Global Tire Derived Fuel Market Size, Share, Trends & Growth Forecast Report By End Use Industry (Cement Kilns, Pulp and Paper Mills and Utility and Industrial Boilers) and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa), Industry Analysis 2024 to 2033

Global Tire Derived Fuel Market Size

The global tire derived fuel market is estimated to grow from USD 459 million in 2024 to USD 818.64 million in 2033, representing a CAGR of 6.64%.

Tire Derived Fuel (TDF) refers to shredded or processed end-of-life tires that are utilized as a supplemental energy source in industrial combustion processes, primarily in cement kilns, pulp and paper mills, and power generation facilities. Characterized by a high calorific value—approximately 33–37 MJ/kg, comparable to coal—TDF offers a dense, consistent energy output with lower moisture content than traditional fossil fuels. The conversion of scrap tires into fuel not only mitigates landfill accumulation but also reduces reliance on coal in energy-intensive operations. Unlike conventional waste-to-energy processes, TDF combustion in preheater kilns achieves near-complete combustion efficiency due to high operating temperatures exceeding 1,400°C, minimizing residual emissions when properly managed. As industries face mounting pressure to decarbonize, TDF has emerged as a transitional fuel that balances waste management imperatives with energy recovery, particularly in regions with limited recycling infrastructure for rubber.

MARKET DRIVERS

Increasing Demand from the Cement Industry for Alternative Fuels to Reduce Carbon Emissions

The global cement industry is actively substituting fossil fuels with alternative feedstocks such as Tire Derived Fuel to meet decarbonization targets. TDF offers a calorific value equivalent to bituminous coal while reducing net carbon emissions. Countries like Germany and France have cement facilities, driven by national carbon pricing mechanisms and emissions trading schemes. Additionally, the high iron content in tire steel belts acts as a flux in clinker formation, improving kiln efficiency. Thus, the scalability of TDF integration presents a compelling pathway to reduce sector-wide emissions while managing waste tires.

Escalating Global Scrap Tire Accumulation and Limited Disposal Options

The exponential growth in vehicle ownership has led to a surge in end-of-life tires. In the absence of scalable recycling pathways, landfilling and illegal dumping remain prevalent, posing severe environmental risks such as leachate contamination and fire hazards. According to the U.S. Environmental Protection Agency, tire fires can burn for weeks, releasing toxic fumes including benzene and polycyclic aromatic hydrocarbons. This mounting waste crisis has prompted governments to explore energy recovery through TDF as a viable disposal mechanism. Moreover, in Indonesia, a notable share of scrap tires are improperly disposed of, leading to increased interest in TDF utilization in cement kilns. By transforming a persistent waste stream into a high-energy fuel, TDF provides a pragmatic solution to dual challenges: waste management and fossil fuel dependency.

MARKET RESTRAINTS

Stringent Air Quality Regulations Limiting TDF Combustion Emissions

The use of Tire Derived Fuel faces regulatory resistance due to concerns over emissions of sulfur oxides (SOₓ), nitrogen oxides (NOₓ), and particulate matter during combustion. In the United States, the Environmental Protection Agency mandates that facilities using TDF comply with Maximum Achievable Control Technology (MACT) standards under the Clean Air Act, requiring advanced flue gas treatment systems such as selective non-catalytic reduction (SNCR) and baghouse filters. According to the American Lung Association, exposure to fine particulates from tire combustion is linked to respiratory diseases, influencing public opposition to TDF facilities near urban zones. Additionally, the presence of zinc oxide and steel wire in tires can lead to heavy metal emissions if combustion temperatures fall below 1,200°C, as noted by the International Solid Waste Association. These regulatory and health-related constraints necessitate significant capital investment in pollution control, deterring smaller operators from adopting TDF despite its economic advantages.

Public Perception and Environmental Opposition to Tire Combustion

Public skepticism and environmental advocacy against the combustion of rubber waste, often framed as "burning trash" rather than energy recovery, is a significant barrier to the expansion of Tire Derived Fuel. Communities near cement plants using TDF frequently raise concerns about odor, visible emissions, and long-term health impacts, even when facilities comply with emission standards. In the United Kingdom, Greenpeace UK has campaigned against TDF use, arguing that it undermines circular economy goals by prioritizing incineration over material recycling. The Ellen MacArthur Foundation emphasizes that true sustainability requires keeping materials in use, not energy recovery through combustion. Furthermore, the presence of persistent organic pollutants such as polycyclic aromatic hydrocarbons (PAHs) in tire smoke, even at low levels, fuels resistance. The World Health Organization has classified certain PAHs as Group 1 carcinogens, amplifying health concerns. This socio-political resistance complicates permitting processes and delays project timelines, constraining market growth despite technical and economic feasibility.

