U.S. C Arms Market Size, Share, Trends & Growth Forecast Report Segmented By Type (Fixed C-arms, Mobile C-arms, Full-size C-arms, Mini C-arms), Detector, Application and Country – Industry Analysis From 2026 to 2034

U.S. C Arms Market Report Summary

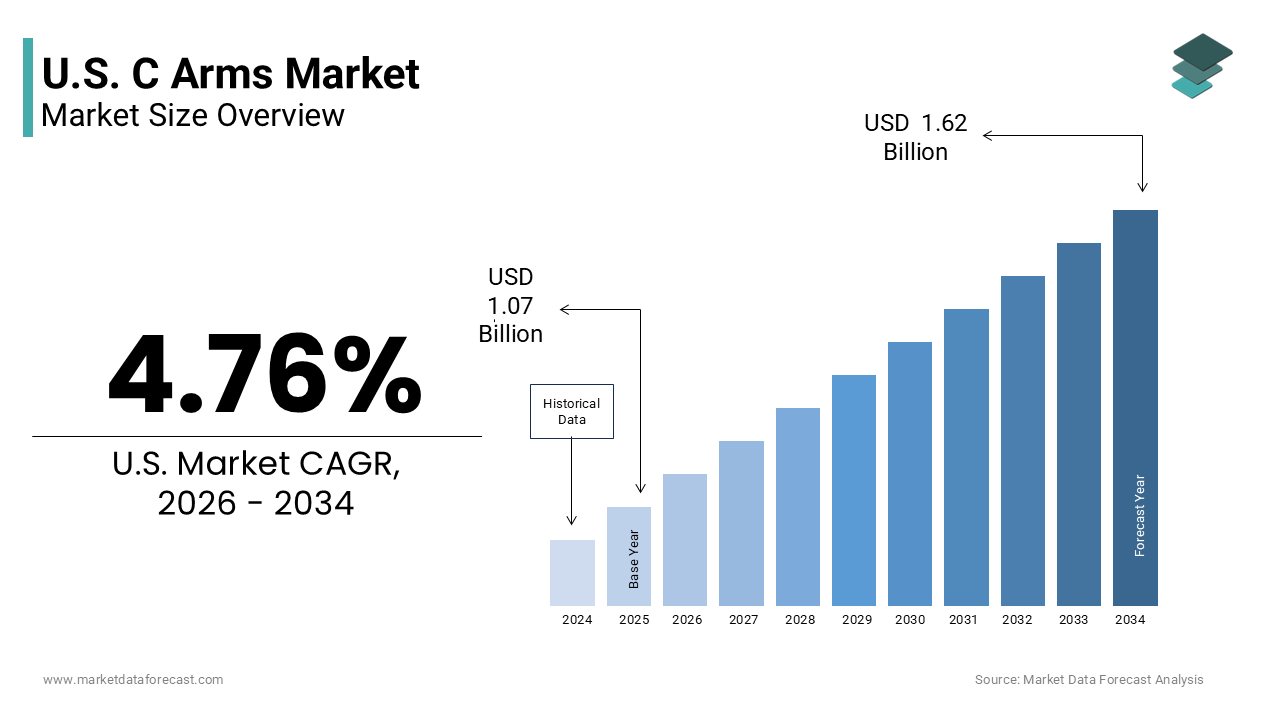

The U.S. C Arms market was valued at USD 1.07 billion in 2025 and is anticipated to reach USD 1.12 billion in 2026 from USD 1.62 billion by 2034, growing at a CAGR of 4.76% during the forecast period from 2026 to 2034. The growth of the U.S. C Arms market is driven by the increasing volume of minimally invasive surgical procedures, rising prevalence of cardiovascular and orthopedic disorders, and growing demand for real-time image-guided interventions. Expanding adoption of advanced fluoroscopic imaging technologies, increasing utilization of outpatient surgical facilities, and growing investments in healthcare infrastructure are further accelerating market growth. Moreover, the integration of artificial intelligence-enabled imaging software, expansion of ambulatory surgical centers, and increasing focus on radiation dose optimization are supporting the expansion of the U.S. C Arms market.

Key Market Trends

- Rising adoption of artificial intelligence-assisted imaging technologies for enhanced image quality and workflow efficiency.

