U.S Commercial Insurance Market Size, Share, Trends & Growth Forecast Report - Segmented By Type, Enterprise, Industry, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Commercial Insurance Market Report Summary

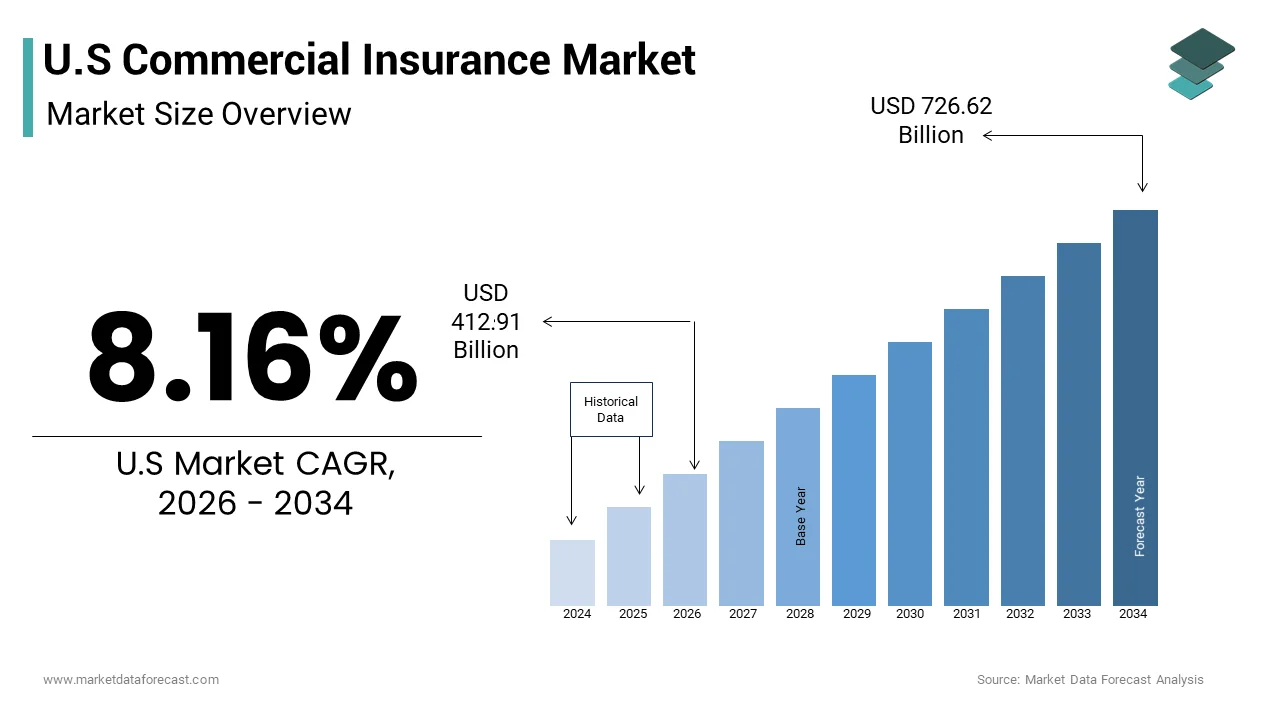

The U.S. commercial insurance market was valued at USD 381.74 billion in 2025, is estimated to reach USD 412.91 billion in 2026, and is projected to reach USD 726.62 billion by 2034, growing at a CAGR of 8.16% during the forecast period from 2026 to 2034. The growth of the U.S. commercial insurance market is driven by rising business risks, increasing regulatory compliance requirements, and growing awareness regarding financial protection against operational disruptions, cyber threats, and liability claims. Expanding industrial activities, rising adoption of digital insurance platforms, and increasing demand for customized commercial coverage solutions are further supporting market expansion across the United States.

Key Market Trends

- Rising demand for liability insurance due to increasing litigation risks, workplace safety concerns, and stricter regulatory frameworks across industries.

