UK Cloud Computing Market Size, Share, Trends & Growth Forecast Report - Segmented By Type, Service, Enterprise, Industry, and By Country - Industry Analysis and Forecast, 2026 to 2034

UK Cloud Computing Market Size

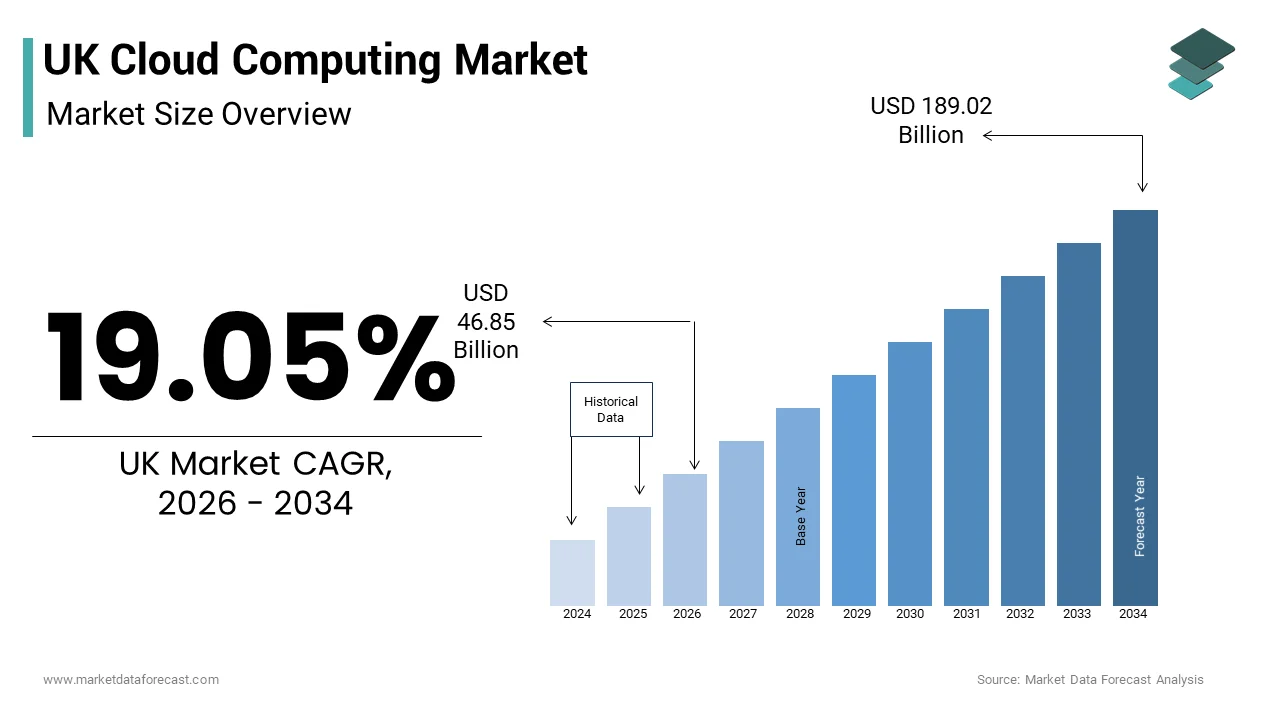

The UK cloud computing market size was valued at USD 39.35 billion in 2025 and is anticipated to reach USD 46.85 billion in 2026 to reach USD 189.02 billion by 2034, growing at a CAGR of 19.05% during the forecast period from 2026 to 2034.

MARKET OVERVIEW AND DEFINITION

Cloud computing is the on-demand delivery of computing services, such as servers, storage, databases, and software, over the internet. The United Kingdom remains the undisputed leader in cloud expenditure across Europe, outpacing countries like Germany and France. Also, the technological paradigm shift has moved beyond mere cost reduction to become a fundamental enabler of business agility and innovation across sectors. As per data from the Office for National Statistics, cloud-based computing has achieved deep penetration across the corporate landscape, with the vast majority of large UK enterprise entities integrating cloud systems into their daily operations. National technology adoption benchmarks show a clear scaling gradient across the corporate spectrum, where mid-sized firms aggressively adopt cloud solutions and small enterprises steadily scale up their infrastructure penetration. The government has mandated that all new public sector technology contracts prioritize cloud first approaches, which accelerates institutional uptake. According to official sector breakdowns from the Department for Science, Innovation and Technology, the digital sector remains a premier driver of national productivity, delivering billions in Gross Value Added (GVA) to the UK economy annually. The regulatory landscape is evolving with the Data Protection and Digital Information Bill aiming to streamline data governance while maintaining high security standards. This environment fosters a mature ecosystem where hyperscalers and specialized providers compete to offer tailored solutions. The integration of artificial intelligence capabilities into cloud platforms further amplifies their strategic value, positioning the market as a central pillar for future economic growth and technological sovereignty in the region.

