United Kingdom Vinyl Market Size, Share, Trends & Growth Forecast Report Segmented By Product Type (LP/EP vinyl records, Single vinyl records), Distribution Channel, End-User and Country – Industry Analysis From 2026 to 2034

Market Size, 2025

$16.24 BnMarket Estimate, 2026

$17.45 BnMarket Forecast, 2034

$31.05 BnCAGR, 2026–2034

7.47%United Kingdom Vinyl Market Report Summary

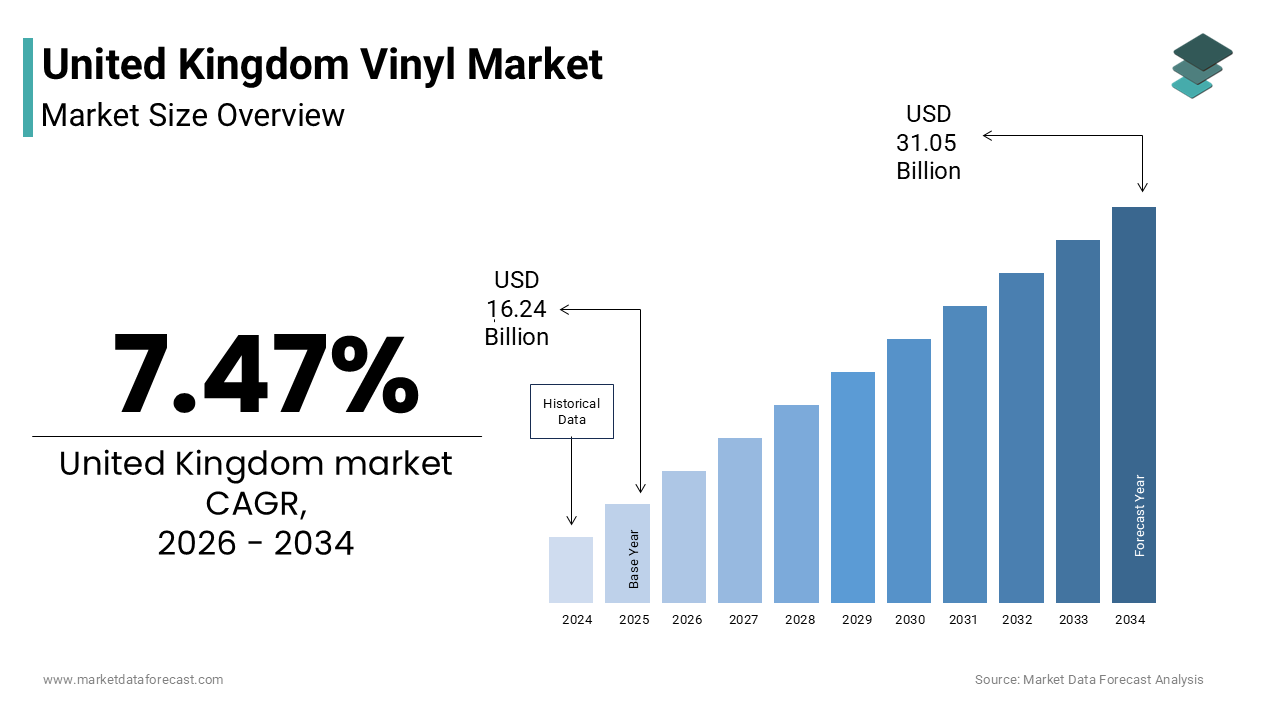

The United Kingdom vinyl market was valued at USD 16.24 billion in 2025 and is anticipated to reach USD 17.45 billion in 2026 from USD 31.05 billion by 2034, growing at a CAGR of 7.47% during the forecast period from 2026 to 2034. The growth of the United Kingdom vinyl market is driven by increasing consumer preference for physical music formats, rising demand for collectible music products, and growing appreciation for high-quality analog audio experiences. Expanding popularity of limited-edition vinyl releases, increasing participation in music culture events, and growing interest among younger demographics in tangible music ownership are further accelerating market growth. Moreover, advancements in vinyl production technologies, expansion of direct-to-consumer sales channels, and increasing demand for premium and exclusive music merchandise are supporting the expansion of the United Kingdom vinyl market.

