Global Second-Hand Clothing Market Size, Share, Trends, Growth Forecast Report By Product Type (Dresses and Tops, Shirts and T-Shirts, Sweaters, Coats and Jackets, Jeans And Pants, and Others), Sector (Resale, Traditional Thrift Stores & Donations), Target Population (Men, Women, and Kids), Sales Channel (Wholesalers or Distributors, Hypermarkets or Supermarkets, Multi-Brand Stores, Independent Small Stores, Departmental Stores, Online Retailers, Other Sales Channel), and Region (North America, Europe, Asia Pacific, Latin America, And Middle East & Africa) - Industry Analysis (2026 to 2034)

Market Size, 2025

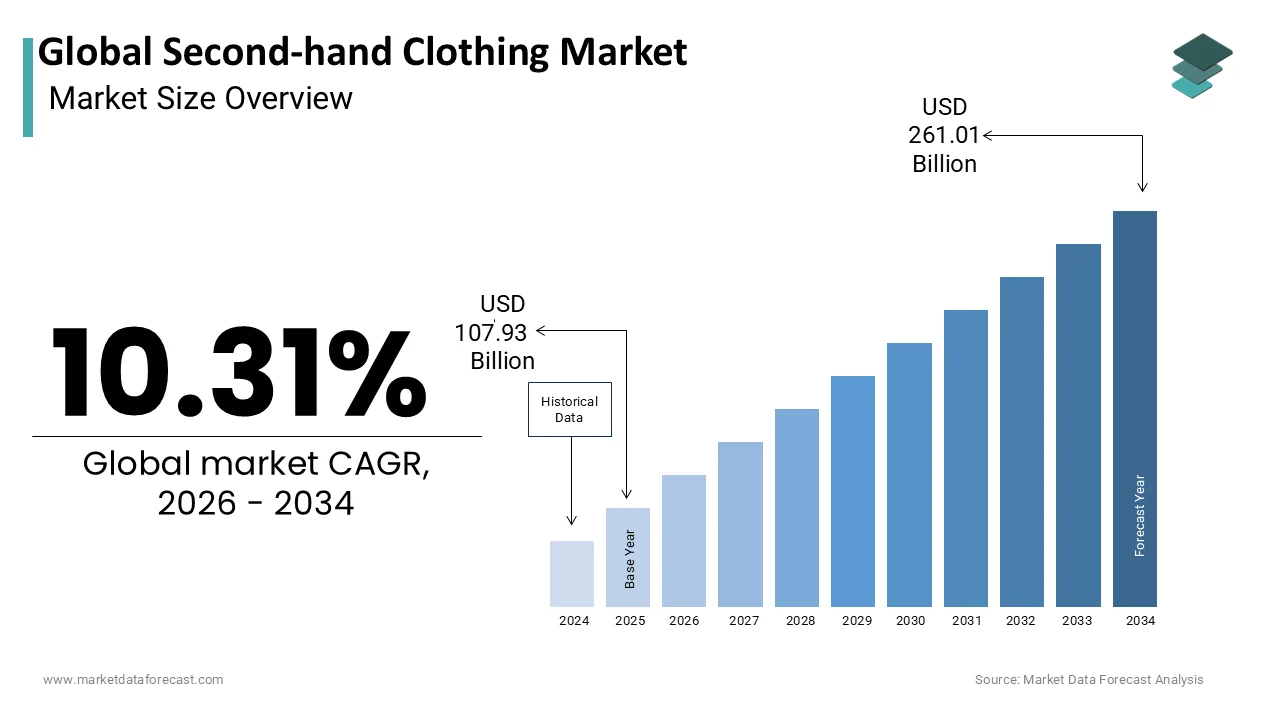

$107.93 BnMarket Estimate, 2026

$119.03 BnMarket Forecast, 2034

$261.01 BnCAGR, 2026–2034

10.31%Global Second-hand Clothing Market Size

The global second-hand clothing market was valued at USD 107.93 billion in 2025, is expected to have a 10.31% CAGR from 2026 to 2034, and be worth USD 261.01 billion by 2034 from USD 119.03 billion in 2026.

