U.S Color Cosmetics Market Size, Share, Trends & Growth Forecast Report Segmented By Target Market (Prestige Products, Mass Products), Distribution Channel, Application, And Country (California, Washington, Oregon, New York & Rest of The United States) – Industry Analysis and Forecast, 2026 To 2034

U.S. Color Cosmetics Market Report Summary

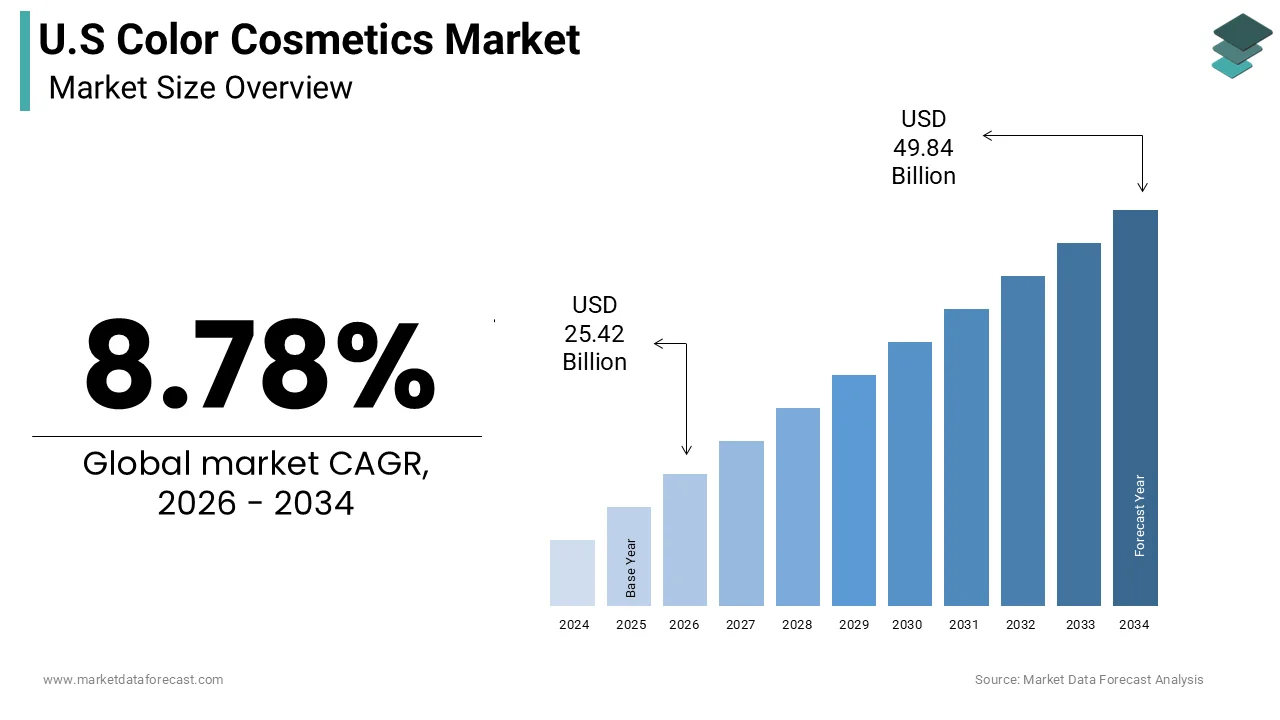

The United States color cosmetics market was valued at USD 23.37 billion in 2025 and is projected to reach USD 49.84 billion by 2034, growing from USD 25.42 billion in 2026 at a CAGR of 8.78% during the forecast period. Market growth is driven by rising beauty consciousness, increasing social media influence, and growing demand for premium and personalized cosmetic products. Innovations in vegan, cruelty-free, and long-lasting makeup formulations are further accelerating the growth of the U.S. color cosmetics market.

