United Kingdom Video Games Market Size, Share, Trends & Growth Forecast Report Segmented By Device (Smartphones, PC/Laptop, Consoles ), Age Group, Platform Type and Country – Industry Analysis From 2026 to 2034

Market Size, 2025

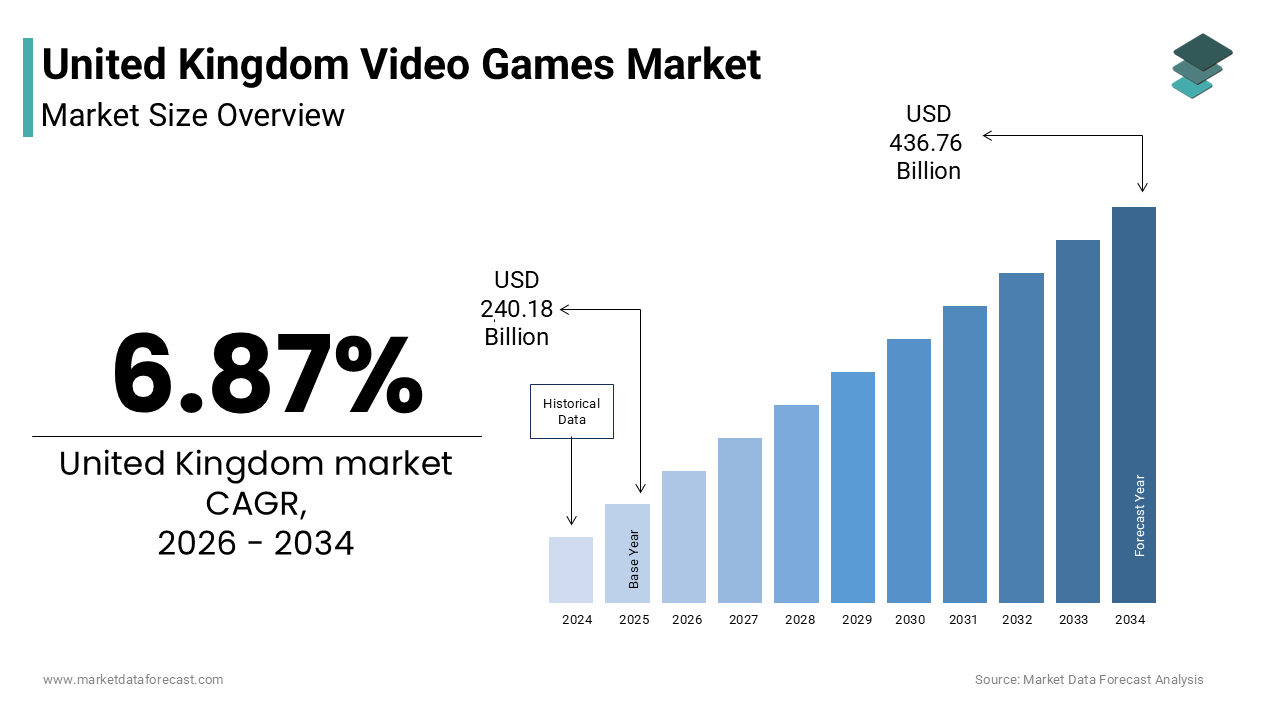

$240.18 BnMarket Estimate, 2026

$256.68 BnMarket Forecast, 2034

$436.76 BnCAGR, 2026–2034

6.87%United Kingdom Video Games Market Report Summary

The United Kingdom video games market was valued at USD 240.18 billion in 2025 and is anticipated to reach USD 256.68 billion in 2026 from USD 436.76 billion by 2034, growing at a CAGR of 6.87% during the forecast period from 2026 to 2034. The growth of the United Kingdom video games market is driven by increasing broadband connectivity, rising popularity of online multiplayer gaming, and growing consumer spending on digital entertainment. Expanding adoption of cloud gaming platforms, increasing engagement with esports and game streaming content, and growing demand for immersive gaming experiences are further accelerating market growth. Moreover, advancements in artificial intelligence-powered game development, expansion of subscription-based gaming services, and increasing integration of cross-platform gaming ecosystems are supporting the expansion of the United Kingdom video games market.

Key Market Trends

- Rising adoption of cloud gaming services enabling access to premium gaming experiences without high-end hardware requirements.

- Increasing integration of artificial intelligence technologies for game development, personalization, and player engagement.

- Growing popularity of esports tournaments and game streaming platforms among younger demographics.

- Strong focus on cross-platform gaming experiences that enhance accessibility and social connectivity.

- Expansion of subscription-based gaming models providing users with access to extensive game libraries.

