- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

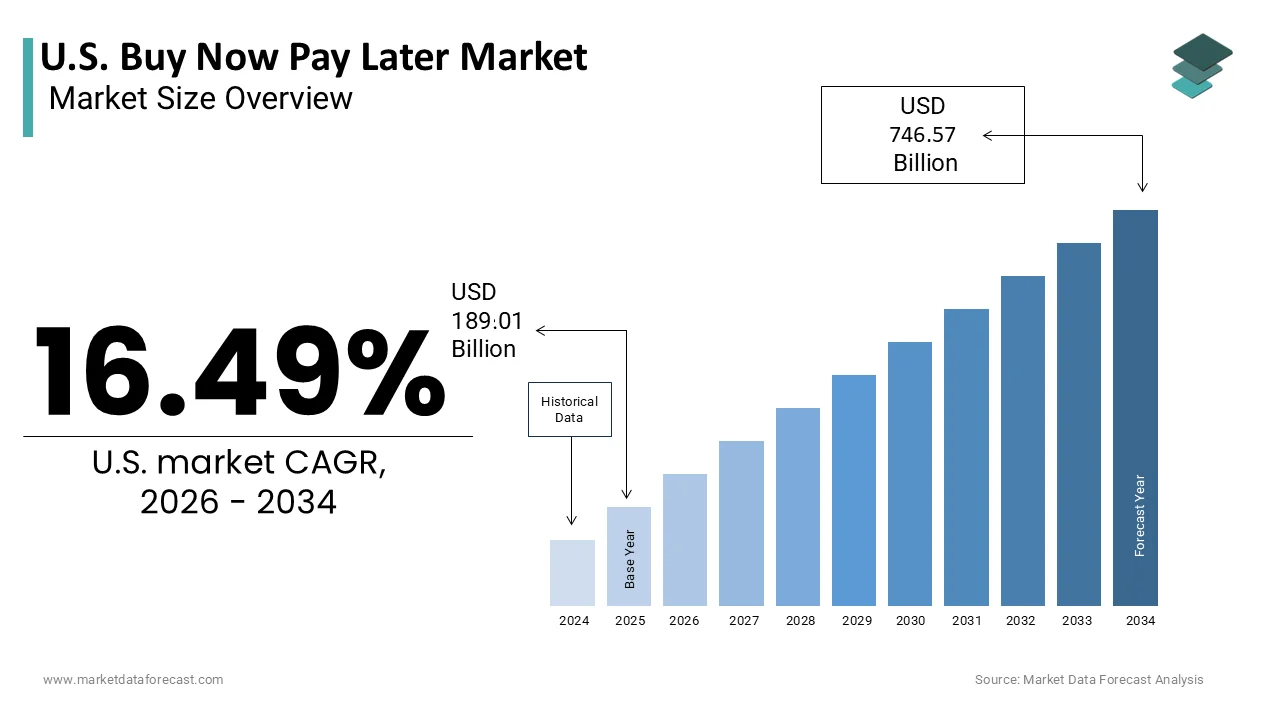

Market Size, 2025

$189.01 BnMarket Estimate, 2026

$220.17 BnMarket Forecast, 2034

$746.57 BnCAGR, 2026–2034

16.49%U.S. Buy Now Pay Later Market Size

The U.S. Buy Now Pay Later Market was valued at USD 189.01 billion in 2025, is estimated to reach USD 220.17 billion in 2026, and is projected to reach USD 746.57 billion by 2034, growing at a CAGR of 16.49% from 2026 to 2034.