Second-hand clothing is the resale, reuse, and redistribution of pre-owned garments through formal retail channels, online platforms, charity shops, and informal exchanges. In 2023, the global population discarded approximately 92 million tons of textile waste, with less than 15% being recycled. Meanwhile, the Ellen MacArthur Foundation estimates that extending the life of clothing by just nine months reduces associated carbon, water, and waste footprints by 20 to 30%. Consumer behavior is shifting markedly among younger demographics, with 62% of Generation Z shoppers in the United States indicating a preference for buying used apparel to reduce environmental impact. Unlike conventional retail, the second-hand clothing ecosystem thrives on circularity, where garments transition through multiple ownership cycles, thereby decoupling fashion consumption from virgin resource extraction.

MARKET DRIVERS

Rising Environmental Consciousness Among Consumers

Environmental awareness is majorly propelling the demand in the second-hand clothing market. Consumers increasingly recognize the ecological toll of textile production, which accounts for roughly 10% of global carbon emissions and consumes nearly 93 billion cubic meters of water annually, as per reports. This awareness is particularly acute among younger cohorts. Many consumers aged 18 to 34 in Western Europe actively consider environmental impact when purchasing apparel, with 58 % having bought second-hand clothing in the past year. Educational campaigns and digital transparency tools have amplified this shift by enabling buyers to trace the lifecycle impact of garments. Platforms like ThredUp and Vestiaire Collective now integrate carbon footprint calculators. Moreover, the European Environment Agency notes that reusing second-hand clothing could reduce the emission of carbon dioxide.

Economic Pressures and Cost Sensitivity in Post-Pandemic Economies

The heightened economic uncertainty and inflationary pressures have significantly intensified consumer reliance on second-hand clothing as a pragmatic alternative to new retail. Amidst this backdrop, households are recalibrating discretionary spending, with second-hand apparel offering substantial savings, typically 50 to 80% lower than original retail prices. This shift is especially pronounced in middle-income segments, where disposable income constraints intersect with fashion aspirations. Furthermore, digital resale platforms have enhanced accessibility and trust, which is transforming thrift from a necessity into a strategic consumption choice.

MARKET RESTRAINTS

Inconsistent Quality and Hygiene Standards Across Resale Channels

The variable quality control and hygiene protocols, which undermine consumer confidence and limit mainstream adoption, are ascribed to limiting the growth of the second-hand clothing market. Pre-owned garments lack standardized grading systems by leading to unpredictable conditions ranging from near new to heavily worn. Tested second-hand garments from unregulated online sellers contained residual biological contaminants, including skin cells and traces of mold, raising health concerns among sensitive populations. Additionally, the absence of universal cleaning mandates means that disinfection practices vary widely. Charity shops in France are required by law to sanitize donations, whereas informal peer-to-peer platforms in the United States operate without such oversight. A 2024 YouGov poll revealed that 51 % of U.S. adults avoid buying second-hand intimate apparel due to hygiene worries.

Logistical and Sorting Inefficiencies in Reverse Supply Chains

The supply chain faces significant inefficiencies that constrain scalability, and profitability is also a factor restraining the growth of he second-hand clothing market. Unlike forward logistics in traditional retail, reverse flows involve unpredictable volumes, heterogeneous item conditions, and labor-intensive sorting processes. The remainder is downcycled, exported, or landfilled by creating economic leakage and environmental burden. Moreover, transportation emissions from global redistribution, such as the shipment of unsold European donations to African countries, have drawn scrutiny. These logistical frictions increase costs, delay inventory turnover, and reduce margins for resellers.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence in Personalized Resale Experiences

The deployment of artificial intelligence in second-hand fashion platforms by enhancing discovery, trust, and transaction efficiency poses a new opportunity for the growth of the second-hand clothing market. AI algorithms now analyze user behavior, body metrics, and style preferences to curate hyper-personalized inventory recommendations, which are significantly improving conversion rates. This reduces human error and accelerates listing times. Additionally, AI-powered authentication tools are combating counterfeit risks. A 2024 study by the European Intellectual Property Office, AI verification reduced fake luxury listings on resale platforms by 61% in six months. These innovations not only elevate user experience but also professionalize the resale ecosystem, attracting brand collaborations and institutional investment.