- Growing adoption of cyber insurance policies as businesses face escalating cybersecurity threats, ransomware attacks, and data breach incidents.

- Increasing integration of artificial intelligence, predictive analytics, and digital underwriting technologies to improve risk assessment and claims management efficiency.

- Expansion of tailored insurance solutions for small and medium-sized enterprises (SMEs) and industry-specific commercial risks.

- Rising focus on climate risk assessment and catastrophe coverage amid growing concerns regarding natural disasters and extreme weather events.

Segmental Insights

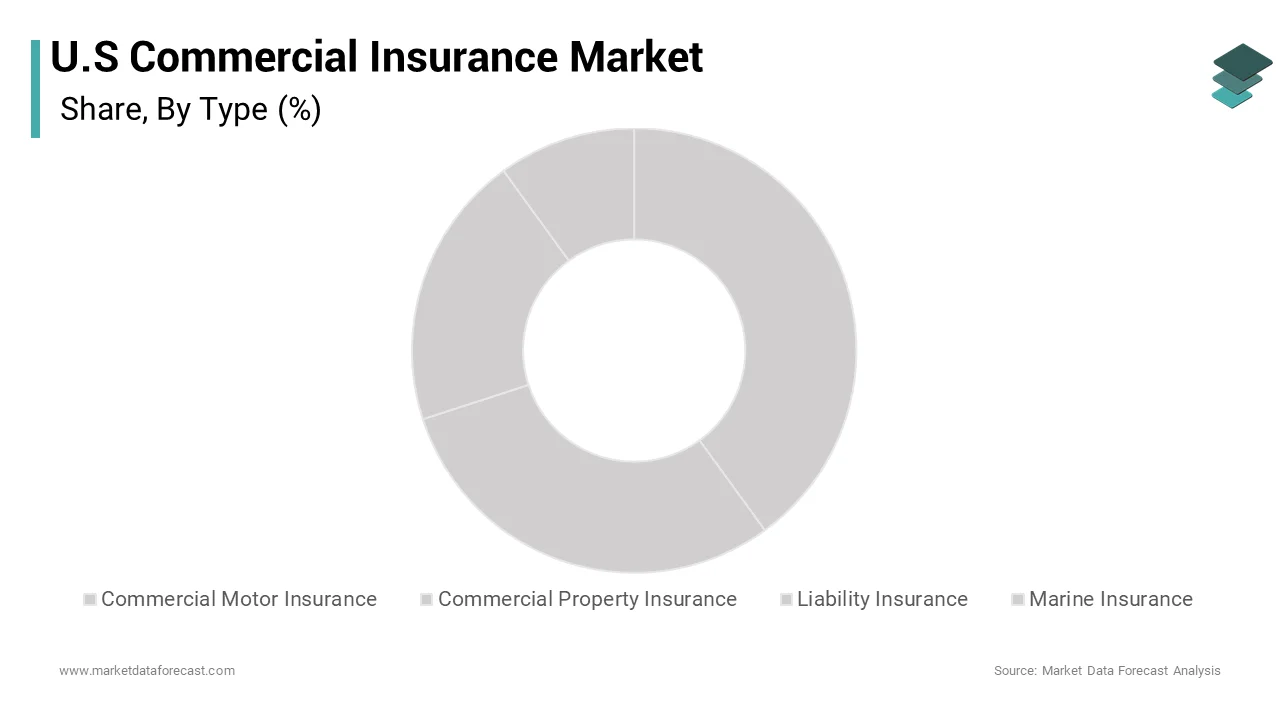

- Based on type, the liability insurance segment accounted for 56.3% of the U.S. commercial insurance market share in 2025. The segment’s dominance is attributed to the increasing need for businesses to protect themselves against legal liabilities, employee-related claims, property damage, and third-party risks.

- Based on enterprise size, the large enterprises segment held 56.2% of the United States commercial insurance market share in 2025. The growth of this segment is driven by higher insurance spending capacity, complex operational structures, and increasing demand for comprehensive risk management solutions among large corporations.

