Global Surgical Lasers Market Size, Share, Trends & Growth Forecast Report By Product Type (Carbon dioxide (CO2) Lasers, Nd: YAG Lasers and Argon Lasers), Procedures (Laparoscopic Surgery, Open Surgery and Percutaneous Surgery), Application (Dentistry, Ophthalmology, Dermatology, Gynecology, Cardiology, Oncology and Urology ) and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa), Industry Analysis From 2026 to 2034

Global Surgical Lasers Market Size

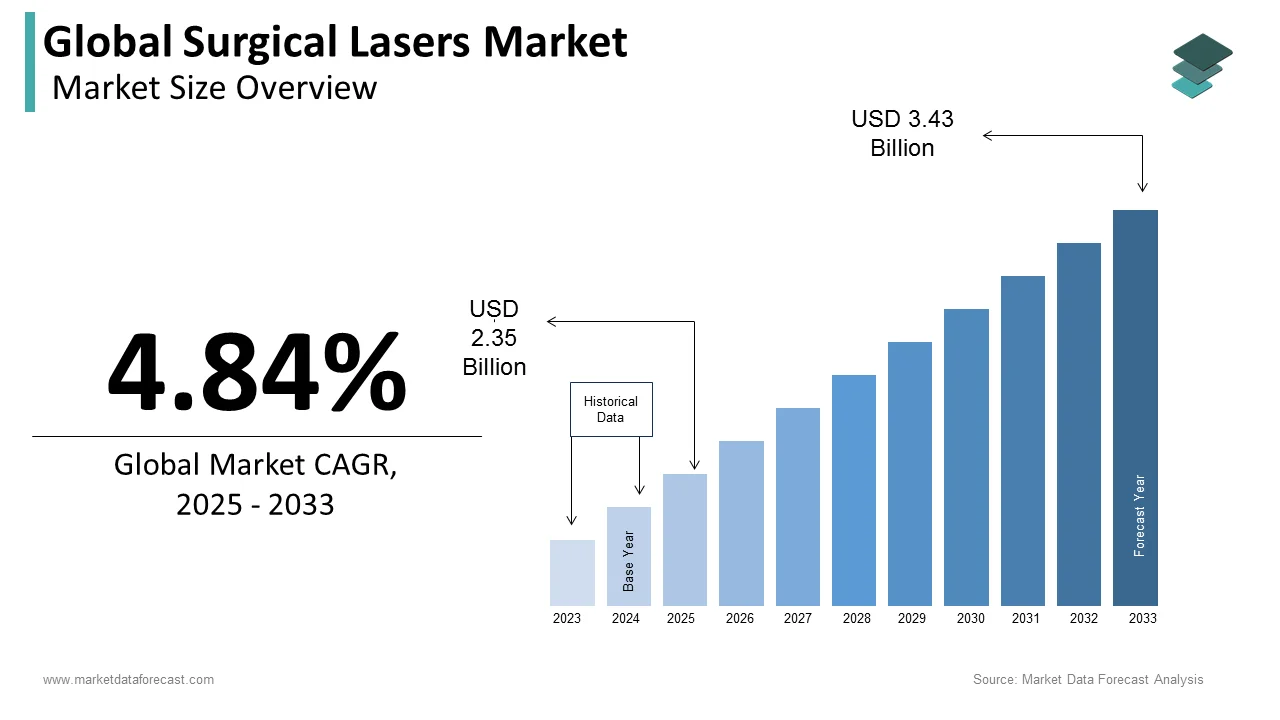

The global surgical lasers market size was valued at 2.35 billion in 2025. The global market is further expected to reach USD 3.60 billion by 2034 from USD 2.46 billion in 2026, growing at a CAGR of 4.84% during the forecast period.

Surgical lasers are specialized medical instruments that use an intense, focused beam of light to perform surgical procedures instead of traditional scalpels or cutting tools. These devices utilize coherent electromagnetic radiation to cut, coagulate, vaporize, or ablate biological tissues with exceptional spatial accuracy. The clinical foundation of this sector rests upon the growing integration of optical technologies into modern operative protocols. Global surgical tracking records that approximately 310 million major operations are performed around the world each year, while the Lancet Commission on Global Surgery highlights that an additional 143 million procedures are still urgently required in low- and middle-income countries to address structural access inequities. According to clinical literature supported by the American College of Surgeons, advanced energy-based modalities and minimally invasive surgical techniques are heavily incorporated into elective workflows to significantly mitigate intraoperative hemorrhage and accelerate postoperative recovery. Furthermore, the World Health Organization's International Classification of Health Interventions (ICHI) provides a standardized framework to code specialized medical and surgical processes, mapping energy and laser applications as procedural actions across subspecialties like ophthalmology, urology, and dermatology. Hospital procurement committees increasingly prioritize these systems due to their capacity to minimize collateral tissue damage and enhance operative field visibility. The regulatory framework governing these instruments mandates rigorous validation of wavelength specificity, pulse duration, and fiber delivery mechanisms to ensure patient safety. As clinical training programs integrate optical curricula into surgical residencies, the operational paradigm continues shifting toward technology-driven precision rather than conventional mechanical dissection. This evolution establishes a robust infrastructure for sustained clinical adoption and technological refinement across contemporary medical environments.