Segmental Insights

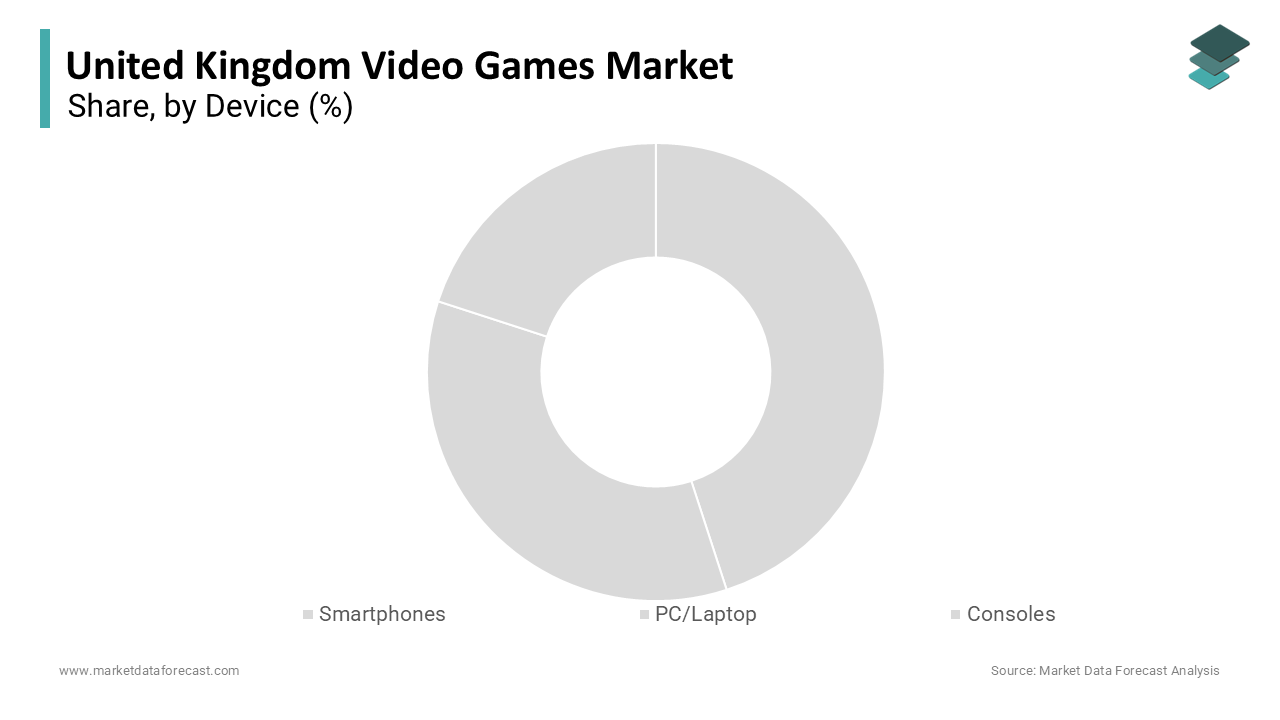

- Based on device, the console segment dominated the United Kingdom video games market and held the largest share in 2025. The segment’s dominance is attributed to exclusive game titles, optimized hardware performance, strong gaming communities, and extensive adoption of premium gaming consoles among dedicated gamers.

- The smartphone segment is projected to witness the fastest CAGR during the forecast period owing to widespread smartphone penetration, accessibility of free-to-play games, increasing mobile internet speeds, and growing popularity of casual gaming experiences.

- Based on age group, the Generation Y segment accounted for the leading share of the United Kingdom video games market in 2025. The dominance of this segment is driven by high disposable income, strong engagement with gaming culture, increasing participation in esports and streaming communities, and demand for premium gaming experiences.

- The Generation Z segment is anticipated to register the fastest CAGR during the forecast period due to its status as a digitally native population, increasing social interaction through gaming platforms, growing mobile gaming adoption, and rising engagement with online gaming communities.

- Based on platform type, the offline segment held the major share of the United Kingdom video games market in 2025 owing to strong demand for premium single-player experiences, ownership of physical game collections, reliable gameplay without internet dependency, and continued popularity of narrative-driven titles.

- The online segment is expected to witness rapid growth during the forecast period because of increasing adoption of multiplayer games, expansion of live-service gaming models, rising esports participation, and growing demand for social gaming experiences.

Regional Insights

The United Kingdom accounted for a significant share of the European video games market in 2025, supported by a strong gaming culture, advanced digital infrastructure, and a thriving game development ecosystem. The country benefits from widespread broadband connectivity, favorable government support for game development through tax incentives, and the presence of globally recognized gaming studios. Increasing adoption of cloud gaming, esports participation, and digital distribution platforms continues to strengthen the market’s growth trajectory across the United Kingdom.

Competitive Landscape

The United Kingdom video games market is highly competitive and characterized by the presence of global gaming publishers, console manufacturers, and innovative domestic game development studios competing through content innovation, technological advancements, and community engagement. Leading companies are focusing on expanding live-service gaming ecosystems, investing in artificial intelligence and cloud gaming technologies, strengthening esports initiatives, and enhancing cross-platform compatibility. Strategic partnerships with streaming platforms, telecom providers, and technology companies are further strengthening market positioning across the gaming value chain Prominent players in the United Kingdom video games market include Sony Interactive Entertainment, Microsoft Gaming, Nintendo Co., Ltd., Electronic Arts Inc., Ubisoft Entertainment SA, Activision Blizzard, Inc., Take-Two Interactive Software, Inc., Tencent Games, King Digital Entertainment plc, Frontier Developments plc, Jagex Ltd., Codemasters, Rebellion Developments Ltd., and Sumo Group plc

United Kingdom Video Games Market Size

The United Kingdom video games market size was valued at USD 240.18 billion in 2025 and is anticipated to reach USD 256.68 billion in 2026 from USD 436.76 billion by 2034, growing at a CAGR of 6.87% during the forecast period from 2026 to 2034.

