United Kingdom Pet Care Market Size, Share, Trends & Growth Forecast Report Segmented By Product Type (Dry Pet Food, Wet Pet Food ), Pet Type, Distribution Channel and Country – Industry Analysis From 2026 to 2034

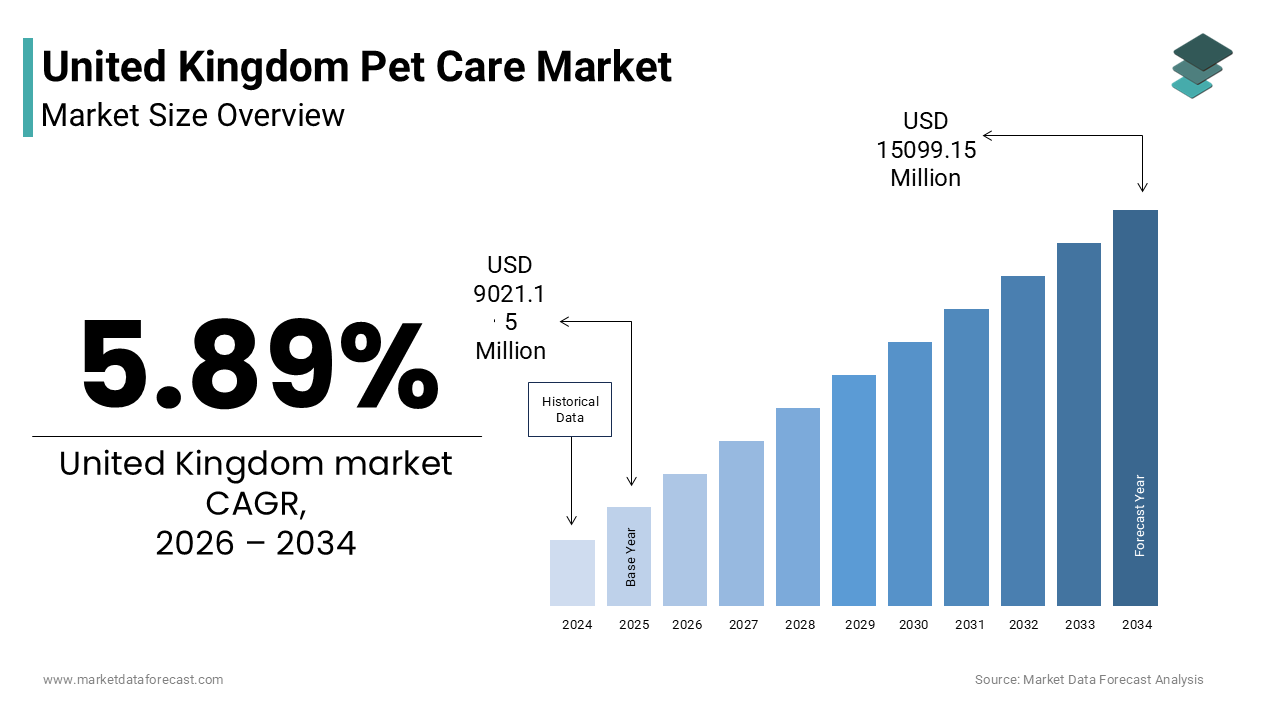

Market Size, 2025

$9,021.15 MnMarket Estimate, 2026

$9,552.50 MnMarket Forecast, 2034

$15,099.15 MnCAGR, 2026–2034

5.89%United Kingdom Pet Care Market Report Summary

The United Kingdom pet care market was valued at USD 9,021.15 million in 2025 and is anticipated to reach USD 9,552.50 million in 2026 from USD 15,099.15 million by 2034, growing at a CAGR of 5.89% during the forecast period from 2026 to 2034. The growth of the United Kingdom pet care market is driven by increasing pet ownership, rising humanization of pets, and growing demand for premium pet products and services. Expanding awareness regarding preventive pet healthcare, increasing spending on pet nutrition and wellness, and growing adoption of digital pet care solutions are further accelerating market growth. Moreover, advancements in pet health monitoring technologies, expansion of telemedicine services for pets, and increasing demand for sustainable and ethically sourced pet products are supporting the expansion of the United Kingdom pet care market.

Key Market Trends

- Rising humanization of pets leading to increased spending on premium nutrition, healthcare, and wellness products.

- Increasing adoption of telemedicine, wearable devices, and digital health monitoring solutions for companion animals.

