UK Digital Advertising Market Size, Share, Trends, and Growth Analysis Report, Segmented by Advertising Format, Platform, Vertical, Target Audience and Country – Industry Forecast From 2026 to 2034

Market Size, 2025

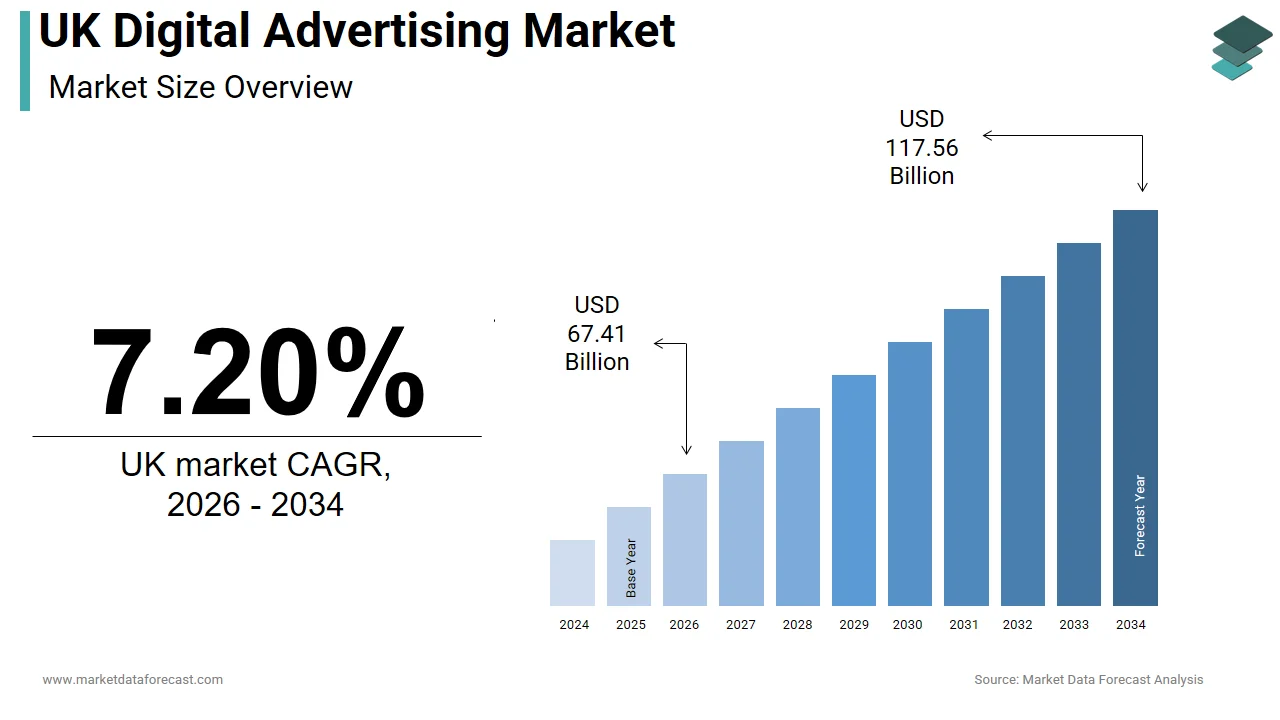

$62.88 BnMarket Estimate, 2026

$67.41 BnMarket Forecast, 2034

$117.56 BnCAGR, 2026–2034

7.20%UK Digital Advertising Market Report Summary

The UK digital advertising market was valued at USD 62.88 billion in 2025 and is projected to grow from USD 67.41 billion in 2026 to USD 117.56 billion by 2034, registering a CAGR of 7.20% from 2026 to 2034. Market growth is driven by increasing internet penetration, rising mobile device usage, and growing investments in data-driven marketing strategies. Businesses across industries are increasingly leveraging digital advertising channels to enhance customer engagement, improve brand visibility, and achieve measurable marketing outcomes. The rapid expansion of e-commerce, advancements in artificial intelligence-driven advertising technologies, and growing adoption of programmatic advertising are further supporting market growth across the United Kingdom.

Key Market Trends

- Rising adoption of programmatic and AI-powered advertising solutions.

- Increasing shift of marketing budgets from traditional media to digital channels.

- Growing importance of mobile-first advertising strategies.

- Expansion of data analytics and personalized advertising campaigns.

- Increasing investment in video advertising, social media marketing, and retail media networks.

Segmental Insights

- Based on advertising format, the search advertising segment dominated the UK digital advertising market in 2025 by accounting for 39.2% market share, driven by its ability to deliver highly targeted campaigns, measurable performance, and strong return on investment for advertisers.

- Based on platform, the mobile applications segment led the market by capturing 63.8% share in 2025, supported by increasing smartphone usage, growing app engagement, and the expansion of mobile commerce activities.

- Based on vertical, the retail segment held the largest share of 21.5% in 2025, driven by intense competition among online retailers, growing e-commerce sales, and the ability of digital advertising platforms to provide measurable conversion outcomes.

Regional Insights

The United Kingdom dominated the European digital advertising market in 2025 by accounting for 22.6% share, supported by a highly developed digital economy, widespread internet penetration, and strong adoption of advanced advertising technologies. The country's mature e-commerce ecosystem, robust digital infrastructure, and growing demand for personalized advertising experiences continue to drive market growth.

Competitive Landscape

The UK digital advertising market is characterized by intense competition among technology companies, advertising platforms, and media agencies focusing on innovation, audience targeting, and data-driven campaign optimization. Market participants are emphasizing artificial intelligence, machine learning, and advanced analytics capabilities to improve advertising effectiveness and customer engagement. Strategic partnerships, acquisitions, and investments in programmatic advertising and retail media solutions are shaping competitive dynamics across the market.