Expansion of In-Store Trade-In and Instant Resale Programs by Major Retailers

The branded retail partnerships are unlocking new growth factors through structured trade-in and instant resale initiatives, which will additionally fuel the growth of the second-hand clothing market in the coming years. Global fashion retailers are increasingly embedding circularity into their customer journeys by offering store credit or cash for used garments, regardless of brand origin. Similarly, Zara launched its “Pre-Owned” section in select European stores by allowing customers to trade items for vouchers redeemable on new purchases. These programs generate dual benefits: they secure consistent inventory streams for resale while enhancing brand loyalty.

MARKET CHALLENGES

Counterfeit and Authentication Risks in High Value Resale Segments

The proliferation of counterfeit goods in premium second-hand channels poses a significant challenge to second-hand clothing market growth. Luxury resale is particularly vulnerable. A 2024, an investigation by the UK’s Trading Standards Institute found that 29% of “designer” handbags listed on peer-to-peer marketplaces were inauthentic, with some replicas indistinguishable without forensic analysis. This erodes buyer confidence, especially among new entrants, and increases operational costs for platforms investing in authentication. Moreover, legal recourse is often unclear in cross-border transactions by leaving buyers unprotected.

Regulatory Fragmentation Across Global Textile Waste and Resale Policies

The patchwork of divergent national regulations governing textile waste, import restrictions, and consumer protection is also hindering the growth of the second-hand clothing market. The European Union is advancing its Circular Economy Action Plan with binding targets for textile collection and reuse by 2030. Countries like Ghana and Chile serve as major import hubs but lack the infrastructure to manage the resulting waste. Accra alone receives over 150,000 tons of second-hand clothing annually, with 40% ultimately discarded in landfills. Simultaneously, data privacy laws like the EU’s General Data Protection Regulation complicate digital resale operations that rely on user profiling. This regulatory asymmetry impedes the development of standardized global resale models, increases legal risk, and fragments supply chains.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Sector, Target Population, Sales Channel |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

| Market Leaders Profiled | Thredup Inc., StockX, The RealReal, Chikatex, Poshmark, HunTex Recycling Kft, Vinted, eBay Inc., Micolet, British Used Clothing Company, Percentil. ma, Tradesy, A&E Used Clothing Wholesale, Thrift+, Mobacotex, and others. |

SEGMENTAL ANALYSIS

By Product Type Insights

The dresses and tops segment accounted for holding largest share of the global second-hand clothing market, with high consumer turnover and style volatility in women’s fashion. This category experiences rapid obsolescence due to seasonal trends, social media influence, and occasion-specific wear, prompting frequent replacement and resale. Additionally, rental and resale hybrid models, such as those offered by Nuuly and By Rotation, that prioritize dresses for special events, further amplify circulation. Female shoppers aged 18 to 35 buy second-hand dresses for weddings, parties, or professional events to avoid single-use purchases, as per the reports. This behavioral pattern, coupled with lower production costs for lightweight tops compared to outerwear, enables higher inventory velocity and margin retention for sellers. The combination of trend sensitivity, digital visibility, and functional versatility solidifies dresses and tops as the market’s cornerstone segment.

The coats and jackets segment is likely to register a CAGR of 9.2% during the forecast period, with the rising demand for premium outerwear and a climate-driven necessity. The second-hand outerwear category grew by 18 % year on year in 2024, with luxury labels like Canada Goose and The North Face dominating resale listings, as per studies. Additionally, colder winters linked to climate variability, such as the 2023–2024 European cold snap that saw temperatures drop 4.2 degrees Celsius below seasonal norms, have intensified demand for functional winter wear. Simultaneously, sustainability messaging around “buy less but better” resonates strongly in this category, as one quality coat replaces multiple cheaper alternatives.