- Based on industry, the manufacturing industry segment dominated the U.S. commercial insurance market by holding 60.1% of the market share in 2025. The segment’s leadership is supported by the sector’s high exposure to operational risks, equipment damage, workplace accidents, supply chain disruptions, and liability-related claims.

Regional Insights

The United States continues to represent one of the largest and most advanced commercial insurance markets globally, supported by strong regulatory frameworks, rising enterprise risk awareness, and increasing insurance penetration across industries. Major business hubs such as New York, California, Texas, and Illinois are witnessing strong demand for commercial insurance products due to expanding corporate activities, industrial operations, and digital business transformation initiatives. The growing frequency of cyber incidents, climate-related risks, and evolving liability regulations are further driving demand for comprehensive commercial insurance coverage throughout the country.

Competitive Landscape

The U.S. commercial insurance market is highly competitive, with leading insurance providers focusing on digital transformation, product innovation, strategic partnerships, and advanced risk analytics to strengthen their market position. Companies are increasingly investing in AI-driven underwriting systems, cloud-based insurance platforms, and customized policy offerings to improve customer experience and operational efficiency. Expansion into emerging risk categories such as cyber insurance, climate risk coverage, and business interruption insurance is further intensifying competition within the market.

Prominent players in the U.S. commercial insurance market include Zurich Insurance Group, Marsh LLC, Chubb, Direct Line Insurance Group, Willis Towers Watson, Allianz, American International Group, Marsh & McLennan Agency, The Hartford, Aviva, AXA, Hanover Insurance Group, Markel Corporation, CNA Financial, and Berkshire Hathaway.

U.S Commercial Insurance Market Size

The U.S commercial insurance market size was valued at USD 381.74 billion in 2025 and is anticipated to reach USD 412.91 billion in 2026 to reach USD 726.62 billion by 2034, growing at a CAGR of 8.16% during the forecast period from 2026 to 2034.

Current Market Overview and Definition

The commercial insurance is risk transfer mechanisms designed to protect businesses from financial losses arising from various operational liabilities. These instruments are essential for maintaining business continuity and ensuring compliance with legal and contractual obligations. As per the National Association of Insurance Commissioners, the total direct written premiums for commercial lines in the United States exceeded 200 billion dollars in recent annual assessments, reflecting the critical role of risk management in corporate strategy. Businesses across industries rely on these products to mitigate risks associated with natural disasters litigation and employee injuries. The landscape is evolving due to emerging threats, such as cyberattacks and supply chain disruptions, which necessitate innovative policy structures. Insurers are increasingly leveraging data analytics to assess risk more accurately and tailor premiums to specific organizational profiles. The integration of technology in underwriting processes has streamlined policy issuance and claims handling enhancing customer experience. Economic fluctuations influence demand as businesses adjust their risk appetite based on financial performance.

MARKET DRIVERS

Escalating Frequency of Cyber Threats Drives Policy Adoption

The increasing prevalence of cyberattacks and data breaches is accelerating the growth of the United States commercial insurance market. Organizations face sophisticated threats from ransomware phishing and distributed denial of service attacks that can disrupt operations and compromise sensitive customer information. As per the Federal Bureau of Investigation, the Internet Crime Complaint Center received over 800000 complaints regarding cybercrime in a single recent year with reported losses exceeding 6 billion dollars. This surge in criminal activity has heightened awareness among business leaders about the potential financial devastation of a security incident. Consequently, companies are prioritizing cyber insurance as a critical component of their risk management strategies to cover costs related to data recovery legal fees and regulatory fines. The complexity of modern IT infrastructures and the rise of remote work have expanded the attack surface making traditional security measures insufficient alone. Insurers respond by offering comprehensive policies that include incident response services and forensic investigations. Regulatory frameworks such as state level data breach notification laws further compel businesses to secure coverage to manage compliance risks. The growing interdependence of digital systems means that a failure in one area can cascade across entire networks amplifying the need for robust protection.