Key Market Trends

- Rising demand for vegan and cruelty-free cosmetics

- Increasing influence of beauty influencers and social media marketing

- Growth in premium and personalized makeup products

- Expansion of online beauty retail and direct-to-consumer brands

- Increasing adoption of multifunctional and skin-friendly cosmetics

Segmental Insights

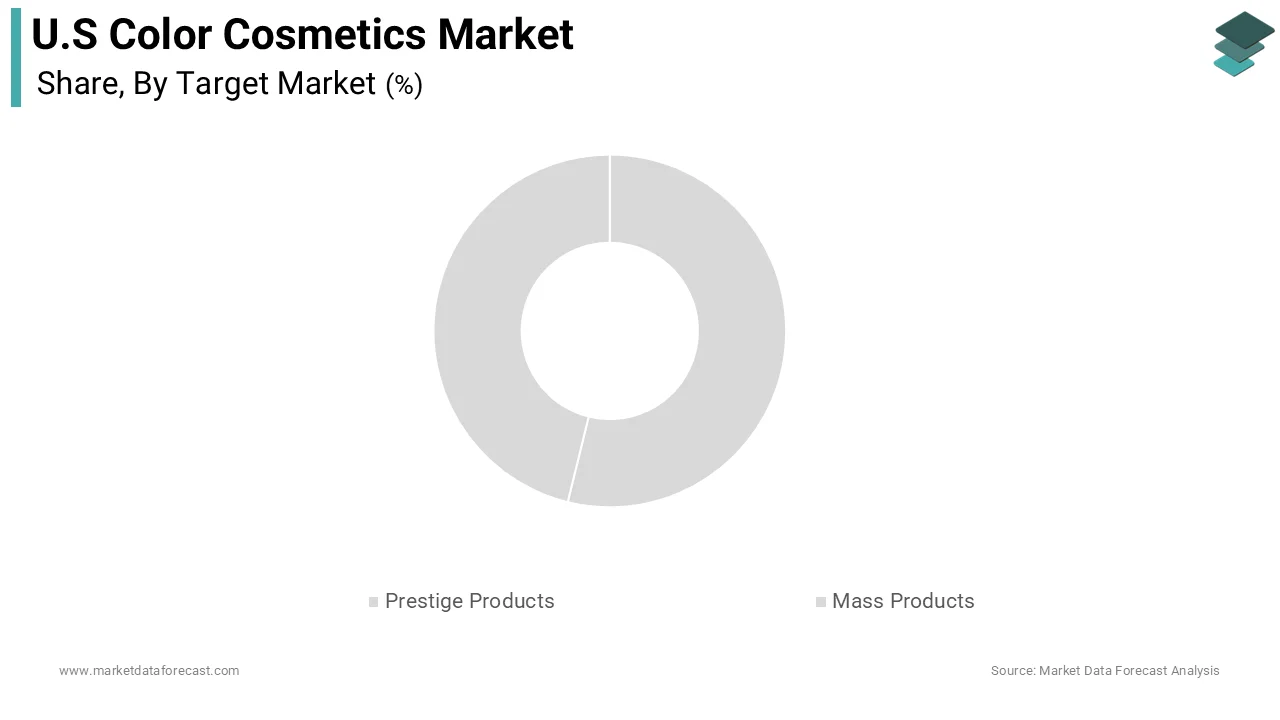

- Based on the target market, the mass products segment dominated the U.S. color cosmetics market in 2025 by accounting for 55.4% of the market share, driven by affordability and broad consumer accessibility.

- Based on distribution channel, the offline segment held the leading share in 2025 by capturing 44.2% of the market share, supported by strong retail presence and in-store product testing experiences.

- Based on application, the face products segment led the market in 2025 by accounting for 44.9% of the market share, driven by high demand for foundations, concealers, powders, and blush products.s

Competitive Landscape

- The U.S. color cosmetics market is highly competitive, with companies focusing on innovative formulations, inclusive product ranges, and digital marketing strategies. Market players are investing in sustainable packaging, AI-powered beauty tools, and celebrity collaborations to strengthen their market presence.

