- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

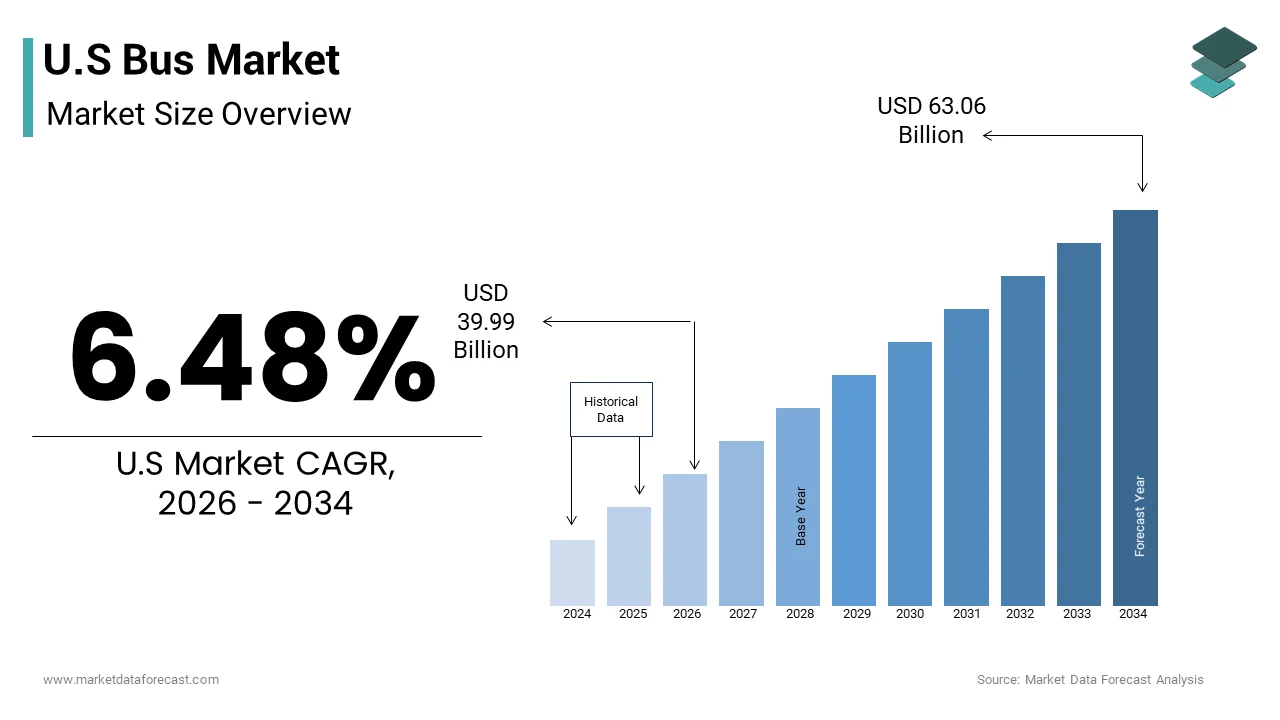

Market Size, 2025

$37.55 BnMarket Estimate, 2026

$39.99 BnMarket Forecast, 2034

$63.06 BnCAGR, 2026–2034

6.48%U.S. Bus Market Report Summary

The U.S. bus market was valued at USD 37.55 billion in 2025, is estimated to reach USD 39.99 billion in 2026, and is projected to reach USD 63.06 billion by 2034, growing at a CAGR of 6.48% during the forecast period from 2026 to 2034. The growth of the U.S. bus market is driven by rising investments in public transportation infrastructure, increasing adoption of electric and low-emission buses, and supportive government initiatives promoting sustainable mobility. Growing urbanization, the modernization of aging transit fleets, and the expansion of smart city projects are further accelerating market growth. The integration of advanced safety technologies, connected fleet management systems, and energy-efficient powertrains is enhancing operational efficiency and passenger safety. Additionally, federal funding for clean transportation, rising demand for reliable intercity and school transportation, and continuous innovation in electric bus technologies are creating significant opportunities for manufacturers and fleet operators across the United States.