By Sector Insights

The resale segment is more prevalent among customers and is anticipated to increase in market size during the forecast period. According to the survey, about 44 per cent of buyers were reducing their expenditure on apparel due to inflated costs. Around 58per cent of customers in the same period purchasing second-hand supported them amid inflation and recession concerns. However, traditional thrift stores are slowly gaining traction with a recent opening in Tokyo, Japan.

By Target Population Insights

Women's segment was the largest by occupying61.2% of the second-hand clothing market share in 2024, owing to higher engagement with fashion cycles and digital resale ecosystems. Women accounted for 63% of second-hand apparel transactions globally, with particularly strong activity in dresses, tops, and accessories. As per a study by the Boston Consulting Group, 57% of women aged 20 to 40 feel social pressure to wear new or different clothing in photos shared online, driving both disposal and acquisition behaviors. Furthermore, women are more likely to utilize peer-to-peer resale apps; data from App Annie shows that female users have active accounts on platforms like Poshmark and Depop. Retailers have responded by tailoring user experiences.

The children’s segment is projected to register a CAGR of 6.3% during the forecast period, with the short usable lifespan of kids’ apparel and heightened parental focus on cost efficiency and sustainability. Children typically outgrow clothing every three to six months, rendering new purchases economically inefficient. A 2024 survey by the U.S. Department of Agriculture, the average American family spends $750 annually on children’s clothing, with 42% expressing interest in second-hand alternatives to reduce this burden. Platforms like Kidizen and ThredUp Kids have capitalized on this need, offering curated bundles and size exchange programs. Environmental concerns also play a role, where parents in the European Union are increasingly aware that producing a single cotton onesie generates 3.5 kilograms of carbon dioxide.

By Sales Channel Insights

The Online retailers segment held 34.4% of the global second-hand clothing market share, owing to the convenience, algorithmic personalization, and expansive inventory access unmatched by physical formats. Digital platforms eliminate geographic constraint by enabling a single user in Oslo to purchase a vintage jacket listed in Los Angeles, thereby aggregating fragmented supply into liquid marketplaces. The dominance of this channel is further reinforced by trust-building features such as AI-powered authentication, standardized condition grading, and seamless return policies.

The independent small stores segment is likely to grow with an anticipated CAGR of 7.3% in the coming years. These boutiques differentiate themselves through curated selections, storytelling, and hyperlocal sourcing, appealing to consumers fatigued by algorithm-driven homogeneity. A 2024 survey found that 54% of U.S. shoppers prefer small businesses for second-hand clothing due to perceived authenticity and reduced packaging waste. These stores often collaborate with local designers for upcycling workshops by creating experiential retail that transcends transactional exchange.

REGIONAL ANALYSIS

Europe Second Hand Clothing Market Analysis

Europe was the top performer of the global second-hand clothing market by occupying 31.2% of the share in 2024, with progressive regulatory frameworks, high environmental literacy, and mature resale infrastructure. The region’s dominance is institutionalized through policies like the EU Strategy for Sustainable and Circular Textiles, which mandates separate textile collection in all member states by 2025. Digital adoption complements physical channels, where Vinted, headquartered in Lithuania. Furthermore, extended producer responsibility laws compel brands like H&M and Zara to fund collection and sorting by creating a self-reinforcing circular loop.

North America Second-Hand Clothing Market Analysis

North America's second-hand clothing market growth is driven by a dynamic digital resale and strong youth-driven adoption. The United States' second-hand clothing market growth is fueled by platforms like Poshmark, ThredUp, and The RealReal, which have normalized peer-to-peer fashion exchange. California and New York lead in policy innovation, with the former enacting the Textile Waste Diversion Act, requiring brands to collect and recycle used garments by 2027. Meanwhile, college campuses serve as micro hubs for circularity; the University of Texas reported a 40 % increase in student participation in clothing swaps between 2022 and 2024.