- Prominent players in the U.S. color cosmetics market include L'Oréal, The Estée Lauder Companies, Coty, Revlon, Shiseido, Procter & Gamble, Unilever, e.l.f. Beauty, Mary Kay, and Avon Products.

U.S Color Cosmetics Market Size

The U.S color cosmetics market was valued at USD 23.37 billion in 2025, is estimated to reach USD 25.42 billion in 2026, and is projected to reach USD 49.84 billion by 2034, growing at a CAGR of 8.78% from 2026 to 2034.

The color cosmetics are pigmented products designed to enhance or alter the appearance of the face and eyes, including foundation, lipstick, eyeshadow, and mascara. Consumer engagement with these products has evolved from routine application to an intricate form of artistic identity and social signaling. As per the United States Census Bureau, the population aged 18 to 34, which represents the core demographic for experimental color cosmetics usage, accounts for approximately 72 million individuals, providing a substantial base for trend-driven consumption. Furthermore, data from the Bureau of Labor Statistics indicates that average annual expenditures on personal care products and services per consumer unit reached 651 dollars in recent years, underscoring the consistent financial commitment households make toward grooming and appearance. The proliferation of digital media platforms has further intensified the visibility of cosmetic trends, creating a rapid cycle of product adoption and obsolescence. Industry observers note that the integration of skincare benefits into color cosmetics has become a standard expectation rather than a niche preference.

MARKET DRIVERS

Social Media Influence Drives Unprecedented Product Discovery and Adoption Rates Among Younger Demographics

The digital platforms, such as Instagram, TikTok, and YouTube, have transformed into primary channels for cosmetic education and trend dissemination, which is positively impacting the growth of the United States color cosmetics market. According to research, approximately 71% of teens and young adults use TikTok regularly, where beauty tutorials and product reviews generate billions of views monthly. This constant exposure creates a powerful pull factor for new launches as consumers seek to replicate looks endorsed by influencers and peers. The visual nature of these platforms emphasizes the immediate transformative power of color cosmetics, encouraging frequent purchases to stay current with fleeting trends. Brands leverage this dynamic by collaborating with digital creators who possess high engagement rates, thereby bypassing traditional advertising barriers. The algorithmic curation of content ensures that users are continuously presented with personalized product recommendations, which reduces the friction between discovery and purchase. This shift indicates that consumer attention has decisively moved away from print and television toward interactive digital environments. The immediacy of social commerce features allows users to purchase products directly from posts, shortening the sales funnel significantly.

Demand for Inclusive Shade Ranges Expands Market Reach Across Diverse Ethnic and Skin Tone Populations

The historical limitation of cosmetic offerings to a narrow spectrum of light shades has been replaced by a comprehensive approach that celebrates diversity. The demand for inclusive shade ranges is expanding the growth of the United States color cosmetics market. Consumers now expect brands to provide extensive options that cater to various undertones and depths, reflecting the multicultural fabric of the United States. This demographic reality necessitates product lines that address the specific needs of melanin-rich skin tones, which have been traditionally underserved. Brands that fail to offer adequate shade diversity risk alienating significant portions of the consumer base and facing public backlash on social media. The success of inclusive lines has demonstrated that broad representation drives loyalty and increases overall sales volume. The beauty brands with diverse product portfolios have experienced higher growth rates compared to those with limited offerings. The push for inclusivity extends beyond shade matching to include marketing campaigns that feature models of various ages, sizes, and abilities. This holistic representation resonates with consumers who seek authenticity and validation from the brands they support.

