United Kingdom EdTech Market Size, Share, Trends & Growth Forecast Report Segmented By Type (Hardware, Software, Content), Application, and Country – Industry Analysis From 2026 to 2034

United Kingdom EdTech Market Report Summary

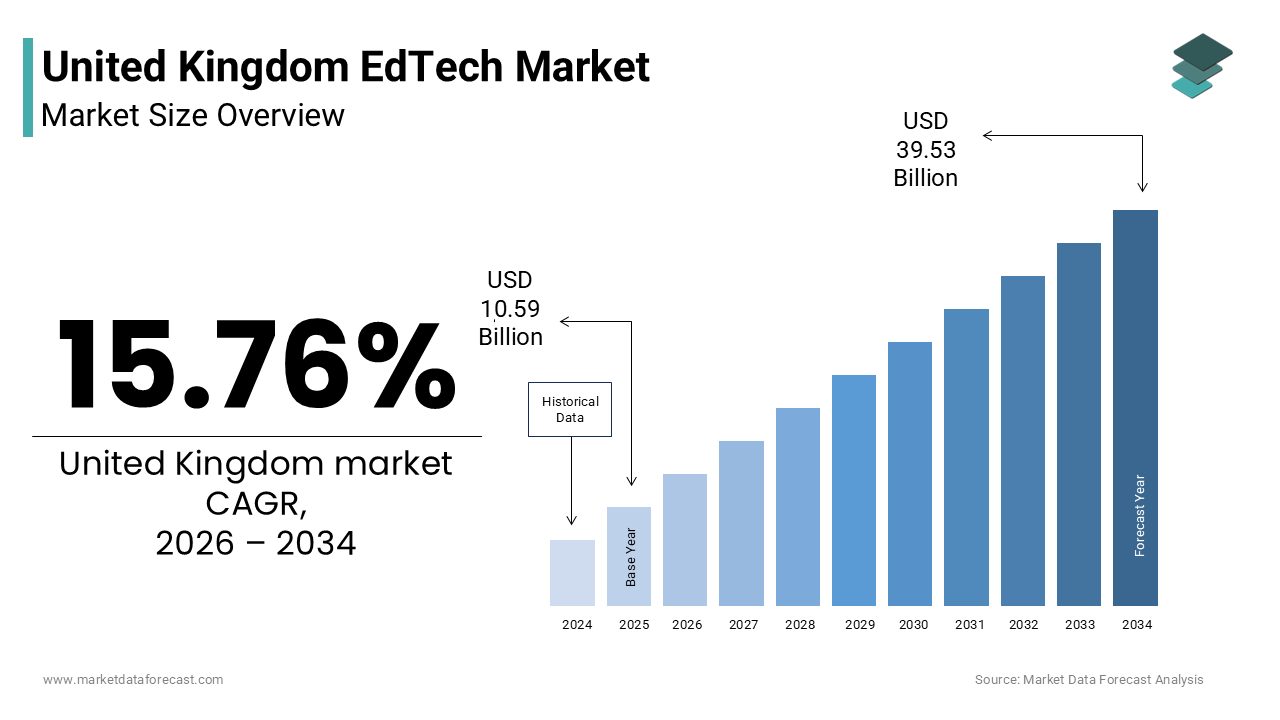

The United Kingdom EdTech market was valued at USD 10.59 billion in 2025 and is anticipated to reach USD 12.26 billion in 2026 from USD 39.53 billion by 2034, growing at a CAGR of 15.76% during the forecast period from 2026 to 2034. The growth of the United Kingdom EdTech market is driven by increasing government initiatives for digital transformation in education, rising demand for personalized learning solutions, and growing adoption of online and hybrid learning models. Expanding investments in artificial intelligence-powered educational platforms, increasing corporate demand for workforce upskilling and reskilling programs, and growing integration of digital learning technologies across educational institutions are further accelerating market growth. Moreover, advancements in immersive learning technologies, expansion of adaptive learning platforms, and increasing focus on improving educational accessibility and outcomes are supporting the expansion of the United Kingdom EdTech market.

Key Market Trends

- Rising adoption of artificial intelligence and machine learning technologies for personalized learning experiences and automated assessments.

- Increasing deployment of virtual reality and augmented reality solutions for immersive and skills-based education.

- Growing demand for cloud-based learning management systems and digital collaboration platforms.

