Global Tin Market Size, Share, Trends, & Growth Forecast Report Segmented By Product Type (Metal, Alloy, Compounds), Application, End-User Industry, and Region (Latin America, North America, Asia Pacific, Europe, Middle East and Africa), Industry Analysis from 2026 to 2034

Global Tin Market Summary

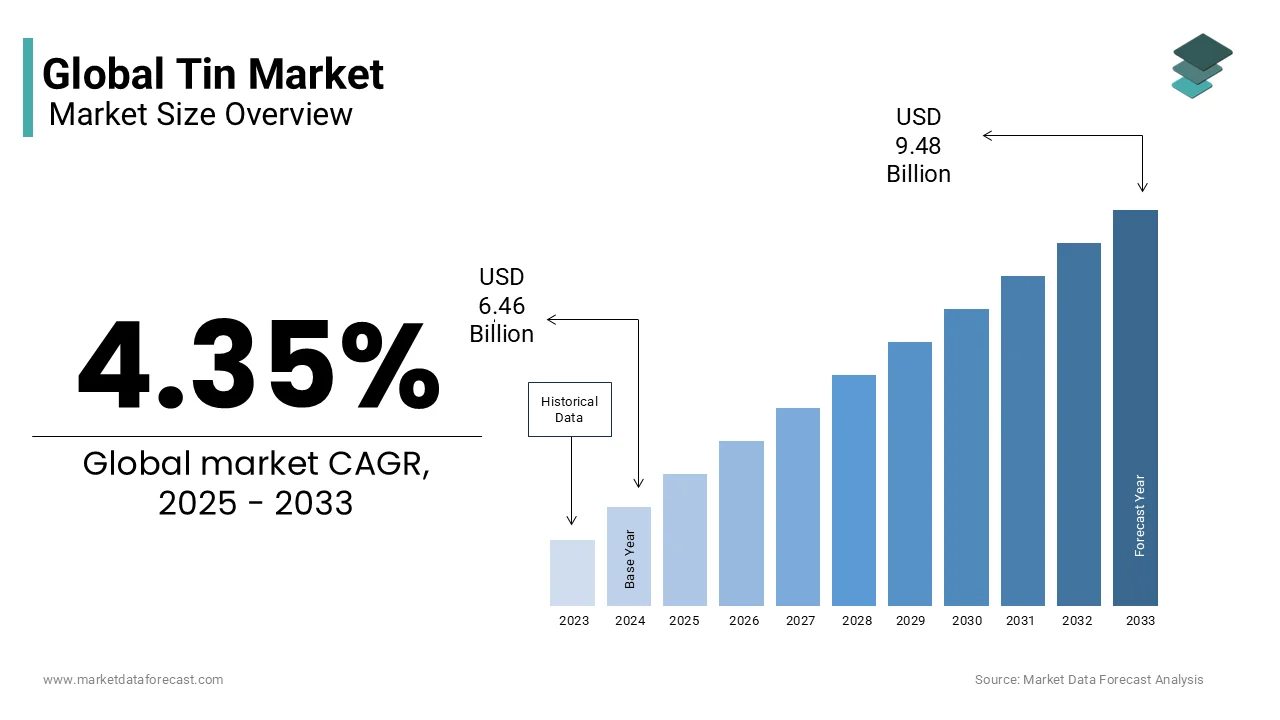

The global tin market was valued at USD 6.74 billion in 2025 and is projected to reach USD 7.03 billion in 2026 and USD 9.89 billion by 2034, growing at a CAGR of 4.35% from 2026 to 2034. The growth of the global tin market is driven by increasing demand from the electronics industry, rising applications of tin in soldering processes, and its use in tin plating and chemicals. Growing adoption of renewable energy technologies, electric vehicles, and electronic devices further accelerates the demand for tin-based solder materials.

Key Market Trends

- Rising demand for lead-free solders in electronics is due to a regulatory push for environmentally friendly materials.

- Growing use of tin in energy storage technologies, including lithium-ion batteries.

- Expanding applications of tin in packaging and coatings for enhanced corrosion resistance.

- Increasing demand for tin-based alloys and chemicals across industrial sectors.

- Asia-Pacific is emerging as a global production and consumption hub for tin.

Segmental Insights

- Based on product type, the tin metal segment held a prominent share of the global market in 2025, supported by its extensive use in electronics, plating, and alloys.

- Based on application, the solder segment dominated the tin market by accounting for 52.3% of the share in 2025, reflecting tin’s critical role in electronics assembly.