Key Market Trends

- Rising deployment of electric and zero-emission buses supported by federal funding and decarburization initiatives.

- Increasing adoption of advanced driver assistance systems (ADAS), telematics, and connected fleet management technologies.

- Growing investments in fleet modernization programs to replace aging diesel buses with cleaner and more efficient alternatives.

- Expansion of smart public transportation networks integrated with digital mobility and real-time passenger information systems.

- Increasing focus on lightweight vehicle designs, battery innovations, and energy-efficient propulsion systems to reduce operating costs and emissions.

Segmental Insights

Based on vehicle, the transit buses segment dominated the U.S. bus market in 2025. The segment's leadership is attributed to rising investments in urban public transportation systems, increasing commuter demand, and government programs aimed at expanding sustainable and accessible transit infrastructure across metropolitan areas.

Based on seating capacity, the 40 to 70 passengers segment accounted for the major share of the U.S. bus market in 2025. This segment remains the preferred choice for public transit agencies due to its optimal passenger capacity, operational flexibility, and suitability for high-density urban and suburban transportation routes.

Based on end use, the government and public transport authorities segment held the leading share of the U.S. bus market in 2025. The segment's dominance is driven by continuous public investments in transportation infrastructure, large-scale fleet procurement initiatives, and national policies encouraging the adoption of environmentally sustainable and accessible public transit systems.

Regional Insights

The United States is expected to remain the primary engine of growth for the North American bus industry throughout the forecast period. The country's leadership is supported by extensive transportation infrastructure, strong government funding for public transit modernization, and increasing investments in zero-emission mobility solutions. Rapid adoption of electric buses, expansion of urban transit networks, and ongoing replacement of aging bus fleets continue to strengthen market growth. Additionally, the presence of leading vehicle manufacturers, favorable regulatory policies, and growing emphasis on reducing greenhouse gas emissions are reinforcing the United States' position as the largest and most technologically advanced bus market in North America.

Competitive Landscape

The U.S. bus market is characterized by intense competition among established global manufacturers and regional bus producers focused on innovation, sustainability, and advanced mobility solutions. Leading companies are investing in electric and hydrogen-powered buses, battery technology improvements, autonomous driving capabilities, and connected fleet management platforms to meet evolving transportation requirements. Strategic partnerships with public transit agencies, expansion of domestic manufacturing facilities, and continuous investments in research and development remain key competitive strategies. Companies are also emphasizing lightweight vehicle construction, enhanced passenger safety features, digital diagnostics, and comprehensive after-sales services to strengthen their market presence. As demand for clean and intelligent public transportation continues to rise, manufacturers are accelerating product innovation and expanding their zero-emission bus portfolios to gain a competitive advantage.

Prominent players in the U.S. bus market include Blue Bird, BYD, CAF, Daimler, Gillig Corporation, New Flyer of America Inc., Golden Dragon, Proterra Inc., Hyundai, Iveco, MAN, Scania, Volvo, and Yutong.

U.S. Bus Market Size

The U.S bus market size was valued at USD 37.55 billion in 2025 and is anticipated to reach USD 39.99 billion in 2026 to reach USD 63.06 billion by 2034, growing at a CAGR of 6.48% during the forecast period from 2026 to 2034.