- Growing demand for sustainable pet products, including eco-friendly packaging and alternative protein-based pet foods.

- Strong focus on preventive healthcare through specialized diets, supplements, vaccinations, and wellness programs.

- Expansion of subscription-based pet food delivery services and personalized pet care solutions.

Segmental Insights

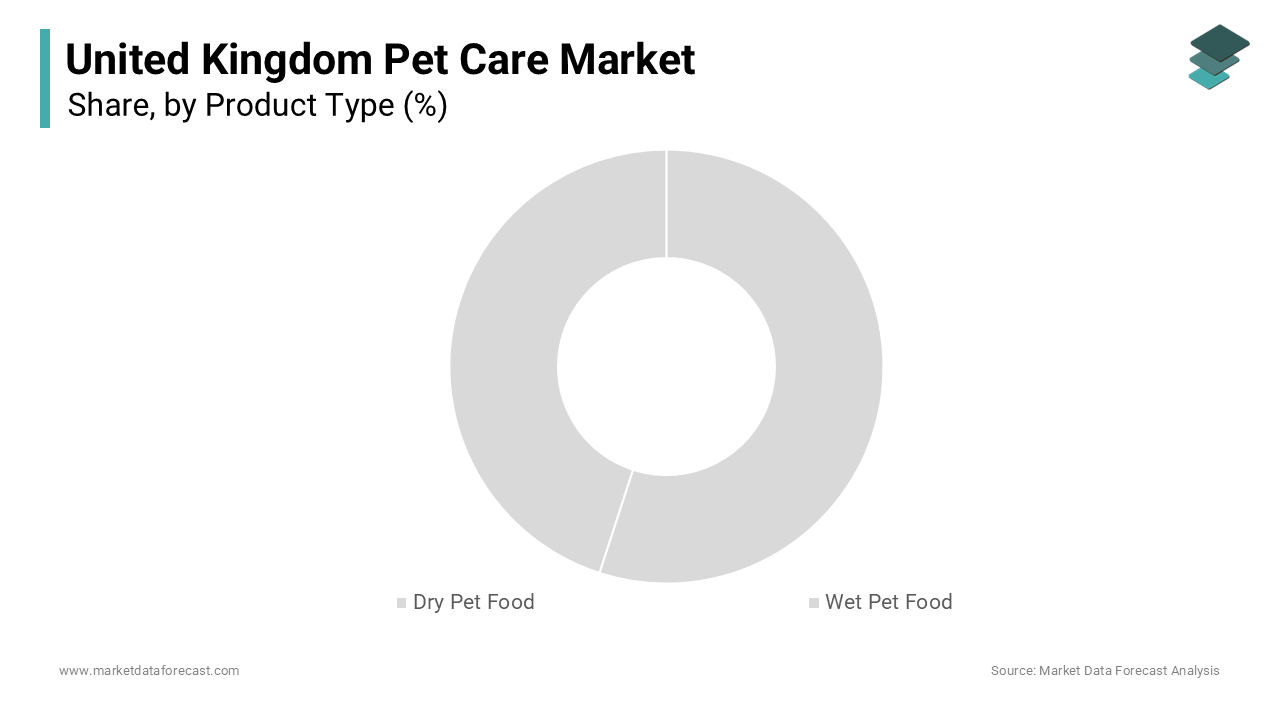

- Based on product type, the dry pet food segment dominated the United Kingdom pet care market and held the largest share in 2025. The segment’s dominance is attributed to its convenience, affordability, longer shelf life, ease of storage, and broad availability across multiple retail channels.

- The wet pet food segment is projected to witness the fastest CAGR during the forecast period owing to increasing consumer preference for premium nutrition, higher palatability, improved hydration benefits, and growing demand for natural and human-grade pet food products.

- Based on pet type, the dog segment accounted for the leading share of the United Kingdom pet care market in 2025. The dominance of this segment is driven by high dog ownership rates, increasing expenditure on healthcare and grooming, rising demand for premium nutrition products, and growing spending on pet accessories and wellness services.

- The cat segment is anticipated to register the fastest CAGR during the forecast period due to increasing urbanization, growing preference for low-maintenance companion animals, rising adoption among younger consumers, and increasing demand for specialized feline nutrition and healthcare products.

- Based on distribution channel, the offline segment held the major share of the United Kingdom pet care market in 2025 owing to strong consumer preference for physical product inspection, immediate product availability, personalized advice from store staff, and integrated veterinary and grooming services.