MARKET DRIVERS

Escalating prevalence of chronic pathologies necessitates precision-focused therapeutic interventions

The expanding global burden of chronic diseases directly stimulates clinical demand for photonic surgical platforms, which drives the growth of the surgical lasers market. According to the World Health Organization, non-communicable chronic conditions account for approximately 74% of all mortality worldwide, creating substantial and compounding requirements for specialized operative and medical care across global health infrastructure. The International Diabetes Federation documents that 537 million adults currently manage diabetes mellitus, with diabetic retinopathy representing the leading cause of vision impairment requiring laser photocoagulation. Clinical facilities experience consistent procedural volume growth as vascular complications demand targeted endovascular laser ablation and tissue remodeling techniques. The National Institutes of Health confirms that minimally invasive photothermal therapies significantly reduce overall patient recovery windows and shorten post-operative hospitalization periods when directly compared to traditional open surgery protocols. This efficiency metric drives institutional procurement as healthcare administrators optimize bed turnover and allocate resources toward high-volume chronic disease management. Furthermore, international health tracking reports that cardiovascular diseases claim approximately 18 to 19 million lives annually, with specialized modalities like laser-guided atherectomy and plaque vaporization serving as critical secondary interventional pathways for complex, heavily calcified blockages. The compounding effect of aging demographics and metabolic syndrome prevalence ensures sustained procedural demand. Surgical departments consequently prioritize wavelength-specific delivery systems to address complex tissue pathologies while maintaining economic viability through accelerated patient discharge cycles.

Technological miniaturization and flexible fiber delivery expand clinical accessibility across diverse specialties

Engineering innovations in photonic transmission mechanisms fundamentally alter how medical institutions integrate laser systems into routine workflows, which further boosts the expansion of the surgical lasers market. According to clinical optics and photonics assessments, advancements in flexible silica fiber optics have heavily expanded the scope of surgical tools, allowing high-power medical laser beams to safely navigate complex, tortuous anatomical pathways without compromising coherence. This structural advancement enables practitioners to deploy photonic energy in previously inaccessible regions such as the biliary tract, bronchial passages, and microvascular networks. The United States Food and Drug Administration regularly reviews and clears multi-functional medical laser platforms, reflecting a steady baseline of commercialization for advanced clinical tabletop and handheld configurations across multiple outpatient specialties. Orthopedic and dental practitioners specifically leverage these compact architectures to perform osseous ablation and soft tissue contouring within ambulatory surgery centers. According to clinical device deployment trends, outpatient procedural facilities have steadily transitioned from bulk optical mirrors and manual alignment systems to integrated, plug-and-play fiber-connected laser modules to minimize maintenance requirements and enhance system mobility. This migration reduces capital expenditure barriers and eliminates complex alignment protocols that previously restricted laser adoption to tertiary academic hospitals. Consequently, surgical teams achieve faster setup times and broader procedural versatility across multiple anatomical regions without requiring specialized engineering support.

MARKET RESTRAINTS

Substantial capital investment and ongoing maintenance expenses restrict widespread institutional deployment

The financial architecture required to acquire and sustain surgical laser systems is a formidable barrier for resource-limited healthcare facilities and the growth of the surgical lasers market. According to World Bank development indicators, public healthcare spending in many low- and lower-middle-income nations remains heavily constrained, leaving limited fiscal headroom for high-cost specialized medical equipment and photonic infrastructure. The initial procurement price for a high-output, specialized clinical surgical laser frequently spans tens to hundreds of thousands of dollars, depending on the required power output, wave modulation, and endoscope delivery configuration. Annual service contracts, regulatory safety calibrations, and routine fiber component replacements impose predictable, recurring expenditures typically equivalent to a notable percentage of the original capital outlay. According to health economic assessments, regional hospitals in resource-constrained environments frequently prioritize frontline pharmaceutical procurement and primary care staffing over capital upgrades for high-end interventional energy devices. Consequently, clinical procurement committees frequently revert to conventional electrocautery and mechanical resection tools despite the documented superiority of photonic tissue management in reducing operative hemorrhage. The financial strain extends to specialized personnel training as manufacturers mandate certified operator programs that require dedicated simulation modules and continuous competency assessments. This economic reality suppresses market penetration in geographies where surgical volume remains high but institutional liquidity remains severely constrained.

Rigorous regulatory compliance frameworks and extended approval cycles delay product commercialization

The stringent oversight governing photonic medical devices imposes substantial temporal and financial burdens on manufacturers seeking market entry, which hampers the expansion of the surgical lasers market. According to FDA performance updates, high-risk Class III Premarket Approval pathways require extensive clinical testing data, resulting in longer review periods and detailed technical revisions before securing final commercial clearance. The European Union Medical Device Regulation has intensified clinical evidence mandates, requiring manufacturers to produce more rigorous real-world procedural outcome data and post-market safety tracking to achieve or retain CE certification. These regulatory expectations demand extensive multiple-center clinical trials, histopathological validation studies, and extended safety monitoring protocols before commercial distribution becomes permissible. Medical device data reveals that novel laser platforms frequently require technical adjustments during the validation phase to safely satisfy stringent international biocompatibility and electromagnetic compatibility standards. Consequently, complex medical device launch timelines frequently fall behind original commercial projections, forcing manufacturing firms to absorb extended research and administrative overhead expenditures before realizing steady clinical revenue. This prolonged validation cycle particularly disadvantages emerging technology firms that lack the financial reserves to sustain extended regulatory engagements. The cumulative effect restricts the velocity of innovation diffusion and delays clinical access to advanced wavelength configurations across global healthcare networks.