- Based on end-user industry, the electronics segment led the market with 48.3% share in 2025, driven by rising consumption of consumer electronics, semiconductors, and automotive electronics.

Regional Insights

- Asia-Pacific was the top performer in the global tin market, capturing 58.3% of the share in 2025, fueled by strong production bases in China, Indonesia, and Myanmar alongside robust electronics demand.

- North America held a steady share, driven by growth in automotive electronics and renewable energy industries.

- Europe recorded significant demand, especially from tinplate packaging and industrial applications.

- Latin America and the Middle East & Africa are emerging markets with moderate but growing tin consumption.

Competitive Landscape

Leading companies in the global tin market include Yunnan Tin, Malaysia Smelting Corp. Berhad, PT Timah, Minsur, Thaisarco, Yunnan Chengfeng, Guangxi China Tin, EM Vinto, Hindustan Tin Works Ltd, and Ardagh Group S.A. These players focus on expansion of mining operations, technological integration, and sustainability-driven production to strengthen their market position.

Global Tin Market Size

The global tin market size was valued at USD 6.74 billion in 2025 and is expected to reach USD 9.89 billion by 2034 from USD 7.03 billion in 2026. The market is projected to grow at a CAGR of 4.35%.

The tin is primarily extracted from cassiterite (SnO₂), with over 70% of global supply originating from hard-rock and alluvial deposits in Southeast Asia, Central Africa, and South America. According to the U.S. Geological Survey, approximately 300,000 metric tons of tin were mined globally in 2023, with Indonesia, China, and the Democratic Republic of the Congo ranking among the top producers. Tin’s unique ability to form eutectic alloys at low melting points makes it indispensable in electronics manufacturing, particularly for lead-free soldering. The International Tin Association confirms that over 50% of refined tin consumption is directed toward electronic assembly, where reliability under thermal cycling is paramount.

MARKET DRIVERS

Expansion of Electronics Manufacturing and Demand for Lead-Free Solder

The proliferation of consumer electronics, automotive electronics, and industrial control systems is a primary driving factor for the growth of tin market. As per the International Electrotechnical Commission, over 95% of printed circuit boards produced since 2020 use tin-based lead-free solders compliant with the Restriction of Hazardous Substances (RoHS) Directive. China alone consumes over 150,000 metric tons of tin annually for electronic assembly, as reported by the China Electronics Federation.

Growth in Food and Beverage Packaging Using Tinplate

Tinplate steel is a consisting of cold-rolled steel coated with a thin layer of tin, continues to be a dominant material in food and beverage canning due to its durability, recyclability, and non-reactivity. According to the European Federation of Corrugated Board Manufacturers, over 120 billion tin-coated cans are produced annually in Europe and North America for products ranging from canned vegetables to pet food. The U.S. Food and Drug Administration recognizes tin-coated steel as safe for direct food contact, which is citing its resistance to oxidation and metal leaching. The rising urbanization and processed food consumption are expanding tinplate usage is greatly to influence the growth of the tin market. Additionally, the high recycling rate of tinplate over 70% in the EU, as per Eurostat that enhances its appeal amid growing environmental scrutiny of plastic packaging.

MARKET RESTRAINTS

Geopolitical Instability and Informal Mining in Key Producing Regions

The global tin supply originates from regions plagued by political instability and unregulated mining practices with supply chain integrity. These operations often lack environmental controls, labor safeguards, and traceability mechanisms, raising concerns about conflict financing and human rights violations. Similarly, in Myanmar, military-controlled concessions have disrupted ethical supply chains, with the Global Witness report of 2023 estimating that over 40% of the country’s tin exports bypass formal regulatory oversight. These governance deficits increase compliance costs, limit access to ESG-conscious buyers, and create volatility in long-term supply planning for downstream industries.

Environmental Degradation from Alluvial and Open-Pit Tin Mining

Tin extraction through alluvial dredging and open-pit methods causes extensive environmental damage, including deforestation, soil erosion, and aquatic ecosystem disruption. Marine tin dredging has devastated coral reefs and seagrass beds, with a 2022 study by the Bogor Agricultural Institute showing a 60% decline in fish biomass in affected waters. The process generates large volumes of tailings containing heavy metals like arsenic and lead, contaminating groundwater. These ecological consequences have triggered stricter regulations and community opposition, which is delaying project approvals and increasing operational costs, thereby constraining sustainable production growth despite rising demand.

