U.S. Biosimilars Market Size, Share, Trends & Growth Forecast Report Segmented By Drug Class (Monoclonal Antibodies, Filgrastim & Pegfilgrastim, Others), Disease Indication and Country – Industry Analysis From 2026 to 2034

U.S. Biosimilars Market Report Summary

The U.S. biosimilars market was valued at USD 25.67 billion in 2025, is estimated to reach USD 35.67 billion in 2026, and is projected to reach USD 495.65 billion by 2034, growing at a CAGR of 38.95% during the forecast period from 2026 to 2034. The growth of the U.S. biosimilars market is driven by supportive legislative mandates, increasing healthcare cost containment initiatives, and rising prevalence of chronic diseases such as cancer, rheumatoid arthritis, and inflammatory bowel disease. Expanding physician acceptance of biosimilars, increasing Medicare reimbursement incentives, and growing availability of interchangeable biosimilar products are further accelerating market growth. Moreover, advancements in biologic manufacturing technologies, increasing demand for cost-effective biological therapies, and expanding home-based treatment solutions are supporting the expansion of the U.S. biosimilars market.

Key Market Trends

- Rising adoption of biosimilars in oncology and autoimmune disease treatment due to significant cost-saving potential.

- Increasing focus on interchangeable biosimilars that enable pharmacy-level substitution and improve patient access.

- Growing demand for self-administered biosimilars using pre-filled syringes and auto-injector delivery systems.

- Strong emphasis on physician education, patient support programs, and real-world evidence generation to improve confidence in biosimilar therapies.

- Expansion of strategic partnerships between manufacturers, payers, and healthcare providers to accelerate biosimilar adoption and formulary inclusion.

Segmental Insights

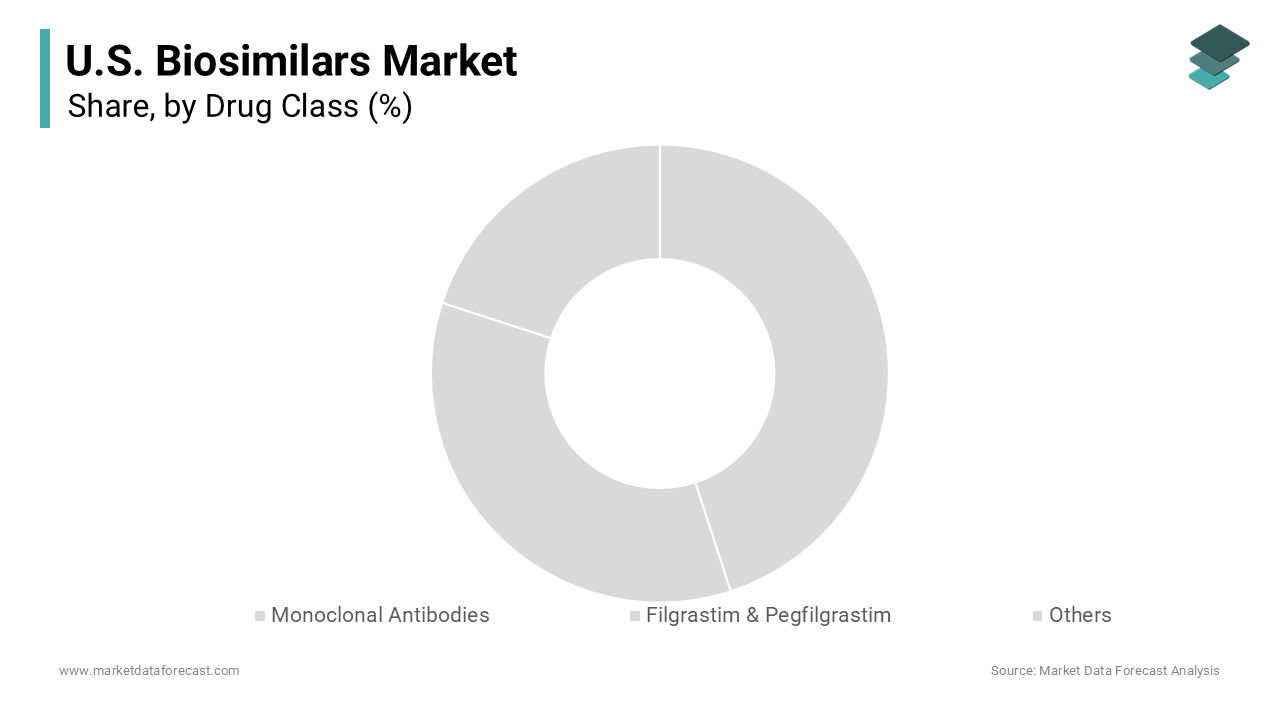

- Based on drug class, the monoclonal antibodies segment dominated the U.S. biosimilars market and held the largest share in 2025. The segment’s dominance is attributed to the high prevalence of cancer and autoimmune diseases, widespread use of monoclonal antibody therapies, and increasing patent expirations of blockbuster biologics.