U.S. Bus Market Comprehensive Analysis

The U.S. bus market is projected to witness significant modernization and a steady increase in fleet electrification over the next few years, maintaining its role as a cornerstone of American infrastructure. The U.S. bus market encompasses the manufacturing, distribution, and operation of medium and heavy duty vehicles designed for public transit, intercity travel, school transportation, and charter services. This sector is a critical component of national infrastructure, facilitating mobility for millions of passengers daily while aiming to reduce urban congestion and carbon emissions. The market includes various vehicle types, such as transit buses, coach buses, school buses, and shuttle buses, powered by diesel, natural gas, battery electric, and hybrid systems. According to the Federal Transit Administration, public transportation agencies in the U.S. operate approximately 60,000 buses across diverse routes, serving urban, suburban, and rural communities. The industry is undergoing a significant transformation, driven by federal mandates for zero emission vehicles and advancements in autonomous driving technologies. As per the American Public Transportation Association, bus transit accounts for approximately 4.3 billion passenger trips annually, highlighting its essential role in the multimodal transportation network. Regulatory frameworks established by the Environmental Protection Agency and the Department of Transportation influence vehicle design, safety standards, and operational efficiency. The definition of the market extends beyond hardware to include maintenance services, charging infrastructure, and digital fleet management solutions. The interplay between government funding, technological innovation and shifting consumer preferences defines the current landscape. Stakeholders are increasingly focusing on sustainability, accessibility, and connectivity to meet evolving societal expectations. The integration of smart city initiatives further enhances the strategic importance of bus systems in modern urban planning.

MARKET DRIVERS

Federal Funding and Infrastructure Investment Initiatives

Federal funding and infrastructure investment initiatives are majorly driving the expansion of the U.S. bus market.. The Bipartisan Infrastructure Law has allocated billions of dollars specifically for public transit improvements, including the purchase of low or no emission buses. According to the Federal Transit Administration, the Low or No Emission Vehicle Program provided $1.5 billion in competitive grants during 2024 to state and local governmental authorities for the procurement of zero emission buses and related infrastructure. This financial support reduces the capital burden on transit agencies, enabling them to replace aging diesel fleets with cleaner alternatives. As per the U.S. Department of Transportation, these investments aim to enhance service reliability and accessibility while reducing greenhouse gas emissions. The availability of federal funds encourages municipalities to accelerate their transition plans and adopt advanced technologies, such as battery electric and hydrogen fuel cell buses. State level matching funds often leverage federal grants, amplifying the total investment in bus infrastructure. The emphasis on domestic manufacturing in these funding programs also stimulates local production and job creation. Transit agencies are prioritizing projects that align with federal sustainability goals, ensuring long term operational viability. The certainty of funding streams allows manufacturers to plan production schedules and invest in research and development. This robust financial backing ensures sustained demand for new buses and associated infrastructure across the nation.

Urbanization and Demand for Sustainable Public Transit

Rapid urbanization and the growing demand for sustainable public transit options significantly drive the U.S. bus market. The concentration of populations in metropolitan areas increases the need for efficient, high capacity transportation solutions that reduce reliance on private vehicles. According to the U.S. Census Bureau, about 80% of the U.S. population lives in urban areas, placing greater strain on existing transportation networks and necessitating expanded bus services. Cities are implementing bus rapid transit systems and dedicated lanes to improve speed and reliability, making buses a more attractive option for commuters. As per the International Transport Forum, public transit usage correlates with reduced traffic congestion and lower per capita carbon emissions, supporting municipal sustainability targets. The shift towards environmental consciousness among consumers encourages ridership and political support for bus infrastructure improvements. Transit agencies are adopting real time tracking and contactless payment systems to enhance user experience and operational efficiency. The integration of buses with other modes of transport, such as rail and bike sharing, creates seamless mobility ecosystems. Government policies promoting transit oriented development further boost demand for bus services in new residential and commercial zones. The economic benefits of reduced traffic delays and improved air quality justify continued investment in bus networks. These factors collectively ensure that urbanization remains a powerful driver for market growth.