Stringent Regulatory Compliance Mandates Increase Coverage Needs

The strict regulatory requirements and legal mandates is another attribute fuelling the growth of the United States commercial insurance market. Businesses must adhere to federal and state laws that require specific types of coverage to operate legally and protect stakeholders. For instance, workers compensation insurance is mandatory in almost every state for employers with employees ensuring that injured workers receive medical care and wage replacement. As per the survey, millions of workplace injuries and illnesses occur annually necessitating robust insurance frameworks to handle claims and liabilities. Additionally, industries, such as healthcare and finance face stringent regulations regarding professional liability and errors and omissions coverage to protect against claims of negligence or malpractice. The Department of Health and Human Services enforces rules that require healthcare providers to maintain adequate liability protection to safeguard patient interests. Environmental regulations also compel companies in manufacturing and construction to secure pollution liability coverage to address potential cleanup costs and third party damages. These legal obligations create a baseline demand for insurance that is resistant to economic downturns. Non compliance can result in severe penalties license revocation and reputational damage making insurance a non-negotiable operational expense. The evolving nature of regulations keeps pace with new risks ensuring that insurance requirements remain relevant and expansive. This regulatory pressure consistently fuels market growth as businesses strive to maintain legal standing and operational integrity.

MARKET RESTRAINTS

Volatility in Catastrophe Losses Constrains Underwriting Capacity

The increasing frequency and severity of natural disasters by straining underwriting capacity and driving up premiums is hindering the growth of the United States commercial insurance market. Climate change has led to more intense hurricanes, wildfires floods, and storms, by causing substantial property damage and business interruption losses. As per the National Oceanic and Atmospheric Administration, the United States experienced 18 separate weather and climate disasters in a recent year where losses exceeded 1 billion dollars each totaling over 100 billion dollars in damages. These catastrophic events deplete insurer reserves and force carriers to reevaluate their risk exposure in high hazard zones. Consequently, insurers may reduce coverage limits increase deductibles or withdraw from certain markets entirely limiting availability for businesses in vulnerable regions. This volatility makes it difficult for insurers to predict long term loss trends resulting in conservative underwriting practices. Small and medium sized enterprises are particularly affected as they may struggle to afford rising premiums or find alternative coverage options. The uncertainty surrounding climate related risks complicates pricing models and capital allocation strategies for insurance companies.

High Operational Costs and Administrative Burdens Limit Efficiency

The elevated operational costs and complex administrative processes by impacting profitability and service delivery is also hampering the growth of the United States commercial insurance market. Insurers face significant expenses related to claims processing underwriting compliance and technology infrastructure maintenance. As per the Property Casualty Insurers Association of America, the expense ratio for many commercial lines remains high due to the labor intensive nature of risk assessment and policy customization. The complexity of commercial policies which often require tailored terms and conditions demands specialized expertise and extensive manual review. This inefficiency increases the time and cost required to issue policies and settle claims leading to slower response times and customer dissatisfaction. Additionally, regulatory compliance requires continuous monitoring and reporting adding to the administrative burden. Insurers must invest heavily in legacy system upgrades and cybersecurity measures to protect sensitive data further escalating operational expenditures. These costs are often passed on to customers in the form of higher premiums reducing the affordability of coverage for some businesses. The lack of standardization across different states and lines of business exacerbates these challenges making it difficult to achieve economies of scale. High barriers to entry for new technologies also hinder modernization efforts.

