- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

Market Size, 2025

$0.70 BnMarket Estimate, 2026

$0.72 BnMarket Forecast, 2034

$0.95 BnCAGR, 2026–2034

3.65%U.S. Apparel Market Report Summary

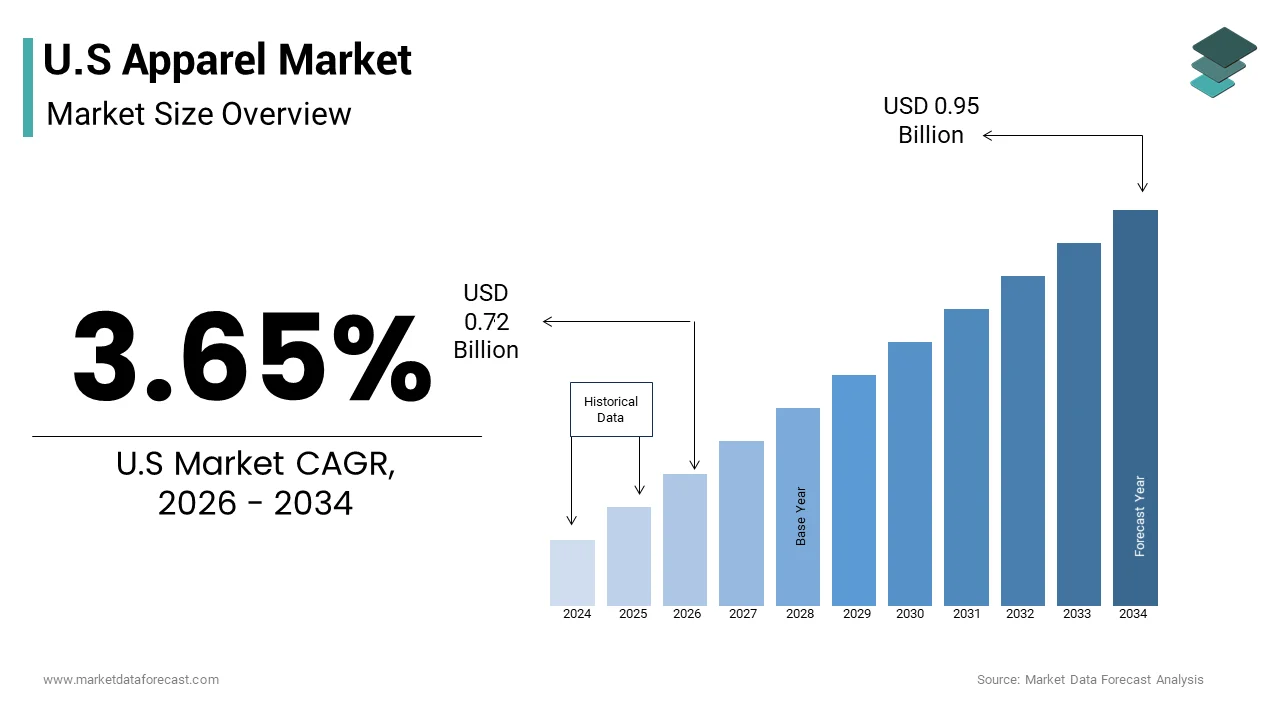

The United States apparel market was valued at USD 0.70 billion in 2025 and is anticipated to reach USD 0.72 billion in 2026 and USD 0.95 billion by 2034, growing at a CAGR of 3.65% during the forecast period from 2026 to 2034. The growth of the U.S. apparel market is driven by evolving fashion trends, rising consumer spending on lifestyle and fashion products, and increasing demand for comfortable and sustainable clothing. The growing influence of social media, celebrity endorsements, and fast-fashion retail models is further accelerating market expansion. In addition, the increasing adoption of omnichannel retail strategies, digital shopping platforms, and personalized shopping experiences is transforming the competitive landscape of the apparel industry across the country.

Key Market Trends

- Rising demand for sustainable and ethically produced apparel driven by increasing consumer awareness regarding environmental and social responsibility.

- Growing popularity of athleisure and casual wear segments fueled by changing work cultures and lifestyle preferences.

- Increasing integration of e-commerce, AI-driven personalization, and virtual fitting technologies to improve customer engagement and shopping convenience.

- Expansion of direct-to-consumer (DTC) business models among apparel brands to strengthen brand loyalty and profit margins.