- Strong focus on reducing teacher workload through automation and intelligent administrative tools.

- Expansion of corporate e-learning and workforce development programs driven by digital transformation initiatives.

Segmental Insights

- Based on type, the software segment dominated the United Kingdom EdTech market and held the largest share in 2025. The segment’s dominance is attributed to the widespread adoption of learning management systems, assessment platforms, administrative software, and cloud-based educational applications that enhance learning efficiency and institutional management.

- The content segment is projected to witness the fastest CAGR during the forecast period owing to increasing demand for interactive digital learning materials, curriculum-aligned educational resources, gamified content, and multimedia-based learning experiences.

- Based on application, the K-12 segment accounted for the leading share of the United Kingdom EdTech market in 2025. The dominance of this segment is driven by government-led digital education initiatives, widespread technology integration in schools, increasing demand for online learning tools, and strong parental engagement in student learning outcomes.

- The corporate training segment is anticipated to register the fastest CAGR during the forecast period due to rising workforce upskilling requirements, growing demand for compliance and professional development training, increasing adoption of microlearning solutions, and rapid digital transformation across industries.

Regional Insights

The United Kingdom accounted for a significant share of the European EdTech market in 2025, supported by strong digital infrastructure, high internet penetration, and a thriving educational technology ecosystem. London remains a major hub for EdTech innovation due to its strong startup environment, access to venture capital funding, and concentration of leading educational technology companies. The country continues to benefit from government support for digital learning initiatives, extensive adoption of online education platforms, and growing collaboration between academic institutions and technology providers.

Competitive Landscape

The United Kingdom EdTech market is highly competitive and characterized by the presence of established education providers, innovative technology startups, and specialized learning platform developers competing through technological innovation, personalized learning experiences, and curriculum-aligned content. Leading companies are focusing on expanding artificial intelligence capabilities, strengthening digital learning ecosystems, investing in immersive educational technologies, and enhancing learner engagement through adaptive platforms. Strategic partnerships with schools, universities, corporations, and government agencies are further strengthening market positioning across the educational technology sector. Prominent players in the United Kingdom EdTech market include Multiverse, Perlego, MyTutor, Atom Learning, Zen Educate, Century Tech, Firefly Learning, Lingumi, Satchel, Learning Technologies Group plc, BridgeU, Springpod, Glean, BibliU, and Synthesia.

United Kingdom EdTech Market Size

The United Kingdom EdTech market size was valued at USD 10.59 billion in 2025 and is anticipated to reach USD 12.26 billion in 2026 from USD 39.53 billion by 2034, growing at a CAGR of 15.76% during the forecast period from 2026 to 2034.

EdTech (short for Educational Technology) is the combined use of hardware, software, and digital learning theories to facilitate and enhance the learning process. This ecosystem encompasses software platforms content delivery systems and analytical tools that facilitate personalized instruction administrative efficiency and remote collaboration. The market dynamics exhibit healthy growth. Moreover, the market has evolved from simple digitization of textbooks to sophisticated adaptive learning environments powered by artificial intelligence and data analytics. According to the Office for National Statistics (ONS), 93% of households in Great Britain had internet access in 2023. The Department for Education (DfE) reports that there are 9.1 million pupils enrolled in schools in England alone (2023/24). As per the DfE’s Working Lives of Teachers and Leaders Survey, teachers spend approximately 5 to 6 hours per week specifically on "general administrative tasks" (e.g., communication, paperwork). This environment fosters intense competition among developers who strive to create intuitive interfaces that reduce cognitive load for both educators and learners. Regulatory frameworks such as the General Data Protection Regulation shape how student data is collected and utilized ensuring privacy while enabling personalized experiences. The shift towards competency based education requires flexible assessment tools that track progress in real time. Institutions increasingly prioritize interoperability between different software systems to create seamless digital ecosystems. The integration of virtual reality allows for immersive simulations in subjects ranging from medicine to engineering. This technological evolution supports inclusive education by providing accessibility features for learners with diverse needs. The market continues to expand as stakeholders recognize the potential of technology to bridge geographical and socioeconomic gaps in educational access.

