U.S. Biopharmaceuticals Market Size, Share, Trends & Growth Forecast Report Segmented By Type (Immunomodulators, Enzymes, Vaccines, Hormones, Others), Application, Distribution Channel and Country – Industry Analysis From 2026 to 2034

U.S. Biopharmaceuticals Market Report Summary

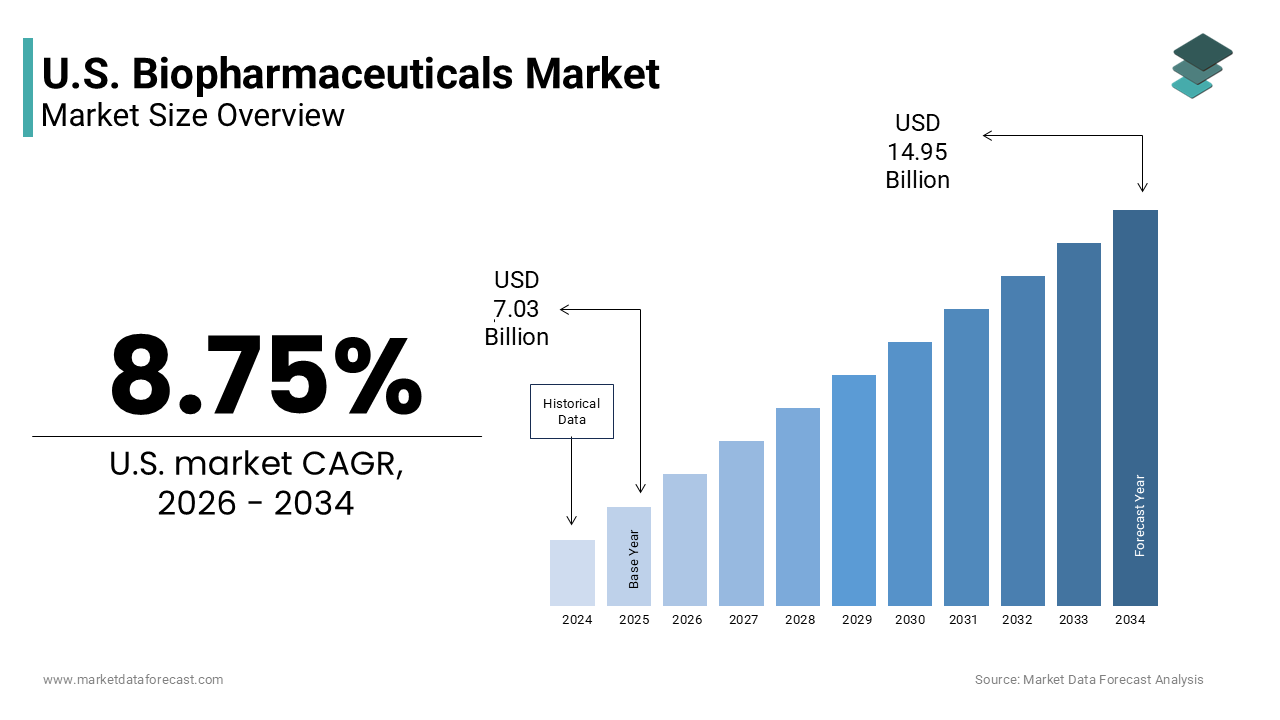

The U.S. biopharmaceuticals market was valued at USD 7.03 billion in 2025, is estimated to reach USD 7.63 billion in 2026, and is projected to reach USD 14.95 billion by 2034, growing at a CAGR of 8.75% during the forecast period from 2026 to 2034. The growth of the U.S. biopharmaceuticals market is driven by the rising prevalence of chronic and rare diseases, rapid advancements in genomic medicine, and increasing adoption of personalized therapies. Expanding investments in biologics research and development, growing demand for targeted therapeutics, and increasing regulatory support for innovative biological products are further accelerating market growth. Moreover, advancements in artificial intelligence-driven drug discovery, expansion of biosimilar development, and growing focus on precision medicine are supporting the expansion of the U.S. biopharmaceuticals market.

Key Market Trends

- Rising adoption of personalized medicine and genomic-based therapies for the treatment of complex and chronic diseases.

- Growing integration of artificial intelligence and machine learning technologies in drug discovery and clinical development processes.