MARKET OPPORTUNITIES

Rapid proliferation of ambulatory surgical facilities creates demand for compact photonic platforms

The structural transition toward outpatient procedural delivery fundamentally reshapes procurement priorities within modern healthcare delivery networks, which is expected to fuel the growth of the surgical lasers market. According to the Ambulatory Surgery Center Association, the footprint of Medicare-certified outpatient facilities expands steadily across the United States, driving high-volume growth as procedures migrate from hospital operating rooms to specialized surgical centers. These environments prioritize space-optimized equipment configurations that maintain clinical efficacy without requiring dedicated infrastructure modifications or specialized utility connections. Compact laser systems align perfectly with these operational parameters as they eliminate the need for centralized gas supplies, chilled water cooling loops, or reinforced flooring. As per the Centers for Medicare & Medicaid Services, individual laser-based urological and dermatological procedures are assigned standardized ambulatory payment classifications, which incentivise facility administrators to leverage mobile or outpatient surgical settings depending on localized cost structures. Furthermore, according to orthopaedic clinical literature, minimally invasive joint procedures conducted in outpatient settings rely on advanced energy-based modalities and arthroscopic tools to minimize tissue damage, reduce post-operative edema, and accelerate functional recovery. This clinical preference drives manufacturers to engineer modular delivery carts and lightweight handheld emitters that integrate seamlessly into high-throughput surgical schedules. The convergence of favorable reimbursement policies and spatial optimization requirements establishes a lucrative commercial pathway for upcoming portable laser configurations.

Artificial intelligence integration enables instantaneous tissue analysis and automated parameter optimization

The convergence of computational algorithms and photonic delivery systems introduces unprecedented precision control during complex operative interventions, which provides promising prospects for the expansion of the surgical lasers market. According to biomedical engineering research, machine learning models paired with advanced optical sensors demonstrate the capacity to track tissue optical property changes in real time, allowing for the automated adjustment of energy density to prevent overheating. The integration of automated computational feedback loops into advanced surgical systems has been shown to minimize collateral thermal damage to surrounding tissue compared to manual operator parameter adjustments. As per the National Institute of Biomedical Imaging and Bioengineering, spectral reflectance mapping and optical diagnostics are being advanced to help clinicians non-invasively differentiate between pathological and healthy tissue structures in real time. Clinical trials evaluating smart parameter optimization indicate that real-time surgical guidance significantly enhances workflow efficiency and reduces total procedural durations while maintaining precise tissue coagulation margins. Furthermore, studies evaluating surgical ergonomics document that surgeon-controlled artificial intelligence interfaces optimize human-machine interaction, reducing mental fatigue and tracking cognitive workload during complex ablation sequences. These performance metrics stimulate institutional interest in advanced photonic consoles that merge automated safety protocols with precision tissue targeting. The continuous refinement of diagnostic algorithms ensures that future laser architectures will achieve autonomous tissue characterization and dynamic energy deployment.

MARKET CHALLENGES

Inadequate clinical training infrastructure limits proficient utilization of advanced photonic systems

The effective deployment of surgical lasers requires comprehensive technical expertise that current medical education frameworks frequently fail to deliver, and thereby hold back the expansion of the global surgical lasers market. According to the Association of American Medical Colleges (AAMC), the projected total US physician deficit is estimated to reach up to 86,000 practitioners by 2036, intensifying competition for specialized operative and medical talent. Surgical residency programs focus primarily on core open and laparoscopic competencies, leaving advanced photonic and laser instrumentation training to vary by institution and subspecialty fellowship tracks. This fragmented training landscape generates inconsistent clinical competency and elevates the risk of procedural complications such as unintended tissue perforation or inadequate hemostasis. Furthermore, the Accreditation Council for Graduate Medical Education (ACGME) mandates access to adequate simulation resources for surgical training, though the specific availability of specialized laser simulation technology depends on local hospital funding. Consequently, healthcare administrators encounter significant operational delays as newly recruited personnel undergo extended credentialing processes before achieving independent procedural authorization. The persistent educational deficit constrains equipment utilization rates and diminishes return on investment for facilities seeking to maximize surgical throughput through optical technology.

Elevated safety protocols and complication risks necessitate rigorous operational safeguards

The inherent physical properties of concentrated electromagnetic radiation demand stringent environmental controls and continuous monitoring during operative applications, which inhibits the expansion of the surgical lasers market. According to The Joint Commission, medical-device-related adverse events, including rare laser-induced surgical fires, remain critical targets for institutional safety protocols and root-cause analyses. These occurrences primarily stem from reflective beam deflection, improper protective eyewear compliance, or inadequate tissue cooling mechanisms during prolonged ablation sequences. The American National Standards Institute (ANSI Z136.3) establishes comprehensive guidelines for clinical laser environments, including the appointment of a Laser Safety Officer and specialized beam barriers, which are enforced by workplace safety regulators. Procedural data indicate that collateral thermal injury remains an inherent risk during high-energy urological and neurosurgical interventions, requiring precise visual tracking despite standardized operating protocols. This risk profile forces institutions to implement redundant safety engineering controls that increase operational overhead and extend procedural setup durations. Furthermore, liability insurance underwriting for surgical facilities evaluates the elevated clinical risks associated with energy-based devices, adjusting institutional risk profiles based on safety compliance and specialty mix. The persistent requirement for exhaustive safety documentation and continuous environmental monitoring creates operational friction that discourages rapid procedural adoption in high-volume surgical departments.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Procedure Type, Application, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | Abbott Laboratories, BISON MEDICAL Co., Ltd. (South Korea), Fotona d.o.o. (Slovenia), Lumenis(Israel), Cynosure, Alma Lasers (Israel), IPG Photonics Corporation (U.S.), Boston Scientific Corporation (U.S.), Spectranetics Corporation (U.S.), Biolitec AG (Austria) |