MARKET RESTRAINTS

High Initial Costs and Infrastructure Requirements

High initial costs and extensive infrastructure requirements are hindering the bus market growth in the U.S. Battery electric and hydrogen fuel cell buses have higher upfront purchase prices compared to traditional diesel models due to expensive battery packs and specialized components. According to the National Renewable Energy Laboratory, the purchase price of an electric bus can be $750,000 to $1,000,000, which is nearly double the cost of a diesel bus, but the initial capital outlay remains a barrier for many transit agencies. Additionally, the deployment of these vehicles requires substantial investment in charging stations or hydrogen refueling facilities, which often lack existing infrastructure. As per the American Public Transportation Association, upgrading electrical grids to support high power charging involves complex engineering and significant costs that smaller municipalities may struggle to afford. The limited availability of skilled technicians for maintaining advanced propulsion systems further increases operational expenses. Budget constraints and competing priorities within local governments often delay procurement decisions and fleet replacements. The uncertainty regarding long term maintenance costs and battery degradation adds financial risk for operators. Without adequate federal or state subsidies, the transition to cleaner technologies slows down. The complexity of coordinating infrastructure development with vehicle procurement creates logistical challenges. These financial and structural barriers hinder the rapid, widespread adoption of next generation buses.

Supply Chain Disruptions and Labor Shortages

Supply chain disruptions and labor shortages present a major restraint on the U.S. bus market. The U.S. market relies on global supplies of semiconductors, batteries, and specialized components, which have faced significant bottlenecks in recent years. According to the Bureau of Labor Statistics, the producer price index for truck and bus bodies increased by approximately 25% between 2021 and 2024, affecting profit margins and delivery timelines. Shortages of critical materials, such as lithium and cobalt, impact the production of electric bus batteries, leading to extended lead times. As per the Manufacturing Institute, there were approximately 600,000 open manufacturing jobs in the U.S. as of 2024, which exacerbates production delays and increases wage pressures. The lack of qualified engineers and technicians hinders the ability of manufacturers to scale up production and innovate rapidly. Logistics challenges, such as port congestion and transportation delays, further complicate the import of parts and export of finished goods. Manufacturers struggle to forecast demand accurately amidst uncertain supply conditions, leading to inventory imbalances. The reliance on single source suppliers for key components increases vulnerability to geopolitical tensions and trade disputes. These disruptions hinder the ability of companies to meet contractual obligations and fulfill orders from transit agencies. Until supply chains stabilize, the industry will face ongoing operational inefficiencies and cost pressures.

MARKET OPPORTUNITIES

Electrification and Zero Emission Mandates

The electrification of bus fleets and stringent zero emission mandates present a significant opportunity for the U.S. bus market. Federal and state regulations are increasingly requiring transit agencies to transition to zero emission vehicles, creating a guaranteed demand for electric and hydrogen buses. According to the California Air Resources Board, the Innovative Clean Transit regulation mandates that 100% of new bus purchases be zero emission by 2029, setting a precedent for other states. This regulatory push drives manufacturers to develop advanced battery technologies and fuel cell systems that offer longer ranges and faster charging. As per the Environmental Protection Agency, the Clean School Bus Program has awarded nearly $3 billion to fund approximately 8,500 clean buses across the country. The opportunity extends to the development of supporting infrastructure, such as smart charging networks and energy storage systems. Companies that lead in electric bus technology can secure long term contracts with major transit authorities and establish brand loyalty. The integration of vehicle to grid technology allows buses to serve as mobile energy storage units, enhancing grid stability. The growing focus on sustainability among corporate charter operators also opens new markets for electric coaches. By capitalizing on these regulatory and technological trends, manufacturers can differentiate their offerings and capture premium market segments. The transition to electrification positions the industry for long term growth and environmental compliance.

Integration of Autonomous and Connected Technologies

The integration of autonomous and connected technologies offers a promising opportunity for the U.S. bus market to enhance safety, efficiency, and user experience. Autonomous buses have the potential to address driver shortages and reduce operational costs by enabling automated routing and platooning. According to the National Highway Traffic Safety Administration, approximately 94% of serious crashes are due to human error, and advanced driver assistance systems can significantly reduce these accidents, improving public confidence in bus transit. Connected vehicle technologies allow for real time data exchange between buses, traffic signals, and control centers, optimizing traffic flow and reducing idle time. As per the Intelligent Transportation Society of America, smart bus systems can provide passengers with accurate arrival predictions and seamless payment options, enhancing convenience. The adoption of artificial intelligence in fleet management enables predictive maintenance, reducing downtime and extending vehicle life. Manufacturers are collaborating with technology firms to develop scalable autonomous solutions for specific use cases, such as campus shuttles and bus rapid transit lines. The data generated by connected buses enables transit agencies to make informed decisions about route planning and service adjustments. The commercialization of autonomous technology promises to revolutionize public transport by increasing throughput and reliability. This technological leap creates new revenue streams and competitive advantages for early adopters in the bus market.