- Increasing focus on advanced biologics including monoclonal antibodies, cell therapies, and gene therapies.

- Strong emphasis on biosimilar development to reduce healthcare costs and improve patient access to biologic treatments.

- Expansion of self-administered biologics and digital health-enabled treatment solutions for home-based care settings.

Segmental Insights

- Based on type, the immunomodulators segment dominated the U.S. biopharmaceuticals market and held the largest share in 2025. The segment’s dominance is attributed to the high prevalence of autoimmune and inflammatory disorders, increasing utilization of biologic therapies for rheumatoid arthritis and inflammatory bowel disease, and strong clinical efficacy of monoclonal antibody treatments.

- The vaccines segment is projected to witness the fastest CAGR during the forecast period owing to advancements in mRNA and viral vector technologies, increasing focus on preventive healthcare, and growing investments in next-generation vaccine development for infectious and chronic diseases.

- Based on application, the oncology segment accounted for the leading share of the U.S. biopharmaceuticals market in 2025. The dominance of this segment is driven by the rising incidence of cancer, increasing adoption of targeted biologics and immunotherapies, and growing demand for advanced oncology treatment solutions.

- The respiratory segment is anticipated to register notable growth during the forecast period due to the increasing prevalence of chronic respiratory diseases such as asthma and chronic obstructive pulmonary disease, along with rising adoption of biologic therapies targeting inflammatory respiratory conditions.

- Based on distribution channel, the hospital pharmacies segment held the major share of the U.S. biopharmaceuticals market in 2025 owing to the clinical requirement for administration of complex intravenous biologics, strong reimbursement support, and centralized procurement systems within healthcare institutions.

- The online pharmacies segment is expected to witness rapid growth during the forecast period because of increasing availability of self-administered biologics, rising preference for home healthcare services, and growing digital integration within pharmaceutical distribution systems.

Regional Insights

The United States dominated the North American biopharmaceuticals market and accounted for a major share in 2025, supported by its advanced research infrastructure, strong regulatory environment, and high healthcare expenditure. California remains a major contributor to the U.S. biopharmaceuticals market due to its strong biotechnology ecosystem, high concentration of research institutions, and increasing investments in biologics innovation. New York, Washington, and Oregon are also witnessing notable growth driven by expanding clinical research activities, increasing adoption of precision medicine, and rising healthcare investments in advanced therapeutics.

Competitive Landscape

The U.S. biopharmaceuticals market is highly competitive and characterized by the presence of multinational pharmaceutical corporations, biotechnology innovators, and specialized biologics manufacturers competing through scientific innovation, strategic collaborations, and pipeline expansion. Leading companies are focusing on advancing biologic drug discovery platforms, strengthening manufacturing capabilities, investing in artificial intelligence technologies, and expanding cell and gene therapy portfolios. Strategic acquisitions, licensing agreements, and investments in advanced biologics manufacturing technologies are further strengthening market positioning across multiple therapeutic areas. Prominent players in the U.S. biopharmaceuticals market include Pfizer Inc., Johnson & Johnson, Eli Lilly and Company, Merck & Co., Inc., AbbVie Inc., Amgen Inc., Bristol-Myers Squibb, Gilead Sciences, Biogen Inc., Regeneron Pharmaceuticals, Moderna Inc., Vertex Pharmaceuticals, AstraZeneca, Novartis AG, and F. Hoffmann-La Roche Ltd.

U.S. Biopharmaceuticals Market Size

The U.S. Biopharmaceuticals Market size was valued at USD 7.03 billion in 2025 and is anticipated to reach USD 7.63 billion in 2026 from USD 14.95 billion by 2034, growing at a CAGR of 8.75% during the forecast period from 2026 to 2034.

According to the Food and Drug Administration, the agency approved 55 novel drugs in 2023, with biologics accounting for a significant proportion of these approvals, reflecting the sector's innovation momentum. As per the National Institutes of Health, federal funding for biomedical research exceeded 47 billion dollars in fiscal year 2024, which is supporting foundational discoveries that translate into commercial therapies. According to the Centers for Disease Control and Prevention, chronic diseases affect 60% of U.S. adults, driving demand for targeted biological interventions that offer superior efficacy over traditional small molecule drugs. Regulatory frameworks such as the Biologics Price Competition and Innovation Act facilitate the introduction of biosimilars, enhancing accessibility while maintaining rigorous safety standards through post marketing surveillance. The integration of advanced manufacturing technologies like continuous bioprocessing and single use systems further defines the operational landscape. This ecosystem is characterized by high research and development intensity lengthy clinical trial timelines and substantial capital requirements distinguishing it from conventional pharmaceutical sectors and positioning it as a critical pillar of modern healthcare infrastructure.