- Strong influence of social media platforms, fashion influencers, and celebrity collaborations on apparel purchasing behavior and brand visibility.

Segmental Insights

- Based on category, the mass market segment dominated the U.S. apparel market and held the highest share in 2025. The dominance of this segment is attributed to the affordability, wide product availability, and increasing consumer preference for fashionable yet cost-effective clothing options.

- Based on end use, the women’s apparel segment occupied the largest share of the U.S. apparel market in 2025. The segment growth is driven by frequent fashion purchases, evolving style preferences, and increasing demand for seasonal and trend-based clothing collections.

- Based on distribution channel, the offline retail segment remained the leading distribution channel in the U.S. apparel market in 2025. The segment continues to dominate due to the tactile nature of clothing purchases, in-store trial experiences, immediate product availability, and strong consumer preference for physical retail shopping.

Regional Insights

The United States is expected to remain the largest and most influential apparel market in North America, supported by strong consumer purchasing power, a well-established retail ecosystem, and rapidly evolving fashion trends. Major fashion and retail hubs such as New York City, Los Angeles, and Miami continue to drive apparel demand due to their strong fashion influence, large consumer base, and presence of global retail brands. The increasing adoption of omnichannel shopping experiences and digital fashion marketing is further supporting nationwide market growth.

Competitive Landscape

The U.S. apparel market is highly competitive, with major companies focusing on product innovation, sustainable fashion initiatives, and digital retail expansion to strengthen their market presence. Leading brands are increasingly investing in eco-friendly materials, AI-powered supply chain optimization, and personalized customer experiences to improve operational efficiency and brand loyalty. Strategic collaborations with celebrities, sports organizations, and fashion influencers are also enhancing brand visibility and consumer engagement across diverse demographics.

Prominent players in the U.S. apparel market include Lululemon Athletica, Burberry Group plc, TJX Companies Inc., Gap Inc., Puma SE, Adidas AG, Nike Inc., H&M, LVMH, Kering Group, PVH Corp., and Inditex.

U.S Apparel Market Size

The U.S apparel market size was valued at USD 0.70 billion in 2025 and is anticipated to reach USD 0.72 billion in 2026 to reach USD 0.95 billion by 2034, growing at a CAGR of 3.65% during the forecast period from 2026 to 2034.

United States Apparel Market Overview

The apparel is the design of clothing items, including outerwear, underwear, sportswear, and formal wear for men, women, and children. The definition extends beyond mere utility to encompass fashion as a medium for social signaling and personal branding. Consumer engagement is heavily influenced by digital connectivity and rapid trend cycles driven by social media platforms. According to the United States Census Bureau, the population aged 16 and older which represents the primary labor force and consumer base for professional and casual attire accounts for approximately 270 million individuals providing a substantial demographic foundation. Furthermore, the average annual expenditures on apparel and services per consumer unit reached 1837 dollars in recent years demonstrating the significant financial allocation households dedicate to clothing. The shift toward remote and hybrid work models has redefined wardrobe requirements reducing demand for formal business wear while increasing interest in comfortable yet presentable casual options. The e-commerce continues to capture a growing share of total apparel sales indicating a structural shift in purchasing behavior. Sustainability concerns are also reshaping production standards as consumers increasingly prioritize ethical sourcing and environmental responsibility.

MARKET DRIVERS

Expansion of E Commerce and Digital Retail Infrastructure

The robust growth of online shopping platforms and digital retail infrastructure is boosting the growth of the United States apparel market. Consumers increasingly prefer the convenience variety and personalized experiences offered by e-commerce channels over traditional brick and mortar stores. This digital shift allows consumers to access a wider range of brands and styles without geographical constraints. The retailers have invested heavily in omnichannel capabilities, such as buy online pick up in store and virtual try on technologies to enhance customer satisfaction. The integration of artificial intelligence in recommendation engines helps shoppers discover products aligned with their preferences increasing conversion rates. Mobile commerce further accelerates this trend as smartphones become the primary device for browsing and purchasing clothing. Social media platforms like Instagram and TikTok serve as discovery engines where influencers showcase trends driving immediate purchase decisions through shoppable posts. The ease of returns and flexible payment options reduces the perceived risk of buying clothes online. This seamless digital ecosystem encourages frequent purchases and impulse buying behaviors. Brands that optimize their online presence and logistics networks gain a competitive advantage by meeting consumer expectations for speed and convenience.

