UK Household Appliances Market Size, Share, Trends & Growth Forecast Report Segmented By Product (Major Home Appliances, Small Home Appliances ), Distribution Channel and Country – Industry Analysis From 2026 to 2034

UK Household Appliances Market Report Summary

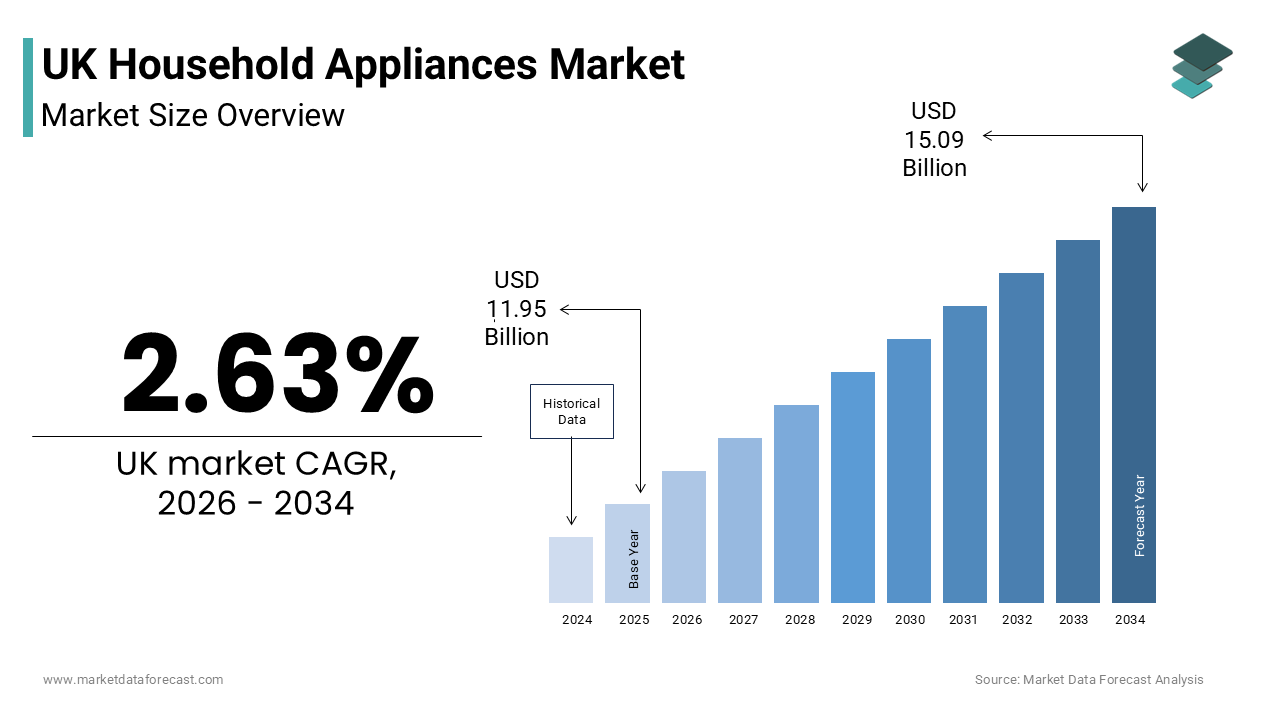

The UK household appliances market was valued at USD 11.95 billion in 2025 and is anticipated to reach USD 12.26 billion in 2026 from USD 15.09 billion by 2034, growing at a CAGR of 2.63% during the forecast period from 2026 to 2034. The growth of the UK household appliances market is driven by stringent energy efficiency regulations, increasing adoption of smart home technologies, and rising consumer preference for energy-efficient appliances. Growing investments in connected home ecosystems, expanding demand for premium and multifunctional appliances, and increasing awareness regarding sustainable living are further accelerating market growth. Moreover, the integration of artificial intelligence into household appliances, expansion of circular economy initiatives, and advancements in predictive maintenance technologies are supporting the expansion of the UK household appliances market.

Key Market Trends

-

Rising adoption of smart home appliances with AI-powered connectivity and remote monitoring capabilities.

-

Increasing consumer preference for energy-efficient appliances driven by stringent environmental regulations.

-

Growing emphasis on circular economy initiatives, including appliance repair, refurbishment, and recycling.

-

Rising integration of predictive maintenance and machine learning technologies into connected appliances.