- The online segment is expected to witness rapid growth during the forecast period because of increasing e-commerce adoption, subscription-based purchasing models, convenient home delivery services, personalized product recommendations, and wider availability of niche pet care products.

Regional Insights

The United Kingdom accounted for a significant share of the European pet care market in 2025, supported by high pet ownership rates, strong animal welfare regulations, and increasing consumer spending on companion animal health and wellness. The country benefits from a well-established retail infrastructure, advanced veterinary healthcare services, and growing adoption of premium and sustainable pet care products. Rising awareness regarding pet nutrition, preventive healthcare, and digital pet care technologies continues to strengthen market growth across the United Kingdom.

Competitive Landscape

The United Kingdom pet care market is highly competitive and characterized by the presence of multinational pet food manufacturers, specialized pet retailers, veterinary service providers, and rapidly growing e-commerce platforms competing through product innovation, premiumization, and customer engagement. Leading companies are focusing on expanding specialized nutrition portfolios, investing in digital pet health solutions, strengthening omnichannel retail capabilities, and enhancing sustainability initiatives. Strategic partnerships with veterinary networks, animal welfare organizations, and technology providers are further strengthening market positioning across the pet care ecosystem. Prominent players in the United Kingdom pet care market include Mars Petcare, Nestlé Purina PetCare, Pets at Home Group Plc, Jollyes, Pet Family Limited, Butternut Box, Forthglade Foods Ltd, Inspired Pet Nutrition Ltd, VetPartners, and CVS Group plc.

United Kingdom Pet Care Market Size

The United Kingdom pet care market size was valued at USD 9021.15 million in 2025 and is anticipated to reach USD 9552.50 million in 2026 from USD 15099.15 billion by 2034, growing at a CAGR of 5.89% during the forecast period from 2026 to 2034.

Pet care is the daily responsibility of maintaining a domesticated animal's health, safety, and overall well-being. This market has evolved from basic sustenance provision to a holistic wellness ecosystem where pets are increasingly regarded as integral family members rather than mere possessions. The market is characterized by high penetration rates sophisticated consumer expectations and a strong emphasis on animal welfare and ethical sourcing. According to UK Pet Food, approximately 60% of households in the United Kingdom owned at least one pet in 2024, reflecting the deep societal integration of companion animals across 17.2 million homes. As per Office for National Statistics (ONS) data, single-person households comprise 30% of all households in the UK. Sociological trends indicate that many of these solitary individuals rely heavily on companion animals for emotional support and comfort. The regulatory environment overseen by bodies such as the Department for Environment Food and Rural Affairs ensures strict standards for animal welfare and product safety. Consumer behavior is shifting toward premiumization with significant demand for natural organic and specialized dietary products. The rise of digital health monitoring telemedicine for pets and subscription based delivery models further modernizes the sector. This dynamic landscape requires continuous innovation to meet the evolving needs of conscientious pet owners who prioritize longevity quality of life and sustainability in their purchasing decisions.

MARKET DRIVERS

Humanization of Pets and Emotional Companionship Trends

The humanization of pets and the growing trend of viewing companion animals as family members are primary factors propelling the United Kingdom pet care market forward. This cultural shift has led to increased willingness among owners to spend on premium products and services that enhance the health happiness and longevity of their pets. According to UK Pet Food (formerly PFMA), over 95% of owners consider their pet a member of the family, a sentiment that drives trends in 'pet humanization' and increased spending on premium nutrition and healthcare. As per research, 55% of pet owners are concerned about filler ingredients (like grains and by-products), a key factor driving the shift toward premium brands that market 'clean labels' and specific health benefits. The emotional bond between humans and animals has intensified particularly following periods of social isolation driving demand for interactive toys grooming services and pet insurance. Owners are increasingly attentive to specific dietary needs such as grain free raw or hypoallergenic options mirroring human food trends. The desire to provide the best possible care results in regular veterinary visits preventive treatments and wellness check ups. This deep emotional connection ensures that pet care remains a priority expense even during economic downturns sustaining consistent market growth and encouraging innovation in product offerings.