The U.S. buy now pay later market is projected to witness sustained expansion through 2026 due to a fundamental shift in consumer payment preferences toward interest-free installment options. The U.S. buy now pay later market represents a rapidly evolving segment of the consumer finance industry, characterized by short-term, interest-free installment loans that facilitate immediate purchase completion. This financial mechanism allows consumers to split transaction costs into multiple payments, typically over a period of six weeks to twelve months, without incurring traditional credit card interest rates. The model has gained significant traction among younger demographics, who seek flexible payment options and transparent fee structures. According to the Federal Reserve Bank of Philadelphia, the proportion of respondents using buy now pay later products reached approximately 20.4% in late 2024, reflecting substantial adoption across retail sectors. The integration of these services into e-commerce checkout processes has streamlined the purchasing experience, reducing friction at the point of sale. Regulatory bodies are increasingly scrutinizing the sector due to concerns regarding consumer protection and debt accumulation. The Consumer Financial Protection Bureau has indicated that millions of Americans utilize these services, with a significant portion being millennials and Generation Z consumers. Unlike traditional credit instruments, buy now pay later providers often perform soft credit checks, making access easier for individuals with limited or no credit history. The market operates within a digital-first ecosystem, leveraging advanced algorithms for real-time risk assessment and approval. Merchant adoption is driven by higher conversion rates and increased average order values. The landscape is competitive, with both specialized fintech firms and established financial institutions vying for market presence through strategic partnerships and technological innovation.

MARKET DRIVERS

Integration with E-Commerce Platforms Driving Conversion Rates

The seamless integration of buy now pay later options into online retail platforms is one of the key factors propelling the growth of the U.S. buy now pay later market. Retailers recognize that offering flexible payment methods significantly influences purchasing decisions, particularly for higher ticket items. According to Adobe Analytics, online retailers that offer buy now, pay later options saw total spending via these services reach a $20 billion milestone during the 2025 holiday season alone. This improvement is attributed to the reduced psychological barrier of paying the full amount upfront,t that allow consumers to manage cash flow more effectively. The ease of integration through application programming interfaces enables merchants to embed these payment solutions directly into their existing infrastructure, without an extensive technical overhaul. Major e-commerce platforms have standardized these integrations, making it accessible for small and medium-sized enterprises to adopt the technology. The visual prominence of buy now pay later logos at checkout instils confidence in buyers, regarding affordability and transparency. Furthermore, the ability to approve transactions instantly without hard credit inquiries appeals to a broader customer base, including those with thin credit files. This accessibility expands the potential customer pool for merchants, driving volume growth. The competitive nature of online retail necessitates such innovations to retain customers who expect diverse payment flexibility. Consequently, the symbiotic relationship between retailers and buy now pay later providers fuels sustained demand and market penetration across various consumer goods categories.

Preference among Millennials and Generation Z Consumers

The strong preference for buy now pay later services among millennials and Generation Z consumers drives significant demand, due to their distinct financial behaviors and attitudes toward traditional credit, which is another major market driver. These demographics often exhibit skepticism toward credit cards, due to high interest rates and complex fee structures, preferring transparent and manageable payment plans. According to the Federal Reserve Bank of Philadelphia, approximately 46.1% of all buy now pay later users were between the ages of 18 and 35 in late 2024, indicating a generational shift in consumption habits. Younger consumers value the ability to budget effectively by spreading costs over time without incurring debt penalties if payments are made on schedule. The digital native nature of these groups aligns with the app-based mobile-first approach of buy now pay later providers, ensuring a user-friendly experience. Social media influence and peer recommendations further amplify adoption, as these services are frequently promoted by influencers and integrated into social commerce platforms. The desire for immediate gratification, combined with financial prudence, makes buy now, pay later an attractive alternative to saving for large purchases. Additionally, the lack of impact on credit scores for many providers appeals to those building or protecting their credit histories. This demographic trend is not transient, but reflects a fundamental change in how younger generations approach personal finance and consumption. Providers tailor their marketing and product features to resonate with these values, ensuring continued growth and loyalty within this key consumer segment.

MARKET RESTRAINTS

Regulatory Uncertainty and Compliance Risks

Increasing regulatory scrutiny and the potential for stringent compliance requirements are hampering the growth of the U.S. buy now pay later market. Regulators are concerned about the lack of uniform consumer protections compared to traditional credit products, leading to calls for stricter oversight. According to the Consumer Financial Protection Bureau, approximately 66% of buy now pay later users take out multiple loans simultaneously, a factor currently under evaluation for potential alignment with credit card regulations. The ambiguity surrounding future regulatory frameworks creates uncertainty for providers, who must anticipate and prepare for potential changes in operational standards. Compliance with emerging rules may require significant investment in legal infrastructure, data reporting, and customer service protocols, increasing operational costs. The possibility of caps on fees or restrictions on marketing practices could limit revenue models and profitability. Furthermore, inconsistent state-level regulations create a fragmented compliance landscape, complicating national expansion strategies for providers. The risk of retroactive enforcement actions adds another layer of financial and reputational risk. Providers must navigate this evolving regulatory environment carefully, balancing innovation with adherence to potential new standards. This uncertainty may deter new entrants and slow down product development, as companies prioritize compliance over expansion. The eventual imposition of strict regulations could fundamentally alter the business model, reducing its appeal to both merchants and consumers.

