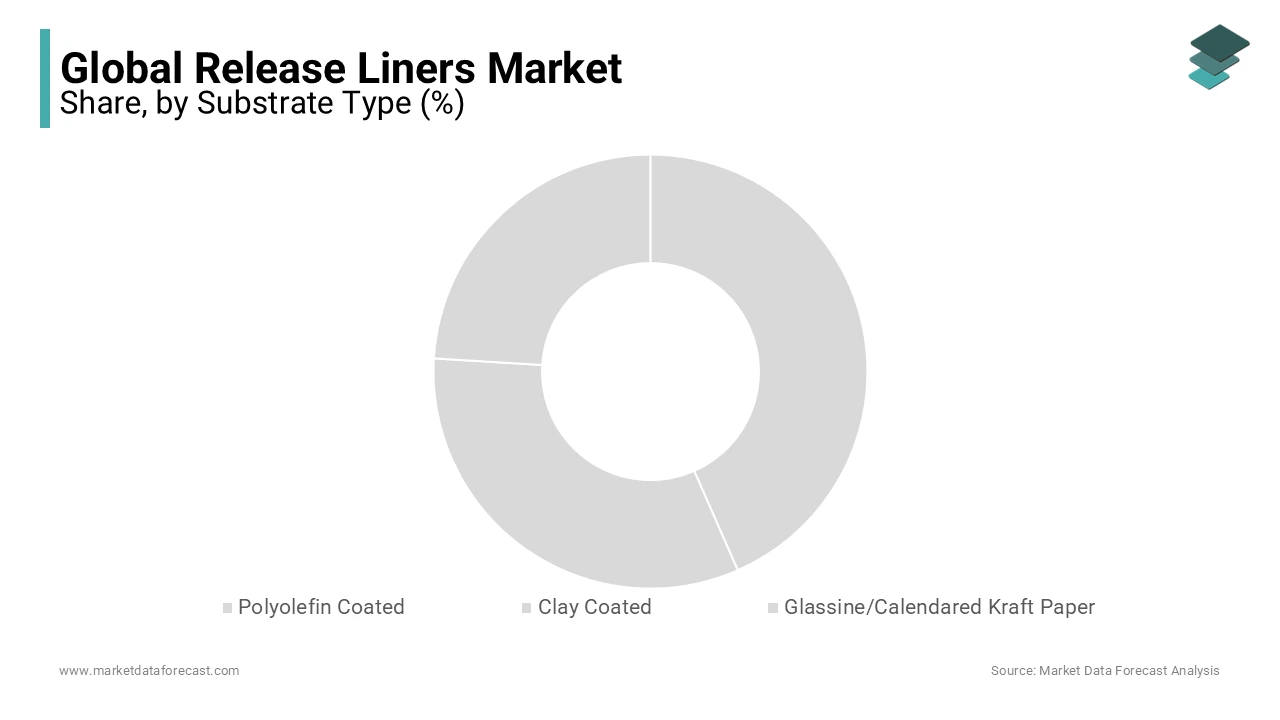

- Based on substrate type, the glassine and calendared kraft paper segment was the largest and held 55.6% of the global release liners market share in 2025. This dominance is attributed to its smooth surface, strength, and suitability for labeling applications.

- Based on application, the labels segment accounted for 46.5% of the global release liners market share in 2025. The segment’s growth is driven by widespread use in packaging, logistics, and retail product identification.

Regional Insights

- The global release liners market is experiencing strong growth across regions, supported by industrial demand and packaging expansion.

- Asia Pacific was the largest contributor, accounting for 40.3% of the global release liners market share in 2025, driven by rapid industrialization, growing packaging industry, and expanding manufacturing base.

Competitive Landscape

The global release liners market is highly competitive, with key players focusing on product innovation, sustainability, and expansion of production capacities to strengthen their market position. Companies are investing in advanced coating technologies, recyclable materials, and supply chain optimization. Prominent players in the global release liners market include 3M Company, Gascogne Laminates, Loparex, Mondi Group, Ahlstrom Munksjö, UPM, Eastman Corporation, Polyplex Corporation Ltd, LINTEC Corporation, Sappi Limited, Rayven Inc, and SilTech.