A video game is an interactive digital game played by using an electronic input device to generate visual feedback on a screen. The United Kingdom holds a premier standing in the European video game ecosystem, primarily competing with Germany for the top spot. This market includes interactive software, hardware platforms, and associated services that engage millions of users across diverse demographics. The market is characterized by rapid technological evolution, where advancements in graphics processing, artificial intelligence, and network infrastructure continuously redefine user experiences. Consumer engagement is no longer limited to solitary play but extends into vibrant online communities, competitive esports arenas, and social virtual spaces. According to the Children's Commissioner for England (and corroborated by Ofcom media literacy reports), approximately 93% of children in the UK play video games, indicating deep penetration among younger generations. Furthermore, data from the Department for Culture, Media and Sport (DCMS) reveals that the Creative Industries, including gaming, contribute over £120 billion to the national economy and employ roughly 2.4 million skilled professionals. The regulatory environment focuses on age appropriate content and consumer protection, ensuring safe interactions for minors. Infrastructure developments such as widespread high speed broadband access facilitate seamless online multiplayer experiences and cloud gaming services. The industry also reflects broader societal trends toward digital literacy and interactive storytelling, influencing education and training sectors. This dynamic landscape requires stakeholders to navigate complex intellectual property rights, evolving monetization models, and shifting consumer preferences while maintaining innovation and ethical standards in product development and community management.

MARKET DRIVERS

Pervasive High Speed Broadband Infrastructure Facilitates Advanced Gaming Experiences

The extensive deployment of high speed broadband infrastructure across the country fuels the growth of the United Kingdom video games market. This is driven by enabling advanced online functionalities and cloud based services. Reliable and fast internet connectivity is essential for modern gaming experiences, including massive multiplayer online games, real time strategy competitions, and streaming services that require low latency and high bandwidth. According to Ofcom, the average fixed-line download speed in the UK has reached 223 Mbps, driven by rapid infrastructure deployment where full-fibre network coverage now expands across 20.7 million premises (69% of the country). This robust infrastructure allows developers to create more complex and data intensive games that rely on constant server communication and regular content updates. Gamers can participate in global tournaments without significant lag, enhancing the competitive integrity and appeal of esports titles. The availability of high speed connections also supports the growth of cloud gaming platforms, which stream high fidelity games directly to devices without requiring expensive local hardware. This accessibility broadens the potential user base, allowing individuals with modest computing resources to enjoy premium gaming experiences. Furthermore, reliable internet facilitates social interaction within games, fostering communities that retain users through shared experiences and collaborative play. The continuous improvement of network capabilities ensures that the UK remains at the forefront of digital entertainment adoption, encouraging investment from international publishers and supporting the domestic development of online focused titles.

Growing Acceptance of Gaming as a Legitimate Social and Professional Pursuit

The increasing societal acceptance of interactive digital gaming as a legitimate social activity and professional career path significantly propels the expansion of the United Kingdom video games market. Gaming is no longer viewed merely as a childish pastime but as a mainstream form of entertainment and socialization for adults and young people alike. According to data cited by UKIE and European trade bodies, the average age of a video game player in the region sits between 31 and 35 years old, challenging traditional stereotypes and demonstrating broad demographic appeal across generations. This shift in perception encourages greater participation across all age groups, leading to higher spending on games, hardware, and accessories. The rise of esports has further legitimized gaming, with professional players attracting substantial sponsorships and media coverage, inspiring aspiring gamers to invest in high performance equipment. Educational institutions increasingly recognize the value of gaming skills, such as strategic thinking and teamwork, integrating them into curricula and extracurricular activities. Social platforms within games provide virtual spaces for friends to connect, particularly important during periods of physical distancing. This social dimension transforms gaming into a communal experience, driving retention and recurring revenue through microtransactions and season passes. The destigmatization of gaming also attracts diverse talent to the development sector, fostering innovation and inclusive content creation. Gaming is increasingly embedded in daily social routines. Thus, the demand for diverse and engaging titles continues to grow, which sustains market momentum.

MARKET RESTRAINTS

Stringent Regulatory Scrutiny On Loot Boxes And Microtransactions Limits Monetization

Intensifying regulatory scrutiny regarding loot boxes and other microtransaction mechanisms is impeding the growth of the United Kingdom video games market. This forces developers to rethink revenue models. Loot boxes, which offer random virtual items for purchase, have drawn criticism for resembling gambling practices, particularly concerning their impact on minors. According to the Department for Culture, Media and Sport (DCMS), extensive government consultations regarding loot boxes and microtransactions have created ongoing regulatory uncertainty for publishers, as compliance standards tighten to protect younger players from in-game spending risks. Potential legislation could mandate age restrictions, probability disclosures, or outright bans, complicating game design and reducing profitability. Developers face increased compliance costs and legal risks, prompting some to remove or modify these features preemptively. This regulatory pressure may lead to higher upfront prices for games to compensate for lost recurring revenue, potentially deterring price sensitive consumers. The ambiguity surrounding future regulations hinders long term planning and investment in live service games that depend on continuous monetization. Industry stakeholders argue that responsible self regulation is preferable to strict laws, but public and political pressure continues to mount. The need to balance commercial interests with consumer protection creates a challenging environment for innovation in business models. Companies must navigate this complex landscape carefully to avoid reputational damage and legal penalties while maintaining financial viability.

