- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

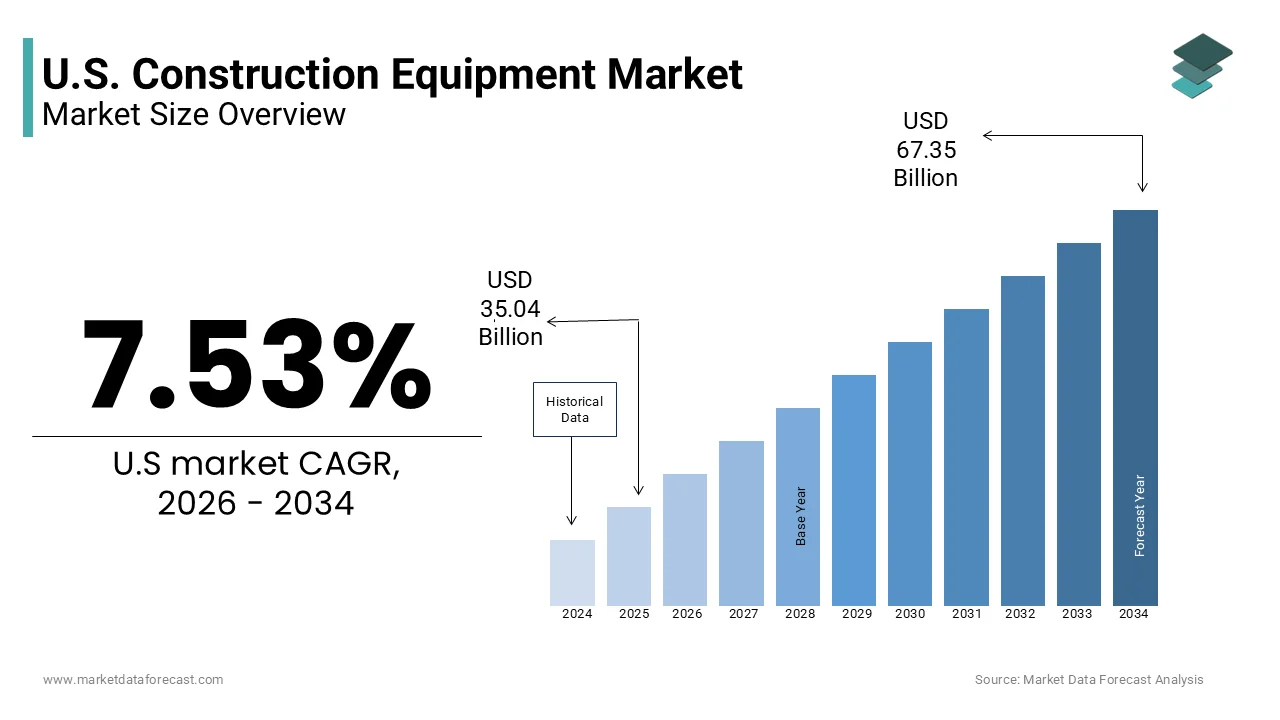

Market Size, 2025

$35.04 BnMarket Estimate, 2026

$37.68 BnMarket Forecast, 2034

$67.35 BnCAGR, 2026–2034

7.53%U.S. Construction Equipment Market Report Summary

The U.S. construction equipment market was valued at USD 35.04 billion in 2025, is estimated to reach USD 37.68 billion in 2026, and is projected to reach USD 67.35 billion by 2034, growing at a CAGR of 7.53% during the forecast period. Market growth is driven by increasing investments in infrastructure development, rising residential and commercial construction activities, and government initiatives focused on modernization and sustainability. Construction equipment plays a critical role in improving productivity, efficiency, and project timelines. The expansion of smart construction technologies and green infrastructure projects is further supporting strong market growth in the United States.

Key Market Trends

- Rising infrastructure development and government investments are driving market growth.

- Increasing residential and commercial construction activities are boosting demand.