MARKET DRIVERS

Rising Prevalence of Chronic and Rare Diseases Fuels Therapeutic Demand

The rising burden of chronic and rare diseases in the United States is primarily fuelling the expansion of the U.S. biopharmaceuticals market. According to the Centers for Disease Control and Prevention, chronic conditions such as heart disease, cancer, and diabetes account for 90% of the nation's 4.1 trillion dollars in annual healthcare costs. As per the National Organization for Rare Disorders, approximately 25 to 30 million Americans suffer from one of more than 7,000 identified rare diseases, creating a substantial unmet medical need. Biopharmaceuticals offer targeted mechanisms of action that address the underlying pathology of these complex conditions, often providing treatment options where none previously existed. The approval of orphan drug designations by the Food and Drug Administration has incentivized development, with over 50% of novel drug approvals receiving this status or priority review in recent years. Furthermore, the aging population exacerbates disease prevalence; with the U.S. Census Bureau projecting that individuals aged 65 and older will comprise nearly 23% of the population by 2050. This demographic shift increases the incidence of age related disorders such as Alzheimer's disease and osteoarthritis, which are key targets for biologic therapies. Clinical data demonstrates that biologics significantly improve quality of life and reduce hospitalization rates for patients with severe autoimmune conditions. Consequently, the convergence of high disease burden, demographic trends, and therapeutic efficacy drives sustained demand for innovative biopharmaceutical solutions.

Advancements in Genomic Medicine and Personalized Therapies Accelerate Innovation

Rapid progress in genomic sequencing and personalized medicine is further contributing to the U.S. biopharmaceuticals market growth. According to the National Human Genome Research Institute, the cost of sequencing a human genome has dropped from nearly 100 million dollars in 2001 to under 1,000 dollars today, enabling widespread application in clinical settings. As per the Precision Medicine Initiative launched by the National Institutes of Health, over 1 million volunteers have contributed data to support the development of tailored treatments based on individual genetic profiles. Biopharmaceutical companies leverage this data to identify novel biomarkers and develop therapies that target specific patient subgroups, enhancing efficacy and minimizing adverse effects. The Food and Drug Administration has approved numerous companion diagnostics alongside biologic drugs, ensuring that treatments are administered to those most likely to benefit. For instance, CAR T cell therapies for cancer rely on modifying a patient's own immune cells, requiring sophisticated biopharmaceutical manufacturing capabilities. Industry analyses indicate that personalized biologics command premium pricing due to their high value proposition in treating refractory diseases. Furthermore, investments in artificial intelligence and machine learning accelerate drug discovery by predicting protein structures and identifying potential drug candidates more efficiently. This technological synergy between genomics, data analytics, and biologic engineering creates a robust environment for continuous innovation and market expansion.

MARKET RESTRAINTS

Stringent Regulatory Requirements and Prolonged Approval Timelines

The rigorous regulatory framework governing biopharmaceutical development in the United States presents a significant barrier to the U.S. biopharmaceuticals market growth. According to the Food and Drug Administration, the average time required to approve a new biologic application, spanning from initial laboratory discovery through all clinical phases to final market launch, typically takes over 10 to 12 years. As per the Tufts Center for the Study of Drug Development, the average capitalized cost to develop and bring a new medicine to market is estimated at 2.6 billion dollars, reflecting the extensive clinical trials and manufacturing validation required. Regulatory agencies mandate comprehensive data on safety, efficacy, purity, and potency, including long term follow up studies for gene and cell therapies, which can extend development timelines further. The complexity of biologics necessitates specialized manufacturing facilities that must adhere to current good manufacturing practices, adding layers of compliance oversight. Any deviation in production processes can result in clinical holds or rejection of applications, causing substantial financial losses. Furthermore, the requirement for Risk Evaluation and Mitigation Strategies for certain high risk biologics imposes additional operational burdens on manufacturers. These regulatory hurdles discourage smaller biotechnology firms with limited resources from advancing promising candidates through late stage trials. Consequently, the prolonged approval process delays patient access to innovative therapies and increases the financial risk for investors, potentially stifling innovation in the sector.