-

Increasing demand for multifunctional and space-saving appliances suited to modern urban lifestyles.

Segmental Insights

- Based on product, the major home appliances segment dominated the UK household appliances market in 2025. The dominance of the segment is attributed to the essential nature of refrigerators, washing machines, ovens, and dishwashers in households, high replacement demand, increasing adoption of energy-efficient models, and growing integration of smart features such as remote diagnostics and automated maintenance alerts. Regulatory support for replacing inefficient appliances further strengthens segment growth.

- The small home appliances segment is projected to witness the fastest CAGR of 7.5% during the forecast period owing to rising consumer interest in healthy cooking, increasing adoption of air fryers, coffee machines, robotic vacuum cleaners, and other convenience-focused appliances, along with growing demand for compact and multifunctional products suitable for urban households.

- Based on distribution channel, the multi-brand stores segment dominated the UK household appliances market and accounted for 54.5% of the market share in 2025. The growth of the segment is driven by extensive product assortments, competitive pricing, attractive promotional offers, expert in-store assistance, and integrated omnichannel retail services such as click-and-collect and home delivery that enhance the overall customer experience.

- The exclusive brand outlets segment is anticipated to register the fastest CAGR of 8.4% during the forecast period due to increasing consumer preference for premium products, personalized shopping experiences, expert product demonstrations, exclusive product launches, customized financing solutions, and comprehensive after-sales support offered directly by manufacturers.

Regional Insights

- England dominated the UK household appliances market in 2025 owing to its large population base, extensive urbanization, strong retail infrastructure, continuous residential construction activities, and high consumer spending on home improvement products. The presence of major distribution centers and widespread adoption of smart home technologies continue to strengthen market growth across the region.

- Scotland is projected to witness notable growth during the forecast period due to increasing government support for energy-efficient home improvements, rising adoption of sustainable household technologies, expanding demand for smart appliances, growing environmental awareness among consumers, and increasing replacement of older appliances with energy-efficient models supported by national climate initiatives.

Competitive Landscape

The UK household appliances market is highly competitive and characterized by the presence of established multinational manufacturers and regional brands competing through technological innovation, energy efficiency, product quality, and smart connectivity features. Leading companies are focusing on developing AI-enabled appliances, integrating smart home ecosystems, improving sustainability through recycled materials and repairability, and expanding omnichannel retail strategies. Strategic partnerships with retailers, investments in research and development, continuous product innovation, and enhanced after-sales services continue to strengthen competitive positioning across the UK household appliances market.The prominent players operating in the UK household appliances market include Samsung Electronics Co., Ltd., LG Electronics Inc., Robert Bosch GmbH, Whirlpool Corporation, Miele & Cie. KG, Beko plc, Hotpoint, Siemens AG, Electrolux AB, Dyson Ltd., Russell Hobbs, and Haier Smart Home Co., Ltd.

UK Household Appliances Market Size

The UK household appliances market size was valued at USD 11.95 billion in 2025 and is anticipated to reach USD 12.26 billion in 2026 from USD 15.09 billion by 2034, growing at a CAGR of 2.63% during the forecast period from 2026 to 2034.

According to the Office for National Statistics, there are approximately 28.2 million households in the UK, each requiring a baseline set of essential appliances, such as refrigerators, washing machines, and ovens. As per the Department for Energy Security and Net Zero, the residential sector accounts for nearly 30% of total national energy consumption, with major appliances contributing significantly to this footprint. The market is characterized by a high penetration rate of white goods and small domestic appliances, driven by urbanization and dual-income households that prioritize convenience and time-saving solutions. Regulatory frameworks, such as the Energy Labelling Regulations, mandate strict efficiency standards, influencing product design and consumer choice. The transition toward smart home ecosystems has further expanded the functional scope of these devices, enabling remote monitoring and automated operation. Consumer behavior is increasingly shaped by sustainability concerns, prompting a preference for durable, energy-efficient models over disposable alternatives. The retail landscape features a mix of specialized electronics retailers, department stores, and growing online platforms that offer competitive pricing and extensive product information. This mature market continues to evolve through innovation in connectivity, material science, and energy management, ensuring alignment with environmental goals and digital integration trends.