Hardware Supply Chain Volatility And Component Shortages Constrain Access

Persistent volatility in hardware supply chains and component shortages is also a major obstacle to the United Kingdom video games market. This ongoing disruption severely limits consumer access to next-generation consoles and high-end PCs. The global semiconductor crisis and logistical disruptions have affected the production of graphics processing units and console systems, leading to stock shortages and inflated prices. According to sources, demand for gaming hardware often outstrips supply during peak periods, frustrating consumers and delaying upgrades. This scarcity restricts the ability of players to experience new titles optimized for latest generation hardware, slowing the adoption of advanced features such as ray tracing and higher frame rates. Retailers struggle to manage inventory levels, resulting in missed sales opportunities and customer dissatisfaction. The high cost of scarce components also increases the price of pre built gaming PCs, making them less accessible to budget conscious buyers. Developers face challenges in optimizing games for a fragmented hardware base, as not all users possess the latest technology. This fragmentation complicates quality assurance and support efforts, increasing development costs. The uncertainty surrounding supply chain stability discourages aggressive marketing campaigns for hardware dependent titles. Production capacities and logistics are currently in a stabilization phase. Until these normalize, the hardware market will continue to face constraints that limit growth potential and consumer satisfaction.

MARKET OPPORTUNITIES

Expansion Into Cloud Gaming Services Offers New Revenue Streams

The expansion of cloud gaming services offers a major opportunity for the United Kingdom video games market. This growth lowers entry barriers while creating new subscription-based revenue streams. Cloud gaming allows users to stream high quality games directly to various devices, eliminating the need for expensive dedicated hardware. According to data from major technology firms, interest in cloud gaming is rising as internet speeds improve and latency issues decrease. This model appeals to casual gamers and those unwilling to invest in costly consoles or PCs, expanding the total addressable market. Publishers can reach wider audiences by offering games through subscription platforms, generating recurring income rather than relying solely on one time purchases. The flexibility of playing across multiple devices enhances convenience and engagement, encouraging longer play sessions. Partnerships between telecom providers and gaming companies can bundle services, increasing adoption rates. Cloud infrastructure also enables instant access to large libraries of games, reducing decision fatigue for consumers. This shift supports the trend toward service based models in the entertainment industry, aligning with consumer preferences for access over ownership. Cloud gaming is poised to become a standard option as technology matures. Consequently, this shift will drive significant growth and innovation in content delivery and user experience design.

Integration Of Artificial Intelligence Enhances Personalization And Development Efficiency

The integration of artificial intelligence into game development and gameplay paves the way for innovation and efficiency in the United Kingdom video games market. AI technologies enable the creation of more realistic non player characters, dynamic environments, and personalized user experiences that adapt to individual playing styles. According to research, AI tools are increasingly used to automate routine coding tasks, accelerate asset creation, and optimize testing processes, reducing development time and costs. This efficiency allows studios to produce higher quality content more frequently, keeping players engaged with fresh updates and expansions. Personalized recommendations driven by AI algorithms help users discover new games tailored to their preferences, increasing conversion rates and satisfaction. Adaptive difficulty systems ensure that games remain challenging yet accessible, broadening their appeal to diverse skill levels. AI also enhances anti cheat measures and moderation in online communities, improving safety and fairness. The use of generative AI for narrative elements and dialogue creates richer storytelling possibilities, immersing players deeper into game worlds. As AI capabilities advance, developers can experiment with novel gameplay mechanics and interactive features that were previously impractical. This technological leap positions UK studios at the forefront of innovation, attracting investment and talent while delivering superior products to global audiences.

MARKET CHALLENGES

Talent Retention And Skills Gap In Specialized Technical Roles

The shortage of specialized technical talent and difficulties in retention are holding back the growth of the United Kingdom video games market. This hinders innovation. The market requires highly skilled professionals in areas such as programming, art design, and data science, but competition for these roles is intense. According to surveys by industry bodies, many studios report difficulties in finding candidates with the necessary expertise in emerging technologies like virtual reality and machine learning. High turnover rates exacerbate the problem, as experienced developers often move to larger companies or different sectors offering better compensation and work life balance. This instability disrupts project timelines and increases recruitment costs, straining resources especially for smaller independent studios. The lack of diverse talent pools limits creative perspectives and inclusivity in game development. Educational institutions sometimes struggle to keep curricula aligned with rapid industry changes, resulting in graduates who require extensive additional training. Remote work trends have expanded the talent pool globally but also increased competition for UK based workers. Addressing this challenge requires coordinated efforts between industry, academia, and government to promote careers in gaming and provide targeted training programs. The UK games market requires a stable and skilled workforce. Without this foundation, the country risks losing its edge globally.

