UK Used Cars Market Size, Share, Trends & Growth Forecast Report - Segmented By Vendor, Vehicle Age, Fuel Type, Body Type, Sales Channel, Ownership, Price Brand, and By Country - Industry Analysis and Forecast, 2026 to 2034

Market Size, 2025

$105.23 BnMarket Estimate, 2026

$118.12 BnMarket Forecast, 2034

$297.73 BnCAGR, 2026–2034

12.25%UK Used Cars Market Report Summary

The UK used cars market was valued at USD 105.23 billion in 2025 and is anticipated to reach USD 118.12 billion in 2026 and further expand to USD 297.73 billion by 2034, growing at a CAGR of 12.25% during the forecast period from 2026 to 2034. The growth of the UK used cars market is driven by increasing consumer demand for affordable vehicle ownership, rising new vehicle prices, and growing confidence in certified pre-owned vehicles. The expansion of digital automotive marketplaces, improved vehicle financing options, and enhanced transparency in vehicle history reporting are further supporting market growth. Additionally, evolving consumer preferences, supply chain dynamics, and the increasing availability of quality used vehicles are creating significant opportunities across the market.

Key Market Trends

- Rising consumer preference for cost-effective transportation solutions amid increasing new vehicle prices and economic uncertainty.

- Growing adoption of certified pre-owned vehicle programs offering quality assurance, warranties, and improved buyer confidence.

- Expansion of online used car marketplaces and digital retail platforms streamlining vehicle discovery and purchasing processes.

- Increasing integration of vehicle inspection, valuation, financing, and trade-in services into used car sales ecosystems.

- Growing demand for fuel-efficient, hybrid, and electric used vehicles as sustainability and operating cost considerations influence purchasing decisions.

Segmental Insights

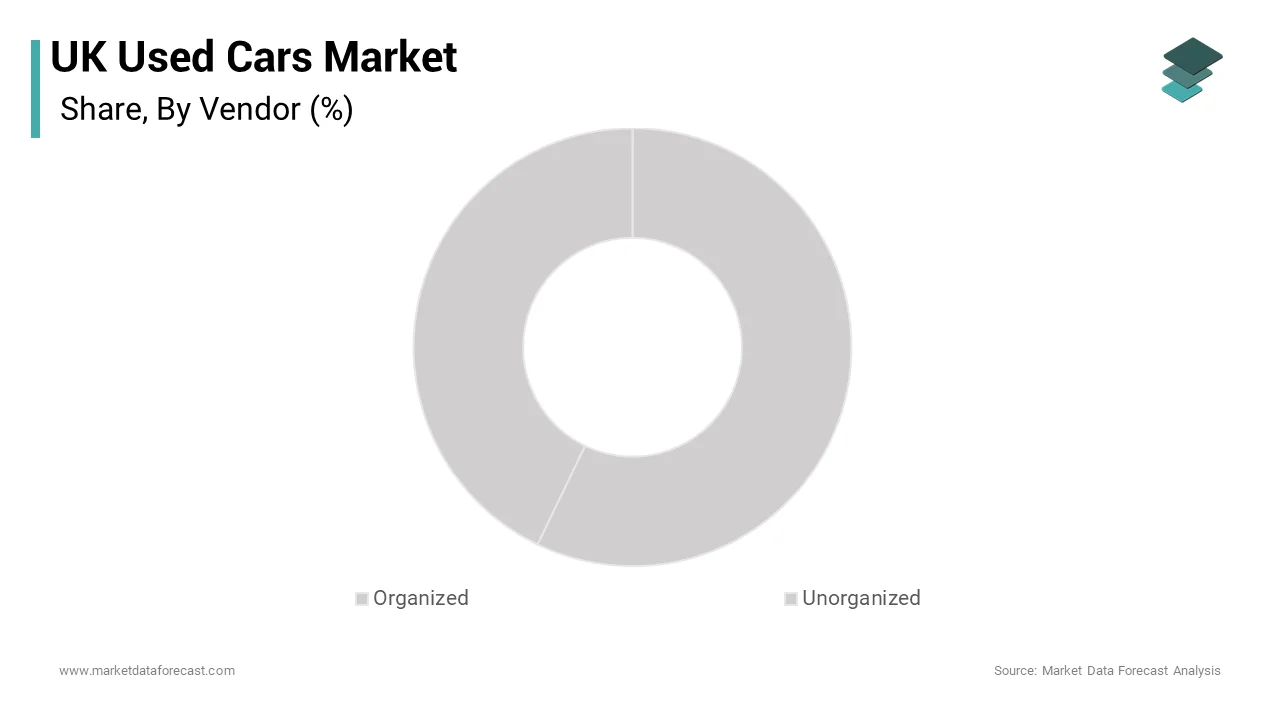

- Based on vendor, the organized segment dominated the UK used cars market and accounted for 58.8% of the market share in 2025. The segment’s leadership is attributed to greater consumer trust, transparent pricing, certified vehicle programs, financing support, and comprehensive after-sales services offered by established dealerships and automotive retailers.

- Based on vehicle age, the 3 to 5 years segment held the largest share of the UK used cars market, capturing 34.3% in 2025. The dominance of this segment is driven by the availability of relatively new vehicles that offer modern features, lower depreciation, favorable pricing, and strong reliability compared to older models.

- Based on sales channel, the offline sales channels segment accounted for the majority share of the UK used cars market in 2025. The segment continues to benefit from consumers' preference for physical vehicle inspections, test drives, direct dealer interactions, and personalized purchasing experiences before making high-value automotive purchases.