MARKET DRIVERS

Accelerated Digital Transformation Initiatives Across Enterprise Sectors

The relentless pursuit of digital transformation is a leading factor for cloud adoption in the country, which boosts the growth of the United Kingdom cloud computing market. This shift is driven by an urgent need for operational resilience and competitive advantage. Organizations are increasingly migrating legacy systems to cloud environments to enhance scalability and reduce capital expenditure on physical hardware. The Confederation of British Industry highlights that a significant majority of UK businesses accelerated their digital transformation strategies in the post-pandemic era to safeguard operational resilience and competitiveness. This strategic shift is particularly evident in the financial services sector, where banks and insurance firms leverage cloud platforms to process millions of transactions securely and in real time. Major financial institutions have aggressively adopted hybrid and multi-cloud strategies to modernize their infrastructure, which the Bank of England acknowledges. However, regulators remain primarily focused on managing the concentration risks associated with relying on a small number of dominant cloud service providers. Furthermore, the retail sector utilizes cloud based analytics to manage supply chain complexities and personalize customer experiences. The Office for National Statistics indicates that online sales structurally stabilized after their pandemic peaks, consistently accounting for more than a quarter (roughly 26% to 27%) of all retail spending in the United Kingdom throughout 2023. The healthcare industry also demonstrates significant momentum, with the National Health Service implementing cloud solutions to integrate patient records and support telemedicine services. This widespread organizational commitment to modernizing IT infrastructure ensures sustained demand for cloud services. Companies seek to leverage advanced technologies, such as machine learning and big data analytics, without the burden of managing on-premises data centers.

Stringent Government Policies Promoting Cloud First Strategies

Government mandates and policy frameworks significantly influence the trajectory of the United Kingdom cloud computing market. This establishes a clear directive for public sector digitalization. The Cloud First policy, originally introduced to ensure that public bodies consider cloud solutions before other options, has been reinforced through subsequent digital strategies aimed at improving efficiency and reducing taxpayer costs. Under guidance from the Central Digital and Data Office, the UK public sector actively leverages cloud infrastructure and collaborative ICT procurement frameworks to modernize legacy systems, streamline digital public services, and reduce unnecessary taxpayer spending. This top down approach creates a substantial baseline demand that encourages private sector alignment and standardization. The National Data Strategy emphasizes the importance of secure and sovereign cloud capabilities, prompting investments in local data centers to ensure compliance with data residency requirements. Additionally, the Cyber Security Centre provides guidelines that help organizations navigate the security implications of cloud adoption, thereby reducing hesitation among risk averse entities. The government’s commitment to achieving net zero emissions by 2050 also plays a role, as cloud providers offer more energy efficient solutions compared to traditional on premises servers. Independent environmental assessments and cloud provider infrastructure analyses indicate that migrating typical localized server workloads to optimized hyperscale cloud data centers can significantly reduce energy consumption and lower carbon emissions. These policy driven incentives not only stimulate immediate adoption but also foster a long term ecosystem where cloud computing is viewed as the default standard for reliable and sustainable digital operations.

MARKET RESTRAINTS

Complexities Surrounding Data Sovereignty and Regulatory Compliance

Navigating the intricate landscape of data sovereignty and regulatory compliance is constraining the growth of the United Kingdom cloud computing market. This constraint is particularly visible in the aftermath of Brexit and evolving global privacy laws. Organizations must ensure that their data handling practices align with the UK General Data Protection Regulation, which imposes strict requirements on data storage location and cross border transfers. According to the Information Commissioner’s Office, fines for non compliance can reach up to £17.5 million or 4 percent of global annual turnover, whichever is higher, creating substantial financial risk for businesses. The uncertainty surrounding adequacy decisions with international partners complicates the use of global cloud providers who may store data in multiple jurisdictions. Legal analyses show that European and UK enterprises carefully evaluate data sovereignty and cross-border data transfer legalities when migrating critical workloads to hyperscale cloud providers subject to foreign jurisdictions. This regulatory ambiguity forces companies to invest heavily in legal counsel and compliance infrastructure, increasing the total cost of ownership for cloud solutions. Furthermore, sector specific regulations in healthcare and finance impose additional layers of complexity, requiring specialized cloud configurations that limit the pool of eligible providers. The lack of harmonized standards across different regions means that multinational corporations operating in the UK must maintain fragmented IT architectures, reducing the efficiency gains typically associated with cloud consolidation. These compliance burdens act as a brake on rapid adoption, particularly for small and medium enterprises that lack the resources to navigate such complex legal terrains effectively.