Rising Disposable Income and Consumer Confidence Levels

The increase in disposable income and sustained consumer confidence levels is greatly enhancing the growth of the United States apparel market. As economic conditions stabilize and wages grow, Americans have more financial flexibility to spend on non-essential items including fashion and accessories. The personal disposable income has shown steady growth enabling households to allocate more funds toward clothing upgrades and seasonal wardrobe changes. Higher income levels correlate with increased spending on premium and luxury apparel brands as consumers seek quality and status symbols. The consumer confidence indices have remained resilient indicating optimism about future financial prospects which encourages discretionary spending. The recovery of the hospitality and travel sectors has also stimulated demand for occasion wear such as vacation outfits and formal attire for events. Younger demographics particularly Millennials and Gen Z are willing to invest in sustainable and ethically produced clothing reflecting their values and purchasing power. The trend toward experiential spending often includes fashion as a key component of social participation. Promotional events and seasonal sales further incentivize purchases by offering perceived value. The psychological boost from new clothing enhances self esteem and social presentation driving repeat purchases.

MARKET RESTRAINTS

Inflationary Pressures and Rising Cost of Living

The persistent inflation and the rising cost of living on spending by reducing household disposable income for non- essential good is hampering the growth of the United States apparel market. As prices for essentials, such as housing food and energy increase consumers prioritize these necessities over discretionary purchases like clothing. The Consumer Price Index for apparel has fluctuated but overall inflation rates have eroded purchasing power leading to cautious spending behavior. Many shoppers are delaying wardrobe updates or opting for lower priced alternatives to manage budgets effectively. The shift toward value oriented shopping means that premium and luxury brands face greater resistance in maintaining sales volumes. Discount retailers and private label brands benefit from this trend as consumers seek affordability without compromising basic quality. The uncertainty regarding future economic conditions encourages savings rather than spending on fashion items. Retailers respond by offering deeper discounts and promotions which can erode profit margins and brand equity. The psychological impact of financial stress reduces the emotional appeal of shopping for pleasure.

Supply Chain Disruptions and Raw Material Volatility

The ongoing challenges from supply chain disruptions and volatility in raw material costs, which impact production efficiency and pricing stability is hindering the growth of the United States apparel market. Dependence on global manufacturing hubs exposes brands to logistical hurdles geopolitical tensions and labor issues. Manufacturing indices have indicated persistent delays in sourcing fabrics and components affecting lead times and inventory availability. Fluctuations in the prices of cotton polyester and other fibers directly influence production costs forcing brands to adjust retail prices. As per data from the Bureau of Labor Statistics producer prices for textile mills and products have experienced significant variability creating uncertainty for long term planning. Shipping container shortages and port congestions further exacerbate delivery delays resulting in missed seasonal opportunities and excess inventory. The complexity of managing multi tier supply chains makes it difficult to ensure timely and cost effective production. Brands struggle to balance inventory levels against unpredictable demand and supply constraints. The need for faster turnaround times conflicts with the realities of global logistics. Smaller brands with limited resources are particularly vulnerable to these disruptions. The environmental cost of expedited shipping also conflicts with sustainability goals. These operational hurdles constrain the ability of companies to meet consumer expectations for availability and affordability.

MARKET OPPORTUNITIES

Adoption of Sustainable and Circular Fashion Models

The growing consumer demand for sustainability to innovate with eco-friendly materials and circular business models, which is creating new opportunities for the growth of the United States apparel market. Shoppers are increasingly prioritizing ethical production and environmental responsibility in their purchasing decisions. Brands can capitalize on this by introducing collections made from recycled fibers organic cotton and biodegradable materials. The circular economy model, which emphasizes reuse repair and recycling offers substantial potential for reducing waste and extending product lifecycles. Resale platforms and rental services are gaining traction allowing consumers to access high quality clothing at lower costs while minimizing environmental impact. Companies that implement take back programs and transparent supply chain practices build trust and loyalty among conscious consumers. Certification labels such as Global Organic Textile Standard provide verification of sustainability claims enhancing credibility. Marketing campaigns that highlight environmental benefits resonate strongly with younger demographics. Partnerships with technology firms enable tracking of material origins and carbon footprints.