Rising Awareness of Preventive Healthcare and Nutrition

Rising awareness of preventive healthcare and the critical role of nutrition in animal longevity is also a powerful force driving demand within the United Kingdom pet care market. Pet owners are becoming more educated about the link between diet exercise and disease prevention leading to proactive management of their pets health. The British Veterinary Association (BVA) identifies pet obesity as a top animal welfare concern; however, a disconnect exists, as UK Pet Food data reveals that only 4% of owners recognize their pet is overweight, and half have never consulted a vet regarding their pet's weight. As per Royal Canin industry insights there is a growing preference for functional foods that support joint health digestive balance and immune system strength particularly for aging pets. The availability of detailed nutritional information on packaging and online resources empowers consumers to make informed choices. Preventive measures such as dental care products flea and tick preventatives and regular vaccinations are now standard practices rather than optional extras. Insurance providers also encourage preventive care through discounts and coverage incentives reducing long term medical costs. This focus on wellness over cure drives sustained demand for specialized supplements veterinary diets and health monitoring tools ensuring that the healthcare segment of the pet care market continues to expand significantly.

MARKET RESTRAINTS

Economic Pressure and Cost of Living Crisis

Economic pressure and the ongoing cost of living crisis are significant restraints hindering discretionary spending within the United Kingdom pet care market. Inflationary pressures on energy food and household essentials have forced many families to reassess their budgets leading to trading down from premium to value brands or delaying non essential veterinary procedures. According to the Office for National Statistics real household disposable income declined in recent years causing financial strain for millions of pet owning households. According to the PDSA, the cost-of-living crisis forced over 30% of pet owners to make personal sacrifices to afford pet care, with 11% of owners actively delaying veterinary visits due to treatment costs. The rising price of raw materials for pet food including meat grains and packaging has led to increased retail prices which are passed on to consumers. Some owners may reduce the frequency of professional grooming or switch to home grooming kits to save money. The financial burden is particularly acute for low income households who may struggle to balance pet care with other essential needs. This economic constraint limits the growth potential of premium segments and forces manufacturers to introduce more affordable alternatives. The uncertainty of future economic conditions makes long term planning difficult for both consumers and businesses in the pet care sector.

Supply Chain Disruptions and Raw Material Volatility

Supply chain disruptions and volatility in raw material prices are major factors affecting the stability and profitability of the United Kingdom pet care market. The industry relies heavily on global supply chains for key ingredients such as poultry fish meal and cereals which are susceptible to geopolitical tensions climate change and logistical barriers. Also, the Department for Environment, Food and Rural Affairs (Defra) show that extreme weather events drastically reduced UK arable crop yields, directly inflating the cost and restricting the availability of core agricultural ingredients used in pet food. According to industry trackers like Logistics UK and the Confederation of British Industry (CBI), global logistics delays, container bottlenecks, and spiked freight costs heavily disrupted supply chains, causing periodic pet food stock shortages and price hikes. The reliance on imported proteins and specialized additives makes the market vulnerable to international trade policies and currency fluctuations. Manufacturers face difficulties in maintaining consistent pricing and product availability which can erode consumer trust and brand loyalty. Small and medium sized enterprises are particularly affected as they lack the bargaining power and inventory buffers of larger corporations. These operational uncertainties require companies to invest in diversified sourcing strategies and resilient logistics networks which increase operational costs. The inability to guarantee stable supply chains poses a persistent risk to market growth and consumer satisfaction.

MARKET OPPORTUNITIES

Expansion of Digital Health and Telemedicine Services

The expansion of digital health and telemedicine services offers substantial opportunities for innovation and convenience within the United Kingdom pet care market. Pet owners are increasingly seeking accessible and efficient ways to monitor their pets health and consult with veterinarians without the need for immediate physical visits. Research shows rapid growth in UK veterinary telehealth platforms, as pet owners increasingly demand the convenience of digital triage for minor ailments, behavior advice, and post-operative checks. As per Amazon Web Services case studies cloud based health monitoring devices allow for real time tracking of vital signs activity levels and sleep patterns providing valuable data for preventive care. Mobile applications that integrate with wearable collars enable early detection of health issues such as arthritis or anxiety allowing for timely intervention. Subscription based telemedicine services offer affordable access to professional advice reducing the burden on traditional veterinary clinics. The integration of artificial intelligence in diagnostic tools enhances accuracy and speed of assessment. This digital transformation not only improves animal welfare but also creates new revenue streams for tech companies and veterinary practices. The growing comfort with digital solutions among pet owners ensures sustained growth in this innovative segment.