MARKET DRIVERS

Stringent Energy Efficiency Regulations Drive Replacement of Older Units

Government mandates and regulatory pressures aimed at reducing carbon emissions are primarily fuelling the replacement of outdated household appliances with high-efficiency models in the UK, which is majorly driving the expansion of the UK household appliances market. The introduction of revised energy labeling schemes and minimum efficiency standards has made older, less efficient units economically and environmentally unviable for many homeowners. According to the Department for Energy Security and Net Zero, new regulations require all newly sold refrigerators and washing machines to meet rigorous energy performance criteria, effectively phasing out lower-rated products from the market. As per the Energy Saving Trust, replacing an old, G-rated washing machine with a new, A-rated model can save a typical household up to 34 pounds annually on energy bills, providing a compelling financial incentive for upgrades. Consumers are increasingly aware of the long-term cost benefits associated with lower energy consumption, leading to a shift in purchasing preferences toward premium efficient appliances. Retailers support this transition by prominently displaying energy ratings and offering trade-in schemes that reduce the upfront cost of new purchases. The regulatory roadmap provides clarity for manufacturers, encouraging investment in innovative technologies, such as heat pump dryers and inverter motors that maximize efficiency. This policy-driven demand ensures a steady flow of replacements, as households seek to comply with environmental standards and reduce their utility expenses amidst rising energy prices.

Rising Adoption of Smart Home Technologies Enhances Convenience and Control

The rapid integration of smart home technologies into household appliances are further contributing to the UK market expansion, as consumers seek greater convenience, connectivity, and control over their domestic environments. Smart appliances equipped with Wi-Fi connectivity and Internet of Things capabilities allow users to monitor and operate devices remotely via smartphone applications, enhancing daily routines and energy management. According to Statista, the number of smart home devices in the UK is projected to reach 45 million by 2025, indicating a robust ecosystem for interconnected appliances. As per YouGov, 40% of UK homeowners expressed interest in smart appliances that offer features such as remote start, diagnostic alerts, and automated replenishment orders. These functionalities appeal to tech-savvy demographics and busy professionals, who value time-saving solutions and real-time insights into appliance performance. Manufacturers respond by developing seamless interfaces that integrate with popular voice assistants and home automation platforms, creating cohesive user experiences. The ability to optimize usage patterns based on off-peak electricity tariffs further enhances the economic appeal of smart devices. Retailers highlight these advanced features in marketing campaigns, differentiating premium models from standard equivalents. This technological evolution transforms traditional appliances into intelligent assets that contribute to overall home efficiency and lifestyle enhancement, driving sustained demand for connected products.

MARKET RESTRAINTS

High Initial Costs and Economic Pressure Limit Consumer Spending Power

The substantial upfront cost associated with purchasing new high-efficiency and smart household appliances are majorly hampering the expansion of the UK household appliances market, particularly during periods of economic uncertainty. While modern appliances offer long-term savings through reduced energy consumption, the initial investment often exceeds several hundred pounds, posing a challenge for budget-constrained households. According to the Office for National Statistics, real household disposable income fell by 2.2% in 2023, reducing the capacity for major home improvements without external financing. As per the Retail Economics report, over 35% of shoppers reported postponing planned appliance purchases or opting for basic models due to financial pressures, affecting overall market volume. Consumers become more price-sensitive, seeking discounts, promotions, and extended warranty offers, rather than investing in premium features that may not provide immediate tangible benefits. The perception of appliances as durable goods allows buyers to extend the life of existing units through repair and maintenance, rather than replacement. Mid-market retailers suffer most as customers trade down to budget brands or wait for significant sales events. This economic restraint limits the ability of companies to invest in new collections and marketing initiatives, as they focus on inventory clearance and cost management. The prolonged nature of these financial challenges creates a subdued market atmosphere, where growth is difficult to achieve without aggressive pricing strategies.

Supply Chain Disruptions and Component Shortages Impact Availability

Ongoing disruptions in global supply chains and shortages of critical electronic components are further hindering the UK market growth, which is affecting production timelines and product availability. The UK market relies heavily on semiconductors, sensors, and specialized metals primarily sourced from Asia, which is making it vulnerable to geopolitical tensions and logistical bottlenecks. According to the British Chambers of Commerce, around 40% of UK businesses reported experiencing supply chain disruption in 2024 due to global manufacturing constraints and geopolitical conflicts, delaying product launches and replenishment. As per the Federation of Small Businesses, rising costs of running operations and acquiring goods have forced over half of small businesses to increase their prices, forcing companies to either absorb losses or pass costs to consumers. These fluctuations create uncertainty in pricing strategies and inventory planning, leading to potential stockouts or excess inventory, depending on demand forecasting accuracy. Labor shortages in manufacturing hubs further exacerbate production delays, limiting output capacity during peak seasons. Retailers struggle to maintain consistent assortments, impacting customer satisfaction and loyalty. The complexity of managing multi-tier supply chains requires significant investment in risk mitigation strategies, such as diversifying suppliers and holding higher safety stocks. These operational hurdles restrict agility and profitability, hindering the industry's ability to respond quickly to emerging trends and consumer demands in a competitive marketplace.