- Increasing utilization of mobile C Arms across operating rooms, emergency departments, and ambulatory surgical centers.

- Growing demand for minimally invasive surgical procedures requiring real-time fluoroscopic guidance.

- Strong focus on low-dose imaging technologies and radiation safety improvements for patients and healthcare professionals.

- Expansion of outpatient and ambulatory care facilities driving demand for compact and portable imaging systems.

Segmental Insights

- Based on type, the mobile C Arms segment dominated the U.S. C Arms market and held the largest share in 2025. The segment’s dominance is attributed to its portability, operational flexibility, widespread adoption across hospitals and ambulatory surgical centers, and ability to support a broad range of surgical and diagnostic applications.

- The mini C Arms segment is projected to witness the fastest CAGR during the forecast period owing to increasing demand for extremity imaging, growing adoption in podiatry and orthopedic clinics, lower radiation exposure, and improved workflow efficiency in office-based procedures.

- Based on application, the orthopedics and trauma segment accounted for the leading share of the U.S. C Arms market in 2025. The dominance of this segment is driven by the high volume of fracture repair procedures, joint replacement surgeries, spinal interventions, and increasing prevalence of musculoskeletal disorders among the aging population.

- The cardiology segment is anticipated to register notable growth during the forecast period due to the rising prevalence of cardiovascular diseases, increasing adoption of catheter-based interventions, growing demand for structural heart procedures, and expansion of advanced cardiac imaging capabilities.

- Based on detector, the flat panel detector segment held the major share of the U.S. C Arms market in 2025 owing to superior image quality, reduced image distortion, lower radiation exposure, improved durability, and compatibility with advanced imaging applications.

- The image intensifier segment is expected to witness moderate growth during the forecast period because of its continued use in cost-sensitive healthcare facilities and established presence across existing imaging infrastructure.

- Based on end user, the hospitals segment dominated the U.S. C Arms market in 2025 due to high surgical procedure volumes, advanced healthcare infrastructure, specialized clinical expertise, and strong investment capacity for advanced imaging technologies.

- The specialty clinics segment is projected to witness the fastest CAGR during the forecast period owing to increasing outpatient procedure volumes, rising demand for image-guided pain management treatments, and expanding orthopedic and ambulatory surgical center networks.

Regional Insights

The United States maintained a strong position in the global C Arms market in 2025, supported by advanced healthcare infrastructure, increasing procedural volumes, and widespread adoption of image-guided surgical technologies. California remains a major contributor to the U.S. C Arms market due to its large healthcare network, high concentration of specialty surgical centers, and strong investment in advanced medical imaging technologies. New York, Washington, and Oregon are also witnessing notable growth driven by increasing adoption of minimally invasive procedures, rising healthcare expenditure, and expanding outpatient care infrastructure.

Competitive Landscape

The U.S. C Arms market is highly competitive and characterized by the presence of global medical imaging manufacturers, specialized fluoroscopy providers, and niche imaging technology companies competing through innovation, image quality enhancement, and workflow optimization. Leading companies are focusing on developing advanced flat panel detector systems, integrating artificial intelligence-driven imaging software, strengthening radiation dose reduction technologies, and expanding portable imaging solutions. Strategic collaborations with hospitals, ambulatory surgical centers, and research institutions are further strengthening market positioning across orthopedic, cardiovascular, and minimally invasive surgical applications. Prominent players in the U.S. C Arms market include GE HealthCare, Siemens Healthineers, Philips Healthcare, Canon Medical Systems Corporation, Shimadzu Corporation, Ziehm Imaging GmbH, FUJIFILM Healthcare, Hologic, Inc., Carestream Health, and OrthoScan, Inc.

U.S. C Arms Market Size

The U.S. C Arms market size was valued at USD 1.07 billion in 2025 and is anticipated to reach USD 1.12 billion in 2026 from USD 1.62 billion by 2034, growing at a CAGR of 4.76% during the forecast period from 2026 to 2034.