MARKET DRIVERS

Government Initiatives for Digital Transformation in Schools

Strategic government funding and policy mandates are accelerating the growth of the United Kingdom EdTech market. This expansion is driven by prioritizing digital infrastructure and literacy in state-funded institutions. The Department for Education has launched several initiatives aimed at equipping schools with necessary hardware and software to support modern pedagogical approaches. The Department for Education’s (DfE) official EdTech Strategy launched with an initial government pledge of £10 million to fund testbeds, demonstrate technology capabilities, and reduce teacher workloads. This financial backing enables schools to purchase learning management systems interactive whiteboards and subscription based educational content without straining local budgets. The National Centre for Computing Education works to integrate computer science into the curriculum requiring schools to adopt specific coding platforms and digital resources. As per data from Ofsted inspections increasingly evaluate how effectively schools use technology to enhance learning rather than just its presence driving demand for high quality pedagogical tools. The emphasis on digital skills as a core competency ensures sustained demand for platforms that teach programming data analysis and digital citizenship. Government partnerships with private edtech firms facilitate the development of standardized tools that meet national curriculum requirements. These collaborations ensure that solutions are scalable and aligned with educational goals. The provision of free or subsidized training for teachers on using new technologies reduces resistance to adoption. This top down approach creates a stable and predictable market for edtech providers who can align their products with public sector procurement cycles. The focus on reducing teacher workload through automation further drives interest in administrative and assessment tools.

Corporate Demand for Upskilling and Reskilling Solutions

The rapid pace of technological change and evolving job requirements drive significant demand for corporate edtech solutions as businesses seek to upskill and reskill their workforces efficiently, which in turn boosts the expansion of the United Kingdom edtech market. Organizations recognize that continuous learning is essential for maintaining competitiveness and retaining talent in a tight labor market. According to the Chartered Institute of Personnel and Development (CIPD) Labour Market Outlook, approximately one in three UK employers (roughly 33.3%) report hard-to-fill vacancies driven by immediate skills gaps. Furthermore, only 21% of learning practitioners rank addressing workforce skills gaps as a top-three organizational priority. Companies prefer scalable online training solutions that can be accessed remotely allowing employees to learn at their own pace without disrupting operations. The rise of hybrid work models necessitates digital tools that facilitate collaboration and knowledge sharing across dispersed teams. According to LinkedIn platform metrics, the 18–24 age cohort (Gen Z) is the fastest-growing professional segment in the UK, expanding by 30% year-on-year as they onboard for early career-planning. Microlearning platforms that deliver content in short digestible modules are particularly popular as they fit into busy work schedules. Employers leverage analytics to track employee progress and identify skill deficiencies enabling targeted interventions. The availability of certified courses from reputable providers enhances the credibility of internal training programs. Industries such as finance healthcare and technology lead in adopting specialized edtech solutions for compliance and technical training. The ability to measure return on investment through improved performance metrics justifies continued spending. This corporate sector demand provides a lucrative revenue stream for edtech companies beyond the traditional academic market. The focus on soft skills leadership and diversity training further expands the scope of available content.

MARKET RESTRAINTS

Data Privacy and Security Concerns Limit Adoption

Stringent data protection regulations and growing concerns about student privacy are slowing down the growth of the UK edtech market. This deceleration occurs because complex compliance requirements are continuously imposed on both service providers and educational institutions. The General Data Protection Regulation and the UK Data Protection Act require explicit consent for data collection and strict safeguards for storing sensitive information. According to the Information Commissioner’s Office (ICO) data security trends, the education and childcare sector reported 347 cyber incidents in 2023 (an increase of 55% from 2022). Schools and universities are often hesitant to adopt new technologies due to the risk of non compliance and potential legal liabilities. The complexity of ensuring that third party vendors adhere to security standards adds administrative burden and delays procurement processes. In addition, the Cyber Security Breaches Survey 2024 published by the government found that 71% of secondary schools and 41% of primary schools identified a breach or attack in the last 12 months, driving high concern levels. The requirement for data minimization limits the amount of information that can be used for personalization potentially reducing the effectiveness of adaptive learning algorithms. Parents and guardians are increasingly aware of digital rights and may object to the use of certain tracking tools. The cost of implementing robust encryption access controls and regular security audits increases operational expenses for edtech startups. Smaller providers may lack the resources to meet these rigorous standards leading to market consolidation. The fear of reputational damage from a data breach discourages some institutions from experimenting with innovative but unproven technologies. Privacy concerns will continue to be a barrier until trust is fully established. This requires implementing transparent practices and certified security measures.