Regional Insights

The United Kingdom is the second-largest used car market in Europe and accounted for 15.2% of the regional market share in 2025. Market growth is supported by a mature automotive ecosystem, strong consumer demand for pre-owned vehicles, widespread dealership networks, and increasing digitalization of vehicle sales. The country's well-established financing infrastructure, vehicle certification programs, and growing adoption of online automotive platforms continue to strengthen the used car market landscape.

Competitive Landscape

The UK used cars market is highly competitive, with leading companies focusing on digital transformation, inventory expansion, customer experience enhancement, and omnichannel retail strategies. Market participants are investing in advanced vehicle inspection technologies, online sales platforms, financing solutions, and data-driven pricing models to strengthen their competitive positions. Strategic acquisitions, dealership network expansion, and integration of end-to-end automotive services remain key growth strategies across the industry.

Prominent players in the UK used cars market include Auto Trader Group plc, Constellation Automotive Group Ltd, Arnold Clark Automobiles Ltd, Cazoo Group Ltd, Car Giant Ltd, Lookers plc, Pendragon plc (CarStore), Vertu Motors plc, Motorpoint Group plc, Manheim (Cox Automotive U.K.), Sytner Group Ltd, Inchcape plc, TrustFord (Ford Retail Ltd), Jardine Motors Group U.K. Ltd, AvailableCar Ltd, Carwow Ltd, Motors.co.uk Ltd, Aramis Group, and Peter Vardy Ltd.

UK Used Cars Market Size

The UK used cars market size was valued at USD 105.23 billion in 2025 and is anticipated to reach USD 118.12 billion in 2026 to reach USD 297.73 billion by 2034, growing at a CAGR of 12.25% during the forecast period from 2026 to 2034.

A used car (also called a pre-owned or secondhand car) is a vehicle that has already been owned or leased by one or more people. It is a vital component of the national automotive ecosystem, facilitating mobility for millions of households through the exchange of pre owned vehicles. This market operates as a dynamic secondary marketplace where vehicles transition between private owners, dealerships, and leasing companies, ensuring continuous circulation of automotive assets. The market is characterized by a diverse inventory ranging from nearly new models to older high mileage vehicles, catering to varied budgetary constraints and consumer preferences. Consumer behavior is heavily influenced by economic conditions, with many buyers viewing used cars as a pragmatic alternative to new vehicle purchases due to lower upfront costs and reduced depreciation impacts. According to the Department for Transport, there are over 33.5 million licensed cars within the United Kingdom's overall pool of 42 million registered vehicles, providing a massive, sustainable foundation for secondary market transactions. The regulatory environment plays a crucial role, with strict emissions standards and safety inspections shaping the availability and desirability of certain vehicle types. Digital transformation has significantly altered transaction methods, with online platforms enabling transparent pricing and broader access to inventory. Trust mechanisms such as vehicle history checks and warranty offerings have become standard expectations, enhancing consumer confidence. The market also reflects broader societal trends toward sustainability, as extending the lifecycle of vehicles aligns with circular economy principles. Infrastructure developments, including charging networks for electric vehicles, further influence market dynamics by affecting the residual values and demand for different powertrains. This complex interplay of economic, regulatory, and technological factors defines the current state of the United Kingdom used cars landscape.

MARKET DRIVERS

Economic Pressure And Affordability Constraints Drive Preference For Pre Owned Vehicles

Persistent economic pressure and rising living costs have significantly intensified the demand for these cars in the country, which accelerates the growth of the United Kingdom used car market. Therefore, consumers are seeking affordable mobility solutions amidst financial uncertainty. High inflation rates and increased interest rates have elevated the cost of new vehicle ownership, making monthly finance payments prohibitive for many households. According to the Office for National Statistics, the consumer price index for transport remained elevated during recent inflationary periods, a factor that automotive market analysts note has driven buyers to prioritize lower initial outlays and vehicles with stable value retention. Used cars offer a compelling alternative by allowing buyers to avoid the steep depreciation associated with new vehicles, which can lose between 30 and 35 percent of their total value within the first year of ownership. This financial prudence is particularly evident among first time buyers and families managing tight budgets, who view pre owned vehicles as a necessary compromise to maintain essential transportation. The availability of competitive finance packages for used cars further supports this trend, with lenders offering flexible terms that align with lower purchase prices. Additionally, the widening gap between new and used car prices has made the secondary market increasingly attractive, as buyers can access higher specification models for the same budget. Research indicates that used car transactions consistently outnumber new car registrations by a significant margin, reflecting this structural shift in consumer behavior. The desire to minimize financial risk while securing reliable transport ensures that economic constraints remain a primary driver sustaining robust demand in the used car sector.

Supply Chain Disruptions In New Car Manufacturing Boost Secondary Market Inventory Demand

Ongoing supply chain disruptions in the new car manufacturing sector have inadvertently strengthened the United Kingdom used cars market. This limits the availability of new vehicles. Semiconductor shortages and logistical bottlenecks have constrained production volumes for major automakers, leading to extended waiting times and reduced stock levels at dealerships. According to the Society of Motor Manufacturers and Traders, new car registrations have faced volatility due to these supply side challenges, pushing consumers toward the more readily available used car market. This scarcity of new vehicles has maintained strong demand for pre owned alternatives, as buyers unwilling to wait months for delivery opt for immediate purchase options. The limited supply of new cars has also supported higher residual values for used vehicles, making them an attractive asset class for both individual sellers and trade in customers. Dealerships have responded by expanding their used car inventories and enhancing refurbishment processes to meet heightened demand. The imbalance between supply and demand in the new car segment has created a ripple effect, sustaining activity levels in the secondary market even during periods of economic slowdown. Furthermore, the delay in new model launches has kept older models relevant for longer periods, extending their commercial lifecycle. This structural constraint in the primary market acts as a persistent driver for the used car sector, ensuring steady transaction volumes as consumers adapt to the realities of limited new vehicle availability.