MARKET OPPORTUNITIES

Advancements in Tin-Based Anodes for Next-Generation Lithium-Ion Batteries

The emerging research into tin as a high-capacity anode material for lithium-ion batteries is likely to create new opportunities for the growth of tin market. As per a 2023 study published in Nature Energy by researchers at Stanford University, tin-antimony and tin-silicon composite anodes demonstrated stable cycling with 80% capacity retention after 1,000 charge-discharge cycles. Companies like Samsung SDI and CATL are actively developing tin-alloy anodes for use in fast-charging EV batteries and portable electronics. The U.S. Department of Energy has included tin-based materials in its Battery500 consortium roadmap, targeting cells with 500 Wh/kg by 2030.

Circular Economy and Tin Recycling from Electronic Waste

The expansion of urban mining and e-waste recycling infrastructure offers a sustainable pathway to augment tin supply while reducing environmental impact. According to the Global E-Waste Monitor 2023, over 50 million metric tons of electronic waste were generated globally in 2022, containing an estimated 65,000 metric tons of recoverable tin. Umicore and Boliden operate industrial-scale plants that extract high-purity tin from end-of-life electronics, with recycled tin now accounting for nearly 30% of global supply, as per the International Tin Association. With the European Union mandating higher recycling quotas under the Circular Economy Action Plan and China enforcing strict e-waste management rules, investment in recovery technologies is accelerating. This shift not only enhances supply security but also aligns with corporate ESG goals, positioning recycled tin as a premium, low-carbon alternative in electronics and packaging sectors.

MARKET CHALLENGES

Price Volatility Due to Concentrated Supply and Speculative Trading

The highly susceptible to price fluctuations due to supply concentration and limited production elasticity is restricting the growth of tin market. Sudden export restrictions, such as Indonesia’s temporary ban on tin concentrates in 2022, or production halts due to monsoon-related flooding in Southeast Asia, trigger sharp supply shocks. Additionally, speculative activity on the London Metal Exchange amplifies price swings, complicating procurement planning for electronics manufacturers.

Substitution Threat from Alternative Materials in Traditional Applications

Tin faces increasing competition from substitute materials in both packaging and electronics, which is driven by cost and performance considerations. In food packaging, aluminum and polymer-lined steel cans are gaining ground due to lighter weight and lower material costs. According to the Aluminum Association, aluminum beverage can production in North America rose by 12% between 2020 and 2023, partly at the expense of tinplate. In soldering, while lead-free tin alloys remain dominant, research into copper-tin pastes and silver sintering for high-power electronics may reduce tin dependency in niche applications. Additionally, conductive adhesives based on silver nanoparticles are being adopted in flexible electronics, where traditional soldering is impractical.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.35% |

| Segments Covered | By Product Type, Application, End-User Industry, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Yunnan Tin, Malaysia Smelting Corp. Berhad, PT Timah, Minsur, Thaisarco, Yunnan Chengfeng, Guangxi China Tin, EM Vinto, Hindustan Tin Works Ltd, and Ardagh Group S.A, and others |

SEGMENTAL ANALYSIS

By Product Type Insights

The tin metal segment held a prominent share of the global tin market in 2025 with its direct applicability in high-demand industrial processes in solder production and tin plating. Refined tin metal, typically 99.85% pure or higher, is essential for manufacturing lead-free solder alloys used in electronics, where minimal impurities ensure reliable electrical conductivity and joint integrity. The U.S. Geological Survey confirms that over 180,000 metric tons of primary tin metal were consumed globally in 2023 in Asia’s electronics manufacturing hubs. Additionally, its malleability and corrosion resistance make it ideal for direct electroplating onto steel substrates for food packaging.

Tin compounds segment is likely to grow with an expected CAGR of 7.8% during the forecast period with the rising demand for organotin and inorganic tin-based stabilizers in polyvinyl chloride (PVC) production in construction and medical applications. Monobutyltin tris(acetate) and dibutyltin dilaurate are widely used as catalysts in silicone and polyurethane manufacturing, with global demand increasing due to expansion in sealant and adhesive industries. Additionally, tin oxide (SnO₂) is gaining traction in gas sensors and transparent conductive coatings for touchscreens, as demonstrated by research at the Fraunhofer Institute for Ceramic Technologies.

By Application Insights

The solder segment was the largest and held 52.3% of global tin market share in 2025 with the indispensable role of tin-based alloys in assembling electronic components across consumer, industrial, and automotive sectors. The shift to lead-free soldering, mandated by the EU’s RoHS Directive and adopted globally has tin’s position as the primary base metal in eutectic alloys such as SAC305 (tin-silver-copper). The Semiconductor Industry Association estimates that each smartphone contains 2–3 grams of tin in its solder joints, with over 1.4 billion units shipped annually. In automotive electronics, the rise of advanced driver-assistance systems (ADAS) and infotainment has increased tin usage per vehicle to over 1.2 kg, according to the German Association of the Automotive Industry.