Consumer Debt Accumulation and Overextension Risks

The risk of consumer debt accumulation and financial overextension is another major restraint on the U.S. buy now, pay later market. The ease of accessing multiple buy-now-pay-later loans simultaneously can encourage impulsive spending beyond a consumer's means. According to the Federal Reserve, nearly 25% of buy now pay later users were late making a payment in 2024, an increase from 18% in the prior year. Unlike traditional loans, where a single monthly payment is common, buy now pay later obligations are often scattered across different providers, making holistic budgeting challenging. This fragmentation can obscure the total debt burden, leading to unintended financial stress. High default rates not only impact provider profitability but also attract negative media attention and regulatory intervention. The lack of comprehensive credit reporting for all buy now pay later transactions means that lenders may not have a complete view of a borrower's indebtedness, increasing lending risk. Consumers facing financial hardship may prioritize other debts over buy now pay later installments, due to perceived lower consequences, although this is changing. The potential for a cycle of debt, where users take new loans to pay off existing ones, undermines the financial health of the consumer base. This systemic risk threatens the long-term sustainability of the market and necessitates responsible lending practices that may constrain growth.

MARKET OPPORTUNITIES

Expansion into Brick and Mortar Retail Environments

The expansion of buy now pay later services into physical brick and mortar retail stores is a significant opportunity for the U.S. buy now pay later market by tapping into the vast majority of retail transactions that still occur offline. While online adoption is high, the in-store sector remains largely underserved, offering substantial growth potential. According to the National Retail Federation, nearly 294 million people lived in U.S. metro areas as of July 2024, indicating a massive concentrated addressable market for physical retail expansions. Integrating these services at physical point of sale terminals allows consumers to access flexible payment options for immediate purchases, enhancing the shopping experience. Providers are developing digital wallets and QR code-based solutions that enable seamless in-store transactions without the need for physical cards. Partnerships with major retail chains facilitate widespread adoption and visibility, driving consumer awareness and usage. The ability to offer buy now, pay later in-store helps retailers compete with e-commerce giants by providing similar financial flexibility. This expansion also allows providers to diversify their revenue streams and reduce dependence on online retail cycles. The integration with mobile devices enables personalized offers and loyalty rewards, further engaging customers. As technology improves, the friction associated with in-store financing decreases, making it a viable option for everyday purchases. This strategic shift into physical retail environments opens new avenues for growth and customer acquisition.

Integration with Digital Wallets and Super Apps

The integration of buy now pay later functionalities into digital wallets and super apps offers a promising opportunity for the U.S. buy now pay later market by embedding financial services into daily consumer interactions. Digital wallets are becoming central hubs for managing payments, subscriptions, and financial tools, making them ideal platforms for buy-now-pay-later services. According to Juniper Research, the number of digital wallet users globally is projected to exceed 6 billion by 2030, with established markets like the U.S. driving significant adoption through value-added features. By embedding buy now pay later options within these ecosystems, providers can offer instant access to credit at the point of decision, across various merchants and services. This integration enhances user convenience by eliminating the need to switch between apps or enter payment details repeatedly. Super apps that combine messaging, shopping, and financial services provide a holistic environment, where buy now, pay later can be contextualized within broader consumer activities. Data sharing within these platforms enables more accurate risk assessment and personalized offers, improving approval rates and customer satisfaction. The stickiness of digital wallet applications ensures higher engagement and retention for buy now, pay later services. Providers partnering with tech giants can leverage their extensive user data and distribution networks to scale rapidly. This synergy between payment infrastructure and flexible credit models drives innovation and creates a seamless financial experience for consumers.

