- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

Market Size, 2025

$0.94 BnMarket Estimate, 2026

$1.06 BnMarket Forecast, 2034

$2.76 BnCAGR, 2026–2034

12.72%Executive Summary: Global Solar Panel Cleaning Market

- Market Scope: Comprehensive global solar panel cleaning market analysis covering technology types, process methods, regional leadership frameworks, and waterless robotic maintenance trends.

- Market Valuation: Valued at USD 0.94 billion (2025), estimated at USD 1.06 billion (2026), and projected to reach USD 2.76 billion by 2034, registering a robust CAGR of 12.72% (2026–2034).

- Primary Growth Drivers: Rapid utility-scale solar expansion in arid regions, performance-based contracts mandating peak efficiency, autonomous robotic systems reducing labor costs by up to 60%, and waterless technologies addressing extreme water scarcity.

Key Market Segment Metrics (2026–2034)

| Category | Leading Segment (Base Position) | Fastest-Growing Segment |

|---|---|---|

| By Technology Type | Wet Cleaning Technology (dominated with 65.3% share) | Dry Cleaning Technology (projected to grow at a CAGR of 14.8% through 2034) |

| By Process / Equipment | Water Brushes (led process segments with a 45.3% share in 2025) | Automated Robotic Cleaning (expected to expand at a CAGR of 16.3%) |

| By Application & Surface | Utility-Scale Solar Parks and Arid Ground-Mounted Installations | Hydrophobic Self-Cleaning Coatings and Autonomous Waterless Systems |

| By Region / Country | Asia-Pacific (accounted for 42.7% share driven by China and India) and Middle East (34.8% share due to extreme dust) | Latin America and Arid Regions (accelerating interest in robotic alternatives due to water scarcity) |

Major Market Players & Market Structure

Market Structure: Highly competitive global solar operations and maintenance landscape where specialized robotics providers, tracker manufacturers, and coating innovators integrate autonomous solutions into utility-scale projects.

Key Companies: Boson Robotics Ltd., Ecoppia, Kärcher, Kashgar Solbright Photovoltaic Technology Co., Ltd., NOMADD, Premier Solar Cleaning LLC, Saint-Gobain Surface Conditioning, Serbot AG, Sharp Corporation, and SunBrush mobil GmbH.

Global Solar Panel Cleaning Market Size

The global solar panel cleaning market size was valued at USD 0.94 billion in 2025 and is anticipated to reach USD 1.06 billion in 2026 from USD 2.76 billion by 2034, growing at a CAGR of 12.72% during the forecast period from 2026 to 2034.

Solar Panel Cleaning includes services, technologies, and equipment designed to remove dust, pollen, bird droppings, and other particulate matter from photovoltaic (PV) surfaces to maintain optimal energy output. Accumulated soiling can significantly impair panel efficiency, particularly in arid, desert, and high-dust environments where natural rainfall is insufficient for self-cleaning. Furthermore, as per the World Bank’s Global Solar Atlas, areas with the highest solar irradiance, such as the Sahara, Thar, and Arabian deserts, also experience the most severe dust accumulation, creating a direct operational imperative for regular cleaning to safeguard energy yield and return on investment.

MARKET DRIVERS

The rapid expansion of utility-scale solar farms in arid and semi-arid regions, where dust accumulation poses a persistent threat to energy generation efficiency, is a primary driver of the Solar Panel Cleaning Market. In India, Rajasthan & Gujarat together account for the majority of India’s installed solar capacity. This operational necessity has led to the institutionalization of scheduled cleaning cycles, driving demand for mechanized and robotic solutions that can service thousands of panels efficiently and safely across vast desert installations.

The increasing integration of performance-based contracts and energy yield guarantees in solar project financing, which compel operators to maintain peak panel efficiency, is another significant driver. Failure to meet these targets can trigger financial penalties or loss of revenue under power purchase agreements. In Egypt, the New and Renewable Energy Authority mandates that independent power producers submit soiling mitigation plans as part of their project approvals. These contractual and regulatory frameworks transform panel cleaning from a maintenance task into a critical operational function, ensuring sustained investment in reliable, data-driven cleaning solutions.