SEGMENTAL ANALYSIS

By Product Insights

The carbon dioxide lasers segment dominated the surgical lasers market and accounted for a share of 26.5% share in 2025. This dominance of the segment was driven by its unparalleled precision in soft tissue ablation and exceptional hemostatic control during delicate procedures. The physical property allows surgeons to perform controlled tissue removal in otolaryngology, gynecology, and dermatology procedures while preserving adjacent healthy structures. Hospital procurement committees prioritize these systems because they support complex resections in confined anatomical spaces such as the larynx or cervical canal. Clinical training programs increasingly incorporate carbon dioxide laser modules into surgical residencies, ensuring consistent operator competency. The convergence of proven clinical outcomes and expanding procedural indications sustains robust institutional demand across advanced healthcare systems.

The breadth of clinical utility enables hospitals to maximize return on investment through high equipment utilization rates across diverse departments. Also, the performance metrics drive continued adoption in both academic medical centers and community hospitals. Manufacturers further enhance appeal through integrated scanning attachments and fiber delivery options that expand procedural flexibility. The cumulative effect of clinical versatility, regulatory endorsement, and procedural efficiency solidifies carbon dioxide lasers as the foundational technology within contemporary surgical laser portfolios.

On the other hand, the diode lasers segment is likely to experience the fastest CAGR of 12.2% from 2026 to 2034 due to its compact architecture, energy efficiency, and expanding clinical indications across outpatient settings. Diode lasers align perfectly with these operational parameters as they eliminate the need for external gas supplies or complex cooling systems. The efficiency metric drives adoption in high-volume dental and dermatology practices. Consequently, surgical teams achieve faster setup times and broader procedural versatility without requiring specialized engineering support. The convergence of favorable reimbursement policies, spatial optimization requirements, and energy efficiency establishes a lucrative commercial pathway for diode laser configurations. The structural advancement enables practitioners to deploy photonic energy in previously inaccessible regions such as the biliary tract, bronchial passages, and microvascular networks. Urological and ENT practitioners specifically leverage these compact architectures to perform soft tissue contouring within ambulatory surgery centers. This migration reduces capital expenditure barriers and eliminates complex alignment protocols that previously restricted laser adoption to tertiary academic hospitals. Consequently, surgical teams achieve faster setup times and broader procedural versatility across multiple anatomical regions without requiring specialized engineering support.

By Procedure Type Insights

The laparoscopic surgery segment led the surgical lasers market and captured a 38.5% share in 2025. This leading position of the segment was attributed to the global transition toward minimally invasive interventions that prioritize patient recovery and procedural efficiency.

According to clinical outcome studies supported by the American College of Surgeons, transitioning from traditional open surgery to minimally invasive laparoscopic procedures significantly reduces overall hospitalization periods, maximizing bed turnover and resource optimization. Clinical surgical literature indicates that minimally invasive photothermal therapies significantly decrease overall postoperative complication rates and wound-related morbidity while maintaining equivalent therapeutic efficacy to open approaches. This clinical advantage drives institutional procurement as healthcare administrators balance quality metrics with economic sustainability. Furthermore, the World Health Organization's International Classification of Health Interventions (ICHI) provides a standardized framework to code specialized medical and surgical processes, mapping energy and laser applications as procedural actions across expanding minimally invasive subspecialties. Hospital procurement committees increasingly prioritize laser-integrated laparoscopic platforms due to their capacity to minimize collateral tissue damage and enhance operative field visibility. The regulatory framework governing these instruments mandates rigorous validation of wavelength specificity, pulse duration, and fiber delivery mechanisms to ensure patient safety. As clinical training programs integrate optical curricula into surgical residencies, the operational paradigm continues shifting toward technology-driven precision rather than conventional mechanical dissection. This evolution establishes a robust infrastructure for sustained clinical adoption and technological refinement across contemporary medical environments. These performance metrics stimulate institutional interest in advanced photonic consoles that merge automated safety protocols with precision tissue targeting. The continuous refinement of diagnostic algorithms ensures that future laparoscopic laser architectures will achieve autonomous tissue characterization and dynamic energy deployment. Consequently, healthcare facilities experience improved procedural throughput and enhanced patient satisfaction scores, reinforcing sustained investment in laser-integrated minimally invasive platforms.