- The filgrastim and pegfilgrastim segment is projected to witness the fastest CAGR during the forecast period owing to increasing cancer incidence, growing demand for chemotherapy supportive care therapies, and rising adoption of long-acting biosimilar formulations that improve patient convenience.

- Based on disease indication, the cancer segment accounted for the leading share of the U.S. biosimilars market in 2025. The dominance of this segment is driven by the high cost of oncology biologics, increasing demand for affordable cancer treatments, and growing utilization of biosimilars for breast cancer, lymphoma, and other oncology indications.

- The autoimmune diseases segment is anticipated to register notable growth during the forecast period due to the rising prevalence of rheumatoid arthritis, psoriasis, and inflammatory bowel disease, along with increasing availability of biosimilars targeting tumor necrosis factor inhibitors and other biologic therapies.

- Based on distribution channel, the hospital pharmacies segment held the major share of the U.S. biosimilars market in 2025 owing to centralized procurement systems, large-scale administration of intravenous biosimilars, and strong reimbursement support through hospital outpatient settings.

- The retail pharmacies segment is expected to witness rapid growth during the forecast period because of increasing availability of self-administered biosimilars, rising patient preference for home-based treatment, and expanding pharmacist-led patient education and support services.

Regional Insights

The United States dominated the North American biosimilars market and accounted for a major share in 2025, supported by a well-established regulatory framework, strong healthcare infrastructure, and increasing focus on reducing biologic treatment costs. California remains a major contributor to the U.S. biosimilars market due to its large patient population, strong biotechnology ecosystem, and high adoption of advanced biologic therapies. New York, Washington, and Oregon are also witnessing notable growth driven by increasing healthcare expenditure, expanding insurance coverage for biosimilars, and rising awareness regarding cost-effective treatment alternatives.

Competitive Landscape

The U.S. biosimilars market is highly competitive and characterized by the presence of multinational pharmaceutical companies, biotechnology firms, and specialized biosimilar developers competing through pricing strategies, interchangeability approvals, and product innovation. Leading companies are focusing on expanding biosimilar pipelines, strengthening manufacturing capabilities, investing in patient-centric delivery systems, and enhancing partnerships with healthcare providers and payers. Strategic collaborations, real-world evidence studies, and aggressive market access initiatives are further strengthening market positioning across multiple therapeutic categories. Prominent players in the U.S. biosimilars market include Pfizer Inc., Amgen Inc., Sandoz International GmbH, Samsung Bioepis, Celltrion Inc., Biocon Biologics, Teva Pharmaceutical Industries Ltd., Viatris Inc., Coherus BioSciences, AbbVie Inc., Novartis AG, F. Hoffmann-La Roche Ltd, Eli Lilly and Company, and Merck & Co., Inc.