MARKET RESTRAINTS

Regulatory Scrutiny on Ingredient Safety Imposes Formulation Constraints and Compliance Costs

The Food and Drug Administration oversees cosmetic safety, but recent legislative efforts aim to strengthen oversight and transparency, which is limiting the growth of the United States color cosmetics market. The Modernization of Cosmetics Regulation Act introduces mandatory facility registration and adverse event reporting, which increases operational burdens for manufacturers. Companies must invest significantly in testing and documentation to ensure their products meet evolving safety standards. These regulatory changes require extensive research and development resources to identify safe alternatives that maintain product efficacy and sensory appeal. The complexity of navigating varying state laws adds another layer of difficulty for national distributors. As per data from the Environmental Working Group, over 2000 chemicals used in personal care products lack sufficient safety data, prompting calls for stricter federal intervention. Brands must proactively audit their supply chains to eliminate controversial ingredients such as parabens, phthalates, and formaldehyde releasers. Failure to comply can result in product recalls, legal penalties, and reputational damage. The smaller enterprises may struggle to bear the financial weight of compliance, potentially leading to market consolidation. This regulatory environment demands vigilance and adaptability from all market participants, ensuring that consumer safety remains paramount while balancing innovation capabilities.

Consumer Skepticism Toward Greenwashing Undermines Trust in Sustainable Claims

As environmental awareness grows, shoppers increasingly scrutinize brand assertions regarding eco-friendliness and ethical sourcing, which is also declining the growth of the United States color cosmetics market. However, the lack of standardized definitions for terms like natural, clean, and sustainable allows for ambiguous marketing practices that mislead consumers. According to a survey by Deloitte, nearly 60% of consumers express confusion over what constitutes a truly sustainable product, leading to hesitation in purchasing decisions. This awareness is fueled by instances where brands exaggerate their environmental efforts without substantive backing. The Federal Trade Commission has updated its Green Guides to provide clearer instructions on environmental marketing claims, aiming to reduce deceptive practices. As per data from Mintel, a significant portion of beauty shoppers now read ingredient labels carefully and seek third-party certifications such as Leaping Bunny or USDA Organic. Brands that fail to provide transparent and verifiable information risk losing credibility and market share to competitors who prioritize honesty. The rise of digital activism means that inaccurate claims are quickly exposed and amplified on social media, causing lasting damage to brand reputation. To counter this, companies must invest in rigorous supply chain transparency and obtain recognized certifications. Building genuine trust requires consistent communication and tangible actions rather than superficial marketing slogans.

MARKET OPPORTUNITIES

Expansion into gender-neutral product lines captures emerging non-binary consumer segments.

The traditional marketing of color cosmetics has predominantly targeted women, but societal shifts toward gender fluidity have opened new avenues for growth. The expansion into a gender-neutral product line is specifically to gear up new opportunities for the growth of the United States color cosmetics market. Younger generations, particularly Gen Z and Millennials, increasingly reject rigid gender binaries in favor of inclusive identities. Brands that adopt gender neutral packaging and messaging appeal to this expanding cohort by fostering a sense of belonging and acceptance. This strategy involves removing gendered language from product descriptions and using diverse models in advertising campaigns. The success of such initiatives is evident in the rising popularity of unisex beauty brands that focus on self-expression rather than conformity. By positioning color cosmetics as tools for artistic expression rather than gender specific necessities, companies can tap into this underserved market. Product development focuses on versatile formulas that suit various skin types and preferences, regardless of gender. This approach not only broadens the customer base but also aligns with contemporary values of equality and freedom. Brands that embrace this inclusivity early establish themselves as progressive leaders in the industry, gaining loyalty from consumers who prioritize social responsibility in their purchasing decisions.

