UK Agricultural Machinery Market Size, Share, Trends & Growth Forecast Report - Segmented By Machinery and By Country - Industry Analysis and Forecast, 2026 to 2034

UK Agricultural Machinery Market Size

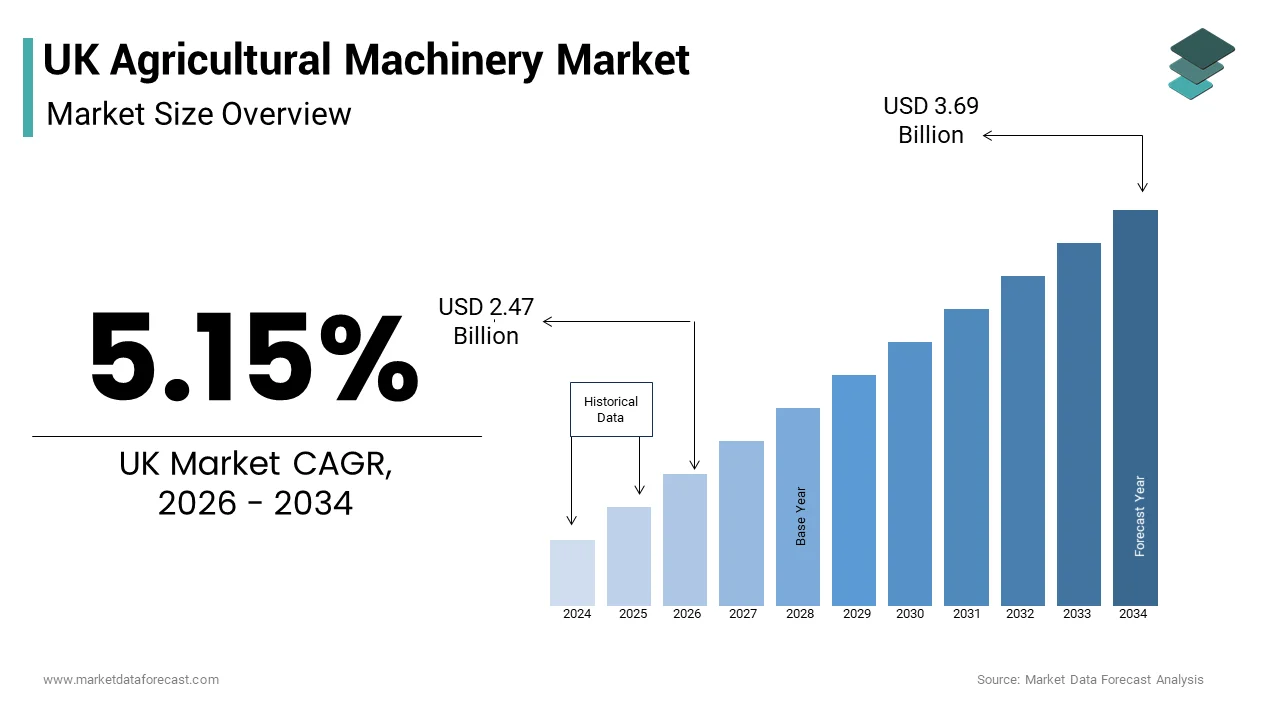

The UK agricultural machinery market size was valued at USD 2.35 billion in 2026 and is anticipated to reach USD 2.47 billion in 2026 to reach USD 3.69 billion by 2034, growing at a CAGR of 5.15% during the forecast period from 2026 to 2034.

The UK agricultural machinery market represents a critical infrastructure sector that underpins the nation's food security and rural economic stability. This industry encompasses the design, manufacture, and distribution of tractors, combine harvesters, planting equipment, and precision farming technologies tailored to the diverse topography and climatic conditions of British farmland. The market is currently undergoing a profound technological transformation driven by the need for efficiency, sustainability, and labor optimization. According to the Department for Environment, Food and Rural Affairs, the total area of farmed land in the UK stands at approximately 17.4 million hectares, providing a substantial operational base for machinery deployment. The demographic landscape of farming is shifting with an aging workforce that requires automation and user friendly interfaces to maintain productivity. Regulatory frameworks, such as the Environmental Land Management schemes, are reshaping investment priorities toward equipment that supports soil health and carbon reduction. The integration of digital connectivity allows for real time data analysis, enabling farmers to make informed decisions about resource allocation. Supply chain dynamics have become increasingly complex, requiring robust logistical networks to ensure timely delivery of spare parts and new units. This ecosystem reflects a broader global trend toward smart agriculture, where mechanical power is augmented by artificial intelligence and satellite navigation. The market serves not only large commercial estates but also smaller, family run holdings that require versatile and cost effective solutions. Stakeholders must navigate evolving environmental standards and economic pressures while delivering innovative tools that enhance yield and reduce ecological footprints.