Persistent Shortage of Specialized Cloud Security Expertise

The acute shortage of skilled professionals with expertise in cloud security and architecture is a formidable restraint on the potential of the United Kingdom cloud computing market. This limits the ability of organizations to fully leverage cloud capabilities safely. As cloud environments become more complex, the demand for specialists who can design secure infrastructures and manage identity access controls outpaces the supply of qualified talent. Data published in the official DSIT Cyber Security Labour Market Survey highlights a persistent, though stabilizing, workforce shortfall of roughly 3,800 professionals annually, with advanced cloud architecture and incident response remaining the most critical unfilled skill gaps. This talent scarcity leads to increased labor costs and prolonged recruitment cycles, delaying digital transformation projects. Multiple studies indicate that widespread technical talent shortages frequently force specialized technology departments to leverage premium external consulting and contingent workers to bridge immediate cloud infrastructure engineering gaps. The lack of in house expertise also increases vulnerability to security breaches, as improper configuration remains a leading cause of cloud data leaks. While the National Cyber Security Centre emphasizes robust identity access and security posture management, global industry telemetry from SentinelOne and IBM verifies that over 30% of cloud-based infrastructure data breaches stem directly from asset misconfigurations and user-access oversight. Consequently, many organizations delay migration plans or opt for less optimal hybrid models to maintain control over sensitive data. This skills gap not only hinders operational efficiency but also undermines confidence in cloud security, causing decision makers to prioritize caution over innovation. Addressing this human capital challenge requires substantial investment in training and education, which remains a slow and resource intensive process for the industry.

MARKET OPPORTUNITIES

Expansion of Edge Computing Integration with Cloud Infrastructure

The convergence of edge computing with traditional cloud services offers a strong opening for the United Kingdom cloud computing market. This enables low latency processing for Internet of Things applications and real-time analytics. As the number of connected devices grows, the volume of data generated at the network edge necessitates processing closer to the source to reduce bandwidth costs and improve response times. The rollout of 5G networks across major UK cities facilitates this integration, allowing for seamless data transmission between edge devices and central cloud platforms. Industries such as manufacturing and autonomous transport benefit significantly from this hybrid model, where critical decisions are made locally while aggregate data is analyzed in the cloud for long term insights. The Advanced Manufacturing Research Centre collaborates directly with UK aerospace and industrial manufacturing partners to deploy advanced cloud infrastructure, predictive modeling, and industrial digitization frameworks to optimize modern assembly lines. This trend opens new revenue streams for cloud providers who can offer integrated edge to cloud platforms with standardized management tools. Furthermore, the development of micro data centers in urban areas supports this architecture, reducing the physical distance data must travel. Cloud vendors can capitalize on this technological synergy to overcome the limitations of centralized processing. In doing so, they can offer more versatile solutions that cater to the diverse needs of modern digital enterprises.

Growth of Artificial Intelligence and Machine Learning Workloads

The escalating demand for artificial intelligence and machine learning capabilities drives key possibilities for the United Kingdom cloud computing market. This is because these technologies require vast computational resources and scalable storage solutions. Organizations are increasingly relying on cloud platforms to train complex models and deploy AI applications without the prohibitive cost of building dedicated supercomputing infrastructure. Official tech sector data shows that UK artificial intelligence companies achieved a massive capital milestone by securing £2.4 billion in equity investment, cementing the UK's position as Europe's premier destination for venture-backed AI startups. Cloud providers offer specialized AI chips and managed services that simplify the implementation of machine learning algorithms, making advanced analytics accessible to a broader range of businesses. The healthcare sector, for instance, uses cloud based AI to analyze medical images and accelerate drug discovery. In structural reviews of national computing capabilities, The Alan Turing Institute emphasizes that secure, scalable cloud platforms are vital to fulfilling the UK's long-term digital strategies and supporting academic AI exploration at scale. Similarly, the financial services industry leverages cloud AI for fraud detection and algorithmic trading, processing terabytes of transactional data in real time. This trend is further supported by the availability of pre trained models and automated machine learning tools that reduce the technical barrier to entry. As AI becomes integral to business strategy, the dependency on cloud infrastructure for computational power and data management intensifies. Cloud providers with robust AI ecosystems and strong security features are well positioned to capture this growing segment. This creates deeper engagement and higher spending from enterprise customers seeking to innovate through intelligent automation.