High Manufacturing Complexity and Supply Chain Vulnerabilities

The intricate nature of biopharmaceutical manufacturing and associated supply chain fragilities constrain the U.S. biopharmaceuticals market expansion. According to the Biotechnology Innovation Organization, producing biologics requires living cells that are sensitive to environmental conditions, making the process far more complex than synthesizing small molecule drugs. As per industry reports, a single batch failure in biomanufacturing can result in losses exceeding 10 million dollars due to the lengthy production cycles and strict quality controls. The reliance on specialized raw materials such as cell culture media and single use resins creates vulnerabilities, particularly when sourcing from limited global suppliers. The COVID 19 pandemic exposed these weaknesses, with disruptions in the supply of critical components leading to production delays for various therapies. Furthermore, the need for cold chain logistics to maintain product stability during distribution adds significant cost and logistical challenges. According to the International Society for Pharmaceutical Engineering, temperature excursions during transport can compromise product integrity, resulting in wasted inventory and potential shortages. The lack of standardized manufacturing platforms across different biologics further complicates scalability and technology transfer. These operational complexities increase production costs and limit the ability of manufacturers to rapidly scale up output in response to surging demand. Consequently, supply chain instability and manufacturing difficulties remain persistent restraints affecting market consistency and accessibility.

MARKET OPPORTUNITIES

Expansion of Biosimilars and Interchangeable Products

The growing adoption of biosimilars is a substantial opportunity for market expansion and cost reduction in the U.S. healthcare system. According to the Food and Drug Administration, over 40 biosimilar products have been approved to date, with many more in the development pipeline targeting high revenue biologics. As per the Congressional Budget Office, the increased utilization of biosimilars was projected to save billions of dollars for the federal government and private insurers over a multi year period. The expiration of patents for blockbuster biologics such as adalimumab and trastuzumab opens lucrative markets for competitors offering lower cost alternatives. Regulatory pathways for interchangeability allow pharmacists to substitute biosimilars for reference products without prescriber intervention, further accelerating uptake. Healthcare systems are increasingly incorporating biosimilars into formularies to manage rising drug expenditures while maintaining quality of care. According to the Association for Accessible Medicines, biosimilars have already generated over 10 billion dollars in savings for U.S. patients and payers. Furthermore, emerging markets in Asia and Europe provide export opportunities for U.S. based manufacturers leveraging established production capabilities. The development of next generation biosimilars with improved delivery devices or formulation stability offers additional competitive advantages. This shift toward cost effective biological therapies aligns with value based care models and supports sustainable healthcare financing, creating a favorable environment for biosimilar developers.

Integration of Artificial Intelligence in Drug Discovery and Development

The incorporation of artificial intelligence and machine learning into biopharmaceutical research offers promising opportunities for the U.S. biopharmaceuticals market. According to the National Institutes of Health, AI algorithms can analyze vast datasets to identify novel drug targets and predict molecular interactions with unprecedented speed and accuracy. As per industry analyses, AI driven drug discovery can reduce the initial identification phase from several years to mere months, significantly lowering early stage development costs. Companies are leveraging AI to optimize clinical trial designs by selecting appropriate patient populations and predicting outcomes, thereby increasing the likelihood of regulatory approval. The Food and Drug Administration has established initiatives to evaluate AI based tools in regulatory decision making, fostering a supportive environment for digital innovation. Furthermore, AI enhances manufacturing processes by monitoring real time data to predict equipment failures and optimize yield, reducing waste and improving consistency. According to McKinsey and Company, AI applications could generate up to 100 billion dollars in annual value for the pharmaceutical industry through improved productivity and successful launches. The collaboration between tech firms and biopharmaceutical companies accelerates the translation of computational insights into tangible therapies. This technological integration not only streamlines operations but also enables the development of complex biologics that were previously inaccessible, expanding the therapeutic horizon.