MARKET OPPORTUNITIES

Integration of Internet of Things for Proactive Risk Management

The integration of Internet of Things (IoT) devices by enabling proactive risk management and personalized pricing is greatly influencing the growth of the United States commercial insurance market. IoT sensors can monitor real time data on equipment performance environmental conditions and employee behavior by allowing insurers to identify and mitigate risks before they result in losses. As per the International Data Corporation, spending on IoT solutions is projected to reach hundreds of billions of dollars globally with a substantial portion allocated to industrial and commercial applications. Insurers leverage this data to offer usage-based insurance models where premiums are adjusted according to actual risk exposure rather than historical averages. For example, telematics in commercial fleets allow insurers to track driving patterns and provide discounts for safe behavior reducing accident frequencies. Similarly smart building systems can detect fire hazards or water leaks early preventing extensive property damage. This shift from reactive indemnification to preventive partnership enhances value for policyholders and improves loss ratios for insurers. The availability of granular data enables more accurate underwriting and faster claims processing through automated verification. Businesses benefit from reduced downtime and lower insurance costs while insurers gain deeper insights into risk dynamics. This technological synergy fosters stronger client relationships and opens new revenue streams through value added services. The adoption of IoT thus transforms the traditional insurance model into a dynamic and interactive risk management ecosystem.

Expansion into Gig Economy and Freelance Workforce Coverage

The rapid growth of the gig economy and freelance workforce to develop specialized products for non-traditional employees is additionally to expand the growth of the United States commercial insurance market. Traditional commercial policies often exclude these workers leaving them vulnerable to liability and income loss risks. Insurers can capitalize on this gap by creating flexible on demand coverage options that align with the irregular nature of gig work. Products, such as portable benefits and short term liability insurance can be integrated directly into digital platforms used by freelancers to find work. This approach simplifies access to protection and ensures continuous coverage regardless of job changes. The rise of remote work also increases demand for home office insurance and cyber liability protection for individual contractors. By tailoring solutions to this demographic-insurers can tap into a large and growing market segment that is currently underserved. Partnerships with gig platforms can facilitate seamless enrollment and payment enhancing user experience. This expansion not only diversifies revenue sources but also promotes financial stability for the freelance workforce.

MARKET CHALLENGES

Data Privacy Concerns and Regulatory Scrutiny

The data privacy concerns and increasing regulatory scrutiny, as insurers handle vast amounts of sensitive customer information is one of the major challenges for the growth of the United States commercial insurance market. The collection and analysis of personal and proprietary data for underwriting and claims purposes expose insurers to significant cybersecurity and compliance risks. The enforcement actions related to data privacy violations have increased with substantial fines imposed on companies that fail to protect consumer information. Insurers must navigate a complex web of state and federal regulations, such as the California Consumer Privacy Act, which impose strict requirements on data handling and consent. Breaches can lead to reputational damage loss of customer trust and costly litigation. The use of advanced analytics and artificial intelligence raises additional ethical questions regarding bias and transparency in decision making. Regulators are closely examining algorithmic underwriting to ensure fairness and prevent discrimination. Compliance with these evolving standards requires significant investment in legal expertise and technology infrastructure. Failure to adhere to privacy norms can result in operational disruptions and financial penalties. Furthermore, customers are becoming more aware of their data rights and may hesitate to share information necessary for accurate risk assessment. This tension between data utility and privacy protection complicates product development and customer engagement strategies.

Talent Shortage and Skills Gap in Specialized Underwriting

The persistent talent shortage and skills gap in specialized underwriting and actuarial sciences is also to decline the growth of the United States commercial insurance market. The industry requires highly skilled professionals, who can assess complex risks interpret data and design innovative policy structures. The aging workforce and difficulty in attracting younger talent to the sector have created a shortage of qualified experts. Many experienced underwriters are reaching retirement age taking with them invaluable institutional knowledge and judgment capabilities. Meanwhile, newer generations often perceive the insurance industry, as traditional and lacking in technological appeal leading to recruitment difficulties. This gap hinders the ability of insurers to adapt to emerging risks such as cyber threats and climate change, which require nuanced understanding and creative solutions. The lack of expertise can result in inadequate pricing poor risk selection and slower response to market changes. Training new employees takes time and resources further straining operational efficiency. The competition for talent with technology and finance sectors exacerbates the problem as insurers struggle to offer comparable compensation and career growth opportunities.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 8.16% |

| Segments Covered | By Type, Enterprise, Industry, and By Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

| Regions Covered | California, Washington, Oregon, New York & Rest of the United States |

| Market Leaders Profiled | Zurich (Switzerland), Marsh LLC. (U.S.), Chubb (U.S.), Direct Line Insurance Group plc (U.K.), Willis Towers Watson (U.K.), Allianz (Germany), American International Group, Inc. (U.S.), Marsh & McLennan Agency (U.S.), The Hartford (U.S.), Aviva (U.K.), AXA (France), Hanover Insurance Group (U.S.), Markel Corporation (U.S.), CNA Financial (U.S.), Berkshire Hathaway (U.S.) |