- Growing adoption of advanced and smart construction equipment is supporting market expansion.

- Expansion of green and sustainable construction projects is enhancing demand.

- Technological advancements in automation and telematics are improving operational efficiency.

Segmental Insights

- Based on equipment type, the earthmoving equipment segment held the largest share of the U.S. construction equipment market in 2025. This dominance is attributed to its extensive use in excavation, grading, and large scale construction activities.

- Based on application, the residential segment led the U.S. construction equipment market in 2025, driven by increasing housing demand and urban development projects.

Regional Insights

- The United States is expected to remain the leading market in North America through the forecast period, supported by strong investment in domestic manufacturing, infrastructure upgrades, and green construction initiatives.

Competitive Landscape

The U.S. construction equipment market is highly competitive, with key players focusing on product innovation, automation technologies, and expansion of production capabilities to strengthen their market position. Companies are investing in electric and hybrid machinery, digital solutions, and strategic partnerships. Prominent players in the U.S. construction equipment market include Caterpillar Inc, Deere and Company, Komatsu Ltd, Liebherr Group, Terex Corporation, The Manitowoc Company Inc, Volvo Construction Equipment, Hitachi Construction Machinery Co Ltd, JCB, CNH Industrial N V, XCMG Group, and Sany Heavy Industry Co Ltd.

U.S. Construction Equipment Market Size

The U.S. construction equipment market was valued at USD 35.04 billion in 2025, is estimated to reach USD 37.68 billion in 2026, and is projected to reach USD 67.35 billion by 2034, growing at a CAGR of 7.53% from 2026 to 2034.

The U.S. is likely to see steady growth in its infrastructure and real estate sectors over the next few years as legislative funding and private development continue to converge. The U.S. construction equipment market encompasses the manufacturing, distribution, and rental of heavy machinery utilized in infrastructure, residential, commercial, and industrial development projects. This sector includes a diverse array of vehicles such as excavators, bulldozers, loaders, cranes, and compactors, which are essential for earthmoving, material handling, and site preparation. The market is deeply integrated with the broader construction economy, serving as a barometer for national economic health and investment activity. According to the U.S. Census Bureau, total construction spending was estimated at a seasonally adjusted annual rate of $2,190.4 billion in January 2026, which is reflecting sustained demand for mechanized solutions across various project types. The market is characterized by a shift towards technologically advanced machinery that offers enhanced fuel efficiency, safety features, and connectivity. As per the Bureau of Labor Statistics, employment in the construction sector grew by 26,000 in March 2026 and is driving the need for efficient equipment to support labor productivity. Regulatory frameworks established by the Environmental Protection Agency influence engine standards and emissions controls, prompting manufacturers to innovate in powertrain technologies. The definition of the market extends beyond sales to include the rapidly growing equipment rental segment, which offers flexibility for contractors managing fluctuating project pipelines. The interplay between federal infrastructure funding, private real estate development, and technological adoption defines the current operational landscape. Stakeholders are increasingly focusing on sustainability and digitalization to meet evolving client expectations and regulatory requirements.

MARKET DRIVERS

Federal Infrastructure Investment and Legislative Funding

Federal infrastructure investment and legislative funding are primarily propelling the expansion of the U.S. construction equipment market by injecting substantial capital into public works projects. The Bipartisan Infrastructure Law provides $973 billion over five years through FY 2026, including $550 billion in new investments for transportation, water, power, and broadband expansion. According to the White House Council of Economic Advisers, this legislation targets the renovation of roads, bridges, and ports, which requires extensive use of excavators, graders, and paving equipment. The allocation of funds specifically for clean water infrastructure and electric vehicle charging networks further diversifies the types of equipment needed for specialized tasks. As per the American Society of Civil Engineers, the long awaited investment in deteriorating assets ensures sustained activity in the civil engineering sector. State and local governments are leveraging these federal grants to initiate stalled projects, thereby accelerating equipment procurement cycles. The emphasis on domestic manufacturing within these funding provisions also supports local equipment producers and suppliers. Public transit improvements and airport modernization projects contribute to the demand for cranes and lifting devices. The certainty of long term funding allows contractors to plan capital expenditures with confidence. This government led stimulus creates a stable baseline demand that mitigates the volatility of private sector construction cycles. The scale of these investments ensures that the construction equipment market remains buoyant despite broader economic uncertainties.