MARKET RESTRAINTS

Stringent Emissions Regulations And Clean Air Zones Restrict Older Vehicle Viability

The implementation of stringent emissions regulations and the expansion of clean air zones across major cities in the country are major restraints for the United Kingdom used car market. This constraint is particularly evident for older diesel and petrol vehicles. Policies such as the Ultra Low Emission Zone in London and similar initiatives in Birmingham and Manchester impose daily charges on non compliant vehicles, reducing their appeal and residual value. According to the Department for Environment, Food & Rural Affairs, Clean Air Zones aim to improve air quality by disincentivizing the use of older, more polluting vehicles, a strategy that critics argue financially penalizes drivers unable to upgrade. Potential buyers are increasingly hesitant to invest in vehicles that may face future restrictions or additional operating costs, leading to a decline in demand for higher emission models. This regulatory pressure accelerates the obsolescence of certain vehicle segments, forcing dealers to discount stock or export vehicles to markets with less stringent rules. The uncertainty surrounding future regulatory changes creates hesitation among consumers, who fear further devaluation of their assets. Small businesses and low income households, who often rely on older affordable vehicles, are disproportionately affected, limiting their mobility options. The compliance costs associated with upgrading to cleaner vehicles are substantial, creating a barrier to entry for many participants in the used car market. This regulatory landscape fragments the market, creating distinct tiers of value based on emission standards and complicating inventory management for retailers who must navigate varying local rules.

Consumer Trust Deficits Regarding Vehicle History And Condition Impede Transactions

A persistent lack of consumer trust regarding a vehicle's history and mechanical condition also hampers the expansion of the United Kingdom used car market. This deters potential buyers from completing transactions. Concerns about clocked mileage, hidden accident damage, and undisclosed mechanical faults create significant perceived risk for purchasers, particularly in private sales. According to Trading Standards, thousands of complaints related to unfair trading practices in the motor industry are recorded annually, highlighting the prevalence of misrepresentation. This trust deficit forces buyers to invest time and money in independent inspections and history checks, adding friction to the purchasing process. Many consumers remain wary of dealership warranties, fearing complex claim procedures or exclusions that leave them unprotected. The variability in vehicle quality makes it difficult for buyers to assess true value, leading to negotiation delays or abandoned purchases. Negative experiences shared through online reviews and social media amplify these concerns, influencing broader market sentiment. The absence of a unified digital record for all vehicles exacerbates the problem, as gaps in service history raise red flags for cautious buyers. This skepticism limits market liquidity, as sellers struggle to convince buyers of their vehicle’s integrity without third party verification. Transaction volumes will remain suppressed due to a persistent trust barrier stemming from a lack of transparency and standardization. Consequently, overall market growth will continue to be constrained, particularly within the private seller segment.

MARKET OPPORTUNITIES

Expansion Of Electric Vehicle Charging Infrastructure Creates Opportunities For Used EVs

The rapid expansion of electric vehicle charging infrastructure across the country is a key growth area for the United Kingdom used car market. This enhances the practicality and appeal of pre-owned EVs. As public charging networks grow in density and reliability, range anxiety diminishes, making used electric cars a viable option for a broader demographic. According to Zap Map, the number of public charging devices in the UK has increased substantially, with thousands of new points installed annually, supporting greater adoption. This infrastructure development improves the residual value proposition of used electric vehicles, encouraging more owners to trade in and buy within the secondary market. Government incentives for home charger installations further reduce ownership barriers, making used EVs more accessible to households without off street parking. The growing awareness of environmental benefits and lower running costs attracts cost conscious buyers to the used electric segment. Dealerships are capitalizing on this trend by certifying pre owned electric vehicles and offering specialized training for staff to address buyer queries. The maturation of battery technology also assures buyers of longevity, reducing fears about replacement costs. As the initial wave of electric leases expires, a surge in high quality used electric inventory will enter the market, meeting rising demand. This alignment of infrastructure readiness and inventory availability creates a fertile ground for growth in the used electric vehicle segment.

Digital Platform Integration And Data Transparency Enhance Buyer Confidence

The integration of advanced digital platforms and enhanced data transparency offers a substantial opportunity for the United Kingdom used cars market. This streamlines transactions and builds consumer confidence. Online marketplaces now provide comprehensive vehicle history reports, valuation tools, and virtual tours, allowing buyers to make informed decisions remotely. According to research, digital retailing tools have increased engagement and conversion rates by reducing information asymmetry between sellers and buyers. The use of artificial intelligence for accurate pricing ensures fair market values, minimizing negotiation friction and speeding up sales cycles. Mobile applications enable seamless scheduling of test drives and financing applications, enhancing convenience for time poor consumers. Blockchain technology is being explored for immutable vehicle records, promising to eliminate fraud and verify maintenance history securely. These digital innovations attract younger demographics who prefer online interactions and expect seamless user experiences. Retailers leveraging these technologies gain competitive advantages through improved operational efficiency and customer satisfaction. The ability to reach national audiences rather than just local buyers expands market reach for sellers, increasing liquidity. As digital literacy grows, the acceptance of online used car purchases will rise, unlocking new revenue streams. This technological evolution transforms the traditional used car buying experience into a modern, transparent, and efficient process, driving market expansion.