SEGMENTAL ANALYSIS

By Type Insights

The liability insurance segment was accounted in holding 56.3% of the United States commercial insurance market share in 2025 with the litigious nature of the business environment and stringent legal requirements. The complexity of modern business operations increases exposure to lawsuits making comprehensive liability coverage essential for risk management. Courts frequently award substantial damages in civil cases prompting companies to secure higher limits of protection. Regulatory mandates also require specific liability policies for industries such as healthcare and finance ensuring a consistent baseline demand. The rise of cyber liability further expands this segment as data breaches lead to costly litigation and regulatory fines. Businesses recognize that liability risks can threaten solvency more severely than property damage leading to prioritized investment in these policies. The continuous evolution of case law introduces new liabilities requiring adaptive insurance solutions. This segment dominates because it addresses the most unpredictable and potentially devastating financial threats facing corporations.

The commercial property insurance segment is swiftly emerging at a fastest CAGR of 4.5% during the forecast period with the rapid growth although liability remains larger in total premium volume certain subsegments, within property are expanding quickly due to asset value inflation. However, if considering pure growth rate relative to base some analysts point to Cyber Insurance, which is often categorized under specialty lines or others but increasingly distinct. The average cost to rebuild commercial structures has risen significantly due to labor and material shortages leading to higher insured values and premiums. The increase is not solely due to new policies but also due to the need to update existing coverage limits to match current reconstruction costs. Businesses are realizing that underinsurance poses a severe risk in the event of total loss. The expansion of commercial real estate in emerging markets and the renovation of existing infrastructure also contribute to this growth.

By Enterprise Insights

The large enterprises segment was the largest by accounting for 56.2% of the United States commercial insurance market share in 2025 due to their extensive operational footprints and complex risk profiles. These organizations possess significant assets diverse workforces and global supply chains that necessitate comprehensive and high limit insurance programs. Their size exposes them to a wider array of risks, including international liability environmental damage and cyber threats requiring specialized and layered coverage solutions. Large corporations often engage in captive insurance arrangements and self-insurance strategies, which still involve significant interaction with the commercial insurance market for excess layers and stop loss coverage. Regulatory scrutiny is higher for large entities mandating strict compliance with safety and financial reporting standards that drive insurance purchases. The complexity of their operations requires bespoke policy wording and risk engineering services, which command higher premiums. Additionally, large enterprises have the financial resources to invest in robust risk management departments that prioritize insurance as a key strategic tool.

The small and medium sized enterprises segment is likely to grow at a fastest CAGR of 11.2% from 2026 to 2034 with the digitalization and increased awareness of risk. As per the Small Business Administration there are over 30 million small businesses in the United States accounting for 99.9% of all US businesses. This vast number creates a huge potential market for insurers who are increasingly leveraging technology to reach this underserved segment. Digital platforms and insurtech companies have simplified the process of obtaining quotes and purchasing policies making insurance more accessible to small business owners. The growth of the gig economy and freelance work has also expanded the definition of SMEs requiring flexible and affordable coverage options. Recent economic trends have highlighted the vulnerability of small businesses to disruptions such as pandemics and natural disasters prompting greater uptake of business interruption and liability coverage. Insurers are developing tailored products for specific niches such as e commerce retailers and tech startups addressing their unique needs. The lower barrier to entry for digital insurance solutions allows SMEs to compare prices and customize coverage easily.