MARKET OPPORTUNITIES

Integration of TDF in Co-Processing within Waste-to-Energy Cement Kilns

The co-processing of Tire Derived Fuel in cement kilns presents a transformative opportunity to align industrial energy needs with sustainable waste management. Unlike conventional incineration, co-processing leverages the high thermal efficiency of kilns—operating above 1,400°C—to achieve complete combustion with minimal residue. This method not only replaces fossil fuels but also utilizes the mineral content of tires as raw material input, reducing the need for limestone and clay. The technology is particularly viable in developing nations where waste infrastructure is underdeveloped.

Government Incentives and Policy Support for Alternative Fuels in Industrial Sectors

Governments worldwide are introducing fiscal and regulatory incentives to promote Tire Derived Fuel as part of broader energy transition and waste management strategies. Moreover, in Canada, Environment and Climate Change Canada includes TDF in its Low Carbon Fuel Standard, allowing producers to earn compliance credits. These policy frameworks reduce financial barriers, accelerate infrastructure development, and legitimize TDF as a sustainable energy vector, fostering market expansion across both developed and emerging economies.

MARKET CHALLENGES

Inconsistent Quality and Preparation Standards for TDF Feedstock

The lack of standardized specifications for TDF quality, leading to variability in calorific value, moisture content, and contaminant levels is a critical operational challenge in the Tire Derived Fuel market. According to the U.S. Tire Manufacturers Association, TDF processed from passenger tires typically has a calorific value of 33–35 MJ/kg, whereas off-the-road mining tires can exceed 37 MJ/kg, creating combustion instability when blended. The presence of steel belts, fiber, and dirt can damage burners and reduce efficiency. In India, the Bureau of Indian Standards has introduced IS 16394 for TDF specifications, but enforcement remains weak, with a large percentage of suppliers failing to meet particle size and ash content requirements, according to the Central Pollution Control Board. In Africa, informal shredding operations produce TDF with high chlorine content from mixed waste tires, increasing dioxin formation during combustion, as reported by the African Clean Air Coalition. Without uniform grading, moisture control below, and metal removal protocols, industrial users face operational risks, including kiln downtime and emission spikes. This inconsistency undermines confidence in TDF as a reliable fuel, limiting long-term contracts and investment in processing infrastructure.

Competition from Emerging Rubber Recycling Technologies

The Tire Derived Fuel market faces increasing competition from advanced recycling technologies that recover raw materials from end-of-life tires, aligning more closely with circular economy principles. Pyrolysis, in particular, has gained traction as a method to convert scrap tires into recovered carbon black, oil, and steel. Companies like Pyrum Innovations and Black Bear Carbon are producing high-purity carbon black suitable for tire re-manufacturing, challenging the notion that tires are only fit for energy recovery. Also, pyrolysis can recover a tire’s mass as usable carbon black, compared to zero material recovery in TDF combustion. In the Netherlands, the government has prioritized material recycling over co-processing, allocating a notable smount to support pyrolysis plants under its Circular Economy 2050 roadmap. This shift threatens TDF’s long-term viability, positioning it as a transitional rather than sustainable solution in the evolving waste valorization landscape.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2024 to 2033 |

| CAGR | 6.64% |

| Segments Covered | By End-User Industry and Region. |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Emanuel Tire, ETR Group, Front Range Tire Recycle, Inc., Globarket Tire Recycling LLC, L & S Tire Company, Lakin Tire West Inc., Liberty Tire Recycling, Ragn-Sells Group, Reliable Tire Disposal, Renelux Cyprus Ltd, ResourceCo Pty Ltd, Scandinavian Enviro Systems AB, Tire Disposal & Recycling, Inc. and West Coast Rubber Recycling Inc., and Others. |