Digital Divide and Infrastructure Inequalities Persist

Disparities in access to reliable internet and suitable devices restrict the equitable distribution of edtech benefits across the country, which holds back the expansion of the United Kingdom edtech market. This is despite high overall connectivity rates. Socioeconomic factors influence the quality of home learning environments creating a gap between advantaged and disadvantaged students. According to the Good Things Foundation’s "Digital Nation 2024" report, 7.9 million adults (approximately 15% of the adult population) lack basic digital skills, which significantly hinders their ability to engage with digital services, including edtech. Rural areas often suffer from slower broadband speeds and unstable connections making it difficult to stream video content or participate in live virtual classes. As per Ofcom's Connected Nations 2023 report, superfast broadband is available to 97% of UK homes, meaning approximately 400,000 to 500,000 premises (not 1.5 million) still lack access to decent superfast speeds. Schools in deprived areas may lack the budget to provide one to one device programs forcing students to share limited resources. The absence of quiet study spaces and parental support further exacerbates the challenge for low income families. This inequality limits the reach of edtech solutions that assume universal access to high quality hardware and connectivity. Providers must design lightweight applications that function well on older devices and low bandwidth networks which can constrain feature development. The digital divide also affects teacher readiness as educators in under resourced schools may receive less training on new technologies. Addressing these structural inequalities requires coordinated efforts from government and industry to ensure inclusive access. Without such measures edtech risks widening rather than closing the achievement gap.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence for Personalized Learning

The application of artificial intelligence and machine learning technologies sets the stage to transform the United Kingdom edtech market. This enables highly personalized and adaptive learning experiences. AI algorithms can analyze student performance data in real time to identify knowledge gaps and recommend tailored content paths. Intelligent tutoring systems provide immediate feedback and support mimicking the guidance of a human instructor which is particularly valuable in large classes. This personalized approach helps learners progress at their own pace thereby increasing completion rates and confidence. According to Pearson's learning efficacy studies, students leveraging AI-powered adaptive practice modules demonstrate higher retention and deeper conceptual understanding. Natural language processing enables automated grading of written assignments and facilitates interactive conversations with virtual assistants. Predictive analytics help educators identify at risk students early allowing for timely interventions and support. The automation of administrative tasks such as scheduling and reporting frees up teachers to focus on mentoring and curriculum development. AI powered content recommendation engines suggest relevant resources based on learner interests and career goals enhancing the overall educational experience. The ability to scale personalized instruction makes high quality education more accessible to larger audiences. This technological advancement transforms passive learning into an active and responsive process. Providers who leverage AI capabilities gain a competitive advantage by offering superior user experiences and measurable results.

Expansion of Immersive Technologies in Vocational Training

The adoption of virtual reality and augmented reality technologies offers lucrative opportunities for the United Kingdom edtech market. This trend is particularly visible in vocational and technical training sectors where practical skills are essential. These immersive tools allow learners to practice complex procedures in safe simulated environments reducing the risk and cost associated with real world training. According to PwC VR learners complete training four times faster than classroom learners and feel 275 percent more confident to act on what they learned after training. Industries such as healthcare engineering and construction are increasingly utilizing VR simulations to train staff on equipment operation safety protocols and emergency responses. VR enables repeated practice without consuming physical resources or endangering participants. Augmented reality overlays digital information onto real world objects assisting technicians with repair and maintenance tasks. The decreasing cost of VR headsets and improved graphics quality make these solutions more accessible to educational institutions. Partnerships between edtech firms and industry leaders ensure that simulations reflect current workplace standards and practices. The ability to track user movements and decisions within simulations provides detailed performance analytics for assessment. This technology bridges the gap between theoretical knowledge and practical application enhancing employability. The scalability of VR training allows organizations to standardize skills development across multiple locations. This innovation positions the UK as a leader in advanced vocational education.