Growth in Residential and Commercial Real Estate Development

Growth in residential and commercial real estate development significantly drives the U.S. construction equipment market as urbanization and population shifts create demand for new structures. The housing shortage in many metropolitan areas has prompted increased construction of multi-family units and single family homes, which require compact and versatile equipment. According to the U.S. Census Bureau, privately owned housing starts in March 2026 were at a seasonally adjusted annual rate of 1,502,000 units, necessitating the use of skid steer loaders, mini excavators, and telehandlers. The commercial sector is also expanding with the development of logistics warehouses, data centers, and healthcare facilities driven by e commerce growth and demographic changes. As per the National Association of Home Builders, the demand for modern energy efficient buildings encourages the adoption of advanced machinery that supports precise and sustainable construction practices. Urban infill projects often require smaller equipment capable of operating in confined spaces, which boosts sales in the compact equipment segment. The renovation and retrofitting of existing commercial properties also contribute to equipment utilization as contractors upgrade facilities to meet new standards. Private investment in real estate continues to outpace other sectors, providing a steady stream of projects for equipment operators. The diversity of real estate applications ensures that various types of machinery remain in high demand. This private sector dynamism complements public infrastructure spending to sustain overall market growth.

MARKET RESTRAINTS

High Interest Rates and Financing Costs

High interest rates and financing costs pose a significant restraint on the U.S. construction equipment market expansion by increasing the cost of capital for contractors and developers. The Federal Reserve has maintained elevated interest rates to combat inflation, which directly impacts the affordability of loans for purchasing heavy machinery. According to the Federal Reserve Board, the prime lending rate has reached levels that discourage small and medium sized contractors from expanding their fleets through debt financing. Higher borrowing costs reduce the return on investment for new equipment purchases, leading many firms to delay upgrades or extend the life of existing assets. As per the Associated General Contractors of America, a majority of 53% of contractors list materials and input costs as a top concern for 2026, as firms grapple with financial pressures. The cost of leasing equipment has also increased as lessors pass on higher capital costs to renters. This financial pressure is particularly acute for independent operators who rely on credit to manage cash flow fluctuations. The uncertainty regarding future rate movements complicates long term financial planning for construction firms. Delayed equipment replacement can lead to higher maintenance costs and reduced operational efficiency over time. The tightening of credit conditions thus acts as a brake on market growth by limiting the ability of buyers to acquire new technology. Until interest rates stabilize or decline, the market will face headwinds from constrained financial accessibility.

Supply Chain Disruptions and Component Shortages

Supply chain disruptions and component shortages present a major restraint on the U.S. construction equipment market by delaying production and increasing lead times. The industry relies on global supplies of semiconductors, hydraulic components, and steel, which have faced significant bottlenecks in recent years. According to the Institute for Supply Management, the Manufacturing PMI registered 52.7% in March 2026, yet the Prices Index jumped to 78.3%, indicating significant cost pressures and supply hurdles. Shortages of microchips used in modern telematics and engine control units have forced producers to slow assembly lines or deliver incomplete machines. As per the Federal Reserve Bank of New York, global supply chain pressure indices reflect ongoing logistical hurdles that impact import dependent industries. The reliance on single source suppliers for specialized components increases vulnerability to geopolitical tensions and trade disputes. Logistics challenges such as port congestion and transportation delays further complicate the distribution of finished equipment to dealers and customers. Manufacturers struggle to forecast demand accurately amidst uncertain supply conditions, leading to inventory imbalances. The increased cost of expedited shipping and alternative sourcing strategies erodes profitability. These disruptions hinder the ability of companies to fulfill contracts and capture new sales opportunities. Until supply chains stabilize, the industry will face ongoing operational inefficiencies and customer dissatisfaction due to delayed deliveries.