U.S. Biosimilars Market Size

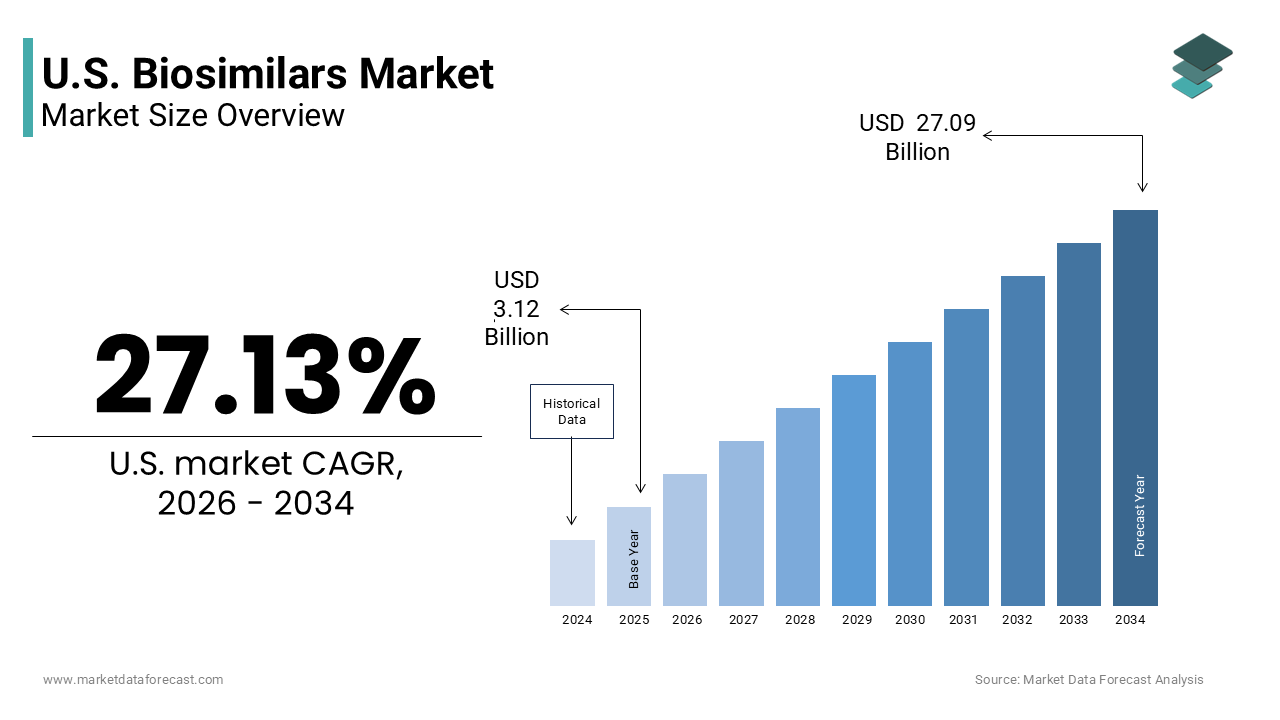

The U.S. biosimilars market size was valued at USD 3.12 billion in 2025 and is anticipated to reach USD 3.97 billion in 2026 from USD 27.09 billion by 2034, growing at a CAGR of 27.13% during the forecast period from 2026 to 2034.

According to the Food and Drug Administration, the agency has approved 53 biosimilar products as of early 2026, reflecting a maturing regulatory pathway established by the Biologics Price Competition and Innovation Act. As per the Centers for Medicare and Medicaid Services, biosimilars generated over 12 billion dollars in savings for the Medicare program between 2017 and 2024, demonstrating substantial economic impact on the healthcare system. The American Medical Association notes that biosimilars provide patients with increased access to life-saving treatments by reducing out-of-pocket costs and improving formulary availability. Clinical equivalence is rigorously evaluated through analytical studies, animal testing, and at least one clinical trial to ensure comparable efficacy and immunogenicity profiles. According to the Kaiser Family Foundation, the adoption of biosimilars has accelerated significantly in oncology and rheumatology sectors, where high-cost biologics historically limited patient access. This evolving landscape is characterized by increasing physician confidence, expanded insurance coverage, and strategic initiatives by manufacturers to differentiate products through delivery devices and patient support programs.

MARKET DRIVERS

Legislative Mandates and Reimbursement Policies Accelerate Market Adoption

Federal and state-level legislative frameworks actively promote the utilization of biosimilars to curb escalating healthcare expenditures and enhance patient accessibility, which is one of the major factors driving the growth of the U.S. biosimilars market. According to the Inflation Reduction Act enacted in 2022, Medicare Part B payment rates for biosimilars were adjusted to provide a minimum add-on payment of 8% of the average sales price, which incentivizes providers to prescribe these lower-cost alternatives. As per data from the Centers for Medicare and Medicaid Services, this policy change resulted in a substantial increase in biosimilar prescribing volume within the first year of implementation among participating healthcare facilities. State laws further reinforce this trend by requiring pharmacy benefit managers to pass through rebates and discounts to patients, thereby reducing financial barriers to adoption. The Department of Health and Human Services reports that nearly all states have enacted biosimilar substitution laws that allow pharmacists to dispense biosimilars in place of reference products without prescriber intervention, provided specific notification requirements are met. These regulatory mechanisms create a favorable economic environment that encourages healthcare systems to integrate biosimilars into standard treatment protocols. Additionally, federal procurement policies prioritize biosimilars for government-funded health programs, amplifying demand across public sector institutions. This comprehensive legislative support structure drives sustained market growth by aligning financial incentives with clinical decision-making processes.

Rising Prevalence of Chronic Diseases Increases Demand for Cost Effective Therapies

The escalating burden of chronic conditions such as cancer, rheumatoid arthritis, and inflammatory bowel disease creates substantial demand for affordable biological therapies in the United States, which is further boosting the U.S. market expansion. According to the National Cancer Institute, approximately 2 million new cancer cases are diagnosed annually in the United States, with many patients requiring expensive biologic treatments like monoclonal antibodies. As per the Centers for Disease Control and Prevention, more than 50 million adults suffer from doctor-diagnosed arthritis, a significant portion of whom rely on biologic disease-modifying antirheumatic drugs for symptom management. The high cost of reference biologics often limits patient access, leading to delayed treatment initiation or non-adherence, which exacerbates disease progression and increases overall healthcare costs. Biosimilars offer a viable solution by providing equivalent clinical outcomes at reduced prices, thereby expanding access to essential therapies. According to the Arthritis Foundation, the introduction of biosimilars for tumor necrosis factor inhibitors has reduced annual treatment costs by up to 30%, enabling more patients to initiate and maintain therapy. Furthermore, the aging population contributes to increased incidence of chronic diseases, with the U.S. Census Bureau projecting that individuals aged 65 and older will comprise over 20% of the population by 2030. This demographic shift amplifies the need for sustainable treatment options, driving robust demand for biosimilars across multiple therapeutic areas.