MARKET CHALLENGES

Teacher Resistance and Lack of Professional Development

The resistance from educators who feel overwhelmed by the rapid introduction of new technologies without adequate training or support remains a significant constraint for the United Kingdom edtech market. Many teachers perceive edtech tools as adding to their workload rather than alleviating it due to steep learning curves and technical issues. According to a 2024 survey by the National Education Union (NEU), the pressing digital statistic is that 76% of teachers now use AI tools in their work (up from 53% the previous year), yet the union highlights a significant lack of formal guidance. This lack of confidence leads to underutilization of purchased software and a reversion to traditional teaching methods. The absence of continuous professional development programs means that educators struggle to keep pace with frequent software updates and new features. As per a study by the Education Endowment Foundation initiatives that fail to include comprehensive teacher training show negligible impact on student attainment. Technical glitches and poor user interface design further frustrate users leading to negative perceptions of edtech value. Schools often prioritize hardware procurement over pedagogical support resulting in unused devices and licenses. The pressure to integrate technology without clear instructional goals creates confusion and inefficiency. Teachers need time and resources to experiment with new tools and adapt their lesson plans accordingly. Without a culture of collaborative learning and peer support adoption remains fragmented. Edtech providers must invest in user friendly design and robust customer support to mitigate these issues. Addressing the human element of technology integration is crucial for sustainable implementation.

Interoperability and Fragmentation of Digital Ecosystems

The fragmentation of the educational technology landscape with numerous incompatible platforms and systems is a major challenge to the United Kingdom edtech market. These issues present a serious obstacle to seamless integration and data flow within the country’s educational institutions. Schools often use multiple software solutions for administration learning management assessment and communication which do not always communicate effectively with each other. The lack of interoperability forces staff to manually transfer data between systems increasing the risk of errors and administrative burden. Also, the absence of universal data standards makes it difficult for new edtech products to integrate with existing infrastructure. As per insights from the Open Standards Board the lack of common APIs hinders innovation and locks institutions into proprietary ecosystems. Vendors may resist open standards to maintain customer lock in limiting choice and flexibility for schools. The complexity of managing multiple logins and interfaces reduces user engagement and satisfaction. Students and parents face confusion when navigating different portals for grades attendance and assignments. Institutions incur higher costs for custom integrations and technical support to bridge these gaps. The fragmentation also complicates data analytics efforts as combining disparate data sources is technically challenging. Until the industry adopts widespread open standards and collaborative frameworks interoperability will remain a persistent obstacle. This issue stifles the potential for comprehensive data driven decision making in education.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 15.76% |

| Segments Covered | By Type, Application, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Market Leaders Profiled | Multiverse, Perlego, MyTutor, Atom Learning, Zen Educate, Century Tech, Firefly Learning, Lingumi, Satchel, Learning Technologies Group plc, BridgeU, Springpod, Glean, BibliU, and Synthesia. |

SEGMENTAL ANALYSIS

By Product Type Insights

The software segment led the United Kingdom edtech market and captured a 38.6% share in 2025. Factors such as the critical need for learning management systems assessment tools and administrative platforms that streamline educational operations have contributed to the leading position of this segment. This category includes cloud based applications that facilitate remote learning data analytics and personalized instruction. Educational institutions across the United Kingdom are increasingly adopting comprehensive learning management systems to centralize course content student data and communication channels. These platforms provide a unified interface for teachers students and parents enhancing collaboration and transparency in the learning process. According to Jisc over 90 percent of higher education institutions in the UK utilize a dedicated learning management system to deliver digital courses and manage assessments. The shift towards blended learning models necessitates robust software infrastructure that can handle high volumes of concurrent users and diverse media formats. Institutions prioritize systems that offer seamless integration with existing student information systems and third party tools to avoid data silos. The ability to track student engagement and performance in real time allows educators to intervene promptly when learners struggle. Cloud based deployment reduces the burden on internal IT teams and ensures automatic updates and security patches. The flexibility of software licenses allows schools to scale their usage based on fluctuating student numbers. This operational efficiency and strategic value sustain the dominance of the software segment in the edtech market.

The pressing need to alleviate the administrative burden on educators drives significant investment in software solutions that automate routine tasks such as grading attendance tracking and reporting. Teachers in the United Kingdom spend a substantial portion of their week on non teaching activities which impacts job satisfaction and retention. Software platforms that use artificial intelligence to grade multiple choice tests and provide feedback on written assignments free up valuable time for instructional planning. These tools also improve accuracy and consistency in record keeping reducing errors associated with manual entry. Parent portal features allow families to access grades and attendance records instantly reducing the volume of inquiries handled by school staff. The integration of scheduling and resource booking systems optimizes facility usage and minimizes conflicts. By streamlining these backend processes software solutions enable educators to focus more on pedagogy and student support. This tangible improvement in workflow efficiency makes software an indispensable component of modern educational infrastructure.