Prominent companies operating in the UK digital advertising market include Google, Meta, Amazon, Alibaba, Microsoft, Apple, Verizon, WPP, and Dentsu.

UK Digital Advertising Market Size

The size of the UK digital advertising market was worth USD 62.88 billion in 2025. The market is anticipated to grow at a CAGR of 7.20% from 2026 to 2034 and be worth USD 117.56 billion by 2034 from USD 67.41 billion in 2026.

Digital advertising is the practice of promoting products, services, or brands through paid placements on online platforms, such as social media, search engines, websites, and mobile apps. The UK boasts one of the most developed and largest digital advertising markets in the world, heavily dominating the overall advertising sector. This market has evolved beyond traditional banner placements into an intricate network of programmatic transactions, real-time bidding, and data-driven personalization strategies. The landscape is characterized by high penetration of mobile devices and widespread broadband access, which facilitates continuous consumer connectivity. According to the Office for National Statistics (ONS), 96% of households in Great Britain had internet access in 2020. Recent estimates suggest this figure has continued to rise, reaching approximately 97–98% in 2023, reflecting a highly mature digital infrastructure. According to Ofcom's Online Nation 2023 report, the average UK adult spent 3 hours and 41 minutes online daily. This figure rose to 4 hours and 20 minutes in the 2024 report, creating substantial inventory for advertisers. This environment fosters intense competition among technology providers, media owners, and agencies who strive to optimize return on investment through advanced analytics and artificial intelligence tools. The regulatory framework, including the General Data Protection Regulation and local privacy laws, shapes how data is collected and utilized, ensuring consumer protection while enabling targeted campaigns. The transition from third-party cookies to first-party data strategies marks a significant shift in operational methodologies. Brands increasingly prioritize direct relationships with audiences to maintain effectiveness amidst changing privacy standards. The integration of commerce media and shoppable ads further blurs the lines between content and transaction, creating seamless pathways for conversion.

MARKET DRIVERS

Surging Mobile Device Penetration Drives Ad Inventory Expansion

The proliferation of smartphones and tablets is the main reason behind the growth of the United Kingdom's digital advertising market. This mobile ubiquity accelerates expansion by expanding available ad inventory and facilitating constant consumer engagement. Mobile devices have become the primary screen for most users, allowing advertisers to reach audiences throughout their daily routines regardless of location. According to research, mobile phone penetration in the United Kingdom reached an exceptionally mature market phase by 2023, with approximately 97% of adults reported as active mobile users, emphasizing an almost ubiquitous reach for digital campaigns. This widespread adoption ensures that digital advertisements can achieve extensive reach and frequency, which are critical metrics for brand awareness campaigns. The convenience of mobile access means that consumers interact with social media platforms, news applications, and entertainment services for extended periods, thereby increasing the opportunities for ad impressions. As per Ofcom data, adults in the United Kingdom spent an average of 3 hours and 41 minutes per day online across all digital platforms in 2023. While mobile screen time has steadily grown to match traditional television viewing, the two media remain highly competitive for consumer attention. This behavioral shift compels advertisers to allocate larger portions of their budgets toward mobile-optimized formats such as vertical video stories and in-app displays. The technical capabilities of modern smartphones, including high-resolution screens and fast processors, enable rich media experiences that capture attention more effectively than static images. Furthermore, the integration of location-based services allows for hyperlocal targeting, which enhances relevance and drives foot traffic to physical stores. Advertisers leverage geofencing and beacon technology to deliver timely messages when consumers are near points of interest. The seamless transition between mobile and other devices through cross-device tracking ensures consistent messaging and improves attribution accuracy. This omnipresence of mobile technology creates a resilient foundation for sustained advertising expenditure growth.

E-Commerce Growth Fuels Performance-Based Advertising Demand

The robust expansion of the online retail sector directly stimulates demand for performance-oriented digital advertising as businesses seek to acquire customers and drive sales through measurable channels, which in turn propels the expansion of the United Kingdom digital advertising market. E-commerce has transformed from a supplementary sales channel into a primary revenue stream for many retailers, necessitating aggressive customer acquisition strategies. According to the Office for National Statistics, online sales accounted for 27 percent of total retail sales in the United Kingdom in 2023, demonstrating the critical role of digital platforms in commercial transactions. This shift prompts retailers to invest heavily in search engine marketing, social commerce, and retargeting campaigns that deliver immediate return on investment. The ability to track user journeys from impression to purchase provides advertisers with clear visibility into campaign effectiveness, which justifies continued spending. As per data from the Interactive Advertising Bureau (IAB UK), paid search alone constitutes 50% of total digital ad spend in the United Kingdom, standing as the primary driver of performance marketing budget allocations. The rise of marketplace platforms such as Amazon and eBay has further intensified competition, requiring brands to bid for visibility through sponsored product listings and display ads within these ecosystems. Advanced attribution models allow marketers to understand the contribution of each touchpoint in the conversion funnel, enabling optimization of bid strategies and creative assets. The integration of shopping features within social media platforms like Instagram and TikTok enables seamless purchasing experiences, which reduces friction and increases conversion rates. Advertisers utilize dynamic product ads that automatically showcase items based on user browsing history, ensuring high relevance. The seasonal spikes in online shopping during events like Black Friday and Christmas drive temporary surges in advertising demand as brands compete for consumer attention. This cyclical pattern reinforces the dependency of e-commerce entities on digital advertising to sustain growth and market share.

MARKET RESTRAINTS

Privacy Regulations Limit Data Collection Capabilities

Stringent privacy laws and regulatory frameworks impose significant constraints on the ability of advertisers to collect and utilize consumer data, which impedes the growth of the United Kingdom's digital advertising market. Consequently, this limitation undermines the precision of targeted campaigns. The implementation of the General Data Protection Regulation (GDPR) and the UK Data Protection Act restricts unauthorized tracking, but allows organizations to utilize multiple lawful bases, such as Legitimate Interests, to process data for personalization without always requiring explicit consent. According to the Information Commissioner's Office (ICO) annual data, organizations submitted 11,680 data breach reports in 2023/24. This high volume reflects strict corporate adherence to legal reporting windows, though fewer than 1% of total notifications resulted in formal regulatory penalties. This regulatory environment forces advertisers to rely on less granular data sets, which reduces the effectiveness of audience segmentation and targeting strategies. The phasing out of third-party cookies by major browsers such as Chrome and Safari disrupts established tracking mechanisms that have long been the backbone of programmatic advertising. According to industry tracking by IAB Europe, the percentage of advertisers who felt confident and prepared for cookie deprecation dropped from 78% in 2022 to 60%, highlighting growing anxiety regarding campaign measurement and attribution alternatives. The loss of cross-site tracking capabilities makes it difficult to build comprehensive user profiles, leading to broader and less relevant ad placements. Advertisers must now invest in alternative solutions such as contextual targeting and clean rooms, which require substantial technological upgrades and operational changes. The complexity of obtaining valid consent through cookie banners often results in lower opt-in rates, further shrinking the addressable audience. Consumers are increasingly aware of their privacy rights and frequently choose to block trackers or use private browsing modes, which exacerbates the data scarcity issue. This fragmentation of data sources complicates the measurement of return on ad spend and challenges the justification of digital advertising budgets. The need to comply with varying regulations across different regions adds administrative burden and increases compliance costs for multinational campaigns.

Ad Fraud and Brand Safety Concerns Erode Trust

The prevalence of fraudulent activities and brand safety risks is a persistent threat to the integrity of the United Kingdom's digital advertising market. These risks cause financial losses and reputational damage for advertisers. Invalid traffic generated by bots and automated scripts inflates impression counts without delivering genuine human engagement, resulting in wasted advertising spend. The systematic deception undermines confidence in digital channels and prompts advertisers to demand greater transparency and verification from their partners. Brand safety issues arise when advertisements appear alongside inappropriate or harmful content, such as hate speech, misinformation, or illegal activities, which can negatively impact brand perception. High-profile incidents where major brands withdrew spending from certain platforms highlight the severity of this challenge and the potential for public relations crises. Advertisers must invest in sophisticated verification tools and manual review processes to ensure their messages appear in suitable contexts, which increases operational costs. The complexity of the programmatic supply chain with multiple intermediaries makes it difficult to trace the origin of traffic and verify the authenticity of inventory. Fraudsters continuously evolve their tactics using sophisticated techniques to mimic human behavior, making detection increasingly challenging. The lack of standardized industry metrics for measuring fraud and brand safety creates confusion and inconsistency in reporting. Advertisers often struggle to reconcile discrepancies between different verification providers, leading to disputes over billing and performance claims. This environment of uncertainty discourages some brands from fully committing to digital channels and limits the overall growth potential of the market.

MARKET OPPORTUNITIES

Emergence of Connected Television Offers New Engagement Avenues

The rapid adoption of connected television offers a lucrative opportunity for advertisers in the United Kingdom digital advertising market. This shift allows them to reach audiences through premium video content on large screens with enhanced targeting capabilities. Streaming services have gained immense popularity as consumers shift away from traditional linear television towards on-demand viewing experiences. According to Ofcom’s Media Nations 2023 report, the number of households subscribing to at least one subscription video-on-demand (SVOD) service in the United Kingdom reached approximately 19 million (66%) in Q1 2023, reflecting a mature market that has plateaued after pandemic-driven peaks. This trend enables advertisers to deliver high-impact video advertisements in a lean-back environment where viewers are highly engaged and less likely to skip content. Connected television platforms offer detailed viewer data, allowing for precise audience segmentation based on demographics, interests, and viewing habits. As per a forecast by Magna Global, connected television (CTV) advertising revenues in the United Kingdom were projected to grow by 32.7% in 2023. Post-year data confirms that while CTV remains a high-growth format, broader digital video ad spend grew by approximately 11% amidst a stabilizing economic environment. The ability to combine the reach of television with the measurability of digital advertising makes connected television an attractive option for brands seeking both awareness and performance outcomes. Interactive features such as shoppable ads and QR codes enable viewers to take immediate action, bridging the gap between viewing and purchasing. The consolidation of streaming services and the introduction of ad-supported tiers by major platforms like Netflix and Disney+ expand the available inventory and lower entry barriers for smaller advertisers. Programmatic buying of connected television inventory allows for real-time optimization and efficient budget allocation across multiple publishers. The integration of connected television data with other digital channels facilitates cross-device attribution, providing a holistic view of campaign effectiveness. Advertisers can leverage sequential messaging to tell compelling stories across different screens, enhancing brand recall and engagement. The premium nature of connected television content ensures that advertisements are associated with high-quality productions, which enhances brand perception.

Artificial Intelligence Enhances Personalization and Efficiency

The integration of artificial intelligence and machine learning technologies unlocks potential for the United Kingdom's digital advertising market. These tools are driving greater relevance and efficiency in digital advertising campaigns across the country. These advanced algorithms analyze vast amounts of data to identify patterns and predict consumer behavior, enabling highly personalized ad experiences. AI-powered tools automate routine tasks such as bid management, creative optimization, and audience segmentation, freeing up marketers to focus on strategic initiatives. Generative artificial intelligence allows for the rapid creation of diverse ad variations tailored to specific audience segments, which improves testing capabilities and performance. Predictive analytics help advertisers anticipate customer needs and deliver timely messages that resonate with individual preferences, increasing conversion probabilities. Natural language processing enables sentiment analysis of social media conversations, allowing brands to adjust their messaging in real time based on public opinion. Chatbots and virtual assistants powered by artificial intelligence provide personalized customer support and guide users through the purchase journey, enhancing the overall experience. The ability to process and analyze unstructured data from various sources provides deeper insights into consumer motivations and pain points. AI-driven attribution models offer more accurate assessment of channel contributions, helping advertisers optimize budget allocation across the marketing mix. The continuous learning capability of machine learning systems ensures that campaigns improve over time, adapting to changing market conditions and consumer behaviors. This technological advancement enables smaller businesses to compete with larger enterprises by accessing sophisticated tools that were previously cost-prohibitive.

MARKET CHALLENGES

Fragmentation of Media Channels Complicates Measurement

The increasing fragmentation of media channels and devices creates major obstacles for advertisers in the United Kingdom digital advertising market. Therefore, these marketers face significant challenges when trying to measure campaign effectiveness and attribute conversions accurately. Consumers interact with brands across multiple touchpoints, including social media, search engines, email, websites, and mobile applications, making it difficult to track the complete customer journey. According to the Interactive Advertising Bureau (IAB), cross-channel measurement remains a paramount focus, with 72% of advertisers prioritizing cross-platform strategies, even as data restrictions have caused brand confidence in partner data accuracy to fluctuate between 52% and 59%. The lack of a unified identifier across platforms prevents seamless tracking of users as they move between different environments, leading to incomplete data sets. This fragmentation results in duplicated efforts and inefficient budget allocation as advertisers may overinvest in channels that appear effective in isolation but contribute less to overall goals. The divergence in measurement standards between walled gardens like Facebook and Google and open web publishers further complicates comparison and optimization. Advertisers often receive conflicting reports from different analytics providers, making it challenging to determine the true return on investment. The reliance on last click attribution models fails to account for the influence of upper funnel activities such as brand awareness campaigns, which play a crucial role in driving eventual conversions. The absence of standardized frameworks for multi-touch attribution leads to subjective interpretations of data and biased decision-making. Small and medium-sized enterprises particularly suffer from this complexity as they lack the resources to invest in advanced measurement tools and expertise. The inability to demonstrate clear value hinders the justification of digital advertising budgets and limits strategic planning capabilities.

Talent Shortage Hinders Strategic Implementation

The scarcity of skilled professionals with expertise in digital advertising technologies data analytics and strategic planning poses a significant challenge to the growth and sophistication of the United Kingdom market. The rapid evolution of advertising technologies requires continuous learning and adaptation which many existing workforces struggle to keep pace with. Also, the shortage limits the ability of organizations to fully leverage advanced tools such as programmatic platforms artificial intelligence and data management systems. The lack of experienced personnel results in suboptimal campaign execution, missed opportunities for innovation and increased reliance on external vendors. Training existing employees requires significant time and financial investment which may not yield immediate returns. The high turnover rate in the digital marketing sector further destabilizes teams and disrupts continuity in strategy implementation. Junior staff often lack the strategic perspective needed to align advertising efforts with broader business objectives leading to tactical rather than strategic approaches. The complexity of privacy regulations and compliance requirements demands specialized knowledge that is in short supply increasing the risk of legal violations. Organizations struggle to build internal capabilities and often depend on fragmented agency partnerships which can lead to inconsistent messaging and inefficiencies. The talent crisis also drives up salary expectations increasing operational costs for agencies and in house marketing departments. This constraint slows down the adoption of new technologies and limits the overall competitiveness of the United Kingdom digital advertising ecosystem.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Advertising Format, Platform, Vertical, Target Audience, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | United Kingdom |

| Market Leaders Profiled | Google, Meta, Amazon, Alibaba, Microsoft, Apple, Verizon, WPP, Dentsu. |

SEGMENTAL ANALYSIS

By Advertising Format Insights

The search advertising segment was the largest in the United Kingdom digital advertising market and occupied a 39.2% share in 2025. Its unparalleled ability to capture high-intent users at the precise moment of purchase consideration has supported the prominence of this segment. This format leverages user queries to deliver highly relevant sponsored results, ensuring that advertisements align directly with consumer needs and interests. The fundamental strength of search advertising lies in its capacity to target individuals who are actively seeking specific products or services resulting in significantly higher conversion rates compared to passive display formats. In addition, the financial efficiency compels advertisers across various sectors to prioritize search budgets as a core component of their marketing mix. The immediacy of search intent means that users are further along in the decision-making process reducing the friction typically associated with brand discovery. Moreover, the disparity highlights the effectiveness of matching ad content with explicit user demand. Furthermore, the integration of shopping ads within search results allows retailers to showcase product images prices and reviews directly in the search engine results page which streamlines the path to purchase. The ability to measure performance through clear metrics such as cost per acquisition and return on ad spend provides advertisers with the transparency needed to justify continued investment. The maturity of keyword bidding ecosystems ensures that advertisers can compete effectively for valuable terms while optimizing budgets through automated bidding strategies. This combination of intent targeting and measurable outcomes solidifies the dominance of search advertising in the overall market landscape.

The continuous evolution of search engine algorithms has significantly improved the relevance and quality of ad placements thereby increasing user engagement and advertiser satisfaction. Modern search platforms utilize machine learning to understand the semantic meaning behind queries rather than relying solely on exact keyword matches. The technological advancement allows advertisers to reach a wider audience without sacrificing relevance as the system identifies related searches that indicate similar intent. The integration of natural language processing enables search engines to interpret complex queries and long tail keywords which often represent niche but highly valuable market segments. Advertisers who leverage these long tail opportunities can achieve lower competition and higher conversion rates. The dynamic insertion of keywords into ad copy ensures that messages remain aligned with user queries enhancing click through rates. Additionally the use of ad extensions such as site links callouts and structured snippets provides additional context and utility to users improving the overall search experience. These features allow advertisers to occupy more screen real estate and provide multiple pathways for engagement. The constant refinement of algorithmic matching ensures that search advertising remains a potent tool for driving qualified traffic and sustaining market leadership.

The video advertising segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 12.5% from 2026 to 2034. This quick surge of the segment is propelled by the increasing consumption of video content across multiple devices and the superior engagement metrics that video formats offer compared to static alternatives. The explosive popularity of short form video platforms has created a vast new inventory for advertisers to engage audiences through immersive and entertaining content. Consumers in the United Kingdom are spending increasing amounts of time on platforms such as TikTok Instagram Reels and YouTube Shorts which favor quick impactful visual stories. The shift in media consumption habits forces brands to adapt their creative strategies to fit vertical formats and shorter attention spans. The algorithmic nature of these platforms ensures that content is distributed to users based on their interests rather than their social connections allowing for organic reach beyond existing follower bases. The high engagement rates associated with video content including likes shares and comments provide valuable social proof and amplify brand messages. Advertisers leverage influencer partnerships to create authentic content that resonates with specific communities enhancing credibility and trust. The ability to integrate shoppable links and interactive elements within videos reduces friction and drives direct response outcomes. The versatility of short form video allows for both brand building and performance marketing objectives making it a flexible tool for diverse campaign goals. The continuous innovation in editing tools and augmented reality filters lowers the barrier to entry for content creation enabling smaller brands to compete effectively.

The migration of television viewing to connected devices has opened up premium video inventory that combines the impact of traditional television with the targeting capabilities of digital advertising. Streaming services have introduced ad supported tiers that provide access to high quality content at lower subscription costs thereby expanding the addressable audience for video advertisers. The ability to target specific demographics and interests ensures that advertisements are delivered to relevant audiences reducing waste and improving efficiency. Moreover, the measurement capabilities of connected television allow advertisers to track view through rates and attribution to online conversions providing a clearer picture of campaign effectiveness. Programmatic buying platforms enable real time bidding for connected television inventory allowing for dynamic optimization based on performance data. The integration of household level data facilitates cross device targeting ensuring consistent messaging across smartphones tablets and televisions. Major broadcasters and streaming platforms are investing heavily in technology infrastructure to support advanced ad formats such as interactive overlays and pause ads. This evolution transforms passive viewing into an engaging experience that drives brand recall and action. The premium nature of connected television content enhances brand perception and associates advertisers with high production value entertainment.

By Platform Insights

The mobile applications segment dominated the United Kingdom digital advertising market and accounted for a 63.8% share in 2025. This dominance of this segment was driven by the extensive time users spend within apps and the rich data available for personalized targeting. The convenience and functionality of apps encourage frequent usage creating numerous opportunities for ad impressions and engagement. Users exhibit significantly higher levels of engagement when interacting with mobile applications compared to mobile websites because apps offer optimized experiences faster load times and personalized interfaces. The substantial time investment provides advertisers with ample opportunity to capture attention through various formats including interstitials native ads and rewarded videos. The sticky nature of popular applications such as social media gaming and productivity tools ensures repeat visits and sustained user retention. Also, the extended interaction time allows for deeper brand storytelling and more complex ad interactions. The ability to leverage device specific features such as push notifications geolocation and camera access enables highly contextual and timely advertising interventions. Gamification elements within apps further enhance engagement by rewarding users for interacting with ads thereby increasing completion rates and brand affinity. The seamless integration of in app purchases and subscription models creates direct monetization pathways that benefit both developers and advertisers. The closed ecosystem of many applications provides a controlled environment where brand safety risks are minimized compared to the open web. Advertisers value the predictability and consistency of app environments which facilitate accurate planning and budget allocation. The continuous improvement of app performance and user experience design ensures that advertising does not disrupt the core utility of the application maintaining positive user sentiment.

Mobile applications provide access to detailed user data including location history device type usage patterns and in app behavior which enables advertisers to execute highly precise targeting strategies. Unlike web browsers which limit data sharing due to privacy restrictions apps can request permissions to access sensitive information that enhances profiling accuracy. The wealth of first party data allows advertisers to segment audiences based on real world behaviors and preferences rather than inferred interests. The ability to track user journeys within the app provides insights into funnel progression and drop off points enabling optimization of user experience and ad placement. The use of software development kits provided by advertising networks facilitates seamless data collection and attribution without compromising app performance. Advertisers can create lookalike audiences based on high value users expanding reach to similar prospects with high conversion potential. The integration of customer relationship management systems with app data enables omnichannel marketing strategies that synchronize messaging across email social media and in app notifications. The granularity of app data supports dynamic creative optimization where ad elements are automatically adjusted based on individual user profiles. This level of personalization increases relevance and reduces ad fatigue leading to higher click through and conversion rates. The competitive advantage gained through data driven insights sustains the dominance of mobile applications as the preferred advertising platform.

The social media platforms segment is expected to exhibit a noteworthy CAGR of 11.8% over the forecast period due to the evolving role of social networks as discovery engines and commerce hubs where users actively seek inspiration and make purchasing decisions. Moreover, the seamless integration of shopping functionalities within social media platforms has transformed these networks from mere communication tools into powerful sales channels that drive direct advertising revenue. Users can now discover browse and purchase products without leaving the app which reduces friction and increases impulse buying. The trend encourages advertisers to invest in shoppable posts and live streaming events that showcase products in real time. The ability to tag products in images and videos allows users to access detailed information and pricing instantly facilitating immediate purchase decisions. Influencers play a crucial role in this ecosystem by providing authentic recommendations and demonstrations that build trust and drive conversions. The use of augmented reality try on features for cosmetics and fashion items enhances the online shopping experience and reduces return rates. Social platforms leverage user data to recommend products based on past interactions and preferences ensuring high relevance. The integration of payment systems within apps streamlines the checkout process further reducing abandonment rates. Advertisers benefit from detailed attribution data that links social interactions directly to sales enabling accurate measurement of return on investment. The viral nature of social content amplifies reach organically reducing the cost per acquisition for successful campaigns. This convergence of content community and commerce sustains the rapid growth of social media advertising.

Advanced recommendation algorithms on social media platforms ensure that content including advertisements is surfaced to users based on their interests and behaviors rather than just their social connections. This shift from social graph to interest graph expands the potential reach of advertisements beyond existing followers to new audiences with high propensity to engage. The discovery mechanism allows smaller brands to achieve viral visibility without substantial initial advertising budgets. The algorithm continuously learns from user interactions such as watch time likes and shares to refine content delivery and improve relevance. Advertisers leverage these trends to create timely and culturally relevant campaigns that resonate with broader audiences. The ability to test multiple creative variations quickly allows brands to identify high performing assets and scale them efficiently. User generated content serves as a powerful form of social proof that enhances the credibility of paid advertisements. Communities formed around shared interests provide niche targeting opportunities that are difficult to replicate on other platforms. The interactive nature of social media including polls questions and challenges encourages active participation rather than passive consumption. This engagement generates valuable data that informs future creative and targeting strategies. The continuous evolution of algorithmic discovery ensures that social media remains a dynamic and effective channel for brand growth and customer acquisition.

By Vertical Insights

In 2025, the retail segment held the majority share of 21.5% of the United Kingdom digital advertising market because of the intense competition for online shoppers and the direct measurability of sales outcomes. Retailers rely heavily on digital channels to drive traffic to e commerce sites and physical stores making them the largest contributors to ad spend. The fierce competition among online retailers necessitates substantial investment in digital advertising to acquire new customers and retain existing ones in a saturated market. With low barriers to entry for e commerce businesses brands must differentiate themselves through targeted messaging and competitive offers. The significant volume of online transactions justifies the high levels of advertising expenditure as retailers strive to capture a larger share of the digital wallet. In addition, the use of performance marketing techniques such as pay per click and affiliate marketing allows retailers to pay only for measurable results ensuring efficient budget utilization. The seasonal nature of retail sales with peaks during Black Friday and Christmas drives temporary surges in advertising demand as brands compete for visibility. Dynamic product ads that automatically update based on inventory and pricing ensure that advertisements remain relevant and accurate. Retargeting campaigns remind users of abandoned carts and previously viewed items recovering lost sales opportunities. The integration of loyalty programs with advertising platforms enables personalized offers that increase customer lifetime value. The ability to track entire customer journeys from click to purchase provides retailers with actionable insights for optimizing marketing strategies. This direct link between advertising spend and revenue generation sustains the leadership of the retail sector in the digital advertising market.

Retailers increasingly adopt omnichannel strategies that seamlessly integrate online and offline experiences requiring coordinated digital advertising efforts across multiple touchpoints. Digital ads drive foot traffic to physical stores through location based targeting and click and collect promotions bridging the gap between digital and physical retail. Retailers use geo fencing technology to send personalized offers to users when they are near physical locations increasing the likelihood of store visits. The synchronization of inventory data across channels ensures that advertisements promote available products reducing customer frustration and returns. Click and collect services promoted through digital channels offer convenience and speed appealing to time constrained consumers. The use of unified customer profiles allows retailers to deliver consistent messaging regardless of the channel used enhancing brand coherence. In store digital screens and mobile apps complement online advertising creating a cohesive brand experience. The collection of data from both online and offline interactions provides a holistic view of customer behavior enabling more effective targeting. Retailers leverage this data to optimize store layouts and product assortments based on digital interest trends. The seamless integration of channels reduces friction and enhances customer satisfaction leading to higher loyalty and repeat purchases. This comprehensive approach to customer engagement reinforces the dominance of the retail sector in digital advertising expenditure.

The health care segment is predicted to witness the highest CAGR of 14.2% between 2026 and 2034 owing to increasing health awareness digitalization of health services and the rise of telemedicine platforms that require aggressive patient acquisition strategies. In addition, the widespread adoption of telemedicine and digital health solutions has created a new avenue for health care providers to reach patients through digital advertising channels. Patients increasingly prefer the convenience of remote consultations and online prescription services driving demand for accessible health care options. Health tech companies and private providers invest heavily in search and social media advertising to attract users to their platforms. The ability to book appointments and consult doctors online appeals to busy professionals and individuals with mobility issues. Advertising campaigns focus on ease of use accessibility and quality of care to build trust with potential patients. The use of educational content such as blogs videos and webinars establishes authority and credibility in the health care space. Patient testimonials and success stories serve as powerful social proof that influences decision making. The integration of wearable device data with health platforms enables personalized health recommendations that are promoted through targeted ads. Regulatory compliance ensures that advertising claims are accurate and evidence based maintaining public trust. The convenience and efficiency of digital health services drive sustained growth in advertising spend as providers compete for market share. This trend is further accelerated by the aging population and the increasing prevalence of chronic conditions that require ongoing management.

There is a growing emphasis on preventive care and wellness initiatives which drives advertising spend by health insurers fitness brands and nutritional supplement companies. Consumers are proactively seeking information and products that support healthy lifestyles leading to increased demand for related digital content. Brands leverage content marketing to educate consumers about nutrition exercise and mental health building brand loyalty and trust. The rise of personalized wellness plans based on genetic testing and biometric data creates opportunities for targeted advertising of customized products. Advertising campaigns highlight the benefits of preventive care in reducing long term health costs and improving quality of life. Partnerships with influencers in the fitness and wellness space amplify reach and credibility among target demographics. The integration of health tracking apps with advertising platforms enables precise targeting based on activity levels and health goals. Corporate wellness programs promoted through digital channels attract employers looking to improve employee health and productivity. The stigma surrounding mental health issues is decreasing encouraging more open discussion and advertising of therapy and counseling services. The holistic approach to health and wellness expands the scope of advertising beyond traditional medical services to include lifestyle and preventive products. This broadening of the health care definition sustains the rapid growth of the sector in the digital advertising market.

COUNTRY ANALYSIS

UK Digital Advertising Market Analysis

The United Kingdom outperformed other countries in the digital advertising market in Europe and accounted for a 22.6% share in 2025. This leading position of the UK market was propelled by high internet penetration advanced technological infrastructure and sophisticated consumer behavior. The United Kingdom benefits from a highly developed digital infrastructure that supports extensive advertising reach and engagement across multiple devices and platforms. Broadband and mobile network coverage is widespread ensuring that consumers have constant access to digital content and advertisements. The average internet speed in the United Kingdom ranks among the highest in Europe facilitating the delivery of rich media formats such as high definition video and interactive ads. Also, the prevalence of smartphones and tablets ensures that advertising can reach consumers throughout their daily routines regardless of location. The maturity of the e commerce sector drives significant demand for performance based advertising as retailers compete for online shoppers. The presence of major technology companies and advertising agencies in London fosters innovation and best practices in digital marketing. The regulatory framework including the General Data Protection Regulation ensures consumer protection while enabling responsible data usage. The high level of digital literacy among consumers means that they are receptive to innovative ad formats and interactive experiences. The stable economic environment and strong consumer spending power support sustained advertising investment across various sectors. The concentration of media ownership and technology providers creates a competitive landscape that drives efficiency and effectiveness. This robust foundation ensures that the United Kingdom remains a leader in digital advertising expenditure and innovation within the European region.

The UK operates under a stringent regulatory framework that governs data privacy and advertising standards fostering an environment of trust and accountability. The implementation of the United Kingdom Data Protection Act and adherence to General Data Protection Regulation principles ensure that consumer data is handled responsibly. According to the Information Commissioner's Office (ICO) Annual Report, there were 11,680 data breach reports submitted in 2023/24. This volume reflects organizations' adherence to mandatory reporting guidelines, though only a small percentage (approx. 3%) resulted in formal investigation or enforcement action. This regulatory scrutiny compels advertisers to adopt transparent practices and obtain explicit consent for data collection enhancing consumer confidence. Research by the Data & Marketing Association (DMA) suggests that while 61% of UK consumers view their personal data as an asset to be exchanged for value, only 39% carefully read privacy policies. However, trust remains a key driver, with 67% of consumers seeking social proof (such as reviews) before sharing their data. The Advertising Standards Authority actively monitors digital advertisements to ensure they are legal decent honest and truthful protecting consumers from misleading claims. The emphasis on brand safety and fraud prevention encourages advertisers to invest in verified inventory and reputable partners. The clarity of regulatory guidelines reduces uncertainty and facilitates compliant campaign execution. Consumers in the United Kingdom are increasingly aware of their digital rights and actively manage their privacy settings influencing advertising strategies. The requirement for clear labeling of sponsored content ensures that users can distinguish between organic and paid messages. The focus on ethical advertising practices enhances brand reputation and long term customer relationships. The regulatory environment encourages innovation in privacy preserving technologies such as clean rooms and contextual targeting. This balance between protection and innovation sustains the growth and integrity of the United Kingdom digital advertising market. The trust established through regulatory compliance serves as a competitive advantage for brands operating in the region.

COMPETITIVE LANDSCAPE

The competitive landscape of the United Kingdom digital advertising market is characterized by intense rivalry among global technology giants specialized agencies and emerging platforms. Established players leverage their vast data ecosystems and advanced technological infrastructure to offer comprehensive advertising solutions that span search social video and display channels. New entrants disrupt the market by introducing innovative formats such as short form video and interactive ads that capture younger audiences. The fragmentation of media consumption requires advertisers to adopt omnichannel strategies which increases demand for integrated measurement and attribution tools. Competition is further intensified by the need to comply with strict privacy regulations which forces companies to innovate in data collection and usage methods. Brands increasingly prioritize transparency and brand safety leading to greater reliance on verified partners and sophisticated verification tools. The race for talent in data science and creative strategy also shapes competitive dynamics as organizations seek to differentiate through superior execution. This dynamic environment ensures continuous innovation and improvement in advertising effectiveness benefiting both marketers and consumers alike.

KEY MARKET PLAYERS

The major players in the UK digital advertising market include

- Meta

- Amazon

- Alibaba

- Microsoft

- Apple

- Verizon

- WPP

- Dentsu

TOP PLAYERS IN THE MARKET

- Google maintains a dominant position in the United Kingdom digital advertising landscape through its comprehensive suite of search and display advertising tools. The company leverages its extensive data ecosystem to deliver highly targeted advertisements across YouTube Gmail and the Google Display Network. Recent initiatives focus on integrating artificial intelligence into campaign management allowing advertisers to automate bidding and creative optimization for better performance. Google has also invested heavily in privacy preserving technologies such as the Privacy Sandbox to address regulatory concerns while maintaining ad effectiveness. The company continues to enhance its connected television offerings by partnering with major broadcasters and streaming services in the region. These efforts ensure that Google remains the preferred platform for brands seeking reach and precision in their digital marketing strategies.

- Meta plays a crucial role in the United Kingdom digital advertising market by providing access to billions of users across Facebook Instagram and WhatsApp. The company focuses on helping businesses connect with audiences through visually engaging formats including stories reels and augmented reality ads. Recent actions include the expansion of shopping features within its apps enabling seamless purchasing experiences for consumers. Meta has also introduced advanced measurement tools that help advertisers understand cross device journeys and attribute conversions accurately. The company is actively developing generative artificial intelligence tools to assist marketers in creating diverse ad variations efficiently. Meta prioritizes user engagement and commercial integration. This strengthens its position as an essential partner for brands aiming to build community and drive sales through social platforms.

- Amazon has emerged as a significant player in the United Kingdom digital advertising market by leveraging its vast e commerce platform and rich customer purchase data. The company offers sponsored product displays and video ads that appear directly within the shopping journey ensuring high relevance and intent. Recent strategies involve expanding its demand side platform to allow advertisers to reach audiences beyond the Amazon ecosystem including third party websites and streaming services. Amazon has also enhanced its attribution capabilities to provide clearer insights into how ads influence offline and online sales. The integration of advertising with its logistics and fulfillment services creates unique value propositions for retailers. Amazon equips advertisers with powerful tools to drive measurable business outcomes and strengthen brand loyalty. This is achieved by combining vast media reach with deep transactional data.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United Kingdom digital advertising market employ several strategic approaches to maintain competitiveness and drive growth. First they invest heavily in artificial intelligence and machine learning technologies to automate campaign optimization and enhance targeting precision. Second companies focus on developing privacy compliant solutions such as clean rooms and contextual targeting to adapt to regulatory changes. Third they expand their connected television offerings to capture the growing audience shifting from traditional broadcast to streaming services. Fourth major participants integrate commerce features directly into their platforms enabling seamless purchasing experiences that shorten the conversion funnel. Fifth they prioritize partnerships with publishers and content creators to secure premium inventory and ensure brand safety. These strategies collectively enable advertisers to achieve higher return on investment while navigating the evolving digital landscape effectively and efficiently.

MARKET SEGMENTATION

This research report on the UK digital advertising market has been segmented and sub-segmented based on the following categories.

By Advertising Format

- Display Advertising

- Search Advertising

- Social Media Advertising

- Video Advertising

- Email Advertising

By Platform

- Websites

- Mobile Applications

- Social Media Platforms

By Vertical

- Retail

- Finance

- Health Care

- Travel

- Automotive

By Target Audience

- B2B

- B2C

- C2C

Frequently Asked Questions

What is the UK digital advertising market?

The UK digital advertising market includes online ads, search advertising, social media ads, display advertising, video ads, and programmatic advertising used by businesses across the United Kingdom.

Why is the UK digital advertising market growing?

The UK digital advertising market is growing due to increased digital transformation, mobile usage, e-commerce expansion, shift from traditional media, and demand for targeted, measurable advertising campaigns.

Who uses the UK digital advertising market?

Businesses of all sizes, e-commerce brands, agencies, startups, retailers, and enterprises use the UK digital advertising market to reach customers through online channels and digital platforms.

What types of advertising are in the UK digital advertising market?

The UK digital advertising market includes search ads, display banners, social media ads, video advertising, native ads, programmatic ads, email marketing, and retargeting campaigns.

How does programmatic advertising impact the UK digital advertising market?

Programmatic advertising drives the UK digital advertising market through automated ad buying, real-time bidding, precise targeting, efficiency, and data-driven campaign optimization across digital channels.

What challenges face the UK digital advertising market?

Challenges in the UK digital advertising market include ad fraud, privacy regulations, data protection, cookie deprecation, ad blocking, and increasing competition for digital ad space.

Which industries use the UK digital advertising market most?

Retail, e-commerce, finance, travel, technology, automotive, and healthcare represent the largest industries in the UK digital advertising market for customer acquisition and brand awareness.

How does social media affect the UK digital advertising market?

Social media shapes the UK digital advertising market through Instagram, Facebook, TikTok, and LinkedIn ads, enabling targeted reach, engagement, influencer partnerships, and social commerce.

What role does mobile advertising play in the UK digital advertising market?

Mobile advertising is central to the UK digital advertising market, as consumers increasingly use smartphones, requiring mobile-optimized ads, in-app advertising, and location-based targeting.

Is the UK digital advertising market competitive?

Yes, the UK digital advertising market is highly competitive with major ad platforms, agencies, programmatic providers, and continuous innovation in targeting, formats, and measurement capabilities.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com