MARKET OPPORTUNITIES

Expansion of Circular Economy and Repair Services

The growing emphasis on sustainability and waste reduction presents a lucrative opportunity for the UK household appliances market. Consumers are increasingly interested in extending the lifespan of their appliances through professional maintenance and refurbishment, rather than immediate replacement. According to the Waste and Resources Action Programme, the UK generates approximately 1.5 million tonnes of electrical waste annually, highlighting the urgent need for effective recycling and reuse strategies. As per the Right to Repair data, over 60% of UK consumers support legislation that mandates manufacturers to provide spare parts and repair manuals, empowering independent technicians and DIY enthusiasts. Brands that offer comprehensive warranty packages, take-back schemes, and certified refurbishment programs build stronger emotional connections with environmentally conscious demographics. Innovations in modular design allow for easier component replacement, reducing repair costs and downtime. Retailers can leverage this trend by partnering with local repair shops and offering incentives for trading in old units. This approach aligns with regulatory pushes for greater corporate responsibility and resource efficiency, ensuring long-term viability. By positioning themselves as stewards of product longevity, companies can differentiate their offerings and capture value from secondary markets, while reducing environmental impact.

Integration of Artificial Intelligence for Predictive Maintenance and Efficiency

The integration of artificial intelligence and machine learning into household appliances offers a significant growth avenue for manufacturers in the UK seeking to enhance user experience and operational efficiency. AI-driven algorithms can analyze usage patterns to optimize performance, predict maintenance needs, and automate energy consumption based on real-time data. According to a report by Deloitte, approximately 40% of large businesses have already integrated artificial intelligence into their broader digital strategies, indicating that the adoption of AI in consumer solutions is expected to grow as users seek smarter and more autonomous home systems. As per Wired UK, appliances equipped with predictive maintenance capabilities can alert users to potential issues before they result in breakdowns, reducing repair costs and inconvenience. Machine learning enables devices to learn user preferences, such as preferred wash cycles or cooling temperatures, adjusting settings automatically for optimal comfort and efficiency. Manufacturers leverage data insights to offer personalized recommendations and firmware updates that keep devices relevant over time. This technological evolution transforms appliances from passive tools into proactive assistants that support sustainable living and convenience. Partnerships with energy providers allow for dynamic pricing integration, where appliances operate during off-peak hours to minimize costs. By focusing on intelligence and automation, companies can command premium prices and build stronger ecosystem lock-in, fostering long-term customer loyalty in a competitive market.

MARKET CHALLENGES

Intense Competition from Private Label and Budget Brands

Fierce competition from private label and budget brands is majorly challenging the growth of the UK household appliances market, as retailers expand their own-label offerings with competitive pricing and improved quality perceptions. Large supermarket chains and electronics retailers leverage their bargaining power to produce cost-effective alternatives that mimic popular branded products in terms of features and aesthetics. According to the Retail Economics data, value retailers and private label appliances captured 20% of the market volume in 2024, reflecting growing consumer acceptance of store brands amid economic pressure. As per the British Retail Consortium, retailer confidence in own-brand quality has grown, leading to enhanced packaging designs and feature sets that narrow the gap with national brands. This trend forces branded manufacturers to justify price premiums through superior innovation, marketing, and brand storytelling, which requires substantial investment. Price wars erode profit margins across the sector, compelling companies to optimize production efficiency and reduce operational costs to remain competitive. Smaller brands struggle to compete against the economies of scale enjoyed by large retailers, who control distribution channels and shelf placement decisions. Consumer loyalty becomes increasingly fragile, as shoppers experiment with alternatives without significant perceived risk. Established players must continuously reinforce brand equity through emotional connections and unique value propositions, to prevent migration to private labels.