Key Market Trends

- Rising demand for limited-edition and colored vinyl records among collectors and music enthusiasts.

- Increasing popularity of vinyl as a premium music format offering tangible ownership and immersive listening experiences.

- Growing adoption of direct-to-consumer sales models by artists and record labels.

- Strong focus on exclusive releases, artist merchandise bundles, and special edition packaging formats.

- Expansion of independent record stores as community hubs for music discovery and cultural engagement.

Segmental Insights

- Based on product type, the LP and EP vinyl records segment dominated the United Kingdom vinyl market and held the largest share in 2025. The segment’s dominance is attributed to strong consumer preference for album-oriented listening experiences, higher perceived artistic value, premium packaging opportunities, and widespread availability of new releases and classic catalog titles.

- The single vinyl records segment is projected to witness the fastest CAGR during the forecast period owing to increasing collector demand, rising popularity of limited-edition releases, lower purchase costs, and growing artist utilization of singles to engage audiences between album launches.

- Based on distribution channel, the offline segment accounted for the leading share of the United Kingdom vinyl market in 2025. The dominance of this segment is driven by consumer preference for physical browsing experiences, immediate product ownership, personalized recommendations from store staff, and the cultural significance of independent record stores.

- Based on packaging, the gatefold packaging segment held the major share of the United Kingdom vinyl market in 2025 owing to its premium presentation, enhanced artwork display, inclusion of additional content, and strong appeal among collectors and audiophiles.

- Based on end-user, the private segment dominated the United Kingdom vinyl market in 2025 due to increasing home listening activities, growing personal record collections, strong emotional attachment to physical music formats, and rising investments in home audio systems.

Regional Insights

The United Kingdom accounted for a significant share of the European vinyl market in 2025, supported by a strong music culture, growing collector communities, and the continued resurgence of physical music formats. The country benefits from a well-established network of independent record stores, active participation in music-related cultural events, and increasing consumer demand for premium audio experiences. Rising interest from younger generations and sustained support from artists and record labels continue to strengthen market growth across the United Kingdom.

Competitive Landscape

The United Kingdom vinyl market is highly competitive and characterized by the presence of major record labels, independent music distributors, specialist vinyl retailers, and record pressing service providers competing through exclusive releases, premium packaging, artist partnerships, and collector-focused offerings. Leading companies are focusing on expanding limited-edition product portfolios, strengthening direct-to-consumer sales channels, investing in sustainable packaging solutions, and enhancing customer engagement through exclusive events and community-driven initiatives. Strategic collaborations with artists, independent record stores, and music festivals are further strengthening market positioning across the vinyl ecosystem. Prominent players in the United Kingdom vinyl market include HMV, Rough Trade, Beggars Group, Universal Music Group, Sony Music Entertainment, Warner Music Group, Diverse Vinyl, Fopp, Flashback Records, Jacaranda Records, BPI (British Phonographic Industry), Proper Music Group, Demon Music Group, PIAS Group, and Cherry Red Records.

United Kingdom Vinyl Market Size

The United Kingdom vinyl market size was valued at USD 16.24 billion in 2025 and is anticipated to reach USD 17.45 billion in 2026 from USD 31.05 billion by 2034, growing at a CAGR of 7.47% during the forecast period from 2026 to 2034.

The vinyl is an analog audio formats have reclaimed significant relevance in a predominantly digital age. Consumers engage with vinyl not merely as a medium for listening but as a physical artifact that offers a ritualistic and immersive experience distinct from streaming services. According to the British Phonographic Industry, vinyl revenues have surpassed those of CDs for several consecutive years, marking a historic shift in physical media consumption. The demographic profile of buyers has broadened significantly, with younger generations driving much of the recent growth alongside older enthusiasts. Retail infrastructure has adapted accordingly, with independent record stores thriving alongside major retailers who have reinstated vinyl sections. The supply chain involves specialized pressing plants, many of which have undergone expansion to meet surging demand. Cultural events such as Record Store Day play a pivotal role in stimulating interest and creating exclusive release windows. This ecosystem reflects a broader societal desire for authenticity and slowness in an increasingly fast paced digital world.