Cybersecurity Threats And Data Privacy Concerns Undermine User Trust

Escalating cybersecurity threats and data privacy concerns are a critical challenge to the United Kingdom video games market. This threatens user trust and operational integrity. Online games collect vast amounts of personal data, making them attractive targets for hackers seeking to steal identities, financial information, or disrupt services. According to cybersecurity agencies, gaming platforms frequently face distributed denial of service attacks, account takeovers, and malware distribution attempts. These incidents can lead to significant financial losses, legal liabilities, and reputational damage for companies. Players are becoming more aware of privacy risks, demanding greater transparency and control over their data. Compliance with stringent regulations such as the General Data Protection Regulation requires robust security measures and administrative oversight, increasing operational costs. Breaches can result in heavy fines and loss of consumer confidence, impacting long term viability. The complexity of securing interconnected online ecosystems makes it difficult to guarantee absolute safety, leaving vulnerabilities exploitable by sophisticated actors. Companies must invest continuously in advanced security technologies and staff training to mitigate risks. Failure to protect user data can lead to churn and negative publicity, undermining market growth. Ensuring a secure and private gaming environment is essential for maintaining trust and sustaining the industry’s reputation in an increasingly digital world.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.87% |

| Segments Covered | By Device, Age Group, Platform Type and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Market Leaders Profiled | Sony Interactive Entertainment, Microsoft Gaming, Nintendo Co., Ltd., Electronic Arts Inc., Ubisoft Entertainment SA, Activision Blizzard, Inc., Take-Two Interactive Software, Inc., Tencent Games, King Digital Entertainment plc, Frontier Developments plc, Jagex Ltd., Codemasters, Rebellion Developments Ltd., and Sumo Group plc |

SEGMENTAL ANALYSIS

By Device Insights

The consoles segment was the largest in the United Kingdom video games market and occupied a 28.1% share in 2025. This prominence of the segment was supported by its ability to offer exclusive high quality titles and optimized hardware performance that appeals to core gamers. Major manufacturers such as Sony and Microsoft invest billions in developing first party franchises that are only available on their platforms, creating strong ecosystem lock in. According to studies, blockbuster releases for PlayStation and Xbox consistently drive hardware adoption and software attachment rates in the UK. The plug and play nature of consoles eliminates the technical complexities associated with PC gaming, such as driver updates and compatibility issues, making them accessible to a broader audience. Consumers value the standardized experience where every unit performs identically, ensuring fair competition in multiplayer environments. The integration of media streaming services further enhances the value proposition, positioning consoles as central entertainment hubs in living rooms. Retailers support this dominance through aggressive bundling strategies during holiday seasons, which boost unit sales significantly. The longevity of console generations, typically spanning seven years, allows developers to fully exploit hardware capabilities, resulting in visually stunning and technically sophisticated games. This cycle of innovation and exclusivity sustains consumer interest and drives recurring revenue through online subscription services. The strong brand loyalty among console users ensures stable demand, making this segment the cornerstone of the UK gaming landscape.

The preeminence of the console segment is amplified by engaged gaming communities and social ecosystems, resulting in prolonged user retention. Online networks such as PlayStation Network and Xbox Live provide seamless connectivity for multiplayer matches, voice chat, and social interactions, creating vibrant digital communities. According to platform provider reports, millions of active users in the UK engage in online multiplayer sessions weekly, highlighting the social importance of these ecosystems. Exclusive online events, tournaments, and early access trials incentivize subscription renewals and deepen user investment in the platform. The ability to share gameplay clips and achievements directly to social media amplifies visibility and attracts new players through peer influence. Console manufacturers regularly update their interfaces to enhance social discovery, making it easier for friends to connect and play together. This social infrastructure transforms gaming from a solitary activity into a shared cultural experience, particularly among younger demographics. The integration of cross platform play in select titles further expands the potential player base, reducing fragmentation. Family sharing options allow multiple users to access purchased content, increasing household penetration. These community driven features create high switching costs, as users are reluctant to leave established social circles and accumulated digital libraries. The emphasis on connectivity and shared experiences ensures that consoles remain the preferred choice for social gamers in the UK.

The smartphone segment is anticipated to witness the fastest CAGR of 8.5% during the forecast period due to the ubiquity of mobile devices and the accessibility of casual gaming. Nearly every adult in the UK owns a smartphone, providing an immense installed base for game distribution without the need for additional hardware purchases. The rise of free to play models with optional microtransactions lowers the barrier to entry, attracting users who may not identify as traditional gamers. Short session lengths fit seamlessly into busy lifestyles, allowing people to play during commutes or breaks. App stores offer vast libraries of games across all genres, ensuring there is something for everyone. Improved mobile hardware capabilities now support complex graphics and mechanics, blurring the line between mobile and console experiences. Social integration within mobile games encourages viral growth through invites and leaderboards. The convenience of instant downloads and updates keeps content fresh and engaging. As mobile internet speeds increase, cloud gaming on smartphones becomes more viable, further expanding possibilities. This combination of accessibility, convenience, and improving technology ensures that the smartphone segment continues to outpace others in growth rate.