Asia Pacific Second-Hand Clothing Market Analysis

The Asia Pacific second-hand clothing market growth is likely to grow with prominent opportunities, with a rapidly evolving position in the export destination for used garments to an emerging consumption hub. Japan and South Korea drive domestic demand with Japan’s vintage culture in Harajuku and Koenji. In South Korea, the rise of “honjok” (solo culture) and digital minimalism has increased interest in curated second-hand pieces. Meanwhile, India and Southeast Asia remain net importers, receiving over 700,000 tons of used clothing annually from Western nations, according to the United Nations Comtrade database.

Latin America Second-Hand Clothing Market Analysis

Latin America's second-hand clothing market growth is driven by the informal trade and is now undergoing digital formalization. Countries like Chile, Colombia, and Mexico have long imported used clothing from the United States. However, a new generation is redefining this legacy through digital platforms. Economic necessity remains a key factor, with inflation averaging 6.4% across the region in 2024. Urban youth increasingly associate vintage fashion with identity expression rather than poverty, shifting cultural perceptions.

Middle East and Africa Second Hand Clothing Market Analysis

The Middle East and African second-hand clothing market growth is driven by the stark contrasts between import dependency and emerging local innovation. Countries like Ghana and Kenya host vast markets such as Kantamanto in Accra, where 30,000 traders handle 15 million items weekly.

COMPETITIVE LANDSCAPE

Competition in the second-hand clothing market is intensifying as digital platforms vie for consumer attention, inventory supply, and brand partnerships. The landscape features a mix of peer-to-peer marketplaces, curated luxury resellers, and tech-enabled mass-scale operators, each pursuing distinct positioning. Differentiation hinges on trust mechanisms such as authentication processes, condition transparency, and return policies. Logistics efficiency and speed to market are critical as consumers expect experiences comparable to new retail. Companies increasingly compete on sustainability metrics, offering carbon impact data and circularity scores to appeal to eco-conscious demographics. The entry of traditional retailers through in-house resale programs adds further pressure, raising the stakes for customer acquisition and retention. Simultaneously, regulatory developments in Europe and North America are reshaping cost structures and compliance requirements. Innovation in AI sorting, reverse logistics, and seller monetization tools defines the new frontier of competitive advantage in this rapidly evolving sector.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global second-hand clothing market include

- Thredup Inc.

- StockX

- The RealReal

- Chikatex

- Poshmark

- HunTex Recycling Kft

- Vinted

- eBay Inc.

- Micolet

- British Used Clothing Company

- PePercentilema

- Tradesy

- A&E Used Clothing Wholesale

- Thrift+

- Mobacotex

TOP LEADING PLAYERS IN THE MARKET

- Vestiaire Collective has established itself as a leading global platform for authenticated pre-owned luxury and designer fashion. Headquartered in Paris, the company operates across North America, Europe, and Asia, emphasizing circularity and brand partnerships. The company also expanded its logistics hub in Belgium to accelerate European fulfillment and introduced AI-driven condition grading to enhance listing accuracy and buyer confidence.

- ThredUp is a major force in scalable second-hand apparel, known for its proprietary Clean Out Kit and data-driven resale infrastructure. Based in the United States, it serves both individual sellers and retail partners through its Resale as a Service model. ThredUp deepened its integration with Walmart by expanding its online second-hand shop and launching a sustainability dashboard for brands to track garment lifecycles by positioning itself as a technology-enabled circularity partner rather than just a marketplace.