Global Release Liners Market Size

The global release liners market size was valued at USD 118.72 billion in 2025, and the market size is expected to reach USD 246.79 billion by 2034 from USD 128.78 billion in 2026. The market is growing at a CAGR of 8.47% during the forecast period.

The release liners are substrate materials coated with silicone or other release agents that serve as temporary carriers for pressure sensitive adhesives labels tapes and medical dressings. These liners are components in the manufacturing and application processes of adhesive products ensuring that the adhesive remains protected and functional until the moment of use. As per the Food and Agriculture Organization of the United Nations, global paper production reached approximately 400 million metric tons in recent years providing a substantial base material for paper based release liners. The versatility of these materials allows them to be utilized across diverse sectors including healthcare automotive electronics and packaging. According to the World Health Organization, the global demand for medical devices, which heavily rely on adhesive technologies has increased significantly driven by an aging population and rising chronic disease prevalence. This demographic shift necessitates robust and sterile adhesive solutions for wound care and transdermal drug delivery systems. Furthermore, the expansion of e commerce has amplified the need for durable labeling and packaging solutions where release liners play a pivotal role in ensuring label integrity during transit. The market operates within a framework of increasing environmental scrutiny prompting manufacturers to explore recyclable and bio based alternatives.

MARKET DRIVERS

Expansion Of E Commerce And Logistics Sector Drives Labeling Demand

The exponential growth of the e-commerce and logistics sector by escalating the demand for high quality labels and packaging materials is solely propelling the growth of release liners market. As per the United Nations Conference on Trade and Development, global e-commerce sales reached 26.7 trillion US dollars in 2023, reflecting a significant increase in online retail activities. This surge necessitates efficient labeling systems for package identification tracking and branding which rely heavily on pressure sensitive adhesives backed by release liners. Each parcel shipped requires multiple labels including shipping addresses barcodes and handling instructions all of which utilize release liner technology during the manufacturing and application process. The complexity of modern supply chains demands labels that can withstand various environmental conditions such as temperature fluctuations and moisture exposure during transit. The rise of quick commerce and same day delivery services has intensified the volume of packages handled daily requiring faster and more reliable labeling processes. Automated sorting facilities depend on high performance labels that adhere securely to diverse packaging materials ranging from cardboard to plastic polybags. Release liners ensure that these labels are applied precisely and without defect maintaining operational efficiency in distribution centers. The continuous expansion of digital retail platforms globally ensures a steady and growing demand for release liners as an integral component of the packaging ecosystem.

Growing Healthcare Sector And Medical Device Adoption Increases Consumption

The expanding healthcare sector and the widespread adoption of medical devices as due to the role these materials play in medical applications is also leveraging the growth of release liners market. As per the World Health Organization, global health expenditure has risen steadily with many countries increasing their investment in healthcare infrastructure and medical supplies. Pressure sensitive adhesives are essential in the production of wound care dressings transdermal patches surgical tapes and diagnostic devices all of which require high quality release liners to maintain sterility and functionality. The aging global population is a key factor contributing to this demand as older individuals, typically require more frequent medical interventions and chronic disease management. According to the United Nations Department of Economic and Social Affairs, the number of people aged 65 years or older is projected to double from 703 million in 2019 to 1.5 billion in 2050. Furthermore, the increasing prevalence of chronic conditions, such as diabetes and cardiovascular diseases necessitates the use of monitoring devices and drug delivery systems that rely on adhesive technologies. Regulatory standards for medical devices mandate strict quality control and material safety ensuring that release liners used in these applications meet rigorous biocompatibility and performance criteria. The innovation in smart medical devices and wearable health monitors also contributes to market growth as these products often incorporate advanced adhesive systems.