MARKET CHALLENGES

Technical Limitations of Alternative Fuel Vehicles

Technical limitations of alternative fuel vehicles are a major challenge to the U.S. bus market by affecting operational reliability and range. Battery electric buses often face issues with range anxiety, particularly in extreme weather conditions which reduce battery efficiency and performance. According to the National Renewable Energy Laboratory, electric buses can lose up to 33% of their range when operating in extreme cold temperatures, requiring additional energy for heating and defrosting. Hydrogen fuel cell buses face challenges related to the limited availability of refueling stations and the high cost of hydrogen production. As per the Department of Energy, as of 2024, there are fewer than 60 public hydrogen refueling stations in the U.S., making it difficult for transit agencies to deploy these vehicles at scale. The weight of large battery packs reduces passenger capacity and increases wear on road surfaces and tires. Charging times for electric buses are longer than refueling times for diesel vehicles, potentially disrupting tight schedules. The complexity of managing mixed fleets with different propulsion systems requires specialized training and maintenance protocols. Manufacturers are working to improve energy density and charging speeds, but technological maturity remains a hurdle. The unpredictability of performance in diverse operating environments creates hesitation among potential buyers. Until these technical issues are resolved, the widespread adoption of alternative fuel buses will remain constrained.

Regulatory Complexity and Policy Uncertainty

Regulatory complexity and policy uncertainty is further challenging the expansion of the U.S. bus market. Varying emission standards and safety regulations across different states and jurisdictions complicate compliance and increase administrative burdens. According to the Environmental Protection Agency, the Phase 3 Greenhouse Gas Standards will require 25% of new vocational vehicles, including buses, to be zero emission by model year 2032, requiring continuous adaptation of vehicle designs and production processes. As per the American Bus Association, inconsistent state level incentives and mandates create confusion for transit agencies planning long term fleet strategies. The lack of a unified national strategy for electric vehicle infrastructure leads to fragmented development and inefficient resource allocation. Policy shifts due to political changes can alter funding priorities and subsidy availability, affecting project viability. The complexity of navigating multiple regulatory frameworks increases legal and compliance costs for industry participants. Manufacturers must balance conflicting requirements, which can delay product launches and increase development expenses. The uncertainty regarding future regulations discourages long term investment in new technologies and facilities. Stakeholders require clear and consistent policy directions to make informed decisions and commit resources. The dynamic nature of the regulatory landscape requires constant monitoring and strategic flexibility. This instability acts as a persistent challenge to market growth and innovation.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.48% |

| Segments Covered | By Vehicle, Seating Capacity, End-User, Service, Propulsion, and By Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

| Regions Covered | California, Washington, Oregon, New York & Rest of the United States |

| Market Leaders Profiled | Blue Bird, BYD, CAF, Daimler, Gillig Corporation, New Flyer of America Inc, Golden Dragon, Proterra Inc, Hyundai, Iveco, MAN, Scania., Volvo, Yutong |

SEGMENTAL ANALYSIS

By Vehicle Insights

The transit buses segment dominated the market by capturing the leading share of the U.S. market in 2025. The dominance of the transit buses segment in the U.S. market is fueled by the extensive network of fixed route services in major metropolitan areas, which rely on transit buses to alleviate traffic congestion and provide affordable mobility. According to the American Public Transportation Association, public transit agencies across the nation operate approximately 60,000 transit buses that facilitate billions of passenger trips annually. The consistent demand for reliable urban transport ensures steady procurement cycles for municipal authorities. As per the Federal Transit Administration, federal funding programs specifically target the replacement and modernization of transit fleets to meet accessibility and emission standards. The shift towards Bus Rapid Transit systems in cities like Los Angeles and Miami further amplifies the need for high capacity transit vehicles. These buses are designed for frequent stops and quick boarding, which optimizes operational efficiency in dense urban environments. The integration of transit buses with other public transport modes, such as subways and light rail, creates a cohesive network that drives ridership. Government mandates for zero emission transit buses in states like California accelerate the adoption of new technologies. This regulatory and operational framework ensures that transit buses remain the backbone of the US bus market.