Growth of Sustainable and Ethical Pet Products

The growth of sustainable and ethical pet products sets the stage for brands to align with environmental values and attract conscientious consumers in the country, which is expected to fuel the expansion of the United Kingdom pet care market. Pet owners are increasingly aware of the ecological footprint of their pets and seek products that minimize environmental impact through responsible sourcing and eco friendly packaging. As per Mars Petcare sustainability report there is rising demand for insect based proteins and plant derived ingredients which require fewer resources and produce lower greenhouse gas emissions compared to traditional livestock. Biodegradable waste bags recycled plastic toys and carbon neutral shipping options are becoming key differentiators for brands. Certifications such as B Corp status and Marine Stewardship Council labels enhance credibility and trust among environmentally aware shoppers. Retailers are expanding their shelves to include green alternatives catering to this niche but growing segment. Marketing transparency regarding supply chains and manufacturing processes builds brand loyalty. This shift toward responsible consumption not only benefits the planet but also drives innovation and competitive advantage for companies that prioritize sustainability in their product development.

MARKET CHALLENGES

Veterinary Workforce Shortages and Access to Care

Veterinary workforce shortages and limited access to professional care are critical challenges in the United Kingdom pet care market. These issues affect the well-being of animals and the satisfaction of owners. The demand for veterinary services has outpaced the supply of qualified professionals leading to long waiting times and increased stress for clinic staff. According to the Royal College of Veterinary Surgeons data the profession faces a significant retention crisis with many veterinarians leaving due to burnout and mental health pressures. As per the British Veterinary Association (BVA) and related industry vacancy trackers, more than half of all UK practices report active difficulties recruiting permanent veterinary surgeons, heavily intensifying existing pressure on staff workloads. This scarcity limits the capacity of clinics to accept new patients and perform routine procedures promptly. Pet owners may struggle to find available appointments for vaccinations surgeries or emergency care leading to delayed treatments and poorer health outcomes. The shortage also drives up the cost of veterinary services as practices compete for limited talent. Rural areas are particularly affected with fewer options for local care requiring owners to travel long distances. Addressing this workforce crisis requires systemic changes in education training and working conditions. The accessibility and affordability of quality care will remain a major challenge for the industry. This will hold true until the supply of veterinary professionals increases.

Regulatory Complexity and Compliance Burdens

Regulatory complexity and stringent compliance burdens constitute enduring barriers for manufacturers and service providers in the United Kingdom pet care market. The market is subject to a web of regulations covering animal welfare food safety labeling requirements and environmental standards which require constant vigilance and adaptation. As per Food Standards Agency guidelines strict controls on ingredient sourcing and additive usage necessitate rigorous testing and quality assurance processes increasing operational costs. Non compliance can result in product recalls fines and reputational damage which can be devastating for brands. The introduction of new laws such as restrictions on certain single use plastics requires rapid reformulation of packaging and product designs. Keeping pace with evolving regulations across different jurisdictions adds complexity for companies operating internationally. Small businesses often lack the resources to navigate these legal landscapes effectively putting them at a disadvantage compared to larger corporations. The administrative burden diverts resources from innovation and marketing slowing down product launches and market entry. Balancing compliance with competitiveness remains a delicate and costly endeavour for all market participants.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.89% |

| Segments Covered | By Product Type, Pet Type, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Market Leaders Profiled | Mars Petcare, Nestlé Purina PetCare, Pets at Home Group Plc, Jollyes, Pet Family Limited, Butternut Box, Forthglade Foods Ltd, Inspired Pet Nutrition Ltd, VetPartners, and CVS Group plc. |

SEGMENTAL ANALYSIS

By Product Type Insights

The dry pet food segment was the largest in the UK pet care market and occupied a 58.5% share in 2025. This is mainly because it provides exceptional convenience for pet owners who prioritize easy storage, simple feeding, and cost-efficiency. Dry kibble has a longer shelf life compared to wet food and does not require refrigeration making it a practical choice for busy households. The ability to leave dry food out for free feeding or use in automatic dispensers appeals to owners with irregular schedules. Additionally, dry food is generally more affordable per serving than wet or raw alternatives making it accessible to a broader demographic including budget conscious consumers. The variety of formulations available from standard maintenance diets to specialized veterinary prescriptions ensures that dry food meets diverse nutritional needs. This combination of practicality affordability and availability ensures that dry pet food remains the dominant product type in the UK market sustaining high volume sales and consistent demand across all retail channels.