But the percutaneous surgery segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 12.4% during the forecast period. This accelerated expansion of the segment is propelled by increasing adoption of image-guided interventions that minimize tissue trauma and accelerate functional recovery. According to the Society of Interventional Radiology, percutaneous laser ablation utilizing real-time ultrasound or computed tomography guidance provides high targeting precision, enabling the safe and effective destruction of deep-seated lesions. Studies published in the American Journal of Roentgenology confirm that laser-assisted percutaneous thermal interventions provide excellent intraoperative hemostasis, minimizing local bleeding risks compared to mechanical cutting techniques. This clinical advantage drives adoption in oncology, urology, and vascular specialties where precise tissue management is critical. Furthermore, according to oncological and urological data, percutaneous thermal ablation (such as cryoablation and radiofrequency ablation) achieves exceptionally high complete tumor eradication rates for small renal masses under 3 centimeters with minimal impact on long-term renal function. These outcomes support expanded clinical indications and favorable reimbursement classifications. Hospital administrators prioritize percutaneous laser platforms because they enable same-day discharge protocols, reducing facility costs and improving patient satisfaction. The convergence of imaging advancements, laser precision, and favorable clinical outcomes establishes percutaneous approaches as a cornerstone of contemporary interventional medicine. The clinical validations drive referral patterns and institutional investment in dedicated interventional suites. Manufacturers enhance appeal through modular platforms that support multiple wavelength configurations, enabling practitioners to address diverse pathological conditions. The cumulative effect of expanding indications, proven efficacy, and favorable safety profiles sustains robust growth in percutaneous laser procedural volume across advanced healthcare systems.

By Application Insights

The oncology segment held the majority share of 34.6% of the surgical lasers market in 2025 because of the critical role of photonic technologies in precise tumor ablation and palliative interventions across multiple cancer types. According to the American Cancer Society, over 1.9 million new cancer diagnoses occur annually in the United States, with a significant proportion requiring surgical intervention. The National Comprehensive Cancer Network (NCCN) guidelines endorse thermal ablation modalities, primarily Radiofrequency Ablation (RFA) and Microwave Ablation (MWA), for early-stage malignancies in organs like the liver, due to their ability to achieve complete tumor destruction with low morbidity. Clinical oncology studies indicate that utilizing advanced energy-based surgical tools and intraoperative imaging options helps minimize positive margin rates during complex tumor resections, supporting lower localized recurrence. Furthermore, the World Health Organization observes that photothermal therapies enable outpatient management of superficial skin cancers, reducing the healthcare system burden. Hospital oncology departments prioritize laser platforms because they support complex resections in anatomically challenging locations while preserving critical structures. The regulatory framework governing these instruments mandates rigorous validation of energy delivery parameters to ensure consistent therapeutic outcomes. As multidisciplinary tumor boards increasingly incorporate laser ablation into treatment algorithms, the operational paradigm continues shifting toward precision photonic interventions. This evolution establishes a robust infrastructure for sustained clinical adoption and technological refinement across contemporary cancer care environments. The efficiency metric drives institutional procurement as healthcare administrators balance quality metrics with economic sustainability. Hospital procurement committees increasingly prioritize these integrated systems due to their capacity to standardize procedural execution across surgical teams. The continuous refinement of haptic feedback and real-time imaging ensures that future robotic laser architectures will achieve autonomous tissue characterization and dynamic energy deployment. Consequently, healthcare facilities experience improved procedural throughput and enhanced patient satisfaction scores, reinforcing sustained investment in advanced photonic oncology platforms.

On the contrary, the dentistry segment is expected to exhibit a noteworthy CAGR of 11.9% over the forecast period, owing to increasing adoption of laser technologies for soft tissue management and minimally invasive restorative procedures. According to dental industry analysis, diode and erbium laser systems are experiencing expanding adoption among dental practitioners as useful technical additions for precise gingival contouring, frenectomy, and biopsy procedures. The Journal of Oral and Maxillofacial Surgery documents that laser-assisted soft-tissue interventions minimize postoperative pain scores and bleeding compared to conventional scalpel techniques while accelerating early wound-healing timelines. This clinical advantage drives adoption in high-volume practices where patient satisfaction and chairside efficiency are critical. Furthermore, according to clinical dental research, laser-based periodontal therapies can successfully achieve significant pocket depth reduction and attachment gains in moderate periodontitis cases with minimal risk of gingival recession. These outcomes support expanded clinical indications and favorable reimbursement classifications. Dental practitioners prioritize laser platforms because they enable bloodless operative fields and reduced need for sutures, simplifying procedural workflows. The convergence of proven clinical outcomes, patient preference for minimally invasive care, and favorable practice economics establishes dentistry as a high-growth application segment within the surgical lasers market. Furthermore, the clinical validations drive referral patterns and institutional investment in dedicated laser suites. Manufacturers enhance appeal through compact handheld designs that integrate seamlessly into existing operatory layouts. The cumulative effect of expanding indications, proven efficacy, and favorable safety profiles sustains robust growth in dental laser procedural volume across advanced healthcare systems.