MARKET CHALLENGES

Escalating Risks of Sophisticated Cyber Threats and Data Breaches

The increasing sophistication of cyber threats is a serious obstacle to the United Kingdom cloud computing market. Attackers continually develop new methods to exploit vulnerabilities in cloud environments. Ransomware attacks, phishing campaigns, and advanced persistent threats target cloud infrastructure to steal sensitive data or disrupt operations, causing significant financial and reputational damage. According to the National Cyber Security Centre, the United Kingdom recorded 2,005 cyber incidents between September 2022 and August 2023, with a significant proportion stemming from attackers exploiting vulnerabilities in public-facing applications. The complexity of multi cloud environments exacerbates this risk, as inconsistent security policies across different providers create gaps that malicious actors can exploit. Global data compiled by the Ponemon Institute and IBM Security reveals that the average cost of a data breach for a UK enterprise reached an all-time high of £4.56 million in 2023. Organizations face the dual challenge of securing their own endpoints while ensuring that their cloud providers maintain rigorous defense mechanisms. The shared responsibility model of cloud security often leads to confusion, with many businesses assuming that providers handle all aspects of protection, leaving critical assets exposed. Furthermore, the rise of supply chain attacks, where hackers compromise third party vendors to access larger networks, adds another layer of vulnerability. Maintaining robust security posture requires continuous monitoring, regular audits, and employee training, which strains resources and diverts attention from core business activities. This persistent threat landscape necessitates ongoing investment in advanced security tools and expertise, challenging the perceived simplicity and safety of cloud adoption.

Interoperability Issues in Multi Cloud and Hybrid Environments

Managing interoperability across multi-cloud and hybrid environments remains a major operational hurdle in the UK cloud computing market. Organizations continually struggle to integrate disparate systems and maintain seamless data flows, which can ultimately impact overall enterprise efficiency. Many enterprises adopt a multi cloud strategy to avoid vendor lock in and optimize performance, but this approach often results in fragmented architectures that are difficult to manage and secure. The global Flexera State of the Cloud Report highlights that approximately 87% of enterprises leverage a multi-cloud strategy, with organizations universally citing cloud cost optimization and security visibility as persistent operational hurdles. The lack of standardized APIs and management tools forces IT teams to develop custom integrations, which are time consuming and prone to errors. This complexity increases operational overhead and reduces the agility that cloud computing is supposed to provide. Data silos emerge when information is stored in different formats across various clouds, hindering comprehensive analytics and decision making. The Cloud Security Alliance emphasize that fragmented identity management and inconsistent security posture enforcement across different cloud environments remain major risk vectors for modern enterprises. Furthermore, migrating workloads between different cloud providers remains a technically challenging and costly endeavor, limiting flexibility. Organizations must invest in sophisticated cloud management platforms and employ specialized staff to navigate these interoperability hurdles. Without effective solutions, the benefits of multi cloud strategies are diminished, leading to inefficiencies and increased risk. Addressing these integration challenges requires industry wide collaboration on standards and the development of more unified management tools, which are still evolving in maturity and adoption.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 19.05% |

| Segments Covered | By Type, Service, Enterprise, Industry, Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

| Regions Covered | London, South East, North West, East of England, South West, Scotland, West Midlands, Yorkshire and The Humber, East Midlands, Others |

| Market Leaders Profiled | Bytemark (U.K.), Content Guru (U.K.), Amazon Web Services, Microsoft Azure, Google Cloud Platform, Hosting Services, Inc. (U.K.), Pulsant (U.K.), Krystal Hosting Ltd (U.K.), Centerprise International Limited (U.K.), CloudM (U.K.), Redcentric Plc (U.K.), Databuzz Ltd (U.K.), Littlefish (U.K.), Transparity (U.K.), Cloud (U.K.) |