MARKET DRIVERS

Labor Shortages and the Imperative for Automation Drive Mechanization

Chronic labor shortages across the UK agricultural sector are a key factor propelling the growth of the UK agricultural machinery market. The departure of seasonal workers following changes in immigration policies has created significant gaps in the workforce, particularly during peak harvesting periods. According to the National Farmers Union, over 50% of farms reported difficulties in recruiting sufficient staff, leading to increased reliance on mechanical solutions to maintain operational continuity. This structural shift compels farmers to invest in autonomous tractors, robotic harvesters, and automated milking systems that can operate with minimal human intervention. The high cost of labor compared to capital investment in machinery makes automation an economically viable, long term strategy. Technologies, such as GPS guided steering and variable rate application systems, allow single operators to manage larger areas with greater precision, reducing the need for manual oversight. The urgency to secure harvests and maintain livestock care standards accelerates the replacement cycle of older equipment with smarter, more efficient models. Government initiatives supporting productivity improvements further encourage this transition by offering grants for technology adoption. As the agricultural workforce continues to shrink and age, the demand for machinery that compensates for human labor deficits will intensify. This driver ensures sustained growth in the sales of high tech equipment that enhances productivity per worker. The integration of robotics into daily farm operations is no longer a futuristic concept, but a necessary response to immediate labor market realities.

Government Incentives for Sustainable Farming Practices Stimulate Equipment Upgrades

Government incentives and regulatory mandates promoting sustainable farming practices significantly stimulate demand for modern agricultural machinery in the UK, which is further boosting the UK market expansion. The transition from the European Union Common Agricultural Policy to the domestic Environmental Land Management scheme places a premium on environmental stewardship and carbon reduction. According to the Department for Environment, Food and Rural Affairs, farmers are encouraged to adopt practices that improve soil health, reduce chemical usage, and protect biodiversity. This policy framework drives investment in precision agriculture equipment, such as smart sprayers that minimize herbicide application and no till drills that preserve soil structure. Machinery that enables precise nutrient management helps farmers comply with strict regulations on nitrate runoff and water quality. The availability of grants and subsidies for purchasing eco-friendly equipment lowers the financial barrier to entry for advanced technologies. Farmers recognize that adopting sustainable machinery not only ensures compliance, but also enhances long term land productivity and resilience against climate change. The push toward net zero emissions encourages the exploration of electric and hybrid tractors, which offer lower operating costs and reduced environmental impact. Retailers and manufacturers respond by expanding their ranges of green technologies and providing training on their optimal use. This regulatory and financial support creates a favorable environment for the uptake of innovative machinery that aligns with national sustainability goals. The alignment of economic incentives with environmental objectives ensures a steady demand for equipment that supports responsible land management.

MARKET RESTRAINTS

High Initial Capital Costs and Economic Uncertainty Restrain Investment

The high initial capital costs associated with advanced agricultural machinery, combined with broader economic uncertainty are significant restraints on the UK market. Modern tractors and combine harvesters equipped with precision technology command premium prices, often exceeding several hundred thousand pounds. According to the Agriculture and Horticulture Development Board, rising input costs for fuel, fertilizers, and feed have squeezed farm profit margins, limiting the capital available for major equipment purchases. Many farmers delay upgrading their fleets, opting instead to repair existing machinery to extend its lifespan. The volatility of commodity prices adds another layer of financial risk, making long term investment decisions challenging. High interest rates increase the cost of financing new equipment, further deterring potential buyers who rely on loans or leasing arrangements. Small and medium sized farms are particularly affected, as they lack the economies of scale to absorb these high upfront costs. The return on investment for sophisticated machinery may take several years to realize, which discourages adoption in an unpredictable economic climate. Manufacturers face pressure to offer flexible financing options, but credit tightening by lenders restricts accessibility. This financial constraint slows the turnover of the machinery park and hinders the widespread adoption of the latest innovations. Until economic stability improves and profitability increases, many farmers will remain cautious about committing to substantial capital expenditures.