MARKET CHALLENGES

Volatility In Residual Values Complicates Inventory Management And Pricing

Volatility in residual values is a major challenge for the United Kingdom used cars market. This complicates inventory management and pricing strategies for dealers and financiers. Fluctuations in fuel prices, regulatory changes, and shifts in consumer preference cause unpredictable swings in vehicle worth, making it difficult to forecast profitability. According to automotive valuation experts, sudden drops in demand for diesel vehicles following policy announcements led to significant write downs for holders of such stock. This unpredictability increases financial risk for lenders and leasing companies, who may tighten credit criteria or reduce loan to value ratios, impacting affordability for buyers. Dealers face difficulties in setting competitive yet profitable prices, often holding inventory longer than anticipated to avoid selling at a loss. The rapid evolution of electric vehicle technology further exacerbates this challenge, as advancements in battery range and cost can quickly render older models less desirable. Economic uncertainty adds another layer of complexity, as consumer spending power fluctuates, affecting demand elasticity. Managing this volatility requires sophisticated data analytics and agile procurement strategies, which smaller players may lack. The risk of holding depreciating assets discourages investment in diverse inventory, potentially limiting consumer choice. This financial instability threatens the sustainability of business models reliant on stable residual values, requiring constant adaptation to mitigate losses.

Fraudulent Activities and Identity Theft Undermine Market Integrity

The prevalence of fraudulent activities and identity theft further slows down the growth of the United Kingdom used car market. This undermines trust and imposes significant costs on legitimate participants. Criminals employ sophisticated methods such as cloning vehicle identification numbers, forging documents, and using stolen identities to sell nonexistent or stolen vehicles. According to the National Fraud Intelligence Bureau, motor vehicle fraud remains a high volume crime, causing substantial financial losses to individuals and insurers. These illicit activities erode consumer confidence, making buyers overly cautious and slowing down legitimate transactions. Victims of fraud face lengthy legal battles and financial hardship, creating negative publicity for the entire sector. Dealerships incur higher insurance premiums and invest heavily in verification processes to protect themselves, increasing operational costs. The anonymity of online platforms facilitates these crimes, as scammers exploit weak verification systems to reach unsuspecting victims. Law enforcement efforts are often hampered by cross border complexities and resource constraints, limiting effective prosecution. The lack of a centralized real time database for vehicle status allows fraudulent listings to persist until reported. This persistent threat requires continuous vigilance and collaboration between industry stakeholders, technology providers, and authorities. Fraud will continue to distort market dynamics and deter participation if the industry lacks robust countermeasures. Left unchecked, this threatens the growth and overall integrity of the used car ecosystem.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 12.25% |

| Segments Covered | By Vendor, Vehicle Age, Fuel Type, Body Type, Sales Channel, Ownership, Price Brand, Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

| Regions Covered | London, South East, North West, East of England, South West, Scotland, West Midlands, Yorkshire and The Humber, East Midlands, Others |

| Market Leaders Profiled | Auto Trader Group plc, Constellation Automotive Group Ltd, Arnold Clark Automobiles Ltd, Cazoo Group Ltd, Car Giant Ltd, Lookers plc, Pendragon plc (CarStore), Vertu Motors plc, Motorpoint Group plc, Manheim (Cox Automotive U.K.), Sytner Group Ltd, Inchcape plc, TrustFord (Ford Retail Ltd), Jardine Motors Group U.K. Ltd, AvailableCar Ltd, Carwow Ltd, Motors.co.uk Ltd, Aramis Group, Peter Vardy Ltd |

SEGMENTAL ANALYSIS

By Vendor Insights

Oganized Sector

The organized segment dominated the United Kingdom used cars market and accounted for a 58.8% share in 2025. Consumer trust and strict adherence to regulatory standards are driving the dominance of this segment. Buyers increasingly prefer dealerships and established platforms that offer verified vehicle histories, warranties, and after sales support, which mitigate the risks associated with private purchases. According to the Motor Ombudsman, a significant majority of consumers express higher confidence in buying from accredited dealers who comply with the Code of Practice for Used Cars. This trust is reinforced by legal protections such as the Consumer Rights Act 2015, which mandates that vehicles must be of satisfactory quality and fit for purpose, providing buyers with recourse if issues arise. Organized vendors invest heavily in reconditioning processes, ensuring that vehicles meet high mechanical and aesthetic standards before sale. The availability of flexible finance options through partnerships with financial institutions further attracts customers who seek manageable payment plans. Additionally, organized players leverage data analytics to price vehicles competitively and transparently, reducing negotiation friction. The professionalization of the sales process, including digital documentation and home delivery services, enhances convenience and appeals to modern consumers. This segment benefits from economies of scale, allowing for better inventory management and marketing reach. As consumers prioritize reliability and peace of mind over lowest possible price, the organized sector continues to dominate, capturing the largest share of transaction value and volume in the UK market.

