Global SONAR Systems Market Size, Share, Trends, & Growth Forecast Report, Segmented by Application (Commercial, Military), System type (Single Beam Scanning Systems, Multi Beam Systems, Synthetic Aperture Systems and Others), Fit (Line-Fit, Retrofit), Components (Receiver, Transmitter, Hydrophone, Beam Forming Processor and Others), & Region, Industry Forecast From 2026 to 2034

Market Size, 2025

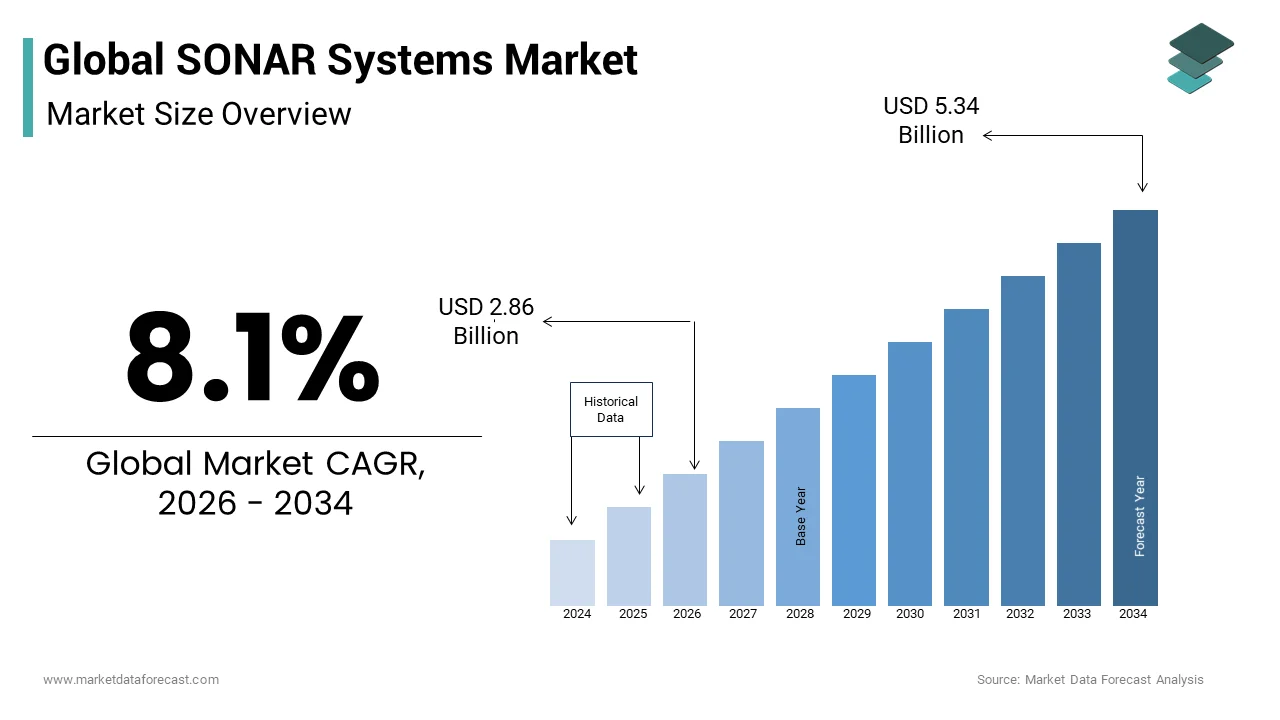

$2.65 BnMarket Estimate, 2026

$2.86 BnMarket Forecast, 2034

$5.34 BnCAGR, 2026–2034

8.1%Global SONAR Systems Market Size

The global SONAR systems market size was valued at USD 2.65 billion in 2025 and is anticipated to reach USD 2.86 billion in 2026 to reach USD 5.34 billion by 2034, growing at a compound annual growth rate (CAGR) of 8.1% during the forecast period from 2026 to 2034.

SONAR stands for Sound Navigation and Ranging, a technique used to detect objects above or below the surface of the water. It can be used for a variety of applications, such as military, commercial, scientific, fishing, hydrology, underwater warfare, and threat detection mines. SONAR systems are also used for robotic navigation and atmospheric navigation. They use very high acoustic frequencies. The side scan and the multi-beam SONAR are cutting-edge technologies that help in detailed mapping and obtaining seabed images.

MARKET DRIVERS

The growing number of maritime trade activities worldwide, the increasing demand for shipowners to comply with maritime safety standards, and the burgeoning marine tourism sector are majorly driving the growth of the

Governments and large corporations are investing heavily in this new technology, which could lead to the growth of the SONAR systems market. Innovation is expected to continue in the synthetic opening. SONAR leads the market to improve the quality of resolution for complementary applications and achieve several contracts. Some of the critical factors affecting the market are advances in underwater combat technology, the development of digital signal processing that has improved the handling and communications underwater, and the growing demand for Sonobu in operations of tactical defense and active development. The increase in investment in research, the use of unmanned underwater vehicles (UUVs), and the acquisition in recent years have greatly improved the market. UUV has become a platform for many commercial and military applications, including surveillance and mining measures. This is likely to stimulate the SONAR systems market in the future.

MARKET RESTRAINTS

The side effects on marine life due to the use of SONAR are a significant challenge in this market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 8.1% |

| Segments Covered | By Components, Application, System Type, Fit, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Thales Group, Kongsberg Gruppen, Lockheed Martin Corporation, Raytheon, Northrop Grumman Corporation, Aselsan AS, Atlas Elektronik GmbH, and others |

SEGMENTAL ANALYSIS

By Components Insights

The beam-forming processor sector covered the market, followed by the hydrophone, which is predicted to be dominant in the coming years.