The content segment is expected to exhibit a noteworthy CAGR of 13.5% from 2026 to 2034. This rapid expansion of the segment is fueled by the demand for engaging interactive and curriculum aligned digital materials. Traditional static textbooks are being replaced by dynamic digital content that incorporates video animations simulations and gamified elements to enhance student engagement and comprehension. Learners respond better to multimedia formats that cater to different learning styles and maintain attention spans. According to Pearson's financial results, the 18% growth figure specifically refers to the Virtual Learning division's sales increase in the second half of the year (driven largely by US semester enrollments). Platforms offering virtual labs and 3D models allow students to visualize complex scientific concepts that are difficult to demonstrate in physical classrooms. The ability to update digital content instantly ensures that materials remain current with curriculum changes and scientific discoveries. Gamification elements such as badges leaderboards and progress bars motivate students to complete tasks and achieve learning goals. Content providers are investing heavily in producing high quality video lessons and animated explanations that simplify difficult topics. The accessibility of digital content on various devices supports flexible learning environments both in school and at home. This shift towards richer more engaging media sustains the high growth rate of the content segment.

The development of digital content that is strictly aligned with the National Curriculum for England and other regional standards drives adoption among schools seeking compliant and reliable teaching materials. Educators require resources that directly support specific learning objectives and assessment criteria to ensure students meet required benchmarks. Content providers collaborate with experienced teachers and subject matter experts to create materials that map precisely to curriculum requirements. As per BBC Bitesize millions of students access its curriculum aligned revision guides and videos annually indicating strong demand for standardized digital content. The availability of differentiated content allows teachers to cater to varying ability levels within the same class ensuring inclusivity. Assessment banks linked to specific curriculum topics help prepare students for standardized tests and examinations. The trust associated with established brands that guarantee curriculum compliance reduces the risk for schools when purchasing new materials. Regular updates ensure that content reflects changes in exam specifications and educational policies. This alignment provides peace of mind for educators and administrators driving consistent procurement of high quality digital content.

By Application Insights

In 2025, the K-12 segment held the majority share of 48.5% of the United Kingdom edtech market because of the large student population and mandatory government initiatives to integrate technology into primary and secondary education. This sector covers a wide range of tools from literacy apps to science simulations. Strong government policies requiring the integration of computing and digital skills into the K-12 curriculum drive substantial investment in educational technology for primary and secondary schools. The National Curriculum mandates that students develop proficiency in coding algorithms and digital citizenship from an early age. The National Centre for Computing Education provides funding and resources to support this mandate ensuring that schools have access to appropriate teaching materials. As per data from Ofsted inspections now evaluate how effectively schools use technology to enhance learning outcomes rather than just its presence. This regulatory pressure encourages headteachers to procure edtech solutions that align with statutory requirements. The emphasis on preparing students for a digital economy ensures long term commitment to technology integration. Government grants and subsidies help schools overcome budget constraints and invest in necessary infrastructure. The standardization of digital skills assessment further reinforces the importance of using technology in daily instruction. This policy driven approach creates a stable and predictable market for edtech providers targeting the K-12 sector.

High levels of parental involvement in education and the desire to support childrens learning at home drive demand for K-12 edtech products such as tutoring apps and practice platforms. Parents seek supplementary resources to help their children succeed academically and close any learning gaps. The convenience of mobile apps allows parents to monitor progress and engage with educational content alongside their children. The competitive nature of school admissions and exams motivates families to invest in additional learning tools. Edtech companies market directly to parents emphasizing ease of use and measurable improvements in grades. The availability of free trials and freemium models lowers the barrier to entry for hesitant buyers. Social proof through reviews and recommendations plays a crucial role in purchasing decisions. This direct to consumer channel complements school procurement and expands the overall market size for K-12 solutions.