The leadership of the dry pet food segment is further reinforced by its perceived nutritional density and benefits for dental health which are increasingly important to conscientious pet owners. Many veterinarians recommend dry kibble as it helps reduce plaque and tartar buildup through the mechanical action of chewing promoting better oral hygiene. The low moisture content allows for higher concentration of nutrients per gram ensuring that pets receive adequate energy and protein without excessive volume. Advances in extrusion technology have improved the palatability and digestibility of dry food addressing previous concerns about taste and absorption. Premium brands now offer grain free limited ingredient and high meat content options that appeal to health focused consumers. These functional benefits combined with scientific backing enhance the value proposition of dry food driving sustained preference and loyalty among UK pet owners who prioritize long term health outcomes for their companions.

The wet pet food segment is likely to experience the fastest CAGR of 8.5% from 2026 to 2034. This rapid expansion of the segment is propelled by the fact that owners are actively seeking highly palatable and hydrating options for their pets. Wet food is often preferred by picky eaters and older animals with dental issues due to its soft texture and strong aroma which stimulates appetite. The perception of wet food as a premium treat or meal enhancer drives frequent purchases even among owners who primarily feed dry kibble. Innovations in packaging such as single serve pouches and trays offer portion control and freshness appealing to modern consumers. The availability of human grade ingredients and gourmet recipes mimicking human dining trends further accelerates adoption. This focus on enjoyment and physiological well being ensures that wet pet food continues to capture market share rapidly driven by increasing awareness of holistic pet wellness.

The rapid expansion of the wet pet food segment is further fueled by the trend toward premiumization and the demand for human grade ingredients that mirror high quality human diets. Consumers are increasingly scrutinizing labels seeking transparent sourcing natural preservatives and high meat content without fillers or artificial additives. The emotional bond between owners and pets drives willingness to pay a premium for products that promise superior quality and ethical production standards. Marketing campaigns emphasizing farm to bowl narratives and sustainability resonate strongly with environmentally conscious buyers. The versatility of wet food allows for easy mixing with supplements or medications enhancing its utility for health management. These factors combine to make wet pet food a dynamic and rapidly growing segment driven by evolving consumer expectations for quality and transparency.

By Pet Type Insights

In 2025, the dog segment led the United Kingdom pet care market and captured a 44.2% share. It remains the most popular companion animal due to its deep cultural and social integration into British family life. Dogs require regular exercise grooming and training driving consistent demand for accessories services and high volume food consumption. The social nature of dogs encourages outdoor activities and interaction with other pet owners fostering community engagement and brand loyalty. Owners often view dogs as active partners in their lifestyle leading to higher expenditure on durable toys travel gear and outdoor equipment. The emotional dependency on dogs for companionship and security further solidifies their status as primary beneficiaries of pet care spending. This high ownership base and multifaceted care requirements ensure that the dog segment generates the largest revenue share in the UK pet care industry sustaining robust growth across all product categories.

The top position of this segment is further reinforced by the significant expenditure on healthcare and preventive services required to maintain canine health and longevity. Dogs are prone to specific health issues such as hip dysplasia skin allergies and dental disease necessitating regular veterinary visits and specialized treatments. The aging dog population has increased demand for geriatric care including arthritis management and cognitive support supplements. Advanced diagnostic tools and surgical procedures are increasingly utilized extending life expectancy and improving quality of life. Owners are willing to invest heavily in these services to ensure their companions remain healthy and active. This commitment to comprehensive healthcare ensures that the dog segment remains the dominant force in the pet care market with sustained demand for both medical and wellness products.

The cat segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 7.2% during the forecast period. This growth is fuelled by urbanization and changing lifestyles, which make felines an attractive choice for modern households. Cats are perceived as lower maintenance than dogs requiring less space and no outdoor exercise making them ideal for apartment living and busy professionals. The quiet and clean nature of cats reduces household disruption attracting renters and those with limited outdoor access. The proliferation of indoor enrichment products such as climbing trees interactive toys and automated litter boxes supports the well being of indoor cats driving product innovation. Social media platforms featuring cat content further popularize feline ownership inspiring new adopters. This alignment with contemporary living patterns ensures that the cat segment continues to grow rapidly capturing a larger share of the pet care market.

The swift expansion of this segment is further fueled by the increasing focus on indoor health and specialized nutrition tailored to the unique needs of domestic felines. Indoor cats are prone to obesity urinary issues and stress related behaviors prompting owners to seek targeted dietary solutions. Owners are increasingly educated about the importance of taurine protein quality and moisture content in maintaining feline health. The availability of breed specific and age specific formulas allows for precise nutritional management. Behavioral health products such as calming treats and pheromone diffusers also contribute to market growth as owners seek to improve their cats mental well being. This heightened awareness of specific health needs drives consistent innovation and spending in the cat care sector ensuring sustained high growth rates.