MARKET CHALLENGES

Pricing Pressure and Reimbursement Uncertainties

Intense pricing pressure and evolving reimbursement landscapes pose significant challenges to the U.S. biopharmaceuticals market growth. According to the Kaiser Family Foundation, specialty drugs, including biologics, often cost thousands of dollars annually per patient, placing a substantial burden on insurance plans and government programs. As per the Inflation Reduction Act, Medicare is now empowered to negotiate prices for certain high expenditure drugs, directly impacting revenue projections for manufacturers. Pharmacy benefit managers frequently impose restrictive formulary placements and prior authorization requirements, limiting patient access and delaying treatment initiation. The lack of transparency in rebate negotiations further complicates pricing strategies, forcing companies to offer significant discounts to secure coverage. According to the Pharmaceutical Research and Manufacturers of America, net prices for many biologics have declined despite increases in list prices due to these hidden rebates. Furthermore, state level initiatives aimed at capping out of pocket costs for insulin and other biologics add regulatory complexity. Payers are increasingly demanding real world evidence to justify premium pricing, requiring manufacturers to invest in post marketing studies. This economic environment squeezes profit margins and discourages investment in high risk therapeutic areas. Consequently, manufacturers must navigate a fragmented and contentious pricing ecosystem that threatens long term sustainability and innovation incentives.

Intellectual Property Disputes and Patent Litigation

Complex intellectual property disputes and extensive patent litigation are further challenging the U.S. market expansion. According to the Federal Trade Commission, originator companies often file multiple secondary patents covering manufacturing processes, formulations, and uses to extend market exclusivity beyond the core patent expiration. As per industry data, patent litigation involving biologics can last five to seven years, consuming significant legal resources and delaying market entry for competitors. The Biologics Price Competition and Innovation Act mandates a period of patent dance negotiations, which frequently results in protracted legal battles rather than timely resolutions. Small biotechnology firms lacking robust legal teams are particularly vulnerable to infringement claims that can halt development or force unfavorable settlements. Furthermore, the ambiguity surrounding patent eligibility for natural biological phenomena and diagnostic methods creates uncertainty for innovators. According to the Supreme Court, rulings on patent subject matter have narrowed the scope of protectable inventions, affecting investment decisions. The threat of litigation also deters collaboration and licensing agreements, as parties fear future disputes. These legal complexities increase the cost of doing business and delay the availability of affordable alternatives. Consequently, the intellectual property landscape remains a formidable challenge that impedes competition and slows the pace of therapeutic advancement in the U.S. market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 8.75% |

| Segments Covered | By Type, Application, Distribution Channel and Region. |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | California, Washington, Oregon, New York, and the rest of the United States. |

| Market Leaders Profiled | Pfizer Inc., Johnson & Johnson, Eli Lilly and Company, Merck & Co., Inc., AbbVie Inc., Amgen Inc., Bristol-Myers Squibb, Gilead Sciences, Biogen Inc., Regeneron Pharmaceuticals, Moderna Inc., Vertex Pharmaceuticals, AstraZeneca, Novartis AG, and F. Hoffmann-La Roche Ltd. |

SEGMENTAL ANALYSIS

By Type Insights

The immunomodulators segment dominated the market by holding 41.4% of the U.S. market share in 2025. The substantial burdens of autoimmune and chronic inflammatory disorders in the United States are driving the dominance of immunomodulators segment in the U.S. market. According to the Centers for Disease Control and Prevention, autoimmune diseases affect approximately 24 million Americans, with conditions such as rheumatoid arthritis, psoriasis, and inflammatory bowel disease requiring long term biological intervention. As per the American College of Rheumatology, over 1.3 million adults in the United States have rheumatoid arthritis, a condition that frequently necessitates treatment with tumor necrosis factor inhibitors and other monoclonal antibodies. The chronic nature of these diseases ensures consistent demand for therapeutic agents that modulate immune responses to prevent tissue damage and alleviate symptoms. Clinical guidelines strongly recommend biologic immunomodulators for patients who do not respond to conventional therapies, driving widespread adoption. According to the Crohn s and Colitis Foundation, approximately 3 million Americans suffer from inflammatory bowel disease, with many relying on interleukin inhibitors for remission maintenance. The high efficacy of these agents in reducing disease activity and improving quality of life reinforces their position as standard of care. Furthermore, the expansion of indications for existing immunomodulators into new patient populations continues to broaden their market reach. This convergence of high disease prevalence, robust clinical evidence, and established treatment protocols creates enduring momentum for the immunomodulator segment.