The C-arms are the medical imaging devices, designed to provide real time visualization of internal anatomical structures during surgical and diagnostic procedures. These devices feature a C shaped arm that connects an X ray source to a detector, allowing for multi angle imaging without moving the patient. The clinical utility of C arms spans across orthopedics cardiology pain management and trauma care where precise guidance is essential for minimally invasive interventions. As per the American Academy of Orthopaedic Surgeons over 1.5 million joint replacement and fracture repair surgeries are performed annually in the United States many of which rely on intraoperative fluoroscopy for accurate implant placement and alignment. Furthermore, the Centers for Disease Control and Prevention states that cardiovascular disease remains the leading cause of death affecting approximately 695000 people in the country each year which drives the high volume of cardiac catheterization and electrophysiology procedures requiring advanced imaging support. The aging demographic profile further amplifies demand as individuals over the age of 65 are more prone to conditions necessitating image guided interventions.

MARKET DRIVERS

Increasing Volume Of Minimally Invasive Surgical Procedures

The escalating volume of minimally invasive surgical procedures is accelerating the growth of the United States C arms market. Minimally invasive techniques, such as laparoscopic surgery, endovascular repairs, and percutaneous spinal interventions, require precise real time imaging to guide instruments through small incisions thereby reducing tissue damage and recovery time. As per the American College of Surgeons minimally invasive surgeries account for over 60% of all general surgical procedures performed in the country reflecting a significant shift away from traditional open surgeries. The preference for these techniques is driven by benefits such as reduced hospital stays lower infection rates and faster return to daily activities. The average length of stay for minimally invasive procedures is significantly shorter than for open surgeries, which encourages hospitals to invest in advanced imaging equipment to support high throughput operations. Additionally, the rising prevalence of chronic conditions such as obesity and diabetes increases the complexity of surgical cases necessitating enhanced visualization capabilities to ensure patient safety. The integration of C arms into operating rooms allows surgeons to navigate complex anatomies with greater confidence reducing the risk of complications. The widespread adoption of minimally invasive approaches creates a consistent and growing demand for high performance C arm systems that offer superior image quality and ergonomic design to meet the rigorous demands of modern surgical workflows.

Growing Prevalence Of Cardiovascular And Orthopedic Disorders

The growing prevalence of cardiovascular and orthopedic disorders are creating a substantial patient pool requiring image guided diagnostic and therapeutic interventions, which is escalating the growth of the United States C arms market. Cardiovascular diseases, including coronary artery disease and arrhythmias often require catheter based procedures, such as angioplasty and stent placement, which rely heavily on fluoroscopic guidance for precision. As per the Centers for Disease Control and Prevention, heart disease affects approximately 20.1 million adults in the United States with millions undergoing cardiac catheterizations annually. Similarly, orthopedic conditions, such as osteoarthritis and fractures are prevalent among the aging population necessitating surgical repairs that utilize C arms for accurate alignment and fixation. The musculoskeletal conditions are the second most common cause of disability in the United States leading to a high volume of orthopedic surgeries. The increasing incidence of these disorders drives the utilization of C arms in both emergency and elective settings ensuring timely and effective treatment. Hospitals and ambulatory surgical centers are expanding their imaging capabilities to accommodate the rising number of patients requiring these specialized procedures. The ability of C arms to provide clear and detailed images of bones and blood vessels enhances diagnostic accuracy and procedural success.

MARKET RESTRAINTS

High Costs Associated With Advanced Imaging Systems

The high costs associated with advanced C arm systems is one of the major restraining factors for the growth of the United States C arms market. State of the art flat panel detector C arms with 3D imaging capabilities and low dose technologies require significant capital investment, which can be prohibitive for smaller hospitals and rural healthcare facilities. The average cost of a high end mobile C arm can exceed 250000 dollars, excluding maintenance and operational expenses. This financial burden is exacerbated by the need for regular upgrades to keep pace with technological advancements and regulatory requirements. The rising healthcare costs continue to strain hospital budgets forcing administrators to prioritize essential services over premium equipment purchases. Reimbursement rates for imaging procedures have not kept pace with inflation limiting the revenue potential for healthcare providers investing in new technology. Many facilities opt to extend the lifecycle of existing equipment rather than replacing it with newer models due to budget constraints. This economic barrier limits the widespread adoption of advanced C arm features such as digital subtraction angiography and cone beam computed tomography.