By Industry Insights

The manufacturing industry segment was the largest by holding 60.1% of the United States commercial insurance market share in 2025 due to its high capital intensity and operational risks. Heavy machinery hazardous materials and complex supply chains that create significant exposure to property damage and liability claims. The manufacturing sector contributes trillions of dollars to the US economy and employs millions of workers generating substantial insurance premiums. The need to protect expensive equipment and inventory from fire theft and mechanical breakdown drives high demand for property insurance. Workers compensation is another major component due to the physical nature of manufacturing jobs and the associated risk of injury. Product liability insurance is essential for manufacturers to protect against claims arising from defective goods that cause harm to consumers. The global nature of manufacturing supply chains also necessitates marine and cargo insurance to cover goods in transit. Regulatory requirements for environmental safety and workplace health further mandate specific coverage types. The scale of manufacturing operations means that even minor incidents can result in significant financial losses making insurance a critical risk management tool.

The healthcare industry segment is expected to register a fastest CAGR of 9.1% from 2026 to 2034 with the regulatory changes and increasing liability risks. This growth translates into increased demand for medical malpractice insurance cyber liability and property coverage for healthcare facilities. The rising frequency of cyberattacks on healthcare providers targeting patient data has spurred significant growth in cyber insurance premiums. Regulatory pressures, such as the Health Insurance Portability and Accountability Act impose strict data security requirements making cyber coverage essential. The aging population increases the volume of patients and procedures raising the potential for malpractice claims. The expansion of telehealth services introduces new liability exposures that insurers are rapidly addressing with specialized products. Healthcare facilities are also investing in advanced medical equipment which requires specialized property insurance. The consolidation of healthcare providers into larger systems creates complex risk profiles that demand comprehensive insurance programs.

COMPETITIVE LANDSCAPE

The competition in the United States commercial insurance market is characterized by intense rivalry among established carriers and emerging insurtech firms. Major insurers leverage their extensive distribution networks and brand recognition to maintain dominance while smaller players innovate with niche products and digital first approaches. Price competition is fierce particularly in standard lines such as property and casualty where margins are thin. Differentiation increasingly relies on service quality speed of claims settlement and value added risk management services. The rise of data analytics enables companies to offer more precise pricing attracting cost conscious businesses. Regulatory compliance remains a significant barrier to entry ensuring that only well capitalized firms can compete effectively. Consolidation through mergers and acquisitions is common as companies seek economies of scale and broader market reach. Cyber insurance has become a key battleground with many carriers vying for leadership in this high growth segment.

KEY MARKET PLAYERS

A few of the market players that are dominating the U.S commercial insurance market are

- Zurich (Switzerland)

- Marsh LLC. (U.S.)

- Chubb (U.S.)

- Direct Line Insurance Group plc (U.K.)

- Willis Towers Watson (U.K.)

- Allianz (Germany)

- American International Group, Inc. (U.S.)

- Marsh & McLennan Agency (U.S.)

- The Hartford (U.S.)

- Aviva (U.K.)

- AXA (France)

- Hanover Insurance Group (U.S.)

- Markel Corporation (U.S.)

- CNA Financial (U.S.)

- Berkshire Hathaway (U.S.)

Top Players In The Market

- Allianz SE maintains a formidable presence in the European commercial insurance sector through its extensive network and diverse product portfolio. The company provides comprehensive risk solutions including property casualty and liability coverage for businesses across various industries. Recent actions include significant investments in digital platforms to enhance customer experience and streamline claims processing. Allianz actively pursues strategic partnerships with insurtech firms to integrate advanced analytics and artificial intelligence into underwriting processes. The company emphasizes sustainability by offering green insurance products that support environmentally responsible business practices. Its strong capital position enables it to underwrite large and complex risks effectively. Allianz continues to expand its specialized services for small and medium enterprises ensuring broad market reach. These initiatives reinforce its reputation as a reliable and innovative insurer in the European landscape.