Integration of Artificial Intelligence and Personalization Technologies

The integration of artificial intelligence and advanced personalization technologies for enhancing customer experience and driving sales is likely to elevate the growth of the United States apparel market. Consumers seek tailored recommendations and seamless shopping journeys that reflect their individual styles and preferences. The use of AI in retail is projected to grow significantly with personalized marketing being a key application area. Brands can leverage data analytics to predict trends optimize inventory and offer customized product suggestions. The shoppers are more likely to purchase from brands that provide personalized experiences including size recommendations and style matches. Virtual fitting rooms and augmented reality tools allow customers to visualize how clothes will look before buying reducing return rates. Chatbots and virtual assistants improve customer service by providing instant support and styling advice. The use of machine learning algorithms helps brands understand consumer behavior and refine marketing strategies. Direct to consumer models benefit from these technologies by building stronger relationships with customers through targeted communication. Subscription boxes and curated selections enhance convenience and discovery.

MARKET CHALLENGES

Intense Competition and Market Saturation

The intense competition and saturation with numerous brands vying for consumer attention in a crowded place is one of the major challenges for the growth of the United States apparel market. Price wars and frequent promotions erode profit margins and devalue brand equity. The consumers are overwhelmed by choices leading to decision fatigue and reduced brand allegiance. The rise of ultra fast fashion retailers offering extremely low prices and rapid trend turnover puts pressure on traditional brands to accelerate their production cycles. This speed often compromises quality and sustainability leading to reputational risks. Differentiation becomes challenging as many products appear similar in style and function. Marketing costs have increased as brands compete for digital advertising space and influencer partnerships. Customer acquisition costs are rising while retention rates decline due to the ease of switching brands. The saturation also leads to shorter product life cycles requiring constant innovation and inventory turnover. Smaller brands struggle to scale amidst dominant players with extensive resources.

Counterfeiting and Intellectual Property Theft

The prevalence of counterfeiting and intellectual property theft poses a severe threat to brand integrity and revenue is also to impede the growth of the United States apparel market. High demand for popular designs and luxury labels creates a lucrative market for fake products that mimic authentic items. The counterfeit goods cost the global economy billions of dollars annually with apparel being a primary target. These inferior copies often fail to meet quality and safety standards damaging brand reputation when confused with genuine products. As per data from United States Customs and Border Protection seizures of counterfeit clothing remain high indicating the scale of the issue. Online marketplaces and social media platforms facilitate the sale of fake items making it difficult for consumers to distinguish between real and counterfeit goods. Legal enforcement is challenging due to the cross border nature of e commerce and varying intellectual property laws. Brands must invest heavily in anti counterfeiting technologies such as holograms and blockchain verification. However, these measures add to operational costs and complexity. The presence of counterfeits undermines pricing strategies and exclusivity associated with premium brands. Consumers who inadvertently purchase fakes may develop negative perceptions of the brand. Protecting intellectual property requires constant vigilance and collaboration with law enforcement.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.65% |

| Segments Covered | By End-User, Distribution Channel Category, and By Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

| Regions Covered | California, Washington, Oregon, New York & Rest of the United States |

| Market Leaders Profiled | Lululemon Athletica, Burberry Group plc, TJX Companies Inc, Gap Inc, Puma SE, Adidas AG, Nike Inc., H & M Hennes & Mauritz AB, LVMH, Kering Group, PVH Corp., Inditex. |

SEGMENTAL ANALYSIS

By Category Insights

The mass segment was the largest by holding 34.4% of the United States apparel market share in 2025 with its affordability accessibility and alignment with the budgetary constraints of a broad consumer base. The clothing sold through large retail chains discount stores and fast fashion brands that prioritize volume and rapid turnover. The economic pressure on disposable income, which compels consumers to seek value-oriented options for everyday wear. The retailers account for the majority of apparel unit sales due to their extensive distribution networks and competitive pricing strategies. The prevalence of private label offerings from major supermarkets and department stores further strengthens this segment by providing comparable quality at lower prices. Fast fashion models enable these retailers to replicate high end trends quickly and affordably appealing to style conscious shoppers with limited budgets. The convenience of one stop shopping at big box retailers also contributes to the segment's dominance as consumers prefer to consolidate purchases. Additionally, the rise of online marketplaces has increased price transparency forcing brands to maintain low margins to remain competitive.