MARKET RESTRAINTS

Stringent Environmental Regulations And Waste Management Challenges

The stringent environmental regulations and the challenges associated with waste management by imposing compliance costs and limiting material choices is impeding the growth of release liners market. Release liners are typically single use items that contribute substantially to industrial waste generating millions of tons of discarded material annually. As per the European Environment Agency, packaging waste in the European Union has reached record levels prompting stricter directives on recycling and waste reduction. Many municipal recycling facilities lack the technology to separate the silicone layer from the substrate leading to contamination and rejection of these materials. Governments are increasingly implementing extended producer responsibility schemes that hold manufacturers accountable for the end of life disposal of their products. These regulations force companies to invest in expensive recycling technologies or alternative materials that may not offer the same performance characteristics. The ban on certain single use plastics in various jurisdictions further restricts the use of polymer-based release liners. Compliance with these evolving legal frameworks requires significant research and development expenditures which can erode profit margins. Additionally, the lack of standardized recycling protocols across different regions creates operational complexities for multinational corporations.

Volatility In Raw Material Prices And Supply Chain Disruptions

The volatility in raw material prices and ongoing supply chain disruptions by creating uncertainty in production costs and availability is another factor degrading the growth of release liners market. The primary materials used in release liner production including paper pulp silicone polymers and plastic films are subject to fluctuating global commodity prices. The cost of wood pulp a key ingredient for paper based liners is influenced by forestry policies weather conditions and demand from other paper industries. Similarly, the price of silicone which is derived from silicon metal is affected by energy costs and production capacity constraints in major producing countries like China. According to the International Monetary Fund, global supply chain pressures have remained elevated causing delays and increased freight costs for imported materials. These fluctuations make it difficult for manufacturers to predict expenses and maintain stable pricing strategies for their customers. Small and medium sized enterprises are particularly vulnerable to these shocks as they lack the bargaining power to secure long term supply contracts at fixed rates. The dependence on a limited number of suppliers for specialized coating chemicals further exacerbates the risk of supply interruptions. Any disruption in the supply of critical raw materials can lead to production downtimes and missed delivery deadlines affecting customer relationships. The inability to fully pass on increased costs to consumers due to competitive market dynamics squeezes profit margins.

MARKET OPPORTUNITIES

Development Of Recyclable And Bio Based Release Liner Solutions

The development of recyclable and bio-based release liner solutions to align with sustainability goals and capture environmentally conscious customers is certainly a major factor to create new opportunities for the growth of release liners market. As per the Ellen MacArthur Foundation, the transition to a circular economy is gaining momentum with businesses seeking innovative ways to eliminate waste and keep materials in use. Traditional silicone coated liners are difficult to recycle but new technologies are emerging that allow for the separation of silicone from paper fibers by enabling the recycling of the substrate. Companies are investing in research to create wash off silicone coatings and alternative release agents that do not contaminate the recycling stream. Bio-based release liners made from renewable resources, such as cellulose and plant based polymers offer a lower carbon footprint compared to petroleum based alternatives. These innovations appeal to consumer goods companies looking to enhance their environmental credentials and meet regulatory requirements. The ability to offer certified compostable or recyclable liners provides a competitive advantage in tenders and contracts with eco focused retailers. Furthermore, partnerships with recycling facilities to establish closed loop systems can create new revenue streams and improve brand loyalty. The market for sustainable liners is expected to grow as legislation tightens and consumer awareness increases.

Expansion Into Emerging Markets With Growing Manufacturing Bases

The expansion into emerging countries with growing manufacturing bases into new sources of demand is to elevate new opportunities for the growth of release liners market. Countries in Asia Pacific, Latin America, and Eastern Europe are experiencing rapid industrialization and urbanization leading to increased production of consumer goods electronics and automobiles. As per the study, manufacturing output in developing economies has grown steadily contributing to global supply chains. These regions are becoming hubs for the production of labeled products, including packaged foods beverages and personal care items, which require release liners. The rising middle class in these markets is driving consumption of branded goods thereby increasing the volume of labels and tapes used. Local manufacturing of release liners can reduce dependency on imports and lower costs for regional producers. Establishing production facilities in these emerging countries that allows companies to serve local customers more efficiently and respond quickly to changes. The adoption of modern labeling technologies in these regions is also creating demand for high performance liners. Government initiatives to boost domestic manufacturing such as Make in India provide further impetus for growth.