MARKET DRIVERS

Physician and Patient Hesitancy Due to Perceived Safety Concerns

Despite regulatory approval and clinical evidence demonstrating equivalence, lingering skepticism among healthcare providers and patients regarding the safety and efficacy of biosimilars impedes the U.S. biosimilars market growth. According to a survey conducted by the American Medical Association, a notable portion of physicians expressed uncertainty about the interchangeability of biosimilars with reference products, citing concerns about potential immunogenicity and long-term safety profiles. As per research published in JAMA Internal Medicine, patient awareness of biosimilars remains low, with only a small minority of respondents indicating familiarity with the concept and many harboring misconceptions about reduced quality or effectiveness. This lack of confidence often translates into reluctance to switch stable patients from reference biologics to biosimilars, a practice known as non-medical switching. The Food and Drug Administration notes that while extensive data supports biosimilar safety, public perception lags behind scientific consensus due to insufficient education and communication efforts. Healthcare providers frequently cite the complexity of explaining biosimilar science to patients as a barrier to adoption, fearing that misunderstandings could compromise trust and adherence. Furthermore, historical incidents involving compounding pharmacies and biological product contamination have heightened general caution regarding non-originator biologics. Addressing these perceptual barriers requires targeted educational initiatives, transparent communication strategies, and robust post-marketing surveillance data to reassure stakeholders and facilitate broader acceptance of biosimilars in clinical practice.

Complex Patent Litigation and Regulatory Hurdles Delay Market Entry

Intellectual property disputes and intricate regulatory requirements are further hindering the U.S. biosimilars market expansion. According to the Federal Trade Commission, originator biologic manufacturers frequently employ patent thickets consisting of numerous secondary patents covering manufacturing processes, formulations, and delivery devices to extend market exclusivity beyond the expiration of core composition of matter patents. As per data from the Biologics Price Competition and Innovation Act, litigation involving biosimilar applicants often lasts several years, with some cases resulting in settlements that postpone market entry until late in the reference product lifecycle. The complexity of demonstrating biosimilarity requires extensive analytical, comparative, and clinical studies, which entail substantial time and financial investment, increasing the risk for developers. The Food and Drug Administration mandates rigorous evaluation of each biosimilar application, ensuring high standards but also contributing to prolonged review timelines compared to small-molecule generics. Furthermore, the lack of automatic substitution laws in many states necessitates individual prescriber approval for each switch, adding administrative burden and slowing uptake. According to industry analyses, these legal and regulatory complexities deter smaller biotechnology firms from entering the market, limiting competition and maintaining higher prices for longer periods. Consequently, the delayed availability of biosimilars restricts patient access to cost-effective treatments and hampers the realization of potential healthcare savings.

MARKET OPPORTUNITIES

Expansion into Self Administration and Home Care Settings

The growing preference for home-based healthcare and self-administered therapies presents a significant opportunity for biosimilar manufacturers to differentiate their products through innovative delivery systems. According to the Visiting Nurse Association of America, the number of patients receiving home health care services in the United States has increased significantly, driven by an aging population and desire for convenience. As per market intelligence data, biosimilars formulated for subcutaneous injection using pre-filled syringes or auto-injectors are gaining traction among patients who prefer avoiding frequent hospital visits for intravenous infusions. Manufacturers can capitalize on this trend by developing user-friendly delivery devices that enhance patient compliance and satisfaction. The Centers for Medicare and Medicaid Services supports home infusion therapy through specific billing codes, encouraging providers to transition eligible patients from clinic-based to home-based administration. Furthermore, digital health integration, including connected devices that track injection adherence and provide real-time feedback, offers additional value propositions for biosimilar brands. According to the Personalized Medicine Coalition, personalized delivery solutions combined with patient support programs can improve outcomes and reduce overall healthcare costs by minimizing complications and hospital readmissions. By focusing on ease of use and patient-centric design, biosimilar companies can capture market share in the expanding home care segment and build brand loyalty among consumers seeking greater autonomy in managing their chronic conditions.