By Distribution Channel Insights

The offline distribution channel segment held the majority share of the United Kingdom pet care market in 2025. Many consumers continue to value physical stores because they offer immediate product availability, tactile evaluation, and personal advice. Supermarkets pet specialty stores and veterinary clinics allow owners to inspect product quality check expiration dates and receive immediate assistance from staff. The ability to speak with knowledgeable staff builds trust and confidence in product choices especially for new pet owners seeking guidance. Promotional displays and in store demonstrations effectively drive impulse purchases and brand trial. The sensory experience of smelling food or feeling toy textures influences buying decisions in ways online images cannot replicate. This tangible interaction and instant gratification ensure that offline channels remain the primary route for pet care procurement despite the rise of digital alternatives.

The dominance of the offline channel is also solidified by the integration of services such as grooming veterinary care and training which drive footfall and foster community engagement. Pet specialty retailers often operate as hubs for pet owners offering bundled experiences that combine shopping with professional services. Staff interactions during service appointments provide opportunities for personalized product recommendations enhancing cross selling effectiveness. Local events adoption days and training classes build loyal communities around physical stores differentiating them from impersonal online retailers. The social aspect of visiting pet stores allows owners to connect with fellow enthusiasts sharing tips and experiences. This holistic approach to pet care creates a sticky ecosystem that sustains the leadership of offline distribution channels.

The online distribution channel segment is expected to exhibit a noteworthy CAGR of 12.5% between 2026 and 2034. This quick surge of the segment is propelled by consumers who prioritize convenience and automated replenishment. E commerce platforms enable homeowners to order heavy bulk items like litter and food directly to their doorsteps saving time and physical effort. The wide selection available online allows consumers to access niche brands and specialized products not found in local stores. Price comparison tools empower shoppers to find the best deals enhancing value perception. Mobile apps facilitate easy reordering and tracking improving the overall user experience. This seamless and efficient shopping model appeals to busy lifestyles ensuring that online channels continue to capture market share rapidly.

The rapid expansion of the online segment is further fueled by advanced personalization and data driven recommendations that enhance the shopping experience and increase customer loyalty. Online retailers leverage purchase history and browsing behavior to suggest relevant products tailored to individual pet needs. Detailed product reviews and user generated content provide social proof helping buyers make informed decisions. Virtual consultations with vets or nutritionists offered through some platforms add value and expertise to the digital journey. Loyalty programs integrated with online accounts reward frequent shoppers with points and exclusive offers. This level of customization and support creates a superior and engaging shopping environment that drives sustained growth in the online distribution channel.

COUNTRY ANALYSIS

The United Kingdom followed closely behind in the pet care market in Europe and accounted for a 23.6% share in 2025. This growth was driven by high ownership rates stringent animal welfare laws and a sophisticated consumer base. The market position shows a deep emotional connection between humans and animals with pets widely regarded as family members deserving of premium care. According to UK Pet Food (formerly PFMA), the UK has one of the highest pet ownership rates in Europe, with over 17.2 million households (approx. 60%) owning a pet, totaling a population of over 36 million pets nationwide. The Animal Welfare Act 2006 (overseen by Defra) ensures rigorous standards for animal welfare and licensed services (such as boarding), whereas pet product safety, specifically food, is regulated by the Food Standards Agency (FSA) under separate animal feed legislation. London and other major cities serve as hubs for innovation in pet tech and specialized veterinary services. The regulatory framework supports ethical sourcing and transparency driving demand for sustainable and natural products. High disposable income among pet owners facilitates spending on premium foods healthcare and insurance. The market is resilient to economic fluctuations due to the non negotiable nature of pet care. Strong presence of international and domestic brands fosters competition and innovation. The UK leads in setting trends for humane treatment and holistic wellness influencing broader European markets. This combination of cultural affection regulatory strength and economic capacity maintains the UK's leadership position in the regional pet care landscape.