Innovative ad-supported models and smart monetization are driving the rapid expansion of the smartphone segment by increasing revenue per user. Developers utilize sophisticated data analytics to optimize in app purchases, battle passes, and loot boxes, tailoring offers to individual player behaviors. According to sources, ad revenue from rewarded videos and interstitial ads constitutes a significant portion of income for free to play titles, allowing developers to sustain operations without charging upfront fees. This model appeals to price sensitive consumers who prefer not to spend money directly but are willing to watch ads for benefits. The diversity of monetization options enables games to cater to both whales who spend heavily and casual players who contribute through engagement. Cross promotion within mobile ecosystems helps discoverability, driving organic installs. Partnerships with brands for in game advertising introduce new revenue streams while enhancing realism. The low cost of user acquisition compared to other platforms allows for aggressive marketing campaigns. Continuous updates and live ops keep players engaged over long periods, increasing lifetime value. As mobile payment systems become more seamless, friction in purchasing decreases, boosting conversion rates. These financial innovations ensure that the smartphone segment remains highly profitable and attractive to investors, sustaining its rapid expansion in the UK market.

By Age Group Insights

In 2025, the generation Y segment held the majority share of 35.9% of the United Kingdom video games market because of its high disposable income and strong nostalgic connection to gaming culture. Having grown up during the rise of home consoles and personal computers, this demographic views gaming as a core part of their identity and leisure routine. Their financial stability allows them to afford high end gaming setups and subscribe to multiple services simultaneously. Nostalgia drives demand for remasters and sequels of classic franchises, which publishers actively exploit to capture this loyal audience. This group values quality and depth, often preferring narrative rich single player experiences or competitive multiplayer titles that require skill and time investment. They are also early adopters of new technologies such as virtual reality, seeking immersive experiences that align with their tech savvy nature. Social gaming remains important, as they use online platforms to maintain connections with friends from school and university. The balance between work and life leads them to seek engaging escapism, making gaming a primary stress relief mechanism. This combination of financial power, emotional attachment, and habitual usage ensures that Generation Y remains the dominant force in the UK gaming economy.

Generation Y's influence in the digital landscape is increasingly driven by their active involvement in esports and streaming communities, which significantly fuels consumer engagement and market spending. Many Millennials are not just players but also spectators, following professional tournaments and content creators on platforms like Twitch and YouTube. The spectatorship translates into purchases of team merchandise, in game skins, and betting activities, contributing to market revenue. Streaming influences purchasing decisions, as viewers often buy games featured by their favorite personalities. This demographic values community and recognition, participating in clans and online forums to discuss strategies and share achievements. The social aspect of gaming provides a sense of belonging and identity, reinforcing loyalty to specific titles and platforms. Brands leverage this engagement through influencer marketing and sponsored events, targeting Millennials effectively. The desire to stay relevant in gaming conversations motivates continuous investment in new releases and hardware upgrades. This deep integration of gaming into their social and cultural lives ensures that Generation Y maintains its dominant position, driving trends and sustaining high levels of activity in the UK market.

The generation Z segment is likely to experience the fastest CAGR of 7.2% from 2026 to 2034 owing to its status as digital natives and the deep integration of gaming into their social lives. Born into a world of ubiquitous internet and smartphones, this cohort considers gaming a primary mode of communication and interaction rather than just a hobby. The social utility drives high frequency usage and retention, as leaving a game means disconnecting from their peer group. Generation Z prefers free to play titles that are accessible to all friends regardless of financial status, fostering inclusive communities. They are highly influenced by viral trends on TikTok and Instagram, which can propel obscure games to mainstream popularity overnight. This responsiveness to social media creates rapid spikes in demand and engagement. Their comfort with digital transactions facilitates easy spending on microtransactions and subscriptions. The desire for self expression through customizable avatars and items drives significant revenue in cosmetic markets. As this generation enters the workforce, their spending power will increase, but their habits are already shaping the market. This deep seated cultural integration ensures that Generation Z continues to grow rapidly, influencing development trends and platform preferences.

The accelerated growth of Generation Z is also fueled by their strong preference for cross platform play and mobile accessibility, which removes barriers to entry and enhances convenience. This demographic expects to play with friends regardless of the device they own, whether it be a console, PC, or smartphone. Mobile gaming plays a crucial role, as smartphones are always accessible, allowing for spontaneous play sessions throughout the day. The seamless transition between devices enables continuous engagement, fitting gaming into fragmented schedules. Generation Z is less loyal to specific hardware brands and more focused on the game itself and the social experience it offers. This attitude encourages developers to prioritize multi platform releases and cloud saving features. The ease of accessing games via app stores or digital storefronts reduces friction, encouraging trial and adoption of new titles. Short form content and quick match formats appeal to their attention spans and lifestyle. As mobile hardware improves, the gap between mobile and traditional gaming narrows, further attracting this demographic. This focus on accessibility and connectivity ensures that Generation Z remains the fastest growing segment, driving the industry toward more open and flexible ecosystems.