By Application Insights

The military sector dominated the overall market, followed by the scientific division, which is projected to lead in the foreseeable future.

By System Insights

The multi-beam SONAR system segment dominated the market, followed by a single-beam system, and this segment is foreseen to be dominant in the estimated period.

By Fit Insights

The retrofit segment of the market is expected to have a higher CAGR than the line adjustment segment during the forecast period. As the number of renewal orders for existing commercial ships increases, the retrofit segment is growing.

REGIONAL ANALYSIS

North America Insights Market Analysis

North America's SONAR systems market was the leading market, followed by Europe. The United States is the dominant region in North America, as well as in the world. Improvements in sensor technology and passive and active SONAR are vital drivers of the SONAR systems market in the United States and North America.

Asia Pacific Insights Market Analysis

The Asia-Pacific SONAT systems market is likely to grow at the highest CAGR during the forecast period. China is expected to be an important market in the Asia-Pacific region. The growing demand for medical applications and the increasing demand for SONAR systems in tactical defense operations are a few key factors driving the demand for these systems in China, as well as in the Asia Pacific. The increasing use of SONAR systems, especially in a variety of applications, such as fishing, weapons, medical, and infrastructure research, supports the Indian market.

Europe Insights Market Analysis

Europe's Sonar systems market is anticipated to grow at a constant rate. The United Kingdom and Germany are the main markets for this industry in Europe. Latin America, the Middle East, and Africa are assumed to grow at a healthy pace during the forecast period. Saudi Arabia and the UAE are the main markets in the Middle East and Africa. In a variety of applications, such as defense, medicine, and research, the growing demand for SONAR systems is one of the key factors driving demand in the Middle East and Africa markets.

KEY MARKET PLAYERS

Companies such as

- Thales Group

- Kongsberg Gruppen

- Lockheed Martin Corporation

- Raytheon

- Northrop Grumman Corporation

- Aselsan AS

- Atlas Elektronik GmbH

Kongsberg Gruppen offers advanced technology systems to customers in the maritime, oil and gas, aerospace, and defense industries. The company provides offshore engine monitoring systems through the Kongsberg Offshore Division. Raytheon is one of the largest defense contractors in the world and serves government and commercial clients.

RECENT MARKET NEWS

-

In June 2019, the experts of the Atlantic Underwater War (ASW) of the US Navy. They ordered a trailer surface ship probe system to help warships track silent enemy submarines on different seabeds.

-

In 2019, Ultra Electronics Maritime Systems announced that it would build and integrate low-frequency active and passive traction array SONAR systems and next-generation hull-mounted SONAR mounted on future Canadian surface combat ships (CSC).

-

In July 2018, the Navy ordered a TB-29X Advanced Tow Array probe system for the US Navy submarine from L-3 Chesapeake Sciences Corp.

-

In 2018, Kongsberg Gruppen signed an agreement to supply five autonomous HUGIN water vehicle systems from Ocean Infinity.

-

In 2018, the Indian Navy announced that it would receive six low-frequency active traction matrix (ACTAS) SONAR systems from Germany, which would be installed in the new Kamorta-class Corvette.

MARKET SEGMENTATION

This research report on the global SONAR systems market has been segmented and sub-segmented based on the components, application, system type, fit, and region.

By components

- Receivers

- Transmitters

- Hydrophones

- Beam-Forming Processors

By Application

- Military

- Commercial

- Scientific Applications

By System type

- Single-Beam Scanning System

- Multi-Beam System

- Synthetic Opening System

- Others

By Fit

- Line-Fit

- Retrofit

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

How big is the global SONAR systems market expected to become in the coming years?

The market is expected to witness robust growth as naval modernization programs, maritime surveillance requirements, and underwater exploration activities continue to expand worldwide.

Why are SONAR systems critical for modern naval and maritime operations?

SONAR systems enable the detection, tracking, and identification of underwater objects, helping naval forces and maritime operators enhance security, navigation, and operational effectiveness.

What is a SONAR system and what are its primary applications?

A SONAR system uses acoustic waves to detect and locate underwater objects and is widely used in defense, commercial shipping, fisheries, oceanography, offshore energy, and underwater research.

Which SONAR technology segment leads the market?

Active SONAR systems account for a significant market share due to their ability to transmit sound pulses and accurately detect underwater targets over long distances.

How do SONAR systems support underwater surveillance and threat detection?

They provide real-time monitoring, submarine tracking, mine detection, seabed mapping, and underwater obstacle identification, improving situational awareness in marine environments.

What industries are generating the strongest demand for SONAR systems?

Defense and naval sectors generate the highest demand, followed by offshore oil and gas, marine research, commercial shipping, fisheries, and underwater infrastructure inspection industries.

What emerging technologies are shaping the future of the SONAR systems market?

Artificial intelligence, autonomous underwater vehicles (AUVs), synthetic aperture SONAR, advanced signal processing, and high-resolution imaging technologies are shaping the future of the market.

Why are governments increasing investments in advanced SONAR capabilities?

Governments are strengthening maritime security, protecting coastal borders, enhancing anti-submarine warfare capabilities, and supporting strategic naval operations.

What challenges could affect the growth of the SONAR systems industry?

High development and deployment costs, environmental concerns regarding underwater acoustics, complex operating conditions, and maintenance requirements could affect market growth.

Which regions are expected to dominate the SONAR systems market?

North America remains a leading market due to strong defense spending, while Europe and Asia Pacific are experiencing significant growth through naval expansion and maritime security investments.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com