COMPETITIVE LANDSCAPE

The competition within the United Kingdom pet care market is intense and characterized by the rivalry between specialized retailers large supermarket chains and rapidly growing e commerce platforms. Established specialists leverage their expertise in animal health and comprehensive service offerings including veterinary care and grooming to differentiate themselves from generalist competitors. Supermarkets compete on convenience and price utilizing their extensive store networks and loyalty programs to capture routine purchases of pet food and essentials. Online giants dominate through vast product selection rapid delivery capabilities and competitive pricing attracting tech savvy consumers who prioritize ease of shopping. Private label brands from both supermarkets and specialists are gaining traction as consumers seek value without compromising on quality. Innovation in product formulation particularly in natural and functional foods serves as a key battleground for brand differentiation. Customer retention relies heavily on emotional engagement trust and consistent service quality. The market sees continuous entry of niche brands focusing on sustainability and ethical sourcing challenging incumbents to adapt their portfolios. This dynamic environment requires constant innovation and strategic agility to maintain relevance and profitability in a saturated landscape.

KEY MARKET PLAYERS

Some of the promising companies that are playing a dominating role in the United Kingdom Pet Care Market include

- Mars Petcare

- Nestlé Purina PetCare

- Pets at Home Group Plc

- Jollyes

- Pet Family Limited

- Butternut Box

- Forthglade Foods Ltd

- Inspired Pet Nutrition Ltd

- VetPartners

- CVS Group plc

Top Players in the United Kingdom Pet Care Market

Pets at Home Group plc

Pets at Home Group plc maintains a prominent position in the United Kingdom pet care sector by operating an integrated model that combines retail stores veterinary services and grooming salons. The company focuses on providing comprehensive care solutions for pet owners through its extensive network of physical locations and online platforms. Recent strategic initiatives include the expansion of its Vets for Pets and Companion Care networks to increase accessibility to professional healthcare. Pets at Home has also enhanced its digital engagement tools allowing customers to manage appointments and purchase products seamlessly. By prioritizing animal welfare and community support the group strengthens its brand loyalty. These efforts aim to create a holistic ecosystem where retail and medical services complement each other ensuring sustained growth and customer retention in the competitive UK market.

J Sainsbury plc

J Sainsbury plc plays a significant role in the United Kingdom pet care market primarily through its supermarket chains which offer a wide range of pet food and accessories. The retailer leverages its strong supply chain and established customer base to provide convenient shopping experiences for pet owners. Recent actions involve expanding its own label pet food ranges to include premium and natural options catering to health conscious consumers. Sainsbury’s has also integrated pet care products into its loyalty program offering personalized discounts and rewards to drive repeat purchases. By focusing on quality affordability and accessibility the company reinforces its position as a trusted provider of everyday pet essentials. These strategies help Sainsbury’s maintain relevance and compete effectively against specialized retailers in the broader pet care landscape.

Amazon UK Services Ltd

Amazon UK Services Ltd contributes significantly to the United Kingdom pet care market by offering an vast selection of pet products through its efficient e commerce platform. The company provides convenience and speed with its Prime delivery service making it a preferred choice for many pet owners seeking regular supplies. Recent developments include the expansion of its private label pet food and accessory brands which offer competitive pricing and quality assurance. Amazon has also enhanced its subscription services allowing customers to automate recurring orders for food and litter. By leveraging advanced data analytics for personalized recommendations the company improves customer satisfaction and retention. These initiatives strengthen Amazon’s position as a leading online destination for pet care products meeting the diverse needs of modern consumers across the UK.

Top Strategies Used by Key Market Participants

Key players in the United Kingdom pet care market predominantly employ product innovation and omnichannel integration to maintain competitive advantage and enhance customer loyalty. Companies invest heavily in developing premium and specialized nutrition formulas that address specific health needs such as weight management and digestive health. Expanding veterinary and grooming services within retail environments creates a holistic care ecosystem that drives footfall and increases customer retention. Implementing subscription models for recurring purchases ensures steady revenue streams and convenience for pet owners. Strategic partnerships with animal welfare organizations build brand trust and demonstrate corporate social responsibility. Enhancing digital platforms with personalized recommendations and easy reordering options improves the overall user experience. Focusing on sustainable packaging and ethical sourcing appeals to environmentally conscious consumers. These combined strategies enable participants to adapt to evolving consumer preferences and sustain growth in a dynamic marketplace

MARKET SEGMENTATION

This research report on the United Kingdom Pet Care Market has been segmented based on the following categories.

By Product Type

- Dry Pet Food

- Wet Pet Food

By Pet Type

- Dog

- Cat

- Others

By Distribution Channel

- Offline

- Online

By Country

- U.K

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com