SEGMENTAL ANALYSIS

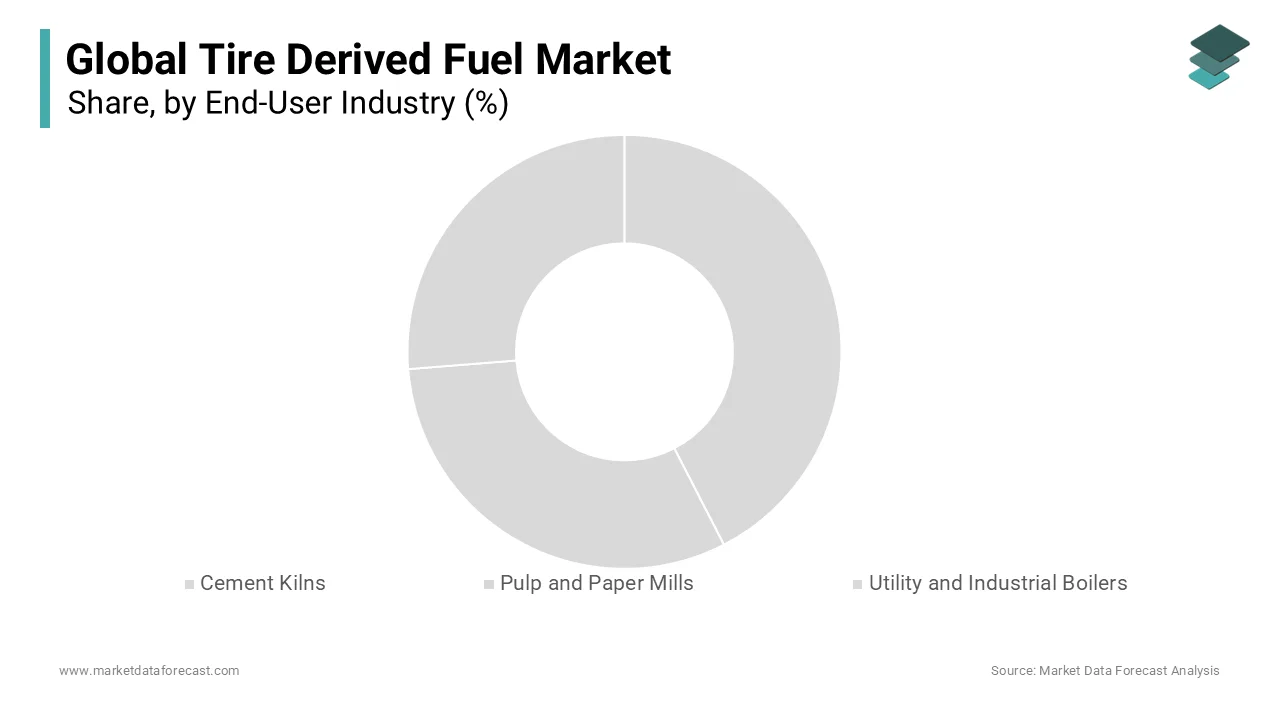

By End-User Industry Insights

market by capturing a 62.5% of total consumption in 2024. This overwhelming dominance is rooted in the inherent compatibility between TDF and the cement manufacturing process, particularly within precalciner kiln systems that operate at sustained temperatures exceeding 1,400°C. One primary driver of this leadership is the high thermal efficiency and complete combustion achieved in rotary kilns. A further critical factor is the dual benefit of energy recovery and raw material contribution: the steel wire in tires acts as an iron source in clinker formation, reducing the need for iron ore additives. Hence, the sector remains the cornerstone of TDF demand.

The pulp and paper mills segment is emerging as the fastest-growing end-use for Tire Derived Fuel and is projected to expand at a CAGR of 9.6% in the coming years. This acceleration is driven by the sector’s urgent need to reduce reliance on fossil fuels and meet corporate sustainability targets. Many paper mills operate recovery boilers originally designed for biomass, which can be retrofitted to accept TDF due to its high calorific value and low moisture content. A further key driver is the economic advantage of TDF over traditional fuels. Besides, the industry’s transition toward circular operations has created synergy with tire waste management. Thus, the scalability of TDF integration positions this sector for sustained growth.