Buyers gain significant value from the organized sector's exclusive certified pre-owned programs and comprehensive warranties, which further cement its market dominance. Major manufacturers and large dealership groups offer certified pre owned vehicles that undergo rigorous multi point inspections and come with extended warranties, bridging the gap between new and used car ownership. According to sources, certified pre owned vehicles command premium prices yet sell faster due to perceived reliability and manufacturer backing. These programs often include additional benefits such as roadside assistance, service packages, and return policies, which are rarely available in the unorganized sector. The presence of warranties reduces the total cost of ownership risk, making used cars a more attractive financial decision for families and business users. Organized vendors also provide trade in facilities, simplifying the upgrade process for existing owners and ensuring a steady flow of quality inventory. The ability to offer seamless integration with insurance and maintenance services creates a holistic ownership experience that fosters loyalty. Retailers use these value added services to differentiate themselves in a competitive landscape, justifying higher margins. The structured nature of these offerings appeals to risk averse consumers who view car buying as a significant investment. This strategic advantage ensures that the organized sector remains the preferred choice for discerning buyers, solidifying its leadership in the UK used cars market.

Unorganized Sector

The unorganized segment is expected to exhibit a noteworthy CAGR of 4.5% from 2026 to 2034 due to the rise of digital peer to peer platforms. Online marketplaces have democratized access to buyers and sellers, removing traditional barriers and enabling direct transactions without intermediary fees. According to data from major online classifieds platforms, private listings have seen a substantial increase in engagement, as sellers seek to maximize returns by avoiding dealer margins. These platforms offer user friendly interfaces, secure messaging, and integrated valuation tools that simplify the selling process for individuals. The convenience of listing vehicles from home and reaching a national audience has attracted a younger demographic of sellers who are comfortable with digital transactions. Buyers are drawn to the potential for lower prices and the ability to negotiate directly with owners. Social media groups and community forums further facilitate these connections, creating niche markets for specific vehicle types. The transparency provided by user reviews and rating systems helps build trust between strangers, mitigating some traditional risks. As smartphone penetration increases and digital literacy improves, more consumers are opting for this streamlined approach. The flexibility and cost effectiveness of peer to peer trading ensure that the unorganized sector continues to expand, capturing a growing share of the market despite the dominance of organized players.

The accelerated growth of the unorganized sector is also driven by economic pressure that pushes consumers toward lower cost private transactions to save money. In a challenging economic environment, both buyers and sellers are motivated to avoid the overhead costs associated with dealerships, such as preparation fees and administrative charges. According to the Office for National Statistics, ongoing household budget constraints have restricted discretionary consumer spending, a pressure that automotive market analysts state has pushed many buyers toward the unorganized private sales market for affordable mobility solutions. Sellers can offer vehicles at lower prices than dealers while still achieving a satisfactory return, creating a win win scenario for both parties. The absence of value added tax on private sales further reduces the final cost for buyers, enhancing affordability. This segment benefits from the large volume of older vehicles that may not meet the stringent criteria for certified pre owned programs but remain reliable for daily use. Community based trust and local knowledge often play a role in these transactions, particularly in rural areas where dealership access is limited. The flexibility in payment terms and negotiation allows for personalized agreements that suit individual financial situations. As economic uncertainty persists, the appeal of cost saving private transactions will continue to drive the growth of the unorganized sector, making it the fastest expanding segment in the UK used cars market.

By Vehicle Age Insights

3-5 Years

The 3 to 5 years age segment led the United Kingdom used cars market and captured a 34.3% share in 2025. This leading position of the segment was attributed to its optimal balance of value depreciation and mechanical reliability. Vehicles in this age bracket have already absorbed the steepest initial depreciation curve, offering significant savings compared to new models while still retaining modern features and safety technologies. According to automotive valuation experts, cars aged 3 to 5 years typically retain around 50 to 60 percent of their original value, making them financially attractive to a broad range of buyers. This segment benefits from the expiration of standard manufacturer leases, which floods the market with well maintained single owner vehicles with documented service histories. Buyers perceive these cars as low risk because they are likely to have remaining factory warranty coverage or are eligible for extended warranty packages. The technology in these vehicles, such as infotainment systems and driver assistance features, remains relevant and functional, satisfying consumer expectations for connectivity and comfort. Fleet operators and leasing companies regularly refresh their inventories, ensuring a consistent supply of high quality stock in this age range. The availability of diverse models and specifications allows buyers to find vehicles that precisely match their needs without compromising on quality. This sweet spot in the lifecycle of a vehicle ensures that the 3 to 5 years segment commands the highest transaction volumes, serving as the backbone of the UK used cars market.

The top position of the 3 to 5 years segment is further reinforced by high demand from first time buyers and families looking to upgrade their vehicles within reasonable budgets. This demographic seeks reliable transportation that does not require immediate major repairs or investments, which characterizes vehicles in this age group. According to survey data from consumer finance providers, a majority of first time car buyers prioritize affordability and low running costs, making 3 to 5 year old cars the ideal entry point into ownership. Families appreciate the enhanced safety features and spaciousness available in newer used models, which are often out of reach in the new car market due to price constraints. The predictability of maintenance costs for vehicles in this age bracket provides financial security, as major components are less likely to fail compared to older cars. Insurance premiums for this segment are generally moderate, balancing coverage costs with vehicle value. The wide availability of finance products tailored for this age group facilitates easier acquisition, with lenders viewing these assets as stable collateral. Retailers focus their marketing efforts on this segment, highlighting the value proposition and peace of mind it offers. The alignment of consumer needs with the attributes of 3 to 5 year old vehicles ensures sustained dominance, making it the most popular choice for practical and economical mobility in the UK.