The corporate training segment is predicted to witness the highest CAGR of 14.2% during the forecast period due to the urgent need for workforce upskilling and compliance training. Moreover, the fast pace of technological advancement creates a widening skills gap that organizations must address through continuous employee training and development programs. Companies rely on edtech solutions to deliver scalable and efficient upskilling initiatives in areas such as data analytics cybersecurity and artificial intelligence. According to the Chartered Institute of Personnel and Development (CIPD) Labour Market Outlook, approximately 47% of UK employers report having "hard-to-fill vacancies" (skills shortages). Online learning platforms allow employees to acquire new competencies without leaving their jobs minimizing disruption to business operations. The LinkedIn Workplace Learning Report indicates that skill sets for jobs have changed by 25% since 2015 and that learners using AI-powered features spend 25% more time learning. Microlearning modules enable workers to learn in short bursts fitting training into busy schedules. The ability to track completion and assess understanding ensures that training objectives are met. Industries undergoing digital transformation such as finance and healthcare are leading adopters of these technologies. The return on investment from improved employee productivity and retention justifies the expenditure. This persistent need for skill adaptation sustains the rapid growth of the corporate training segment.

Strict regulatory requirements across various industries mandate regular training for employees in areas such as health and safety data protection and anti money laundering fuelling demand for standardized edtech solutions. Organizations must ensure that all staff complete these compulsory courses to avoid legal penalties and reputational damage. According to the Health and Safety Executive (HSE) Annual Report, the regulator completed 248 criminal prosecutions in 2023/24 (convicting 92% of defendants). E learning platforms provide auditable records of completion and assessment results simplifying compliance reporting. As per insights from the Information Commissioners Office organizations use digital training tools to ensure staff understand GDPR obligations and data handling procedures. The consistency of online delivery ensures that all employees receive the same accurate information regardless of location. Automated reminders and recertification alerts help maintain ongoing compliance without manual administration. The cost effectiveness of digital training compared to instructor led sessions makes it the preferred choice for large workforces. The ability to update content quickly in response to regulatory changes ensures relevance. This regulatory pressure creates a steady and recurring revenue stream for edtech providers specializing in compliance training.

COUNTRY ANALYSIS

The United Kingdom was the next prominent player in the European edtech market and occupied a 20.1% share in 2025. This expansion of the UK market was driven by its strong educational heritage and supportive startup ecosystem. The country serves as a testbed for new pedagogical technologies and business models. It benefits from a vibrant edtech startup scene supported by venture capital incubators and government initiatives that foster innovation and growth. London in particular is recognized as a global center for edtech entrepreneurship attracting talent and funding from around the world. According to research, UK edtech companies have raised a total of £2.60 billion in equity funding, with £1.84 billion (71%) of that total secured since 2020. Accelerator programs such as EduTech UK provide mentorship and networking opportunities for early stage companies helping them refine their products and go to market strategies. As per sources, the number of active edtech companies in the UK has grown by 158% over the past ten years (2015–2025), reflecting both a diversity of education applications and a relatively low barrier to entry for software-led learning products. The presence of world class universities facilitates collaboration between researchers and entrepreneurs leading to evidence based product development. Government grants such as those from Innovate UK support research and development in emerging technologies like AI and VR. The supportive regulatory environment encourages experimentation while protecting user rights. This dynamic ecosystem ensures a continuous flow of new solutions addressing diverse educational challenges. The concentration of expertise and capital positions the UK as a dominant force in the European edtech landscape.

The widespread availability of high speed internet and digital devices creates a favorable environment for the adoption of edtech solutions across all sectors in the United Kingdom. Reliable connectivity ensures that students and employees can access online learning resources without interruption. According to the Office for Communications 97 percent of UK premises have access to superfast broadband enabling the use of rich media content and cloud based applications. The high penetration of smartphones and tablets among the population facilitates mobile learning and anytime access to educational materials. As per data from the Office for National Statistics 96 percent of households had internet access in 2023 providing a near universal audience for digital education. Schools and businesses have invested heavily in digital infrastructure ensuring that hardware and software needs are met. The digital literacy of the population reduces barriers to entry for new technologies. Government initiatives to improve digital skills further enhance the capability of users to engage with edtech tools. This strong foundational infrastructure supports the scalability and effectiveness of digital learning solutions. The readiness of the market to adopt new technologies sustains the UK position as a leader in the region.