SEGMENTAL ANALYSIS

By Type Insights

In 2025, the public cloud segment held the majority share of the United Kingdom cloud computing market. This segment maintained supremacy mainly due to its cost efficiency and scalability for diverse business needs. Organizations favor public cloud solutions because they eliminate the need for substantial upfront capital expenditure on hardware and maintenance. Also, the Office for National Statistics indicates that cloud-based computing has become the standard operational framework for large enterprise entities across the United Kingdom, serving as the core of modern IT infrastructure. The ability to scale resources up or down based on demand allows companies to optimize operational costs significantly. This model is particularly attractive for startups and small enterprises that lack the financial resources to build private data centers. The widespread availability of managed services from major hyperscalers further simplifies adoption, enabling businesses to focus on core competencies rather than IT management. In addition, the Confederation of British Industry highlight that UK firms view cloud migration as a vital lever for operational resilience, business agility, and long-term digital modernization. The robust ecosystem of third party applications and integrations available on public platforms enhances their utility, making them indispensable for modern digital operations. The continuous innovation in public cloud offerings, including advanced analytics and artificial intelligence tools, ensures that this segment remains the preferred choice for organizations seeking agility and competitive advantage in a rapidly evolving digital landscape.

However, the hybrid cloud segment is estimated to register the fastest CAGR of 14.2% over the forecast period. This rapid expansion of the segment is fueled by the need for organizations to balance security requirements with the flexibility of public cloud services. Many enterprises retain sensitive data on private infrastructure while leveraging public clouds for less critical workloads, creating a balanced approach to digital transformation. According to the global Flexera State of the Cloud Report, roughly 87% to 89% of enterprise organizations have adopted a multi-cloud or hybrid strategy to avoid vendor lock-in and optimize workloads. The hybrid model allows businesses to maintain compliance with strict data sovereignty regulations while still accessing the innovative capabilities of public cloud providers. This segmentation is particularly crucial for regulated industries such as finance and healthcare, where data privacy is paramount. The Advanced Manufacturing Research Centre actively collaborates with industrial partners to implement secure hybrid cloud models, allowing manufacturers to leverage IoT data analytics while protecting proprietary intellectual property. The development of sophisticated management tools that provide unified visibility across both environments further accelerates adoption. As companies seek to optimize performance and reduce latency for specific applications, the hybrid architecture offers the necessary flexibility. This strategic blend of control and scalability positions hybrid cloud as the most dynamic segment, catering to complex enterprise needs that neither pure public nor private solutions can fully address alone.

By Service Insights

The Software as a Service (SaaS) segment dominated the United Kingdom cloud computing market and accounted for a 43.4% share in 2025. This dominance of the segment was driven by the widespread adoption of collaborative and productivity tools across all business sectors. The shift towards remote and hybrid work models has intensified the demand for cloud based software solutions that enable seamless communication and project management. National technology adoption trends show that Software-as-a-Service (SaaS) applications, particularly cloud-based communication and office suites, represent the most widely adopted cloud service layer across the UK business spectrum. The subscription based pricing model of SaaS reduces financial barriers, allowing organizations to access enterprise grade software without significant upfront investments. This accessibility has democratized technology usage, enabling small and medium enterprises to compete with larger counterparts using similar digital tools. The ease of deployment and automatic updates provided by SaaS vendors ensure that businesses always have access to the latest features and security patches. UK technology ecosystem reports highlight that Software-as-a-Service (SaaS) business models remain a primary driver of venture capital attraction and corporate procurement due to their immediate impact on workforce productivity. The integration of artificial intelligence into SaaS platforms further enhances their value, offering intelligent automation and data insights. The vast ecosystem of specialized SaaS applications catering to niche industry needs ensures continued dominance, as organizations increasingly prefer modular software solutions that can be easily integrated into existing workflows.

On the other hand, the Platform as a Service (PaaS) segment is anticipated to witness the fastest CAGR of 16.8% from 2026 to 2034 due to the increasing complexity of application development and the need for faster time to market. PaaS provides developers with a comprehensive framework that includes operating systems, database management, and development tools, allowing them to focus on coding rather than infrastructure management. According to data from the Department for Science, Innovation and Technology, the UK remains a leading hub for technology startups, with founders heavily utilizing cloud-native platforms to achieve rapid prototyping and deployment. The rise of low code and no code platforms within the PaaS ecosystem enables non technical users to create applications, broadening the user base beyond professional developers. This democratization of development accelerates digital innovation across various industries. The integration of DevOps practices with PaaS solutions further enhances efficiency, enabling continuous integration and delivery pipelines. To combat a competitive technical labor market, enterprise IT departments are increasingly adopting low-code tools and Platform-as-a-Service (PaaS) solutions to streamline the software development lifecycle and optimize existing developer resources. The ability to scale applications automatically based on demand ensures optimal performance during peak usage periods. These factors collectively drive the rapid adoption of PaaS, making it a critical enabler of agile software development and digital transformation initiatives.