MARKET CHALLENGES

Technical Complexity In Recycling Silicone Coated Materials

The technical complexity involved in recycling silicone coated materials by hindering the implementation of effective waste management solutions is one of the major challenges for the growth of release liners market. Silicone coatings are designed to be highly stable and resistant to degradation which makes them difficult to separate from the paper or film substrate during the recycling process. This contamination reduces the quality of the recycled paper and limits its applications in high value products. The presence of silicone can cause issues in paper mills, such as foam formation and reduced strength of the final product. Current recycling technologies are often energy intensive and require significant capital investment making them economically unviable for many facilities. The lack of standardized collection systems for release liner waste further complicates the recycling effort. Most liners end up in landfills or incinerators contributing to environmental pollution and resource depletion. Developing chemical or mechanical processes that can efficiently recover both the substrate and the silicone is a significant scientific hurdle. Research into enzymatic treatments and advanced separation techniques is ongoing but commercial viability remains elusive.

High Cost Of Alternative Eco Friendly Materials And Technologies

The high cost of alternative eco-friendly materials and technologies by limiting their widespread adoption and competitiveness is additionally to slow down the growth of release liners market. Bio-based and recyclable release liners often require specialized raw materials and complex manufacturing processes that are more expensive than traditional silicone coated papers. As per the International Renewable Energy Agency, the production costs for bio-based polymers remain higher than those for conventional plastics due to limited scale and immature supply chains. The investment required to develop and commercialize new release agents such as water based or solvent free coatings is substantial posing a financial burden on manufacturers. Many end users are price sensitive and reluctant to pay a premium for sustainable liners unless mandated by regulation. Small and medium sized converters may lack the financial resources to upgrade their equipment to handle new materials effectively. The economic viability of recycling technologies is also constrained by the high operational costs and low value of the recovered materials. Manufacturers must balance the desire for sustainability with the need for profitability navigating a challenging economic landscape.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 8.47% |

| Segments Covered | By Substrate Type, Application, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa. |

| Market Leaders Profiled | 3M Company (US), Gascogne Laminates (France), Loparex (US), Mondi Group (Austria), Ahlstrom-Munksjo (Sweden), UPM (Finland), Eastman Corporation (US), Polyplex Corporation Ltd. (India), LINTEC Corporation (Japan), Sappi Limited (South Africa), Rayven Inc(US) and SilTech(Canada), and Others. |

SEGMENTAL ANALYSIS

By Substrate Type Insights

The glassine and calendared kraft paper segment was the largest by holding 55.6% of the release liners market share in 2025 due to their cost effectiveness and widespread compatibility with existing converting equipment used in the label and tape industries. The manufacturing process for glassine and kraft paper is well established allowing for high volume production at competitive prices which appeals to cost sensitive sectors such as food packaging and logistics. The paper based liners are preferred for their recyclability potential compared to plastic alternatives aligning with growing sustainability mandates. The smooth surface of glassine ensures consistent silicone coating and reliable release performance, which is for high speed automated labeling applications. Furthermore, the stiffness and dimensional stability of calendared kraft paper make it ideal for heavy duty applications where durability is required. The versatility of these paper substrates allows them to be used across a wide range of adhesive types including acrylics and hot melts. The ability to print directly on the liner or the face stock enhances their utility in branding and identification.