0-2 Years

The 0 to 2 years age segment is predicted to witness the highest CAGR of 5.8% during the forecast period owing to consumer desire for near new condition vehicles with full warranty coverage. Buyers in this segment seek to avoid the initial depreciation hit of new cars while enjoying the benefits of modern technology and pristine mechanical state. According to sources, the availability of ex demonstration and short term lease vehicles has increased, providing a steady stream of high quality inventory. These vehicles often come with remaining manufacturer warranties, offering the same peace of mind as new car purchases at a reduced price. The appeal is particularly strong among tech savvy consumers who want the latest connectivity and safety features without the premium price tag. Corporate fleet renewals contribute significantly to this supply, as businesses upgrade vehicles frequently to maintain image and efficiency. The perception of these cars as virtually new reduces the psychological barrier to buying used, attracting buyers who might otherwise consider new vehicles. Finance companies promote this segment aggressively, offering competitive rates that mirror new car deals. The minimal wear and tear associated with such young vehicles ensures lower immediate maintenance costs, enhancing total cost of ownership appeal. This combination of novelty, security, and value drives rapid adoption, making the 0 to 2 years segment the fastest expanding category in the UK used cars market.

The swift expansion of the 0 to 2 years segment is also fueled by ongoing supply chain constraints in the new car market, which limit availability and extend delivery times for brand new vehicles. According to the Society of Motor Manufacturers and Traders, delays in new car production have prompted many consumers to turn to nearly new used cars as a viable alternative. Buyers unwilling to wait months for a new order find that 0 to 2 year old vehicles offer immediate availability with minimal compromise on specification or condition. This substitution effect has strengthened demand for young used cars, driving up their residual values and transaction volumes. Dealerships capitalize on this trend by marketing nearly new stock as a smart alternative to waiting lists, emphasizing the immediate benefit of ownership. The scarcity of new cars has also reduced the incentive for buyers to wait for the latest model year, as the difference in features between current and recent models is often marginal. This shift in consumer behavior has created a robust market for young used vehicles, supported by strong residual values that protect buyer investment. As supply chain issues persist, the appeal of immediate gratification through nearly new purchases will continue to drive the rapid growth of this segment, establishing it as a key growth engine in the UK used cars landscape.

By Sales Channel Insights

Offline

The offline sales channels segment held the majority share of the United Kingdom used cars market in 2025 because of the consumer need for tactile inspection and immediate possession of vehicles. Buying a car is a significant financial decision, and many buyers prefer to physically examine the vehicle, test drive it, and assess its condition firsthand before committing. According to the British Retail Consortium, a substantial majority of used car transactions still conclude in physical dealerships, where trust is built through face to face interaction. The ability to negotiate in person and receive immediate handover of keys and documents appeals to buyers who value certainty and speed. Dealerships offer professional environments where staff can address concerns, explain features, and arrange finance on the spot, creating a seamless experience. The presence of service centers and parts departments at dealership locations provides added convenience for future maintenance, reinforcing customer loyalty. Physical showrooms allow for the display of multiple vehicles, enabling comparative shopping and impulse decisions based on visual appeal. For many consumers, especially older demographics, the traditional dealership model remains the most trusted and familiar method of purchase. The tangible nature of the product makes offline channels indispensable, ensuring they retain the largest share of the market despite digital advancements. This preference for physical verification and personal service sustains the dominance of offline sales in the UK used cars sector.

Strong dealer networks and grassroots trust keep offline channels ahead of the curve, advantages digital platforms simply cannot copy. Local dealerships often have long standing relationships with customers, built on reputation and repeat business over many years. According to studies, consumers frequently recommend dealers based on personal experiences and word of mouth, which drives foot traffic and sales. These dealers understand local market dynamics and customer preferences, allowing them to curate inventory that meets specific regional demands. The physical presence of a dealership provides a sense of accountability and recourse for buyers, who know where to go if issues arise post purchase. Community engagement through local events and sponsorships enhances brand visibility and goodwill. Offline channels also benefit from trade in opportunities, where customers can exchange their old vehicles for new ones in a single visit, simplifying the transaction process. The expertise of sales staff in assessing vehicle condition and explaining technical details adds value that automated systems cannot fully replace. This human element fosters confidence and reduces anxiety associated with large purchases. As long as trust and personal interaction remain critical factors in car buying, offline channels will maintain their leading position in the UK used cars market, serving as the primary touchpoint for most consumers.

Online

The online sales channel segment is estimated to register the fastest CAGR of 7.2% between 2026 and 2034. This rapid growth of the segment is propelled by unparalleled convenience and access to expanded inventory. Digital platforms allow buyers to browse thousands of vehicles from the comfort of their homes, filtering by price, mileage, and specifications to find exact matches quickly. According to the Office for National Statistics, e commerce adoption in retail has surged, with used cars benefiting from improved digital tools and logistics. Online marketplaces offer transparent pricing, detailed vehicle history reports, and high resolution images, reducing information asymmetry and building confidence. The ability to compare multiple options side by side saves time and effort, appealing to busy professionals and younger buyers. Home delivery services and contactless handover options have further enhanced the appeal of online purchases, eliminating the need for dealership visits. Virtual tours and video calls enable remote inspections, addressing some limitations of digital buying. The breadth of inventory available online exceeds any single physical dealership, giving buyers access to rare or specific models that may not be available locally. This extensive choice and ease of access drive rapid adoption, making online channels the preferred method for an increasing number of UK car buyers.