By Enterprise Insights

The large enterprises segment led the United Kingdom cloud computing market and captured a 65.8% share in 2025 because of its extensive IT budgets and complex operational requirements that necessitate robust and scalable cloud solutions. The Office for National Statistics indicates a clear digital divide across the UK corporate spectrum, with large enterprise entities leading in cloud adoption while small enterprises scale up their infrastructure at a more gradual pace. These organizations leverage cloud computing to manage vast amounts of data, support global collaborations, and drive innovation through advanced analytics and artificial intelligence. The ability to consolidate disparate IT systems into unified cloud platforms reduces operational complexity and improves efficiency. Large enterprises also benefit from negotiated enterprise agreements with cloud providers, which offer significant cost savings and customized service level agreements. The Bank of England monitors the financial sector's increasing migration to cloud infrastructure, while actively regulating financial institutions to ensure legacy systems and critical transaction processing maintain operational resilience against concentrated cloud outages. Furthermore, the need for business continuity and disaster recovery solutions drives large corporations to adopt multi cloud strategies that ensure resilience against disruptions. The strategic importance of digital transformation in maintaining competitive advantage compels these entities to invest heavily in cloud technologies. Their early adoption and continuous expansion of cloud capabilities set the pace for the broader market, influencing trends and standards that smaller businesses eventually follow.

On the contrary, the small and medium enterprises segment is likely to experience the fastest CAGR of 18.5% during the forecast period owing to the increasing affordability and accessibility of cloud solutions tailored to smaller business needs. Research from the Federation of Small Businesses highlights that expanding digital capabilities and cloud-based software tools are top priorities for UK small-and-medium enterprises looking to boost productivity and lower overhead costs. The shift away from capital intensive on premises infrastructure allows SMEs to allocate resources towards growth initiatives and innovation. Cloud based tools for accounting, customer relationship management, and e commerce enable these businesses to compete effectively in the digital economy. The government’s Digital Growth Plan emphasizes support for SME digitalization, providing grants and training that encourage cloud adoption. UK technology ecosystem reports track a structural shift in how small-and-medium enterprises operate, with remote and hybrid work models driving a permanent baseline adoption of cloud-hosted collaboration tools. The availability of pay as you go pricing models reduces financial risk, allowing smaller firms to experiment with new technologies without long term commitments. As digital literacy improves among SME owners, the perceived complexity of cloud migration decreases, further accelerating uptake. This segment’s agility and willingness to adopt new technologies position it as a key driver of future market growth.

By Industry Insights

The Banking, Financial Services, and Insurance (BFSI) segment was the largest in the United Kingdom cloud computing market and occupied a 24.5% share in 2025. This prominence of the segment was supported by the critical need for secure, scalable, and compliant data processing capabilities. Financial institutions leverage cloud technologies to enhance customer experiences, streamline operations, and develop innovative financial products. While UK banking institutions heavily leverage hybrid and multi-cloud environments to improve agility, regulators closely monitor these architectures to manage compliance with operational resilience frameworks. The sector’s reliance on real time data analytics for fraud detection and risk assessment necessitates the computational power provided by cloud platforms. Cloud based solutions enable insurers to process claims faster and personalize policies based on detailed customer data. The Financial Conduct Authority has issued guidelines that facilitate cloud adoption by clarifying regulatory expectations, thereby reducing uncertainty for financial firms. In addition, the ability to scale resources during peak transaction periods ensures service reliability and customer satisfaction. Furthermore, the integration of artificial intelligence and machine learning in cloud environments supports advanced trading algorithms and personalized banking services. This strategic investment underscores the sector’s commitment to digital transformation, maintaining its position as the leading industry in cloud adoption.