The polyolefin coated segment is likely to witness a fastest CAGR of 5.8% from 2026 to 2034 with the increasing demand for durable and moisture resistant liners in harsh industrial and outdoor environments. As per the International Energy Agency, the expansion of the automotive and electronics sectors requires labeling solutions that can withstand extreme temperatures chemicals and UV exposure. Polyolefin films, such as polyethylene and polypropylene offer superior mechanical strength and water resistance compared to paper based alternatives. The production of polyolefin resins continues to rise due to their versatility and low cost supporting the availability of raw materials for liner manufacturing. These films are essential for applications, such as vehicle wraps construction tapes and electronic component labelling, where failure is not an option. The ability of polyolefin liners to maintain integrity during high-speed dispensing and application processes enhances operational efficiency for end users. Furthermore, the lightweight nature of film based liners reduces shipping costs and carbon emissions associated with transportation. The development of thinner gauges without compromising performance allows for more efficient material usage. Innovations in coating technologies have improved the adhesion and release characteristics of polyolefin films making them suitable for a broader range of adhesives.

By Application Insights

The labels segment was the largest by holding 46.5% of the release liners market share in 2025 with the ubiquitous use of labels in packaging logistics and retail sectors, which require reliable adhesive solutions for product identification and branding. As per the United Nations Conference on Trade and Development, global merchandise trade volumes have remained resilient driving the demand for shipping labels and barcodes. Every packaged product typically requires at least one label for regulatory compliance pricing and marketing purposes creating a vast and consistent demand base. According to Euromonitor International the packaged food and beverage industry continues to expand globally particularly in emerging markets where urbanization is increasing consumption of branded goods. The complexity of modern supply chains necessitates durable labels that can withstand handling storage and transportation conditions. Release liners ensure that these labels are applied accurately and efficiently during high speed packaging operations. The rise of e-commerce has further amplified the need for shipping labels which must adhere to various surfaces including cardboard plastic and metal. The versatility of label applications across diverse industries ensures steady growth for the release liner market. Furthermore, innovations in smart labels and radio frequency identification tags are creating new opportunities for specialized liners.

The hygiene application segment is expected to register a fastest CAGR of 6.2% from 2026 to 2034 owing to the increasing health awareness and the aging global population, which drives the consumption of adult incontinence products and feminine hygiene items. As per the United Nations Department of Economic and Social Affairs, the number of people aged 60 years or older is expected to reach 2.1 billion by 2050. These hygiene products rely heavily on pressure sensitive adhesives for fit and comfort, which require high performance release liners during manufacturing. The rising disposable incomes in developing countries are enabling greater access to premium hygiene products thereby increasing volume demand. Manufacturers are focusing on developing softer and more breathable materials that enhance user comfort requiring specialized release liners for precise assembly. The stigma surrounding adult incontinence is decreasing leading to higher adoption rates and expanded product ranges. Furthermore, innovations in leak protection and odor control technologies drive product replacement cycles.

REGIONAL ANALYSIS

Asia Pacific Release Liners Market Analysis

Asia Pacific was the top performer in the release liners market by holding 40.3% of the share in 2025 with the rapid industrialization and a booming manufacturing sector, particularly in China, India, and Southeast Asian countries. The region continues to be the factory of the world driving demand for industrial tapes labels and packaging materials. The expanding middle class is fueling consumption of packaged goods and personal care products, which rely heavily on release liner technologies. The presence of major global release liner manufacturers alongside local players creates a competitive landscape that drives innovation and cost efficiency. The growth of e-commerce platforms in countries like China and India has amplified the need for shipping labels and packaging solutions. Government initiatives to improve infrastructure and logistics further facilitate market expansion. The availability of raw materials such as paper pulp and polymers supports local production capabilities. Furthermore, the increasing awareness of hygiene and healthcare in the region boosts demand for medical and personal care applications.