On the other end, the shuttle and airport bus segment is a promising segment and is estimated to showcase a CAGR of 6.2% during the forecast period in the U.S. market owing to the resurgence of air travel and the expansion of hospitality and corporate shuttle services. According to the Federal Aviation Administration, passenger enplanements exceeded 850 million in 2023, driving increased demand for ground transportation solutions at airports. Hotels, resorts, and corporate campuses are expanding their shuttle fleets to enhance customer convenience and reduce reliance on ride sharing services. As per the International Air Transport Association, the rise in international and domestic tourism necessitates efficient last mile connectivity between terminals and destinations. Shuttle buses offer a cost effective and flexible solution for transporting groups and luggage over short distances. The proliferation of off airport parking facilities also contributes to this trend as operators require reliable shuttles to transport customers to terminals. Manufacturers are introducing smaller, more fuel efficient shuttle models that are easier to maneuver in congested airport zones. The adoption of electric shuttles by hotels and airports aligns with sustainability goals and reduces operational noise. These factors collectively propel the shuttle and airport bus segment at a faster pace than traditional transit or coach segments.

By Seating Capacity Insights

The buses with a seating capacity of 40 to 70 passengers segment accounted for the major share of the U.S. market in 2025 due to its widespread use in public transit, intercity coach services, and school transportation where moderate passenger volumes are common. According to the National Highway Traffic Safety Administration, this size range accounts for the majority of the nearly 500,000 school buses operating in the United States. The 40 to 70 seat configuration allows operators to maintain frequent service intervals without the high operating costs associated with larger articulated buses. As per the American Bus Association, coach operators prefer this capacity for regional routes, as it offers sufficient luggage space and passenger comfort for medium distance travel. School districts also favor this size for standard routes, ensuring efficient student transport while adhering to safety regulations. The availability of both diesel and alternative fuel options in this category provides flexibility for buyers. Manufacturers have optimized the design of these buses to maximize interior space and accessibility features. The economies of scale in production for this standard size reduce unit costs, making it an attractive option for fleet operators. This segment benefits from established maintenance infrastructure and driver familiarity. The consistent demand across multiple sectors ensures that 40 to 70 seat buses remain the market leader.

However, the below 40 seating capacity segment is expected to exhibit a CAGR of 7.4% over the forecast period in the U.S. market owing to the rising demand for flexible and accessible transportation solutions, the increasing popularity of micro transit and on demand services that utilize smaller buses to serve low density areas. According to the Shared Use Mobility Center, as of 2024, there are over 100 active micro transit pilots across the U.S. where large buses are inefficient and costly to operate. Smaller buses offer better fuel efficiency and lower emissions, which aligns with environmental sustainability goals. As per the Federal Transit Administration, grants for innovative coordinated mobility services often support the procurement of cutaway buses and minibuses. The aging population requires paratransit services that accommodate wheelchairs and mobility devices, which are easier to manage in smaller vehicles. Corporate campuses and universities are also adopting small shuttle buses for internal circulation due to their ease of navigation. The lower initial cost and maintenance requirements make below 40 seat buses attractive for private operators and startups. Manufacturers are introducing electric models in this segment to cater to urban last mile delivery and passenger transport. The adaptability of these vehicles to various roles ensures rapid market expansion.