But the healthcare segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 19.3% between 2026 and 2034. This quick surge is fuelled by the urgent need to digitize patient records, support telemedicine services, and enable collaborative research. The National Health Service has prioritized cloud adoption as part of its Long Term Plan, aiming to create a unified digital infrastructure that improves patient care and operational efficiency. Under strategic guidelines from NHS England, regional healthcare trusts are encouraged to transition legacy patient records and operational data to secure cloud environments to facilitate better regional data interoperability. The COVID-19 pandemic accelerated the adoption of telehealth solutions, which rely heavily on cloud infrastructure for video consultations and remote monitoring. Policy papers from The King’s Fund emphasize that integrated data analytics and modern digital infrastructure are essential tools for optimizing NHS resource allocation and managing public health workloads. The integration of Internet of Medical Things devices with cloud platforms allows for real time patient monitoring and early intervention. Regulatory frameworks such as the Data Security and Protection Toolkit ensure that cloud providers meet stringent security standards, building trust among healthcare organizations. The potential for cloud enabled artificial intelligence to assist in diagnosis and treatment planning further drives investment. This transformative impact on patient outcomes and operational efficiency positions healthcare as the most dynamic growth segment in the market.

COUNTRY ANALYSIS

In 2025, the United Kingdom remained the top performer in the cloud computing market in Europe. The demand for cloud computing in the UK was driven by high penetration rates across all business sizes, with a strong emphasis on security and compliance. It is characterized by a mature digital infrastructure and a proactive regulatory environment that fosters innovation. According to official national data, the digital economy contributes over £300 billion ($385 billion) annually to the UK economy, with cloud services and advanced infrastructure acting as core drivers of this national productivity. The government’s Cloud First policy has been instrumental in driving public sector adoption, setting a benchmark for private industry. The presence of major hyperscale data centers operated by global providers ensures low latency and high availability for domestic users. International benchmarks like the IMD Business School World Digital Ranking place the UK 19th globally in overall digital competitiveness. However, the nation remains Europe's top scaling tech ecosystem and a primary destination for foreign digital technology investments. The post Brexit regulatory framework, including the Data Protection and Digital Information Bill, aims to streamline data governance while maintaining high standards, attracting international investment. The concentration of fintech and healthtech startups in London and other major cities creates a vibrant ecosystem that demands advanced cloud capabilities. The commitment to net zero emissions by 2050 also influences market dynamics, with providers investing in energy efficient data centers. This combination of policy support, infrastructure quality, and economic demand solidifies the UK’s position as a leader in the European cloud computing landscape.

COMPETITIVE LANDSCAPE

The competition in the United Kingdom cloud computing market is intense and characterized by the presence of global hyperscalers alongside specialized regional providers. Major international players leverage their vast resources and extensive service portfolios to dominate the enterprise segment while niche firms focus on specific industry verticals or specialized technologies. Differentiation occurs through superior customer support, localized data centers, and compliance with stringent UK data protection regulations. Price competition remains fierce particularly for standard infrastructure services prompting providers to bundle value added services such as security and analytics. Strategic acquisitions and partnerships are common tactics used to expand capabilities and enter new market segments. The rise of hybrid and multi cloud architectures has intensified competition as vendors strive to offer seamless integration and management tools. Innovation in artificial intelligence and edge computing serves as a key battleground for capturing future growth. Regulatory compliance and sustainability commitments increasingly influence purchasing decisions adding layers of complexity to competitive dynamics. This dynamic environment drives continuous improvement and innovation benefiting customers through enhanced services and reduced costs.

KEY MARKET PLAYERS

A few of the market players that are dominating the UK cloud computing market are

- Bytemark (U.K.)

- Content Guru (U.K.)

- Amazon Web Services

- Microsoft Azure

- Google Cloud Platform

- Hosting Services, Inc. (U.K.)

- Pulsant (U.K.)

- Krystal Hosting Ltd (U.K.)

- Centerprise International Limited (U.K.)

- CloudM (U.K.)

- Redcentric Plc (U.K.)

- Databuzz Ltd (U.K.)

- Littlefish (U.K.)

- Transparity (U.K.)

- cloud (U.K.)

Top Players In The Market

- Amazon Web Services maintains a dominant presence in the United Kingdom through its extensive infrastructure and comprehensive service portfolio. The company operates multiple availability zones across London and other regions to ensure high availability and low latency for local customers. Recent initiatives include significant investments in renewable energy sources to power its data centers, aligning with national sustainability goals. Amazon Web Services actively collaborates with UK government bodies to support digital transformation projects in healthcare and education. The provider continuously expands its artificial intelligence and machine learning capabilities tailored for British enterprises. By offering specialized compliance tools for UK data protection regulations, it addresses critical security concerns. The company also invests heavily in training programs to upskill the local workforce in cloud technologies. These strategic efforts reinforce its position as a preferred partner for organizations seeking scalable and secure cloud solutions.