MARKET RESTRAINTS

The scarcity of water in regions with the highest solar potential, making traditional water-based cleaning methods unsustainable and environmentally contentious, is a major restraint in the Solar Panel Cleaning Market. According to the United Nations Water Development Report, over 2 billion people live in countries experiencing high water stress, including key solar markets like Egypt, Iran, and Chile. Despite the availability of waterless alternatives, their higher upfront costs and limited scalability hinder widespread adoption, especially in budget-constrained projects, creating a critical sustainability dilemma.

The lack of standardized performance metrics and regulatory oversight for cleaning efficacy, leading to inconsistent service quality and difficulty in ROI assessment, is another critical restraint. Unlike electrical components, solar cleaning is rarely monitored with calibrated sensors or performance tracking protocols, making it challenging to quantify gains. In Europe, fewer solar operators in Southern Europe use soiling sensors to measure pre- and post-cleaning efficiency improvements. In India, the Central Electricity Authority has not established mandatory cleaning standards, allowing untrained laborers to perform cleaning using abrasive tools that can scratch anti-reflective coatings. Improper cleaning techniques reduced panel lifespan due to micro-abrasions. Without enforceable guidelines or certification for cleaning providers, asset owners face elevated risks of subpar service, equipment damage, and unverified performance claims, undermining trust in the sector.

MARKET OPPORTUNITIES

The development and deployment of autonomous robotic cleaning systems, particularly in large-scale desert solar parks where manual labor is inefficient and costly, is a transformative opportunity. Also, robotic cleaners can reduce labor costs by up to 60% while improving cleaning frequency and consistency. As per the U.S. Department of Energy, robotic systems can extend panel life by preventing uneven soiling and reducing human contact. With advancements in solar-powered robotics and edge computing, this segment is poised to redefine operational efficiency in utility-scale solar asset management.

The integration of hydrophobic and self-cleaning coatings into solar panel manufacturing, reducing the frequency and cost of manual intervention, is another emerging opportunity. These nanotechnology-based coatings repel dust and water, enabling rain or dew to wash away contaminants without human input. Companies like Saint-Gobain and 3M have commercialized such coatings, which can be applied during production or retrofitted. With panel manufacturers increasingly offering coated modules as standard, the market is shifting toward preventive maintenance, creating new revenue streams for chemical and materials innovators while reducing long-term cleaning dependency.

MARKET CHALLENGES

The risk of physical damage to solar panels during cleaning, particularly from improper tools, abrasive materials, or untrained personnel, is a major challenge in the Solar Panel Cleaning Market. Moreover, micro-scratches on anti-reflective coatings caused by improper wiping can reduce panel efficiency permanently. High-pressure water jets, commonly used in truck-mounted systems, can compromise sealants and lead to moisture ingress, accelerating delamination. Besides, walking on panels during rooftop cleaning, still practiced in some regions, increases the risk of cell fracture. These risks are exacerbated by the absence of formal training programs for cleaning crews, undermining system longevity and warranty compliance.

The seasonal and geospatial variability in soiling rates, which complicates the scheduling and economic justification of cleaning services, is another pressing challenge. Soiling is influenced by local conditions such as wind patterns, agricultural activity, construction dust, and bird migration, making uniform cleaning schedules inefficient. In addition, coastal solar installations in Chile experience salt deposition rather than dust, requiring different cleaning chemistries and frequencies. Without real-time monitoring and predictive analytics, operators face either over-cleaning, increasing costs and wear, or under-cleaning, sacrificing energy yield. This dynamic complexity demands intelligent, data-driven approaches that many current service providers are not equipped to deliver.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 12.72% |

| Segments Covered | By Technology, Process, Mode of Operation, Application, and Region. |

| Various Analyses Covered | Global, Regional and Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Boson Robotics Ltd., Ecoppia, Karcher, Kashgar Solbright Photovoltaic Technology Co., Ltd., NOMADD, Premier Solar Cleaning, LLC, Saint-Gobain Surface Conditioning, Serbot AG, Sharp Corporation, SunBrush Mobil GmbH, and Others. |