MARKET OPPORTUNITIES

Adoption of Telematics and Digital Construction Solutions

The adoption of telematics and digital construction solutions is a significant opportunity for the U.S. construction equipment market to enhance operational efficiency and data driven decision making. Telematics systems enable real time monitoring of equipment location, fuel consumption, and maintenance needs, allowing fleet managers to optimize utilization and reduce downtime. According to the Associated Equipment Distributors, the integration of Internet of Things technology in heavy machinery is becoming a standard expectation for contractors seeking to improve productivity. Digital platforms provide actionable insights that help prevent costly breakdowns and extend the lifespan of assets through predictive maintenance. As per the National Institute of Standards and Technology, the construction industry is increasingly investing in digital twins and building information modeling, which require connected equipment to function effectively. The data generated by smart machines can be used to automate reporting and compliance processes, reducing administrative burdens. Manufacturers are developing proprietary software ecosystems that lock customers into their brands by offering superior analytics and support services. The rise of autonomous and semi-autonomous equipment further expands the potential for digital integration in hazardous or repetitive tasks. Contractors who leverage these technologies can achieve competitive advantages through lower operational costs and improved project timelines. The transition towards smart construction sites creates new revenue streams for equipment providers through software subscriptions and data services.

Expansion of Electric and Hybrid Equipment Lines

The expansion of electric and hybrid equipment lines offers a promising opportunity for the U.S. construction equipment market to align with sustainability goals and regulatory mandates. Battery electric and hybrid machinery produce zero or reduced emissions, making them ideal for indoor projects and urban environments with strict air quality regulations. According to the Environmental Protection Agency, new emissions standards for non-road diesel engines are encouraging the development of cleaner alternatives that reduce environmental impact. Major manufacturers are introducing electric excavators, loaders, and compactors that offer lower noise levels and reduced operating costs compared to traditional diesel models. As per the California Air Resources Board, state level mandates for zero emission off road equipment are driving early adoption and creating a niche market for green machinery. Government incentives and grants for purchasing clean technology further enhance the economic viability of electric equipment for contractors. The total cost of ownership for electric machines is becoming competitive due to lower fuel and maintenance expenses over the lifecycle. Urban construction projects, particularly in dense cities, benefit from the quiet operation of electric equipment, which minimizes community disturbance. Manufacturers that lead in electrification can differentiate their brands and capture premium market segments. The transition to electric powertrains positions the U.S. market for long term resilience and compliance with evolving environmental standards.

MARKET CHALLENGES

Skilled Labor Shortage and Operator Training

Skilled labor shortage and operator training is a major challenge to the U.S. construction equipment market by limiting the effective utilization of advanced machinery. The construction industry faces a significant gap in qualified equipment operators who can safely and efficiently handle complex modern vehicles. According to the Associated General Contractors of America, approximately 62% of participants in 2026 are concerned about an economic slowdown while struggling with persistent labor availability and cost. The increasing complexity of telematics and automated systems requires operators to possess technical skills beyond traditional mechanical knowledge. As per the Bureau of Labor Statistics, employment in construction grew by 26,000 in March 2026, but the supply of highly skilled technical operators remains insufficient. The lack of trained operators leads to underutilization of expensive equipment and increased risk of accidents and damage. Training programs are often insufficient to keep pace with technological advancements, leaving many workers unprepared for new machinery. The cost of recruiting and training new employees adds to operational expenses for contractors. The shortage also limits the ability of firms to take on additional projects despite having available equipment. Manufacturers are attempting to simplify user interfaces to reduce the learning curve, but human capital constraints persist. Until the industry addresses the workforce crisis through better education and retention strategies, the full potential of modern equipment will remain unrealized.