The luxury segment is likely to witness a fastest CAGR of 7.2% during the forecast period with the increasing wealth of high net worth individuals and the aspirational spending habits of younger demographics, who view luxury goods as investments and status symbols. The resilience of the affluent consumer base, which remains largely unaffected by broader economic fluctuations. The millennial and Gen Z consumers are expected to account for a significant portion of luxury spending by 2030 driving demand for exclusive and branded items. The shift toward experiential luxury where purchasing high end clothing is part of a lifestyle narrative further amplifies demand. Brands are leveraging digital platforms to reach younger audiences through immersive online experiences and social media campaigns. The scarcity and exclusivity associated with luxury apparel create a sense of urgency and desire among consumers. Additionally the rise of resale markets for authenticated luxury items has made these products more accessible to a wider audience while maintaining brand prestige. This convergence of wealth concentration generational shifts and digital engagement positions the luxury segment for sustained rapid growth.

By End Use Insights

The women segment was the largest by holding 43.2% of the United States apparel market share in 2025 with the higher frequency of purchase greater variety in clothing categories and strong cultural emphasis on fashion, as a form of self-expression. Women typically own larger wardrobes and engage in more frequent shopping trips compared to men and children. According to the Bureau of Labor Statistics, women spend approximately 30% more on apparel and services than men reflecting this higher engagement level. The diverse range of occasions requiring specific attire such as work leisure social events and fitness activities. The influence of social media and fashion influencers heavily targets female demographics creating constant demand for new styles and trends. The expansion of size inclusive ranges has also broadened the market reach ensuring that women of all body types have access to fashionable options. Additionally, the rise of athleisure has blurred the lines between casual and active wear encouraging multiple purchases for versatile use. Women are also more likely to respond to promotional offers and seasonal sales driving volume sales. The emotional connection between clothing and identity fosters brand loyalty and repeat purchases.

The sportswear segment is expected to grow at an anticipated CAGR of 8.6% from 2026 to 2034 with the increasing integration of athletic wear into daily lifestyles and the rising participation in fitness activities. The athleisure trend, which has normalized the wearing of sports inspired clothing in non-athletic settings, such as offices and social gatherings. As per the study, over 50% of Americans participate in some form of physical activity regularly creating a steady demand for performance apparel. The sales of athletic footwear and apparel have outpaced traditional clothing categories due to their comfort and versatility. The health and wellness movement encourages consumers to invest in high quality gear that supports active lifestyles. Major brands are innovating with sustainable materials and advanced technologies, such as moisture wicking and temperature regulation enhancing product appeal. The influence of celebrity endorsements and fitness influencers on social media further drives demand among younger demographics. The shift toward remote work has also increased the preference for comfortable clothing over formal business attire. Additionally, the expansion of women’s sportswear lines addressing specific biomechanical needs has unlocked new growth opportunities.

By Distribution Channel Insights

The offline segment was accounted in holding 56.2% of the United States apparel market share in 2025 with the consumer preference for tactile evaluation fit assessment and immediate possession of products. Physical stores, including department stores specialty boutiques and outlet malls provide a sensory shopping experience that online channels cannot fully replicate. The primary ability to try on clothes before purchasing which reduces the likelihood of returns and increases customer satisfaction. As per data from the International Council of Shopping Centers mall traffic has stabilized with consumers seeking social and experiential shopping environments. The presence of knowledgeable staff who offer styling advice and personalized service enhances the overall shopping journey. Immediate gratification allows shoppers to take home their purchases instantly avoiding shipping delays and costs. Retailers have invested in omnichannel strategies such as buy online pick up in store to bridge the gap between digital and physical channels. The visual merchandising and in store promotions create impulse buying opportunities that drive sales. Furthermore, the return process is often perceived as easier and faster in physical stores.

The online segment is projected to witness a significant CAGR of 10.5% from 2026 to 2034 with the convenience of home delivery extensive product selection and advanced digital tools. E-commerce platforms allow consumers to browse thousands of styles and compare prices effortlessly from any location. The e-commerce sales continue to capture an increasing share of total retail revenue with apparel being a top category. The improvement in logistics and return policies, which have reduced the friction associated with online shopping is also bolstering the growth of the segment. The mobile commerce has surged as smartphones become the primary device for browsing and purchasing clothing. Virtual try on technologies and augmented reality features help mitigate the inability to physically test items increasing consumer confidence. Direct to consumer brands leverage social media marketing to reach targeted audiences effectively bypassing traditional retail intermediaries. Subscription services and personalized recommendations enhance customer retention and lifetime value. The ability to access global brands and niche products not available locally expands consumer choices. Additionally, the ease of price comparison and access to reviews empowers shoppers to make informed decisions. This digital convenience combined with technological innovation ensures that the online segment continues to grow rapidly.