Stringent Regulatory Standards For Radiation Safety

The stringent regulatory standards for radiation safety by imposing rigorous compliance requirements that increase operational complexity and costs, which is limiting the growth of the United States C arms market. The Food and Drug Administration and the Conference of Radiation Control Program Directors mandate strict guidelines for radiation exposure limits equipment performance and personnel training to protect patients and healthcare workers. The regulations medical device manufacturers must undergo extensive premarket approval processes to demonstrate the safety and efficacy of new C arm systems, which can delay product launches. Healthcare facilities are required to implement comprehensive radiation safety programs, including regular equipment calibration dose monitoring and staff certification. These standards requires dedicated resources and specialized personnel adding to the operational burden of healthcare institutions. Non-compliance can result in severe penalties licensure revocation and legal liabilities making healthcare providers cautious about adopting new technologies without exhaustive validation. The fear of regulatory scrutiny often leads to conservative purchasing decisions favoring established vendors over innovative startups. Furthermore, frequent updates to safety guidelines necessitate continuous education and system upgrades increasing long term costs.

MARKET OPPORTUNITIES

Integration Of Artificial Intelligence And Advanced Software

The integration of artificial intelligence and advanced software is enhancing image quality and procedural efficiency, which is attributed in creating new opportunities for the growth of the United States C arms market. AI algorithms can optimize image acquisition reduce noise and automatically adjust exposure settings to minimize radiation dose while maintaining diagnostic clarity. Advanced software features, such as automatic vessel detection and bone segmentation assist surgeons in navigating complex anatomies with greater precision reducing procedure times and improving outcomes. The research funding for AI in medical imaging has increased substantially fostering innovation in intelligent imaging solutions. The ability of AI to analyze real time data and provide predictive insights supports decision making during critical interventions. Manufacturers have the opportunity to develop smart C arms that integrate seamlessly with electronic health records and hospital information systems enhancing workflow efficiency. BThe adoption of AI driven features differentiates products in a competitive market and appeals to healthcare providers seeking to enhance patient safety and operational efficiency through digital transformation.

Expansion Of Ambulatory Surgical Centers And Outpatient Care

The expansion of ambulatory surgical centers and outpatient care facilities is another factor to boost new opportunities for the expansion of the United States C arms market. Ambulatory surgical centers are increasingly performing complex procedures that were traditionally conducted in hospitals driven by cost containment efforts and patient preference for convenient care settings. The number of certified ASCs in the United States has grown to over 6000 with many specializing in orthopedics pain management and gastroenterology. These facilities require mobile C arms that are easy to operate space efficient and capable of delivering high quality images for a variety of procedures. The outpatient procedures are reimbursed at lower rates encouraging the shift of services to ASCs, where overhead costs are reduced. The portability and ease of use of modern C arms make them ideal for these high turnover environments where efficiency is paramount. Manufacturers can capitalize on this trend by developing lightweight and user-friendly systems tailored to the specific needs of outpatient settings.

MARKET CHALLENGES

Shortage Of Skilled Radiologic Technologists

The shortage of skilled radiologic technologists is limiting the capacity of healthcare facilities to operate imaging equipment effectively, which is likely to be one of the major challenges for the growth of the United States C arms market. The complexity of modern C arm systems requires specialized training and expertise to ensure optimal image quality and patient safety yet the pipeline of qualified professionals is insufficient to meet growing demand. The workforce gap leads to increased workload for existing staff contributing to burnout and higher turnover rates. The demand for radiologic technologists is projected to grow but the supply of graduates remains inadequate to fill open positions. The lack of skilled personnel hinders the adoption of advanced C arm technologies that require sophisticated operation and maintenance. Additionally, the reliance on temporary staffing agencies increases operational costs and reduces continuity of care. This labor crisis forces healthcare providers to seek automation and user-friendly interfaces to compensate for human resource deficits but the transition period remains challenging.