MARKET DRIVERS

Nostalgia And Tangible Ownership Drive Emotional Connection To Music

The profound emotional connection fostered by nostalgia and the desire for tangible ownership is fuelling the growth of the United Kingdom vinyl market. In an era, where music is often consumed as ephemeral data streams, vinyl records offer a physical manifestation of artistic expression that listeners can hold, display, and cherish. A significant proportion of UK consumers cite the tactile experience and visual appeal of large format artwork as key reasons for purchasing vinyl. This sensory engagement creates a deeper bond between the listener and the music, transforming listening into a deliberate and mindful activity rather than background noise. The ritual of removing a record from its sleeve, placing it on the turntable, and carefully lowering the needle encourages focused attention and appreciation of the album as a complete work. For older demographics, vinyl evokes memories of youth and earlier musical eras, while younger buyers seek authenticity and a connection to music history. The collectibility aspect further enhances this drive, with limited editions and colored pressings becoming sought after items. Owning a physical copy provides a sense of permanence and legacy that digital licenses cannot replicate.

Superior Audio Quality And Audiophile Appeal Attract Discerning Listeners

The perception of superior audio quality and the specific appeal to audiophiles is another factor boosting the growth of the United Kingdom vinyl market. Many enthusiasts argue that analog recordings offer a warmer, richer, and more authentic sound profile compared to compressed digital files. According to audio engineering experts, the continuous wave form of vinyl captures nuances and dynamics that may be lost in digital conversion processes in high resolution masterings. This technical advantage attracts discerning listeners who invest in high end turntables, amplifiers, and speakers to maximize their listening experience. The resurgence of vinyl has spurred innovation in audio equipment manufacturing, with both vintage and modern brands catering to this growing segment. Audiophiles appreciate the depth and spatial separation that well pressed vinyl can provide, especially for genres such as jazz, classical, and rock where instrumental detail is crucial. The format encourages active listening, allowing fans to discover subtle layers in productions that might be overlooked in passive streaming. Reviews and forums dedicated to vinyl pressing quality further educate consumers, raising standards and expectations. Artists and labels often release special audiophile editions using premium materials and half speed mastering techniques to cater to this demand. This focus on sonic excellence differentiates vinyl from other formats and justifies its higher price point.

MARKET RESTRAINTS

Production Capacity Constraints And Supply Chain Bottlenecks Limit Availability

The persistent production capacity constraints and supply chain disruptions is limiting the growth of the United Kingdom vinyl market. The global shortage of pressing plants and specialized equipment has created long lead times for new releases, sometimes extending to six months or more. According to industry associations, the number of operational pressing machines worldwide remains insufficient to handle the current volume of orders by causing delays for both major labels and independent artists. This scarcity forces retailers to manage limited stock carefully, often resulting in missed sales opportunities and customer dissatisfaction. The reliance on a few key manufacturers for raw materials such as polyvinyl chloride pellets exacerbates the problem, as any disruption in chemical supply chains impacts production schedules. Small independent labels struggle to compete with major corporations for pressing slots, limiting diversity in available titles. The backlog of orders also increases costs, as expedited shipping and premium slot fees become necessary to secure timely releases. These logistical challenges frustrate consumers who face uncertainty regarding release dates and availability. The inability to scale production quickly in response to trend spikes means that popular albums may sell out rapidly and remain unavailable for extended periods.

High Retail Prices And Economic Pressure Deter Price Sensitive Consumers

The elevated retail prices and broader economic pressure by deterring price sensitive consumers is also impeding the growth of the United Kingdom vinyl market. Vinyl records are significantly more expensive than digital downloads or streaming subscriptions, with new releases often costing over 25 pounds. According to the Office for National Statistics, rising inflation and cost of living pressures have reduced disposable income for many households, leading to more cautious spending on non essential items. For casual listeners, the high entry cost of building a vinyl collection is prohibitive, especially when considering the additional expense of playback equipment. Budget conscious consumers may prioritize essential goods over luxury entertainment formats by reducing overall demand. The price disparity between vinyl and other formats makes it difficult for the medium to achieve mass penetration beyond dedicated enthusiasts. Retailers face difficulties in passing on increased production and logistics costs to consumers without further dampening demand. Promotional discounts are less common due to tight margins, limiting incentives for hesitant buyers. The perception of vinyl as a premium product excludes lower income demographics who might otherwise be interested in the format. Economic uncertainty also affects gift giving trends, with buyers opting for cheaper alternatives during holiday seasons. This financial barrier restricts the market to a narrower segment of affluent consumers by limiting its broader cultural impact and commercial potential.