Integration of Augmented Reality Technology Enhances Online Shopping Experiences and Reduces Return Rates

Virtual try-on tools allow consumers to test products digitally before purchasing, addressing a major barrier in e-commerce. The integration of augmented reality technology enhances online shopping experiences and reduces return rates, in addition to leveraging the growth of the United States color cosmetics market. The retailers offering augmented reality experiences report a 94% higher conversion rate compared to those without such features. This technology uses facial mapping to simulate how lipstick foundation or eyeshadow appears on the user’s skin in real time. The accuracy of these simulations has improved significantly with advancements in artificial intelligence and camera resolution. Consumers appreciate the convenience of experimenting with multiple shades without the hygiene concerns associated with physical testers. The engagement tool also reduces the likelihood of returns, which are costly for retailers and environmentally damaging. Brands integrate these features into their mobile apps and websites, creating interactive experiences that keep users engaged for longer periods. The data collected from virtual try-ons provides valuable insights into consumer preferences, helping companies refine their product offerings. Additionally, social media platforms incorporate similar filters, allowing users to share their virtual looks with friends, further amplifying brand visibility. The seamless blend of entertainment and utility makes augmented reality a powerful driver of sales.

MARKET CHALLENGES

Supply Chain Volatility Disrupts Raw Material Availability and Increases Production Costs

The color cosmetics industry relies on a complex global network of suppliers for ingredients, packaging, and manufacturing, which is one of the major challenging factors for the growth of the United States color cosmetics market. Geopolitical tensions, trade disputes, and natural disasters can interrupt these flows, leading to shortages and price spikes. The manufacturing sector has faced persistent challenges in sourcing key materials, such as mica, iron oxides, and plastic resins. Mica, essential for shimmer effects in eyeshadows and highlighters, is often sourced from regions with unstable political environments, raising ethical and logistical concerns. Fluctuations in oil prices directly impact the cost of petroleum-based ingredients and packaging materials, which constitute a significant portion of production expenses. The producer price index for chemical and allied products has shown considerable volatility, affecting input costs for cosmetic manufacturers. These disruptions force companies to seek alternative suppliers or reformulate products, which can compromise quality and delay launches. Inventory management becomes more challenging as businesses strive to balance stock levels against uncertain supply conditions. The reliance on single-source suppliers exacerbates vulnerabilities, making diversification a critical strategy. However, finding qualified alternatives takes time and resources, straining operational efficiency. Brands must invest in robust risk management frameworks to mitigate these impacts, ensuring continuity of supply.

Intense Market Saturation Leads to Price Wars and Diminished Brand Loyalty

The low barriers to entry in the color cosmetics sector have resulted in an overcrowded marketplace with thousands of brands competing for consumer attention, which acts as a barrier to the growth of the United States color cosmetics market. From legacy giants to indie startups and private label offerings, the sheer volume of choices overwhelms shoppers. The number of beauty brands launched annually in the United States has increased significantly, with many failing within the first two years. This saturation drives aggressive pricing strategies as brands attempt to differentiate themselves through discounts and promotions. Such tactics erode profit margins and devalue brand equity, making it difficult to sustain long-term growth. Consumers become accustomed to deals, reducing their willingness to pay full price and switching brands frequently based on cost rather than loyalty. The retention rate for beauty customers has declined as shoppers explore new options driven by social media trends. Established brands face pressure from agile newcomers who can quickly capitalize on emerging trends using direct-to-consumer models. The noise in the market makes it challenging for any single brand to stand out, requiring substantial marketing investments to maintain visibility. This environment fosters a transactional relationship between brands and consumers where emotional connection is weak. To survive, companies must innovate continuously and build strong community engagement beyond product features. However, the constant need for novelty exhausts creative resources and increases operational stress. Breaking through this clutter requires distinctive branding and authentic storytelling that resonates deeply with target audiences amidst the cacophony of competing messages.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 8.78% |

| Segments Covered | By Target Market, Distribution Channel, Application, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | L'Oréal S.A., Estée Lauder Companies, Coty Inc., Revlon Inc., Shiseido Company Limited, Procter & Gamble, Unilever, e.l.f. Beauty, Mary Kay Inc., Avon Products Inc. |