Complex Regulatory Compliance and Environmental Standards

Navigating the complex and evolving regulatory landscape regarding energy efficiency, waste management and chemical safety imposes significant compliance burdens on household appliance manufacturers in the UK, which is further challenging the UK market expansion. Authorities enforce strict guidelines under the Ecodesign for Energy-Related Products Regulations, requiring rigorous testing and documentation to ensure products meet environmental standards. According to the Office for Product Safety and Standards, enforcement actions and safety notifications are closely tracked, with product safety and non-compliance reviews increasing in recent years, highlighting enforcement rigor. As per the Competition and Markets Authority, misleading environmental claims face tighter verification requirements to prevent greenwashing under stricter consumer protection codes. Manufacturers must invest in extensive testing and legal review to ensure compliance, which increases time to market and operational costs. Changes in approved substance lists necessitate frequent reformulations, disrupting supply chains and consumer familiarity. The ambiguity surrounding certain materials and recycling processes leads to cautious formulation approaches that may compromise efficacy. Consumer advocacy groups monitor labels closely, reporting violations that damage brand reputation. Navigating this complex regulatory landscape requires dedicated compliance teams and continuous monitoring of legislative updates. Non-compliance risks severe penalties and loss of consumer trust, making adherence a critical but burdensome aspect of business operations.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 2.63% |

| Segments Covered | By Product, Distribution Channel and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Market Leaders Profiled | Samsung Electronics Co., Ltd., LG Electronics Inc., Robert Bosch GmbH, Whirlpool Corporation, Miele & Cie. KG, Beko plc, Hotpoint, Siemens AG, Electrolux AB, Dyson Ltd., Russell Hobbs, and Haier Smart Home Co., Ltd. |

SEGMENTAL ANALYSIS

By Product Insights

The major home appliances segment dominated the market by holding the highest share of the UK market in 2025. The growth of the major home appliances segment in the UK market can be credited to their fundamental role in daily domestic operations and high unit value. These large white goods are considered essential infrastructure for modern households, requiring significant capital investment and long-term usage, which sustains consistent demand through replacement cycles. According to the Office for National Statistics, over 95% of households in the UK own a refrigerator and washing machine, indicating near universal penetration and necessity. As per the Department for Energy Security and Net Zero, the average lifespan of these appliances ranges from 10 to 15 years, creating a predictable replacement market that is less susceptible to short-term economic fluctuations compared to discretionary items. The regulatory push for energy efficiency has accelerated the retirement of older, inefficient models, as consumers seek to reduce rising utility bills. Manufacturers focus on innovation in compressor technology and water conservation to meet strict environmental standards, ensuring continued relevance. Retailers prioritize this segment due to higher transaction values and opportunities for extended warranty sales and installation services. The integration of smart features into major appliances further enhances their appeal by offering remote monitoring and automated maintenance alerts. This combination of functional necessity, regulatory compliance, and technological advancement ensures that major home appliances remain the cornerstone of the market, generating substantial revenue volume.

On the other hand, the small home appliances segment is estimated to record a promising CAGR of 7.5% during the forecast period owing to the changing lifestyle patterns, health consciousness, and the desire for culinary experimentation. Devices such as air fryers, coffee machines, blenders, and robotic vacuums offer convenience and specialized functionality that align with modern, busy schedules and wellness goals. According to a retail sales report by Mintel, spending on small kitchen appliances has seen sharp cyclical jumps, with over 30% of consumers investing in new cooking solutions to save energy and match shifting dining habits. As per YouGov, 45% of UK adults reported purchasing at least one new small appliance in the past year, citing ease of use and health benefits, such as reduced oil consumption, as primary motivators. The rise of social media food trends drives demand for specific tools, like air fryers and espresso makers, that enable users to recreate restaurant-quality experiences at home. Compact designs suit smaller urban living spaces, while affordable price points encourage impulse purchases and gift-giving. Manufacturers rapidly iterate designs to match aesthetic trends, and introduce multifunctional devices that save counter space. This segment benefits from lower entry barriers and frequent product launches, keeping consumer interest high and driving repeat purchases across diverse demographic groups.