Risk Of Radiation Exposure And Biological Effects

The risk of radiation exposure and its potential biological effects with both clinical practice and regulatory oversight is also to impede the growth of the United States C arms market. Prolonged or excessive exposure to ionizing radiation during fluoroscopic procedures can lead to deterministic effects, such as skin injuries and stochastic effects for both patients and healthcare workers. As per the National Council on Radiation Protection and Measurements, occupational exposure to radiation remains a significant concern for interventional cardiologists and surgeons who frequently use C arms. The healthcare workers in catheterization laboratories have a higher incidence of cataracts and other radiation related health issues compared to the general population. This risk necessitates stringent safety protocols protective gear and continuous monitoring which add to the complexity and cost of procedures. Patients are also becoming more aware of radiation risks leading to increased scrutiny of imaging practices. Manufacturers must continuously innovate to reduce dose levels while maintaining image quality a challenging technical balance. Negative public perception regarding radiation safety can deter patients from undergoing necessary procedures impacting procedural volumes.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.76% |

| Segments Covered | By Type, Detector, Application and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | GE HealthCare, Siemens Healthineers, Philips Healthcare, Canon Medical Systems Corporation, Shimadzu Corporation, Ziehm Imaging GmbH, FUJIFILM Healthcare, Hologic, Inc., Carestream Health, and OrthoScan, Inc. |

SEGMENTAL ANALYSIS

By Type Insights

The mobile C arms segment was the dominant by holding 54.3% of the United States C arms market share in 2025 due to their versatility portability and widespread adoption across various clinical settings. Unlike fixed systems, which are confined to specific rooms mobile C arms can be easily transported between operating rooms emergency departments and intensive care units allowing for flexible usage in diverse medical procedures. There are over 6000 hospitals in the United States with a significant majority utilizing mobile imaging solutions to support high patient volumes and efficient workflow management. The ability to perform intraoperative imaging without moving critically ill patients is a critical advantage in trauma and surgical care. According to the Centers for Disease Control and Prevention, approximately 139 million visits are made to hospital emergency departments annually many of which require immediate diagnostic imaging for fractures and foreign body detection. Mobile C arms facilitate rapid assessment and treatment in these time sensitive scenarios. Furthermore, the rise of ambulatory surgical centers has increased the demand for compact and easy to operate imaging devices that do not require extensive infrastructure. The American Ambulatory Surgery Center Association notes that over 6000 ASCs operate in the country relying heavily on mobile fluoroscopy for orthopedic and pain management procedures. The cost effectiveness of mobile units compared to fixed installations also drives their preference among smaller healthcare facilities.

The mini C arms segment is esteemed to grow at a fastest CAGR of 6.8% during the forecast period with the increasing demand for specialized imaging solutions in extremity surgery and podiatry where high resolution images of small bones are required. Mini C arms offer a smaller footprint and lower radiation dose compared to full size systems making them ideal for office-based procedures and ambulatory surgical centers. As per the American Podiatric Medical Association, over 1.5 million foot and ankle surgeries are performed annually in the United States many of which utilize mini C arms for precise guidance. The convenience of having a dedicated imaging device in the operating room or clinic reduces workflow interruptions and improves efficiency. According to the Journal of Foot and Ankle Surgery the use of mini C arms has been shown to reduce procedure times by up to 20% compared to traditional large C arms. The lower cost of acquisition and maintenance also appeals to private practices and specialty clinics looking to expand their service offerings. Additionally, advancements in digital detector technology have improved image quality making mini C arms competitive with larger systems for specific applications.

By Application Insights

The orthopedics and trauma segment was accounted in holding 44.3% of the United States C arms market share in 2025 due to the high volume of surgical procedures requiring intraoperative imaging for bone and joint repairs. Fracture fixation joint arthroplasty and spinal fusion are common interventions that rely on fluoroscopy to ensure proper alignment and stability of implants. As per the American Academy of Orthopaedic Surgeons, approximately 1.5 million total knee and hip replacements are performed annually in the United States with each procedure typically requiring extensive use of C arm imaging. Additionally, trauma cases involving complex fractures necessitate real time visualization to guide the placement of screws plates and rods. The Centers for Disease Control and Prevention reports that falls are the leading cause of injury related deaths among adults aged 65 and older resulting in millions of emergency department visits and subsequent orthopedic surgeries each year. The aging population contributes significantly to this burden as older individuals are more prone to osteoporotic fractures and degenerative joint diseases. Hospitals and trauma centers prioritize the availability of high-performance C arms to handle the influx of emergency cases efficiently. The integration of C arms into orthopedic workflows has become standard practice enhancing surgical precision and reducing complication rates.