REGIONAL ANALYSIS

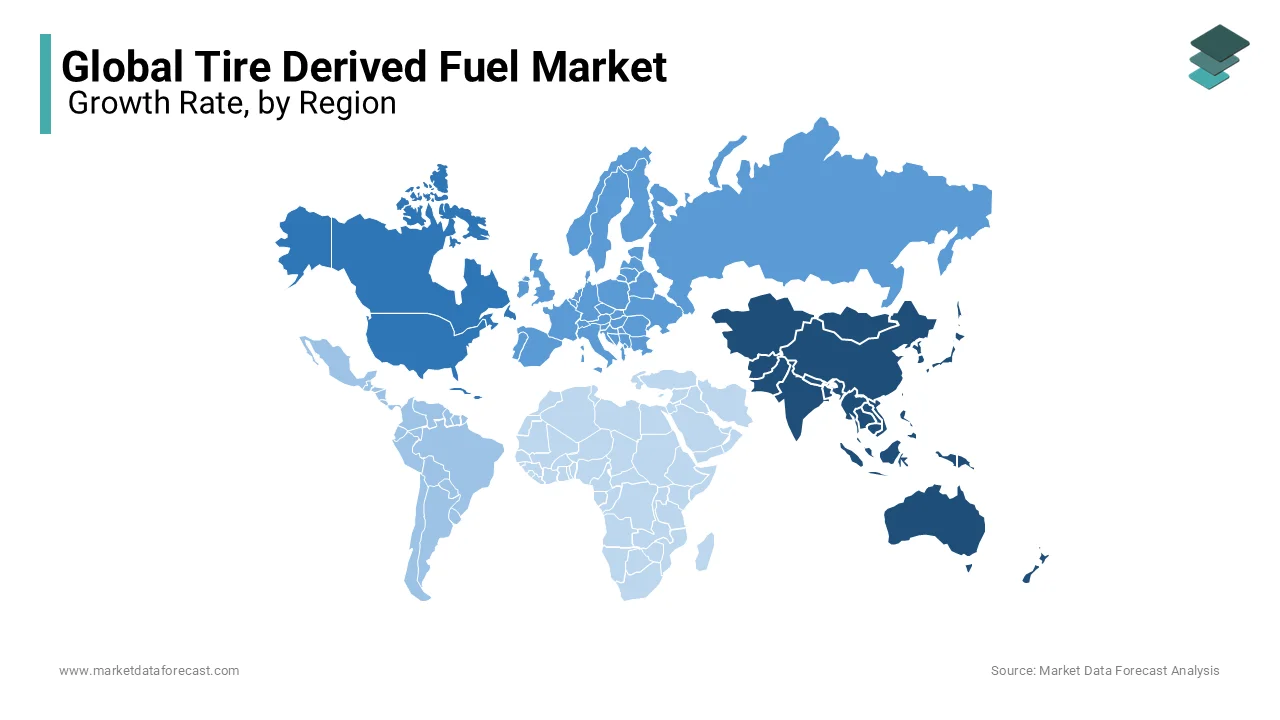

North America Tire Derived Fuel Market Insights

North America held a 34% share of the global Tire Derived Fuel market and positioning it as a leader in structured TDF utilization and regulatory integration. The United States, in particular, has developed a well-established TDF ecosystem driven by decades of industrial adoption and environmental policy alignment. States like Texas, California, and Ohio have implemented robust scrap tire management programs, diverting millions of tires from landfills. Canada complements this landscape with provincial incentives. The presence of major TDF processors such as Liberty Tire Recycling. With strong interagency coordination between environmental and energy departments, North America remains a benchmark for scalable, compliant TDF deployment.

Europe Tire Derived Fuel Market Insights

Europe is distinguished by its advanced regulatory framework and emphasis on circular economy integration, as stated by the European Tyre and Rubber Manufacturers’ Association. The European Union’s Industrial Emissions Directive and Waste Framework Directive have institutionalized co-processing in cement kilns. Germany leads the region, where a significant share of cement facilities use TDF, supported by the country’s strict landfill bans on untreated tires enforced since 2005. In Scandinavia, Sweden and Finland have adopted TDF in district heating and combined heat and power (CHP) plants, leveraging their district energy networks to maximize energy recovery. However, public scrutiny remains high. The European Commission’s Horizon Europe program has funded research into low-emission TDF combustion, reflecting a commitment to balancing waste valorization with air quality. These dynamics position Europe as a model of regulated, sustainable TDF deployment.

Asia-Pacific Tire Derived Fuel Market Insights

The Asia-Pacific region is a key region the global Tire Derived Fuel market, with growth propelled by escalating scrap tire volumes and expanding industrial energy demand, as reported by the Asia Pacific Tire Recycling Council. China, the world’s largest tire producer, discards millions of end-of-life tires annually, with lesser formally recycled. This waste burden has prompted the adoption of TDF in cement kilns, particularly in provinces like Shandong and Hebei. India is witnessing rapid expansion. In Japan, TDF is integrated into waste-to-energy systems under the Sound Material-Cycle Society framework. South Korea’s Extended Producer Responsibility system mandates tire recyclers to supply feedstock for energy recovery. With urbanization and vehicle ownership rising, the region’s TDF market is poised for accelerated growth, driven by necessity as much as sustainability.