By Distribution Channel Insights

The multi-brand stores segment led the market by capturing 54.5% of the regional market share in 2025 due to their extensive product assortments, competitive pricing, and one-stop shopping convenience. These retailers offer consumers the ability to compare multiple brands, specifications, and price points side by side, facilitating informed decision-making for high-involvement purchases. According to the British Retail Consortium, multi-brand outlets account for the majority of white goods sales, leveraging their bargaining power to secure favorable terms from manufacturers and pass savings to customers. As per Kantar Worldpanel, 70% of shoppers prefer visiting large retail chains for major appliance purchases, citing the availability of promotional deals, bundle offers, and immediate stock availability as key factors. The physical presence allows customers to inspect build quality and interact with knowledgeable staff, who can provide technical advice and demonstrations. Retailers invest heavily in showroom layouts that simulate home environments, helping customers visualize products in their own spaces. Integrated online and offline services, such as click-and-collect and home delivery, enhance the shopping experience. This channel remains indispensable for mass-market brands seeking volume and visibility in a highly competitive retail environment, where price and convenience are paramount.

However, the exclusive brand outlets segment is estimated to witness a promising CAGR of 8.4% during the forecast period owing to the rising demand for premium products, personalized service, and immersive brand experiences. These dedicated stores allow manufacturers to showcase their full product range, including high-end and innovative models that may not be available in multi-brand retailers. According to Deloitte, consumers are increasingly willing to pay a premium for direct brand interactions that offer expert consultation, customization options, and superior after-sales support. As per Retail Week, flagship showrooms for major appliance brands have seen stable foot traffic, as shoppers seek tactile experiences and detailed product demonstrations that build trust and loyalty. Exclusive outlets enable brands to control the narrative around their technology and design philosophy, fostering deeper emotional connections with customers. They also serve as hubs for launching new products and hosting exclusive events that generate buzz and media coverage. The ability to offer tailored financing packages and extended warranties directly enhances perceived value. This channel thrives on its ability to differentiate through service excellence and brand prestige, appealing to affluent consumers who prioritize quality and exclusivity over price.

REGIONAL ANALYSIS

England Household Appliances Market Analysis

England held the major share of the UK market share in 2025 and is expected to maintain its position as the primary driver of market growth and high-volume demand for household appliances over the next few years, due to concentrated property developments. England holds the dominant position in the UK household appliances market, accounting for approximately 85% of total national sales due to its high population density, concentration of economic activity, and extensive retail infrastructure. The region contains the majority of the country's major cities, including London, Manchester, and Birmingham, which serve as centers of consumption and distribution for electrical goods. According to the Office for National Statistics, England is home to over 57 million people, representing the largest consumer base with significant disposable income for home improvements and appliance upgrades. As per the Ministry of Housing, Communities and Local Government, the continuous need for new home building and urban regeneration in the South East and London creates a stable pipeline of customers needing to furnish new homes with essential appliances. Urban living trends drive demand for compact and efficient models suitable for apartments, while suburban areas support sales of larger family-sized units. The presence of major distribution centers ensures efficient supply chain operations and timely delivery across the region. Marketing campaigns often target English consumers through local influencers and regional promotions, reinforcing brand relevance. Continuous urban regeneration projects and new housing developments sustain long-term demand, ensuring that England remains the primary engine of growth for the UK household appliances industry.

Scotland Household Appliances Market Analysis

Scotland is poised to expand its deployment of high-efficiency household technologies over the coming years, as state-backed climate strategies accelerate the replacement of old appliances. Scotland holds a significant and distinct position in the UK household appliances market, characterized by strong growth potential driven by ambitious energy efficiency targets and specific rural heating and appliance needs. Consumers in Scotland are increasingly attentive to energy consumption due to higher heating costs and environmental awareness, leading to higher adoption rates of A-rated and smart appliances. According to the Scottish Government, the Heat in Buildings Strategy encourages the uptake of energy-efficient technologies, creating opportunities for appliance manufacturers to promote low-consumption models. As per Home Energy Scotland, rural properties, which make up a significant portion of the housing stock, often require robust and reliable appliances that can withstand varying conditions and limited service access. The cooler climate increases the usage intensity of washing machines and tumble dryers, driving replacement frequency. Government grants for energy-efficient home improvements stimulate demand for upgraded appliances among low-income households. Urban centers, like Edinburgh and Glasgow, drive commercial and residential demand through modernization projects. The strong sense of community and support for local businesses fosters loyalty toward brands that offer excellent customer service and durability. This unique combination of policy support, climatic necessity, and rural dynamics ensures that Scotland remains a vital and growing component of the overall UK household appliances market landscape.