Supply Chain Disruptions and Component Shortages Delay Deliveries

Persistent supply chain disruptions and component shortages present a major restraint on the UK agricultural machinery market by causing significant delays in production and delivery. The global semiconductor crisis and logistical bottlenecks have affected the availability of critical electronic components required for modern smart farming equipment. According to industry reports, lead times for new tractors and harvesters have extended from months to over a year in some cases, frustrating farmers who need timely replacements. The reliance on international suppliers for specialized parts makes the market vulnerable to geopolitical tensions and trade barriers post Brexit. Customs checks and administrative burdens add complexity and cost to the import process, further slowing down the supply chain. Dealers struggle to manage customer expectations and maintain service levels when inventory is unpredictable. The shortage of spare parts also impacts after sales service, leading to prolonged downtime for existing machinery, which reduces overall farm productivity. Manufacturers are forced to prioritize high margin models, leaving gaps in the entry level and mid-range segments. This instability undermines confidence in the reliability of supply chains and encourages farmers to hold onto older equipment longer than planned. The inability to secure timely deliveries hampers the ability of farmers to capitalize on favorable weather windows for planting and harvesting. These logistical challenges create a bottleneck that constrains market growth and operational efficiency across the sector.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Precision Agriculture Technologies

The integration of artificial intelligence and precision agriculture technologies offers substantial opportunities for growth of the UK agricultural machinery market. Advanced sensors, drones, and machine learning algorithms enable farmers to monitor crop health, soil moisture, and pest levels with unprecedented accuracy. According to McKinsey, precision agriculture solutions can improve yields by up to 15% while reducing input costs by nearly 20%. Machinery manufacturers have the opportunity to develop smart implements that automatically adjust settings based on real time field conditions, optimizing resource use. The demand for interoperable platforms that connect various machines and software systems creates a niche for innovative solutions. Partnerships between machinery makers and tech firms can accelerate the development of user friendly interfaces that simplify complex data interpretation. Farmers are increasingly willing to invest in technologies that provide actionable insights and improve decision making. The rise of farm management software creates opportunities for bundled offerings that combine hardware with digital services. Subscription based models for software updates and data analytics provide recurring revenue streams for manufacturers. As connectivity improves in rural areas, the potential for cloud based monitoring and remote control expands. This technological convergence positions the UK market at the forefront of smart agriculture, attracting investment and fostering innovation. Companies that lead in AI integration can capture premium segments and build strong customer loyalty through enhanced value propositions.

Expansion of Electric and Alternative Fuel Powered Machinery

The expansion of electric and alternative fuel powered machinery presents a significant opportunity for the UK agricultural machinery market as environmental regulations tighten and sustainability becomes a priority. With the government targeting net zero emissions by 2050, there is growing interest in low carbon alternatives to traditional diesel engines. According to energy sector reports, advancements in battery technology are making electric tractors and utility vehicles more viable for short duration and light duty tasks. Manufacturers can capitalize on this trend by introducing hybrid models that reduce fuel consumption and emissions without compromising power. The development of hydrogen fuel cell technology offers potential for heavy duty applications where battery weight is a constraint. Grants and subsidies for green technology adoption lower the financial barrier for farmers transitioning to cleaner equipment. Rural charging infrastructure is gradually improving, supporting the feasibility of electric machinery operations. Brands that pioneer sustainable powertrains can differentiate themselves and appeal to environmentally conscious consumers and corporate buyers. The opportunity extends to retrofitting existing machinery with electric conversion kits, extending asset life and reducing waste. Collaborations with energy providers can create integrated solutions that include renewable energy generation and storage. This shift toward electrification aligns with broader societal goals and opens new markets for innovative engineering. Early movers in this space can establish brand leadership and shape future industry standards.