Latin America Tire Derived Fuel Market Insights

Latin America holds a notable share of the global Tire Derived Fuel market, with growth concentrated in industrialized nations responding to mounting tire waste and energy cost pressures. Brazil leads the region. The state of São Paulo has implemented landfill bans on whole tires, driving the development of processing facilities near industrial clusters. Mexico follows closely. Chile has introduced tax incentives for industries using alternative fuels. However, fragmented waste collection and limited processing infrastructure hinder scalability. Also illegal tire dumps in urban peripheries pose fire and mosquito breeding risks, increasing public health urgency. With regional investment in waste management rising under the LAC Climate Action Plan, Latin America is gradually building the foundation for structured TDF utilization.

Middle East and Africa Tire Derived Fuel Market Insights

The Middle East and Africa collectively account for small share of the global Tire Derived Fuel market, with nascent but strategic development driven by large-scale industrial projects and waste management reforms. Saudi Arabia is at the forefront, integrating TDF into its Vision 2030 waste-to-energy roadmap. The NEOM smart city project includes a dedicated waste valorization plant designed to process tires for industrial energy use. South Africa remains the regional leader in formal recycling. With increasing investment in industrial parks and energy security, the region is laying the groundwork for expanded TDF integration.

In terms of consumption, the United States is an important country in the market for tire-derived fuels. In the United States, more than 270 million scrap tires were produced in 2032. Of these, 81.4% of scrap tires were recycled and reemployed for various applications. More than 100 million tires have been employed for fuel in pulp and paper mills, cement manufacturing, and utility boilers, among others.

KEY PLAYERS IN THE MARKET AND COMPETITIVE LANDSCAPE

Companies playing a prominent role in the global tire derived fuel market include Emanuel Tire, ETR Group, Front Range Tire Recycle, Inc., Globarket Tire Recycling LLC, L & S Tire Company, Lakin Tire West Inc., Liberty Tire Recycling, Ragn-Sells Group, Reliable Tire Disposal, Renelux Cyprus Ltd, ResourceCo Pty Ltd, Scandinavian Enviro Systems AB, Tire Disposal & Recycling, Inc. and West Coast Rubber Recycling Inc., and Others.

The competition in the Tire Derived Fuel market is characterized by a fragmented yet evolving landscape where industrial operators, waste processors, and technology providers intersect to shape market dynamics. Dominance is not defined by market share concentration but by operational integration, regulatory compliance, and technological capability. Established cement producers leverage their thermal infrastructure to become primary consumers, while specialized recyclers focus on feedstock preparation and quality assurance. The competitive edge lies in the ability to deliver consistent, low-contaminant TDF that meets combustion efficiency and emission standards. In regions like Europe and North America, competition is mature and regulation-driven, whereas in Asia Pacific and Latin America, early movers are establishing supply chains and technical benchmarks. Strategic alliances between tire processors and industrial end-users are becoming critical differentiators. Innovation in shredding, metal recovery, and real-time monitoring systems further separates leaders from smaller operators. Public perception and environmental scrutiny add complexity, requiring companies to demonstrate transparency and sustainability. As policy frameworks evolve and circular economy mandates gain traction, competition is shifting from cost efficiency to credibility, compliance, and long-term environmental stewardship.

Top Players in the Tire Derived Fuel Market

Liberty Tire Recycling

Liberty Tire Recycling operates one of the most extensive end-of-life tire collection and processing networks globally, with a growing footprint in the Asia Pacific region through strategic partnerships and technology transfer. The company supplies processed Tire Derived Fuel to industrial clients, particularly cement manufacturers, and has established collaboration frameworks with Asian recyclers to support TDF standardization. In 2022, Liberty launched a technical advisory program to assist emerging processors in India and Indonesia in meeting international TDF specifications for moisture, size, and metal content. The company also contributed to the development of ASTM D7520, the standard test method for tire-derived fuel analysis, enhancing global credibility. By sharing operational best practices and combustion efficiency data with kiln operators in Thailand and Vietnam, Liberty has positioned itself as a knowledge enabler in the TDF value chain. Its investment in high-capacity shredding and steel recovery systems ensures consistent fuel quality, making it a preferred partner for co-processing facilities aiming to optimize alternative fuel integration while maintaining emission compliance.