SEGMENTAL ANALYSIS

By Target Market Insights

The mass products segment was the largest by holding 55.4% of the United States color cosmetics market share in 2025, with its accessibility and affordability for a broad consumer base. The economic pressure on household budgets, which prioritizes value without compromising on basic quality, is also expected to enhance the growth of the segment. The consumer price index for personal care products has seen moderate increases, prompting consumers to seek cost-effective alternatives to prestige brands. Mass market brands have significantly improved their formulation quality and packaging aesthetics, narrowing the perceived gap with luxury counterparts. The widespread distribution network ensures that these products are available in nearly every community, removing geographical barriers to purchase. Furthermore, the rise of private label offerings from major retail chains has intensified competition within the mass segment, providing consumers with even more affordable options. These store brands often mimic popular trends and shades from high-end labels at a fraction of the cost. This accessibility, combined with consistent innovation in product performance, sustains the mass segment's position as the market leader.

The prestige products segment is projected to register the fastest CAGR of 5.8% throughout the forecast period, with the increasing disposable income of millennials and Gen Z consumers, who view beauty purchases as investments in self-care and social status. The aspirational value associated with luxury brands which offer superior packaging, exclusive ingredients, and enhanced sensory experiences. The luxury beauty sector has outpaced the overall beauty market growth with prestige skincare and makeup seeing double-digit increases in certain quarters. Consumers are willing to pay a premium for products that align with their personal values, such as cruelty-free certifications and sustainable sourcing practices. The influence of social media influencers, who showcase high-end routines, further amplifies demand among younger demographics who seek to emulate these lifestyles. Limited edition collaborations with celebrities and designers create urgency and exclusivity, driving rapid sell-outs and brand loyalty. Additionally, the integration of advanced skincare benefits into prestige color cosmetics appeals to consumers seeking multifunctional products.

By Distribution Channel Insights

The offline segment accounted in holding 44.2% of the United States color cosmetics market share in 2025 due to the tactile nature of beauty products and the immediate gratification of physical retail. Consumers prefer to test shades, textures, and formulations in person to ensure compatibility with their skin tone and type before purchasing. According to the National Retail Federation, brick and mortar stores still account for approximately 70% of total retail sales in the beauty category, highlighting the enduring relevance of physical shopping experiences. The ability to receive instant feedback from beauty advisors and participate in in-store events fosters a sense of community and trust that digital channels struggle to replicate. The impulse purchases remain a significant driver of offline sales, with visually appealing displays and promotional offers influencing buying decisions at the point of sale. Major retailers have invested heavily in upgrading store aesthetics and integrating technology such as smart mirrors to enhance the shopping experience. The presence of established brands in prominent retail locations reinforces brand visibility and credibility among consumers. Furthermore, the return process for offline purchases is often perceived as more straightforward and immediate, reducing the hesitation associated with online buying.

The online segment is likely to have the fastest CAGR of 9.2% during the forecast period, with the rapid expansion driven by the convenience of home delivery, extensive product selection, and the integration of advanced digital tools that mitigate the limitations of virtual shopping. The widespread adoption of mobile commerce and social media platforms that seamlessly connect discovery with purchase. The e-commerce sales in the beauty sector have grown consistently with online channels by capturing an increasing share of total beauty revenue. The availability of detailed customer reviews, tutorials, and influencer recommendations provides shoppers with the confidence to buy products without physical testing. The beauty brands that offer personalized online experiences, such as virtual try-ons and shade matching quizzes, report significantly higher conversion rates. The rise of direct-to-consumer models allows brands to bypass traditional retail intermediaries, offering competitive pricing and exclusive products that attract digital native consumers. Subscription services and auto-replenishment options further enhance customer retention by ensuring consistent access to favorite items. Additionally, the global reach of online platforms enables niche and indie brands to access diverse audiences across the country without the need for extensive physical infrastructure.