MARKET CHALLENGES

Volatility in Raw Material Prices Impacts Manufacturing Costs

Volatility in raw material prices poses a major challenge to the UK agricultural machinery market by increasing manufacturing costs and squeezing profit margins. Steel, aluminum, and rare earth metals, essential for constructing durable machinery and electronic components, are subject to fluctuating global commodity prices. According to industry data, sudden spikes in metal costs force manufacturers to either absorb losses or pass them on to consumers through higher prices. This price instability makes long term planning and budgeting difficult for both producers and buyers. Farmers facing tight margins may resist price increases, leading to decreased sales volumes. The unpredictability of supply costs complicates contract negotiations and inventory management. Manufacturers must constantly adjust pricing strategies, which can erode customer trust and brand loyalty. Hedging against commodity risks requires financial expertise and resources that smaller companies may lack. The reliance on imported materials exposes the industry to currency exchange rate fluctuations, adding another layer of financial uncertainty. Efforts to recycle materials and improve design efficiency are necessary, but require significant investment and time to implement. This challenge necessitates agile supply chain management and strategic sourcing partnerships to mitigate risks. Without stable input costs, the competitiveness of UK manufactured machinery in both domestic and export markets may be compromised.

Complexity of Regulatory Compliance and Safety Standards

The complexity of regulatory compliance and stringent safety standards are further challenging the UK agricultural machinery market expansion. Manufacturers must adhere to a myriad of regulations covering emissions, noise levels, operator safety, and environmental impact. According to legal experts, navigating the post Brexit regulatory landscape requires careful attention to both UK specific rules and international standards for export markets. Compliance testing and certification processes are rigorous and time consuming, delaying product launches. Changes in legislation, such as stricter emission limits for non-road mobile machinery, require frequent redesigns and engineering adjustments. The cost of maintaining compliance teams and conducting regular audits adds to operational overheads. Non-compliance can result in hefty fines, product recalls, and reputational damage. The diversity of regulations across different regions complicates the production of standardized models, forcing manufacturers to create multiple variants. Keeping pace with evolving safety requirements for autonomous and connected machinery adds further complexity. Small and medium sized enterprises often struggle with the administrative burden, limiting their ability to innovate. This regulatory maze requires continuous monitoring and adaptation, straining resources. Companies must balance innovation with compliance, ensuring that new features do not violate existing standards. This challenge demands robust legal and technical expertise to navigate successfully.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.15% |

| Segments Covered | By Machinery, Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

| Regions Covered | London, South East, North West, East of England, South West, Scotland, West Midlands, Yorkshire and The Humber, East Midlands, Others |

| Market Leaders Profiled | Deere & Company, CNH Industrial N.V., AGCO Corporation, Kubota Corporation, Claas KGaA mbH, J.C. Bamford Excavators Ltd., Kuhn Group (Bucher Industries AG), SDF Group S.p.A., Bernard Krone Holding SE & Co. KG, Horsch Maschinen GmbH, Amazone-Werke H. Dreyer SE & Co. KG, GRIMME Landmaschinenfabrik GmbH & Co. KG, LEMKEN GmbH & Co. KG, Vaderstad Group |

SEGMENTAL ANALYSIS

By Machinery Insights

The tractors segment dominated the market by capturing the highest share of the global market in 2025 due to their fundamental role as the primary power source for a wide array of farming operations. Unlike specialized equipment that serves single purposes, tractors are versatile machines capable of performing plowing, planting, spraying, and transport tasks when equipped with various implements. According to the Department for Environment, Food and Rural Affairs, there are approximately 17.4 million hectares of farmed land in the UK requiring consistent mechanical intervention throughout the year. The tractor is indispensable for both arable and livestock farms, making it the most widely owned piece of heavy machinery. Farmers prioritize tractors because they offer the highest utility per pound invested, ensuring that every acre can be managed efficiently. The replacement cycle for tractors is regular as older models become less fuel efficient and lack modern connectivity features. High horsepower models are essential for large scale commercial farms, while compact tractors serve smaller holdings and hobby farms. This broad applicability across different farm sizes and types ensures sustained demand. Manufacturers focus heavily on this segment, offering diverse ranges from entry level to high end premium models. The centrality of the tractor to daily farm life means that investment in this category is non-negotiable for operational continuity. This universal need cements the tractor segment as the largest and most stable component of the agricultural machinery market.