MARKET OPPORTUNITIES

Expansion Into Direct To Consumer Sales And Exclusive Merchandise Bundles

The expansion into direct to consumer sales and exclusive merchandise bundles by enhancing profit margins and strengthening artist fan connections is setting up new opportunities for the growth of the United Kingdom vinyl market. Artists and independent labels can bypass traditional retail intermediaries by selling vinyl directly through their websites, retaining a larger share of revenue. Fans are increasingly willing to purchase premium bundles that include signed records, posters, and clothing alongside the music. This strategy leverages the emotional loyalty of followers who value unique and personalized items. Direct sales allow for better inventory management and immediate feedback on demand, reducing the risk of overproduction. Exclusive variants such as colored vinyl or limited-edition pressings create urgency and drive immediate purchases. Social media platforms facilitate targeted marketing campaigns that reach dedicated fan bases effectively. This approach empowers emerging artists, who may lack support from major labels to monetize their work effectively. The trend toward supporting independent creators aligns with consumer preferences for authenticity and ethical consumption.

Revitalization Of Independent Record Stores And Community Hubs

The revitalization of independent record stores and their evolution into community hubs by fostering local engagement and cultural discovery is also to escalate the growth of the United Kingdom vinyl market in coming years. These stores serve as vital spaces for music enthusiasts to connect, share recommendations, and participate in events such as in store performances and listening parties. Their curated selections provide personalized service that algorithms cannot match, guiding customers toward new discoveries. Events like Record Store Day drive significant foot traffic and sales, highlighting the importance of physical retail in the vinyl ecosystem. Collaborations with local cafes, bars, and cultural institutions create vibrant social scenes that attract younger demographics. Independent stores often champion local artists, providing a platform for regional talent to reach audiences. This community focused model builds strong customer loyalty and repeat business. The experiential aspect of browsing physical shelves and interacting with knowledgeable staff enhances the shopping journey.

MARKET CHALLENGES

Volatility In Raw Material Costs And Environmental Sustainability Concerns

The volatility in raw material costs and growing environmental sustainability concerns is to pose as a challenge for the growth of the United Kingdom vinyl market. The primary material for records, polyvinyl chloride, is derived from fossil fuels by making its price susceptible to fluctuations in oil markets. According to chemical industry analysts, energy intensive production processes further exacerbate cost instability, impacting profit margins for manufacturers and retailers. Additionally, increasing awareness of plastic pollution and carbon footprints has led to scrutiny of vinyl’s environmental impact. Consumers and regulators are demanding more sustainable practices, pressuring the industry to explore eco-friendly alternatives. However, developing viable biodegradable substitutes that maintain audio quality is technically challenging and costly. Recycling programs for vinyl are limited due to the complexity of separating materials and the lack of infrastructure. The perception of vinyl as an environmentally unfriendly product may deter eco conscious buyers, particularly among younger generations who prioritize sustainability. Companies face the dual challenge of managing rising production costs, while investing in green initiatives to maintain brand reputation. Failure to address these issues could lead to regulatory restrictions or consumer backlash.

Competition From Resurgent Compact Discs And Digital Streaming Convenience

The intense competition from resurgent compact discs and the unparalleled convenience of digital streaming services is to limit the growth of the United Kingdom vinyl market. While vinyl appeals to enthusiasts, CDs offer similar physical ownership benefits at a lower price point and with greater durability. CD sales have shown signs of recovery as consumers seek affordable physical media options. The compact size and ease of storage make CDs practical for large collections by appealing to space constrained households. Meanwhile, streaming platforms provide instant access to vast libraries of music for a monthly subscription fee, which is eliminating the need for physical storage or maintenance. The convenience of playlists and algorithmic recommendations caters to casual listeners who prioritize variety and ease over fidelity. This dual threat squeezes vinyl from both ends, limiting its appeal to a niche audience. Younger consumers raised on streaming may view vinyl as an unnecessary luxury rather than a primary listening format. The dominance of mobile devices for music consumption further reduces the relevance of home based audio systems. Vinyl must continually justify its premium status against these more practical alternatives. Marketing efforts must emphasize unique value propositions such as sound quality and collectibility to retain relevance.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.47% |