By Application Insights

The face products segment was the largest by capturing 44.9% of the United States color cosmetics market share in 2025, owing to their fundamental role in creating a polished and uniform complexion. These products are considered essential staples in most beauty routines, serving as the canvas for other cosmetic applications. The innovation in formulas that offer long-wearing coverage, hydration, and sun protection has expanded the appeal of face products to a broader demographic, including men and older consumers. The demand for multi-functional face products that combine makeup with skincare benefits has surged, aligning with the holistic beauty trend. Consumers are increasingly educated about ingredients, seeking non-comedogenic and hypoallergenic options that support skin health while enhancing appearance. The availability of extensive shade ranges in face products has also driven adoption among diverse ethnic groups who previously faced limited options. Major brands invest heavily in research and development to improve texture and finish, ensuring that face products meet the high-performance expectations of modern users.

The lip products segment is emerging at a fastest CAGR of 6.5% in the coming years with the versatility of lip cosmetics, which serve as both subtle enhancements and bold statement pieces, allowing for easy experimentation with trends. The influence of social media trends that enhance lip artistry and the popularity of celebrity-owned brands that focus heavily on lip formulations. The lipsticks and lip glosses are among the most frequently purchased color cosmetics items due to their relatively low price point and immediate visual impact. The development of innovative textures, such as matte liquids, plumping glosses, and hydrating balms, has revitalized consumer interest and encouraged multiple purchases. The sales of premium lip products have increased as consumers treat themselves to affordable luxuries during periods of economic uncertainty. The trend of mask wearing during recent health crises also shifted focus to eye and lip makeup, with lips becoming a key area for expression. Furthermore, the integration of nourishing ingredients like hyaluronic acid and vitamins appeals to health-conscious consumers who seek functionality alongside aesthetics. The ease of application and portability of lip products make them ideal for on-the-go touch-ups, enhancing their utility in daily routines.

COMPETITION OVERVIEW

The competitive landscape of the United States color cosmetics market is characterized by intense rivalry among established multinational corporations and agile indie brands. Legacy players leverage their extensive distribution networks and substantial marketing budgets to maintain visibility and consumer loyalty. However, they face increasing pressure from niche entrants that capitalize on digital native strategies and rapid trend adaptation. The barrier to entry has lowered due to accessible contract manufacturing and social media marketing, allowing new brands to launch quickly. This saturation leads to frequent product launches and short life cycles, requiring constant innovation. Price competition is fierce in the mass segment, while prestige brands compete on exclusivity and brand heritage. Retailers play a pivotal role by curating assortments that balance popular staples with emerging trends. Private label offerings from major retail chains further intensify competition by providing affordable alternatives. Consumer loyalty is fragmented as shoppers frequently switch brands based on reviews and influencer endorsements. Companies must therefore invest in building emotional connections through authentic storytelling and community engagement. Regulatory compliance and sustainability claims also serve as competitive differentiators.

KEY MARKET PLAYERS

A few major players of the U.S color cosmetics market include

- L'Oréal S.A

- Estée Lauder Companies

- Coty Inc

- Revlon Inc

- Shiseido Company Limited

- Procter & Gamble

- Unilever

- e.l.f. Beauty

- Mary Kay Inc

- Avon Products Inc

Top Strategies Used by Key Market Participants

Key players in the United States color cosmetics market employ several strategic initiatives to maintain a competitive advantage and drive growth. Product innovation remains paramount as companies continuously develop new formulations that integrate skincare benefits with cosmetic performance. Brands invest heavily in research to create clean vegan and cruelty-free options that align with ethical consumer values. Digital transformation is another critical strategy involving the use of augmented reality for virtual try-ons and artificial intelligence for personalized recommendations. These technologies enhance online shopping experiences and reduce return rates. Strategic collaborations with influencers and celebrities help brands reach wider audiences and build cultural relevance. Companies also focus on expanding inclusive shade ranges to cater to diverse demographic groups. Sustainability efforts such as eco-friendly packaging and transparent supply chains are increasingly used to differentiate brands. Mergers and acquisitions allow larger corporations to absorb niche brands and access new market segments. Direct-to-consumer channels are optimized to build stronger customer relationships and gather valuable data.