By End Use Insights

The government and public transport authorities segment held the leading share of the U.S. market in 2025 due to the substantial federal, state, and local funding dedicated to maintaining and expanding public transit networks. According to the Federal Transit Administration, public agencies manage a combined fleet of approximately 650,000 vehicles, including 60,000 heavy duty buses, to serve urban and suburban populations. The mandate to provide accessible and reliable transport for all citizens ensures consistent demand regardless of economic fluctuations. As per the American Public Transportation Association, public transit agencies are increasingly investing in zero emission buses to meet climate action plans and regulatory requirements. The scale of procurement by government entities allows for bulk purchasing agreements, which influence market trends and pricing. The focus on improving service frequency and coverage in growing cities drives the need for new vehicles. Government initiatives to upgrade aging infrastructure and fleets create a stable pipeline for manufacturers. The emphasis on safety and compliance with federal standards ensures that public sector purchases prioritize quality and durability. This segment benefits from long term planning horizons and dedicated budget allocations. The critical role of public transport in urban mobility solidifies the leading position of government authorities in the bus market.

However, the private fleet operator segment is anticipated to record a CAGR of 6.7% during the forecast period in the U.S. market owing to the expansion of charter services, employee transportation, and contract operations and corporations and institutions outsourcing their transportation needs to specialized private operators to reduce liability and operational complexity. According to the American Bus Association, the private motorcoach industry provides approximately 600 million passenger trips annually as business travel and group tourism recover. Companies are increasingly providing shuttle services for employees to address commuting challenges and enhance workforce satisfaction. As per the Bureau of Labor Statistics, the employment of bus drivers in the private sector is projected to grow by 5% through 2032, which supports the expansion of private logistics and passenger transport firms. Private operators are quicker to adopt new technologies and flexible business models compared to public agencies. The rise of remote work hubs has created new demand for localized shuttle services connecting residential areas to office parks. Private fleets are also leading the adoption of premium coaches with enhanced amenities for long distance travel. The ability to tailor services to specific client needs gives private operators a competitive edge. The segment benefits from deregulation and favorable leasing options those lower entry barriers. These factors collectively drive the rapid expansion of private fleet operations.

COUNTRY LEVEL ANALYSIS

The United States is anticipated to remain the primary engine of growth for the North American bus industry, as federal sustainability mandates drive a massive overhaul of aging transit infrastructure. According to the Federal Transit Administration, the U.S. public transportation network includes over 2,200 transit agencies operating diverse bus fleets. The domestic manufacturing base includes major global players who produce a wide range of bus types for local and export markets. As per the Bureau of Economic Analysis, the transportation and warehousing sector contributed approximately $1.3 trillion to U.S. GDP in 2023, which underscores the economic importance of bus services. The regulatory environment emphasizes safety, accessibility, and environmental sustainability, influencing vehicle design and operational standards. Consumer preference for sustainable travel options is growing, influencing public policy and procurement decisions. The integration of advanced technologies, such as electric propulsion and autonomous driving features, positions the U.S. as a leader in innovation. The market is supported by a strong network of dealers, service centers, and financing options. The resilience of the public transit sector ensures steady demand despite economic fluctuations. The U.S. remains a central hub for bus manufacturing and innovation, driving global trends in commercial passenger transportation. The combination of geographic scale and economic power ensures that the U.S. maintains its dominant position in the regional bus market.

COMPETITIVE LANDSCAPE

The competition in the U.S. bus market is characterized by intense rivalry among established manufacturers and emerging electric vehicle specialists who compete on technology price and regulatory compliance. The market structure is moderately consolidated with key players holding significant influence over public sector procurement processes. Competitive intensity is driven by the race to develop reliable zero emission buses with sufficient range and durability for daily transit operations. Innovation in battery technology and charging infrastructure plays a vital role as firms seek to differentiate their offerings. Regulatory compliance regarding emissions and domestic content requirements serves as a barrier to entry for international competitors without local manufacturing. Established players leverage their extensive service networks and proven track records to maintain customer trust. Price competition is escalating as federal funding increases access to capital for transit agencies. The focus on total cost of ownership and lifecycle emissions is becoming a key differentiator. Overall the competitive landscape requires continuous adaptation to technological advancements and shifting policy environments.