| Segments Covered | By Product Type, Distribution Channel, End-User and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Market Leaders Profiled | HMV, Rough Trade, Beggars Group, Universal Music Group, Sony Music Entertainment, Warner Music Group, Diverse Vinyl, Fopp, Flashback Records, Jacaranda Records, BPI (British Phonographic Industry), Proper Music Group, Demon Music Group, PIAS Group, and Cherry Red Records.. |

SEGMENTAL ANALYSIS

By Product Type Insights

The LP and EP vinyl records segment was accounted in holding 43.2% of the United Kingdom vinyl market in 2025 with the enduring cultural preference for album oriented listening experiences and the artistic value associated with long format releases. Consumers view albums as complete artistic statements rather than collections of individual songs by making the LP format the preferred medium for deep engagement with music. LPs account for the vast majority of vinyl sales volume, significantly outpacing singles in both unit numbers and revenue. Fans appreciate the ritual of playing a full side of an album, which encourages uninterrupted listening and appreciation of sequencing and flow. Major artists continue to prioritize LP releases for new albums by ensuring a steady stream of high profile titles that drive consumer interest. The format also supports higher price points, allowing labels to invest in premium packaging and mastering quality. Collectors often seek out specific pressings of classic albums by sustaining demand for back catalog titles. The social aspect of sharing albums with friends further cements the LP’s role in music culture. This segment benefits from the perception of vinyl as a serious medium for music appreciation, distinguishing it from casual digital consumption.

The single vinyl segment is projected to register a fastest CAGR of 12.5%, fueled by their high collectibility and the popularity of limited-edition releases. Unlike LPs, singles are often produced in small batches with unique colors, picture discs, or special packaging, making them highly sought after by collectors. The exclusive single releases tied to major artist launches or events like Record Store Day sell out rapidly, driving intense demand. The lower price point compared to LPs makes singles an accessible entry point for new collectors or casual fans who want a physical memento without a large investment. The trend of releasing multiple variants of the same single encourages fans to purchase several copies to complete their collections. Social media platforms amplify this behavior, as users showcase their rare finds and trade items within online communities. Artists leverage singles to maintain visibility between album cycles, keeping fans engaged and excited. The compact size of singles also appeals to those with limited storage space. This segment benefits from the hype culture surrounding modern music releases, where scarcity drives value.

By Distribution Channel Insights

The offline distribution channels segment held a dominant share of the United Kingdom vinyl market in 2025 with the inherent need for tactile experience and immediate gratification that physical stores provide. Vinyl is a sensory product, and buyers often prefer to inspect the condition of the sleeve, the weight of the disc, and the quality of the pressing before purchasing. The independent record stores and major high street retailers attract customers, who value the ritual of browsing and discovering hidden gems. The ability to take home a purchase immediately satisfies the desire for instant ownership, which online shipping delays cannot match. Staff expertise in local stores provides personalized recommendations and builds trust, enhancing the shopping experience. Events, such as in store performances and signing sessions create community hubs that draw foot traffic and foster loyalty. The visual appeal of window displays and organized shelves stimulates impulse buys and exploration. For many enthusiasts, visiting a record store is a leisure activity in itself, offering social interaction and cultural engagement. This experiential aspect differentiates offline retail from digital alternatives, maintaining its relevance despite the rise of e commerce. The trust associated with established brick and mortar businesses also reassures buyers regarding authenticity and condition.