CEMEX

CEMEX has emerged as a global leader in the utilization of Tire Derived Fuel, with its Asia Pacific operations playing a pivotal role in advancing co-processing in cement manufacturing. The company’s plants in the Philippines, Malaysia, and Indonesia have successfully integrated TDF into their thermal processes, achieving alternative fuel substitution rates exceeding 40% in some facilities. In 2023, CEMEX launched its “Future in Action” initiative in Vietnam, investing in a dedicated TDF reception and feeding system at its Binh Duong cement plant to reduce coal dependency and lower carbon intensity. The company collaborates with local waste management authorities to establish tire collection chains, ensuring a reliable feedstock supply. CEMEX’s partnership with the Thailand Greenhouse Gas Management Organisation has enabled third-party verification of emission reductions achieved through TDF use. Additionally, its adoption of real-time combustion monitoring systems ensures compliance with air quality standards. By aligning TDF integration with its broader climate action goals, including a target of 40% alternative fuels by 2030, CEMEX is setting industry benchmarks for sustainable industrial energy practices across the region.

Hermann Püchner GmbH & Co. KG

Hermann Püchner, a German-based specialist in alternative fuel processing, has extended its technological expertise into the Asia Pacific market by supplying advanced TDF preparation systems to industrial operators in Japan, South Korea, and Australia. The company’s shredding and refining technologies are designed to produce high-purity TDF with less than 1% residual steel, meeting stringent combustion efficiency and emission requirements. In 2023, Püchner delivered a turnkey TDF processing line to a cement plant in Fukuoka, Japan, enabling the facility to process 15,000 tons of scrap tires annually for on-site energy recovery. The system incorporates automated metal separation and particle size control, ensuring compatibility with kiln injection systems. Püchner also provides technical training and operational support to local engineers, enhancing long-term system reliability. In Australia, the company partnered with a waste-to-energy facility in New South Wales to retrofit its boiler feed system for TDF use. By focusing on precision engineering and compliance readiness, Hermann Püchner has become a critical enabler of high-efficiency TDF deployment in technologically advanced markets across the region.

RECENT HAPPENINGS IN THE MARKET

- In June 2022, Liberty Tire Recycling launched a technical advisory program for TDF processors in Southeast Asia, providing engineering support and combustion optimization data to improve fuel quality and facilitate integration into cement kilns, enhancing regional supply chain reliability and operational standards.

- In September 2022, CEMEX inaugurated a dedicated Tire Derived Fuel feeding system at its Binh Duong cement plant in Vietnam, enabling the facility to substitute over 40% of its coal consumption with TDF and significantly reducing its carbon footprint in alignment with global decarbonization targets.

- In March 2023, Hermann Püchner delivered a fully automated TDF processing line to a cement facility in Fukuoka, Japan, capable of producing 15,000 tons of high-purity fuel annually, setting a new benchmark for contamination control and combustion efficiency in industrial applications.

- In July 2023, CEMEX partnered with the Thailand Greenhouse Gas Management Organisation to verify emission reductions from TDF co-processing, obtaining third-party certification that strengthens regulatory compliance and enhances corporate sustainability reporting across its Asia Pacific operations.

- In November 2023, Liberty Tire Recycling collaborated with a major Indonesian waste management company to establish a regional TDF hub in Surabaya, integrating tire collection, shredding, and quality control to supply standardized fuel to industrial boilers and cement plants across Java and Sumatra.

MARKET SEGMENTATION

This research report on the global tire derived fuel market has been segmented and sub-segmented based on end-user industry, and region.

By End-User Industry

- Cement Kilns

- Pulp and Paper Mills

- Utility and Industrial Boilers

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

1. What is the definition of Tire Derived Fuel Market ?

Tire-derived fuel is a fuel extracted from all types of employed tires such as whole tires or tires made in uniform flowable parts that meet end-user specifications, Employed tires are an exceptional source of fuel due to their high calorific value.

2. What can be the total Tire Derived Fuel Market value?

The Global Tire Derived Fuels Market was worth USD 459 million in 2024 and is predicted to reach USD 818.64 million in 2033, with a CAGR of 6.64% during the forecast period.

3. Name any three Tire Derived Fuel Market key players?

Lakin Tire West Inc, Liberty Tire Recycling, Ragn-Sells Group are the global Tire Derived Fuel Market Key Players.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com