COMPETITIVE LANDSCAPE

The competitive landscape of the United States apparel market is characterized by intense rivalry among established global corporations and agile direct to consumer brands. Large players leverage strong brand equity and extensive distribution networks to maintain dominance while smaller brands compete on niche appeal and speed. Price competition is fierce in the mass market segment whereas premium brands compete on quality and exclusivity. The rise of e commerce has lowered barriers to entry allowing new entrants to gain traction quickly. Consumer loyalty is increasingly fragmented as shoppers prioritize style and value over brand heritage alone. Retailers play a crucial role by curating assortments that balance popular staples with trending items. Intellectual property protection is vital as counterfeiting remains a persistent issue. Companies must adapt rapidly to changing consumer preferences and technological advancements. Success depends on balancing innovation with operational efficiency and strong brand storytelling.

KEY MARKET PLAYERS

A few of the market players that are dominating the U.S apparel market are

- Lululemon Athletica

- Burberry Group plc

- TJX Companies Inc

- Gap Inc

- Puma SE

- Adidas AG

- Nike Inc.

- VF Corporation

- H & M Hennes & Mauritz AB

- LVMH

- Kering Group

- PVH Corp.

- Inditex

Top Players In The Market

- Nike Inc maintains its leadership position in the United States apparel market through continuous innovation in performance wear and strong brand storytelling. The company focuses on developing proprietary fabrics and sustainable materials that enhance athlete performance while appealing to eco conscious consumers. Recent actions include expanding its direct to consumer digital platforms which allow for personalized shopping experiences and exclusive product releases. Nike has also invested heavily in membership programs that drive loyalty and repeat purchases. Collaborations with high profile athletes and celebrities keep the brand culturally relevant and desirable among younger demographics. These strategies ensure Nike remains at the forefront of both performance and lifestyle segments in the competitive US market.

- VF Corporation exerts significant influence through its diverse portfolio of iconic brands including The North Face Vans and Timberland. The firm focuses on outdoor and active lifestyle segments where it commands strong loyalty among adventure enthusiasts and urban youth. Recent strategies involve enhancing sustainability initiatives by using recycled materials and reducing carbon footprints across its supply chain. VF Corporation has optimized its distribution network by prioritizing direct to consumer channels to improve margins and customer engagement. The company leverages data analytics to understand consumer preferences and tailor product offerings effectively. Investments in digital marketing and social media campaigns help maintain brand visibility and relevance.

- Gap Inc contributes to the market through its portfolio of accessible brands such as Old Navy Gap and Banana Republic. The company focuses on providing versatile and affordable clothing for families and individuals across various demographics. Recent actions include revitalizing its brand identity with modern designs and inclusive sizing to appeal to contemporary shoppers. Gap Inc has strengthened its e commerce capabilities by improving online user interfaces and offering flexible pickup options. The firm actively promotes diversity and inclusion in its marketing campaigns resonating with modern consumers. Investments in supply chain efficiency have reduced lead times and improved inventory management. These initiatives help the company compete effectively against fast fashion rivals and specialty retailers in the US market.

Top Strategies Used by Key Market Participants

Key players in the United States apparel market employ diverse strategies to maintain competitive advantage and drive growth. Product innovation remains central with companies developing sustainable materials and performance driven fabrics. Brands focus on direct to consumer channels by enhancing digital platforms and offering personalized shopping experiences. Strategic collaborations with influencers and celebrities help generate hype and cultural relevance. Sustainability initiatives are increasingly important as consumers demand ethically sourced and eco friendly products. Companies leverage data analytics to optimize inventory and predict trends accurately. Omnichannel integration ensures seamless experiences between online and physical stores. Limited edition releases create scarcity and drive urgency among consumers. Marketing campaigns emphasize storytelling and community engagement to build emotional connections.

MARKET SEGMENTATION

This research report on the U.S apparel market is segmented and sub-segmented into the following categories.

By Category

- Mass

- Premium

- Luxury

By End Use

- Women

- Casual Wear

- Formal Wear

- Sportswear

- Night Wear

- Inner Wear

- Ethnic Wear

- Others

- Men

- Casual Wear

- Formal Wear

- Sportswear

- Night Wear

- Inner Wear

- Ethnic Wear

- Others

- Children

- Casual Wear

- Formal Wear

- Sportswear

- Night Wear

- Inner Wear

- Ethnic Wear

- Others

By Distribution Channel

- Offline

- Supermarkets & Hypermarkets

- Clothing Stores

- Others

- Online

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States