On the other side, the vaccines segment is predicted to register a CAGR of 17.4% during the forecast period in the U.S. market owing to the technological advancements in mRNA platforms and increased focus on preventive health. The emergence of messenger RNA and viral vector technologies has revolutionized vaccine development, driving exceptional growth in this segment. According to the National Institutes of Health, mRNA vaccines can be designed and produced rapidly in response to emerging pathogens, offering a significant advantage over traditional egg based methods. As per the Centers for Disease Control and Prevention, the successful deployment of mRNA vaccines during the pandemic demonstrated their efficacy and safety, paving the way for applications against influenza, respiratory syncytial virus, and other infectious diseases. The flexibility of these platforms allows for quick updates to address viral variants, ensuring sustained protection. Furthermore, viral vector vaccines provide robust immune responses by delivering genetic material into cells using harmless viruses. According to the Biomedical Advanced Research and Development Authority, federal investments exceeding 2 billion dollars support the development of next generation vaccine technologies. These innovations enable the creation of vaccines for previously untreatable conditions such as HIV and malaria. The ability to combine multiple antigens into single formulations also enhances convenience and coverage. This technological versatility, combined with proven clinical success, positions vaccines as the fastest growing segment in the U.S. biopharmaceuticals market.

By Application Insights

The oncology segment led the market by holding the highest share of the U.S. biopharmaceuticals market in 2025. The growth of the oncology segment in the U.S. market is attributed to the high incidence of cancer and the critical role of biologics in treatment protocols. This segment includes therapies for breast, lung, colorectal, and hematologic malignancies. The pervasive burden of cancer in the United States significantly propels the dominance of the oncology application segment in the U.S. market. According to the American Cancer Society, approximately 2 million new cancer cases are diagnosed annually in the United States, with cancer remaining the second leading cause of death. As per the National Cancer Institute, over 600,000 Americans die from cancer each year, creating an urgent need for effective therapeutic interventions. Biopharmaceuticals such as monoclonal antibodies and antibody drug conjugates have become standard of care for many cancer types, offering superior survival outcomes compared to traditional chemotherapy. The approval of targeted therapies for specific genetic mutations has transformed treatment landscapes for diseases like non small cell lung cancer and melanoma. According to the Surveillance, Epidemiology, and End Results program, the five year relative survival rate for all cancers combined has increased to over 69%, reflecting the impact of advanced biologics. Furthermore, the aging population contributes to higher cancer incidence, with the majority of diagnoses occurring in individuals aged 65 and older. This demographic trend ensures sustained demand for oncology biologics. The high cost of these therapies is offset by their ability to extend life and improve quality of life, justifying their central role in healthcare spending.

On the other side, the respiratory application segment is estimated to progress at a CAGR of 14.4% in the U.S. market during the forecast period owing to the rising prevalence of chronic respiratory diseases and recent therapeutic breakthroughs. The increasing burden of chronic respiratory conditions significantly drives expansion in this segment. According to the Centers for Disease Control and Prevention, approximately 14 million adults in the United States have been diagnosed with chronic obstructive pulmonary disease, while over 24 million have asthma. As per the American Lung Association, chronic lower respiratory diseases are a leading cause of death in the United States, highlighting the severity of the health crisis. Biopharmaceuticals such as monoclonal antibodies targeting interleukins have transformed the management of severe asthma and eosinophilic conditions. These agents reduce exacerbation rates and hospitalizations, improving patient outcomes and reducing overall healthcare costs. The aging population is particularly susceptible to respiratory decline, with smoking history and environmental exposures contributing to disease progression. According to the Global Initiative for Chronic Obstructive Lung Disease guidelines, biologics are increasingly recommended for patients with frequent exacerbations despite standard therapy. Furthermore, the recognition of asthma as a heterogeneous disease has led to personalized treatment approaches using specific biologics. This shift toward precision medicine enhances efficacy and patient satisfaction. The availability of self-injectable formats improves adherence and convenience. Consequently, the respiratory segment benefits from a large and growing patient population requiring advanced biological therapies.