The accelerated growth of the online segment is also fueled by advanced data analytics and personalized user experiences that enhance decision making and engagement. Digital platforms utilize algorithms to recommend vehicles based on browsing history and preferences, creating a tailored shopping journey that increases conversion rates. According to sources, personalized recommendations significantly improve user satisfaction and reduce search time, encouraging repeat visits and purchases. Online retailers offer instant valuation tools for trade ins, providing immediate feedback and streamlining the selling process. Integrated finance calculators and approval systems allow buyers to secure funding seamlessly within the platform, reducing friction. Customer reviews and ratings provide social proof, helping buyers assess dealer reliability and vehicle quality. Mobile apps enable notifications for price drops or new listings, keeping users engaged and informed. The use of artificial intelligence for fraud detection and verification enhances trust in online transactions. These technological advantages create a superior user experience that traditional offline methods cannot match in terms of efficiency and customization. As digital literacy grows and technology improves, the online segment will continue to expand rapidly, capturing a larger share of the UK used cars market through innovation and convenience.

COUNTRY ANALYSIS

United Kingdom Used Car Market Analysis

The United Kingdom is currently the second-largest used car market in Europe and captured a 15.2% share in 2025. This growth of the UK market was driven by a robust secondary vehicle trade and sophisticated consumer preferences. As a distinct entity post Brexit, the UK has established independent regulatory frameworks that influence vehicle standards and trade dynamics. According to the Department for Transport, the UK has over 30 million licensed cars facilitating a vibrant used car ecosystem, despite having a lower density of vehicle ownership per capita than the European average. The market status is resilient, supported by a strong culture of vehicle turnover and a well established infrastructure for inspections and financing. Consumers in the UK are discerning and well informed, demanding high levels of transparency and quality from sellers. The retail landscape is a mix of large franchise dealerships, independent specialists, and growing online platforms, offering diverse choices to buyers. Regulatory bodies enforce strict safety and emissions standards, ensuring that only compliant vehicles circulate in the market. The country’s advanced digital infrastructure supports the rapid growth of online sales channels, making it a leader in digital automotive retailing in Europe. Cultural factors, such as the importance of personal mobility and status associated with vehicle ownership, drive consistent demand. The UK serves as a benchmark for best practices in consumer protection and vehicle certification, influencing trends in neighboring markets. This combination of regulatory rigor, technological adoption, and consumer sophistication ensures that the United Kingdom remains a pivotal and dynamic hub for the used car industry in Europe.

The United Kingdom used cars market is driven by several key factors, including economic pragmatism, regulatory changes, and technological advancement. According to the Office for National Statistics, economic pressures have increased the appeal of used cars as a cost effective alternative to new vehicles, sustaining high transaction volumes. The implementation of clean air zones and emissions regulations has shifted demand toward newer, cleaner used vehicles, accelerating the turnover of older stock. The expansion of electric vehicle charging infrastructure supports the growing segment of used electric cars, encouraging adoption among environmentally conscious buyers. Digital transformation has streamlined the buying process, with online platforms offering greater transparency and convenience, attracting younger demographics. The presence of strong consumer protection laws builds trust, encouraging participation in the formal market. Fleet renewal cycles contribute significantly to supply, ensuring a steady flow of well maintained vehicles into the secondary market. Finance availability plays a crucial role, with competitive lending rates making used cars accessible to a wider audience. The cultural emphasis on mobility and independence drives consistent demand across various demographic groups. These dynamics create a complex but vibrant market environment where adaptability and innovation are key to success. The UK’s proactive approach to sustainability and digital integration positions it at the forefront of automotive retail evolution, ensuring continued relevance and growth in the European context.

COMPETITIVE LANDSCAPE

The competition in the United Kingdom used cars market is intense and characterized by a mix of large national retailers, independent dealerships, and growing online platforms. Major players compete on price, quality assurance, and customer service excellence to capture market share. National chains leverage economies of scale to offer competitive pricing and extensive warranties, attracting risk averse buyers. Independent dealers often differentiate themselves through specialized knowledge and personalized service, catering to niche segments. Online platforms have disrupted traditional models by offering greater transparency and convenience, forcing physical dealers to adopt digital tools. The rise of certified pre owned programs has raised industry standards, compelling all participants to improve vehicle quality and inspection processes. Regulatory pressures regarding emissions and consumer protection further shape competitive dynamics, favoring compliant and transparent operators. Price volatility and supply chain constraints add complexity, requiring agile inventory management strategies. Trust remains a critical factor, with reputation and reviews influencing buyer decisions significantly. The market rewards innovation and adaptability, as companies must continuously evolve to meet changing consumer expectations and technological advancements. This dynamic environment ensures that only those who prioritize customer value and operational efficiency thrive in the long term.

KEY MARKET PLAYERS

A Few of the most dominant market players that are in the UK used cars market are

- Auto Trader Group plc

- Constellation Automotive Group Ltd

- Arnold Clark Automobiles Ltd

- Cazoo Group Ltd

- Car Giant Ltd

- Lookers plc

- Pendragon plc (CarStore)

- Vertu Motors plc

- Motorpoint Group plc

- Manheim (Cox Automotive U.K.)

- Sytner Group Ltd

- Inchcape plc

- TrustFord (Ford Retail Ltd)

- Jardine Motors Group U.K. Ltd

- AvailableCar Ltd

- Carwow Ltd

- Motors.co.uk Ltd

- Aramis Group

- Peter Vardy Ltd

Top Players In The Market

- Arnold Clark Automobiles stands as a prominent family owned retailer with an extensive network of dealerships across the United Kingdom. The company contributes significantly by offering a wide variety of new and used vehicles alongside comprehensive after sales services. Recent actions include substantial investments in digital infrastructure to enhance online browsing and purchasing experiences for customers. Arnold Clark has also expanded its electric vehicle offerings to align with environmental regulations and consumer demand. The company strengthens its position through rigorous quality checks and transparent pricing models that build consumer trust. Its commitment to customer service excellence and community engagement fosters long term loyalty among buyers. By integrating advanced technology into its operations, Arnold Clark ensures efficient inventory management and personalized customer interactions. These strategic initiatives enable the company to maintain a competitive edge and adapt to evolving market dynamics while delivering value to stakeholders.

