- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

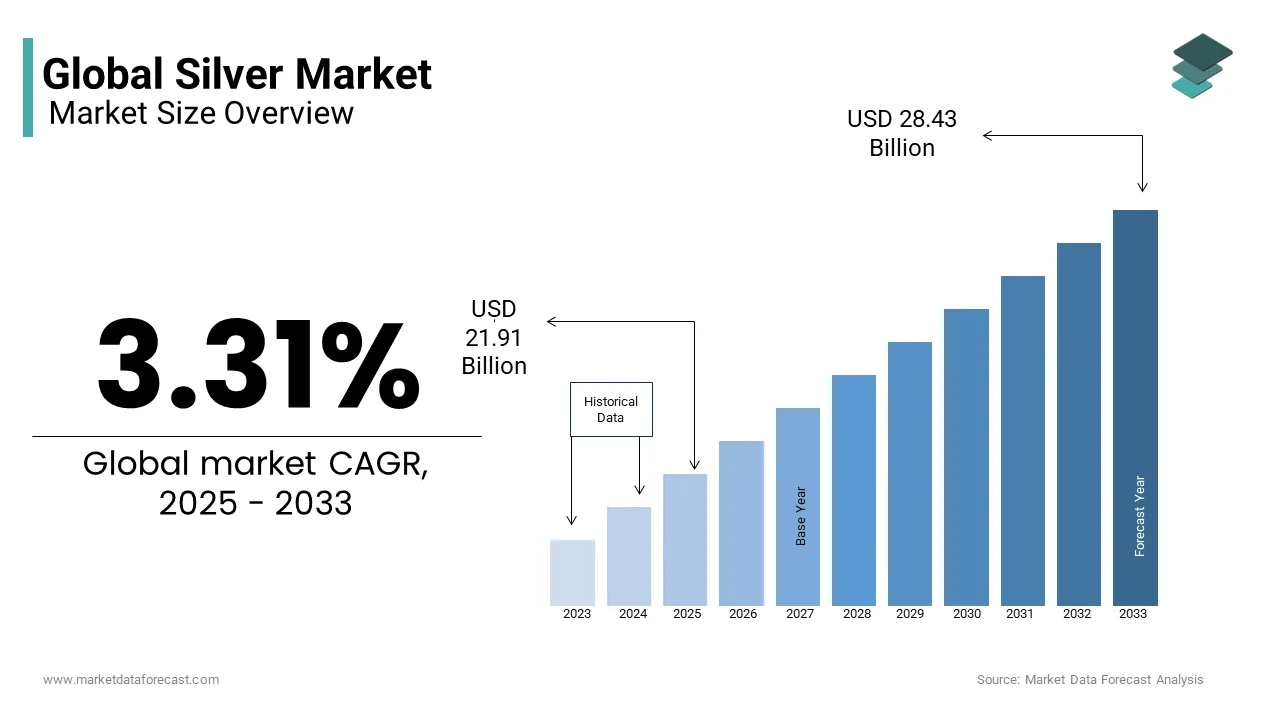

Market Size, 2025

$21.91 BnMarket Estimate, 2026

$22.64 BnMarket Forecast, 2034

$29.37 BnCAGR, 2026–2034

3.31%Global Silver Market Size

The Global silver market size was valued at USD 21.91 billion in 2025 and is anticipated to reach USD 22.64 billion in 2026 to reach USD 29.37 billion by 2034, growing at a CAGR of 3.31% during the forecast period from 2026 to 2034.

MARKET DRIVERS

Industrial Applications: A Pillar of Growth

Silver’s exceptional conductivity makes it indispensable in industries like electronics, automotive, and renewable energy. Solar energy installations, which require significant quantities of silver for photovoltaic cells, are a major contributor. The International Energy Agency estimates that global solar capacity additions hit a record 238 gigawatts in 2022, driving up silver demand. Additionally, the rise of electric vehicles (EVs), which utilize silver in batteries and control systems, has further fueled consumption.

Investment Demand: A Safe Haven Asset

Silver’s dual nature as both an industrial metal and a monetary asset boosts its appeal among investors. Historically, during periods of currency devaluation or stock market volatility, silver prices tend to spike. For instance, during the 2008 financial crisis, silver prices rose by over 150% within two years. Furthermore, younger investors are increasingly drawn to physical silver products, with the U.S. Mint reporting a 22% increase in silver coin sales in 2023 compared to the previous year.