By Distribution Channel Insights

The hospital pharmacies segment captured the largest share of 54.6% of the U.S. market in 2025. The growth of the hospital pharmacies segment in the U.S. market can be credited to the necessity for professional administration of complex intravenous biopharmaceuticals. According to the American Hospital Association, thousands of hospitals in the United States operate specialized infusion centers equipped to handle high risk biological products. As per the Centers for Medicare and Medicaid Services, Medicare Part B covers drugs administered in hospital outpatient departments, providing a reliable reimbursement mechanism for expensive biologics. Many oncology and autoimmune therapies require careful monitoring for infusion reactions and adverse events, which can only be safely managed in clinical settings. This logistical requirement ensures that hospitals remain the primary distribution channel for these high value products. Furthermore, hospital pharmacy and therapeutics committees play a critical role in evaluating and selecting biologics for formulary inclusion, ensuring standardized use across the institution. According to Premier Inc. supply chain data, hospital group purchasing organizations negotiate substantial discounts for biologics, leveraging volume to secure favorable pricing. The integration of biologics into electronic health records and order sets facilitates seamless prescribing and administration. This combination of clinical necessity, regulatory compliance, and procurement efficiency creates enduring momentum for hospital pharmacies as the leading distribution channel.

On the other side, the online pharmacy segment is predicted to expand at a CAGR of 19.4% during the forecast period in the U.S. market owing to the shift towards self administered subcutaneous biologics and digital health integration. The increasing availability of biopharmaceuticals formulated for subcutaneous self administration significantly drives expansion in the online pharmacy channel. According to the National Community Pharmacists Association, a substantial majority of independent community pharmacies offer some form of home delivery services. As per industry data, biologics for conditions such as rheumatoid arthritis and multiple sclerosis are increasingly available in pre filled syringes or auto injectors that patients can administer at home. This convenience reduces the need for frequent hospital visits and aligns with patient preferences for autonomy and comfort. Online pharmacies play a crucial role in educating patients on proper injection techniques and storage requirements, ensuring safe and effective use. According to the Centers for Disease Control and Prevention, pharmacist led education improves medication adherence and reduces errors associated with self administration. Furthermore, the expansion of biosimilar indications for self injection has broadened the customer base for online pharmacies. Insurance plans often prefer online distribution for self administered drugs due to lower overhead costs compared to hospital outpatient departments. According to the Pharmaceutical Research and Manufacturers of America, online pharmacy utilization for self administered therapies has shown continuous increases, reflecting this shifting trend. This convergence of product innovation, patient preference, and payer incentives creates powerful growth momentum for online pharmacies.

COUNTRY ANALYSIS

The United States biopharmaceutical sector is expected to maintain its global leadership position and experience steady clinical and commercial expansion for the next few years. This market leadership reflects the convergence of advanced research infrastructure, robust regulatory frameworks, and high healthcare expenditure that distinguishes the United States from international peers. The unparalleled research ecosystem and supportive regulatory environment in the United States significantly propel its market dominance. According to the National Institutes of Health, federal funding for biomedical research exceeds 47 billion dollars annually, supporting foundational discoveries that translate into commercial therapies. As per the Food and Drug Administration, the agency maintains a rigorous yet efficient approval process for biologics, ensuring high standards for safety and efficacy while facilitating innovation. The United States boasts the highest number of biopharmaceutical companies and clinical trials globally, with over 40% of all new molecular entities originating from U.S. based research. According to the Biotechnology Innovation Organization, the sector employs over 1.8 million people and attracts significant venture capital investment, fostering a dynamic innovation hub. The presence of world class academic institutions and teaching hospitals facilitates collaboration between researchers and clinicians, accelerating the translation of scientific breakthroughs into treatments. Furthermore, the Orphan Drug Act and other legislative incentives encourage development of therapies for rare diseases, expanding the therapeutic portfolio. According to the Pharmaceutical Research and Manufacturers of America, the United States accounts for the largest share of global biopharmaceutical patents and publications. This combination of financial support, regulatory clarity, and scientific excellence ensures that the United States remains the central hub for biopharmaceutical development and commercialization.

COMPETITIVE LANDSCAPE

The United States biopharmaceuticals market features intense competition among multinational pharmaceutical corporations specialized biotechnology firms and emerging innovators. Established players leverage extensive resources regulatory expertise and global distribution networks to maintain leadership while agile biotechs differentiate through novel mechanisms and targeted therapies. Competition centers on scientific innovation with companies investing billions in research and development to discover first in class biologics. Patent protection and intellectual property rights remain critical battlegrounds as firms seek to extend exclusivity periods for blockbuster drugs. Pricing pressures from payers and government programs force manufacturers to demonstrate superior clinical value and cost effectiveness. Strategic collaborations and licensing agreements are common as companies seek to fill pipeline gaps and share development risks. The rise of biosimilars adds competitive pressure on originator brands prompting differentiation through improved delivery devices and patient support services. Regulatory pathways for accelerated approval encourage rapid market entry for breakthrough therapies. This dynamic environment drives continuous advancement in therapeutic options ensuring patients benefit from the latest scientific discoveries while companies strive for sustainable growth and market relevance in a highly regulated landscape.