REGIONAL ANALYSIS

North America Surgical Lasers Market Analysis

North America was the top performer in the global surgical lasers market and accounted for a 44.7% share in 2025. This supremacy of the North American market was supported by advanced healthcare infrastructure, favorable reimbursement policies, and early adoption of precision surgical technologies across the region. According to the Centers for Medicare & Medicaid Services, individual laser-based urological and dermatological procedures are assigned standardized ambulatory payment classifications, which incentivise healthcare systems to leverage mobile or outpatient surgical settings depending on localized cost structures. According to hospital infrastructure trends, the vast majority of tertiary care centers in the United States maintain multi-modality operating rooms equipped with portable medical laser platforms to support intricate oncological and ophthalmological workflows. This institutional commitment drives consistent equipment refresh cycles and technology upgrades. Furthermore, the United States Food and Drug Administration regularly reviews and clears multi-functional medical laser platforms, reflecting a steady baseline of commercialization for advanced clinical photonic systems across multiple specialties. Hospital procurement committees prioritize laser-integrated platforms due to their capacity to minimize collateral tissue damage and enhance operative field visibility. The regulatory framework governing these instruments mandates rigorous validation of wavelength specificity, pulse duration, and fiber delivery mechanisms to ensure patient safety. As clinical training programs integrate optical curricula into surgical residencies, the operational paradigm continues shifting toward technology-driven precision rather than conventional mechanical dissection. This evolution establishes a robust infrastructure for sustained clinical adoption and technological refinement across contemporary medical environments in North America.

According to the National Institutes of Health, over 200 active clinical trials currently evaluate novel laser applications across oncology, ophthalmology, and neurosurgery in the United States alone. This research output drives evidence-based guidelines and accelerates technology diffusion across community hospitals. Furthermore, the Biomedical Advanced Research and Development Authority allocates substantial funding for photonic device development, supporting next-generation laser platforms. Hospital administrators prioritize institutions with strong research affiliations because they gain early access to innovative technologies and specialized training programs. The convergence of robust research ecosystems, favorable regulatory pathways, and strong commercial infrastructure establishes North America as the innovation hub for the global surgical lasers market. Consequently, healthcare facilities experience improved procedural outcomes and enhanced patient satisfaction scores, reinforcing sustained investment in advanced photonic platforms.

Europe Surgical Lasers Market Analysis

Europe was positioned second by capturing a 30.7% share of the global surgical lasers market in 2025. This growth of the European market was driven by well-established healthcare systems, strong emphasis on advanced surgical practices, and harmonized regulatory frameworks across the region. Under the European Union's Medical Device Regulation (MDR), standardized and heightened clinical evidence requirements are enforced for laser systems through Notified Bodies, aiming to ensure safety and clinical efficacy across all member states. The European Board of Surgery establishes rigorous post-graduate fellowship frameworks, where specialized training in advanced energy devices and photonic instrumentation is increasingly utilized across distinct urological and ophthalmic subspecialties. This educational commitment ensures consistent operator competency and safe procedural execution. Furthermore, according to the Organisation for Economic Co-operation and Development (OECD), total healthcare expenditure among member nations averages approximately 8.8% of GDP, providing robust financial backing for public and private medical technology procurement. Hospital procurement committees prioritize laser-integrated platforms due to their capacity to minimize collateral tissue damage and enhance operative field visibility. The regulatory framework governing these instruments mandates rigorous validation of wavelength specificity, pulse duration, and fiber delivery mechanisms to ensure patient safety. As clinical training programs integrate optical curricula into surgical residencies, the operational paradigm continues shifting toward technology-driven precision rather than conventional mechanical dissection. This evolution establishes a robust infrastructure for sustained clinical adoption and technological refinement across contemporary medical environments in Europe.

The European Cancer Organisation documents that over 3.5 million new cancer diagnoses occur annually across the region, with a significant proportion requiring surgical intervention. The International Diabetes Federation confirms that 61 million adults in Europe currently manage diabetes mellitus, with diabetic retinopathy representing a leading cause of vision impairment requiring laser photocoagulation. Clinical facilities experience consistent procedural volume growth as vascular complications demand targeted endovascular laser ablation and tissue remodeling techniques. Hospital administrators prioritize laser platforms because they support complex resections in anatomically challenging locations while preserving critical structures. The convergence of demographic shifts, disease burden, and clinical efficacy sustains robust demand for surgical lasers across European healthcare systems. Consequently, healthcare facilities experience improved procedural throughput and enhanced patient satisfaction scores, reinforcing sustained investment in advanced photonic platforms.

Asia Pacific Surgical Lasers Market Analysis

Asia Pacific plays a major role in the global market due to rapid healthcare expansion, rising surgical volumes, and increasing adoption of advanced medical technologies across the region. According to World Bank development tracking, public health spending across emerging Asian economies has scaled significantly over the past decade, driven by state-backed infrastructure modernization plans that have expanded capital access for high-end medical technologies. As per the regional development assessments, healthcare investments across India, China, and Southeast Asia have accelerated significantly since 2020, resulting in the construction of numerous multi-specialty tertiary care facilities equipped with modern surgical systems. Furthermore, according to global aesthetic registries and trade data, medical tourism for cosmetic and reconstructive procedures represents a booming market in Thailand, Singapore, and South Korea, with these nations capturing a massive share of the international patient base. This inbound patient flow drives institutional investment in premium laser platforms to meet international quality expectations. Hospital procurement committees prioritize laser integrated systems due to their capacity to minimize collateral tissue damage and enhance operative field visibility. The regulatory framework governing these instruments mandates rigorous validation of wavelength specificity, pulse duration, and fiber delivery mechanisms to ensure patient safety. As clinical training programs integrate optical curricula into surgical residencies, the operational paradigm continues shifting toward technology-driven precision rather than conventional mechanical dissection. This evolution establishes a robust infrastructure for sustained clinical adoption and technological refinement across contemporary medical environments in the Asia Pacific. The institutional commitments create favorable environments for technology adoption and procedural expansion. Hospital administrators prioritize institutions with strong research affiliations because they gain early access to innovative technologies and specialized training programs. The convergence of government support, rising health awareness, and clinical efficacy sustains robust demand for surgical lasers across Asia Pacific healthcare systems. Consequently, healthcare facilities experience improved procedural outcomes and enhanced patient satisfaction scores, reinforcing sustained investment in advanced photonic platforms.