Tin plating segment is likely to grow with an expected CAGR of 6.9% from 2026 to 2034 with the increasing demand for corrosion-resistant, food-safe metallic coatings in packaging and industrial components. Tinplate steel coated with a thin layer of tin remains the standard for food and beverage cans due to its non-reactivity and hermetic seal. According to the Can Manufacturers Institute, over 130 billion tin-coated cans are produced annually in North America and Europe, with a 5% year-on-year increase in demand for pet food and shelf-stable meals. Additionally, tin plating is gaining ground in electric motor components and battery terminals, where its low contact resistance and solderability enhance performance.

By End-User Industry Insights

The electronics industry segment was the largest and held 48.3% of the global tin market share in 2025, with the tin’s irreplaceable role in surface-mount technology and printed circuit board (PCB) assembly. Over 90% of all electronic devices, from smartphones to industrial controllers, use tin-based solders for interconnecting microchips and passive components. The Consumer Technology Association estimates that global electronics production surpassed 4.5 trillion units in 2023, each requiring precise solder joints. Additionally, the proliferation of IoT devices, wearables, and smart home systems continues to expand the addressable market.

The automotive sector is projected to grow at a CAGR of 8.2% during the forecast period with the electrification and digitalization of vehicles, which significantly increase electronic content. As per the European Automobile Manufacturers Association, the average modern vehicle now contains over 100 electronic control units (ECUs), each assembled with tin-rich solder. Additionally, tin plating is used in connectors, terminals, and sensor housings for corrosion resistance.

REGIONAL ANALYSIS

Asia Pacific Tin Market Insights

Asia Pacific was the top performer of the global tin market by accounting for 58.3% of share in 2025. Japan and South Korea are major importers of refined tin for high-end solder and specialty alloys with the Japan Nonferrous Metals Association noting that 95% of domestically used tin goes into electronics. India’s growing automotive and packaging sectors are increasing demand, with tin consumption rising at 6.5% annually, as per the Indian Bureau of Mines.

North America Tin Market Insights

North America was positioned second with high-value consumption and stringent regulatory standards. The United States is the largest consumer in the region, importing over 12,000 metric tons of refined tin annually, as documented by the U.S. Geological Survey for electronics, aerospace, and food packaging. The semiconductor industry in Texas and Arizona, supported by the CHIPS and Science Act, is expanding production capacity, increasing demand for high-purity solder alloys.

Europe Tin Market Insights

The tin market growth in Europe is likely to grow with its emphasis on sustainability, circularity, and advanced manufacturing. Germany and the United Kingdom are the largest consumers by utilizing tin in automotive electronics, renewable energy systems, and food-safe packaging. According to the European Automobile Manufacturers Association, each new vehicle contains an average of 1.1 kg of tin, primarily in electronic systems. Additionally, the Restriction of Hazardous Substances (RoHS) Directive has institutionalized lead-free tin solders across all electronic goods. As per the Fraunhofer Institute, over 70% of tin used in the EU is either recycled or sourced from certified responsible mines.

Latin America Tin Market Insights

The Latin American market is likely to grow with Brazil and Bolivia serving as key players in both production and consumption. Bolivia holds significant cassiterite reserves in the Potosí and Oruro regions, with the Bolivian Ministry of Mining estimating 400,000 metric tons of tin resources, though extraction remains underdeveloped. Brazil consumes over 4,000 metric tons annually, primarily for food packaging and electronics, as reported by the Brazilian Association of Technical Standards. The country’s packaging industry uses tinplate in over 80% of canned beverages and preserved foods. Additionally, automotive manufacturing in São Paulo and Belo Horizonte is increasing demand for tin-based solders and platings.

Middle East & Africa Tin Market Insights

The Middle East and African market growth is driven by the import-driven and concentrated in select industrial centers. Nigeria and South Africa are the largest consumers, using tin in food packaging, construction, and telecommunications infrastructure. The UAE imports over 1,200 metric tons of tin annually, primarily for electronics assembly in Dubai’s technology zones and for architectural tin plating.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

These are some of the market players that are dominating the global tin market.

- Yunnan Tin

- Malaysia Smelting Corp. Berhad

- PT Timah

- Minsur

- Thaisarco

- Yunnan Chengfeng

- Guangxi China Tin

- EM Vinto

- Hindustan Tin Works Ltd

- Ardagh Group S.A.