SEGMENTAL ANALYSIS

By Technology Insights

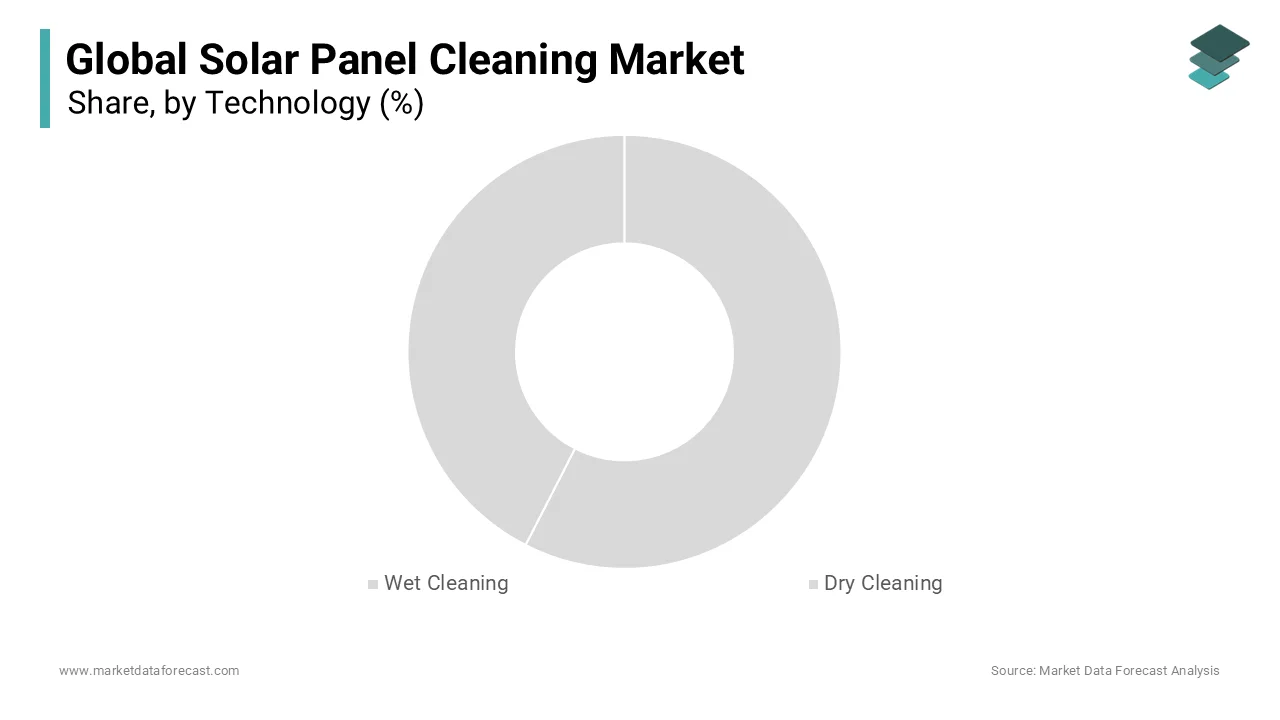

The wet cleaning segment dominated the solar panel cleaning market by capturing a 65.3% of the global share in 2024. This dominance is primarily driven by its widespread use in utility-scale and rooftop solar installations where visible soiling significantly impacts energy output. Wet cleaning methods, ranging from manual brushing with deionized water to automated truck-mounted systems, are favored for their proven effectiveness in removing stubborn contaminants such as cement dust, bird droppings, and pollen.

The dry cleaning segment is the fastest-growing and is projected to expand at a CAGR of 14.8% from 2026 to 2034. This is driven by escalating water scarcity and the rising adoption of waterless technologies in arid solar zones. Dry methods, particularly electrostatic and automated robotic systems, use air jets, soft brushes, or electrostatic repulsion to remove dust without water, making them ideal for desert environments. As per the United Nations Water Development Report, 17 countries, home to a quarter of the world’s population, face extreme water stress, including key solar markets like Saudi Arabia, Egypt, and Chile. With environmental regulations tightening and ESG pressures mounting, dry cleaning is emerging as a sustainable, long-term solution for large-scale solar asset operators.

By Process Insights

The water brushes segment led the market by accounting for 45.3% in 2025. This is due to its cost-effectiveness, simplicity, and broad applicability across diverse solar installations. This method involves the use of soft, rotating brushes combined with a flow of purified or deionized water to gently scrub panel surfaces, minimizing micro-scratching while ensuring thorough cleaning. Their scalability and proven reliability ensure continued dominance despite growing interest in waterless alternatives.