MARKET CHALLENGES

Data Privacy and Security Concerns

Data privacy and security concerns present a major challenge for the U.S. buy now pay later market, as buy now pay later providers collect and process vast amounts of sensitive consumer financial information. The reliance on real-time data analytics for credit decisions requires robust security measures to prevent breaches and unauthorized access. According to the Identity Theft Resource Center, data breaches in the financial sector have increased, exposing millions of consumers to potential identity theft and fraud. Buy now, pay later platforms are attractive targets for cybercriminals due to the volume of personal and financial data they hold. Any security incident can severely damage consumer trust and brand reputation, leading to loss of users and regulatory penalties. Compliance with data protection laws, such as the California Consumer Privacy Act, adds complexity to data management practices. Consumers are increasingly aware of privacy issues and may hesitate to share detailed financial information with newer fintech entities, compared to established banks. The challenge of balancing personalized service with data minimization principles requires sophisticated technological solutions. Providers must invest heavily in cybersecurity infrastructure and transparency initiatives to reassure users. The potential for misuse of data for aggressive marketing or selling to third parties further exacerbates consumer apprehension. Addressing these privacy concerns is critical for maintaining legitimacy and ensuring long-term viability in a trust-dependent industry.

Economic Volatility and Credit Risk Management

Economic volatility and the associated rise in credit risk are further challenging the expansion of the U.S. buy now pay later market. During periods of economic uncertainty, such as inflation or recession, consumers may face reduced disposable income, leading to higher default rates on installment loans. According to the Bureau of Labor Statistics, employment in the nation's metro areas rose by 1.1% between 2023 and 2024, yet fluctuations in real wages continue to impact consumers' ability to meet financial obligations. Buy now, pay later providers often serve younger or less creditworthy borrowers, who are more vulnerable to economic shocks. Managing credit risk in a dynamic economic environment requires advanced predictive modeling and adaptive lending criteria, which can be costly and complex. Higher default rates erode profit margins and may necessitate tighter lending standards, potentially reducing transaction volumes. The lack of collateral for these unsecured loans means that recovery of funds is difficult in case of default. Providers must balance growth ambitions with prudent risk management to avoid excessive exposure to bad debt. Economic downturns may also lead to decreased consumer spending overall, reducing the total addressable market for buy now, pay later services. The sensitivity of the model to macroeconomic conditions makes it less resilient than traditional secured lending. Navigating these economic headwinds requires careful strategic planning and financial buffering to sustain operations during challenging times.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Channel, End-User Type, Age Group, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Affirm Holdings, Inc., Afterpay US Services, LLC, Klarna Inc., PayPal Holdings, Inc., Zip Co Limited, Sezzle Inc., Splitit Payments Ltd., Perpay Inc., Uplift, Inc., Amazon.com, Inc., Synchrony Financial, American Express Company |

SEGMENTAL ANALYSIS

By Channel Insights

The online channel held the dominant position in the U.S. buy now pay later market in 2025, holding the highest share of the U.S. market in 2025. The dominance of the online channel segment in the U.S. market is mainly driven by the seamless integration of digital payment solutions into e-commerce platforms and the inherent compatibility of the model with digital shopping behaviors. The frictionless integration of buy now, pay later options directly into the checkout processes of major e-commerce platforms is further contributing to the expansion of the online channel segment in the U.S. market. According to Adobe Analytics, consumers spent approximately $69.5 billion using buy now pay later services between January and October 2025, primarily through online channels. The ability to embed buy now,w pay later widgets directly onto product pages and checkout screens allows consumers to visualize payment breakdowns instantly, reducing psychological barriers to purchase. This integration is technically straightforward for merchants due to the standardized application programming interfaces provided by leading fintech companies. The instant approval process, based on soft credit checks, ensures that the purchasing flow is not interrupted, maintaining the momentum of the transaction. Online shoppers particularly value the transparency and speed of these digital solutions, which do not require physical documentation or lengthy approval times. The widespread adoption of this technology by major online marketplaces has normalized its use, making it a default expectation for digital consumers. The scalability of online integration allows providers to reach millions of users simultaneously, without the logistical constraints associated with physical retail infrastructure. This technological synergy between e-commerce and flexible financing solidifies the online channel as the leader in the market.