The online distribution channel segment is likely to grow at a fastest CAGR of 9.8% from 2026 to 2034 with the unparalleled convenience and access to global inventory. Digital platforms allow buyers to search for specific titles, rare pressings, and out of print albums that may not be available locally. The online retailers offer vast catalogs that exceed the physical capacity of any single store, enabling consumers to find exactly what they want quickly. The ability to compare prices, read reviews, and check condition grades remotely simplifies the decision-making process. Home delivery eliminates the need for travel, appealing to busy professionals and those in rural areas with limited local options. Mobile apps and user-friendly websites enhance the shopping experience, making it easy to browse and purchase on the go. Secure payment systems and reliable return policies build trust in online transactions. The rise of specialized online vinyl marketplaces connects buyers with sellers worldwide, expanding choices significantly. Subscription services for monthly vinyl deliveries also contribute to this growth, offering curated selections to subscribers.

By Packaging Insights

The gatefold packaging segment was the largest by accounting for 47.1% of the United Kingdom vinyl market share in 2025 with its enhanced visual appeal and perception as a premium product format. The double sided sleeve allows for expansive artwork, lyrics, and photographs that enrich the aesthetic experience of owning a record. Buyers frequently cite the quality and size of artwork as key factors in their purchasing decisions, with gatefolds offering the most impressive presentation. This format is standard for most LP releases in rock, pop, and progressive genres, where visual storytelling is integral to the album concept. The sturdy construction of gatefold sleeves protects the discs better than single pockets, adding to their perceived value. Collectors appreciate the additional space for inserts, posters, and liner notes, which provide deeper context and engagement. Major artists and labels prioritize gatefold packaging for flagship releases to justify higher price points and distinguish their products in retail environments. The tactile satisfaction of opening a gatefold sleeve contributes to the ritualistic nature of vinyl listening. This format has become synonymous with the vinyl revival, representing the antithesis of disposable digital media. Its widespread adoption across genres ensures consistent demand and production volume.

The colored vinyl packaging segment is expected to grow at a fastest CAGR of 15.2% from 2026 to 2034 with the aesthetic customization and intense collector demand. Buyers are increasingly drawn to visually striking variants such as translucent, splatter, and marble effects that make each record a unique decorative item. The limited edition colored pressings often sell out faster than standard black vinyl, driving urgency and hype. Artists and labels use colored vinyl to differentiate releases and create buzz around new albums. The variety of color options allows for creative expression aligned with album themes or artistic visions. Collectors often seek multiple variants of the same album to complete their sets, boosting sales volume. Online communities dedicated to vinyl aesthetics amplify interest through photos and discussions. The perceived rarity of certain color combinations enhances their desirability and resale value. Pressing plants have improved techniques for producing consistent and vibrant colors, meeting quality expectations.

By End-User Insights

The private end users segment was the largest by holding 45.6% of the United Kingdom vinyl market share in 2025 with the desire for personal enjoyment and the establishment of home listening rituals. Individuals purchase vinyl for their own collections, valuing the intimate and immersive experience it provides in domestic settings. The ritual of selecting a record, cleaning it, and placing it on the turntable creates a mindful break from digital distractions. Private users appreciate the control over their listening environment by allowing for high fidelity playback through personal audio systems. The emotional connection to music is heightened in private settings, where listeners can focus without external interruptions. Building a personal collection serves as a form of self- expression and identity, reflecting individual tastes and memories. Gifts of vinyl among friends and family also contribute to this segment, reinforcing social bonds. The privacy of home listening allows for exploration of diverse genres without judgment. This segment benefits from the trend toward home improvement and nesting, where audio equipment becomes a central feature of living spaces.

The commercial end user segment is projected to witness a fastest CAGR of 10.5% during the forecast period owing to the adoption in the hospitality sector for ambiance creation. Bars, cafes, restaurants, and hotels are increasingly using vinyl records to curate unique atmospheres and differentiate their brands. Establishments view vinyl as a tool for enhancing customer experience and conveying sophistication or authenticity. DJs and staff select records that align with the venue’s identity by creating memorable sonic landscapes. The visual presence of turntables and record collections serves as decor and conversation starters for patrons. This trend aligns with the broader movement toward experiential dining and drinking, where every detail contributes to the overall impression. Commercial buyers purchase durable equipment and extensive libraries to support daily operations. The use of vinyl signals a commitment to quality and attention to detail, appealing to discerning customers.