The automated robotic cleaning process is the fastest-growing and is expected to grow at a CAGR of 16.3% through 2033. It is fueled by the demand for precision, labor efficiency, and operational continuity in large-scale solar parks. These robots, either rail-mounted or autonomous, operate during non-peak hours, reducing downtime and eliminating the need for manual labor on elevated or hazardous surfaces. The U.S. Department of Energy shows that solar-powered robots eliminate grid dependency, making them ideal for remote installations. As AI and machine learning enhance navigation and soil detection, robotic cleaning is becoming the gold standard for high-efficiency solar asset management.

REGIONAL ANALYSIS

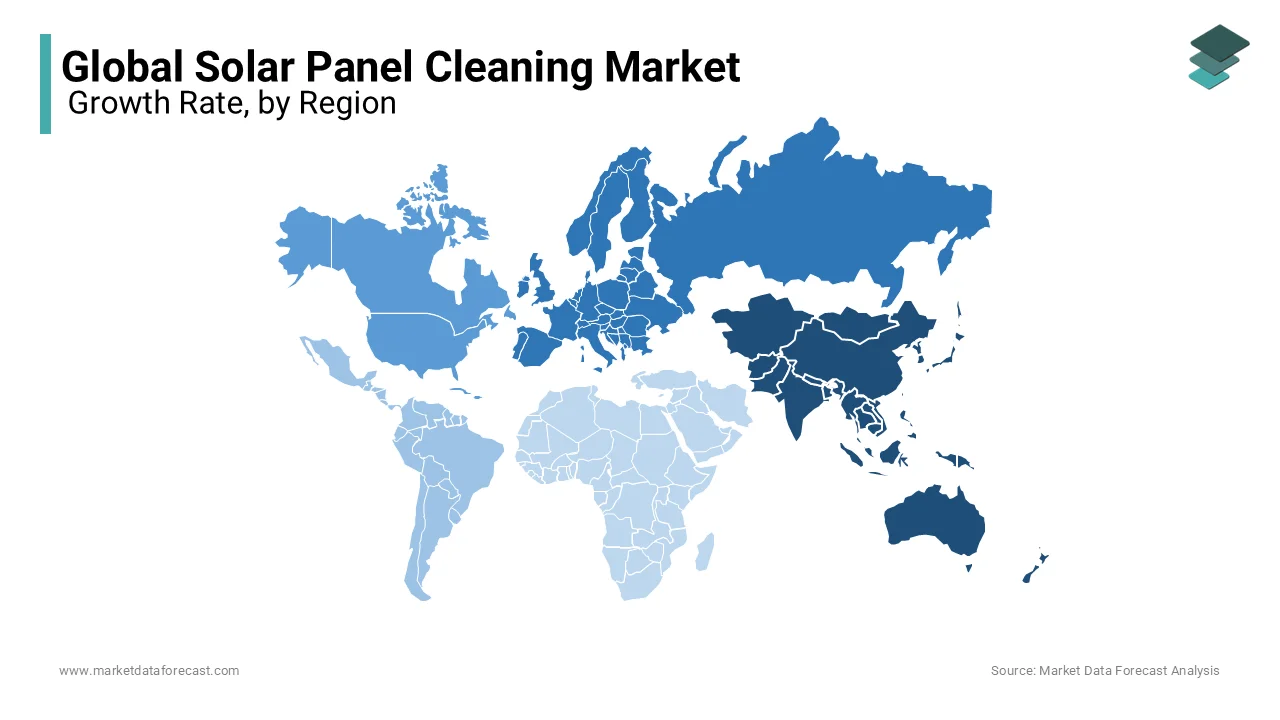

The Middle East commanded the global solar panel cleaning market by capturing a 34.8% in 2025, with Saudi Arabia and the UAE leading deployment due to extreme dust conditions and rapid solar expansion. The region’s vast desert terrain generates high particulate loads, with dust accumulation rates exceeding 0.5 grams per square meter per day. Saudi Arabia’s Vision 2030 includes a substantial investment in renewable energy, with over 40 GW of solar capacity planned, all requiring frequent cleaning. The UAE’s Ministry of Energy and Infrastructure mandates bi-weekly cleaning for all solar farms to maintain performance ratios. Dubai Electricity and Water Authority has integrated robotic and electrostatic cleaning into its Mohammed bin Rashid Al Maktoum Solar Park, the world’s largest single-site solar project. With water scarcity driving innovation in dry cleaning, the Middle East is at the forefront of developing sustainable, scalable cleaning solutions for harsh environments.