The cardiology segment is likely to grow at a fastest CAGR of 7.2% from 2026 to 2034 with the increasing prevalence of cardiovascular diseases and the rising number of interventional cardiology procedures, such as angioplasty stenting and electrophysiology studies. As per the Centers for Disease Control and Prevention, heart disease remains the leading cause of death in the United States affecting approximately 695000 people annually. The demand for minimally invasive cardiac interventions has surged as these procedures offer faster recovery times and lower risks compared to open heart surgery. According to the American College of Cardiology, over 1 million cardiac catheterizations are performed each year in the country many of which utilize advanced C arm systems with flat panel detectors for high resolution vascular imaging. The development of structural heart interventions such as transcatheter aortic valve replacement TAVR has further expanded the use of C arms in cardiology suites. These complex procedures require precise three dimensional visualization and real time guidance which modern C arms provide. Hospitals are upgrading their catheterization laboratories with state of the art imaging equipment to support these advanced therapies.

By Detector Insights

The flat panel detectors segment was the dominant by capturing 32.1% of the United States C arms market share in 2025 due to their superior image quality compact design and enhanced durability compared to traditional image intensifiers. These detectors provide high resolution digital images with excellent contrast and minimal distortion enabling surgeons to visualize fine anatomical details with greater clarity. The flat panel technology has become the standard of care in many hospitals and ambulatory surgical centers due to its ability to support advanced imaging features, such as digital subtraction angiography and road mapping. The compact size of flat panel detectors allows for easier maneuverability in crowded operating rooms and reduces the overall footprint of the C arm system. The absence of moving parts in flat panel detectors also reduces maintenance requirements and increases reliability. Healthcare providers value these advantages for improving diagnostic accuracy and procedural efficiency. The gradual phase out of image intensifier technology by major manufacturers further accelerates the adoption of flat panel systems.

The flat panel detectors segment is anticipated to grow at a fastest CAGR of 8.5% from 2026 to 2034 owing to the ongoing replacement of outdated image intensifier systems with modern flat panel technology across healthcare facilities. The regulatory pressures and safety standards encourage the adoption of newer technologies that offer lower radiation doses and better performance. Many hospitals are upgrading their imaging equipment to meet these standards and improve operational efficiency. The total cost of ownership for flat panel systems is becoming more competitive due to reduced maintenance needs and longer lifespan compared to image intensifiers. The availability of refurbished flat panel C arms also makes this technology accessible to smaller clinics and ambulatory surgical centers. Manufacturers are introducing cost effective models specifically designed for budget conscious buyers further accelerating adoption. The transition to digital workflows in healthcare also favors flat panel detectors which integrate seamlessly with electronic health records.

By End User Insights

The hospitals segment was the largest by accounting for 21.2% of the United States C arms market share in 2025 due to their capacity to perform a high volume of complex surgical and diagnostic procedures. These facilities possess the necessary infrastructure specialized medical staff and financial resources to invest in advanced imaging equipment. The concentration of emergency departments and operating rooms in hospitals creates a consistent demand for mobile and fixed C arms to support urgent and elective cases. The ability of hospitals to handle complex cases, such as multi-level spinal fusions and structural heart interventions necessitates the use of high end C arm systems with advanced features. Large academic medical centers and trauma hubs further drive demand by performing specialized procedures that require precise imaging guidance. The consolidation of healthcare systems has also led to standardized purchasing agreements that favor established suppliers.

The specialty clinics segment is swiftly growing at an anticipates CAGR of 7.5% during the forecast period with the increasing shift of outpatient procedures from hospitals to specialized clinics such as orthopedic centers pain management clinics and ambulatory surgical centers. These facilities offer cost effective and convenient care for patients requiring minor surgical interventions and diagnostic imaging. The rise in chronic pain conditions and musculoskeletal disorders has increased the demand for image guided injections and minor surgeries in outpatient settings. According to the American Academy of Pain Medicine millions of epidural and facet joint injections are performed annually many of which take place in specialty clinics. The lower overhead costs and faster turnaround times of specialty clinics attract patients and payers alike. Reimbursement policies increasingly favor outpatient care encouraging the expansion of these facilities. Specialty clinics are also adopting advanced imaging technologies to compete with hospitals and offer comprehensive care.