North America Release Liners Market Analysis

North America release liners market held second position with the mature consumption patterns and a strong focus on sustainability and technological innovation. The strict regulations on waste management and recycling drive the adoption of eco-friendly release liner solutions. The United States and Canada are home to leading global manufacturers, who invest heavily in research and development to create advanced coating technologies. The packaging industry in the United States remains robust supported by strong consumer spending and export activities. The healthcare sector in North America is highly advanced driving demand for high quality medical tapes and wound care dressings. The prevalence of chronic diseases and an aging population sustain the need for these medical applications. The region is a pioneer in the adoption of smart labels and radio frequency identification technologies which require specialized release liners. The strong presence of retail giants and e commerce leaders ensures consistent demand for labeling solutions. Regulatory compliance regarding food safety and product labeling further supports market stability.

Europe Release Liners Market Analysis

Europe release liners market growth is likely to grow with the stringent environmental regulations and high consumer awareness. As per the European Environment Agency, packaging waste directives are driving manufacturers to develop recyclable and compostable release liner alternatives. Countries such as Germany, France, and the United Kingdom are leading the adoption of sustainable materials in the packaging and hygiene sectors. The region has a strong pharmaceutical and medical device industry which demands high performance and sterile release liners for medical applications. Consumer preference for eco-friendly products pushes brands to adopt sustainable packaging solutions. The presence of major chemical and material science companies facilitates innovation in coating technologies. Regulatory pressure combined with consumer demand creates a dynamic environment for green innovation.

Latin America Release Liners Market Analysis

Latin America release liners market growth is driven by the economic volatility but supported by a growing population and increasing urbanization. Brazil and Mexico are the largest contributors in the region with expanding manufacturing bases for consumer goods. The investment in infrastructure and logistics is improving supply chain efficiency facilitating growth. The rising middle class is adopting modern retail formats, which require standardized labeling and packaging solutions. The healthcare sector is also expanding increasing the demand for medical adhesives and hygiene products. Local manufacturers are increasingly partnering with global players to introduce advanced technologies and products. The potential for increased penetration of modern retail and e-commerce offers further growth opportunities.

Middle East and Africa Release Liners Market Analysis

The Middle East and Africa release liners market growth is likely to grow with the varying levels of economic development and industrialization. In the Middle East, countries like Saudi Arabia and the United Arab Emirates are investing heavily in diversifying their economies beyond oil, which includes developing manufacturing and logistics sectors. The urbanization in Africa is accelerating creating opportunities for packaged food and beverage industries. The healthcare sector in both regions is expanding improving access to medical supplies and hygiene products. Despite these challenges, the long term demographic trends and economic diversification efforts support gradual growth. The potential for increased industrialization and retail modernization offers opportunities for release liner manufacturers.

COMPETITIVE LANDSCAPE

The competition in the release liners market is characterized by the presence of established global giants and specialized regional players who compete on technology sustainability and service quality. Leading corporations leverage their extensive distribution networks and economies of scale to dominate the market while niche players focus on innovative coatings and customized solutions. The industry faces intense pressure to develop eco friendly alternatives due to stringent environmental regulations and consumer demand for sustainable packaging. This drives significant investment in research and development for recyclable and bio based materials. Price competition remains moderate as customers prioritize performance and compliance over cost alone. Strategic acquisitions and collaborations are common as companies seek to expand their geographic footprint and technological capabilities. The barrier to entry is high due to the capital intensive nature of coating machinery and the need for specialized technical expertise.

Key Market Players

The major key players in the global release liners market are

- 3M Company

- Gascogne Laminates

- Loparex

- Mondi Group

- Ahlstrom-Munksjö

- UPM

- Eastman Corporation

- Polyplex Corporation Ltd.

- LINTEC Corporation

- Sappi Limited

- Rayven Inc.

- SilTech

Top Players in the Market

- Ahlstrom Munksjo is a global leader in fiber based materials and plays a pivotal role in the Release Liners Market through its extensive portfolio of specialty papers. The company provides high performance glassine and kraft liners that are essential for label and tape applications across various industries. Ahlstrom focuses on sustainability by developing recyclable and bio based solutions that meet stringent environmental regulations. Recent actions include investing in production capacity expansion in Europe and North America to address growing demand for sustainable packaging materials. The corporation actively collaborates with customers to create customized release liner solutions that enhance converting efficiency and end use performance. Their commitment to circular economy principles drives the development of products that support waste reduction and recycling initiatives.