Strategic Partnerships and Vertical Integration among Stakeholders

Collaborative arrangements between biosimilar manufacturers, payers and healthcare providers create opportunities to streamline adoption and optimize supply chain efficiency, which is another prominent opportunity in the U.S. biosimilars market. According to the Pharmaceutical Research and Manufacturers of America, vertical integration among pharmacy benefit managers, insurers, and specialty pharmacies facilitates faster formulary inclusion and preferential positioning of biosimilars. As per industry reports, strategic partnerships enable manufacturers to secure guaranteed volume commitments in exchange for competitive pricing and rebates, thereby ensuring market access and revenue stability. The integration of biosimilars into value-based care models allows healthcare systems to share savings generated from lower drug costs with payers and patients, aligning financial incentives across the ecosystem. The American Hospital Association notes that integrated delivery networks are increasingly adopting standardized biosimilar protocols to reduce variation in care and maximize cost efficiencies. Furthermore, collaborations with academic medical centers for real-world evidence generation help validate biosimilar performance in diverse patient populations, enhancing physician confidence and supporting broader utilization. According to the National Institute for Health Care Management, these collaborative frameworks also facilitate educational initiatives that address knowledge gaps and promote best practices for biosimilar prescribing. By leveraging synergies among stakeholders, biosimilar manufacturers can overcome market entry barriers, accelerate adoption rates, and establish sustainable competitive advantages in the evolving U.S. healthcare landscape.

MARKET CHALLENGES

Interchangeability Designation and Switching Protocols Create Clinical Uncertainty

The distinction between biosimilarity and interchangeability is a significant challenge to seamless market adoption, as not all approved biosimilars carry the interchangeable designation from the Food and Drug Administration. According to the FDA, only a subset of approved biosimilars has been designated as interchangeable, meaning they can be substituted at the pharmacy level without prescriber intervention, similar to generic small-molecule drugs. As per the American Society of Health-System Pharmacists, the lack of interchangeability status for many biosimilars requires physicians to actively write new prescriptions for switches, creating administrative friction and delaying patient access. This regulatory nuance confuses healthcare providers and patients, who may perceive non-interchangeable biosimilars as inferior or less safe despite meeting rigorous approval standards. The complexity of switching protocols varies by state, with some jurisdictions imposing strict notification requirements or prohibiting substitution entirely for non-interchangeable products. According to a study in Health Affairs, this fragmented regulatory landscape leads to inconsistent prescribing patterns and undermines efforts to standardize care across different healthcare settings. Furthermore, the absence of long-term real-world data on multiple switches between reference products and various biosimilars raises concerns about cumulative immunogenicity effects. Addressing these challenges requires harmonized state laws, clear clinical guidelines, and robust evidence generation to support confident switching practices and maximize the therapeutic potential of biosimilars.

Pricing Pressure and Rebate Dynamics Complicate Market Viability

Intense pricing competition and opaque rebate structures within the U.S. pharmaceutical supply chain present significant challenges to the U.S. biosimilars market growth. According to the Congressional Budget Office, while biosimilars are priced lower than reference products, the net price difference is often obscured by complex rebate agreements between manufacturers and pharmacy benefit managers. As per data from the Institute for Clinical and Economic Review, rebates can account for a large portion of the list price differential, reducing the actual savings realized by patients and payers. This dynamic discourages manufacturers from launching biosimilars at aggressively low prices, fearing margin erosion and unsustainable business models. Furthermore, originator companies often engage in contracting strategies, such as bundling reference products with other high-volume drugs, to maintain market share and disincentivize biosimilar uptake. The Federal Trade Commission highlights that these practices distort market dynamics and limit the expected cost benefits of biosimilar competition. Additionally, the high cost of development and manufacturing for biological products means that biosimilar makers operate on thinner margins compared to traditional generic manufacturers. According to industry analyses, these financial pressures can lead to market exit or reduced investment in future biosimilar pipelines, ultimately restricting patient access to affordable alternatives and hindering the long-term sustainability of the biosimilars market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 38.95% |

| Segments Covered | By Drug Class, Disease Indication, and Region. |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | California, Washington, Oregon, New York, and the rest of the United States. |

| Market Leaders Profiled | Pfizer Inc., Amgen Inc., Sandoz International GmbH, Samsung Bioepis, Celltrion Inc., Biocon Biologics, Teva Pharmaceutical Industries Ltd., Viatris Inc., Coherus BioSciences, AbbVie Inc., Novartis AG, F. Hoffmann-La Roche Ltd, Eli Lilly and Company, and Merck & Co., Inc. |

SEGMENTAL ANALYSIS

By Drug Class Insights

The monoclonal antibodies segment dominated the market by holding 66.4% of the U.S. market share in 2025. The growth of the monoclonal antibodies segment in the U.S. market is driven by the extensive application of monoclonal antibody biosimilars in treating prevalent chronic conditions. According to the Centers for Disease Control and Prevention, over 50 million adults in the United States have been diagnosed with arthritis, many of whom require biologic therapies such as tumor necrosis factor inhibitors. As per the National Cancer Institute, approximately 2 million new cancer cases are diagnosed annually, with a substantial proportion requiring monoclonal antibody treatments like trastuzumab for breast cancer or rituximab for lymphoma. The high prevalence of these conditions creates consistent demand for effective therapeutic interventions. Monoclonal antibody biosimilars offer equivalent efficacy to reference products at reduced costs, making them attractive options for healthcare systems managing large patient populations. According to the American College of Rheumatology, clinical guidelines strongly support the use of biosimilar monoclonal antibodies for rheumatoid arthritis and other inflammatory conditions, reinforcing provider confidence. Furthermore, the expiration of patents for major blockbuster biologics has enabled multiple manufacturers to enter the market, increasing availability and competition. This convergence of high disease burden, robust clinical evidence, and expanded product availability creates enduring momentum for the monoclonal antibody segment.