COMPETITIVE LANDSCAPE

The competition in the United Kingdom vinyl market is characterized by a dynamic interplay between major record labels, independent distributors, and specialized retailers. Major labels leverage their extensive catalogs and financial resources to dominate mainstream releases and secure prime retail placement. Independent entities compete by focusing on niche genres, curated selections, and strong community ties that foster loyalty. The barrier to entry for new labels is moderate, but supply chain constraints favor established players with existing pressing agreements. Price competition is limited due to high production costs, shifting the focus to value added features such as exclusive artwork and bonus content. Retailers differentiate themselves through customer service, event hosting, and unique inventory. The rise of online marketplaces has intensified competition by increasing price transparency and global access. Brands must continuously innovate in packaging and marketing to stand out in a crowded field. Consumer preference for authenticity and quality drives brands to maintain high standards.

KEY MARKET PLAYERS

Some of the promising companies that are playing a dominating role in the United Kingdom vinyl market include

- HMV

- Rough Trade

- Beggars Group

- Universal Music Group

- Sony Music Entertainment

- Warner Music Group

- Diverse Vinyl

- Fopp

- Flashback Records

- Jacaranda Records

- BPI (British Phonographic Industry)

- Proper Music Group

- Demon Music Group

- PIAS Group

- Cherry Red Records

Top Players in the UK Vinyl Market

Virgin Music Label and Artist Services

Virgin Music Label and Artist Services plays a pivotal role in the United Kingdom vinyl market by supporting independent artists and labels with comprehensive distribution and marketing solutions. The company facilitates the physical release of records through its extensive network, ensuring wide availability across retail channels. Recent actions include expanding its pressing partnerships to reduce lead times for clients and launching specialized vinyl promotion campaigns. Virgin strengthens its position by offering data analytics tools that help artists optimize release strategies for physical formats. The company also invests in sustainable packaging initiatives to address environmental concerns within the industry. This holistic approach fosters long term relationships with talent and reinforces its status as a key enabler in the UK vinyl ecosystem.

PIAS Group

PIAS Group is a leading independent music company that significantly contributes to the UK vinyl market through its robust label services and distribution arm. The organization supports a diverse roster of artists, facilitating the production and global distribution of vinyl records. Recent actions involve strategic investments in supply chain infrastructure to improve efficiency and reliability for physical releases. PIAS strengthens its market position by collaborating with independent record stores to promote exclusive titles and host community events. The company also focuses on digital integration, linking physical sales with online engagement to enhance artist visibility.

Warner Music UK

Warner Music UK remains a dominant force in the United Kingdom vinyl market, leveraging its vast catalog and major artist roster to drive physical sales. The company actively promotes vinyl reissues and new releases through targeted marketing campaigns and retail partnerships. Warner strengthens its position by investing in advanced mastering techniques to ensure superior audio quality for audiophiles. The company also collaborates with high profile brands for cross promotional opportunities that expand reach beyond traditional music channels. Its global resources enable efficient logistics and widespread distribution, ensuring consistent availability of products. This strategic focus on quality and innovation sustains its influence in the evolving vinyl landscape.

Top Strategies Used By Key Market Participants

Key players in the United Kingdom vinyl market employ several strategic approaches to maintain competitiveness and drive growth. Product differentiation is central, with companies offering colored variants and limited editions to appeal to collectors. Strategic partnerships with pressing plants ensure priority access to production capacity and reduced lead times. Direct to consumer sales channels are expanded to capture higher margins and build direct fan relationships. Sustainability initiatives are adopted to address environmental concerns and meet consumer expectations for eco-friendly practices. Marketing efforts focus on storytelling and artist connections to enhance emotional engagement with physical products. Retail collaborations create exclusive release windows that drive foot traffic and urgency. These combined strategies enable key participants to navigate supply constraints and capitalize on the enduring appeal of vinyl.

MARKET SEGMENTATION

This research report on the United Kingdom vinyl market has been segmented based on the following categories.

By Product Type

- LP/EP vinyl records

- Single vinyl records

By Distribution channel

- Online

- Offline

By Packaging

- Colored

- Picture

- Gatefold

By End-user

- Private

- Commercial

By Country

- U.K

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com