COMPETITIVE LANDSCAPE

The UK household appliances market features intense competition characterized by established global brands and agile local players vying for consumer attention in a mature yet evolving landscape. Major competitors leverage strong brand equity extensive distribution networks and significant marketing budgets to dominate shelf space and influence purchasing decisions. Innovation in energy efficiency and smart connectivity serves as a key differentiator driving frequent product launches and upgrades. Price sensitivity remains high during economic uncertainty prompting retailers to offer promotional deals and bundle offers to stimulate volume. The rise of private label offerings from large supermarkets poses a constant threat by providing comparable quality at lower price points attracting budget conscious shoppers. Digital engagement becomes crucial as brands utilize online platforms to showcase technical specifications and user reviews. Success depends on the ability to balance technological advancement with affordability and sustainability credentials. Companies must continuously adapt to regulatory changes and consumer expectations to maintain relevance and profitability in this highly competitive environment.

KEY MARKET PLAYERS

Some of the promising companies that are playing a dominating role in the UK Household Appliances Market include

- Samsung Electronics Co., Ltd.

- LG Electronics Inc.

- Robert Bosch GmbH

- Whirlpool Corporation

- Miele & Cie. KG

- Beko plc

- Hotpoint

- Siemens AG

- Electrolux AB

- Dyson Ltd.

- Russell Hobbs

- Haier Smart Home Co., Ltd.

Top Players In The UK Household Appliances Market

Dyson Ltd

Dyson Ltd stands as a premier innovator in the UK household appliances sector renowned for its advanced engineering and distinctive design philosophy. The company focuses on solving common household problems through proprietary technologies such as digital motors and air multiplication. Recently Dyson has strengthened its market position by expanding its portfolio into smart home cleaning solutions including robotic vacuums with advanced navigation systems. They have invested heavily in research and development facilities in the UK to accelerate product innovation and sustainability initiatives. Their commitment to premium quality and performance allows them to command higher price points while maintaining strong brand loyalty. By emphasizing durability and energy efficiency Dyson appeals to environmentally conscious consumers seeking long term value and superior functionality in their daily domestic routines.

Beko Plc

Beko Plc contributes significantly to the UK market by offering a wide range of affordable and energy efficient home appliances that cater to diverse consumer needs and budgets. The brand is recognized for its reliability and extensive distribution network across major retailers and independent stores. Recent actions include the launch of new product lines featuring advanced hygiene technologies and smart connectivity options to meet evolving consumer expectations. Beko has enhanced its sustainability credentials by introducing appliances made from recycled materials and promoting repairability through accessible spare parts. They actively engage with customers through digital platforms providing usage tips and maintenance support. By balancing cost effectiveness with innovative features Beko maintains its appeal to families and first time buyers seeking practical and dependable solutions for modern living.

Samsung Electronics UK Limited

Samsung Electronics UK Limited plays a vital role in the household appliances market by delivering cutting edge technology and seamless smart home integration across its product range. The company leverages its expertise in consumer electronics to create connected ecosystems where appliances communicate with smartphones and other devices. Recently Samsung has introduced AI powered features in washing machines and refrigerators that optimize performance and energy consumption based on user habits. They have expanded their retail presence with experiential showrooms allowing customers to interact with products firsthand. Samsung prioritizes sustainability by using recycled ocean bound plastics in manufacturing and offering trade in programs. Their focus on design aesthetics and technological sophistication attracts tech savvy consumers who value convenience and modern lifestyle enhancements in their home environments.

Top Strategies Used By Key Market Participants

Key players in the UK household appliances market prioritize innovation by integrating smart technologies and artificial intelligence to enhance user convenience and energy efficiency. Companies focus on sustainability by adopting circular economy principles such as using recycled materials and offering repair services to extend product lifecycles. Strategic partnerships with retailers and online platforms ensure widespread availability and competitive pricing strategies. Brands invest in direct to consumer channels to build stronger customer relationships and gather valuable data for personalized marketing. Emphasis on premium design and multifunctional features helps differentiate products in a crowded marketplace. These strategies enable manufacturers to adapt to changing consumer preferences while maintaining competitiveness and driving growth in the dynamic home appliance sector.

MARKET SEGMENTATION

This research report on the UK Household Appliances Market has been segmented based on the following categories.

By Product

- Major Home Appliances

- Small Home Appliances

By Distribution Channel

- Multi-Brand Stores

- Exclusive Brand Outlets

- Online

- Other Distribution Channels

By Country

- U.K

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com