On the other side, the filgrastim and pegfilgrastim segment is expected to be the fastest growing segment and register a CAGR of 19.1% during the forecast period in the U.S. market owing to the critical role of these agents in supporting chemotherapy induced neutropenia management. The rising incidence of cancer and the corresponding increase in myelosuppressive chemotherapy treatments drive exceptional growth for Filgrastim and Pegfilgrastim biosimilars. According to the American Cancer Society, the number of cancer survivors living in the United States is expected to reach 26 million by 2040, reflecting a steady increase in diagnosis rates and survival outcomes. As per the National Comprehensive Cancer Network guidelines, granulocyte colony-stimulating factors such as filgrastim and pegfilgrastim are recommended for primary prophylaxis in patients receiving chemotherapy regimens with a high risk of febrile neutropenia. The widespread adoption of these guidelines ensures consistent demand for these supportive care agents. Biosimilars for filgrastim and pegfilgrastim were among the first to enter the U.S. market, establishing a mature supply chain and strong physician familiarity. According to the Oncology Nursing Society, the use of long-acting pegfilgrastim biosimilars has increased significantly due to their convenience of single-dose administration per chemotherapy cycle compared to daily filgrastim injections. This operational efficiency reduces hospital visits and nursing workload, enhancing patient quality of life. Furthermore, the competitive landscape features multiple approved biosimilars, driving aggressive pricing strategies that improve accessibility. This combination of clinical necessity, guideline adherence, and operational convenience creates powerful growth momentum for this segment.

By Disease Indication Insights

The cancer segment dominated the market by capturing the highest share of the U.S. biosimilars market in 2025. The dominance of cancer segment in the U.S. market is primarily attributed to the high cost of oncology biologics and the critical need for cost-effective treatment options. The substantial burden of cancer in the United States, coupled with the high cost of biologic therapies, significantly propels the dominance of the cancer indication segment. According to the National Cancer Institute, cancer remains the second leading cause of death in the United States, with over 600,000 deaths projected annually. As per the American Society of Clinical Oncology, the financial burden of cancer care is substantial, with biologic agents comprising a significant portion of this expenditure. Biosimilars for oncology indications, such as trastuzumab for HER2-positive breast cancer and rituximab for non-Hodgkin lymphoma, offer substantial savings without compromising clinical outcomes. The introduction of these biosimilars has enabled healthcare systems to treat more patients within fixed budgets, improving overall access to care. According to the Centers for Medicare and Medicaid Services, total spending on specialty drugs remains a primary driver of healthcare cost inflation, highlighting the financial pressure on the system. Payers and providers actively prioritize oncology biosimilars to mitigate these costs. Furthermore, clinical trials have demonstrated non-inferiority of biosimilars in various cancer settings, reinforcing provider confidence. This convergence of high disease prevalence, substantial economic burden, and proven clinical equivalence creates sustained demand momentum for cancer indication biosimilars.

However, the autoimmune diseases segment is predicted to record a CAGR of 23.1% during the forecast period in the U.S. market owing to the expanding portfolio of biosimilars for conditions such as rheumatoid arthritis, psoriasis, and inflammatory bowel disease. The increasing prevalence of autoimmune disorders and the requirement for long-term biological therapy drive rapid expansion in this segment. According to the Centers for Disease Control and Prevention, autoimmune diseases affect millions of Americans, with rheumatoid arthritis and psoriasis being among the most common conditions. As per the Arthritis Foundation, a large number of adults in the United States live with rheumatoid arthritis, a chronic condition that often requires continuous treatment with biologic disease-modifying antirheumatic drugs. The chronic nature of these diseases necessitates lifelong medication adherence, creating a stable and recurring demand for therapeutic agents. Biosimilars for adalimumab, etanercept, and infliximab have become widely available, offering significant cost reductions for patients and payers. According to the Crohn's and Colitis Foundation, millions of Americans suffer from inflammatory bowel disease, with many relying on anti-tumor necrosis factor therapies for remission maintenance. The introduction of biosimilars has improved access to these essential treatments for patients who previously faced financial barriers. Furthermore, patient assistance programs provided by biosimilar manufacturers enhance affordability and support adherence. This combination of high disease prevalence, chronic treatment needs, and improved accessibility creates powerful growth momentum for the autoimmune diseases segment.