However, the POS channel segment is a ppromisingd is estimated to record a CAGR of 27.7% in the U.S. market during the forecast period, owing to the expansion of physical retail adoption and technological advancements in in-store payment systems. The aggressive expansion of buy now pay later services into physical brick and mortar stores is a key driver of growth for the Point of Sale channel. As per the National Retail Federation, physical stores still account for the majority of retail sales in the U.S., representing a massive untapped market for flexible payment solutions. Retailers are increasingly installing point-of-sale terminals that support buy-now, pay-later transactions, allowing customers to access these benefits in person. This expansion is facilitated by the development of QR code-based systems and digital wallet integrations, which enable quick and easy enrollment at the register. Major retail chains are partnering with buy now,w pay later providers to offer consistent payment options across both online and offline channels, creating a unified customer experience. The ability to split payments for high-ticket items, such as furniture and electronics, in-store, encourages larger purchases and increases average transaction values. In-store associates are trained to promote these options at the point of decision, enhancing conversion rates. The visibility of buy now pay later signage in physical stores raises awareness among consumers, who may not be familiar with the service online. This strategic push into physical retail environments is unlocking new revenue streams and driving rapid adoption among traditional shoppers.

By End User Type Insights

The fashion and apparel segment led the market in 2025 due to the high frequency of purchases, the emotional nature of clothing shopping, and the strong alignment with fast fashion trends. The fashion and apparel sector benefits from the high frequency of consumer purchases and the rapid turnover of trends, which drives consistent demand for flexible payment options. According to Empower research data from June 2025, approximately 39% of buy now pay later consumers use the service specifically to purchase clothing and fashion accessories. The impulsive nature of fashion shopping often leads to basket sizes that exceed immediate budget constraints, making installment plans an attractive solution for managing cash flow. Fast fashion retailers have heavily adopted buy now, pay later services to encourage larger basket sizes and repeat visits. The ability to try on clothes and return them easily, combined with the flexibility of delayed payments, reduces the perceived risk of online clothing purchases. Younger consumers, who are the primary drivers of fashion trends, are also the most likely users of buy now, pay later services, creating a strong demographic overlap. Social media influences and seasonal sales events further stimulate demand, prompting consumers to utilize flexible payment methods to maximize their purchasing power. The visual and aspirational nature of fashion marketing complements the instant gratification offered by buy now, pay later models. This synergy between consumer behavior and payment flexibility ensures that fashion and apparel remain the leading end-user segment in the market.

On the other hand, the home improvement segment is expected to expand at a CAGR of 31.3% during the forecast period in the U.S. market, owing to the rising housing costs and the increasing trend of home renovation projects. The rising cost of housing and the subsequent trend of homeowners investing in renovations, rather than moving, are driving rapid growth in the home improvement segment. According to Motley Fool Money research, furniture and appliances accounted for 36% of buy now pay later purchases by 2025, reflecting significant investment in living spaces. Buy now,w pay later services provide a viable financing alternative for these projects, which often involve upfront costs for materials and labor. Consumers are using these services to purchase furniture, appliances, and building materials, allowing them to spread the financial burden over time. The ability to finance home upgrades without tapping into home equity lines of credit or high-interest personal loans is particularly appealing to middle-income households. The DIY culture has also expanded, with more individuals undertaking smaller projects that are well-suited for short-term installment plans. The visibility of home improvement projects on social media platforms inspires consumers to invest in their living environments, further fueling demand. The practical nature of these purchases, combined with the financial flexibility of buy now, pay later, makes this segment a high-growth area. As housing markets remain tight, the focus on improving existing homes will continue to drive adoption in this category.