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

Key players in the tin market are deploying integrated strategies centered on vertical integration, sustainability certification, and technological innovation to secure competitive advantage. Companies are investing in end-to-end control from mine to refined metal to ensure quality, compliance, and supply chain transparency. Adoption of blockchain and digital traceability platforms is enabling verification of conflict-free and environmentally sound sourcing, meeting stringent requirements in Europe and North America. Strategic partnerships with research institutions are accelerating the development of next-generation tin-based technologies. Additionally, companies are enhancing recycling capabilities and forming alliances with e-waste processors to tap into urban mining, reducing reliance on primary extraction.

COMPETITIVE OVERVIEW

The competitive landscape of the tin market is shaped by a concentrated supply base, geopolitical sensitivities, and diverging regional demands. A handful of producers dominate mining output, with Indonesia, China, and Peru accounting for over 60% of global supply, creating oligopolistic dynamics that influence pricing and availability. Competition is not solely based on volume but on purity, traceability, and compliance with environmental and social governance standards. Chinese refiners lead in scale and downstream integration, while Latin American and Malaysian producers emphasize responsible mining credentials to access premium markets. Smaller players are challenged by capital intensity, regulatory scrutiny, and price volatility. The rise of e-waste recycling and material substitution in soldering adds complexity, forcing incumbents to innovate.

TOP PLAYERS IN THE MARKET

- Yunnan Tin Group, headquartered in China, is a pivotal force in the global tin industry and a dominant player in the Asia Pacific region. The company operates the world’s largest integrated tin production complex, encompassing mining, smelting, refining, and downstream product development. In Southeast Asia, it has strengthened supply partnerships with electronics manufacturers in Vietnam and Thailand, providing high-purity tin ingots and solder alloys compliant with RoHS and REACH standards.

- PT Timah Tbk, Indonesia’s state-owned tin mining and processing enterprise, plays a central role in the Asia Pacific tin supply chain. As one of the largest producers in the region, the company supplies refined tin to electronics and packaging industries across China, Japan, and South Korea. PT Timah has intensified efforts to formalize artisanal mining cooperatives in Bangka-Belitung, bringing over 10,000 small-scale miners into its certified supply network as per Indonesia’s Ministry of Energy and Mineral Resources.

- Minsur S.A., a leading Peruvian mining company, exerts significant influence in the Asia Pacific market through its high-grade tin production and commitment to responsible sourcing. Although based in South America, Minsur supplies a substantial portion of its refined tin to Japan, South Korea, and Malaysia, where purity and traceability are paramount for electronics manufacturing. The company’s San Rafael mine in southern Peru is one of the few large-scale, underground tin operations globally, producing over 20,000 metric tons annually, as reported by the Peruvian Ministry of Energy and Mines.

RECENT HAPPENINGS IN THE MARKET

- In November 2023, Malaysia Smelting Corporation upgraded its Port Klang refinery to produce 99.99% purity tin, catering to high-end semiconductor clients in Taiwan and Singapore.

MARKET SEGMENTATION

This research report on the global tin market is segmented and sub-segmented into the following categories.

By Product Type

- Metal

- Alloy

- Compounds

By Application

- Solder

- Tin Plating

- Chemicals

- Other Applications (Specialized Alloys and Lead-acid Batteries)

By End-user Industry

- Automotive

- Electronics

- Packaging (Food and Beverage)

- Glass

- Other End-user Industries (Chemical, Tool Making, Medical Devices)

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

1. What is the Tin Market?

The tin market covers the production, trade, and applications of tin metal in soldering, packaging, chemicals, and electronics.

2. What drives growth in the Tin Market?

Rising demand from electronics, renewable energy, and packaging industries is fueling market expansion.

3. What are the major applications of tin?

Tin is widely used in soldering, food packaging, chemicals, glass coatings, and plating.

4. Which region dominates the Tin Market?

Asia-Pacific leads due to strong electronics manufacturing, with China and Indonesia as key producers.

5. Who are the leading players in the Tin Market?

Key players include Yunnan Tin, Malaysia Smelting Corp., PT Timah, Minsur, and Thaisarco.

6. What trends are shaping the Tin Market?

Trends include rising demand for lead-free solder, sustainable packaging, and renewable energy storage.

7. What challenges does the Tin Market face?

Challenges include fluctuating ore supply, environmental regulations, and price volatility.

8. What is the future outlook for the Tin Market?

The tin market is expected to grow steadily, driven by electronics, renewable energy, and sustainable materials.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com