By Platform Type Insights

The offline platforms segment continued to led the United Kingdom video games market and captured a notable share in 2025. This position was attributed to the enduring appeal of premium single player experiences and the tangible value of physical collectibles. Many gamers prefer immersive narrative driven titles that do not require constant internet connectivity, allowing for uninterrupted play and deeper engagement with storylines. The ownership of physical media provides a sense of permanence and resale value that digital licenses lack, appealing to budget conscious consumers who trade in old games. Offline play eliminates concerns about server shutdowns or online toxicity, offering a safe and controlled environment. High profile exclusives on consoles often drive hardware sales, reinforcing the importance of offline capable platforms. The ability to play without subscription fees or internet dependencies makes offline gaming accessible to households with limited connectivity. Retailers support this segment through pre order incentives and limited edition bundles that enhance perceived value. The prestige associated with completing challenging single player campaigns fosters community discussion and longevity. This preference for curated, high quality offline experiences ensures that this segment remains dominant, catering to core gamers who prioritize depth and ownership over convenience.

The adoption of offline platforms is further supported by their reliability and independence from network constraints, which appeals to users in areas with inconsistent internet service or those concerned about data privacy. Offline games guarantee access regardless of server status or maintenance schedules, providing a consistent user experience. According to research, many players appreciate the ability to play anywhere without worrying about latency or disconnections. This reliability is crucial for travel or rural locations where broadband access may be limited. Offline modes also protect user privacy, as no personal data needs to be transmitted to external servers, addressing growing concerns about digital surveillance. The absence of mandatory online checks respects consumer rights to use purchased products freely. Developers often include robust offline components in hybrid titles to cater to this demand, ensuring broader appeal. The stability of offline performance allows for precise control and responsiveness, which is critical for certain genres like fighting or racing games. This technical advantage reinforces the preference for offline play among competitive and purist gamers. Internet costs and reliability remain variable issues for some demographics. Consequently, the assurance of offline accessibility sustains the segment’s leadership in the UK market.

The online platform segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 9.1% over the forecast period. This quick surge of the segment is fuelled by the prevalence of live service models and intense community interaction. Games designed as ongoing services receive regular content updates, seasonal events, and new features that keep players engaged for years rather than weeks. The social nature of online gaming fosters strong communities where players collaborate, compete, and communicate, creating emotional attachments to the game world. Multiplayer modes encourage repeat playthroughs and skill improvement, driving long term retention. The integration of social features such as guilds, friends lists, and voice chat enhances the sense of belonging. Live operations allow developers to respond to player feedback in real time, improving satisfaction and loyalty. The success of battle royale and massive multiplayer online games demonstrates the power of shared experiences in driving growth. These models generate consistent revenue through microtransactions and season passes, supporting continuous development. As social interaction becomes increasingly digital, online platforms serve as vital virtual spaces for connection. This dynamic and evolving nature ensures that the online segment continues to expand rapidly, capturing a larger share of player time and spending.

The accelerated growth of the online segment is also fueled by the expansion of esports and competitive gaming ecosystems, which attract millions of viewers and participants. Professional tournaments and ranked leagues provide structured competitive environments that motivate players to improve and invest in their skills. The aspiration to compete professionally or achieve high ranks drives intense engagement and spending on performance enhancing items or coaching. Streaming platforms amplify this effect by showcasing high level play and creating celebrities out of top players. Sponsorships and prize pools add legitimacy and excitement, drawing in casual observers who may eventually become players. Online platforms facilitate easy entry into competitive scenes through matchmaking systems that pair players of similar skill levels. This accessibility lowers the barrier to competitive play, expanding the participant base. The thrill of competition and recognition within the community sustains long term interest. As esports infrastructure improves with better broadcasting and training facilities, the appeal of online competitive gaming will continue to grow. This vibrant ecosystem ensures that the online segment remains the fastest growing category, driven by passion, competition, and community.

REGIONAL ANALYSIS

The United Kingdom holds a significant position in the European video games market and accounted for a 24.5% share in 2025. This expansion is mainly driven by a vibrant creative sector and high consumer engagement. As a leading market, the UK boasts a rich history of innovation, home to renowned studios that have produced globally successful franchises. According to UKIE, the games industry contributes billions to the national economy and supports tens of thousands of jobs, reflecting its strategic importance. The market status is robust, with high penetration rates across all age groups and a strong culture of gaming acceptance. Consumers in the UK are early adopters of new technologies, driving demand for next generation consoles, virtual reality, and cloud gaming services. The regulatory framework supports intellectual property protection and consumer safety, fostering a trustworthy environment for digital transactions. Educational initiatives promote digital literacy and coding skills, nurturing future talent for the industry. The presence of major international publishers and independent developers creates a diverse ecosystem that encourages creativity and competition. Infrastructure investments in broadband and 5G networks support the growth of online and mobile gaming segments. Cultural events such as gaming conventions and esports tournaments enhance community engagement and visibility. The UK’s influence extends beyond its borders, setting trends in game design and monetization that resonate globally. This combination of creative talent, technological infrastructure, and enthusiastic consumer base ensures that the United Kingdom remains a dominant and influential force in the global video games market.