However, the harvesting machinery segment is estimated to register a CAGR of 6.4% during the forecast period in the UK agricultural machinery market during the forecast period owing to the acute labor shortages and the urgent need for operational efficiency. The availability of seasonal labor for manual harvesting has declined significantly, which is prompting farmers to invest in mechanized solutions, such as combine harvesters, potato harvesters, and fruit pickers. According to the National Farmers Union, many farms have struggled to secure enough workers for harvest seasons, leading to crop losses and increased reliance on automated machinery. Modern harvesting equipment offers speed and consistency that human labor cannot match, ensuring that crops are gathered at peak quality and within tight weather windows. Advanced sensors and cameras in harvesting machines allow for selective picking and real time quality assessment, minimizing waste. The high initial cost of harvesting machinery is offset by the long term savings in labor costs and reduced crop loss. As farm sizes consolidate and scale increases, the economic justification for owning or leasing high capacity harvesting equipment becomes stronger. The urgency to secure food supply chains and maximize yield per hectare drives this investment trend. Manufacturers are responding with more efficient and gentle harvesting technologies that protect delicate crops. This structural shift toward mechanization ensures that the harvesting machinery segment continues to expand rapidly.

COUNTRY ANALYSIS

The UK held the major share of the European agricultural machinery market in 2025 and is expected to experience steady growth and high adoption rates of automated agri-tech infrastructure over the next few years, maintaining its position as a mature and technologically advanced market within the European agricultural machinery sector characterized by high levels of mechanization and a strong focus on sustainability. As a key player in the region, the UK boasts a sophisticated farming infrastructure that demands high quality and innovative equipment. According to the Agriculture and Horticulture Development Board, the UK agricultural sector contributes significantly to the national economy with a strong emphasis on productivity and environmental stewardship. The market status is robust with a steady demand for replacement machinery and upgrades to precision technologies. Consumers in the UK are well informed and prioritize reliability, after sales support, and digital integration in their purchasing decisions. The regulatory environment is stringent with strict emissions standards and safety regulations governing machinery design and operation. Post Brexit trade arrangements have introduced new dynamics affecting imports and exports, but domestic manufacturing remains resilient. The presence of major international manufacturers and a network of specialized dealers ensures competitive pricing and wide product availability. The UK serves as a testing ground for new technologies, such as autonomous tractors and electric machinery, due to its supportive research ecosystem. This combination of technical expertise, regulatory rigor, and market sophistication ensures that the UK remains a pivotal hub for agricultural innovation and machinery adoption in Europe.

COMPETITIVE LANDSCAPE

The competition in the UK agricultural machinery market is intense and characterized by a mix of global giants and specialized regional manufacturers. Major multinational corporations dominate through extensive product portfolios and strong brand recognition. They leverage economies of scale to offer competitive pricing and advanced technological features. Independent dealers and smaller manufacturers compete by providing personalized service and niche solutions tailored to specific local needs. The rise of precision agriculture has intensified competition in the digital space with companies vying to offer superior data analytics and connectivity. Price sensitivity among farmers due to economic pressures forces manufacturers to balance cost and quality. After sales support and reliability are critical differentiators as downtime can severely impact farm productivity. Innovation in sustainable technologies such as electric and autonomous machinery creates new battlegrounds for market leadership. Companies must continuously adapt to regulatory changes and evolving farmer expectations. This dynamic environment requires agility and strategic investment to maintain relevance and profitability in the long term.

KEY MARKET PLAYERS

A few of the market players that are dominating the UK agricultural machinery market are

- Deere & Company

- CNH Industrial N.V.

- AGCO Corporation

- Kubota Corporation

- Claas KGaA mbH

- J.C. Bamford Excavators Ltd.

- Kuhn Group (Bucher Industries AG)

- SDF Group S.p.A.

- Bernard Krone Holding SE & Co. KG

- Horsch Maschinen GmbH

- Amazone-Werke H. Dreyer SE & Co. KG

- GRIMME Landmaschinenfabrik GmbH & Co. KG

- LEMKEN GmbH & Co. KG

- Vaderstad Group

Top Players in the UK Market

- AGCO Corporation maintains a strong presence in the UK through its renowned brands such as Massey Ferguson and Fendt. The company contributes significantly by providing advanced tractors and harvesting equipment tailored to British farming needs. Recent actions include expanding its precision farming technologies and integrating digital solutions into machinery to enhance operational efficiency. AGCO strengthens its market position by investing in local dealer networks and offering comprehensive training programs for farmers. The company also focuses on sustainability by developing fuel efficient engines and alternative power options. By prioritizing innovation and customer support AGCO ensures it remains a trusted partner for UK agriculturalists seeking reliable and high performance equipment for diverse farming operations.