KEY MARKET PLAYERS

A few of the market players that are dominating the U.S bus market are

- Blue Bird

- BYD

- CAF

- Daimler

- Gillig Corporation

- New Flyer of America Inc

- Golden Dragon

- Proterra Inc

- Hyundai

- Iveco

- MAN

- Scania

- Volvo

- Yutong

Top Three Players In This Market

- New Flyer of America Inc is a leading manufacturer of heavy duty transit buses in North America with a strong presence in the U.S. market. The company specializes in producing low floor and articulated buses powered by diesel natural gas and electric systems. New Flyer strengthens its position through the Xcelsior CHARGE H2 hydrogen fuel cell bus program which supports zero emission mandates. The company recently expanded its manufacturing facilities to increase production capacity for battery electric buses. New Flyer focuses on digital solutions such as the Flyer Connect telematics platform to enhance fleet management efficiency. Its commitment to domestic manufacturing aligns with federal Buy America requirements ensuring eligibility for government contracts. These initiatives reinforce its reputation for reliability and innovation in public transportation.

- Gillig Corporation is a prominent player in the US bus market known for its durable and customizable transit and school buses. The company leverages its independent status to offer flexible solutions tailored to specific agency needs. Gillig strengthens its market position by introducing the Gillig Battery Electric Bus which features advanced lithium titanium oxide battery technology for improved safety and longevity. The company recently partnered with charging infrastructure providers to support seamless electrification for transit agencies. Gillig focuses on lightweight composite materials to enhance fuel efficiency and reduce maintenance costs. Its robust dealer network ensures comprehensive service support across the nation. These efforts demonstrate Gilligs commitment to sustainable and efficient public transportation solutions.

- Proterra Inc is a key innovator in the US bus market specializing in battery electric transit buses and charging systems. The company focuses exclusively on zero emission technology driving the transition away from fossil fuels. Proterra strengthens its position through strategic partnerships with major transit agencies and original equipment manufacturers to license its battery technology. The company recently launched the Proterra Catalyst E2 max range bus which offers extended operational capabilities. Proterra invests heavily in research and development to improve battery energy density and charging speeds. Its integrated approach combining vehicles and infrastructure provides a holistic solution for electrification. These actions enable Proterra to maintain a competitive edge in the rapidly evolving electric bus sector.

Top Strategies Used by Key Market Participants

Key players in the U.S. bus market primarily employ strategies such as electrification strategic partnerships and digital integration to strengthen their market position. Companies frequently invest in developing battery electric and hydrogen fuel cell buses to comply with environmental regulations and meet sustainability goals. This approach allows them to capture government incentives and appeal to eco conscious transit agencies. Strategic collaborations with charging infrastructure providers help create comprehensive ecosystems that support vehicle adoption. By focusing on telematics and data analytics firms enhance operational efficiency and predictive maintenance capabilities for fleet operators. Additionally manufacturers emphasize domestic production to align with federal procurement requirements and secure public sector contracts. Product customization is another key strategy as companies tailor vehicles to specific route needs and accessibility standards. These combined strategies enable market participants to maintain competitiveness and drive growth in a regulated industry landscape.

MARKET SEGMENTATION

This research report on the U.S bus market is segmented and sub-segmented into the following categories.

By Vehicle Type

- Transit buses

- Standard 12 m city buses

- Articulated buses

- Others

- Coach buses

- Intercity scheduled coaches

- Luxury and sleeper coaches

- Others

- School buses

- Type A

- Type B

- Type C

- Type D

- Shuttle and airport buses

- Others

By Seating Capacity Type

- Below 40

- 40-70

- Above 70

By Service Type

- Intercity

- Intracity

By Propulsion Type

- ICE

- BEV

- FCEV

- PHEV

- HEV

By End Use Type

- Government / Public transport authorities

- Private fleet operators

- Corporate / Institutional fleets

- Tourism & travel operators

- Educational institutions

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States