MARKET RESTRAINTS

Supply Chain Disruptions: A Persistent Challenge

Geopolitical tensions and logistical bottlenecks have significantly hampered silver production and distribution. Political instability, coupled with labor strikes and regulatory hurdles, has curtailed mining activities, which is creating supply shortages. For example, protests in Peru led to temporary closures of several major mines by reducing output by an estimated 15 million ounces in early 2023. Additionally, global shipping delays caused by port congestion and rising freight costs have exacerbated supply chain inefficiencies. These challenges have widened the gap between supply and demand, pushing premiums higher.

Environmental Regulations: Balancing Sustainability and Profitability

Stringent environmental policies have imposed additional costs on silver producers, impacting profitability. The International Council on Mining and Metals reports that compliance expenses now account for 10-15% of total operational costs for many mining companies. Stricter waste management standards and carbon emission targets have forced firms to invest heavily in cleaner technologies, often at the expense of production efficiency. For instance, Australia mandated a 30% reduction in greenhouse gas emissions from mining operations by 2030 by compelling silver producers to adopt costly mitigation measures. While these regulations aim to promote sustainability, they also deter new entrants and slow expansion projects.

MARKET OPPORTUNITIES

Green Energy Transition

The global shift toward renewable energy presents a transformative opportunity for the silver market. As per the International Renewable Energy Agency, solar power capacity is projected to quadruple by 2050, which will require substantial amounts of silver for photovoltaic cell manufacturing. Currently, each gigawatt of solar capacity consumes approximately 80 metric tons of silver, translating into immense demand potential. Moreover, advancements in thin-film technology have made silver usage more efficient without compromising performance, ensuring its continued relevance.

Technological Innovations: Expanding Application Horizons

Emerging technologies are opening new avenues for silver utilization beyond traditional sectors. Wearable devices, flexible displays, and RFID tags are among the applications driving this trend. Additionally, the rise of 5G infrastructure has increased demand for silver-coated components, given their superior conductivity. MarketLine estimates that 5 G-related investments will reach $1 trillion globally by 2025 by directly benefiting the silver market. Innovations in antimicrobial coatings, leveraging silver’s biocidal properties, are also gaining traction, especially post-pandemic. The expanding scope of silver applications positions it as a critical material for future technological breakthroughs.

MARKET CHALLENGES

Volatile Pricing Dynamics: Impeding Stability

Silver’s price volatility poses a significant challenge for both producers and consumers, complicating planning and investment decisions. According to Trading Economics, silver prices swung between 18and25 per ounce in 2023, reflecting sensitivity to macroeconomic factors such as interest rates and currency fluctuations. The Federal Reserve’s aggressive monetary tightening has weighed heavily on precious metals, with silver experiencing sharper declines compared to gold. This volatility discourages long-term contracts and disrupts supply chains, particularly for industrial users who rely on stable input costs.

Recycling Constraints: Limiting Secondary Supply

Recycling plays a crucial yet constrained role in meeting silver demand. According to the World Silver Survey 2023, recycled silver contributes only 15% of the total supply, with recovery rates hindered by technical and economic barriers. Electronic waste, a major source of recyclable silver, often ends up in landfills due to inefficient collection systems. The United Nations Environment Programme estimates that less than 20% of e-waste is formally recycled globally by leaving vast amounts of recoverable silver untapped. Additionally, the high cost of extracting silver from complex materials limits profitability for recyclers.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.31% |

| Segments Covered | By Type, Application Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Americas Gold and Silver Corporation, Avino Silver & Gold Mines Ltd., Coeur Mining, Inc., Compañía de Minas Buenaventura S.A.A., First Majestic Silver Corp., Fortuna Silver Mines Inc., Fresnillo plc, Hecla Mining Company, Hindustan Zinc, Honey Badger Silver Inc., IMPACT Silver Corp., Industrias Peñoles, MAG Silver Corp, Orla Mining Ltd. |

SEGMENTAL ANALYSIS

By Type Insights

The fine silver segment dominated the silver market share in 2025. The growth of the segment is driven by its unparalleled applicability across industries and investment portfolios. One of the key factors propelling fine silver’s leadership is its critical role in industrial applications, particularly in solar energy. According to the International Energy Agency, the global solar photovoltaic (PV) market expanded by 22% in 2022, with each solar panel requiring approximately 20 grams of fine silver per square meter. Another driving factor is its prominence in physical investments. The U.S. Mint reported that fine silver bullion sales reached 35 million ounces in 2023, which reflects heightened investor interest amid economic uncertainties. Additionally, fine silver’s liquidity and universal acceptance make it a preferred choice for institutional buyers. Analysts at S&P Global estimate that investment-grade silver accounts for nearly 40% of total fine silver consumption, with its dual appeal as both an industrial and monetary asset.