Regulatory Compliance and Emission Standards

Regulatory compliance and evolving emission standards pose a significant challenge to the U.S. construction equipment market by increasing development costs and operational complexity. The Environmental Protection Agency has implemented stringent Tier 4 Final emission standards that require advanced after treatment systems such as diesel particulate filters and selective catalytic reduction. According to the Engine Manufacturers Association, complying with these regulations adds thousands of dollars to the cost of each machine, affecting affordability for small contractors. The complexity of meeting varying state and federal regulations creates administrative burdens for manufacturers and fleet operators. As per the California Air Resources Board, stricter state level mandates often exceed federal requirements, forcing manufacturers to produce different configurations for different markets. The transition to cleaner technologies requires significant research and development investments, which may not yield immediate returns. Non-compliant older equipment faces restrictions on usage in certain zones, reducing its utility and resale value. The risk of non-compliance penalties discourages innovation in some areas and increases legal risks. Manufacturers must balance regulatory requirements with performance and durability, which is a complex engineering challenge. The dynamic nature of environmental policy requires constant adaptation and strategic planning. This regulatory landscape creates barriers to entry and increases the cost of doing business for all participants in the construction equipment sector.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.53% |

| Segments Covered | By Equipment Type, Application, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Caterpillar Inc., Deere & Company, Komatsu Ltd., Liebherr Group, Terex Corporation, The Manitowoc Company, Inc., Volvo Construction Equipment, Hitachi Construction Machinery Co., Ltd., JCB, CNH Industrial N.V., XCMG Group, and Sany Heavy Industry Co., Ltd |

SEGMENTAL ANALYSIS

By Equipment Type Insights

The earthmoving equipment segment dominated the market by holding the highest share of the U.S. market in 2025. The growth of the earthmoving segment in the U.S. market is attributed to its fundamental role in site preparation, excavation, and infrastructure development. The dominance of this segment is further fueled by the extensive requirement for excavators, bulldozers, and loaders in both residential and commercial construction projects. According to the U.S. Census Bureau, earthmoving activities constitute the initial phase of nearly all construction projects, ensuring consistent demand regardless of the specific building type. The Bipartisan Infrastructure Law has allocated substantial funds for road and bridge repairs, which heavily rely on earthmoving machinery for grading and trenching. As per the Associated General Contractors of America, the producer price index for materials used in nonresidential construction rose 3.6% over 12 months, highlighting the value of maintaining efficient earthmoving fleets. The versatility of modern earthmoving equipment allows it to be used across diverse applications, from mining to urban development. Manufacturers have integrated advanced hydraulic systems and GPS technology into these machines, enhancing precision and efficiency. The replacement cycle for heavy earthmoving equipment is relatively short due to intense usage conditions, further driving sales volume. The segment benefits from a robust rental market where contractors prefer accessing late model excavators without long term capital commitment. This combination of universal application and technological advancement ensures that earthmoving equipment remains the cornerstone of the construction machinery industry.

On the other hand, the material handling equipment and cranes segment is predicted to expand at a CAGR of 7.4% during the forecast period in the U.S. construction equipment market owing to the surge in vertical construction and the increasing complexity of modern building designs. According to the National Association of Home Builders, the rise in multi-story residential and commercial structures necessitates the use of tower cranes and mobile lifting solutions to transport materials to higher elevations. The expansion of industrial warehouses and logistics centers, driven by e commerce, also boosts demand for forklifts and automated guided vehicles. As per the Bureau of Labor Statistics, the transportation and warehousing sector added 21,000 jobs in March 2026, reflecting the expansion of facilities that require advanced material handling. The integration of smart sensors in cranes allows for real time load monitoring and safety compliance, which appeals to risk averse contractors. The trend towards prefabricated construction modules requires precise lifting capabilities, further driving crane adoption. Urban infill projects with limited space favor compact and versatile material handling equipment. The rental sector for cranes is expanding as specialized lifting needs vary by project scope. These factors collectively propel the material handling segment at a faster pace as construction methods evolve towards greater height and efficiency.