- UPM Raflatac is a prominent provider of self adhesive label materials and significantly contributes to the Release Liners Market through its innovative substrate offerings. The company specializes in producing high quality paper and film based release liners that cater to diverse labeling requirements in retail logistics and industrial sectors. UPM emphasizes resource efficiency by utilizing renewable raw materials and optimizing manufacturing processes to minimize environmental impact. Recent initiatives include the launch of recycled content release liners and the expansion of its global production network to enhance supply chain resilience. The company invests heavily in research and development to improve the performance and sustainability of its products. UPM also engages in strategic partnerships with brand owners to promote circular economy practices in the label value chain.

- LINTEC Corporation is a leading manufacturer of adhesive functional materials and holds a strong presence in the Release Liners Market with its advanced coating technologies. The company offers a wide range of release liners for labels tapes hygiene products and industrial applications. LINTEC is known for its precision engineering and ability to produce high performance films and papers that meet rigorous quality standards. Recent actions include expanding its manufacturing facilities in Asia and Europe to capture growing demand in emerging markets. The corporation focuses on developing eco friendly products such as thin film liners and recyclable paper options to address environmental concerns. LINTEC also invests in automation and digital technologies to enhance production efficiency and product consistency.

Top Strategies Used by the Key Market Participants

Key players in the Release Liners Market primarily focus on sustainability driven innovation to maintain competitive advantage. Companies invest heavily in research and development to create recyclable bio based and compostable release liner alternatives that comply with strict environmental regulations. Expansion of production capacity in emerging markets is another critical strategy allowing manufacturers to meet rising demand from Asia Pacific and Latin America. Strategic partnerships with brand owners and converters help integrate sustainable solutions into the supply chain effectively. Diversification of product portfolios to include specialized films and papers for niche applications such as healthcare and electronics enhances market reach. Automation and digitalization of manufacturing processes improve operational efficiency and reduce costs. These strategies enable companies to address environmental challenges while capturing growth opportunities in evolving markets.

MARKET SEGMENTATION

This research report on the global release liners market has been segmented and sub-segmented based on substrate type, application, and region.

By Substrate Type

- Polyolefin Coated

- Clay Coated

- Glassine/Calendared Kraft Paper

By Application

- Labels

- Pressure-Sensitive Tapes

- Hygiene

By Region

- North America

- Latin America

- Europe

- Asia Pacific

- Middle East & Africa

Frequently Asked Questions

1.What is the release liners market?

The release liners market involves the production and supply of coated papers and films used as carriers for pressure sensitive adhesives in labels, tapes, and graphic applications.

2.What are the key drivers of the release liners market growth?

Market growth is driven by rising demand for pressure sensitive labels, growth of packaging and logistics industries, and increased use in medical and hygiene products.

3.What materials are commonly used in release liners?

Common materials include paper based liners, polyethylene films, polypropylene films, and polyester films.

4.What coatings are applied to release liners?

Silicone coatings are most widely used due to their excellent release properties, thermal stability, and chemical resistance.

5.Which end use industries consume the most release liners?

Major end use industries include packaging, food and beverage, pharmaceuticals, personal care, electronics, and automotive.

6.How does the packaging industry influence the release liners market?

Growth in flexible packaging, labeling, and e commerce significantly increases demand for high performance release liners.

7.What role do release liners play in pressure sensitive labels?

Release liners protect the adhesive layer until application, ensuring easy handling, accurate placement, and consistent performance.

8.What are the key types of release liners available in the market?

Key types include paper based release liners and film based release liners designed for different durability and performance needs.

9.Which regions dominate the global release liners market?

Asia Pacific, North America, and Europe dominate the market due to strong manufacturing activity and high demand for packaged goods.

10.What challenges does the release liners market face?

Key challenges include raw material price volatility, recycling complexity, and environmental concerns related to liner waste.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com