- Pendragon PLC operates as a leading automotive retailer managing numerous franchises and independent dealerships throughout the United Kingdom. The company plays a vital role in the used car sector by providing certified pre owned vehicles with robust warranty packages. Recent strategies involve optimizing its dealership footprint to focus on high performance locations and improving operational efficiency. Pendragon has invested heavily in digital platforms to streamline the sales process and offer seamless omnichannel experiences. The company emphasizes staff training to ensure high standards of customer care and technical expertise. By leveraging data analytics, Pendragon enhances inventory selection and pricing accuracy to meet consumer preferences. Its focus on sustainability includes promoting electric and hybrid vehicles within its used stock. These efforts help Pendragon strengthen its market presence by delivering reliable and convenient automotive solutions to a diverse customer base across the region.

- Lookers PLC is a major automotive retailer with a strong presence in the United Kingdom through its extensive dealership network. The company contributes to the market by offering a broad selection of used cars backed by thorough inspection processes. Recent actions include the adoption of digital retailing tools that allow customers to view and purchase vehicles online with ease. Lookers has focused on enhancing its customer journey through improved website functionality and virtual consultation services. The company actively promotes sustainable practices by increasing the availability of low emission vehicles in its inventory. Strategic partnerships with manufacturers ensure access to high quality trade in vehicles. Lookers prioritizes transparency and trust by providing detailed vehicle history reports to buyers. These initiatives enable the company to attract discerning customers and maintain a reputable brand image in the competitive UK automotive landscape.

Top Strategies Used By Key Market Participants

Key players in the United Kingdom used cars market employ several strategic approaches to maintain competitiveness and drive growth. Digital transformation is central, with companies investing in online platforms that offer virtual tours and seamless purchasing experiences. Certification programs are widely used to build trust, ensuring vehicles meet strict quality and safety standards before sale. Omnichannel integration allows customers to switch between online research and offline purchases effortlessly, enhancing convenience. Sustainable practices are increasingly adopted, with retailers expanding their electric and hybrid vehicle inventories to meet regulatory demands. Customer experience enhancement through personalized service and transparent pricing helps differentiate brands in a crowded market. Strategic partnerships with finance providers offer flexible payment options, making vehicles more accessible to a broader demographic. Data analytics are utilized to optimize inventory management and predict consumer trends accurately. These combined strategies enable key participants to navigate market challenges and capitalize on emerging opportunities effectively.

MARKET SEGMENTATION

This research report on the UK used cars market is segmented and sub-segmented into the following categories.

By Vendor Type

- Organized

- Unorganized

By Vehicle Age

- 0 - 2 Years

- 3 - 5 Years

- 6 - 8 Years

- More than 8 Years

By Fuel Type

- Petrol

- Diesel

- Hybrid

- Battery Electric

- Plug-in Hybrid

- Other Alt-Fuels (CNG/LPG)

By Body Type

- Hatchback

- Sedan

- Sport Utility Vehicle (SUV)

- Multi-Purpose Vehicle (MPV)

By Sales Channel

- Online

- Offline - Franchised Dealers

- Offline - Independent Dealers

- Private-to-Private

By Ownership Type

- First-Owner

- Second-Owner

- Third-or-More Owners

By Price Band

- Less than USD 7,000

- USD 7,001 - USD 15,000

- USD 15,000 - USD 30,000

- More than 30,000

Frequently Asked Questions

What is driving demand in the UK used cars market?

Affordability concerns, a wide selection of vehicles, and increasing consumer preference for cost-effective transportation are driving demand.

How is the UK used cars market categorized by vehicle type?

The market is categorized into hatchbacks, sedans, SUVs, pickup trucks, luxury vehicles, and electric used vehicles.

Which vehicle segment dominates the UK used cars market?

Hatchbacks and SUVs dominate the market due to their popularity, practicality, and broad consumer appeal.

Why are consumers choosing used cars instead of new vehicles in the UK?

Used cars offer lower purchase costs, reduced depreciation, and access to higher-specification models at competitive prices.

Who are the primary buyers in the UK used cars market?

Individual consumers, first-time car buyers, fleet operators, dealerships, and budget-conscious households are the primary buyers.

How are digital platforms transforming the used car buying experience?

Online marketplaces, virtual vehicle inspections, digital financing options, and home delivery services are transforming the buying experience.

What market trends are influencing the UK used cars industry?

Growth in certified pre-owned vehicles, increasing demand for used electric vehicles, and digital retailing are influencing the industry.

What challenges are affecting the UK used cars market?

Vehicle supply shortages, fluctuating resale values, financing constraints, and changing regulatory requirements can affect market growth.

How are dealerships strengthening their competitive advantage in the used cars market?

Dealerships are offering vehicle history reports, extended warranties, flexible financing, and online purchasing options.

What future opportunities are expected to shape the UK used cars market?

Rising demand for affordable mobility, expanding used EV inventories, and advancements in digital automotive retail are expected to create significant growth opportunities.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com