COMPETITIVE LANDSCAPE

The competition in the United States C arms market is characterized by the presence of established global manufacturers and specialized niche players who strive to differentiate themselves through technological innovation and service quality. Major corporations leverage their extensive distribution networks and broad product portfolios to capture significant portions of the hospital and ambulatory surgical center segments. These industry leaders continuously invest in research and development to introduce advanced imaging platforms that enhance procedural efficiency and patient safety. Smaller companies often focus on specific applications such as mini C arms for extremity surgery or specialized veterinary imaging to carve out niche market positions. The market witnesses frequent strategic alliances and collaborations aimed at expanding geographic reach and enhancing product capabilities. Regulatory compliance serves as a significant barrier to entry favoring companies with robust quality management systems and financial resources. Price competition is moderate as healthcare providers prioritize image quality and reliability over cost when selecting diagnostic solutions. However, value based care initiatives are prompting manufacturers to demonstrate the economic benefits of their technologies.

KEY MARKET PLAYERS

Some of the promising companies that are playing a dominating role in the U.S. C arms market include

- GE HealthCare

- Siemens Healthineers

- Philips Healthcare

- Canon Medical Systems Corporation

- Shimadzu Corporation

- Ziehm Imaging GmbH

- FUJIFILM Healthcare

- Hologic, Inc.

- Carestream Health

- OrthoScan, Inc.

Top Players in the United States C Arms Market

GE HealthCare Technologies Inc

GE HealthCare Technologies Inc is a pivotal leader in the United States C arms market offering a comprehensive portfolio of mobile and fixed fluoroscopy systems. The company contributes significantly to clinical excellence through its OEC and Brivo series which provide high resolution imaging with advanced dose management features. Recent actions to strengthen its market position include the integration of artificial intelligence algorithms into its imaging platforms to enhance workflow efficiency and image quality. GE HealthCare actively collaborates with healthcare providers to develop customized solutions that address specific clinical needs in orthopedics and cardiology. The company also invests heavily in research and development to introduce compact and lightweight C arms suitable for ambulatory surgical centers.

Siemens Healthineers AG

Siemens Healthineers AG plays a critical role in the United States C arms market by delivering advanced imaging technologies, such as the Arcadis and Luminos series. The company is renowned for its flat panel detector technology which offers superior image clarity and reduced radiation exposure for patients and staff. Recent efforts to bolster its market presence include the launch of smart guidance software that assists surgeons in real time during complex procedures. Siemens Healthineers actively engages in partnerships with academic medical centers to validate new imaging protocols and improve clinical outcomes. The company also expands its service offerings to include predictive maintenance and remote monitoring capabilities that enhance equipment uptime.

Koninklijke Philips NV

Koninklijke Philips NV significantly influences the United States C arms market through its innovative Zenition and Veradius mobile C arm systems. The company focuses on providing ergonomic and user friendly designs that facilitate ease of use in diverse clinical settings. Recent actions to strengthen its position include the enhancement of its Image Guided Therapy suite with advanced visualization tools and cloud based data analytics. Philips actively promotes value based care by offering solutions that reduce procedure times and improve patient throughput. The company also invests in training programs for radiologic technologists and surgeons to ensure optimal utilization of its technologies.

Top Strategies Used by Key Market Participants

Key players in the United States C arms market primarily focus on technological innovation and strategic collaborations to maintain their competitive edge. Companies invest heavily in research and development to create advanced flat panel detector systems that offer higher resolution and lower radiation doses. The integration of artificial intelligence and machine learning into imaging software is a common strategy to enhance diagnostic accuracy and workflow efficiency. Manufacturers also pursue mergers and acquisitions to expand their product portfolios and access new markets or technologies. Partnerships with healthcare providers and academic institutions facilitate clinical validation and accelerate the adoption of novel imaging techniques. Additionally, companies emphasize service and support offerings such as remote monitoring and predictive maintenance to build long term relationships with customers. Regulatory compliance and quality assurance remain central to their strategies as they navigate stringent federal guidelines.

MARKET SEGMENTATION

This research report on the U.S. C arms market has been segmented based on the following categories.

By Type

- Fixed C-arms

- Mobile C-arms

- Full-size C-arms

- Mini C-arms

By Detector

- Flat Panel Detector

- Image Intensifier

By Application

- Orthopedics and Trauma

- Cardiology

- Neurology

- Gastroenterology

- Oncology

- Others

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com