By Application Insights

The residential segment led the market with the highest share of the U.S. market in 2025. The growth of the residential segment in this market is attributed to the persistent housing shortage and strong demographic demand for new homes. According to the U.S. Census Bureau, housing starts were at a seasonally adjusted annual rate of 1,502,000 in March 2026, creating a steady pipeline for equipment usage. The shift towards suburban living post pandemic has increased land development activities, which require extensive earthmoving and site preparation machinery. As per the National Association of Home Builders, the average size of new homes has stabilized, but the volume of construction remains high, sustaining demand for compact and mid sized equipment. Residential projects often utilize skid steer loaders, mini excavators, and compact track loaders due to their maneuverability in confined spaces. The renovation and remodeling sector also contributes significantly as homeowners invest in property improvements. The fragmentation of the residential construction industry means that many small contractors rely on equipment rentals, boosting the utilization rates of newer machines. Government incentives for first time home buyers further stimulate construction activity. This segment benefits from the essential nature of housing, which ensures demand even during economic fluctuations. The widespread geographic distribution of residential projects ensures broad market penetration for equipment manufacturers.

However, the industrial construction segment is experiencing the fastest growth and is expected to exhibit a CAGR of 8.4% during the forecast period due to the expansion of manufacturing facilities and logistics infrastructure, the re-shoring of manufacturing operations and the booming e commerce sector, which requires massive distribution centers. According to the Federal Reserve Bank of New York, investment in industrial construction has surged as companies build semiconductor plants, battery factories, and automotive assembly lines. These large scale projects require heavy duty equipment such as large excavators, cranes, and concrete pumps for foundation work and structural erection. As per the Commercial Real Estate Development Association, the demand for last mile delivery hubs has led to a construction boom in urban and peri urban areas. Industrial facilities often feature complex mechanical and electrical systems, requiring specialized lifting and installation equipment. The push for renewable energy infrastructure, including solar farms and wind turbine installations, also falls under the industrial umbrella, driving demand for specialized civil engineering equipment. The speed of industrial project completion is critical, leading to higher equipment intensity and shorter rental cycles. Government subsidies for domestic manufacturing under the CHIPS Act further accelerate this trend. These factors collectively ensure that the industrial application segment expands rapidly, outpacing traditional commercial and residential sectors.

COUNTRY LEVEL ANALYSIS

The U.S. is likely to lead North American construction equipment revenue through the end of the decade as investment in domestic manufacturing and green infrastructure intensifies. According to the Association of Equipment Manufacturers, the U.S. is a key production hub for global construction machinery brands, hosting major manufacturing facilities for excavators, loaders, and cranes. The domestic market benefits from a strong rental culture that accounts for a significant portion of equipment utilization, allowing contractors to access latest technologies without heavy capital expenditure. As per the U.S. Department of Commerce, total construction spending reached a rate of $2,190.4 billion in early 2026, reflecting confidence in the sector. The regulatory environment emphasizes safety and emissions compliance, driving the adoption of Tier 4 Final engines and electric prototypes. The presence of a skilled workforce and advanced supply chain networks supports efficient equipment deployment. Consumer preference for reliable and high performance machinery influences product development strategies. The integration of telematics and autonomous features positions the U.S. as a leader in smart construction solutions. The market is supported by a dense network of dealers and service centers, ensuring minimal downtime. The resilience of the construction sector against economic volatility ensures steady demand. The U.S. remains a central driver of global trends in construction technology and sustainability.