Asia Pacific accounts for a significant share of the market, with India, China, and Japan driving demand through aggressive renewable energy targets and large-scale solar deployments. India’s Ministry of New and Renewable Energy reports that over 70 GW of solar capacity is operational. In China, the National Energy Administration has installed over 400 GW of solar capacity, with desert projects in Ningxia and Qinghai relying on automated truck-mounted systems. Japan promotes water-efficient cleaning for rooftop installations in urban areas. With rising O&M standardization, the Asia Pacific is transitioning from manual to technology-driven cleaning models.

North America holds a notable share of the market, with the United States as the primary driver due to its extensive utility-scale solar infrastructure and growing focus on operational efficiency. As per the U.S. Energy Information Administration, solar capacity exceeded 100 GW in 2023, with major installations in California, Nevada, and Texas, regions prone to dust storms and low rainfall. Soiling losses in Arizona can reach a notable portion within a month without cleaning. California’s Independent System Operator mandates performance tracking for all solar farms, incentivizing regular maintenance. Companies like Nextracker and First Solar have integrated robotic cleaning into their solar park designs. The U.S. Department of Energy supports R&D in self-cleaning coatings and autonomous robots through its Solar Energy Technologies Office. With strong private investment and technological innovation, North America is advancing smart, data-driven cleaning solutions that optimize energy yield and reduce water use.

Europe is also a key player in the market, with Spain, Italy, and Germany leading in solar cleaning adoption due to expanding solar capacity and regulatory emphasis on energy efficiency. Spain saw solar power generation increase, with large farms in Andalusia and Extremadura facing significant dust accumulation from nearby agricultural activity. In Greece, the Regulatory Authority for Energy requires solar farms to submit soiling mitigation plans as part of licensing. The Fraunhofer Institute shows that robotic cleaning has reduced O&M costs in German agrivoltaic projects. With the EU’s Green Deal promoting sustainable operations, Europe is increasingly adopting water-efficient and low-impact cleaning technologies, particularly in water-stressed Mediterranean regions.

Latin America holds a small share of the market, with Chile, Brazil, and Mexico emerging as key adopters due to growing solar capacity and unique environmental challenges. Chile’s Atacama Desert hosts some of the world’s highest solar irradiance but also extreme dust and salt deposition from coastal winds. Soiling can reduce panel efficiency within weeks, necessitating frequent cleaning. In Brazil, the National Agency of Electric Energy (ANEEL) has approved over 15 GW of solar capacity, with rooftop and utility farms in the northeast requiring cleaning due to red dust and pollen. The Inter-American Development Bank notes that water scarcity in northern Mexico limits wet cleaning, accelerating interest in robotic and electrostatic alternatives. While adoption is still in early stages, increasing private investment and public-private partnerships are driving the deployment of mechanized cleaning systems, particularly in mining-linked solar projects requiring high reliability.

COMPETITIVE LANDSCAPE

The competitive landscape of the Solar Panel Cleaning Market is evolving into a bifurcated ecosystem where technological innovators and regional service providers compete on different value propositions. Global leaders focus on advanced robotics, AI integration, and waterless solutions, targeting large utility-scale projects with performance guarantees. Regional players dominate through cost-effective, adaptable systems suited for diverse climatic and economic conditions. Differentiation increasingly hinges on cleaning efficacy, water efficiency, and compatibility with next-gen solar modules. The absence of universal standards allows for fragmented service quality, but rising investor scrutiny on O&M performance is driving consolidation and standardization. As solar asset owners prioritize yield optimization and sustainability, competition is shifting from price to total lifecycle value, favoring companies that combine reliability, innovation, and environmental responsibility in their service offerings.

KEY MARKET PLAYERS

Companies playing a prominent role in the global solar panel cleaning market include

- Boson Robotics Ltd. (China)

- Ecoppia (Israel)

- Kärcher (Germany)

- Kashgar Solbright Photovoltaic Technology Co., Ltd. (China)

- NOMADD (Saudi Arabia)

- Premier Solar Cleaning, LLC (U.S.)