By Age Group Insights

The millennial age group segment captured the leading share of the U.S. buy now pay later market in 2025. The growth of the millennial age group segment in the U.S. market can be credited to their substantial purchasing power, their comfort with digital financial tools, and their preference for flexible budgeting methods. Millennials exhibit high digital fluency and a strong preference for financial tools that offer transparency and control, which aligns perfectly with the buy now, pay later model. According to the Federal Reserve Bank of Philadelphia, millennials and Gen Z together account for approximately 50% of the buy now pay later consumer base as of 2024. This generation has grown up with internet technology and is comfortable managing finances through mobile applications and online platforms. They are often skeptical of traditional credit cards, due to hidden fees and complex interest structures, preferring the straightforward nature of installment plans. The ability to track payments and avoid debt traps through clear scheduling appeals to their desire for financial stability. Millennials are also in a life stage characterized by major expenditures, such as home furnishings and family needs, making flexible payment options highly relevant. Their influence on retail trends encourages merchants to prioritize buy now, pay later integration to capture this valuable demographic. The social aspect of sharing financial tips and recommendations within peer networks further amplifies adoption. The combination of technological comfort and financial prudence ensures that millennials remain the dominant user group in the market.

However, the Generation Z segment is the fastest-growing age group in the U.S. buy now pay later market and is projected to progress at a CAGR of 24.4% during the forecast period, owing to their entry into the workforce, their digital native status, and their inclination toward ethical and flexible consumption. The entry of Generation Z into the workforce and their early adoption of fintech solutions are primary drivers of their rapid growth in the buy now pay later market. According to research from Fortune, approximately 30 million young people in the U.S., or 44% of Gen Z, utilized buy now pay later services by mid 2025. As they begin earning income, they are establishing their financial habits and preferences, with buy now, pay later often being their first experience with credit-like products. The ease of access and lack of hard credit checks make these services appealing to young adults with limited credit history. They view buy now, pay later as a tool for building financial independence and managing entry-level salaries effectively. The integration of these services with social commerce platforms, where Generation Z spends significant time, further accelerates adoption. Influencer marketing and peer recommendations play a crucial role in shaping their financial behaviors. The transparency and simplicity of the model resonate with their values of honesty and clarity. As this generation gains economic power, their usage of buy now, pay later is expected to expand rapidly, driving overall market growth.

COUNTRY LEVEL ANALYSIS

U.S.

The United States is projected to solidify its status as the world's most advanced buy now pay later ecosystem over the next few years, as traditional banking institutions increasingly integrate these flexible credit solutions into their core offerings. The U.S. stands as the largest and most mature market for buy now pay later services globally due to the high consumer adoption, extensive merchant integration, and a dynamic regulatory environment that shapes industry practices. The U.S. benefits from high consumer adoption rates and extensive integration of buy now,w pay later services across a diverse range of merchants. According to the Federal Reserve Bank of Philadelphia, approximately 20.4% of survey respondents in Q4 2024 had used these products, a steady increase that underscores their widespread acceptance. The presence of major fintech players and traditional financial institutions entering the space has created a competitive landscape that drives innovation and accessibility. Consumers in the U.S. are accustomed to digital payment methods and value the flexibility offered by instalment plans, particularly in the context of high inflation and economic uncertainty. The integration of these services into major e-commerce platforms and physical retail stores ensures that they are readily available for a wide variety of purchases. The cultural emphasis on consumerism and immediate gratification aligns well with the buy now, pay later model. The robust digital infrastructure and high smartphone penetration facilitate seamless user experiences. The diversity of the US retail market allows for broad application of these services across different sectors, from fashion to home improvement. This comprehensive ecosystem supports sustained growth and solidifies the U.S. position as the global leader in the buy now, pay later market.

COMPETITIVE LANDSCAPE

The competition in the U.S. buy now pay later market is intense and characterized by the presence of specialized fintech firms and established financial giants vying for dominance. Specialized providers leverage innovative technology and user-centric designs to attract younger demographics seeking transparent and flexible payment options. Traditional financial institutions and payment processors utilize their extensive merchant networks and brand trust to capture market share through seamless integrations. Differentiation is achieved through unique value propositions such as no-fee structures, rewards programs, and extended repayment terms. The barrier to entry is relatively low, ow leading to a fragmented landscape with numerous players competing for merchant partnerships. Consolidation through mergers and acquisitions is common as larger entities seek to scale rapidly and diversify their offerings. Regulatory scrutiny adds complexity,ity requiring companies to balance growth with compliance and responsible lending practices. Customer loyalty is driven by ease of use and reliability,lity prompting continuous investment in platform stability and customer support. The competitive dynamics foster rapid innovation but also pressure profit margins as companies subsidize costs to gain market traction. This environment necessitates strategic agility and strong capital reserves for sustained success.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S buy now pay later (BNPL) market include

- Affirm Holdings, Inc.