The argentium silver segment is projected to grow at a CAGR of 12.5% from 2025 to 2033. This rapid growth is fueled by increasing adoption in the jewelry and luxury goods sectors. A significant driver is shifting consumer preferences toward sustainable and hypoallergenic materials. Technological advancements also play a pivotal role. Innovations in metallurgy have enabled manufacturers to produce Argentium silver with higher purity levels while maintaining affordability. Furthermore, rising disposable incomes in emerging economies like India and China are boosting demand.

By Application Insights

The electrical and electronics segment was the largest share of the silver market by accounting for 35.3% of the total share in 2024 due to silver’s exceptional conductivity, which makes it indispensable in high-performance applications. One major factor driving this segment’s prominence is the proliferation of electronic devices. This synergy between green energy and electronics ensures sustained demand. Another contributing factor is the growing adoption of IoT devices, which rely on silver for miniaturized sensors and antennas.

The pharmaceuticals segment is poised to grow with a CAGR of 9.8% from 2025 to 2033. The rapid expansion is driven by silver’s antimicrobial properties, which are increasingly utilized in medical coatings, wound dressings, and drug delivery systems. A key factor behind this growth is the escalating threat of antibiotic resistance. The World Health Organization states that resistant infections could claim 10 million lives annually by 2050 by prompting researchers to explore alternative solutions like silver nanoparticles.

Another driving force is innovation in healthcare technology. Silver-based antimicrobial coatings are now integral to hospital equipment and implants, reducing infection risks significantly. Furthermore, the post-pandemic emphasis on hygiene has spurred demand for silver-infected products, such as face masks and sanitizers.

REGIONAL ANALYSIS

North America Market Analysis

North America was the largest contributor with an estimated share of 18.3% in 2024. The United States dominates this region, driven by its robust industrial base and strong investment culture. According to the U.S. Energy Information Administration, solar installations in the U.S. grew by 30% in 2022, which requires substantial amounts of silver for photovoltaic cells. Additionally, the U.S. Mint reported record sales of 50 million ounces of silver coins and bars in 2023, reflecting heightened investor demand amid inflationary pressures.

The

The

Canada Market Analysis

Canadian silver market is growing at a faster rate in the coming years. The region’s advanced infrastructure and stringent environmental regulations ensure sustainable silver extraction, appealing to eco-conscious investors.

Europe Market Analysis

The Europe silver market held 16.3% of the share, with Germany, the UK, and France leading the charge. This region’s dominance is fueled by its aggressive push toward renewable energy and premium industrial applications. According to the European Photovoltaic Industry Association, Europe installed 41 gigawatts of solar capacity in 2022, which is driving demand for silver in photovoltaic cells. Germany alone accounted for 7 gigawatts of this capacity, making it a key consumer of silver for green technologies.

Asia Pacific Market Analysis

Asia-Pacific is likely to grow with the global silver market. The Chinese Ministry of Industry and Information Technology reports that the country produced 230 gigawatts of solar panels in 2022 by consuming over 145 million ounces of silver. India and Japan also play crucial roles, albeit in different sectors. Meanwhile, Japan’s advancements in semiconductor technology have increased demand for silver in microelectronics, with Nikkei Asia estimating a 12% annual growth in semiconductor exports through 2025. Additionally, rising disposable incomes across Southeast Asia are boosting investment demand in physical silver products like bars and coins.

Latin America Market Analysis

The Latin American silver market is expected to grow in the coming years. Mexico and Peru are the region’s powerhouses, collectively producing over 200 million ounces of silver annually. Peru’s contribution is equally significant, though geopolitical challenges have occasionally disrupted operations.

Middle East And Africa Market Analysis

The Middle East and Africa silver market is growing at a steady pace, with silver’s role evolving beyond traditional uses. Saudi Arabia’s Vision 2030 initiative is also promoting renewable energy projects, with plans to invest $100 billion in solar energy, indirectly boosting silver consumption. Meanwhile, Africa’s growing population and urbanization trends are increasing demand for affordable jewelry and silverware.

COMPETITIVE LANDSCAPE

The global silver market is highly competitive, characterized by a mix of established giants and emerging players vying for dominance. Large-scale miners like Fresnillo, Pan American Silver, and Polymetal International dominate the upstream segment, leveraging their vast resources and technological prowess. Meanwhile, mid-tier and junior miners compete fiercely to secure financing and partnerships to develop new projects. Downstream, industrial users and investment firms influence pricing dynamics by creating volatility that challenges even seasoned players.

Geopolitical factors and regulatory frameworks further intensify competition, with countries like Mexico, Peru, and China playing pivotal roles due to their abundant reserves. Consolidation through mergers and acquisitions has become a common trend, enabling companies to achieve economies of scale and mitigate risks. Additionally, the push toward green energy and electrification has created new battlegrounds for market share, particularly in sectors like solar panels and EV components.