- Poshmark operates a social commerce-driven platform where users buy and sell used clothing through community-based interactions. Originating in the United States, it has extended its footprint into Canada, Australia, and India. Poshmark enhanced its seller tools with AI-powered pricing suggestions and introduced Posh Pass, a subscription service offering unlimited shipping, to increase user retention. The company also hosted virtual shopping events tied to cultural moments, blending entertainment with commerce to drive engagement and transaction frequency.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the second-hand clothing market prioritize authentication rigor to build consumer trust, especially in luxury segments. They invest heavily in artificial intelligence for condition assessment, pricing,g, and personalized recommendations. Strategic brand collaboration, through take-back and resale partnerships, is increasingly common to formalize circular supply chains. Expansion of logistics and sorting infrastructure enables faster inventory turnover and geographic reach. Platforms also deploy gamified and social features to boost user engagement and community loyalty. Sustainability storytelling is integrated into user interfaces to reinforce ethical consumption. Many offer seller incentives such as instant payouts or shipping subsidies to secure consistent inventory. Regulatory preparedness, particularly around extended producer responsibility, shapes long-term operational modelsMobile-firstst experiences dominate product development, reflecting user behavior trends.

GLOBAL SECOND-HAND CLOTHING MARKET NEWS

- In May 2024, Rakuten Group from Japan signed a partnership agreement with eBay to examine the demand for used Japanese fashion goods in the United States. In the same month, it commenced operations with only dealers on Rakuten's second-hand goods unit, Rakuma, to take advantage of currency impact and also of cost-of-living pressures worldwide, reducing expenditure.

MARKET SEGMENTATION

This research report on the global second-hand clothing market has been segmented and sub-segmented based on product, sector, target population, and sales channel.

By Product Type

- Dresses and Tops

- Shirts and T-shirts

- Sweaters, Coats, and Jackets

- Jeans and Pants

- Others

By Sector

- Resale

- Traditional Thrift Stores & Donations

By Target Population

- Men

- Women

- Kids

By Sales Channel

- Wholesalers or Distributors

- Hypermarkets or Supermarkets

- Multi-brand Stores

- Independent Small Stores

- Departmental Stores

- Online Retailers

- Other Sales Channel

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

1. How does the Global Second-Hand Clothing Market contribute to sustainable fashion?

The Global Second-Hand Clothing Market supports sustainability by promoting apparel reuse, reducing textile waste, and encouraging circular economy principles within the fashion industry.

2. Which are the leading online resale platforms in the Global Second-Hand Clothing Market?

Key online platforms like thredUP, Poshmark, and The RealReal lead the Global Second-Hand Clothing Market by facilitating convenient buying and selling of pre-owned clothing.

3. What role do consumer preferences play in the Global Second-Hand Clothing Market growth?

Consumer demand for affordable, eco-friendly, and unique fashion drives the Global Second-Hand Clothing Market, especially among Gen Z and millennial shoppers seeking conscious lifestyles.

4. How significant is the online segment in the Global Second-Hand Clothing Market?

The online resale segment of the Global Second-Hand Clothing Market is significant, largely expanding through innovations like mobile-first apps, AI personalization, and live shopping experiences.

5. Which regions hold major shares in the Global Second-Hand Clothing Market?

North America and Europe dominate the Global Second-Hand Clothing Market due to advanced e-commerce infrastructure and high consumer awareness, with APAC emerging quickly.

6. How do luxury and fast-selling brands impact the Global Second-Hand Clothing Market?

Luxury and fast-selling brands are essential segments within the Global Second-Hand Clothing Market, providing high-demand resale items that boost market diversity and value.

7. What are the main challenges faced by the Global Second-Hand Clothing Market?

Challenges in the Global Second-Hand Clothing Market include authentication of products, logistics for cross-border resale, and overcoming consumer stigma attached to used clothes.

8. How have rental and subscription models influenced the Global Second-Hand Clothing Market?

Rental and subscription services offer cost-effective fashion alternatives, extending garment lifecycles and contributing to the circular economy within the Global Second-Hand Clothing Market.

9. What environmental benefits does the Global Second-Hand Clothing Market offer?

By reducing the need for new clothing production, the Global Second-Hand Clothing Market helps conserve water, lower carbon emissions, and minimize landfill waste from textiles.

10. What technological innovations are shaping the Global Second-Hand Clothing Market?

Technologies such as digital product passports, AI-driven personalization, and enhanced authentication methods are shaping the future of the Global Second-Hand Clothing Market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com