- Microsoft Azure leverages its strong enterprise relationships and integrated software ecosystem to drive substantial adoption across the United Kingdom. The company operates several data center regions within the country to meet strict data residency requirements and ensure optimal performance. Microsoft recently announced major expansions in its AI infrastructure to support growing demand for generative AI services among UK businesses. It partners extensively with public sector organizations to modernize legacy systems and improve citizen services through cloud based solutions. The integration of Azure with popular productivity tools enhances user experience and drives seamless workflow adoption. Microsoft also focuses on cybersecurity enhancements by offering advanced threat protection features tailored to the UK regulatory landscape. Its commitment to carbon negative operations resonates with environmentally conscious organizations. These actions solidify its role as a key enabler of digital innovation and operational efficiency in the region.

- Google Cloud Platform strengthens its foothold in the United Kingdom by emphasizing data analytics and open source technologies. The company established its first cloud region in London to provide localized services and comply with data sovereignty laws. Google Cloud actively engages with UK startups and scale ups through dedicated accelerator programs that provide technical resources and mentorship. It collaborates with academic institutions to advance research in artificial intelligence and quantum computing. The platform offers robust tools for sustainable business practices, helping organizations track and reduce their carbon footprints. Google Cloud also enhances its security offerings with advanced encryption and identity management features designed for regulated industries. Its focus on hybrid and multi cloud solutions appeals to enterprises seeking flexibility and vendor neutrality. Google Cloud positions itself as an innovative and collaborative partner in the UK digital economy. It achieves this by fostering a vibrant developer community and supporting open standards.

Top Strategies Used By Key Market Participants

Key players in the United Kingdom cloud computing market primarily employ strategies centered on infrastructure expansion and strategic partnerships to enhance their competitive positioning. Companies invest heavily in building local data centers to ensure low latency and compliance with data residency regulations. They frequently collaborate with government entities and industry leaders to drive large scale digital transformation initiatives. Developing specialized artificial intelligence and machine learning tools tailored to specific sectors such as finance and healthcare is another common approach. Providers also focus on sustainability by powering operations with renewable energy to align with national net zero targets. Enhancing cybersecurity offerings through advanced threat detection and compliance frameworks helps address growing security concerns. Additionally, firms invest in workforce training programs to bridge the skills gap and foster customer loyalty. These multifaceted strategies enable providers to differentiate their services and capture diverse market segments effectively.

MARKET SEGMENTATION

This research report on the UK cloud computing market is segmented and sub-segmented into the following categories.

By Type

- Public Cloud

- Private Cloud

- Hybrid Cloud

By Service

- Infrastructure as a Service (IaaS)

- Platform as a Service (PaaS)

- Software as a Service (SaaS)

By Enterprise Type

- SMEs

- Large Enterprises

By Industry

- BFSI

- IT and Telecommunications

- Government

- Consumer Goods and Retail

- Healthcare

- Manufacturing

- Others

Frequently Asked Questions

What is accelerating the adoption of cloud computing solutions across the UK?

Digital transformation initiatives, increasing remote work adoption, and growing demand for scalable IT infrastructure are accelerating cloud computing adoption.

How is the UK cloud computing market categorized by deployment model?

The market is categorized into public cloud, private cloud, hybrid cloud, and multi-cloud deployment models.

Which cloud service model generates the highest revenue in the UK cloud computing market?

Software-as-a-Service (SaaS) generates the highest revenue due to widespread adoption across businesses of all sizes.

Why are organizations migrating their workloads to cloud platforms?

Organizations are migrating to improve operational flexibility, reduce infrastructure costs, enhance security, and support business agility.

Who are the major users of cloud computing services in the UK?

Enterprises, government agencies, healthcare providers, financial institutions, educational organizations, and SMEs are major users.

How is cloud computing transforming business operations in the UK?

It enables faster innovation, improves collaboration, supports data-driven decision-making, and enhances operational efficiency.

What technology trends are influencing the UK cloud computing market?

Artificial intelligence integration, edge computing, serverless computing, hybrid cloud strategies, and cloud-native application development are influencing the market.

What challenges could affect the growth of the UK cloud computing industry?

Data privacy concerns, cybersecurity risks, regulatory compliance requirements, and cloud migration complexities could affect growth.

How are cloud providers enhancing their competitive position in the market?

Providers are expanding data center capacity, introducing advanced security solutions, and offering industry-specific cloud services.

What opportunities are expected to drive the future expansion of the UK cloud computing market?

Increasing digitalization, growing adoption of AI and analytics, demand for business continuity solutions, and investment in next-generation technologies are expected to drive market expansion.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com