KEY MARKET PLAYERS

These are the market players that are dominating the global silver market include are

- Americas Gold and Silver Corporation

- Avino Silver & Gold Mines Ltd.

- Pan American Silver Corp

- Polymetal International plc

- Coeur Mining, Inc.

- Compañía de Minas Buenaventura S.A.A.

- First Majestic Silver Corp.

- Fortuna Silver Mines Inc.

- Fresnillo plc

- Hecla Mining Company

- Hindustan Zinc

- Honey Badger Silver Inc

- IMPACT Silver Corp.

- Industrias Peñoles

- MAG Silver Corp

- Orla Mining Ltd.

Top Players In the Silver Market

- Fresnillo plc, headquartered in Mexico, is one of the largest silver producers globally, contributing significantly to global supply chains. The company operates some of the world’s most productive mines, including the Fresnillo and Saucito mines, which are renowned for their high-grade ore. Fresnillo has consistently focused on sustainable mining practices and technological innovation to enhance efficiency. Additionally, Fresnillo actively engages in community development programs by fostering goodwill in regions where it operates.

- Pan American Silver Corp, based in Canada, is a key player in the silver market, known for its diversified portfolio of mines across North and South America. The company prioritizes operational excellence and sustainability, leveraging cutting-edge technologies to optimize production. It has also expanded its footprint through strategic acquisitions, such as the acquisition of Tahoe Resources in 2019, which bolstered its reserves and production capacity. Pan American Silver emphasizes corporate responsibility, with initiatives aimed at reducing carbon emissions and promoting biodiversity conservation in mining areas.

- Polymetal International plc, a London-based mining giant, plays a pivotal role in the global silver market through its focus on precious metals. Operating primarily in Russia and Kazakhstan, Polymetal leverages its expertise in complex ore processing to extract silver efficiently. The company has invested heavily in modernizing its facilities by adopting digital tools to monitor and improve productivity. Polymetal is also committed to environmental stewardship, implementing water recycling systems and reducing energy consumption. Its robust financial performance and innovative approach have cemented its status as a leader in the industry.

Top Strategies Used by Key Market Participants

Strategic Acquisitions

Key players in the silver market frequently employ acquisitions to expand their resource base and operational capabilities. For instance, acquiring smaller mining companies or those with untapped reserves allows larger firms to consolidate their market presence. This strategy not only boosts production capacity but also reduces competition by absorbing potential rivals. Acquisitions also enable companies to diversify geographically by mitigating risks associated with reliance on specific regions.

Adoption of Advanced Technologies

The integration of advanced technologies is a cornerstone strategy for enhancing efficiency and sustainability. Companies invest in automation, AI-driven analytics, and IoT-enabled equipment to streamline operations and reduce costs. For example, using drones for geological surveys and autonomous vehicles for transportation improves precision and safety. These innovations help companies meet rising demand while adhering to stringent environmental regulations by ensuring long-term viability in the competitive landscape.

Focus on Sustainability Initiatives

Sustainability has become a critical differentiator in the silver market. Leading firms prioritize eco-friendly practices, such as reducing carbon footprints and improving waste management. Initiatives like reforestation projects, renewable energy adoption, and water conservation programs enhance brand reputation and attract environmentally conscious investors. By aligning with global sustainability goals, these companies not only comply with regulations but also build trust among stakeholders by securing their position as industry leaders.

RECENT MARKET NEWS

- In April 2024, Fresnillo plc announced the launch of a $500 million initiative to upgrade its mining infrastructure with AI-driven tools by aiming to boost production efficiency by 15%.

- In June 2023, Pan American Silver completed the acquisition of Maverix Metals, a move designed to expand its royalty portfolio and strengthen its financial resilience amid fluctuating silver prices.

- In February 2023, Polymetal International implemented a renewable energy program at its Kyzyl mine by reducing carbon emissions by 20% and setting a benchmark for sustainable mining practices.

- In September 2022, Fresnillo partnered with local governments in Mexico to launch a community development fund, which allocates $10 million annually to education and healthcare projects near its mining sites.

- In November 2021, Pan American Silver introduced blockchain technology to track the origin of its silver supplies by enhancing transparency and appealing to ethically conscious consumers.

MARKET SEGMENTATION

This research report on the global silver market is segmented and sub-segmented into the following categories.

By Type

- Fine Silver

- Sterling Silver

- Argentium Silver

- Coin Silver

- Other Types

By Application

- Physical Investment (bars)

- Electrical and Electronics

- Photographic Films

- Brazing Alloys

- Jewelry and silverware

- Pharmaceuticals

- Other Applications

By Country

- North America

- Asia Pacific

- Latin America

- Europe

- Middle East And Africa