The country’s market is driven by several key factors, including strong domestic development capabilities, high disposable income, and widespread digital connectivity. According to the Department for Digital Culture Media and Sport, government tax reliefs for video game development have stimulated investment and job creation, encouraging both local and foreign studios to establish operations in the UK. This supportive policy environment fosters innovation and ensures a steady supply of high quality content. Consumer spending power remains resilient, with gamers willing to invest in premium hardware and software despite economic fluctuations. The widespread availability of high speed internet facilitates the growth of online multiplayer and cloud gaming services, expanding access to diverse audiences. Cultural acceptance of gaming as a mainstream entertainment form drives participation across demographics, from children to seniors. The rise of esports and streaming has created new avenues for engagement and revenue, attracting sponsorship and media attention. Collaboration between academia and industry ensures a pipeline of skilled professionals, maintaining the UK’s competitive edge. Retail and digital distribution channels are well developed, offering consumers convenient access to products. These dynamics create a thriving ecosystem where creativity and commerce intersect, driving continuous growth and innovation. The UK’s proactive approach to industry support and consumer protection ensures its sustained leadership and relevance in the evolving global gaming landscape.

COMPETITIVE LANDSCAPE

The competition in the United Kingdom video games market is fierce and characterized by a mix of global giants and innovative independent studios. Major international publishers dominate through extensive resources and established franchises that attract large audiences. However, independent developers compete effectively by focusing on niche genres and unique artistic visions that differentiate their products. The rise of digital distribution has lowered entry barriers, allowing smaller studios to reach global markets directly. This democratization increases product diversity but also intensifies the struggle for visibility and consumer attention. Intellectual property strength plays a crucial role, with established brands commanding premium pricing and loyalty. Technological innovation drives differentiation, as companies race to implement advanced graphics and artificial intelligence. Consumer preferences for quality and value force continuous improvement in game design and customer support. The market rewards creativity and agility, making it essential for players to adapt quickly to trends and feedback. This dynamic environment ensures that only those who deliver exceptional experiences and maintain strong community connections thrive in the long term.

KEY MARKET PLAYERS

Some of the promising companies that are playing a dominating role in the United Kingdom Video Games Market include

- Sony Interactive Entertainment

- Microsoft Gaming

- Nintendo

- Electronic Arts

- Ubisoft

- Activision Blizzard

- Take-Two Interactive

- Tencent Games

- King

- Frontier Developments

- Jagex

- Codemasters

- Rebellion Developments

- Sumo Group

Top Players in the UK Video Games Market

Rockstar North

Rockstar North stands as a premier development studio based in Edinburgh and plays a pivotal role in the United Kingdom video games landscape. The company is renowned for creating critically acclaimed open world titles that set global standards for narrative depth and technical innovation. Recent actions include continuous support for its flagship online multiplayer platform through regular content updates and community events. Rockstar strengthens its position by investing heavily in advanced graphics technology and artificial intelligence to enhance player immersion. The studio collaborates closely with international publishing partners to ensure wide distribution and marketing reach. Its commitment to quality and detail fosters intense brand loyalty among gamers. The UK's creative economy receives a major boost from Rockstar North's work. The studio achieves this economic impact by leveraging high production values and highly engaging storytelling to maintain its leadership position.

Frontier Developments

Frontier Developments is a leading independent game developer and publisher headquartered in Cambridge that contributes significantly to the UK gaming sector. The company specializes in simulation and strategy genres, offering deep and complex gameplay experiences that appeal to dedicated enthusiasts. Recent actions involve expanding its live service models for popular franchises to ensure long term player engagement and recurring revenue. Frontier strengthens its market position by leveraging proprietary engine technology to create detailed and dynamic virtual worlds. The studio actively recruits top talent from UK universities and supports local educational initiatives to nurture future developers. Its focus on community feedback drives iterative improvements and content additions. Frontier Developments reinforces its status as a key innovator and employer within the British video games industry. It achieves this by maintaining creative independence and consistently delivering high-quality simulations.

Creative Assembly

Creative Assembly is a prominent game development studio located in Horsham that makes substantial contributions to the United Kingdom video games market. Known for its strategic and tactical gaming expertise, the company produces highly regarded titles that combine historical accuracy with engaging mechanics. Recent actions include enhancing its total war series with new factions and downloadable content to keep the player base active and interested. Creative Assembly strengthens its position by investing in research and development for improved artificial intelligence and battlefield realism. The studio participates in industry events and collaborates with other UK developers to share best practices and drive innovation. Its dedication to excellence in strategy gaming attracts a loyal global audience. Creative Assembly maintains its industry influence by consistently delivering polished and immersive experiences. In doing so, it also supports the growth of the domestic gaming ecosystem.

Top Strategies Used By Key Market Participants

Key players in the United Kingdom video games market employ several strategic approaches to maintain competitiveness and drive growth. Content diversification is central, with companies developing titles across multiple genres to appeal to broad audiences. Live service models are widely adopted to generate recurring revenue through regular updates and seasonal events. Strategic partnerships with hardware manufacturers ensure optimization and exclusive features that enhance user experience. Investment in emerging technologies such as virtual reality and cloud gaming allows firms to stay ahead of technological curves. Community engagement is prioritized through social media interaction and esports sponsorships to build loyal fan bases. Talent acquisition and retention programs help secure skilled developers necessary for high quality production. These combined strategies enable key participants to navigate market challenges and capitalize on emerging opportunities effectively.

MARKET SEGMENTATION

This research report on the United Kingdom Video Games Market has been segmented based on the following categories.

By Device

- Smartphones

- PC/Laptop

- Consoles

By Age Group

- Generation X

- Generation Y

- Generation Z

By Platform Type

- Online

- Offline

By Country

- U.K

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com