COMPETITIVE LANDSCAPE

The competition in the U.S. construction equipment market is characterized by intense rivalry among global giants and specialized manufacturers who compete on technology reliability and service quality. The market structure is moderately consolidated with key players holding significant influence over pricing and innovation trends. Competitive intensity is driven by the race to develop autonomous and electric machinery that offers superior efficiency and lower emissions. Innovation in telematics and digital platforms plays a vital role as firms seek to differentiate their offerings through data driven insights. Regulatory compliance regarding safety and environmental standards serves as a barrier to entry for smaller competitors without substantial capital. Established players leverage their extensive dealer networks and financing options to maintain customer trust and loyalty. Price competition is evident in the standard equipment segment while premium sectors focus on total cost of ownership. The focus on after sales support and parts availability is becoming a key differentiator. Overall the competitive landscape requires continuous adaptation to technological advancements and shifting customer preferences for sustainable and connected solutions.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. construction equipment market include

- Caterpillar Inc.

- Deere & Company

- Komatsu Ltd.

- Liebherr Group

- Terex Corporation

- The Manitowoc Company, Inc.

- Volvo Construction Equipment

- Hitachi Construction Machinery Co., Ltd.

- JCB

- CNH Industrial N.V.

- XCMG Group

- Sany Heavy Industry Co., Ltd.

Top Players in the Market

- Caterpillar Inc is a dominant force in the U.S. construction equipment market offering a comprehensive portfolio of machinery and engines. The company leverages its extensive dealer network to provide superior customer support and service across the nation. Caterpillar strengthens its position by investing heavily in autonomous technologies and telematics solutions that enhance operational efficiency for clients. The company recently expanded its electric vehicle lineup including battery electric excavators to meet sustainability demands. Caterpillar focuses on digital integration through its Cat Connect platform which provides real time data analytics. Its commitment to durability and innovation ensures high customer retention. These strategic initiatives reinforce its reputation as a leader in heavy machinery and infrastructure solutions.

- Deere and Company is a major player in the US construction sector known for its robust line of earthmoving and material handling equipment. The company integrates advanced agricultural technology into its construction machinery to improve precision and productivity. Deere strengthens its market position through strategic acquisitions and partnerships that expand its digital capabilities and service offerings. The company recently launched new smart construction tools that utilize artificial intelligence for site management. Deere focuses on sustainable engineering by developing hybrid and electric models for compact equipment. Its strong brand loyalty among contractors supports consistent sales volume. These efforts enable Deere to compete effectively in the evolving landscape of connected and efficient construction solutions.

- Volvo Construction Equipment is a leading manufacturer in the U.S. market specializing in articulated haulers excavators and wheel loaders. The company prioritizes safety and environmental sustainability in its product design and manufacturing processes. Volvo strengthens its position by pioneering electric construction equipment such as the electric articulated hauler and compact excavator. The company recently invested in charging infrastructure partnerships to support the adoption of zero emission machines. Volvo focuses on connectivity through its CareTrack telematics system which optimizes fleet management for customers. Its emphasis on operator comfort and fuel efficiency appeals to cost conscious contractors. These actions demonstrate Volvo's commitment to leading the transition towards cleaner and smarter construction technologies.

Top Strategies Used by Key Market Participants

Key players in the U.S. construction equipment market primarily employ strategies such as electrification digital integration and service expansion to strengthen their market position. Companies frequently invest in developing battery electric and hybrid machinery to comply with environmental regulations and meet sustainability goals. This approach allows them to capture early adopters and government incentives for green technology. Strategic partnerships with software firms help implement advanced telematics and autonomous features that enhance operational efficiency. By focusing on predictive maintenance services firms reduce downtime for customers and create recurring revenue streams. Additionally manufacturers expand their rental fleets to offer flexible solutions for contractors facing project uncertainty. Product customization is another key strategy as companies tailor equipment to specific industry needs. These combined strategies enable market participants to maintain competitiveness and drive growth in a technologically advancing industry landscape.

MARKET SEGMENTATION

This research report on the U.S. construction equipment market is segmented and sub-segmented into the following categories.

By Equipment Type

- Earthmoving Equipment

- Material Handling Equipment and Cranes

- Concrete Equipment

- Road Building Equipment

- Civil Engineering Equipment

- Crushing and Screening Equipment

- Others

By Application

- Residential

- Commercial

- Industrial

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States