COMPETITIVE LANDSCAPE

The competitive landscape of the United Kingdom edtech market is characterized by a diverse mix of established global publishers agile startups and specialized technology providers. Traditional educational publishers compete with pure play tech firms by leveraging their content expertise while adopting digital delivery models. Large multinational corporations offer comprehensive platforms whereas niche players focus on specific subjects or pedagogical approaches such as gamification or adaptive learning. Innovation in artificial intelligence data analytics and immersive technologies serves as a key differentiator among competitors. Price competition is moderate as institutions prioritize quality efficacy and compliance over lowest cost options. Partnerships between content creators and technology platforms are common as companies strive to offer integrated ecosystems. Regulatory compliance and data protection standards create barriers to entry for new participants lacking robust security infrastructure. The market sees continuous consolidation through mergers and acquisitions as larger entities seek to expand their capabilities. Customer retention relies heavily on demonstrated learning outcomes and user experience. This dynamic environment drives constant improvement in service quality and technological sophistication benefiting the education sector.

KEY MARKET PLAYERS

Some of the promising companies that are playing a dominating role in the United Kingdom edtech market include

- Multiverse

- Perlego

- MyTutor

- Atom Learning

- Zen Educate

- Century Tech

- Firefly Learning

- Lingumi

- Satchel

- Learning Technologies Group plc

- BridgeU

- Springpod

- Glean

- BibliU

- Synthesia

Top Players in the United Kingdom EdTech Market

Pearson PLC

Pearson PLC remains a dominant force in the United Kingdom edtech landscape by transitioning from traditional publishing to comprehensive digital learning services and assessment solutions. The company provides essential qualifications and online courseware for schools higher education institutions and corporate clients. Recent actions include significant investments in artificial intelligence driven adaptive learning platforms that personalize student experiences and improve outcomes. Pearson has expanded its partnership network with universities to deliver fully online degree programs enhancing accessibility for diverse learners. The organization focuses on developing robust data analytics tools that help educators track progress and identify areas for intervention. By integrating vocational training with academic pathways Pearson addresses the growing demand for skills based education. Its commitment to digital transformation ensures it remains a trusted provider of credible and effective educational technology solutions across the region.

Century Tech

Century Tech is a leading artificial intelligence powered learning platform in the United Kingdom that combines neuroscience with advanced technology to create personalized learning paths for students. The company serves schools colleges and corporations by offering adaptive content that responds to individual learner needs in real time. Recent initiatives involve expanding its AI capabilities to provide deeper insights into student cognition and engagement patterns. Century Tech has strengthened its market position through strategic partnerships with major exam boards and educational trusts to align content with national curriculum standards. The platform emphasizes reducing teacher workload by automating administrative tasks and providing actionable data for instructional planning. Its focus on evidence based pedagogy ensures high efficacy and user trust. Century Tech continuously refines its algorithms and expands its subject coverage. As a result, the company maintains its reputation as an innovative and impactful player in the UK edtech sector.

Oxford University Press

Oxford University Press leverages its prestigious academic heritage to deliver high quality digital educational resources and platforms to learners and educators across the United Kingdom. The press offers a wide range of interactive ebooks assessment tools and online courses for primary secondary and tertiary education. Recent actions include the development of integrated digital ecosystems that combine print and online materials for a seamless learning experience. Oxford University Press has invested heavily in creating accessible and inclusive content that meets diverse learning needs and regulatory requirements. The organization collaborates with teachers to ensure its digital products are pedagogically sound and practical for classroom use. By focusing on literacy language learning and professional development OUP strengthens its relevance in the digital age. Its brand reputation for accuracy and quality continues to drive adoption among schools and institutions seeking reliable educational technology solutions.

Top Strategies Used by Key Market Participants

Key players in the United Kingdom edtech market employ strategic initiatives to enhance their competitive positioning and drive sustainable growth. First they invest heavily in artificial intelligence and machine learning to personalize learning experiences and automate administrative tasks for educators. Second companies form strategic partnerships with schools universities and corporations to expand their reach and ensure curriculum alignment. Third they focus on developing mobile friendly and accessible platforms to accommodate diverse learning environments and user needs. Fourth providers emphasize data security and compliance with privacy regulations to build trust among institutions and parents. Fifth they prioritize evidence based product development by collaborating with researchers to validate educational efficacy. These strategies collectively enable organizations to deliver high value scalable and effective educational solutions that address the evolving demands of modern learners and educators effectively.

MARKET SEGMENTATION

This research report on the United Kingdom EdTech Market has been segmented based on the following categories.

By Type

- Hardware

- Software

- Content

By Application

- Preschool

- K-12

- Higher Education

- Others

By Country

- U.K

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com