- CNH Industrial is a major player in the UK agricultural machinery market known for its Case IH and New Holland brands. The company delivers a wide range of equipment from compact tractors to large combine harvesters. Recent actions involve launching autonomous farming solutions and enhancing connectivity features in its latest models. CNH Industrial strengthens its position by collaborating with tech firms to develop smart farming ecosystems that improve productivity. The company also emphasizes sustainable practices by introducing methane powered engines and electric prototypes. Through robust after sales service and innovative product development CNH Industrial continues to meet the evolving demands of UK farmers while driving technological advancement in the sector.

- John Deere holds a prominent position in the UK agricultural machinery market with its iconic green and yellow equipment. The company offers a comprehensive portfolio including tractors sprayers and harvesting machines equipped with cutting edge technology. Recent actions focus on expanding its autonomous capabilities and data analytics platforms to support precision agriculture. John Deere strengthens its market position by enhancing its digital services and providing real time insights to farmers. The company also invests in sustainable engineering by developing electric and hybrid machinery options. With a strong commitment to innovation and customer engagement John Deere remains a leader in delivering efficient and environmentally responsible solutions for UK agriculture.

Top Strategies Used By Key Market Participants

Key players in the UK agricultural machinery market employ several strategic approaches to maintain competitiveness and drive growth. Product innovation is central with companies integrating artificial intelligence and automation into equipment. Sustainability initiatives including electric powertrains and precision application systems are prioritized to meet environmental regulations. Strategic partnerships with technology firms enhance digital capabilities and data analytics offerings. Expansion of after sales services and maintenance contracts builds long term customer loyalty. Flexible financing options are introduced to mitigate high capital costs for farmers. These combined strategies enable key participants to address labor shortages and efficiency demands effectively.

MARKET SEGMENTATION

This research report on the UK agricultural machinery market is segmented and sub-segmented into the following categories.

By Machinery Type

- Tractor

- Less than 50 HP

- 50 to 100 HP

- 100 to 150 HP

- Above 150 HP

- Equipment

- Plows

- Harrows

- Cultivators and Tillers

- Other Equipment (Seed Drills, Rollers, etc.)

- Irrigation Machinery

- Sprinkler Irrigation

- Drip Irrigation

- Other Irrigation Machinery (Center Pivot Systems, Micro Sprinklers, etc.)

- Harvesting Machinery

- Combine Harvesters

- Forage Harvesters

- Other Harvesting Machinery (Potato Harvesters, Beet Harvesters, etc.)

- Haying and Forage Machinery

- Mowers and Conditioners

- Balers

- Other Haying and Forage Machinery (Rakes, Tedders)

- Other Machinery Types

Frequently Asked Questions

What key forces are driving growth in the UK agricultural machinery market?

Rising farm mechanization, labor shortages, and the growing need to improve agricultural productivity are driving market growth.

How is the UK agricultural machinery market organized by equipment category?

The market is organized into tractors, harvesters, planting equipment, spraying machinery, tillage equipment, and precision farming systems.

Which machinery segment generates the highest demand in the UK agricultural machinery market?

Tractors generate the highest demand due to their extensive use in a wide range of farming operations.

What benefits are encouraging farmers to invest in advanced agricultural machinery?

Advanced machinery helps increase operational efficiency, reduce labor dependence, improve accuracy, and enhance crop yields.

Who are the main customers in the UK agricultural machinery market?

Commercial farms, agricultural contractors, cooperatives, and large-scale farming enterprises are the main customers.

How is precision agriculture influencing machinery adoption in the UK?

Precision agriculture is increasing demand for GPS-enabled equipment, automated machinery, and data-driven farming technologies.

What industry trends are transforming the UK agricultural machinery sector?

The adoption of autonomous equipment, smart farming technologies, electric machinery, and digital farm management systems is transforming the sector.

What challenges could impact the growth of the UK agricultural machinery market?

High equipment costs, fluctuating farm incomes, supply chain disruptions, and maintenance expenses could impact market growth.

How are manufacturers enhancing the capabilities of agricultural machinery?

Manufacturers are integrating automation, artificial intelligence, telematics, and real-time monitoring features into modern equipment.

What future opportunities are expected to support the UK agricultural machinery market?

Increasing investment in sustainable farming, precision agriculture, and farm modernization initiatives is expected to create strong growth opportunities.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com