Middle East and Africa Surgical Lasers Market AnalysisThe

Middle East and Africa region grew steadily in the global market owing to gradual improvements in healthcare infrastructure and rising demand for advanced surgical procedures across select nations within the region. According to the Dubai Health Authority, over 500000 international patients sought medical care in the United Arab Emirates in 2024, with laser-based cosmetic and ophthalmological procedures representing high-demand services. Financial monitoring of the sub-Saharan private healthcare landscape notes steady capital allocation from major hospital networks toward upgrading operating theaters and procuring advanced medical instruments to expand specialty care capacity. Hospital procurement committees prioritize laser-integrated platforms due to their capacity to minimize collateral tissue damage and enhance operative field visibility. The regulatory framework governing these instruments mandates rigorous validation of wavelength specificity, pulse duration, and fiber delivery mechanisms to ensure patient safety. As clinical training programs integrate optical curricula into surgical residencies, the operational paradigm continues shifting toward technology-driven precision rather than conventional mechanical dissection. This evolution establishes a robust infrastructure for sustained clinical adoption and technological refinement across contemporary medical environments in the Middle East and Africa. These institutional commitments create favorable environments for technology adoption and procedural expansion. Hospital administrators prioritize institutions with strong international affiliations because they gain access to specialized training programs and equipment maintenance support. The convergence of partnership initiatives, capacity-building efforts, and clinical efficacy sustains gradual but meaningful demand for surgical lasers across emerging healthcare systems in the Middle East and Africa.

Latin America Surgical Lasers Market Analysis

Latin America is anticipated to expand notably in the global market from 2026 to 2034 due to gradual improvements in healthcare infrastructure and rising demand for advanced surgical procedures across select nations within the region. According to the Pan American Health Organization, health financing overviews, the expansion of healthcare access across Latin American nations has steadily grown, though high reliance on private, out-of-pocket spending remains a defining trait of the region's capital medical procurement. As per the national health data, Brazil's private medical sector represents a primary driver for technology adoption, consistently absorbing state-of-the-art diagnostic and surgical equipment across its expanding urban hospital networks. Furthermore, data compiled by national aesthetic surgery associations confirms that Mexico, Brazil, and Colombia rank among the absolute top destinations globally for international patients seeking surgical and non-surgical aesthetic interventions. This inbound patient flow drives institutional investment in premium laser platforms to meet international quality expectations. Hospital procurement committees prioritize laser integrated systems due to their capacity to minimize collateral tissue damage and enhance operative field visibility. The regulatory framework governing these instruments mandates rigorous validation of wavelength specificity, pulse duration, and fiber delivery mechanisms to ensure patient safety. As clinical training programs integrate optical curricula into surgical residencies, the operational paradigm continues shifting toward technology-driven precision rather than conventional mechanical dissection. This evolution establishes a robust infrastructure for sustained clinical adoption and technological refinement across contemporary medical environments in Latin America. These institutional commitments create favorable environments for technology adoption and procedural expansion. Hospital administrators prioritize institutions with strong research affiliations because they gain early access to innovative technologies and specialized training programs. The convergence of government support, rising health awareness, and clinical efficacy sustains robust demand for surgical lasers across Latin American healthcare systems. Consequently, healthcare facilities experience improved procedural outcomes and enhanced patient satisfaction scores, reinforcing sustained investment in advanced photonic platforms.

COMPETITIVE LANDSCAPE

The surgical lasers market exhibits moderate concentration with established multinational corporations leveraging technological expertise and global distribution networks to maintain a competitive advantage. Leading participants differentiate through wavelength-specific platforms that address diverse clinical applications while emphasizing energy efficiency and procedural precision. Innovation cycles accelerate as companies integrate artificial intelligence for real-time tissue analysis and automated parameter optimization, enhancing procedural consistency and safety. Strategic acquisitions enable rapid expansion of technological portfolios and geographic reach while reducing time to market for novel platforms. Competitive intensity increases as emerging manufacturers introduce cost-effective solutions targeting ambulatory surgery centers and specialty clinics in price-sensitive markets. Regulatory compliance remains a critical differentiator, with companies investing substantially in quality systems and clinical evidence generation to secure approvals across diverse jurisdictions. The convergence of technological advancement, clinical validation, and strategic commercialization shapes a dynamic, competitive landscape where operational excellence and innovation drive sustained market leadership within the global surgical lasers industry.

KEY MARKET PLAYERS

Some of the companies that are playing a notable role in the global surgical lasers market profiled in this report are

- Abbott Laboratories

- BISON MEDICAL Co., Ltd.

- Fotona d.o.o.