- Saint-Gobain Surface Conditioning (France)

- Serbot AG (Switzerland)

- Sharp Corporation (Japan)

- SunBrush mobil GmbH (Germany)

Top Players in the Solar Panel Cleaning Market

Ecoppia has emerged as a global leader in autonomous, water-free robotic cleaning, with growing influence across the Asia Pacific region through strategic partnerships and localized deployments. The company’s T-Series robots, which operate on solar-powered rails without water, have been adopted in India’s Bhadla Solar Park, the world’s largest, where dust accumulation can exceed 1.5 grams per square meter daily. The company also established a regional service hub in Hyderabad to support rapid maintenance and software updates. By aligning with India’s National Green Hydrogen Mission, which demands high solar uptime, Ecoppia is positioning its dry-cleaning technology as essential infrastructure for next-generation renewable projects. Its zero-water model resonates with regulators and investors focused on ESG compliance, particularly in water-stressed states.

Kärcher leverages its global reputation in cleaning technology to expand its footprint in the Asia Pacific solar panel cleaning market, offering integrated wet and semi-automated solutions tailored for diverse climates. The company has introduced specialized deionized water trucks and soft-brush systems for large-scale solar farms in China and Vietnam, where monsoon residue and industrial soot accelerate soiling. In Japan, the company launched a compact, rooftop-compatible cleaning unit for residential installations, addressing urban space constraints. Kärcher also conducted training programs for O&M teams in Thailand and Indonesia, enhancing service standardization. By combining decades of fluid dynamics expertise with localized product adaptation, Kärcher is establishing itself as a trusted provider of reliable, scalable cleaning solutions across commercial, utility, and residential segments in the region.

SunBrush is a regional innovator with deep penetration in India and Southeast Asia, specializing in cost-effective, semi-automated cleaning systems designed for high-dust environments. The company’s modular water brush units, mounted on electric or diesel carts, are widely used in Gujarat and Tamil Nadu solar parks, where frequent cleaning is mandated by grid operators. The company also introduced a real-time soiling monitoring add-on that alerts operators when cleaning thresholds are breached. Collaborating with the Solar Energy Corporation of India, SunBrush contributed to the development of O&M best practice guidelines. By focusing on affordability, durability, and ease of repair, SunBrush has become a preferred choice for mid-tier solar operators seeking reliable, low-tech solutions that balance performance and cost in challenging environmental conditions.

Top Strategies Used by Key Market Participants

Key players in the Solar Panel Cleaning Market are deploying technological innovation, strategic partnerships, and regional customization to strengthen their competitive positioning. Companies are investing in waterless robotic systems, AI-driven soiling prediction, and IoT-enabled monitoring to enhance efficiency and reduce operational costs. Expansion into high-growth regions like the Asia Pacific and the Middle East is being accelerated through joint ventures with local solar operators and O&M providers. Product diversification, including hybrid wet-dry systems and retrofit kits for existing farms, is enabling broader market penetration. Emphasis on sustainability, particularly zero-water cleaning, is aligning with ESG mandates and regulatory requirements. Additionally, firms are establishing regional service centers and training programs to ensure rapid deployment, maintenance, and compliance with local environmental and labor standards.

RECENT HAPPENINGS IN THE MARKET

- In January 2022, Ecoppia deployed 1,200 water-free robotic cleaners at India’s Bhadla Solar Park in collaboration with ReNew Power, enhancing cleaning efficiency and reducing water consumption.

- In June 2022, Kärcher partnered with Trina Solar to develop a non-abrasive cleaning protocol for high-efficiency bifacial solar modules, improving panel longevity.

- In March 2023, SunBrush launched a solar-powered cleaning trolley in India, reducing operational costs by 40% and increasing accessibility for mid-sized solar farms.

- In September 2023, Ecoppia established a service and maintenance hub in Hyderabad, strengthening its regional support network for robotic cleaning systems in South Asia.

- In April 2024, DynaTou Solar Panel Cleaning Marketch, a kiosk solutions provider, acquired KioWare, a kiosk management software company. This Solar Panel Cleaning Market acquisition is anticipated to allow DynaTouch to offer more comprehensive kiosk solutions and strengthen the Genomics Market's market presence.

MARKET SEGMENTATION

This research report on the global solar panel cleaning market has been segmented and sub-segmented based on technology, process, mode of operation, application, and region.

By Technology

- Wet Cleaning

- Automated

- Water Brushes

- Semi-Automated

- Dry Cleaning

- Electrostatic

- Automated Robotic

By Process

- Automated

- Semi-Automated

- Water Brushes

- Automated Robotic

- Electrostatic

By Mode of Operation

- Autonomous

- Manual

By Application

- Commercial

- Residential

- Industrial

- Utility

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa