U.K. E-Waste Management Market Size, Share, Trends & Growth Forecast Report By Service Type, By Source of E-Waste, By End User, and By Country (United Kingdom) – Industry Analysis and Forecast, 2026 to 2034

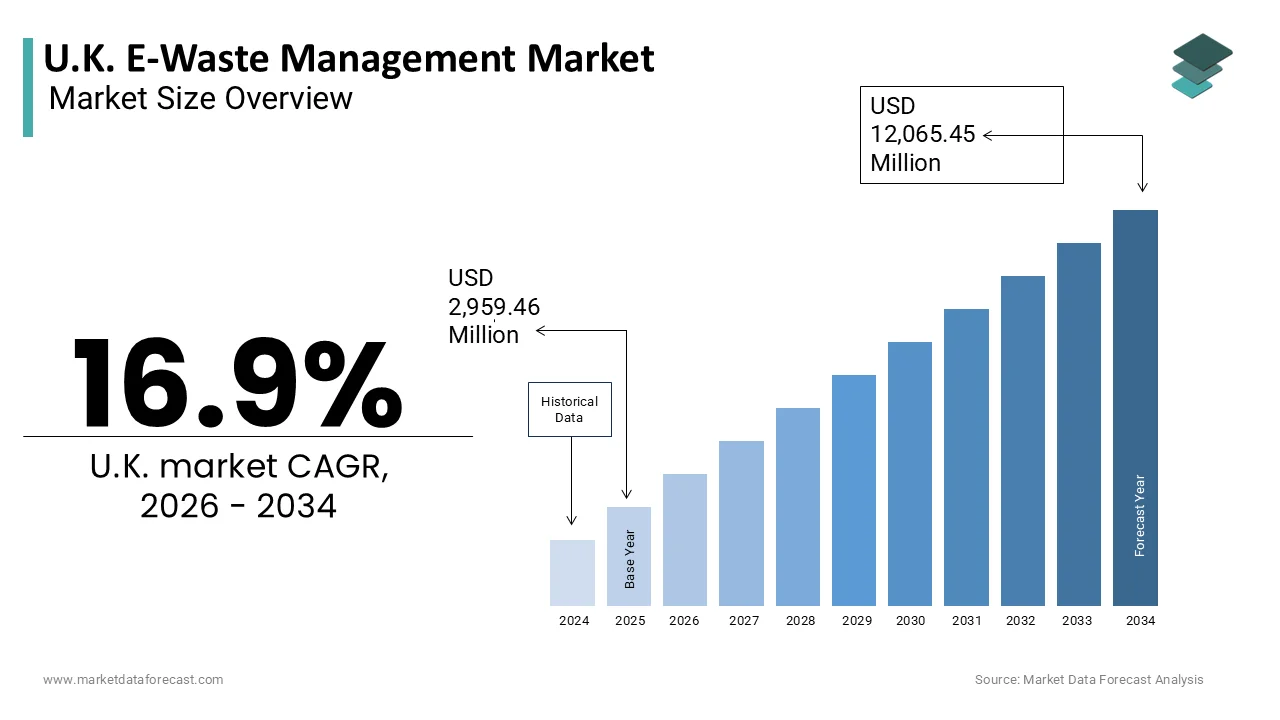

Market Size, 2025

$2,959.46 MnMarket Estimate, 2026

$3,459.61 MnMarket Forecast, 2034

$12.07 BnCAGR, 2026–2034

16.9%U.K. E-Waste Management Market Size

The UK e-waste management market was valued at USD 2,959.46 million in 2025 and is estimated to reach USD 3,459.61 million in 2026. The market is projected to grow to USD 12,065.45 million by 2034, registering a CAGR of 16.9% from 2026 to 2034.

E-Waste Management is the systematic collection, recycling, and disposal of discarded electronic devices. It treats items with plugs, cords, or batteries (e.g., phones, appliances) to prevent toxic chemical leaks and recover critical raw materials through methods like "urban mining". This market operates within a stringent regulatory framework designed to transition the nation towards a circular economy by minimizing landfill dependency and maximizing material recovery. The landscape is defined by the increasing volume of obsolete devices ranging from household appliances to complex industrial machinery, which necessitates specialized handling due to toxic components such as lead mer, mercury, and cadmium. According to data published by environmental action groups like WRAP, the average household in the United Kingdom actually owns approximately 25 electronic devices, highlighting a high penetration of technology where a significant percentage sits unused or hoarded before becoming waste. Global tracking data from the Global E-Waste Monitor indicates that the United Kingdom generates an estimated 1.6 million tonnes of electronic waste annually, presenting a major logistical challenge as a large portion of this volume falls outside of official domestic collection streams. Public awareness regarding environmental sustainability drives participation in take-back schemes and designated recycling centers. The integration of advanced sorting technologies and automated dismantling processes enhances the efficiency of resource extraction. Compliance with the Waste Electrical and Electronic Equipment Regulations mandates producers to finance the collection and treatment of their products, ensuring shared responsibility. The market is further influenced by international trade policies governing the export of hazardous waste and the import of secondary raw materials. Strategic partnerships between local authorities, third-party recyclers, and manufacturers facilitate the development of robust infrastructure capable of handling diverse waste streams while adhering to strict health and safety standards.

MARKET DRIVERS

Stringent Regulatory Frameworks Mandate Compliance and Recovery

Robust legislative measures are driving the United Kingdom's e-waste management market. They achieve this by enforcing strict obligations on producers and retailers to responsibly manage end-of-life electronics. The Waste Electrical and Electronic Equipment Regulations require manufacturers to cover the costs of collecting, treating, ng and recycling discarded items,s which creates a funded infrastructure for waste processing. Official figures published by the Department for Environment, Food & Rural Affairs (DEFRA) show that annual national household WEEE recycling collection targets are set near the 470,000 to 485,000-tonne mark, reflecting the ongoing domestic push to regulate and log consumer electronics waste streams. These regulations set ambitious collection targets that compel local authorities and take-backs to expand their take-back services and improve accessibility for consumers. The introduction of extended producer responsibility principles ensures that companies design products with easier disassembly and higher recyclability in mind, thereby reducing downstream processing costs. Under the Waste Electrical and Electronic Equipment Regulations, the Environment Agency enforces strict legal sanctions and substantial financial penalties against non-compliant firms, though sector audits indicate that logistical errors and misreported waste classifications remain ongoing enforcement challenges. The government regularly reviews and updates these targets to align with European Union benchmarks and national sustainability goals. This regulatory pressure drives investment in advanced recycling facilities and logistics networks capable of handling increasing volumes. The clarity of legal requirements provides stability for investors and operators, encouraging long-term planning and infrastructure development. Furthermore, public sector procurement policies often prioritize suppliers with strong environmental credentials, reinforcing the importance of compliant waste management practices across the supply chain.

Rising Consumer Awareness and Environmental Consciousness

Growing public concern regarding environmental degradation and resource depletion further accelerates tKingdom's e-wastete the Kingdom's e-waste management market. This significantly boosts the demand for professional waste management services as consumers actively seek responsible disposal options. Educational campaigns and media coverage have heightened awareness about the wasteful effects of improper e-waste disposal on soil and water systems, prompting behavioral changes. Generic public opinion polling indicates that a strong majority of UK residents express an ideological desire to protect the environment. However, localized electronic waste data shows that a significant portion of the population still actively throws small appliances into general refuse. This sentiment translates into increased participation in council-run collection schemes and retail take-back programs, which provide convenient avenues for disposal. The rise of the circular economy movement encourages individuals to view old devices as valuable resources rather than trash, sh fostering a culture of reuse and recycling. Social media influencers and environmental organizations play a crucial role in disseminating information about proper disposal methods and the benefits of resource recovery. Consumers increasingly prefer brands that demonstrate commitment to sustainable waste management, including transparent e-waste management policies. This demand-side pressure forces retailers and manufacturers to enhance their reverse logistics capabilities and offer seamless return experiences. The willingness of consumers to pay eco-friendly prices for eco-friendly products further incentivizes companies to invest in certified recycling partners. This shift in consumer behavior creates a stable and growing waste feedstock for the e-waste management industry.

MARKET RESTRAINTS

Complexity of Modern Electronic Devices Hinders Processing

The increasing technical complexity and miniaturization of modern electronic devices are major restraints to the efficiency and cost-effectiveness of operations in the United Kingdom waste management market. Contemporary gadgets such as smartphones, tablets, and wearable technology are designed with glued components and integrated circuits that are difficult to dismantle without specialized tools and expertise. Academic literature published by the Royal Society of Chemistry (RSC) notes that extracting rare earth elements from e-waste requires precise chemical separation, yet emphasizes that this "urban mining" process often yields significantly higher element concentrations than traditional geological mining. Traditional mechanical shredding methods often fail to separate these materials effectively, leading to lower recovery rates and potential contamination of other waste streams. Technological research shows that the rapid evolution of consumer tech designs requires advanced automated processing to sort materials. This rapid obsolescence of sorting technology increases capital expenditure for recyclers who struggle to achieve economies of scale. The lack of standardized design across manufacturers complicates the development of universal dismantling protocols, forcing facilities to handle each device type individually. Lithium-ion instances, such as lithium-ion batteries, pose fire risks during processing, requiring additional safety measures and insurance costs. The short lifespan of consumer electronics exacerbates the volume of waste while reducing the time available for developing efficient recycling methods. These technical barriers limit the profitability of recycling operations and discourage investment in new facilities. The market faces ongoing challenges in adapting to evolving product architectures. This is primarily due to a lack of manufacturer mandates for design for recycling.

High Operational Costs and Infrastructure Limitations

Substantial operational expenses and inadequate infrastructure capacity constraKingdom's e-wastef the Kingdom's e-waste management market. This limits the ability of processors to handle increasing volumes efficiently. The collection, transportation, and sorting of waste require significant financial investment in specialized vehicles,s secure storage facilities,s and advanced processing machinery. The cost of complying with environmental permits and health and safety regulations adds to the financial burden on smaller operators who lack the resources of larger multinational firms. The geographic distribution of recycling facilities is uneven, ven with rural areas often lacking a nearby processing center, resulting in higher transportation emissions and costs. Energy price volatility impacts the profitability of energy-intensive recycling processes such as smelting and chemical leaching. Limited access to financing for infrastructure upgrades prevents many operators from adopting the latest technologies that could improve efficiency and recovery rates. The fragmentation of the supply chain with multiple intermediaries increases transaction costs and reduces transparency. These economic and logistical hurdles make it challenging for the industry to scale up operations to meet rising demand. The market risks are becoming a barrier to the national waste management strategy. Overcoming this hurdle requires substantial public or private investment.

MARKET OPPORTUNITIES

Recovery of Critical Raw Materials Presents Economic Value

The extraction of critical raw materials, such as gold, silver, copper, and rare-earth elements, from e-waste offers a lucrative opportunity for the United Kingdom market. This reduces dependence on imported minerals. Urban mining allows recyclers to recover these valuable resources from discarded devices, providing a sustainable alternative to virgin material extraction. : Scientific analysis from the Global E-Waste Monitor reveals that the concentration of gold in a single tonne of discarded mobile phones is significantly higher than what is found in a tonne of primary geological gold ore, illustrating the vast untapped value locked in urban electronics waste streams. Advances in hydrometallurgical and pyrometallurgical technologies enable more efficient and environmentally friendly recovery processes that maximize yield and minimize waste. Financial modeling from UK environmental research groups like Material Focus indicates that the United Kingdom could recover hundreds of millions of pounds worth of valuable raw materials annually if domestic electronic waste recycling streams are optimized. The global push for electrification and renewable energy increases demand for critical minerals used in batteries and solar panels, creating a ready market for recovered materials. Government incentives for domestic resource recovery encourage investment in advanced recycling facilities that can process complex electronics. Partnerships between recyclers and manufacturers facilitate closed-loop systems where recycled materials are reintegrated into new products. This circular approach reduces the environmental footprint of manufacturing and enhances supply chain security. The development of blockchain technology for tracking material flows improves transparency and trust in the secondary materials market. The United Kingdom can establish itself as a leader in urban mining to create high-value jobs. This strategy will simultaneously stimulate innovation within the green technology sector.

Expansion of Repair and Refurbishment Services

The growing emphasis on extending the lifecycle of electronic devices through repair and refurbishment creates significant prospects for businesses in the United Kingdom e-waste management market. Right to repair legislation and consumer demand for affordable refurbished goods drive the expansion of this segment, which diverts functional devices from waste streams. Community data logged by The Restart Project and its network of volunteer repair cafés demonstrates that localized troubleshooting initiatives successfully extend the life cycle of household electricals, successfully diverting tonnes of preventable hardware away from early waste streams. Professional refurbishers test, clean, nd upgrade electronicssed electronics,,nics ensuring they meet quality standards before resale, which appeals to budget-conscious consumers. Bay confirms that refurbished items remain a central strategic focus category driving positive Gross Merch,,andise Volume (GMV) growth, showcasing a rising consumer appetite for certified pre-owned tech. This trend reduces the volume of waste generated and conserves the resources embedded in manufactured products. Manufacturers are increasingly offering official refurbishment programs to maintain brand loyalty and control the secondary market. The development of modular designs facilitates easier repair and component replacement, lowering maintenance costs. Educational initiatives promote repair skills among the general public, fostering a culture of maintenance rather than replacement. Tax incentives for repair services could further stimulate growth in this sector. By integrating repair into their business model, LS companies can capture value from multiple stages of the product lifecycle. This approach aligns with circular economy principles and reduces the environmental impact of constant consumption. The expansion of repair networks creates local employment opportunities and strengthens community resilience.

MARKET CHALLENGES

Illegal Export and Dumping Undermine Legitimate Operations

The illicit export of e-waste to developing countries with lax environmental regulations impedes the United States, which diverts waste from compliant recycling channels. Criminal networks exploit loopholes in waste classification laws to label hazardous e-waste as second hand goode-wastexporsecond-hand strict domestic treatment requirements. Investigations by Interpol, such as Operation Enigma, have revealed that thousands of tonnes of illegal electronic waste are systematically misdeclared and smuggled from Europe to West Africa, where informal burning practices cause extensive environmental and health damage. This illegal trade undermines legitimate recyclers who incur higher costs to comply with safety and environmental standards, creating an uneven playing field. Intelligence-led enforcement data from the Environment Agency demonstrates an ongoing battle against waste traffickers who exploit shipping loopholes, aligning with global United Nations Environment Programme (UNEP) reports showing that a vast majority of the world's electronic waste is illegally traded or dumped annually. The lack of rigorous inspection at ports and borders facilitates this illicit flow,w depriving the domestic industry of valuable feedstock. Developing nations often lack the infrastructure to process e-waste safely, leading to wasteful burning and acid bathing practices that release toxic fumes. This global injustice damages the reputation of the United Kingdom's recycling sector and hinders international cooperation. Enforcement agencies struggle with limited resources and complex jurisdictional issues, making prosecution difficult. The anonymity of online marketplaces facilitates the sale of broken devices that are ultimately exported as waste. Addressing this challenge requires stronger international collaboration, stricter border controls, and harmonized definitions of waste versus used goods. Illegal exports will continue to distort the market until these measures are implemented. Furthermore, this activity harms global environmental health.

Data Security Concerns Deter Consumer Participation

Fear of data breaches and identity theft associated with discarded electronic devices significantly hinders consumer willingness to participate in formal-waste recycling programs, i.e., waste country, which further slows down the expansion of the United Kingdom e-waste management market. Individuals retain old smartphones, laptops, and hard drives due to concerns that personal information may not be completely erased during the recycling process. National research published by the UK electronics recycling campaign Material Focus reveals that data security concerns are a primary driver behind device hoarding, causing millions of households to store old tech in drawers rather than sending it to recycling streams. Tithoarding behavior reduces the volume of e-waste entering official collection streams and delays the recovery of valuable materials. Professional recyclers must invest in certified data destruction services including physical shreddi, ng and software wiping to reassure customers whi, ch increases operatio,nal costs. Under statutory UK GDPR enforcement guidelines regulated by the Information Commissioner’s Office (ICO), organizations that fail to perform certified data erasure on discarded IT hardware face substantial legal penalties and regulatory actions for exposing personal consumer information. The lack of standardized certification for data destruction creates confusion among consumers about which providers are trustworthy. Small and medium-sized enterprises are particularly cautious due to the sensitive nature of corporate data. The complexity of modern encryption and cloud storage adds layers of difficulty to ensuring complete data removal. Marketing efforts often fail to adequately communicate the security measures taken by legitimate recyclers. Building trust requires transparent processes and third-party audits, which are third-party intensive. A large portion of e-waste will remain outside the formal management system. This will persist until data security guarantees are universally recognized and trusted.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Service Type, Source of E-Waste, End User, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | United Kingdom |

| Market Leaders Profiled | Veolia Environment S.A., SUEZ Recycling and Recovery UK Ltd., Biffa plc, WasteCare Group Ltd., Sims Lifecycle Services, Inc., ERP UK Ltd., Enva Group, Recycling Lives Ltd., Restore Technology Ltd., European Metal Recycling (EMR) Ltd., Viridor Limited, Currys plc (Tech Recycling Services) |

SEGMENTAL ANALYSIS

By Service Type Insights

The material recovery segment dominated the United Kingdom e-waste management market, accounting for a 55.5% share in 2025. This dominance of the segment was driven by the high economic value associated with extracting precious and base metals from discarded electronics. Moreover, this process involves sophisticated chemical and physical techniques to isolate gold, silver,r copper, and palladium, which are then reintroduced into manufacturing supply chains. The main driver for material recovery is the substantial financial return generated from extracting precious metals that are present in higher concentrations in e-waste than in natural ore. Research published in the Global E-Waste Monitor shows that a single tonne of discarded mobile phones yields approximately 300 grams of gold, which is up to 100 times more highly concentrated than traditional geological ore, illustrating the immense potential of urban mining. This economic incentive compels recycling facilities to invest in advanced hydrometallurgical and pyrometallurgical processes that maximize yield and purity. Research from electronic recycling campaigns indicates that while the raw material value embedded in total generated e-waste is massive, the UK fails to capture hundreds of millions of pounds worth of precious metals annually because items are hoarded or binned incorrectly. The volatility of global commodity prices further encourages domestic recovery as it reduces reliance on imported raw materials and hedges against supply chain disruptions. Companies prioritize the recovery of copper and aluminum due to their widespread use in electrical wiring and casings, which ensures consistent demand. The development of closed-loop systems, where manufacturers buy back recovered materials, creates stable markets for recyclers. Government incentives for using secondary raw materials in production enhance the competitiveness of recovered metals. The ability to certify the origin and quality of recycled materials through blockchain technology increases trust among buyers. This financial attractiveness ensures that material recovery remains the cornerstone of the e-waste management industry.

Strict environmental regulations and circular economy targets mandate high rates of material recovery, forcing companies to prioritize extraction over simple disposal or shredding. The Waste Electrical and Electronic Equipment Regulations set specific recovery and recycling targets that operators must meet to maintain their compliance certificates. Under the UK Waste Electrical and Electronic Equipment (WEEE) Regulations administered by the Department for Environment, Food and Rural Affairs (DEFRA), compliance schemes mandate an 85% recovery rate and an 80% recycling and reuse target for large household appliances to enforce material efficiency. These legal requirements ensure that valuable resources are not lost to landfill and that hazardous substances are properly managed. The European Union Circular Economy Action Plan influences UK policy by setting ambitious goals for material reuse and recycling across all sectors. Non-compliance results in significant fines and reputational damage, motivating companies to exceed minimum standards. The integration of extended producer responsibility means that manufacturers financially support recoveryeffortst,s linking product design tend-of-lto the end-of-life. Public procurement policies often favor suppliers who demonstrate a high material recovery rate, creating additional market pressure. The alignment of national sustainability strategies with international climate goals reinforces the importance of resource efficiency. This regulatory framework provides a stable and predictable environment for long-term investment in recovery infrastructure.

The refurbishment segment is estimated to register the fastest CAGR of 14.5% between 2026 and 2034, owing to consumer demand for affordable technology and legislative support for the right to repair. The rising cost of living and increasing environmental consciousness drive consumers to seek high-quality refurbished devices at a cost-effective and sustainable price compared to new devices. Refurbished products offer significant savings while maintaining performance standards appealing to budget-conscious households and businesses. A study indicates that over 60% of UK consumers are willing to purchase refurbished electronic devices, driven primarily by a combination of retail cost savings and reduced environmental footprints. This shift in consumer behavior creates a robust market for professional refurbishers who test clean and repair used devic,, es t,o meet rigorous quality standards. The stigma associated with second-hand goods is diminishing as major retailers and manufacturers launch certified refurbished programs with warranties. Social media campaigns highlighting the environmental impact of e-waste encourage younger de-wastehics to embrace pre-owned technology. The pre-owned property of flexible payment plans for refurbished items further enhances accessibility for lower-income groups. Corporate clients also adopt refurbished IT equipment to reduce capital expenditure and meet sustainability targets. The growth of online marketplaces specializing in refurbished goods improves visibility and trust in the sector. This demand-side momentum sustains the high growth rate of the refurbishment segment.

Government initiatives promoting the right to repair and extending product lifecycles provide a favorable regulatory environment for the refurbishment industry in the United Kingdom. New laws require manufacturers to make spare parts and repair manuals available to independent technicians f, facilitating easier and cheaper repairs. These measures reduce the technical barriers to refurbishment and lower the cost of restoring devices to working condition. The extension of warranty periods for certain components encourages consumers to repair rather than replace faulty items. Tax incentives for repair services and reduced VAT rates on refurbished goods are being considered to further stimulate the market. Educational programs in schools and colleges promote repair skills,s ensuring a future workforce capable of supporting the industry. Manufacturers are increasingly designing modular products that are easier to disassemble and upgrade, de aligning with refurbishment needs. The standardization of charging ports and connectors simplifies the refurbishment process for diverse device types. This supportive policy framework accelerates the growth of the refurbishment sector by making it economically and technically viable.

By Source of E-Waste Insights

The household appliances segment led the United Kingdom market and captured a 40.3% share in 2025. This leading position of the segment was attributed to the high volume of large white goods such as refrigerators, washing machines and dishwa, and dishwashers discarded annually. These items contain significant amounts of steel, plastic, and hazardous refrigerant,igerant,s requiring specialized handling. The sheer quantity of large household appliances reaching the g end of life drives the dominance of this segment, as these items constitute a major portion of total e-waste. Consumers replace these durable goods every 10 to 15 years,s creating a steady and predictable stream of waste. Research tracking the UK circular economy indicates that millions of large household appliances are decommissioned annually, representing a primary source of bulk tonnage entering domestic waste streams. The bulk and weight of these items necessitate dedicated collection logistics and processing facilities equipped to handle heavy machinery. National data submitted to UK environmental regulators confirms that large household appliances consistently represent the largest single category of electrical waste by mass, accounting for nearly half of the total tonnage managed by processing infrastructure. The presence of hazardous substances such as chlorofluorocarbons in older refrigerators mandates careful extraction to prevent environmental damage. Take-back schemes are particularly effective for this category, as delivery of new appliances often coincides with the removal of old ones. The high etal content in these appliances makes them attractive for material recovery, providing economic justification for collection efforts. Local authorities prioritize the collection of large items to prevent illegal fly tipping,ng which remains a persistent issue. The standardized size and composition of many appliances facilitate automated dismantling processes,ses improving efficiency. This consistent volume ensures that household appliances remain the primary focus of e-waste management operations. Obligatory requirements obliging retailers to accept old appliances when selling new ones ensure high collection rates for this segment and drive its dominance in the market. The Distributor Take Back Scheme allows retailers to contribute to local authority collection facilities instead of offering in-store take back, but many major retailers choose direct collection to enhance customer service. Under statutory regulations administered by the Department for Environment, Food and Rural Affairs (DEFRA), major electrical retailers are legally obligated to provide robust take-back arrangements, including free collections when delivering equivalent new items, to increase consumer access to dedicated recycling pathways. This convenience encourages proper disposal rather than illegal dumping or storage in homes. The integration of reverse logistics into supply chains allows retailers to optimize transportation costs by combining delivery and collection routes. Consumer awareness of these schemes is high due to prominent labeling and advertising at the point of sale. The obligation extends to online retailers who must provide free take-back services for small appliances,s as well as further boosting volumes. Compliance monitoring by enforcement agencies ensures that retailers adhere to their responsibilities. The effectiveness of these schemes reduces the burden on municipal waste services and improves overall recycling rates. The mandatory nature of these arrangements guarantees a steady flow of household appliances into the management system.

The consumer electronics segment is anticipated to witness the fastest CAGR of 12.8% over the forecast period due to rapid technological obsolescence and high consumption rates. In addition, the accelerated pace of innovation in consumer electronics leads to frequent upgrades and shorter productlifecyclesy,cles resulting in a surge of disassembled devices. Consumers replace smartphones and tablets every two tothree ,,years driven by marketing campaigns and feature enhancements rather than functional failure. The inability to repair or upgrade components such as batteries and screens forces users to discard entire devices. The proliferation of wearable technology such as smartwatches and fitness trackers adds to the volume of small, complex devices that are difficult to recycle. Planned obsolescence strategies by manufacturers,turers including software updates that slow down older devices, further incentivize replacement, cement. The lack of standardized charging ports until recently created compatibility issues, leading to the accumulation of unused chargers and cables. The high value of components in these devices attracts informal recycling but also drives formal collection efforts. The sheer number of units sold annually ensures that this segment will continue to grow rapidly. Addressing this trend requires design changes and consumer education to extend device usability.

The ubiquitous presence of mobile devices in daily life ensures a vast and continuous supply of e e-wastes. Nearly every individual in the United Kingdom owns multiple electronic gadgets. High adoption rates mean that even small increases in replacement frequency result in large absolute volumes of waste. The trend towards owning multiple devices su, such as a phone, tablet, ablet,, and smartwatch, increases the per capita e-waste generation. Also, the compact size of these devices often leads to them being stored in drawers rather than disposed of correctly,rrectly but eventual clearance drive,,s periodic spikes in waste volumes. The integration of personal data in these devices raises security concerns that could delay disposals, a l but also drives demand for certified destruction services. The popularity of trade in programs offered by network providers and manufacturers facilitates the collection of used devices for refurbishment or recycling. The constant release of new models keeps consumer interest high and drives upgrade cycles. This widespread ownership and frequent turnover sustain the rapid growth of the consumer electronics waste segment.

By End User Insights

The residential segment was the largest in the United Kingdom e-waste management market and occupied a 60.3% share in 2025. This prominence of the segment was supported by the high volume of electronic goods consumed by households and the widespread availability of collection services for domestic users. Individual consumers generate the majority of small and large e-waste items. The extensive waste of electronic devices in UK homes generates a substantial volume of waste as residents regularly upgrade and discard items ranging from kitchen appliances to entertainment systems. In addition, the diversity of devices owned by each household i,, including multiple screens g, gaming consoles, nd smart home gadgets c, contributes to the complexity and volume of waste. The convenience of online shopping has increased the frequency of purchases and subsequent disposals as consumers easily replace broken or outdated items. The lack of awareness about proper disposal methods among some residents leads to mixed waste, but targeted campaigns are improving separation rates. The emotional attachment to certain devices can delay disposal, but eventual clearance contributes to bulk collections. The seasonal nature of purchasing, with peaks during holidays, leads to corresponding spikes in waste generation. The high density of population in urban areas facilitates efficient collection logistics for residential waste. This consistent and large volume of feedstock ensures the residential sector remains the primary contributor to the e-waste market.

The availability of convenient collection services provided by local councils significantly drives participation from residential users and sustains the dominance of this sector. Most local authorities offer curbside collection for small electrical items or operate household waste recycling centers where residents can drop off larger appliances. The ease of access encourages residents to dispose of items responsibly rather than illegally dumping them. Public awareness campaigns run by councils educate residents on what can be recycled and how to prepare items for collection. The integration of e-waste collection with general waste services reduces the effort required from households. Some councils partner with charities to collect working items for reuse p, providing an additional incentive for residents to separate usable goods. The standardization of collection practices across regions helps build consistent user habits. The funding provided through producer compliance schemes supports the operational costs of these services, ensuring their sustainabili, ty. This robust infrastructure makes it easy for residents to participate,e driving high volumes into the formal management system.

The commercial segment is likely to experience the fastest CAGR of 11.5% from 2026 to 2034. This swift growth is propelled by the rapid digitalization of businesses and strict corporate sustainability mandates. Businesses across various industries are undergoing rapid digital transformation re,, requiring frequent upgrades of IT infrastructure, including servers, docking equipment. This generates significant e-waste. The shift to cloud computing does not eliminate hardware needs but accelerates the refresh cycle for edge devices and user terminals. Companies replace equipment to maintain security compatibility andperformancen,ce leading to regular disposal cycles. The adoption of Internet of Things devices in offices and retail environments adds to the volume of small electronic waste. The need to comply with data protection regulations requires secure destruction of storage media w,, which drives demand for specialized commercial e-waste services. The scale of corporate disposals allows for efficient bulk collection and processing r,, reducing per unit costs. The professional nature of commercial waste ensures higher quality feedstock with better documentation and less contamination. This systematic approach to asset management sustains the rapid growth of the commercial segment.

Increasing pressure from investors and regulators to meet environmental so,cial an,,d governance criteria compels companies to manage their waste responsibly and transparently. Organizations are required to report on their waste diversion rates and carbon footprint w, which includes the impact of electronic equipment disposal. The regulatory scrutiny drives businesses to partner with certified e-waste recyclers who can provide detailed audit trails and certificates of destruction. Also, the use of reputable e-waste management partners enhances brand reputation and demonstrates commitment to sustainability. Employees and customers increasingly prefer businesses with strong environmental credentials i,, influencing procurement decisions. The implementation of circular economy principles within corporate procurement policies encourages the purchase of refurbished equipment and the responsible disposal of old assets. The availability of detailed analytics from e-waste providers helps companies track progress against sustainability goals. This strategic focus on ESG performance ensures that commercial e-waste management remains a priority and continues to grow.

COUNTRY LEVEL ANALYSIS

United Kingdom E-Waste Management Market Analysis

In 2025, the United Kingdom was positioned as a leader in the European e-waste management market and accounted for an 18.4% share because of its advanced regulatory framework and high consumer awareness. The country serves as a model for effective waste segregation and resource recovery initiatives. A robust legal framework in the United Kingdom helps protect the environment. Also, a key component is the Waste Electrical and Electronic Equipment Regulations, which enforce producer responsibility and mandate high collection targets. This regulatory clarity ensures consistent investment in infrastructure and encourages compliance among businesses and consumers. However, according to data from the Department for Environment, Food and Rural Affairs (DEFRA), the UK has historically struggled to meet its strict domestic and European-aligned WEEE collection targets, triggering government inquiries into how the nation manages electrical waste. The Environment Agency actively monitors compliance and enforces penalties for non-adherence, maintaining high standards across the sector. Research shows that household recycling habits remain hindered by data gaps in supply chain transparency and consumer confusion surrounding inconsistent material labeling. The integration of extended producer responsibility ensures that manufacturers finance the end-of-life management of their products re, reducing the burden on taxpayers. The government regularly updates regulations to address emerging challenges such as battery waste and small electronics. This proactive regulatory stance fosters innovation in recycling technologies and business models. The strong compliance culture among UK businesses ensures that waste is handled professionally and safely. The alignment with international best practices enhances the credibility of the UK market. This stable regulatory environment attracts investment and supports long-term planning for waste management operators.

Strong public awareness campaigns and educational initiatives have cultivated a culture of environmental responsibility among UK residents, ts leading to high participation rates in waste recycling programs. Consumers are increasingly knowledgeable about the environmental impacts of e e-wastend the benefits of resource recovery. Local councils and charities play a crucial role in educating the public through community events and clear signage at recycling centers. The popularity of repair cafes and swap shops reflects a growing interest in extending product lifecycles. Social media influencers and environmental organizations amplify messages about sustainable consumption and proper disposal. Take-back initiatives of retailer take-back schemes further encourage participation by removing barriers to entry. The high level of digital literacy among the population facilitates access to online information about recycling options. This engaged citizenry provides a stable and growing volume of high-quality e-waste for the management system. The collective effort of individuals and communities sustains the leadership position of the UK in the European market.

COMPETITIVE LANDSCAPE

The competitive landscape of the United States markets is characterized by the presence of large multinational corporations, specialized regional processes, and emerging technology-driven startups. Established players leverage their extensive infrastructure and logistical networks to offer comprehensive services, while niche firms focus on specific aspects such as data security or rare metal recovery. Competition is intense based on service quality, compliance, reliability, liability, and technological innovation. Companies differentiate themselves through advanced sorting capabilities, transparent and parent reporting, and strong customer relationships. Regulatory compliance serves as a significant barrier to entry, ensuring that only qualified operators can participate effectively. The market sees continuous consolidation as larger entities acquire smaller specialists to expand their capabilities and geographic reach. Price competition remains moderate as clients prioritize certified and secure disposition. In addition, artificial intelligence and automation lead to efficiency gains and reduce operational costs. Partnerships with technology providers enable companies to offer smarter solutions for waste tracking and management. The focus on circular economy principles encourages collaboration between competitors to achieve shared sustainability goals. This dynamic environment fosters continuous improvement and ensures high standards for environmental protection and resource recovery across the sector.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.K. E-Waste Management Market include

- Veolia Environment S.A.

- SUEZ Recycling and Recovery UK Ltd.

- Biffa plc

- WasteCare Group Ltd.

- Sims Lifecycle Services, Inc.

- ERP UK Ltd.

- Enva Group

- Recycling Lives Ltd.

- Restore Technology Ltd.

- European Metal Recycling (EMR) Ltd.

- Viridor Limited

- Currys plc (Tech Recycling Services)

TOP LEADING PLAYERS IN THE MARKET

- Sims Limited operates as a global leader in metal recycling with a significant presence in the United Kingdom e-waste management sector through its advanced processing facilities. The company specializes in recovering precious and base metals from discarded electronics using sophisticated shredding and separation technologies. Recent actions include substantial investments in artificial intelligence-driven systems to enhance material purity and recovery rates. Sims has expanded its partnerships with original equipment manufacturers to create closed-loop chains for critical raw materials. The company actively promotes transparency by publishing detailed sustainability reports that highlight its environmental impact and circular economy contributions. By focusing on high-value recovery, Sims strengthens its position as a key partner for businesses seeking waste-free and efficient e-waste solutions. Its commitment to innovation ensures compliance with strict UK regulations while maximizing resource efficiency.

- Veolia UK and Ireland provides comprehensive environmental services,c including specialized waste collection, treatment, and recycling solutions for residential commerci, al and industrial clients. The company leverages its extensive logistics network to ensure efficient pickup and processing of electrical and electronic equipment across the region. Recent initiatives involve the development of digital platforms that allow customers to track their waste streams and verify compliance with data destruction standards. State-of-the-art investments are invested in state-of-the-art dismantling facilities capable of handling complex devices such as smartphones and laptops safely. The company collaborates with local authorities to improve public access to recycling points and educate communities on proper waste disposal. By integrating e-waste services with its broader resource recovery offerings, Veolia enhances operational efficiency and customer value. Its focus on sustainable practices reinforces its reputation as a trusted provider in the UK market.

- Biffa PLC is a leading integrated waste and resource management company in the United Kingdom, offering tailored e-waste management services to diverse sectors. The company focuses on safe collection, ion, high-quality destruction, and high-quality material recovery from discarded electrical items. Recent actions include the expansion of its specialist hazardous waste handling capabilities to manage batteries and other dangerous components found in electronics. Biffa has introduced innovative customer portals that simplify booking and reporting for corporate waste requiring regular waste disposal. The company actively engages in industry collaborations to develop best practices for recycling rare earth elements and precious metals. By prioritizing health and safety standards and regulatory compliance,ce Biffa builds trust with its client base. Its strategic investments in processing technology enable higher recovery rates and reduced environmental footprint. This approach solidifies its role as a vital contributor to the UK circular economy.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United Kingdom waste management market employ strategic approaches to enhance competitiveness, ensure efficiency,s and drive growth. First, they invest heavily in advanced sorting and recycling technologies to improve material recovery rates and operational efficiency. Second companies form strategic partnerships with manufacturers and retailers to establish closed-loop supply chains and secure, consistent feedstock. Third, they expand their digital capabilities to offer transparent tracking and reporting services that ensure regulatory compliance for clients. Four, the participants focus on diversifying their service offerings to include rep, air refurbish,ment, and secure data destruction. Fifth,h they prioritize sustainability initiatives and carbon reduction goals to align with corporate social responsibility expectations. These strategies collectively enable organizations to deliver high-value, e-compliant,t and environmentally responsible e-waste management solutions.

MARKET SEGMENTATION

This research report on the UK e-waste management market is segmented and sub-segmented into the following categories.

By Service Type

- Material Recovery

- Refurbishment

- Recycling

- Disposal

By Source of E-Waste

- Household Appliances

- Consumer Electronics

- IT & Telecommunications Equipment

- Industrial Electronics

- Others

By End User

- Residential

- Commercial

- Industrial

- Government

- Others

By Country

- United Kingdom

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com