- Lumenis

- Cynosure

- Alma Lasers

- IPG Photonics Corporation

- Boston Scientific Corporation

- Spectranetics Corporation

- Biolitec AG

TOP PLAYERS IN THE MARKET

- Lumenis maintains a prominent position in the global surgical lasers market through its comprehensive portfolio of photonic systems spanning ophthalmology, urology, and general surgery applications. The company leverages decades of clinical expertise to develop wavelength-specific platforms that deliver precise tissue interaction with minimal collateral damage. Recent strategic initiatives include the launch of next-generation multi-wavelength consoles that support multiple specialties through a single integrated system, enhancing procedural flexibility and operating room efficiency. Lumenis actively collaborates with academic medical centers to validate novel clinical applications and refine energy delivery parameters. The company prioritizes user-centered design principles, incorporating intuitive interfaces and automated safety protocols that reduce operator cognitive load. Furthermore, Lumenis invests substantially in global training programs, ensuring consistent operator competency and optimal clinical outcomes across diverse healthcare settings. These efforts reinforce the company's reputation for clinical excellence and technological innovation within the surgical lasers market.

- Boston Scientific Corporation contributes significantly to the surgical lasers market through its specialized urology and cardiology-focused photonic platforms. The company emphasizes minimally invasive solutions that enable precise tissue ablation with reduced procedural trauma and accelerated patient recovery. Recent strategic actions include the expansion of its laser-based urology portfolio with enhanced fiber delivery technologies aimed at improving precision and control in stone fragmentation and prostate procedures. Boston Scientific actively integrates digital workflow tools that match laser energy to tissue characteristics in real time, enhancing procedural consistency and safety. The company maintains strong relationships with interventional specialists to identify unmet clinical needs and co-develop targeted solutions. Furthermore, Boston Scientific prioritizes regulatory excellence, securing timely approvals across major markets to accelerate technology diffusion. These initiatives strengthen the company's competitive positioning and support sustained growth within the surgical lasers market.

- IPG Photonics Corporation advances the surgical lasers market through its leadership in high-power fiber laser technology and energy-efficient photonic systems. The company emphasizes robust, reliable platforms that deliver consistent performance across demanding clinical environments. IPG Photonics actively collaborates with original equipment manufacturers to integrate its laser sources into specialized surgical consoles spanning oncology, dermatology, and ophthalmology applications. The company prioritizes manufacturing excellence, maintaining stringent quality controls that ensure long-term operational reliability. Furthermore, IPG Photonics invests in research and development to expand wavelength capabilities and improve beam delivery flexibility. These efforts reinforce the company's reputation for technological innovation and operational excellence within the surgical lasers market.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key participants in the surgical lasers market employ strategic acquisitions to expand technological capabilities and geographic reach while accelerating product development timelines. Companies prioritize research and development investments to advance wavelength-specific platforms and integrate artificial intelligence for real-time tissue analysis and parameter optimization. Strategic partnerships with academic medical centers enable clinical validation of novel applications and refinement of energy delivery protocols. Market leaders focus on user-centered design principles, incorporating intuitive interfaces and automated safety features that reduce operator cognitive load and enhance procedural consistency. Companies expand their service and training infrastructure to ensure optimal equipment utilization and clinical outcomes across diverse healthcare settings. Furthermore, participants pursue regulatory excellence, securing timely approvals across major markets to accelerate technology diffusion and commercialization. These multifaceted strategies strengthen competitive positioning and support sustained growth within the evolving surgical lasers market landscape.

MARKET SEGMENTATION

This research report on the global surgical lasers market has been segmented and sub-segmented based on product, procedure type, application and region.

By Product

- Carbon dioxide (CO2) lasers

- Nd YAG lasers

- argon lasers

By Procedure Type

- Laparoscopic surgery

- Open surgery

- Percutaneous surgery

By Application

- Dentistry

- Ophthalmology

- Dermatology

- Gynecology

- Cardiology

- Oncology

- Urology

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. What is the global surgical lasers market?

The global surgical lasers market includes laser systems used for minimally invasive surgeries across dermatology, ophthalmology, urology, and other medical fields worldwide

2. What drives growth in the global surgical lasers market?

Growth is driven by rising chronic diseases, preference for minimally invasive surgeries, technological advances, and increasing demand for aesthetic laser procedures

3. Which regions dominate the global surgical lasers market?

North America leads due to advanced healthcare infrastructure, while Asia-Pacific shows fastest growth owing to rising medical infrastructure and awareness

4. What are the main types of lasers in the global surgical lasers market?

Diode, solid-state, and CO2 lasers are major types used across dermatology, ophthalmology, and urology treatments in the global surgical lasers market

5. How are minimally invasive surgeries affecting the global surgical lasers market?

They boost demand for surgical lasers by reducing recovery time, infection risk, and improving precision in the global surgical lasers market

6. Who are key players in the global surgical lasers market?

Top companies include Cynosure, Lumenis, IPG Photonics, biolitec AG, and Alma Lasers, dominating the global surgical lasers market through innovation

7. What challenges does the global surgical lasers market face?

High equipment costs, regulatory hurdles, and physician training needs pose challenges in the global surgical lasers market

8. How is technology evolving in the global surgical lasers market?

Advanced laser platforms, integration with imaging, and portable devices are driving innovation in the global surgical lasers market

9. What applications are served by the global surgical lasers market?

Applications include dermatology, ophthalmology, dental surgery, oncology, and gynecology markets globally

10. How does aesthetic surgery influence the global surgical lasers market?

Increasing preference for cosmetic procedures fuels demand for specialized surgical laser systems worldwide

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com