- Afterpay US Services, LLC

- Klarna Inc.

- PayPal Holdings, Inc.

- Zip Co Limited (Quadpay)

- Sezzle Inc.

- Splitit Payments Ltd.

- Perpay Inc.

- Uplift, Inc.

- Amazon.com, Inc.

- Synchrony Financial

- American Express Company

TOP LEADING PLAYERS IN THE MARKET

- Affirm Holdings Inc is a pioneering force in the U.S. buy now pay later sector, known for its transparent pricing and consumer-friendly approach. The company partners with major retailers to offer installment loans at the point of sale without hidden fees or compounding interest. Recent actions include expanding its partnership network to include large e-commerce platforms and physical retail chains. Affirm has also launched a debit card product that integrates directly with its app, allowing users to manage payments and earn rewards. This strategic move enhances customer retention and increases engagement within its ecosystem. The company focuses on responsible lending practices using advanced machine learning models for real-time credit decisions. By prioritizing user experience and financial transparency, Affirm strengthens its position as a trusted provider in the competitive fintech landscape. Its continuous innovation in product offerings ensures it remains relevant to diverse consumer segments.

- PayPal Holdings Inc leverages its extensive global payment network to dominate the buy now,w pay later space through its Pay in 4 service. The company integrates this feature seamlessly into its existing checkout infrastructure, providing millions of merchants with immediate access to flexible payment options. Recent initiatives involve enhancing the visibility of Pay in 4 at online checkouts and expanding eligibility criteria to reach more consumers. PayPal utilizes its vast data resources to offer personalized financing options while maintaining robust fraud detection systems. The company actively promotes its own, with pay-later services through targeted marketing campaigns and merchant incentives. By embedding these services within its broader digital wallet ecosystem, PayPal drives higher transaction volumes and customer loyalty. Its established brand trust and widespread acceptance among retailers provide a significant competitive advantage. PayPal continues to innovate by exploring longer-term financing options to meet evolving consumer needs.

- Block Inc contributes significantly to the U.S. buy now pay later market through its Afterpay platform, which it acquired to expand its financial services portfolio. Afterpay allows consumers to split purchases into four interest-free installments, appealing to younger demographics. Block has integrated Afterpay into its Cash App ecosystem,m enabling seamless transfers and enhanced user convenience. Recent actions include launching shopping directories and exclusive deals within the app to drive engagement and repeat usage. The company focuses on building a comprehensive commerce ecosystem that connects merchants and consumers through flexible payment solutions. Block leverages its technological expertise to improve risk management and operational efficiency for Afterpay. By combining the strengths of Cash App and Afterpay, ay Block creates a powerful platform for financial inclusion. This integration strategy strengthens its market position by offering a holistic financial experience that extends beyond simple transactions.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the U.S. buy now pay later market primarily focus on strategic partnerships with major retailers to expand their merchant networks and increase transaction volume. Companies invest heavily in technology to enhance user experience through seamless integration and instant approval processes. Diversification of product offerings includes launching debit cards and savings accounts to create comprehensive financial ecosystems. Marketing efforts emphasize transparency and responsible lending to build consumer trust and differentiate from traditional credit products. Expansion into physical retail channels via point of sale integrations captures offline spending opportunities. Data analytics are utilized for personalized marketing and improved assessments, ensuring sustainable growth. Regulatory compliance is prioritized to navigate evolving legal landscapes and maintain operational legitimacy. These strategies collectively enable providers to strengthen their market positions and adapt to changing consumer preferences in the dynamic financial technology sector.

MARKET SEGMENTATION

This research report on the U.S. buy now pay later market is segmented and sub-segmented into the following categories.

By Channel

- Online

- Point-of-Sale (POS)

By End-User Type

- Fashion & Apparel

- Home Improvement

By Age Group

- Millennials

- Generation Z

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States