KEY MARKET PLAYERS

Some of the promising companies that are playing a dominating role in the U.S. Biopharmaceuticals Market include

- Pfizer Inc.

- Johnson & Johnson

- Eli Lilly and Company

- Merck & Co., Inc.

- AbbVie Inc.

- Amgen Inc.

- Bristol-Myers Squibb

- Gilead Sciences

- Biogen Inc.

- Regeneron Pharmaceuticals

- Moderna Inc.

- Vertex Pharmaceuticals

- AstraZeneca

- Novartis AG

Top Players in the U.S. Biopharmaceuticals market

Pfizer Inc

Pfizer Inc stands as a global leader in the United States biopharmaceutical sector with a diversified portfolio spanning oncology rare diseases and vaccines. The company leverages its extensive research and development capabilities to advance novel biologics including monoclonal antibodies and gene therapies. Pfizer recently strengthened its market position through strategic acquisitions such as Seagen to expand its oncology pipeline and enhance antibody drug conjugate technologies. The company actively collaborates with academic institutions and biotechnology firms to accelerate drug discovery and clinical development. Pfizer also invests heavily in manufacturing infrastructure to ensure reliable supply of complex biological products. These initiatives reinforce its commitment to delivering innovative therapies while maintaining operational excellence and regulatory compliance across diverse therapeutic areas.

Johnson and Johnson

Johnson and Johnson contributes significantly to the U.S. biopharmaceuticals market through its innovative medicines segment focusing on immunology oncology and neuroscience. The company utilizes advanced platforms to develop bispecific antibodies and cell therapies targeting high unmet medical needs. Johnson and Johnson recently expanded its immunology portfolio by launching new formulations for autoimmune conditions enhancing patient convenience and adherence. The company engages in strategic partnerships to integrate artificial intelligence into drug discovery processes improving efficiency and success rates. Furthermore Johnson and Johnson maintains robust clinical trial networks to generate real world evidence supporting product efficacy. These efforts strengthen its competitive stance by addressing complex disease mechanisms and delivering personalized treatment solutions to patients across the United States healthcare system.

Merck and Co

Merck and Co plays a pivotal role in the U.S. biopharmaceutical landscape with a strong focus on oncology vaccines and hospital acute care. The company is renowned for its flagship immuno oncology therapy which has transformed cancer treatment standards globally. Merck recently announced significant investments in manufacturing capacity to support the production of next generation biologics and conjugate vaccines. The company actively pursues collaborations with emerging biotech firms to license promising early stage assets and diversify its pipeline. Merck also emphasizes digital health integration to improve patient outcomes and streamline clinical data collection. Through sustained innovation and strategic expansion Merck reinforces its leadership in developing life saving biological medicines that address critical health challenges in the United States.

Top Strategies Used by Key Market Participants

Key players in the United States biopharmaceuticals market employ strategic approaches to maintain competitive advantages and drive growth. Companies prioritize mergers and acquisitions to acquire innovative pipelines and expand therapeutic portfolios rapidly. Strategic partnerships with academic institutions and biotechnology firms facilitate access to cutting edge research and novel platforms. Manufacturers invest heavily in advanced manufacturing technologies such as continuous bioprocessing to enhance efficiency and reduce costs. Regulatory engagement initiatives ensure streamlined approval processes and compliance with evolving safety standards. Digital transformation efforts integrate artificial intelligence and machine learning into drug discovery and clinical trials to accelerate development timelines. Market participants also focus on patient centric services including adherence programs and digital health tools to improve outcomes. These coordinated strategies enable companies to navigate complex regulatory environments while delivering high value biological therapies to diverse patient populations effectively.

MARKET SEGMENTATION

This research report on the U.S. biopharmaceuticals market has been segmented based on the following categories.

By Type

- Immunomodulators

- Enzymes

- Vaccines

- Hormones

- Others

By Application

- Cardiology

- Oncology

- Respiratory

- Immunology

- Neurology

- Others

By Distribution Channel

- Hospital Pharmacies

- Drug Stores & Retail Pharmacies

- Online Pharmacies

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com