- AXA SA contributes significantly to the European commercial insurance market by leveraging its global expertise and local market knowledge. The company offers tailored insurance solutions for corporations focusing on cyber risk climate change and professional liability. Recent strategies involve the acquisition of niche insurers to strengthen its position in specialized segments such as health and protection. AXA invests heavily in research and development to create predictive models that improve risk assessment accuracy. The company also prioritizes customer centric innovation by launching digital tools that facilitate real time policy management. Its commitment to corporate social responsibility enhances brand loyalty among socially conscious clients. AXA collaborates with governments and industry bodies to shape regulatory frameworks promoting stable market conditions.

- Zurich Insurance Group plays a pivotal role in the European commercial insurance market by delivering robust risk management services. The company focuses on helping businesses navigate complex challenges such as supply chain disruptions and cyber threats. Recent actions include the expansion of its captive insurance solutions allowing large corporations to retain more control over their risk financing. Zurich enhances its digital capabilities by implementing cloud based systems that improve operational efficiency and data security. The company actively engages in sustainability initiatives offering incentives for clients who adopt eco friendly practices. Its strong reinsurance partnerships provide additional capacity for handling catastrophic events. Zurich also invests in employee training to ensure high levels of technical expertise and customer service. These strategic moves strengthen its competitive edge and deepen client relationships across the European region.

Top Strategies Used By Key Market Participants In The Market

Key players in the United States commercial insurance market primarily utilize digital transformation and strategic acquisitions to enhance their competitive positioning. Companies invest heavily in artificial intelligence and machine learning to improve underwriting accuracy and automate claims processing reducing operational costs. This technological integration allows for faster policy issuance and personalized pricing models that appeal to modern businesses. Mergers and acquisitions are frequently employed to expand product portfolios and enter new geographic markets efficiently. Insurers also focus on developing specialized coverage for emerging risks such as cyber liability and climate related damages. Partnerships with insurtech startups facilitate innovation and access to novel data sources for better risk assessment. Customer experience enhancement through seamless digital interfaces serves as a critical differentiator in a crowded marketplace. Additionally, companies prioritize sustainability by offering green insurance products that align with corporate environmental goals.

MARKET SEGMENTATION

This research report on the U.S commercial insurance market is segmented and sub-segmented into the following categories.

By Type

- Commercial Motor Insurance

- Commercial Property Insurance

- Liability Insurance

- Marine Insurance

By Enterprise Type

- Large Enterprises

- SMEs

- Small-sized Enterprises

By Industry

- Manufacturing

- Construction

- IT & Telecom

- Healthcare

- Energy & Utilities

- Transportation & Logistics

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

What is the U.S. commercial insurance market?

The U.S. commercial insurance market includes insurance policies designed to protect businesses from financial and operational risks.

Why is the U.S. commercial insurance market growing rapidly?

The market is growing due to increasing business risks, regulatory requirements, and rising demand for financial protection solutions.

Which types of commercial insurance are most popular in the U.S.?

Popular types include general liability insurance, property insurance, workers’ compensation, and cyber insurance.

Which commercial insurance segment leads the U.S. market?

General liability insurance leads the market due to its broad coverage for business-related risks and claims.

Who typically buys commercial insurance in the U.S.?

Small businesses, large enterprises, contractors, healthcare providers, and retailers are major buyers of commercial insurance.

How is digital technology transforming the U.S. commercial insurance market?

AI-driven underwriting, digital claims processing, and data analytics are improving efficiency and customer experience.

Why is cyber insurance demand increasing in the U.S.?

Businesses are adopting cyber insurance to protect against rising cyberattacks and data breach risks.

What are the biggest challenges in the U.S. commercial insurance market?

Rising claim costs, regulatory complexities, and increasing fraud risks can impact market growth.

How are small businesses influencing the commercial insurance market?

Growing startup activity and expanding small business operations are increasing demand for customized insurance coverage.

What is the future outlook for the U.S. commercial insurance market?

The market is expected to grow steadily with increasing risk awareness and expanding digital insurance solutions.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com