By Distribution Channel Insights

The hospital pharmacies segment occupied the major share of 54.5% of the U.S. market in 2025. The growth of the hospital pharmacies segment in the U.S. market can be credited to the centralized purchasing power of hospitals and the necessity for intravenous administration of many biosimilars. According to the American Hospital Association, thousands of hospitals in the United States operate pharmacy departments that manage the procurement and administration of complex biological products. As per the Premier Inc. supply chain data, hospital group purchasing organizations negotiate substantial discounts for biosimilars, leveraging volume to secure favorable pricing from manufacturers. Many high-value biosimilars, such as those for cancer and severe autoimmune conditions, require intravenous infusion, which must be administered in a clinical setting under medical supervision. This logistical requirement ensures that hospitals remain the primary distribution channel for these products. According to the Centers for Medicare and Medicaid Services, Medicare Part B covers drugs administered in hospital outpatient departments, providing a reliable reimbursement mechanism that supports hospital-based utilization. Furthermore, hospital pharmacy and therapeutics committees play a critical role in evaluating and selecting biosimilars for formulary inclusion, ensuring standardized use across the institution. The integration of biosimilars into electronic health records and order sets facilitates seamless prescribing and administration. This combination of procurement efficiency, clinical necessity, and reimbursement stability creates enduring momentum for hospital pharmacies as the leading distribution channel.

On the other hand, the retail pharmacy segment is predicted to witness a CAGR of 20.2% during the forecast period in the U.S. market owing to the shift towards self-administered subcutaneous biosimilars and expanded scope of practice for pharmacists. The increasing availability of biosimilars formulated for subcutaneous self-administration significantly drives expansion in the retail pharmacy channel. According to the National Community Pharmacists Association, a vast majority of pharmacies now offer injection coordination services or facilitate home delivery of self-injectable medications. As per industry data, biosimilars for conditions such as rheumatoid arthritis and psoriasis are increasingly available in pre-filled syringes or auto-injectors that patients can administer at home. This convenience reduces the need for frequent hospital visits and aligns with patient preferences for autonomy and comfort. Retail pharmacies play a crucial role in educating patients on proper injection techniques and storage requirements, ensuring safe and effective use. According to the Centers for Disease Control and Prevention, pharmacist-led education improves medication adherence and reduces errors associated with self-administration. Furthermore, the expansion of biosimilar indications for self-injection has broadened the customer base for retail pharmacies. Insurance plans often prefer retail distribution for self-administered drugs due to lower overhead costs compared to hospital outpatient departments. According to the Pharmaceutical Research and Manufacturers of America, commercial insurance claims for self-injectable biological products have shown consistent growth over recent years, reflecting this shifting trend. This convergence of product innovation, patient preference, and payer incentives creates powerful growth momentum for retail pharmacies.

COUNTRY ANALYSIS

The United States accounted for 34.6% of the global market share in 2025. The dominance of U.S. in the global market can be credited to the convergence of a large patient population, robust regulatory framework, and intense focus on healthcare cost containment. The comprehensive regulatory pathway established by the Food and Drug Administration and supportive legislative measures significantly propel United States market dominance. According to the Biologics Price Competition and Innovation Act, the FDA has created a clear and rigorous approval process for biosimilars, ensuring high standards for safety and efficacy. As per the Inflation Reduction Act, financial incentives such as increased Medicare Part B add-on payments for biosimilars have accelerated provider adoption and market penetration. The United States boasts the highest number of approved biosimilars globally, with over 50 products currently available across multiple therapeutic areas. According to the Centers for Medicare and Medicaid Services, the implementation of these policies has resulted in billions of dollars in savings for the federal healthcare system. Furthermore, the presence of major global pharmaceutical companies and specialized biosimilar developers in the United States fosters a competitive and innovative market environment. The country's advanced healthcare infrastructure, including widespread insurance coverage and sophisticated supply chains, supports efficient distribution and access. According to the Pharmaceutical Research and Manufacturers of America, the United States accounts for the largest share of global biosimilar investment and clinical trial activity. This combination of regulatory clarity, financial incentives, and market infrastructure ensures that the United States remains the central hub for biosimilar development and commercialization.

COMPETITIVE LANDSCAPE

The United States biosimilars market features intense competition among established pharmaceutical giants specialized biotech firms and emerging generic manufacturers. Incumbent players leverage extensive manufacturing capabilities regulatory expertise and established distribution networks to maintain leadership while new entrants differentiate through innovative pipeline candidates and agile commercialization strategies. Competition centers on achieving interchangeability status which allows for automatic substitution at the pharmacy level creating a significant advantage in market penetration. Pricing dynamics are highly competitive with manufacturers offering substantial discounts and rebates to secure formulary preference from pharmacy benefit managers and insurance plans. Patent litigation remains a critical battleground as originator companies employ defensive strategies to delay biosimilar entry extending market exclusivity periods. Companies also compete on patient support services including injection training and financial assistance programs to enhance brand loyalty and adherence. The landscape is characterized by rapid consolidation through mergers and acquisitions as firms seek to expand portfolios and achieve economies of scale. Strategic collaborations with healthcare providers and payers facilitate evidence generation and promote value based care models. This dynamic environment drives continuous innovation and cost reduction ultimately benefiting patients and the healthcare system through increased access to affordable biological therapies.