Leading Players in the United States Color Cosmetics Market

- L'Oréal USA maintains a formidable presence through its diverse portfolio spanning luxury consumer, active, and professional divisions. The company leverages advanced research and development to introduce innovative formulations that address evolving consumer needs for sustainability and efficacy. Recent initiatives include expanding its inclusive shade ranges across major brands like Maybelline and Lancôme to cater to diverse skin tones. L'Oréal has also intensified its digital transformation by integrating artificial intelligence tools for virtual try-ons and personalized skincare diagnostics. These efforts enhance consumer engagement and drive online sales growth. The company actively partners with influencers and content creators to amplify brand visibility on social media platforms.

- Estée Lauder Companies Inc exerts significant influence through its prestigious brand portfolio, including MAC, Clinique, and Too Faced. The firm focuses on high-end prestige segments where it commands strong loyalty among affluent consumers. Recent strategies involve enhancing direct-to-consumer capabilities through improved e-commerce platforms and omnichannel experiences. The company has invested heavily in digital marketing campaigns that highlight diversity and inclusivity across its brand communications. Estée Lauder also emphasizes innovation in product technology, such as long-wearing formulas and skincare-infused makeup. Collaborations with global celebrities and artists help maintain cultural relevance and attract younger demographics. The organization continues to optimize its supply chain to ensure product availability and reduce environmental impact.

- Coty Inc holds a robust position in the mass and prestige sectors with iconic brands like CoverGirl, Rimmel, and Gucci Beauty. The company has undergone significant restructuring to streamline operations and focus on core growth categories such as fragrance and color cosmetics. Recent actions include revitalizing legacy brands through modernized packaging and updated product formulations that appeal to contemporary tastes. Coty has strengthened its digital footprint by leveraging data analytics to better understand consumer preferences and tailor marketing efforts. The firm actively pursues partnerships with high-fashion houses to expand its luxury portfolio and enhance brand prestige. Sustainability initiatives such as reducing plastic usage and sourcing ethical ingredients are central to its corporate strategy. Coty also engages with Gen Z consumers through authentic social media interactions and influencer collaborations.

MARKET SEGMENTATION

This research report on the US color cosmetics market has been segmented and sub-segmented based on target market, distribution channel, application & region.

By Target Market

- Prestige Products

- Mass Products

By Distribution Channel

- Offline

- Online

By Application

- Nail Products

- Hair Products

- Lip Products

- Face Products

- Others

By Region

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

1. What is driving the growth of the U.S. color cosmetics market?

The market is growing due to rising beauty awareness, increasing social media influence, and demand for premium and organic cosmetic products.

2. Which products are included in the color cosmetics market?

The market includes lipsticks, foundations, eyeliners, mascaras, blushes, nail polishes, concealers, and eyeshadows.

3. Who are the major players in the U.S. color cosmetics market?

Leading companies include L'Oréal S.A., Estée Lauder Companies, and Coty Inc..

4. Why is demand for organic cosmetics increasing in the U.S.?

Consumers are becoming more conscious about skin health and prefer products made with natural and chemical-free ingredients.

5. Which distribution channels dominate the color cosmetics market?

Supermarkets, specialty beauty stores, online retail platforms, pharmacies, and department stores are major channels.

6. What role does social media play in the market?

Social media platforms and beauty influencers strongly impact consumer buying behavior and product trends.

7. What challenges does the U.S. color cosmetics market face?

Challenges include intense competition, counterfeit products, changing fashion trends, and strict cosmetic regulations.

8. Which cosmetic category has high demand in the U.S.?

Face makeup and lip products hold significant demand due to daily usage and fashion trends.

9. What packaging trends are emerging in the cosmetics industry?

Sustainable, refillable, and eco-friendly packaging solutions are becoming increasingly popular.

10. What is the future outlook for the U.S. color cosmetics market?

The market is expected to witness strong growth due to product innovation, rising beauty trends, and increasing online beauty purchases.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com