KEY MARKET PLAYERS

Some of the promising companies that are playing a dominating role in the U.S. Biosimilars Market include

- Pfizer Inc.

- Amgen Inc.

- Sandoz International GmbH

- Samsung Bioepis

- Celltrion Inc.

- Biocon Biologics

- Teva Pharmaceutical Industries Ltd.

- Viatris Inc.

- Coherus BioSciences

- AbbVie Inc.

- Novartis AG

- F. Hoffmann-La Roche Ltd

- Eli Lilly and Company

- Merck & Co., Inc.

Top Players in the U.S. Biosimilars Market

Sandoz Group AG

Sandoz Group AG stands as a global leader in the United States biosimilars market with a robust portfolio spanning oncology immunology and ophthalmology. The company recently completed its strategic separation from Novartis in October 2023 establishing itself as an independent publicly traded entity focused exclusively on generics and biosimilars. Sandoz has strengthened its market position by launching multiple interchangeable biosimilars for adalimumab and expanding its manufacturing capabilities in Europe and North America. The company actively collaborates with U.S. healthcare providers to ensure seamless integration of its products into clinical workflows. Sandoz also invests heavily in research and development to advance next generation biosimilar candidates targeting high value biological medicines. Its comprehensive supply chain infrastructure ensures reliable product availability across hospital and retail pharmacy channels reinforcing its commitment to improving patient access to affordable biological therapies.

Amgen Inc

Amgen Inc plays a pivotal role in the United States biosimilars market through its pioneering entry with filgrastim and pegfilgrastim biosimilars. The company leverages its extensive experience in biologic manufacturing to produce high quality cost effective alternatives to reference products. Amgen has expanded its biosimilar portfolio to include agents for inflammatory bowel disease and osteoporosis demonstrating its commitment to diverse therapeutic areas. Recent actions include strategic partnerships with commercialization experts to enhance market penetration and educational initiatives aimed at increasing physician confidence in biosimilar adoption. Amgen also focuses on developing advanced delivery devices such as auto injectors to improve patient convenience and adherence. By integrating biosimilars into its broader biopharmaceutical strategy Amgen reinforces its leadership in biotechnology while contributing to sustainable healthcare solutions through reduced treatment costs and improved accessibility for patients with chronic conditions.

Pfizer Inc

Pfizer Inc contributes significantly to the United States biosimilars market through its dedicated biosimilars division which focuses on oncology and immunology indications. The company has launched several key biosimilars including trastuzumab and bevacizumab leveraging its global manufacturing network to ensure consistent supply. Pfizer strengthens its market position by engaging in value based agreements with payers and healthcare systems to demonstrate the economic benefits of its products. The company also invests in real world evidence studies to validate the safety and efficacy of its biosimilars in diverse patient populations. Pfizer collaborates with patient advocacy groups to raise awareness about biosimilar options and reduce out of pocket costs. Furthermore the company continues to expand its pipeline with new candidates targeting high burden diseases ensuring a steady flow of innovative affordable treatments that support the long term sustainability of the U.S. healthcare system.

Top Strategies Used by Key Market Participants

Key players in the United States biosimilars market employ multifaceted strategies to secure competitive advantages and drive adoption. Companies prioritize securing interchangeability designation from the Food and Drug Administration to enable pharmacy level substitution and streamline access. Strategic partnerships with contract development and manufacturing organizations enhance production scalability and reduce costs. Manufacturers engage in aggressive pricing strategies and value based contracts with payers to secure favorable formulary placement. Extensive educational programs target physicians pharmacists and patients to address misconceptions and build trust in biosimilar safety and efficacy. Investment in advanced delivery technologies such as pre filled syringes and auto injectors improves patient convenience and adherence. Legal teams actively navigate patent litigation landscapes to accelerate market entry timelines. Portfolio diversification across therapeutic areas reduces dependency on single products and mitigates revenue risks. These coordinated efforts enable market participants to overcome barriers and maximize the potential of biosimilars in the evolving healthcare landscape.

MARKET SEGMENTATION

This research report on the U.S. biosimilars market has been segmented based on the following categories.

By Drug Class

- Monoclonal Antibodies

- Filgrastim & Pegfilgrastim

- Others

By Disease Indication

- Cancer

- Autoimmune Diseases

- Arthritis

- Psoriasis

- Neutropenia

- Others

- Others

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com